The future of fishing and the seafood industry Ragnar Tveteras University of Stavanger, Norway...

37

The future of fishing and the seafood industry Ragnar Tveteras University of Stavanger, University of Stavanger, Norway Norway International Fishmeal and Fish Oil Organisation Annual Conference 2006 Barcelona, Spain

-

Upload

abraham-hodges -

Category

Documents

-

view

217 -

download

0

Transcript of The future of fishing and the seafood industry Ragnar Tveteras University of Stavanger, Norway...

The future of fishing and the seafood industry

Ragnar Tveteras

University of Stavanger, NorwayUniversity of Stavanger, Norway

International Fishmeal and Fish Oil Organisation

Annual Conference 2006 Barcelona, Spain

Issues

Global supply trends

Global demand trends

Development of prices at different stages of supply chain for selected species/products

Emergence of large suppliers of seafood with focus on processing and distribution

At what stages of seafood supply chains will profits be earned in the future?

Strategic challenges for the aquaculture industry

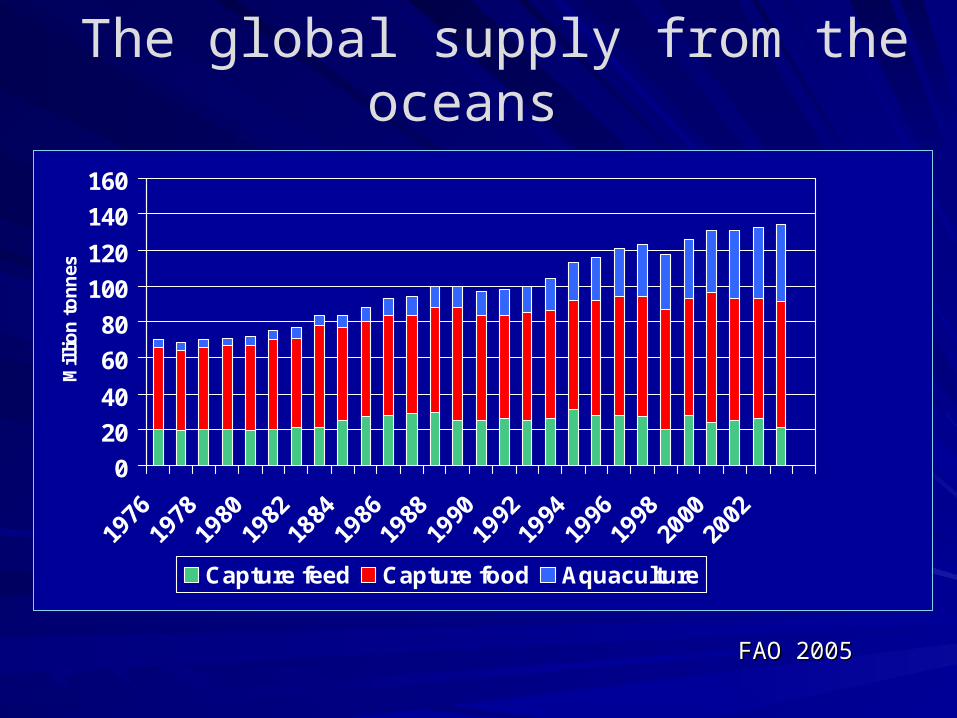

The global supply from the oceans

0

20

40

60

80

100

120

140

160

1976

1978

1980

1982

1884

1986

1988

1990

1992

1994

1996

1998

2000

2002

Mil

lio

n t

on

nes

Capture feed Capture food Aquaculture

FAO 2005FAO 2005

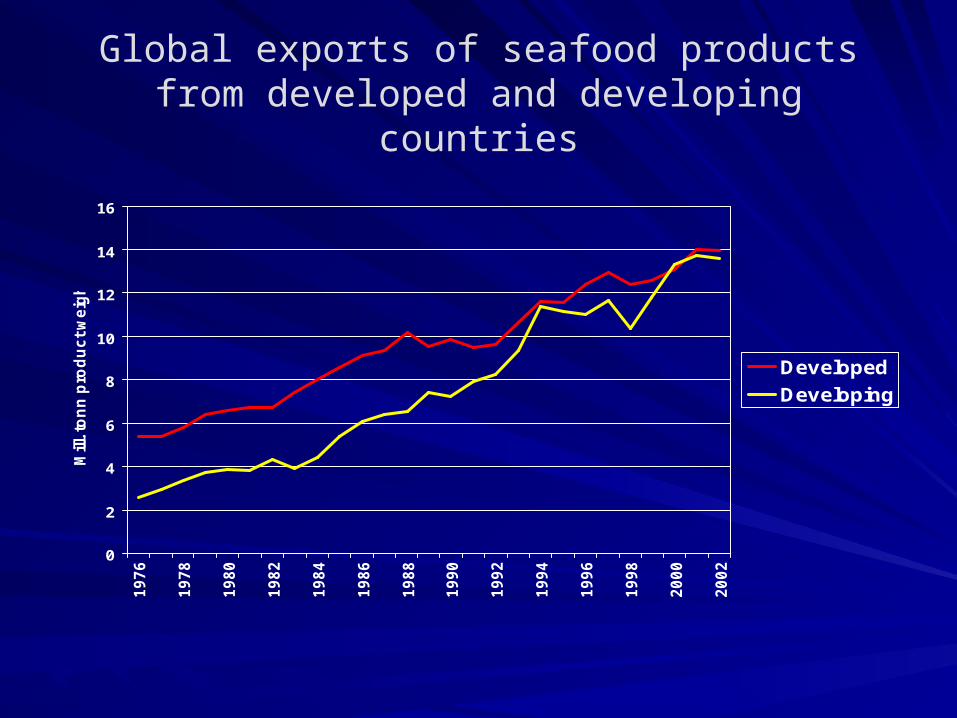

Global exports of seafood products from developed and developing countries

0

2

4

6

8

10

12

14

16

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

Mill

. to

nn

pro

du

ct

we

igh

t

Developed

Developing

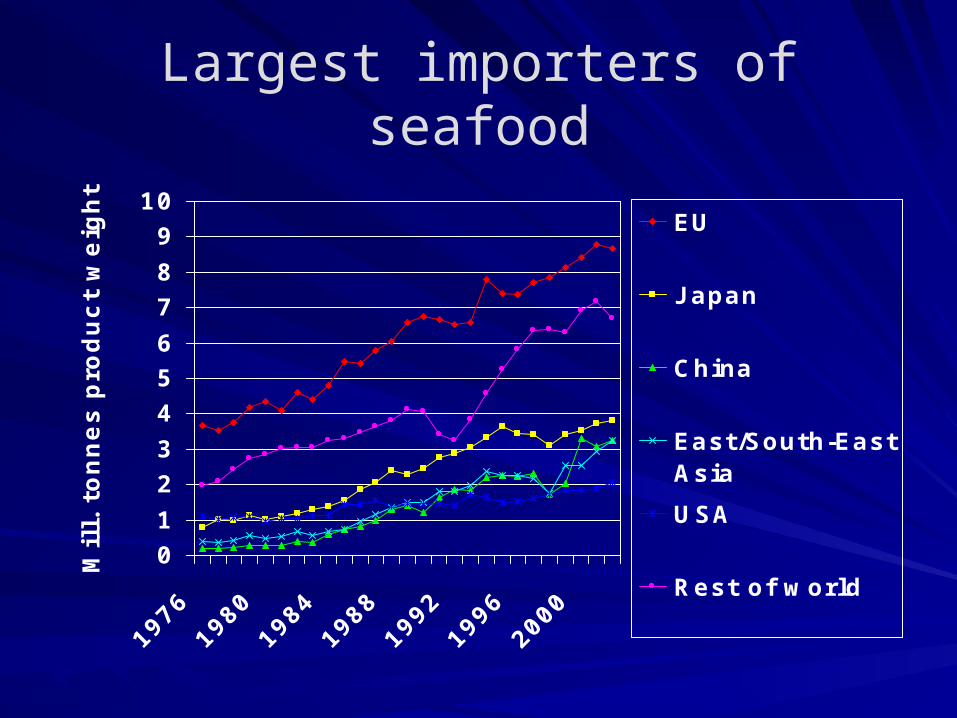

Largest importers of seafood

0

1

2

3

4

5

6

7

8

9

10

1976

1980

1984

1988

1992

1996

2000

Mil

l. t

on

ne

s p

rod

uc

t w

eig

ht

EU

J apan

China

East/South-EastAsia

USA

Rest of world

Supply side trends in food fisheries

Many food fisheries struggle with poor regulation– Both in developed and developing countries, for

example, the European Union– Technology and capacity versus political will and

resources– It will take a long time to improve regulation

performance

Some food fisheries sectors are improving their competitiveness through increased ability to supply modern distribution channels with e.g. fresh fish

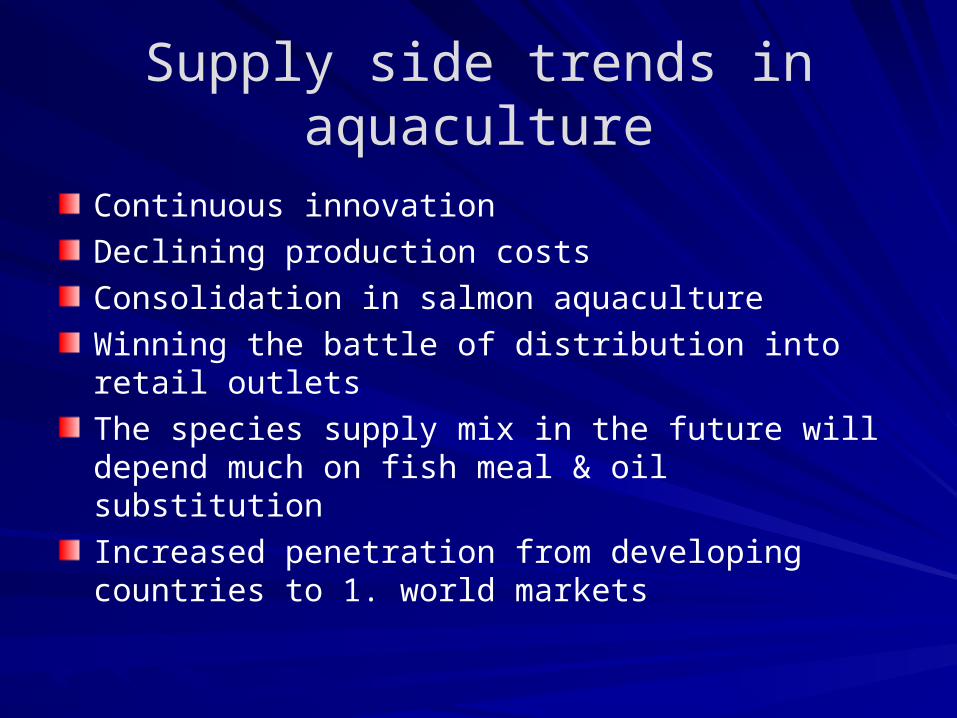

Supply side trends in aquaculture

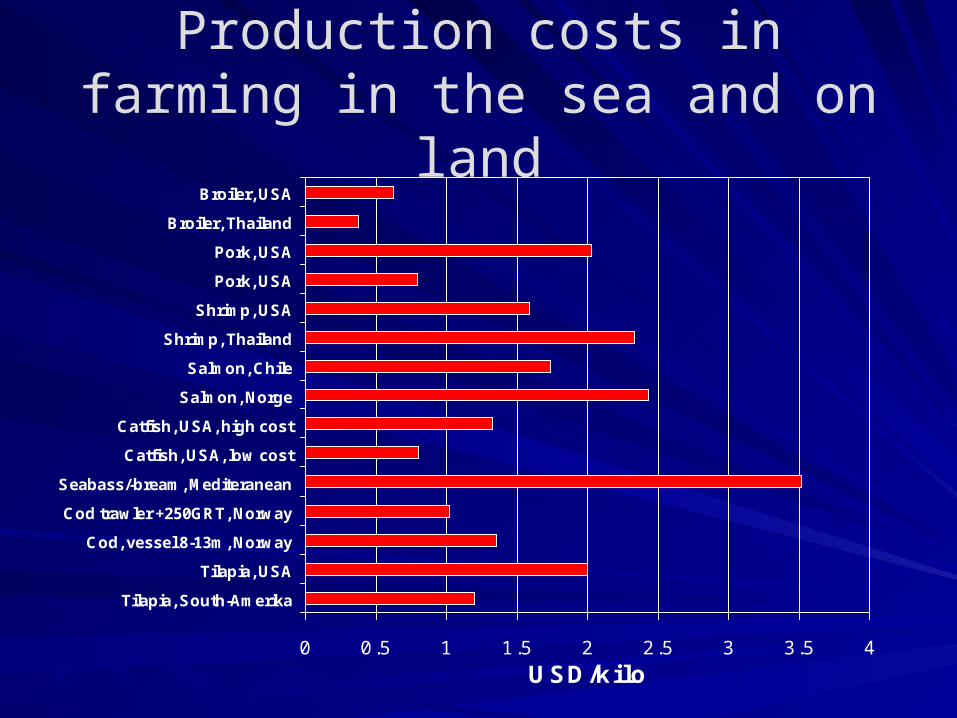

Continuous innovationDeclining production costsConsolidation in salmon aquacultureWinning the battle of distribution into retail outletsThe species supply mix in the future will depend much on fish meal & oil substitutionIncreased penetration from developing countries to 1. world markets

Production costs in farming in the sea and on land

0 0.5 1 1.5 2 2.5 3 3.5 4

Tilapia, South-Amerika

Tilapia, USA

Cod, vessel 8-13m, Norway

Cod trawler +250GRT, Norway

Seabass/-bream, Mediteranean

Catfish, USA, low cost

Catfish, USA, high cost

Salmon, Norge

Salmon, Chile

Shrimp, Thailand

Shrimp, USA

Pork, USA

Pork, USA

Broiler, Thailand

Broiler, USA

USD/kilo

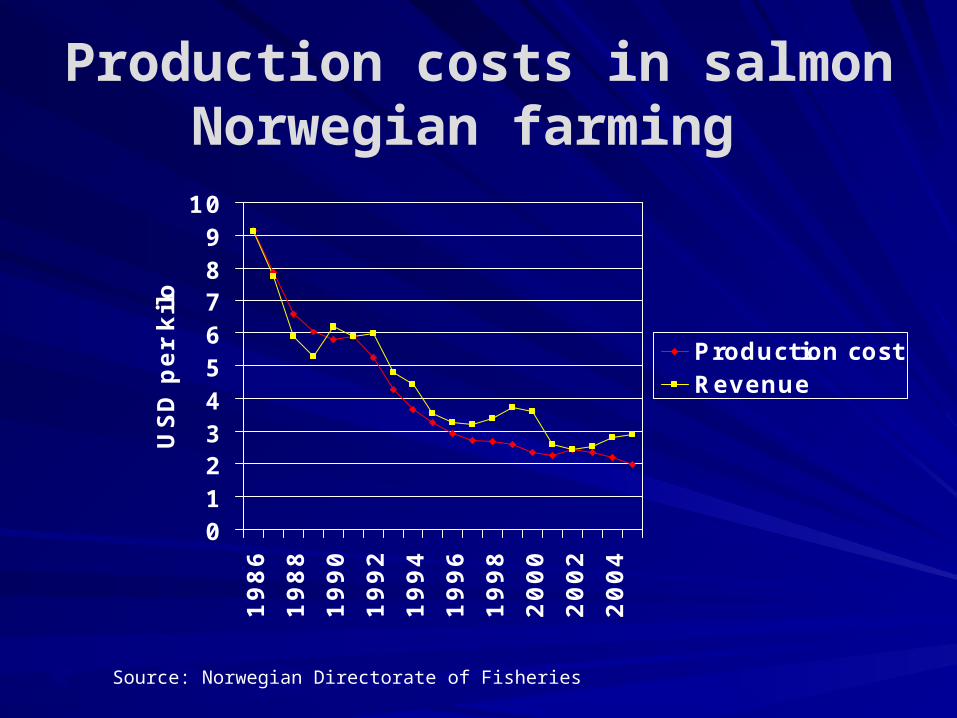

Production costs in salmon Norwegian farming

Source: Norwegian Directorate of Fisheries

0123456789

10

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

US

D p

er

kilo

Production costRevenue

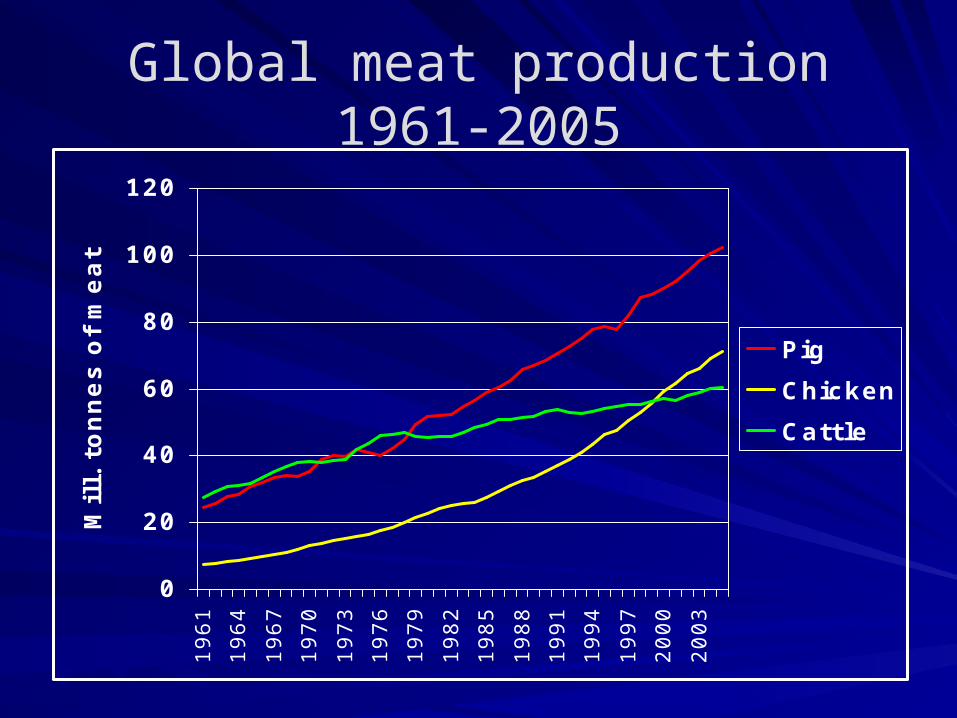

Global meat production 1961-2005

0

20

40

60

80

100

1201

96

1

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

Mil

l. t

on

ne

s o

f m

ea

t

Pig

Chicken

Cattle

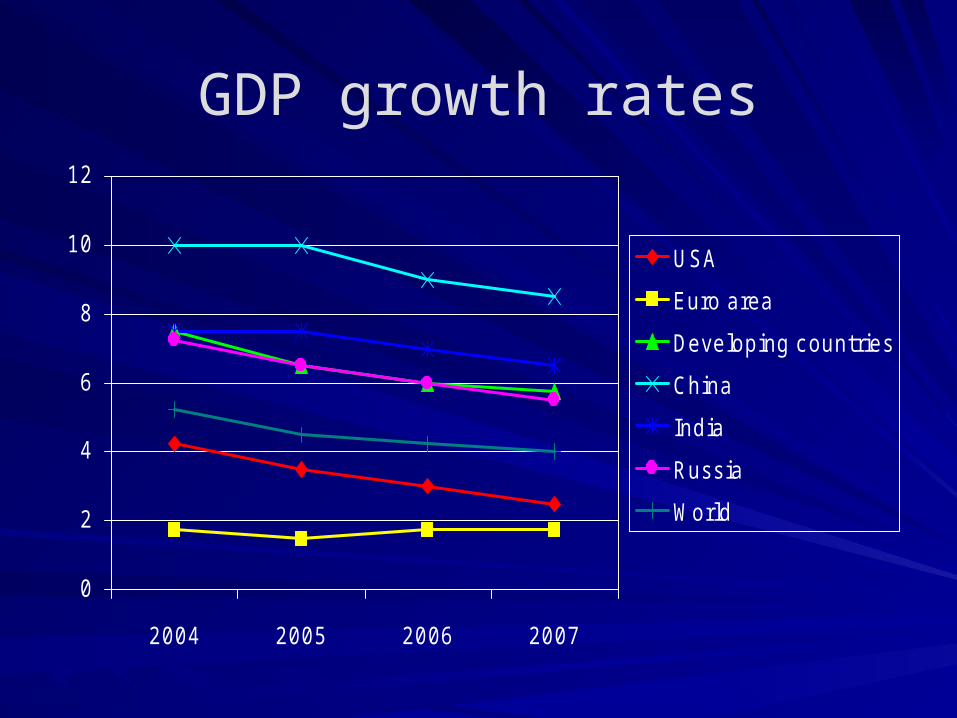

GDP growth rates

0

2

4

6

8

10

12

2004 2005 2006 2007

USA

Euro area

Developing countries

China

India

Russia

World

Global seafood demand trends

Income growth in many countries– Middle class grows– Accompanied by development of modern food distribution

systems and shift in distribution channels to consumers– Shift from cheap proteins to more luxury seafood– Industrialized aquaculture species benefits particularly from

thisHealth trends in developed countries– Omega-3 is one of the winners when consumers search for

healthy alternatives in their diets

Fish meal & oil sector benefit from increased demand for fish in general and carnivorous fish and shrimp in particular

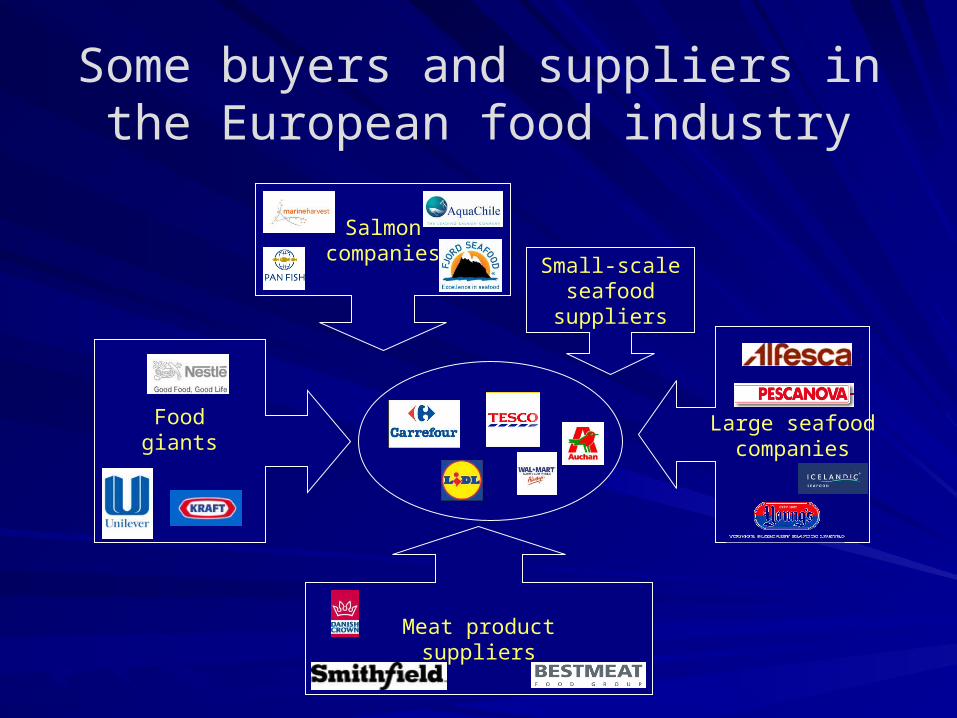

Some buyers and suppliers in the European food industry

Foodgiants

Meat productsuppliers

Large seafoodcompanies

Salmoncompanies

Small-scaleseafoodsuppliers

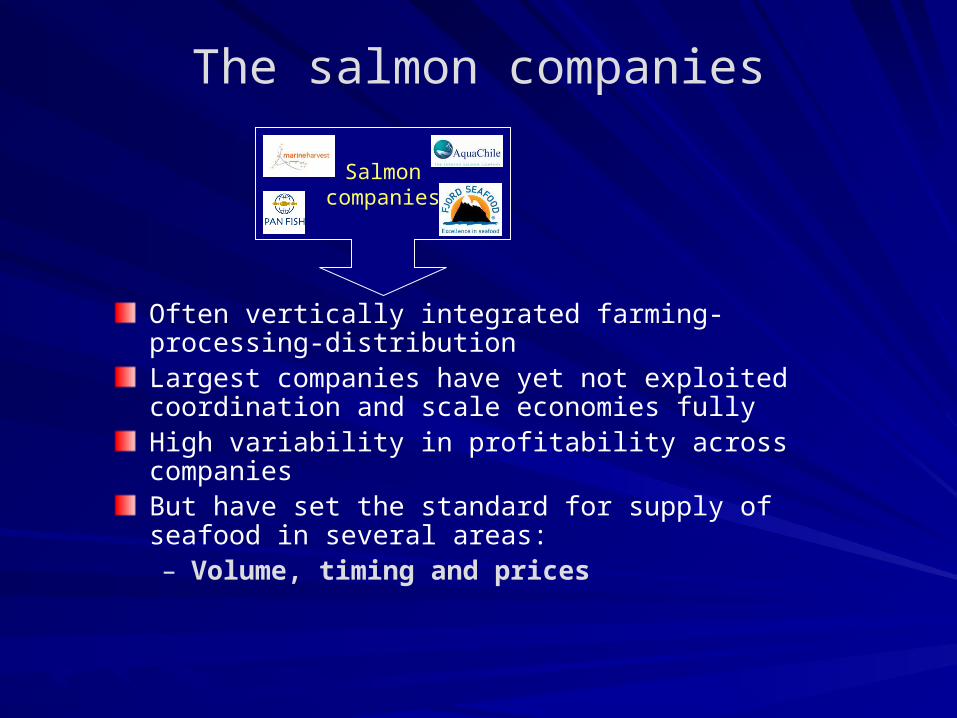

The salmon companies

Salmoncompanies

Often vertically integrated farming-processing-distributionLargest companies have yet not exploited coordination and scale economies fullyHigh variability in profitability across companiesBut have set the standard for supply of seafood in several areas:– Volume, timing and prices

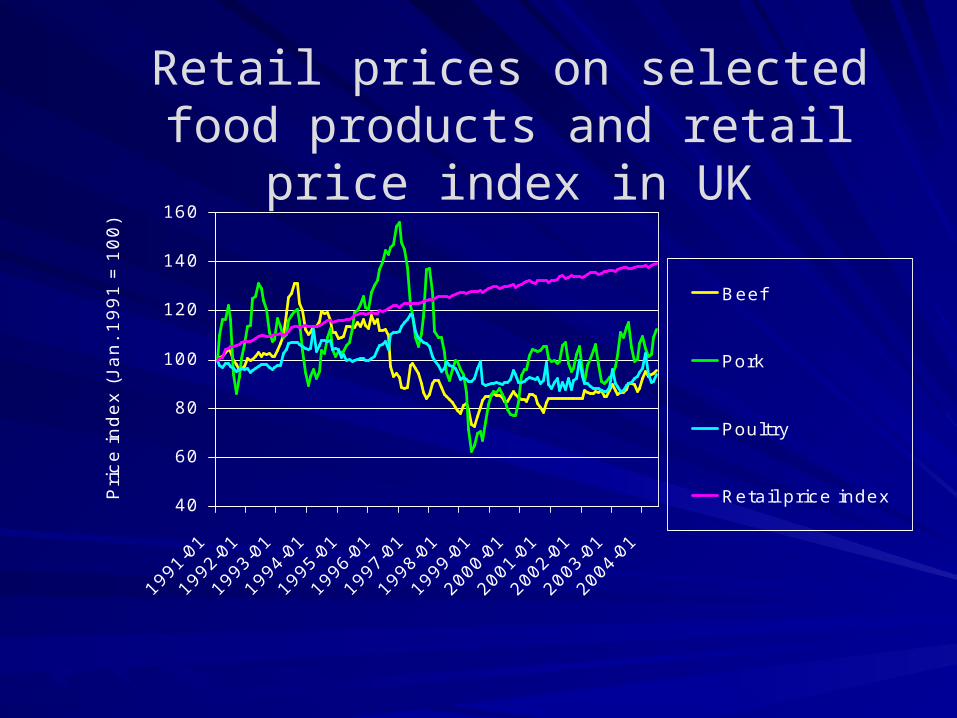

Retail prices on selected food products and retail price index

in UK

40

60

80

100

120

140

160

Pri

ce

in

de

x (

Ja

n. 1

99

1 =

10

0)

Beef

Pork

Poultry

Retail price index

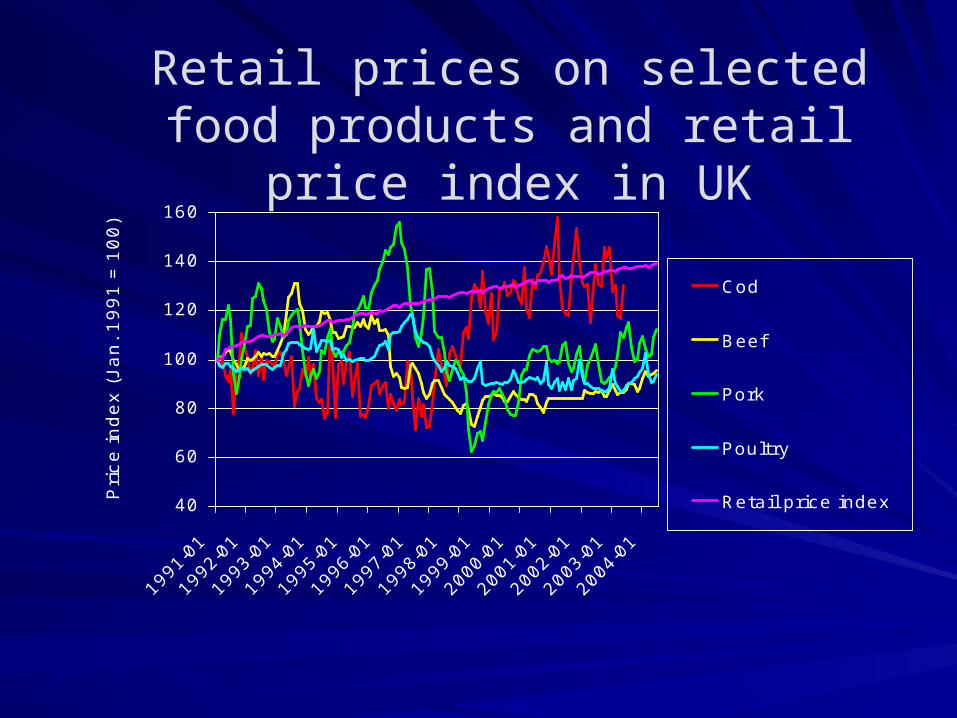

Retail prices on selected food products and retail price index

in UK

40

60

80

100

120

140

160

Pri

ce

in

de

x (

Ja

n. 1

99

1 =

10

0)

Cod

Beef

Pork

Poultry

Retail price index

Retail prices on selected food products and retail price index

in UK

40

60

80

100

120

140

160

1991-0

1

1992-0

1

1993-0

1

1994-0

1

1995-0

1

1996-0

1

1997-0

1

1998-0

1

1999-0

1

2000-0

1

2001-0

1

2002-0

1

2003-0

1

2004-0

1

Pri

ce

in

de

x (

Ja

n. 1

99

1 =

10

0)

Cod

Beef

Pork

Poultry

Salmon

Retail price index

The salmon companies

Salmoncompanies

Often vertically integrated farming-processing-distributionLargest companies have yet not exploited coordination and scale economies fullyHigh variability in profitability across companiesBut have set the standard for supply of seafood in several areas:– Volume, timing and prices

– Availability of fresh fish to consumers

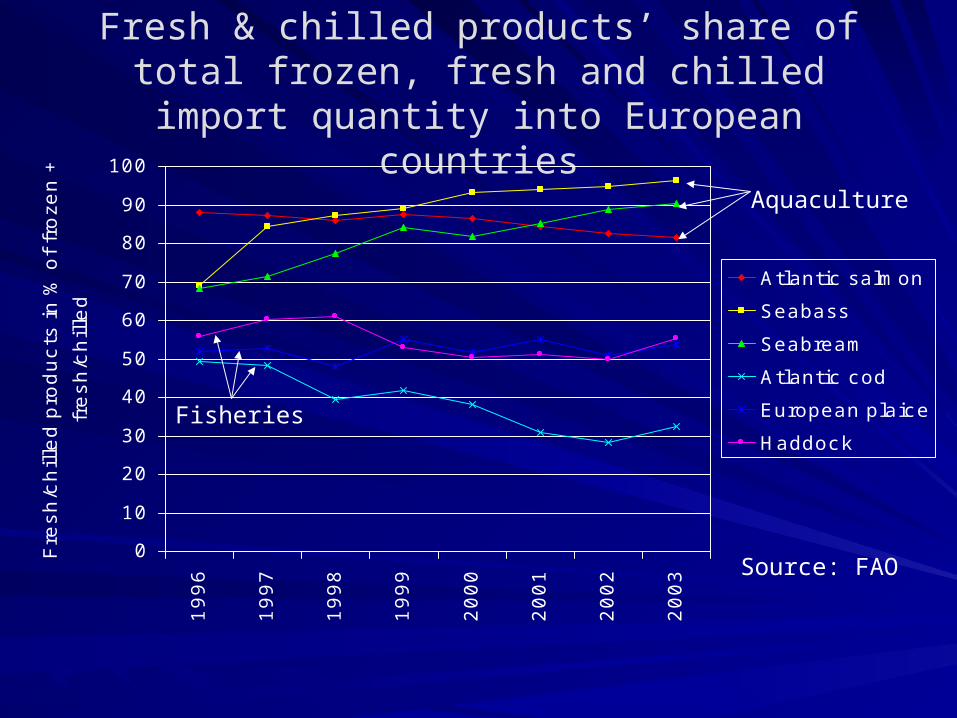

Fresh & chilled products’ share of total frozen, fresh and chilled import quantity into

European countries

0

10

20

30

40

50

60

70

80

90

100

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

Fre

sh

/ch

ille

d p

rod

uc

ts in

% o

f fr

oze

n +

fre

sh

/ch

ille

d Atlantic salmon

Seabass

Seabream

Atlantic cod

European plaice

Haddock

Source: FAO

Aquaculture

Fisheries

The salmon companies

Salmoncompanies

Is the ‘one-species’ strategy viable?When will they include significant volumes of other species?How will the salmon sector deal with increased scarcity of fish meal and oil?

The new players – large seafood companies

Sales 500 mill. to 1.2 billion USDExpanding rapidlyMoving downstream in value chainsSupply a broad range of species and products

Large seafoodcompanies

The new players – large seafood companies

Try to copy some of the strategies of leading food companies– Global sourcing of seafood– Adaptation to retailer

requirements (product range, volumes, regularity, etc.)

– Market intelligence– Economies of scope in

purchasing, processing and distribution

– Invest in brands

Large seafoodcompanies

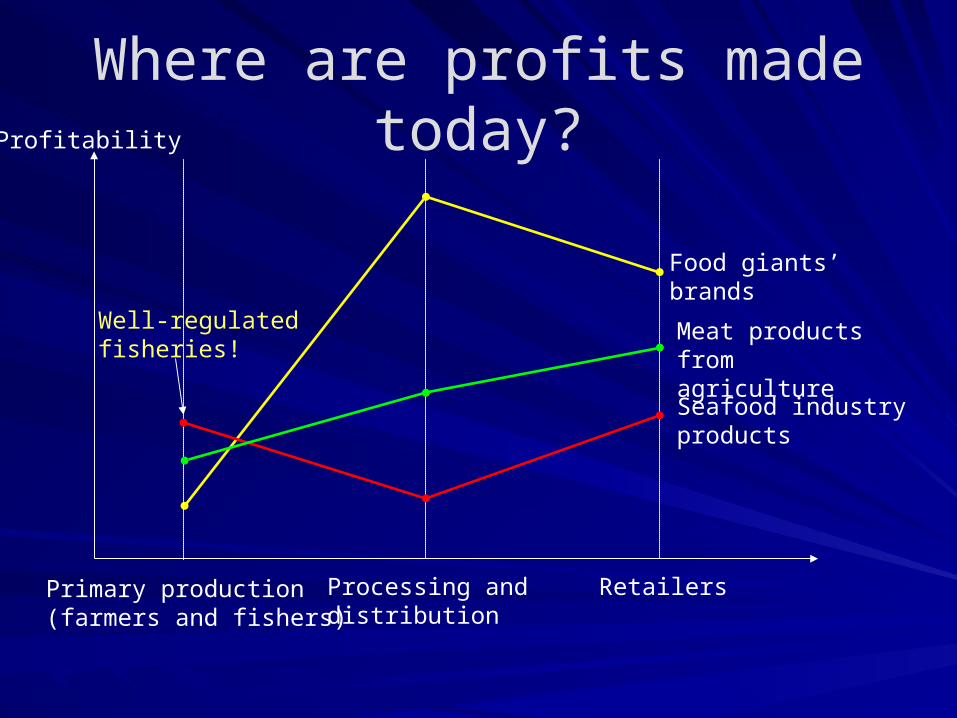

Where are profits made today?

Primary production(farmers and fishers)

Processing anddistribution

Retailers

Profitability

Food giants’ brands

Meat products fromagriculture

Seafood industryproducts

Well-regulatedfisheries!

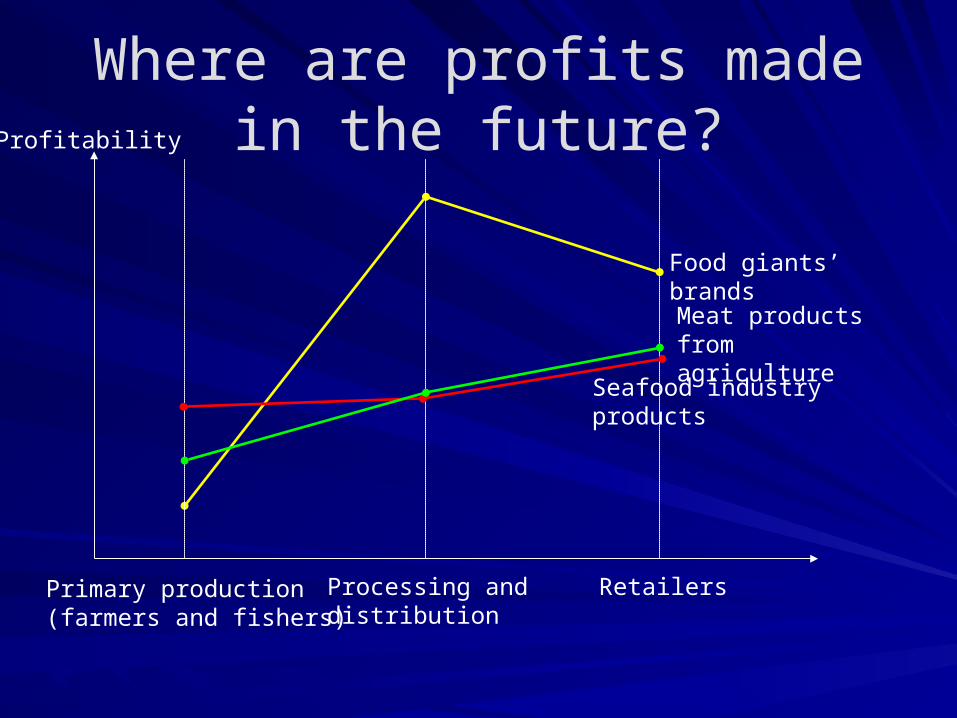

Where are profits made in the future?

Primary production(farmers and fishers)

Processing anddistribution

Retailers

Profitability

Food giants’ brands

Meat products fromagriculture

Seafood industryproducts

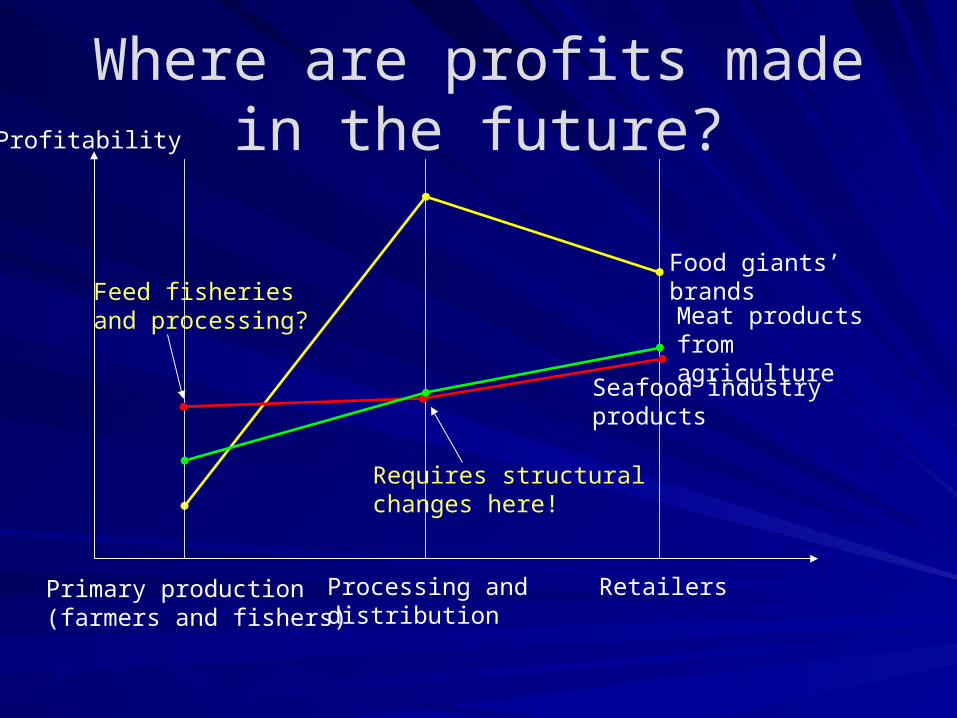

Where are profits made in the future?

Primary production(farmers and fishers)

Processing anddistribution

Retailers

Profitability

Food giants’ brands

Meat products fromagriculture

Seafood industryproducts

Requires structuralchanges here!

Feed fisheriesand processing?

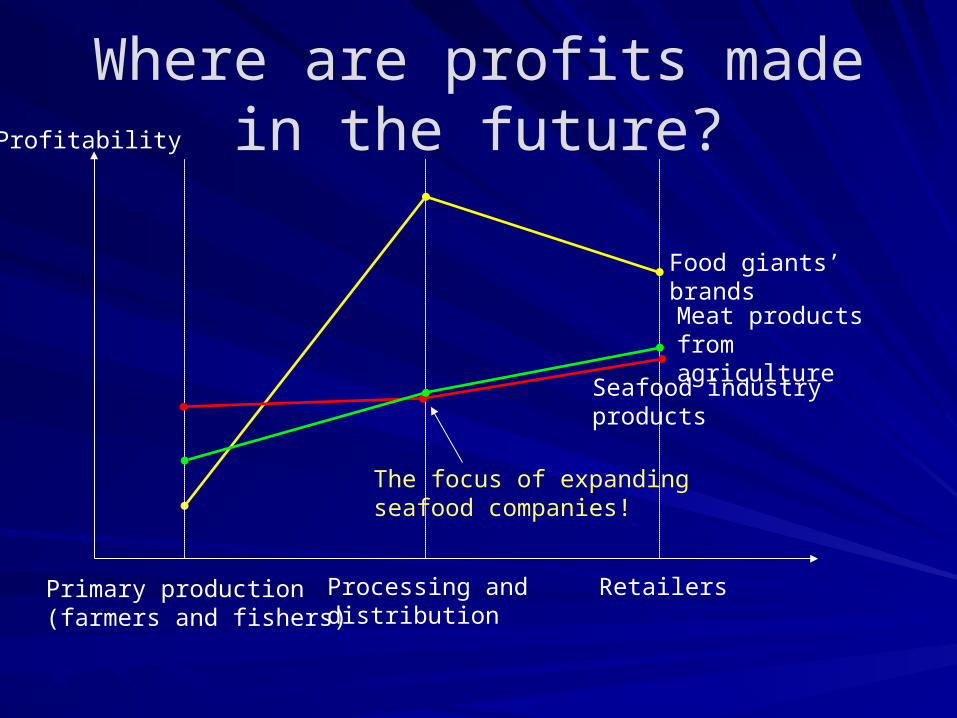

Where are profits made in the future?

Primary production(farmers and fishers)

Processing anddistribution

Retailers

Profitability

Food giants’ brands

Meat products fromagriculture

Seafood industryproducts

The focus of expandingseafood companies!

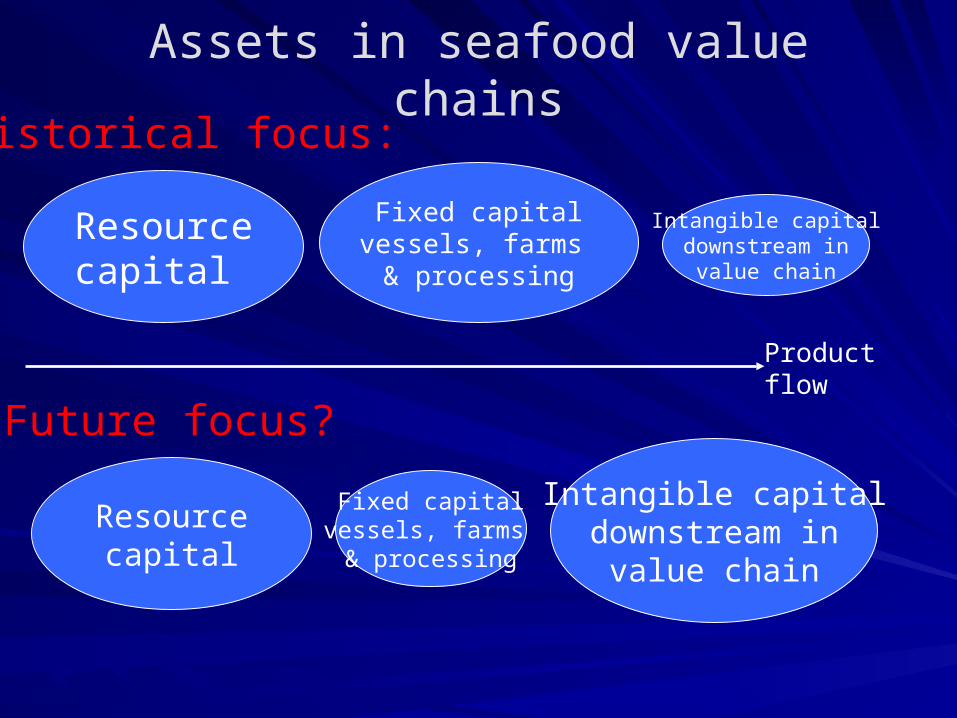

The seafood industry has so far largely ignored

The traditional seafood industry has so far largely ignored the importance of investments in downstream activities – Knowledge on consumers and buyers– Product development– Branding and promotion– Distribution systems– Relationships with buyers

Most of these investments are in intangible assets

Assets in seafood value chains

Resourcecapital

Fixed capitalvessels, farms & processing

Intangible capitaldownstream in

value chain

Historical focus:

Resourcecapital

Fixed capitalvessels, farms & processing

Intangible capitaldownstream in

value chain

Future focus?

Productflow

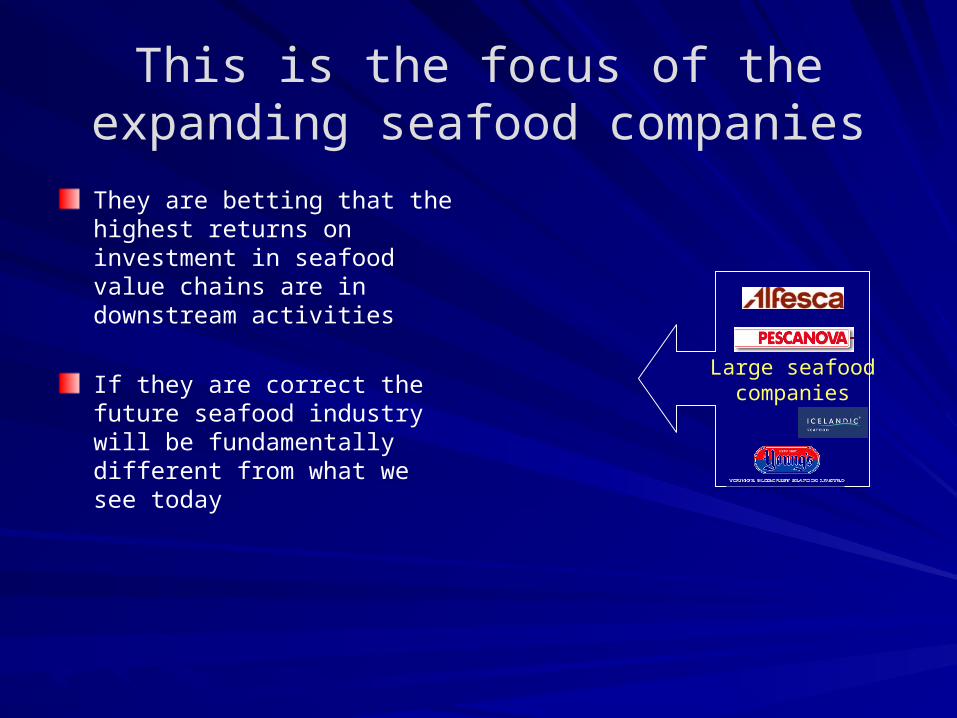

This is the focus of the expanding seafood companies

They are betting that the highest returns on investment in seafood value chains are in downstream activities

If they are correct the future seafood industry will be fundamentally different from what we see today

Large seafoodcompanies

But the growth of the seafood sector, particularly

aquaculture, has not gone unnoticed...

Global seafood industry is subject to increased scrutiny

Growth and success increase visibility

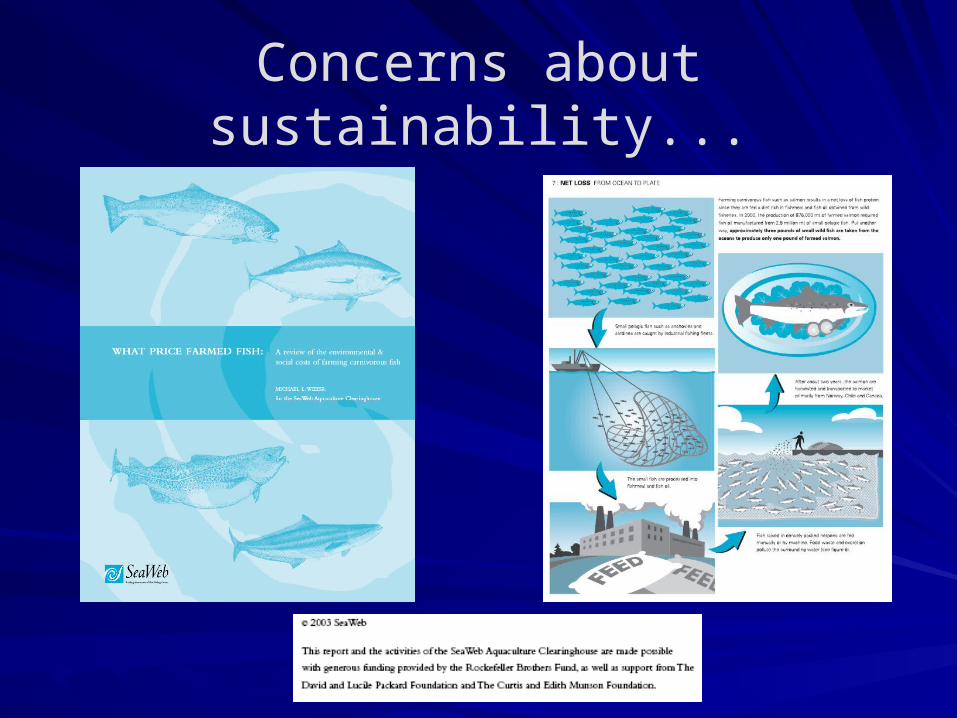

Focus on sustainability and food safety

Aquaculture products are being undermined by adverse criticism on sustainability

Concerns about sustainability...

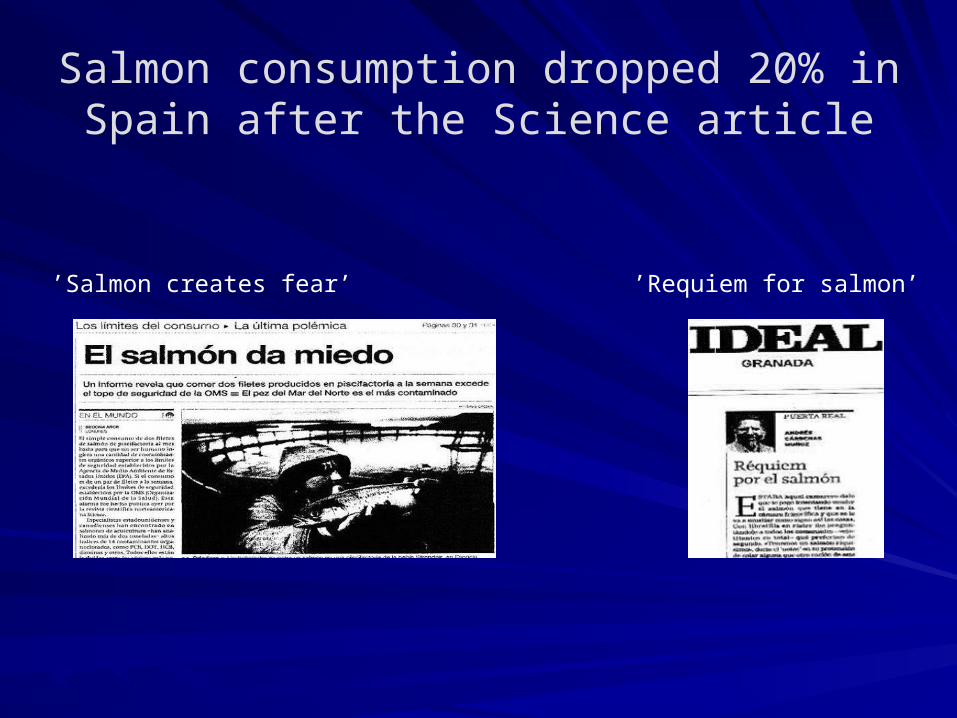

Salmon consumption dropped 20% in Spain after the Science article

’Requiem for salmon’’Salmon creates fear’

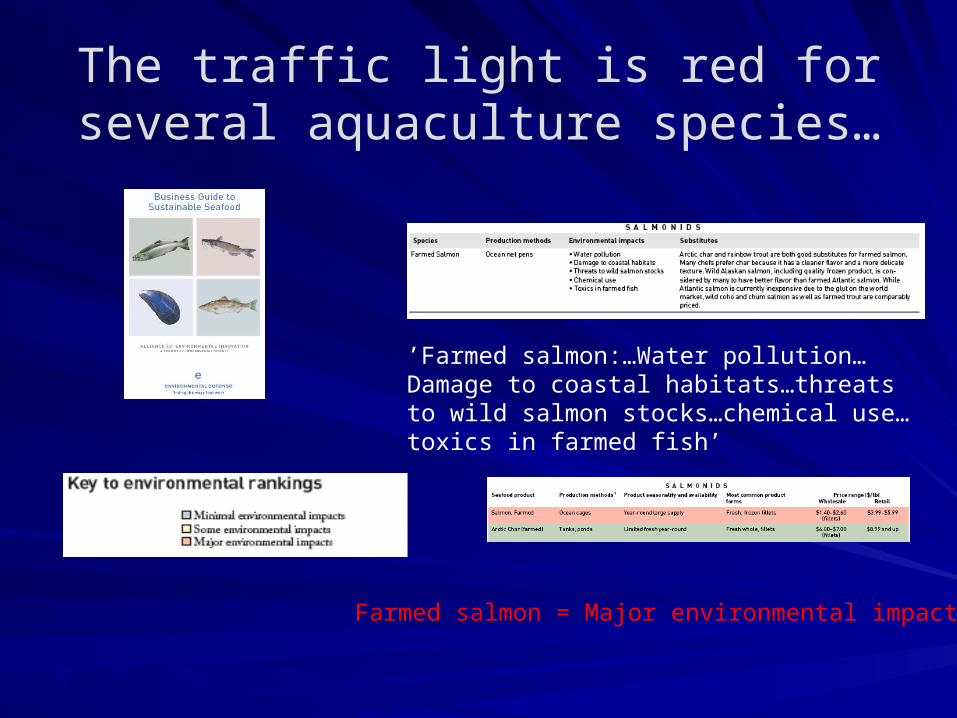

The traffic light is red for several aquaculture species…

Farmed salmon = Major environmental impact!

’Farmed salmon:…Water pollution…Damage to coastal habitats…threats to wild salmon stocks…chemical use…toxics in farmed fish’

Sustainability and food safety - major risks

Sustainability and food safety are major strategic risks for industrialized aquaculture

The aquaculture industry, both feed producers and fish farmers, have to manage these risks

A more consolidated industry will together with other stakeholders (NGOs and final buyers) be able to exercise increased pressure on parts of the industry that do not perform according to their standards

Where is the fish meal and oil industry in this picture?

The industry supplies feed inputs that will only become more scarce in the futureHow high prices will go depends on:– Rate of growth for species that use fish meal & oil

intensively – depends on consumers’ willingness-to-pay

– Omega-3 trends– Effect of innovations on substitution possibilities with

vegetable alternatives– The perceived sustainability and food safety of

seafood with high fish meal & oil inclusion rates

Concluding remarks

Fish meal and oil are valuable assets, not only due to a limited global supply, but also because of the health benefits they bring to consumers

But buyers of fishmeal and fish oil for the aquaculture sector, both in developed and developing countries, face challenges from markets in North America, EU and other rich countries

By forming strategic alliances with buyers and other stakeholders in the aquaculture sector to deal with issues of concern, whether real or perceived, the fish meal & oil industry adds value and reduce risk for buyers...

... and at the same time adds value and reduces risk for itself