DEVEX 2021 Day 1 Monday 7 June 2021 A Novel Sampling and ...

The Future of the North Sea:

Tackling the Challenges Facing our

Industry

Presentation to DEVEX

6th May 2014

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Dan Cole

McKinsey & Company | 1

A view of the oil industry from the late 1990s

“$10 might actually be too optimistic. We may be heading for $5.”

“Thanks to new technology and productivity gains, you might expect the price of oil, like that of most other commodities, to fall slowly over the years. Judging by the oil market in the pre-OPEC era, a ‘normal’ market price might now be in the $5-10 range.”

- The Economist, March 4th 1999

McKinsey & Company | 2

1997 forecast of UK decommissioning

21 kboe/dExpected 2006

production

Expected decommission dates for U.K. end of field life assets

McKinsey & Company | 3

Just three fields actually decommissioned

McKinsey & Company | 4

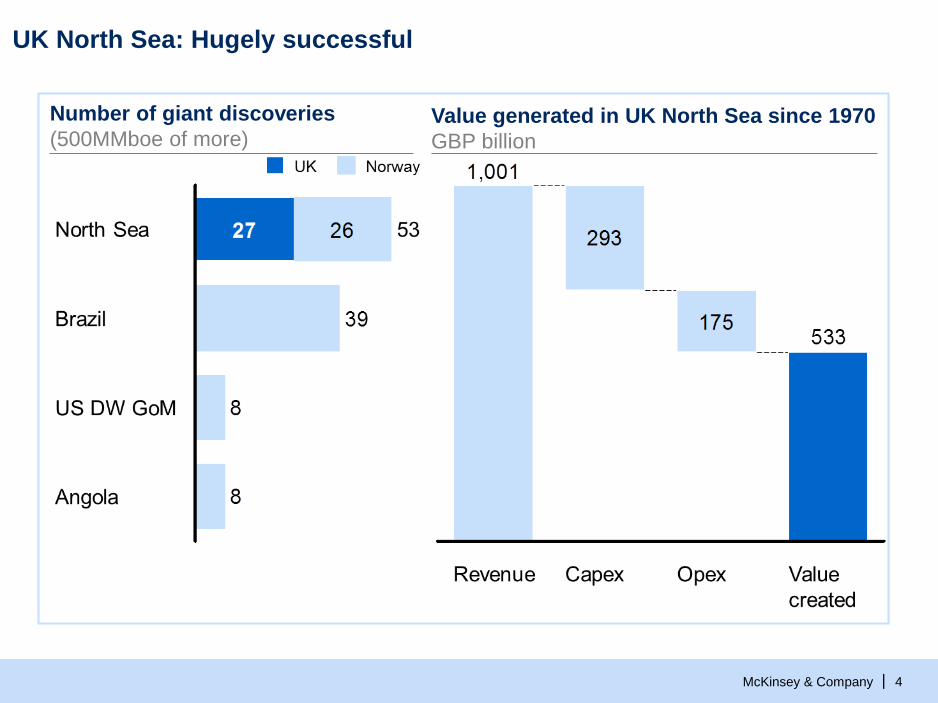

UK North Sea: Hugely successful

Number of giant discoveries

(500MMboe of more)Value generated in UK North Sea since 1970

GBP billion

McKinsey & Company | 5

What we are going to need to get right

Ability to manage costs

Delivering safety & asset integrity

Adding resources

Keeping production efficiency high

McKinsey & Company | 6

What we are going to need to get right

Ability to manage costs

Delivering safety & asset integrity

Adding resources

Keeping production efficiency high

McKinsey & Company | 7

Offshore efficiency decreased in the North Sea over the last decade

Asset Efficiency

SOURCE: McKinsey Global Offshore Asset Efficiency Database

Country averages, % of estimated production potential based on monthly production

McKinsey & Company | 8

Asset Efficiency

Norway appears to follow the UK trend – with a 10-year lag

SOURCE: McKinsey Global Offshore Asset Efficiency Database

Country averages, % of estimated production potential based on monthly production

McKinsey & Company | 9SOURCE: McKinsey Global Offshore Asset Efficiency Database

The range of AE performance in the North Sea has widened sharply over

the past decade

Note: North Sea includes UK and Norway only, and excludes dry gas fields

% of estimated production potential based on monthly production

McKinsey & Company | 10

Possible causes for the fall in efficiency

▪ Increasing average age

▪ Higher dependency on

more vulnerable export

routes

▪ Different types of asset

(e.g., more subsea)

▪ Less redundancy in

production systems

▪ More challenging

production (e.g., higher

water cut, more HPHT)

▪ More challenging locations

Changes in the structural

characteristics of the assets,

infrastructure, reservoir

▪ Poorer maintenance and

reliability practices

▪ Low previous investment

▪ Lower risk appetite/ and

increased focus on asset

integrity

▪ Changes in contracting

strategy (e.g., outsourcing)

▪ Lower focus in operators’

portfolios

▪ Changes in organizational

set-up

Changes in operator

approaches

▪ Higher commodity prices

“allowing” lower efficiency

▪ Regulatory changes

▪ Supply chain constraints

▪ Increasing impact of “train-

wreck” events

▪ Increasing exposure to

harsh weather (e.g., more

production in NNS, WoS)

Changes in operating

environment, and other

external factors

McKinsey & Company | 11

Possible causes for the fall in efficiency

▪ Increasing average age

▪ Higher dependency on

more vulnerable export

routes

▪ Different types of asset

(e.g., more subsea)

▪ Less redundancy in

production systems

▪ More challenging

production (e.g., higher

water cut, more HPHT)

▪ More challenging locations

▪ Poorer maintenance and

reliability practices

▪ Low previous investment

▪ Lower risk appetite/ and

increased focus on asset

integrity

▪ Changes in contracting

strategy (e.g., outsourcing)

▪ Lower focus in operators’

portfolios

▪ Changes in organizational

set-up

▪ Higher commodity prices

“allowing” lower efficiency

▪ Regulatory changes

▪ Supply chain constraints

▪ Increasing impact of “train-

wreck” events

▪ Increasing exposure to

harsh weather (e.g., more

production in NNS, WoS)

1

2

3 4

Changes in the structural

characteristics of the assets,

infrastructure, reservoir

Changes in operator

approaches

Changes in operating

environment, and other

external factors

McKinsey & Company | 12SOURCE: McKinsey Global Offshore Asset Efficiency Database

Age alone does not explain lower asset production efficiency

Asset production efficiency of UK installations by age

% of estimated production potential based on monthly production

1

McKinsey & Company | 13

Indirect hubs have significantly lower efficiency than direct hubs

SOURCE: McKinsey Global Offshore Asset Efficiency Database

2

Asset efficiency of UK installation by network position

% of estimated production potential based on monthly production

McKinsey & Company | 14

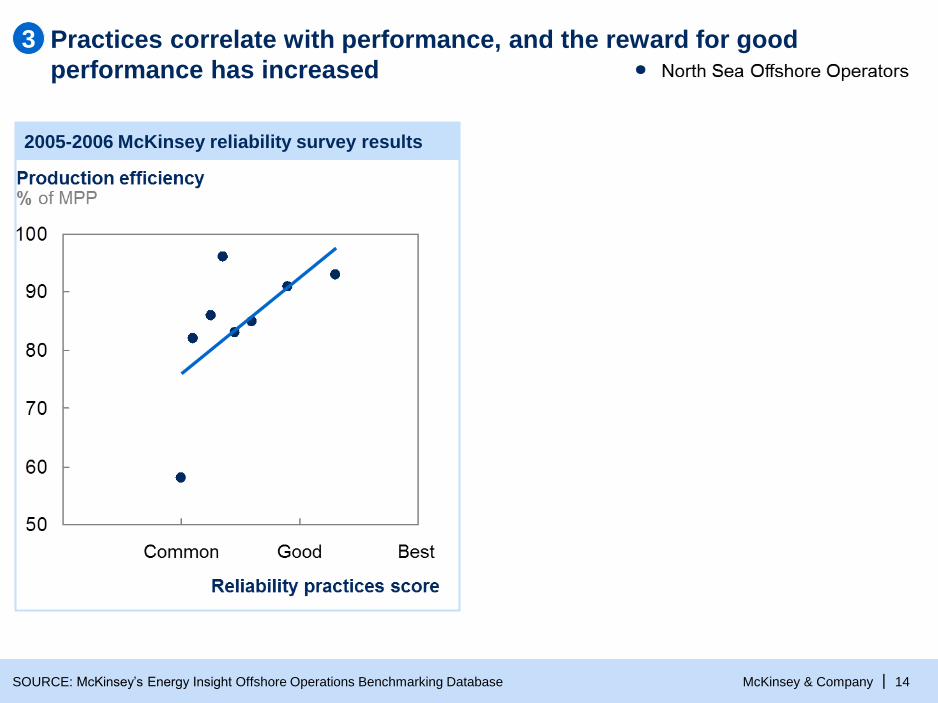

Practices correlate with performance, and the reward for good

performance has increased

2005-2006 McKinsey reliability survey results

3

SOURCE: McKinsey’s Energy Insight Offshore Operations Benchmarking Database

McKinsey & Company | 15

Practices correlate with performance, and the reward for good

performance has increased

SOURCE: McKinsey’s Energy Insight Offshore Operations Benchmarking Database

3

2010-2013 McKinsey reliability survey results

McKinsey & Company | 16

Clear correlation with the oil price – but is there any causation?

SOURCE: McKinsey Global Offshore Asset Efficiency Database, BP Statistical Review

4

McKinsey & Company | 17

What we are going to need to get right

Ability to manage costs

Delivering safety & asset integrity

Adding resources

Keeping production efficiency high

McKinsey & Company | 18

Change in costs 2001-2010

% of 2001 costs

Cost inflation

McKinsey & Company | 19

Cost inflation

1 Unweighted average of total lifting cost for 14 platforms (total cost, not cost per barrel)

Change in costs 2001-2010

% of 2001 costs

SOURCE: McKinsey’s Energy Insight Offshore Operations Benchmarking Database

McKinsey & Company | 20

We have remained optimistic that improvements are around the corner!

SOURCE: Oil & Gas UK 2012 Economic Report

McKinsey & Company | 21

But no sign of them yet

#% Annual change

1 Money of the day; based on a “basket” of installations

SOURCE: McKinsey’s Energy Insight Offshore Operations Benchmark

Lifting cost trends (North Sea example)1

Index, 1992 = 100, GBP base currency

McKinsey & Company | 22

What is behind the 10% increase?

Increased activity

McKinsey & Company | 23

What is behind the 10% increase?

McKinsey & Company | 24

What is behind the 10% increase?

McKinsey & Company | 25

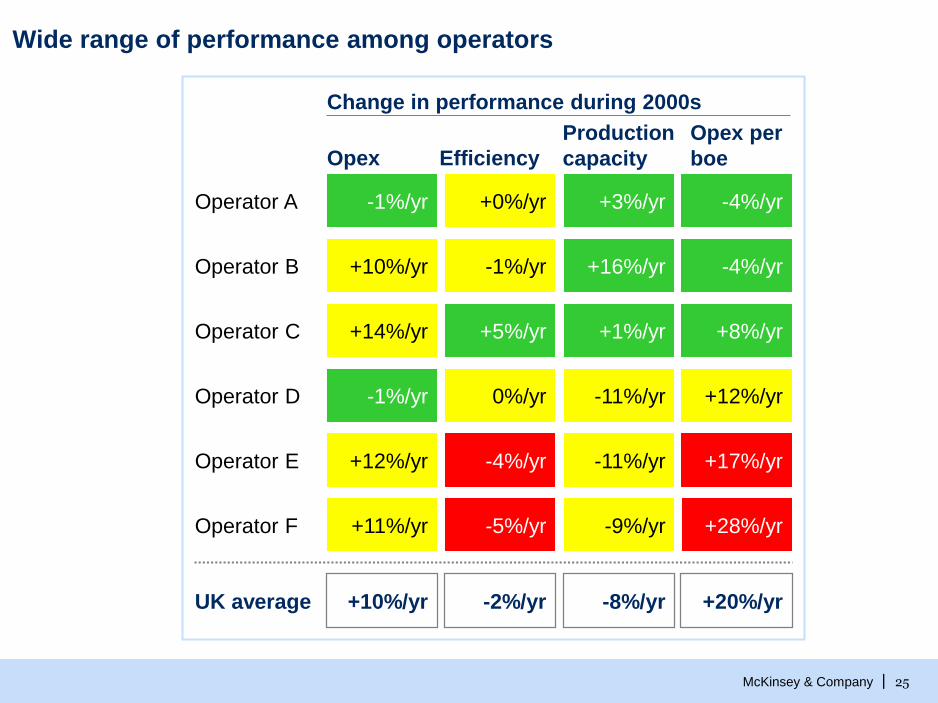

Wide range of performance among operators

Change in performance during 2000s

Opex Efficiency

Production

capacity

Opex per

boe

+10%/yr -2%/yr -8%/yr +20%/yrUK average

Operator A -1%/yr +0%/yr +3%/yr -4%/yr

Operator E +12%/yr -4%/yr -11%/yr +17%/yr

Operator F +11%/yr -5%/yr -9%/yr +28%/yr

Operator D -1%/yr 0%/yr -11%/yr +12%/yr

Operator C +14%/yr +5%/yr +1%/yr +8%/yr

Operator B +10%/yr -1%/yr +16%/yr -4%/yr

McKinsey & Company | 26

What might help?

Ownership and operatorship

▪ Consolidation of asset ownership and operatorship around key infrastructure?

▪ Exit of players from positions that are no longer material?

▪ Entry of additional experienced mature asset focused players?

McKinsey & Company | 27

What might help?

Ownership and operatorship

▪ Consolidation of asset ownership and operatorship around key infrastructure?

▪ Exit of players from positions that are no longer material?

▪ Entry of additional experienced mature asset focused players?

Operating practices and technology

▪ Systematic adoption of global operating best practices?

▪ Adoption of remote operations, “big data”, other technologies?

▪ Shared standards by operators and contractors for field integrity and reliability?

McKinsey & Company | 28

What might help?

Ownership and operatorship

▪ Consolidation of asset ownership and operatorship around key infrastructure?

▪ Exit of players from positions that are no longer material?

▪ Entry of additional experienced mature asset focused players?

Operating practices and technology

▪ Systematic adoption of global operating best practices?

▪ Adoption of remote operations, “big data”, other technologies?

▪ Shared standards by operators and contractors for field integrity and reliability?

Regulation

▪ Full transparency of data on operating reliability?

▪ Inspection regime to ensure shared infrastructure is operated and maintained

to high standards?

▪ Even sanctions for operators who consistently fail to meet reliability

expectations?

![At Scale Deployment of Enhanced Oil Recovery in BP Devex 2012v7)-MakingE... · Title: Microsoft PowerPoint - DEVEX 2012 (v7) - Making EOR Happen - Devex web.ppt [Compatibility Mode]](https://static.fdocuments.in/doc/165x107/5e4383bcde82b064140e1792/at-scale-deployment-of-enhanced-oil-recovery-in-bp-devex-v7-makinge-title.jpg)