THE FUTURE OF SHIPPING - Breaking Waves 2019 · THE FUTURE OF SHIPPING 4. GROWTH 3. Marke ting 2....

34

THE FUTURE OF SHIPPING Martin Stopford Non-Exec President, Clarkson Research Breaking waves 2018, Helsinki 3-4- December 2018

Transcript of THE FUTURE OF SHIPPING - Breaking Waves 2019 · THE FUTURE OF SHIPPING 4. GROWTH 3. Marke ting 2....

THE FUTURE OF SHIPPING

Martin Stopford

Non-Exec President, Clarkson Research

Breaking waves 2018, Helsinki 3-4- December 2018

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 2

1. Four “re-alignments” in maritime business

2. Meeting IMO emissions targets 2050

3. Spec out shipping’s long term business strategy

4. Make ships work better

5. Make sea transport systems work better.

6. Develop people & organizations to manage all this

THE FUTURE OF SHIPPING

4.

GROWTH

3. Marke

ting

2. Produc

t development

1.

idea

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 3

1. FOUR RE-ALIGNMENTS IN MARITIME BUSINESS

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 4

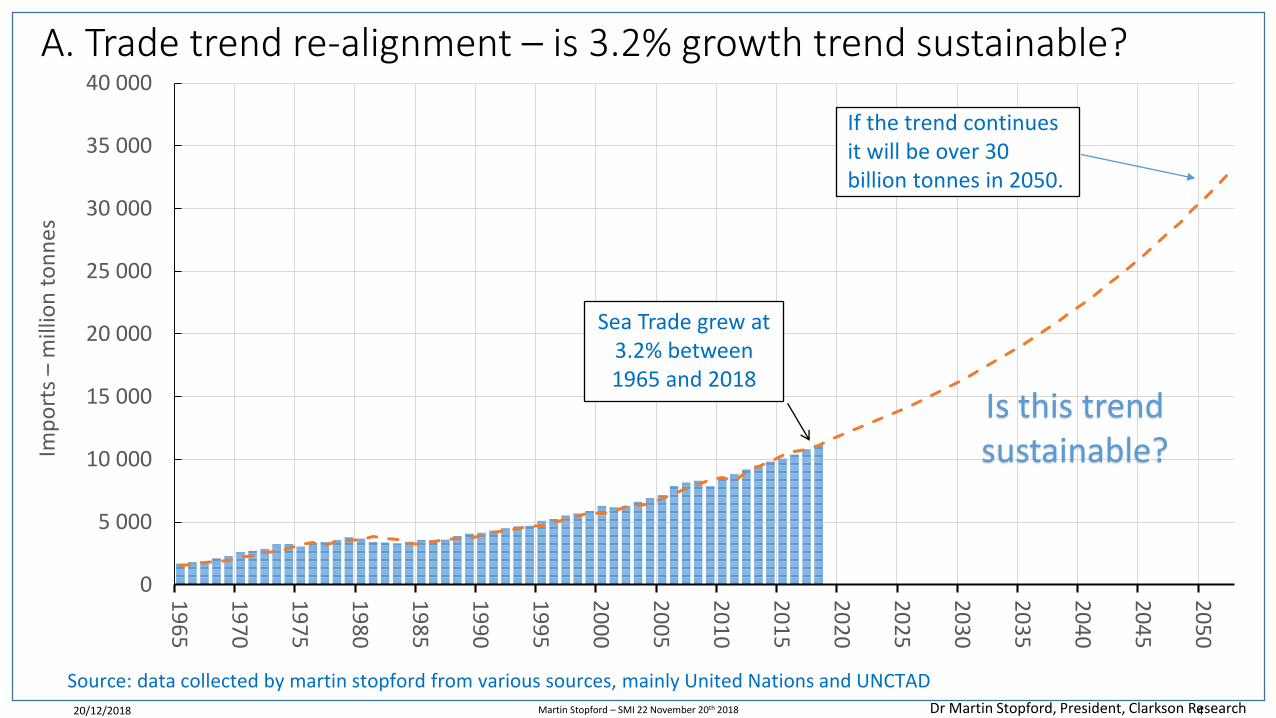

A. Trade trend re-alignment – is 3.2% growth trend sustainable?

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

20

20

20

25

20

30

20

35

20

40

20

45

20

50

Imp

ort

s –

mill

ion

to

nn

es

Sea Trade grew at 3.2% between 1965 and 2018

If the trend continues it will be over 30 billion tonnes in 2050.

Dr Martin Stopford, President, Clarkson Research

Source: data collected by martin stopford from various sources, mainly United Nations and UNCTAD

Is this trend sustainable?

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 5

20%

30%

40%

50%

60%

70%

80%

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Shows the of OECD & Non-OECD Imports as a % of world seaborne imports

1965: OECD 67% imports

Today Non-OECD is 67% imports –

new cargo matrix

B. Regional re-alignment – big change in control of sea imports

Source: United Nations, UNCTAD, compilation by Martin Stopford

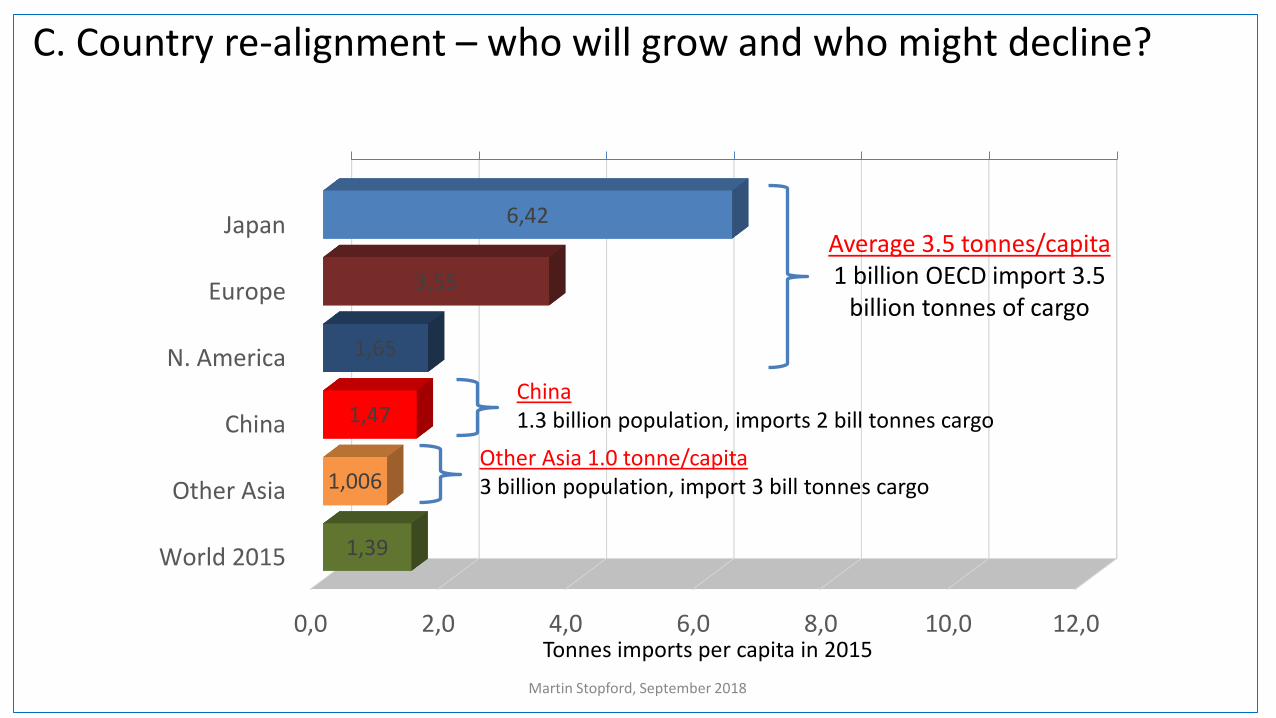

C. Country re-alignment – who will grow and who might decline?

0,0 2,0 4,0 6,0 8,0 10,0 12,0

Japan

Europe

N. America

China

Other Asia

World 2015

6,42

1,47

1,006

1,65

3,55

1,39

Martin Stopford, September 2018

Average 3.5 tonnes/capita1 billion OECD import 3.5

billion tonnes of cargo

Other Asia 1.0 tonne/capita3 billion population, import 3 bill tonnes cargo

Tonnes imports per capita in 2015

China1.3 billion population, imports 2 bill tonnes cargo

5 0

98

4 0

62

4 1

71

3 3

37

4 2

01

4 7

96

5 2

86

4 7

92

3 3

81

4 6

70

6 9

22

5 8

72

6 6

84

7 6

43

7 7

63

11

69

9

14

65

2

17

25

3

23

59

5

17

69

1

22

41

1

31

00

0

31

95

0

29

70

0 26

65

0

13

25

0

10

65

0

15

25

0

18

30

0

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$0

00

PER

DA

Y B

un

ker

cost

$ T

C r

ate

Aframax 1 year timecharter rate

in $/day

Based on Aframax tanker, 1 year TC rate and bunker cost at 50 TPD, 14.5 KTS, Rotterdam 380cst

In 2004 the daily cost of an Aframax tanker

was 4X cost of bunkers

NOW BUNKERS

COST MORE THAN SHIP

D. Factor price re-alignment – fuel now costs more than the ship

Bunker cost in $/day

Conclusion: OECD Europe’s share of global trade

and its influence on the way the industry uses ships is already slipping.

What preparations needed?

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 9

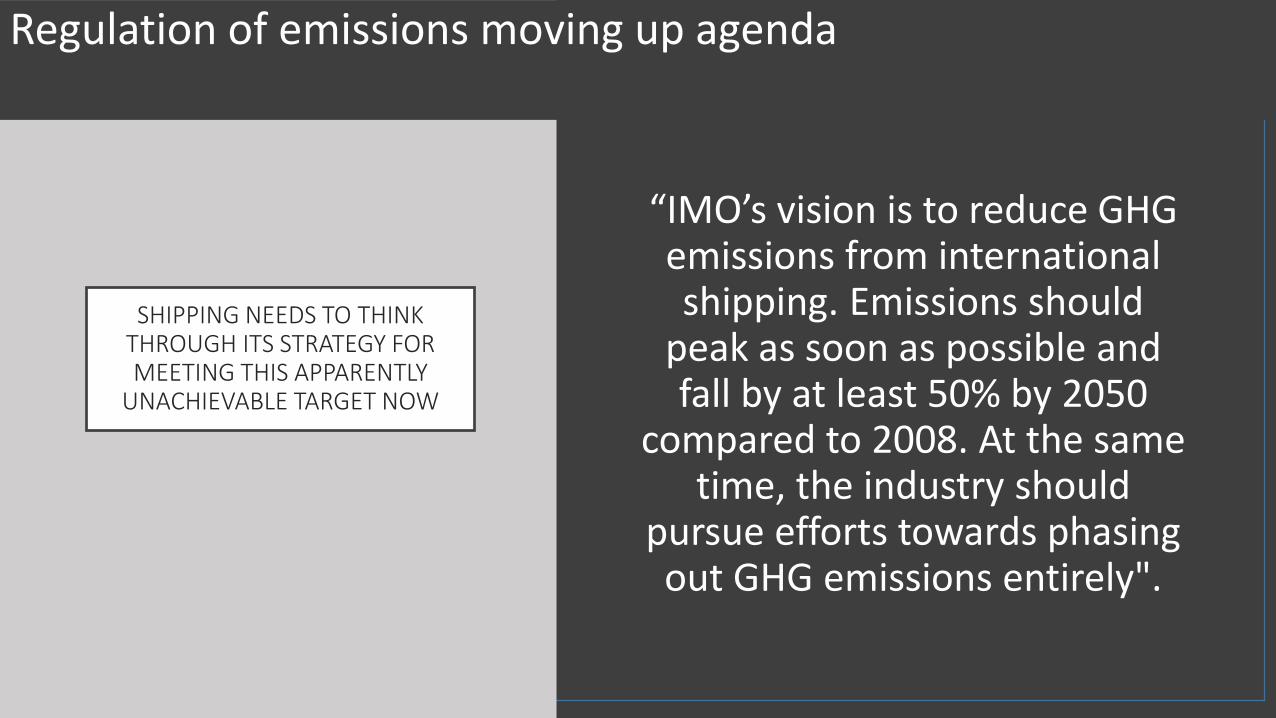

2: MEETING IMO EMISSIONS TARGETS IN 2050

SHIPPING NEEDS TO THINK THROUGH ITS STRATEGY FOR MEETING THIS APPARENTLY

UNACHIEVABLE TARGET NOW

“IMO’s vision is to reduce GHG emissions from international shipping. Emissions should

peak as soon as possible and fall by at least 50% by 2050

compared to 2008. At the same time, the industry should

pursue efforts towards phasing out GHG emissions entirely".

Regulation of emissions moving up agenda

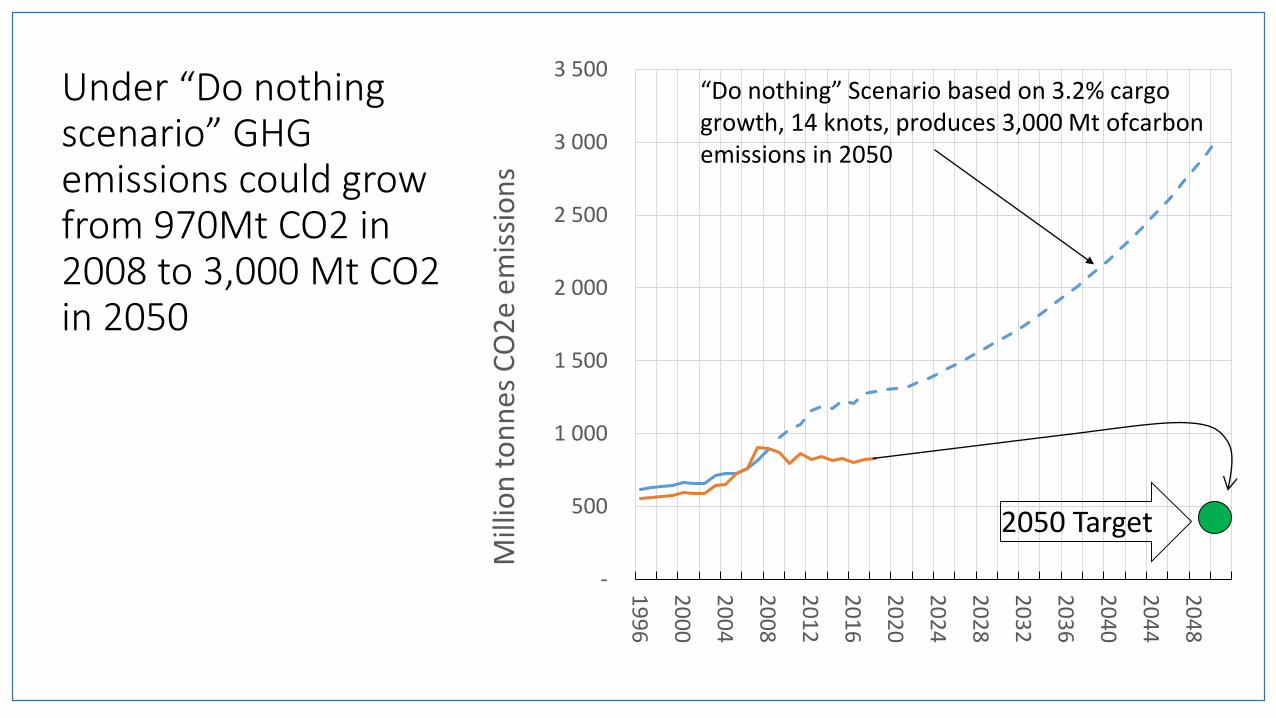

Under “Do nothing scenario” GHG emissions could grow from 970Mt CO2 in 2008 to 3,000 Mt CO2 in 2050

-

500

1 000

1 500

2 000

2 500

3 000

3 500

19

96

20

00

20

04

20

08

20

12

20

16

20

20

20

24

20

28

20

32

20

36

20

40

20

44

20

48

Mill

ion

to

nn

es C

O2

e em

issi

on

s

“Do nothing” Scenario based on 3.2% cargo growth, 14 knots, produces 3,000 Mt ofcarbonemissions in 2050

2050 Target

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 13

Four ways to CO2 emissions in 2050 from 3,000 Mt to 470 Mt

• Step 1: Transport less cargo by changing trading patterns, transport policies, pricing and better information systems (38% saving)

• Step 2: Cut carbon emissions/ship km by slowing down to 10.1 knots; using bigger “small” ships; designs; retrofitting for safe operation at slow speeds etc (40% saving)

• Step 3: Develop zero carbon propulsion systems. Electric fuel cells look the best bet for volume and performance (8.5% saving)

• Step 4: Finally make solutions 1-4 effective by a complete re-think of the industry’s organization and personnel structures

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 14

CO2 Emissions by the world cargo fleet -5 ways to cut them

-

500

1 000

1 500

2 000

2 500

3 000

3 500

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

20

42

20

44

20

46

20

48

20

50

Mill

ion

to

nn

es

CO

2e

emis

sio

ns

2050 IMO target 470 Mt CO2e

4. 10.1 knots, 2.2% pa cargo

2.Double ship size

from 32,000 dwt to

70,000 dwt

Key conclusion…“We must start actively planning for ships to go much slower in future. And introduce hydrogen (e.g. powering fuel cells or internal combustion engines), as soon as possible to finish the job”

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 15

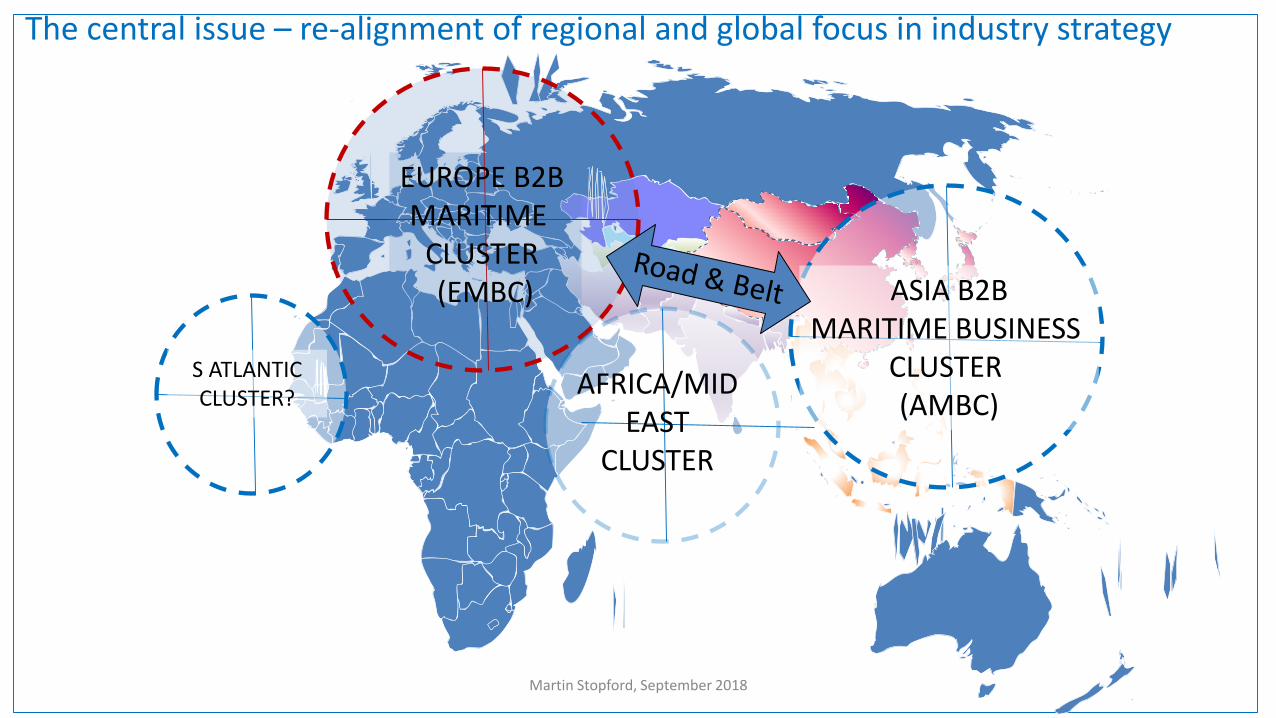

3. SHAPING SHIPPING’S 2050 STRATEGY

Martin Stopford, September 2018

The central issue – re-alignment of regional and global focus in industry strategy

EUROPE B2B MARITIME

CLUSTER (EMBC) ASIA B2B

MARITIME BUSINESS CLUSTER (AMBC)

AFRICA/MID EAST

CLUSTER

S ATLANTIC CLUSTER?

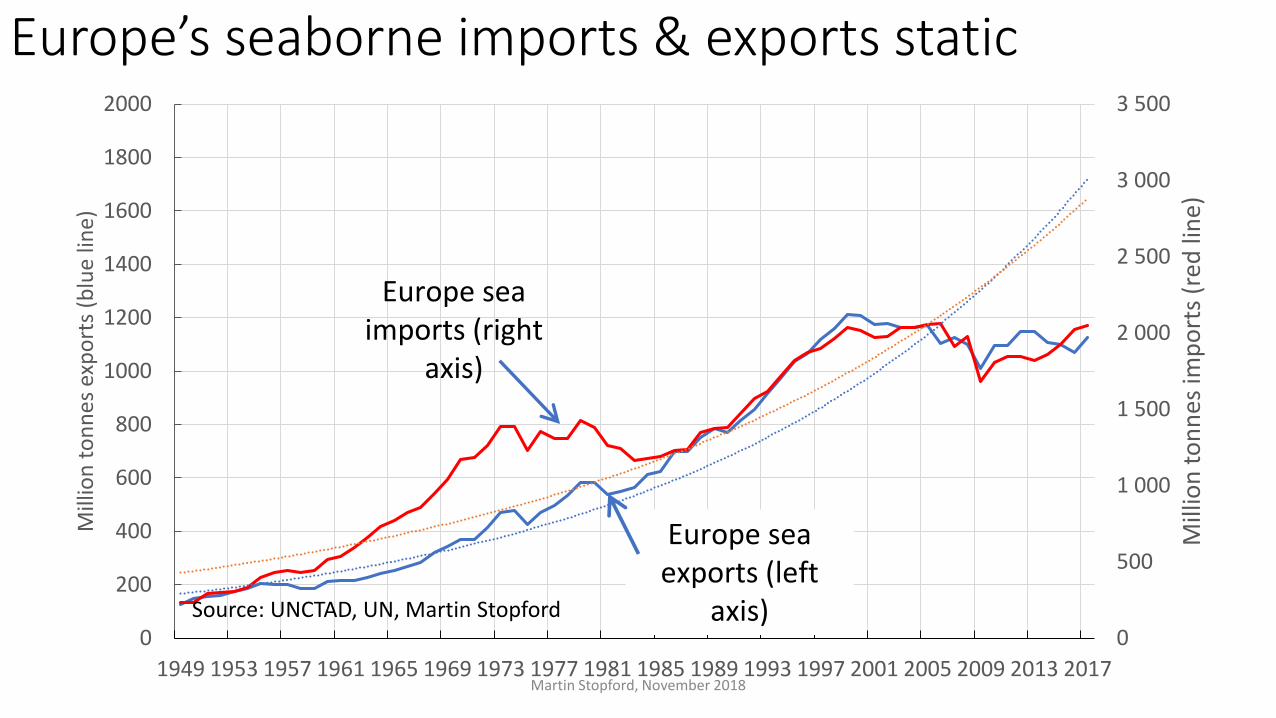

Europe’s seaborne imports & exports static

0

500

1 000

1 500

2 000

2 500

3 000

3 500

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1949 1953 1957 1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009 2013 2017

Mill

ion

to

nn

es im

po

rts

(red

lin

e)

Mill

ion

to

nn

es

exp

ort

s (b

lue

lin

e)

Europe sea imports (right

axis)

Europe sea exports (left

axis)

Martin Stopford, November 2018

Source: UNCTAD, UN, Martin Stopford

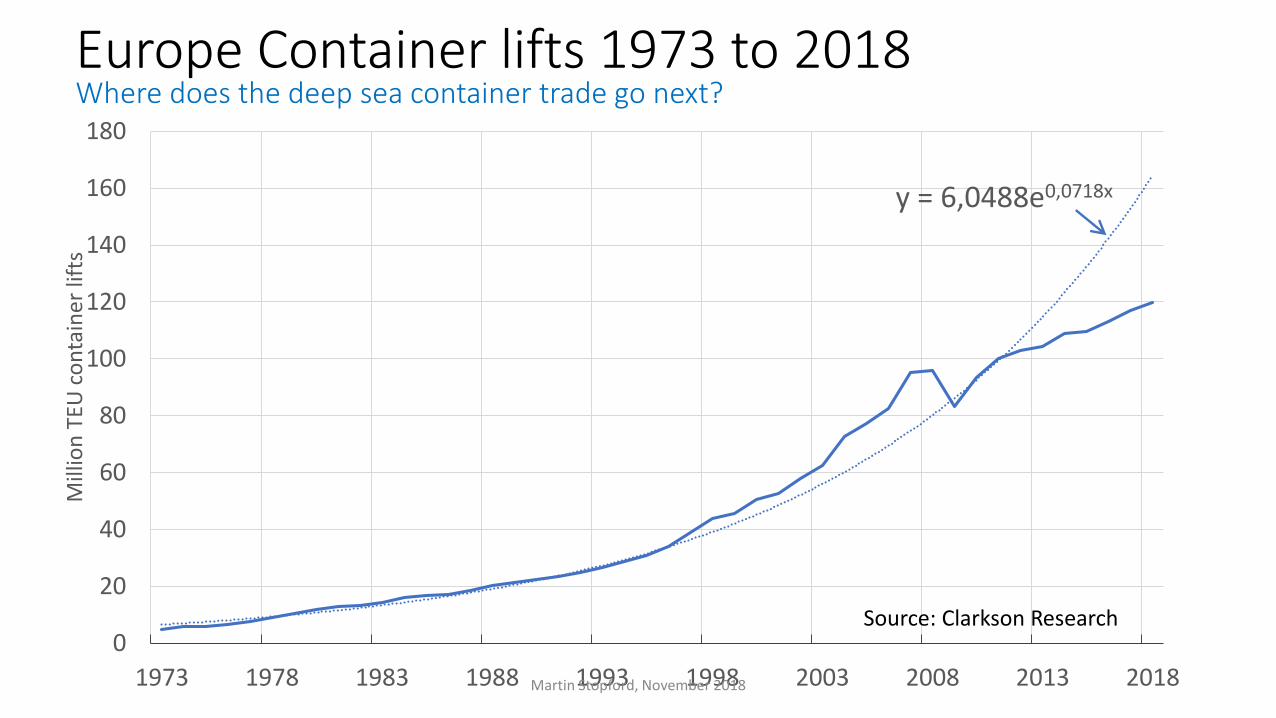

Europe Container lifts 1973 to 2018

y = 6,0488e0,0718x

0

20

40

60

80

100

120

140

160

180

1973 1978 1983 1988 1993 1998 2003 2008 2013 2018

Mill

ion

TEU

co

nta

iner

lift

sWhere does the deep sea container trade go next?

Martin Stopford, November 2018

Source: Clarkson Research

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 20

PART 4: MAKING

SHIPS WORK BETTER BY

2050

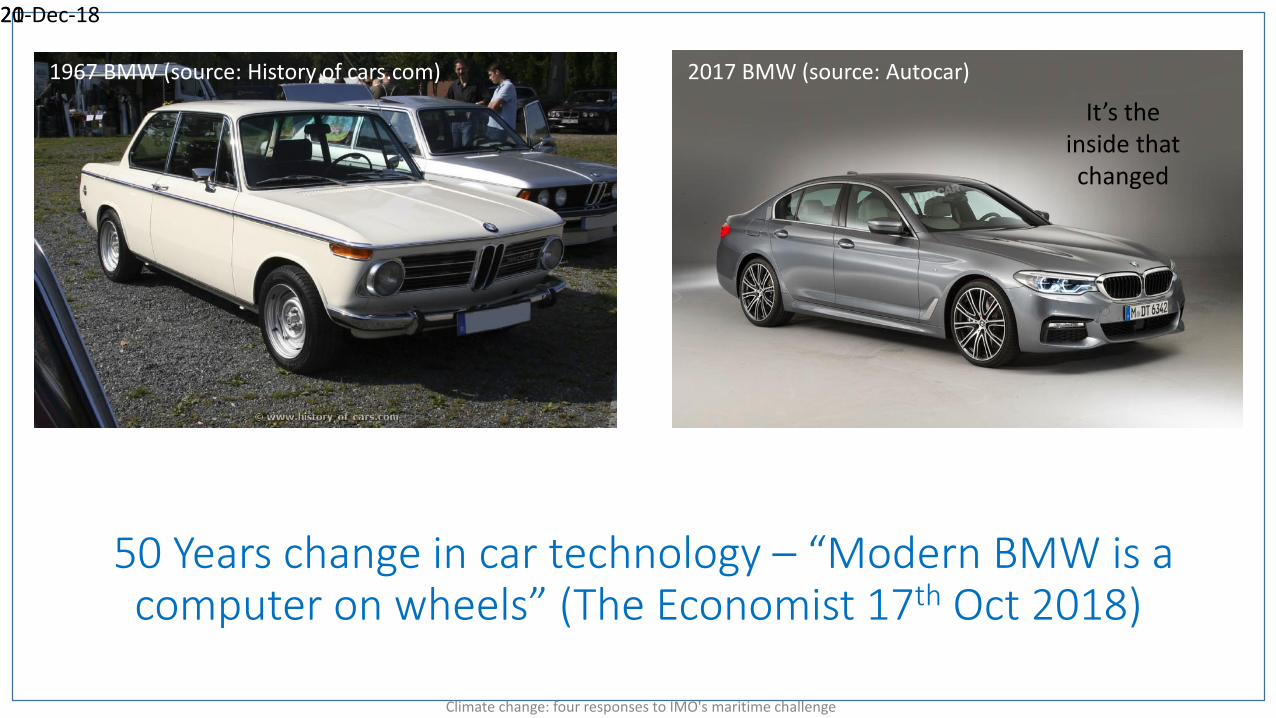

50 Years change in car technology – “Modern BMW is a computer on wheels” (The Economist 17th Oct 2018)

Climate change: four responses to IMO's maritime challenge

1967 BMW (source: History of cars.com) 2017 BMW (source: Autocar)

It’s the inside that changed

20-Dec-1821

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 22

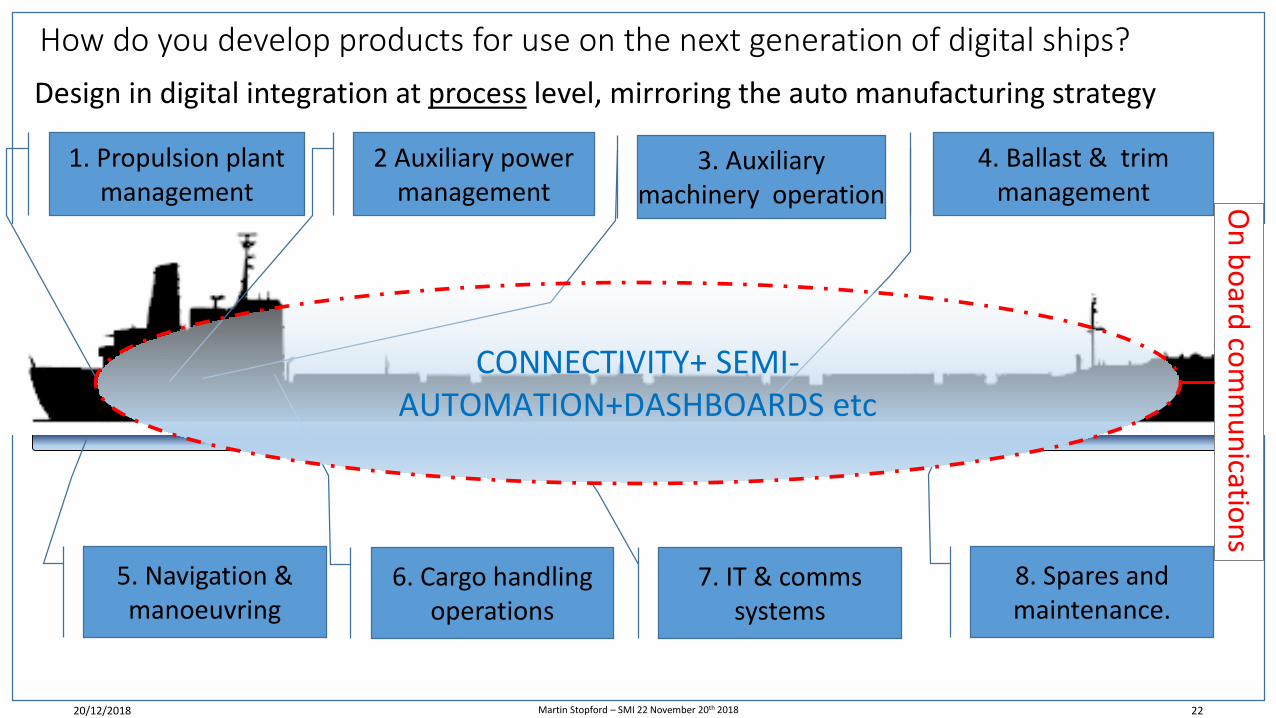

How do you develop products for use on the next generation of digital ships?

5. Navigation & manoeuvring

1. Propulsion plant management

2 Auxiliary power management

3. Auxiliary machinery operation

4. Ballast & trim management

6. Cargo handling operations

7. IT & comms systems

8. Spares and maintenance.

Design in digital integration at process level, mirroring the auto manufacturing strategy

CONNECTIVITY+ SEMI-AUTOMATION+DASHBOARDS etc

On

bo

ard co

mm

un

ication

s

Example 1: Seamless - voyage management systems

Shipping office voyage analysis team

Fleet management dashboardFleet liaison managerShip managers

Terminal management dashboard

Terminal scheduling team

Martin Stopford, November 2018

Voyage monitoring and weather planning systemData exchange to & from ships

Example 2: Improved -mooring systems

• Hawser mooring is dangerous and labour intensive

• For example officer on Zara (top left) suffered severe head injuries when he was struck by a parted HMPE mooring rope

• Big ships needs to carry five or six people to manage the mooring

• Dynamic magnetic and suction cup systems are in operation for bunkering and mooring deep sea vessels.

Moormaster 400 units, each have two

suction cup panels of twenty tons power.

Combined whole system delivers a

mooring force of 160 tons. Martin Stopford, November 2018

Example 3: autonomous cargo handling - 25,600 dwt LNG self-discharging bulk carrier

• Haaga and Viikki are first bulkers with autonomous self-discharging cranes. This function should be operative in the next few months.

• Using sensor technology, cameras and laser scanners, the cranes analysethe topography of each cargo hold and determine the optimal lifting points.

• An 'intelligent' self-learning algorithm ensures the bucket is not overloaded and compensates for heeling to ensure even unloading. The algorithm also calculates which shoreside hopper to discharge into.

• Some of the technology, such as the grab’s learning capability, will be adapted for use with other systems such as small container ships

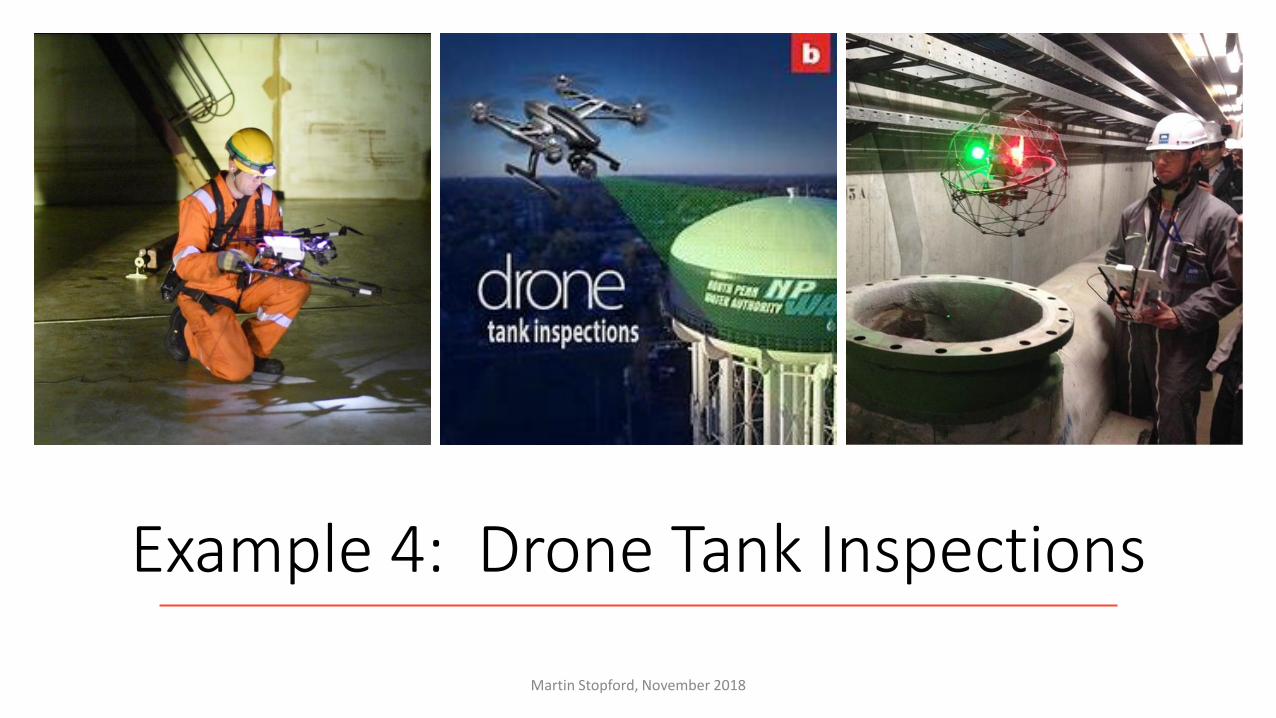

Example 4: Drone Tank Inspections

Martin Stopford, November 2018

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 27

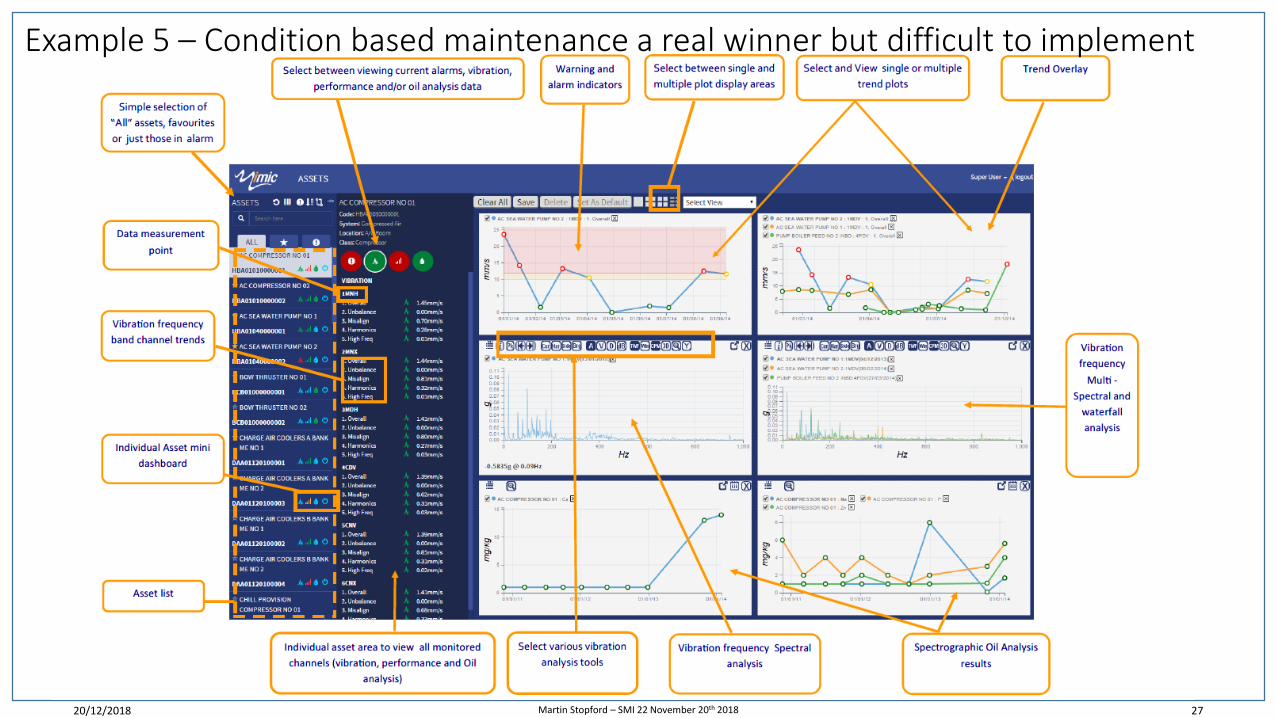

Example 5 – Condition based maintenance a real winner but difficult to implement

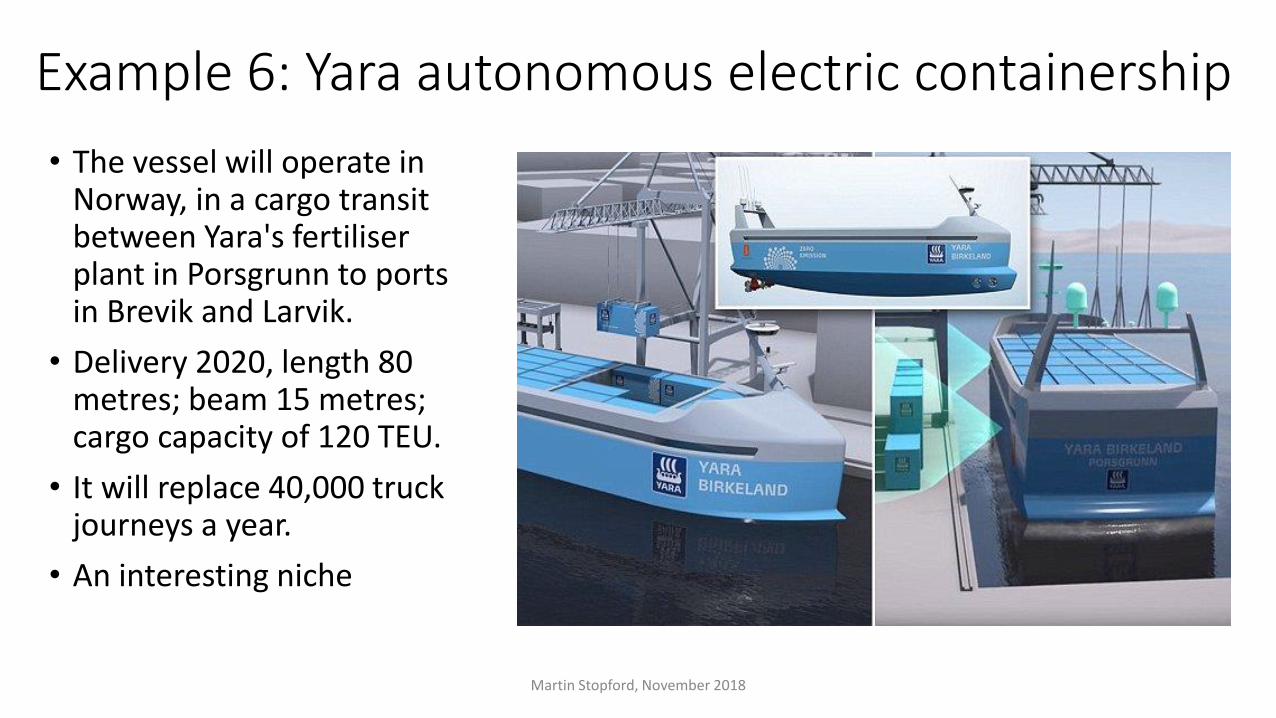

Example 6: Yara autonomous electric containership

• The vessel will operate in Norway, in a cargo transit between Yara's fertiliser plant in Porsgrunn to ports in Brevik and Larvik.

• Delivery 2020, length 80 metres; beam 15 metres; cargo capacity of 120 TEU.

• It will replace 40,000 truck journeys a year.

• An interesting niche

• es

Martin Stopford, November 2018

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 29

PART 5: MAKING SEA

TRANSPORT SYSTEMS WORK BETTER BY 2050

The Fleet: manage the fleet of ships as an I4 “Transport Factory”

Martin Stopford, September 2018

Source: Martin Stopford 2016

DATA READY SHIPS

1. Navigation 2. Operations3. Comms.

Core systems

1. SHIP TEAMS

ship servers managing data, apps & comms

6. SHIPBUILDERS & EQUIPMENT

SUPPLIERS

5.CUSTOMERS WITH CARGO SYSTEMS

7. PORTS & THROUGH

TRANSPORT

Warehouse(on cloud?)

Company Systems:-1. Process management2. STQ monitoring3. Messaging system4. Intranet & dashboards5. Fleet maintenance6. LPWAN & APIs

3. SYSTEM

S. TEAM

S

1. Support systems2. Process data3. Automation4. Build apps5. Manage stats

1. Technical support 2. Maintenance systems3. Regulatory reports4. Fleet performance5. Personnel management

4. TEC

HN

ICA

L TEAM

S

2. SH

OR

E TEAM

S

Fleet managementBut… how do you link all these

systems together?

PART 6:HELPING PEOPLE WORK BETTER BY

2050

20-Dec-18 Climate change: four responses to IMO's maritime challenge

32

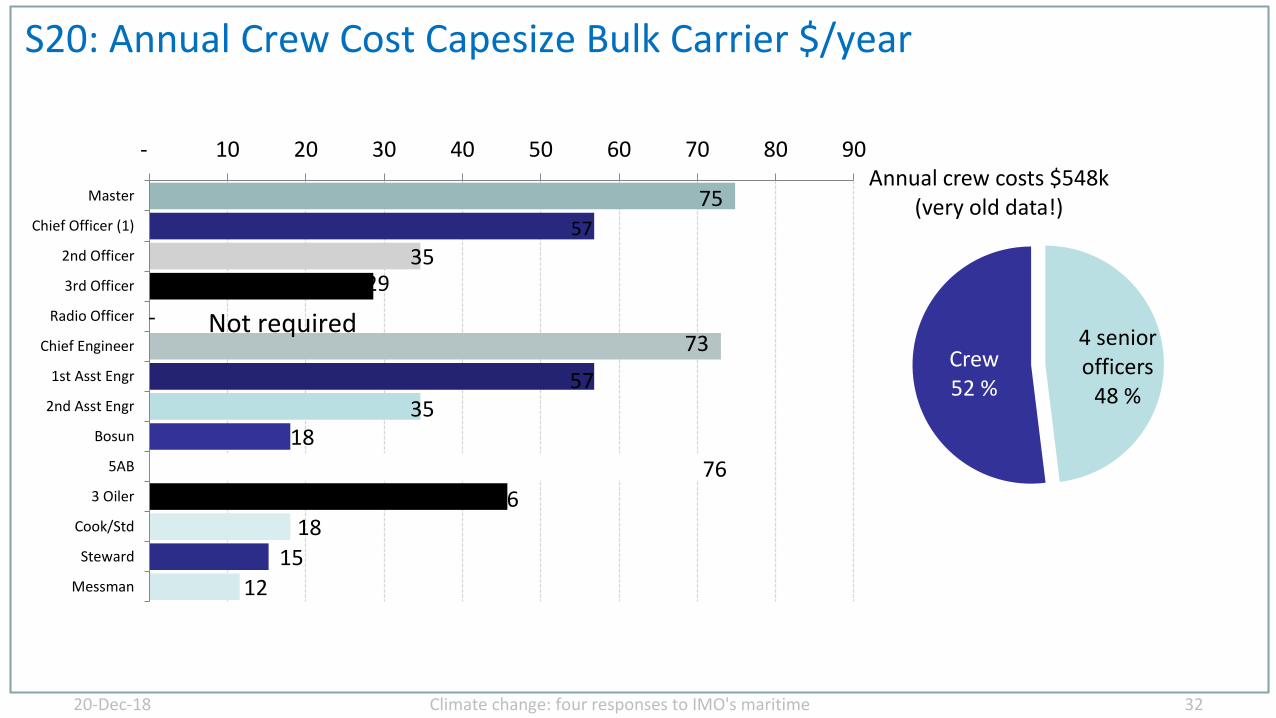

S20: Annual Crew Cost Capesize Bulk Carrier $/year

75

-

57

35 29

73

57 35

18

76

46 18

15

12

- 10 20 30 40 50 60 70 80 90

Master

Chief Officer (1)

2nd Officer

3rd Officer

Radio Officer

Chief Engineer

1st Asst Engr

2nd Asst Engr

Bosun

5AB

3 Oiler

Cook/Std

Steward

Messman

4 senior officers

48 %

Crew52 %

Annual crew costs $548k(very old data!)

Not required

Manage the fleet as a Transport Factory (teamwork across group & with others)

DATA READY SHIPS

6. SHIPBUILDERS & EQUIPMENT

SUPPLIERS

5.CUSTOMERS WITH CARGO SYSTEMS

7. PORTS & THROUGH

TRANSPORT

TRA

NSP

OR

T FA

CTO

RY

Warehouse(on cloud?)

Company Systems:-1. Process management2. STQ monitoring3. Messaging system4. Intranet & dashboards5. Fleet maintenance6. LPWAN & APIs

3. SYSTEM

S. TEAM

S 2

. SHO

RE TEA

MS

Fleet management

Performance measurement is key!!

4. TEC

HN

ICA

L TEAM

S

1. Technical support 2. Maintenance systems3. Regulatory reports4. Fleet performance5. Personnel management

1. Support systems2. Process data3. Automation4. Build apps5. Manage stats

1. Navigation 2. Operations3. Comms.

Core systems

1. SHIP TEAMS

ship servers managing data, apps & comms

Better balanced personnel system? Spot the difference!

Climate change: four responses to IMO's maritime challenge

Conclusions1. The maritime trade role of the OECD Europe is slipping.

2. B2B maritime logistics and GHG reduction are super strategic goals – we can excel in both, so lets go for it!!

3. We need smart trade management to ensure trade adds value in commercial & carbon terms.

4. Also increase ship size, focussing on the smaller end.

5. ASAP cut GHG emissions with a new generation of ships optimised for e.g. 10 knots and low carbon.

6. Replace diesel engines with hydrogen power (e.g. fuel cells/plasma) from the mid-20s onwards.

7. Massively improve performance measurement

8. Re-think of organisation structures for smart management, teamwork and more balanced workforce

20-Dec-18 34

The trick is to decide where you

want to go, get your head down,

and GO

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 35

THE END

20/12/2018 Martin Stopford – SMI 22 November 20th 2018 36

“The statistical, graphical information contained in this paper are drawn from the Clarkson Research Services Limited ("CRSL") database and other sources. CRSL advises that: (i) some information in CRSL's database is derived from estimates or subjective judgments; and (ii) the information in the databases of other maritime data collection agencies may differ from the information in CRSL's database; and (iii) whilst CRSL has taken reasonable care in the compilation of the statistical and graphical information and believes it to be accurate and correct, data compilation is subject to limited audit and validation procedures and may accordingly contain errors; and (iv) CRSL, its agents, officers and employees do not accept liability for any loss suffered in consequence of reliance on such information or in any other manner; and (v) the provision of such information does not obviate any need to make appropriate further enquiries; (vi) the provision of such information is not an endorsement of any commercial policies and/or any conclusions by CRSL; and (vii) shipping is a variable and cyclical business and anyone who thinks they can forecast it needs their head examining. Where views are expressed they are in the context of this general presentation and should not be used or relied on in any other context without appropriate investigation, validation and the written permission of the author

Disclaimer

![Deterroinin ftxed and operat n costs o£ ]o in £qu pment](https://static.fdocuments.in/doc/165x107/615a0afcc0db1800ce0a4f58/deterroinin-ftxed-and-operat-n-costs-o-o-in-qu-pment.jpg)