THE FUNDAMENTALS OF CREDIT Mr. Calkins Spring 2008.

24

THE FUNDAMENTALS OF CREDIT Mr. Calkins Spring 2008

-

Upload

rylie-badgley -

Category

Documents

-

view

224 -

download

3

Transcript of THE FUNDAMENTALS OF CREDIT Mr. Calkins Spring 2008.

THE FUNDAMENTALS OF CREDIT

Mr. Calkins

Spring 2008

THE FUNDAMENTALS OF CREDIT

• WHAT CREDIT IS– Credit is the privilege of using someone else’s

money for a period of time. That privilege is based on the belief that the person receiving credit will honor a promise to repay the amount owed at a future date.

THE FUNDAMENTALS OF CREDIT

• TYPES OF CREDIT– If you borrow money to be used for some

special purpose, you are using loan credit– If you charge a purchase at the time you buy

the good or service, you are using sales credit– Trade credit is used by a business when it

receives goods from a wholesaler and pays for them at a later specified date

THE FUNDAMENTALS OF CREDIT

• USERS OF CREDIT– If you as a typical American consumer, you

will use credit for many purposes. You may use credit to buy fairly expensive products that will last for a long time, such as a car, house, or major appliance. Or you may use credit for convenience in making smaller purchases, such as meals and CDs. Paying for medical care, vacations, taxes, and even paying off other debts are other common uses of credit.

THE FUNDAMENTALS OF CREDIT

• GRANTING OF CREDIT– Credit Information– The Tree Cs of Credit

THE FUNDAMENTALS OF CREDIT

• CREDIT INFORMATION– the business that is considering you as a

credit risk will generally ask you about your financial situation and request credit references.

THE FUNDAMENTALS OF CREDIT

• THE THREE Cs of CREDIT– Character- refers to your honesty and

willingness to pay a debt when it is due– Capacity- refers to your ability to pay a debt

when it is due– Capital- is the value of the borrower’s

possessions

THE FUNDAMENTALS OF CREDIT

• BENEFITS OF CREDIT TO BUSINESSES– Businesses benefit in several ways. By being

allowed to buy on credit, customers will tend to purchase more, and the business will increase its profits. If the business buys its merchandise using trade credit, the merchandise can be paid for after it has been sold to customers.

THE FUNDAMENTALS OF CREDIT• BENEFITS OF CREDIT TO CUSTOMERS

– Ways in which consumers benefit from their use of credit:• Convenience- credit can make it convenient for you to

buy. There may be times when you do not have enough cash and have a need for something.

• Immediate possession- credit allows you t o have immediate possession of the item that you want.

• Savings- Credit allows you to buy an item when it goes on sale, possibly at a much lower price.

• Credit rating- if you buy on credit and pay your bills when they are due, you gain a reputation for being dependable

• Useful in an emergence- access to credit can help you in an emergence. Having an oil company credit card, for example, can come in handy when you run out of gas and cash at the same time

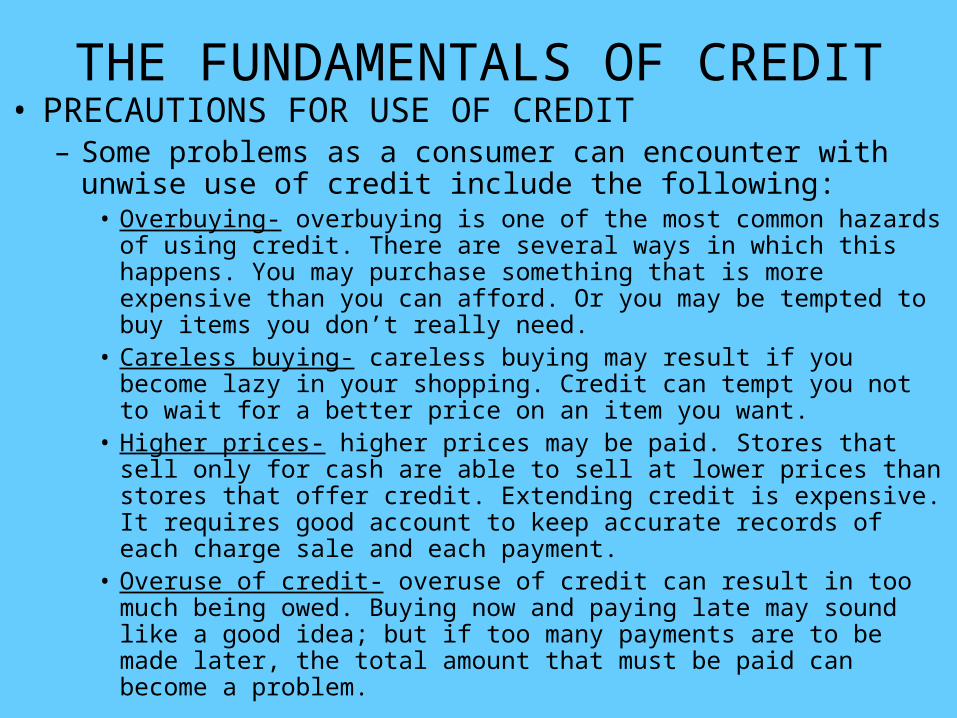

THE FUNDAMENTALS OF CREDIT• PRECAUTIONS FOR USE OF CREDIT

– Some problems as a consumer can encounter with unwise use of credit include the following:

• Overbuying- overbuying is one of the most common hazards of using credit. There are several ways in which this happens. You may purchase something that is more expensive than you can afford. Or you may be tempted to buy items you don’t really need.

• Careless buying- careless buying may result if you become lazy in your shopping. Credit can tempt you not to wait for a better price on an item you want.

• Higher prices- higher prices may be paid. Stores that sell only for cash are able to sell at lower prices than stores that offer credit. Extending credit is expensive. It requires good account to keep accurate records of each charge sale and each payment.

• Overuse of credit- overuse of credit can result in too much being owed. Buying now and paying late may sound like a good idea; but if too many payments are to be made later, the total amount that must be paid can become a problem.

THE FUNDAMENTALS OF CREDIT

• QUESTIONS TO ASK– Before making a final decision whether to buy on

credit, there are some questions you as a consumer should ask:

• How am I benefiting from this use of credit?• Is this the best buy I can make or should I shop around

some more?• What will be the total cost of my purchase, including the

cost of charging the item?• What would I save if I paid cash?• Will the payments be too high considering my income?

THE FUNDAMENTALS OF CREDIT

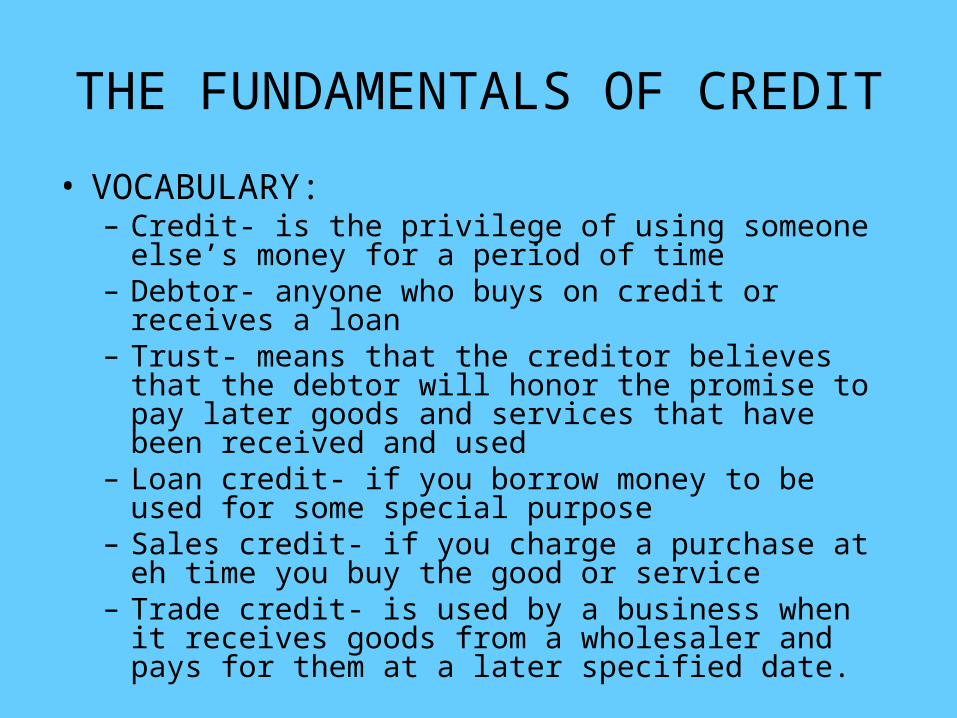

• VOCABULARY:– Credit- is the privilege of using someone else’s money

for a period of time– Debtor- anyone who buys on credit or receives a loan– Trust- means that the creditor believes that the debtor

will honor the promise to pay later goods and services that have been received and used

– Loan credit- if you borrow money to be used for some special purpose

– Sales credit- if you charge a purchase at eh time you buy the good or service

– Trade credit- is used by a business when it receives goods from a wholesaler and pays for them at a later specified date.

THE FUNDAMENTALS OF CREDIT

• VOCABULARY Continued…– Credit references- are businesses or individuals from

whom you have received credit in the past and/or who can help verify your credit record

– Character- refers to your honesty and willingness to pay a debt when it is due

– Capacity- refers to your ability to pay a debt when it is due

– Capital- is the value of the borrower’s possessions– Credit rating- if you buy on credit and pay your bills

when they are due, you gain a reputation for being dependable. In that way, you establish a favorable credit rating.

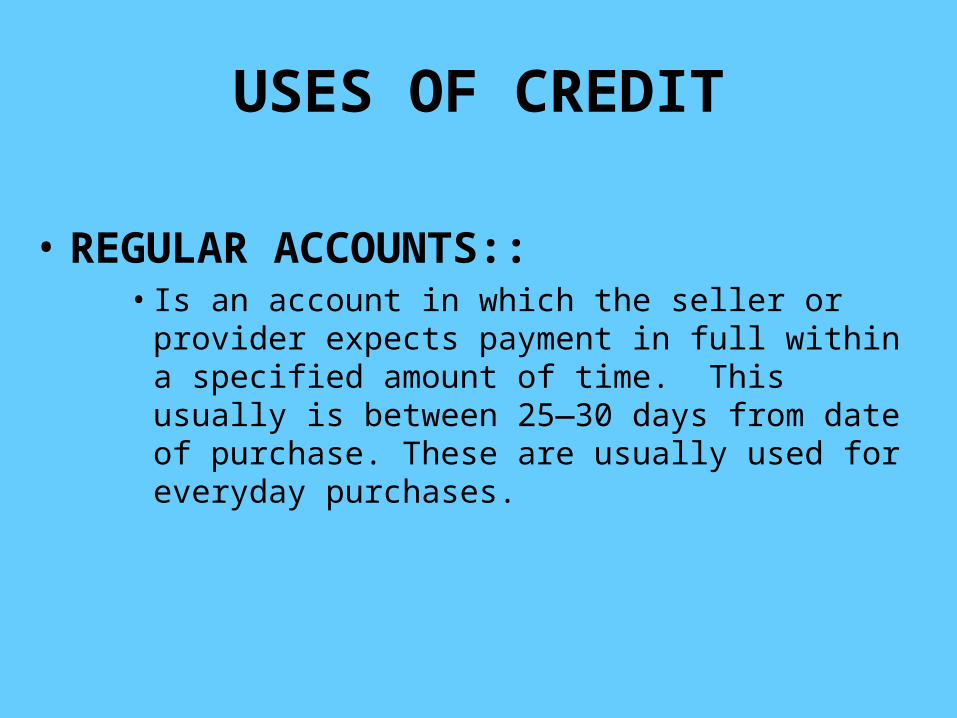

USES OF CREDIT

• TYPES OF CHARGE ACCOUNTS• REGULAR ACCOUNTS• BUDGET ACCOUNTS• REVOLVING ACCOUNTS

USES OF CREDIT

• REGULAR ACCOUNTS::• Is an account in which the seller or provider expects

payment in full within a specified amount of time. This usually is between 25—30 days from date of purchase. These are usually used for everyday purchases.

USES OF CREDIT

• BUDGET ACCOUNTS::• Are accounts that payments of a certain amount be

made over several months. A budget plan offered in many businesses is the 90—day three payment plan. This is the most common one seen payments made in three equal sums.

USES OF CREDIT

• REVOLVING ACCOUNT::• Are purchases that can charged at any time but only

part of the debt need be paid each month. There is usually a maximum amount which is owed at one particular time. A monthly payment is required. A finance charge is included to use this type of credit.

USES OF CREDIT

• HOW/WHAT CREDIT CARDS USED::• BANK CARDS• TRAVEL & ENTERTAINMENT PURPOSES• OIL COMPANY CARDS• RETAIL STORE CARDS

USES OF CREDIT

• HOW/WHAT CREDIT CARDS USED::• BANK CARDS—These have become quite

popular over the past several years the most common used are VISA and Mastercard. There is usually an annual fee for the privelege of using these cards.

USES OF CREDIT

• HOW/WHAT CREDIT CARDS USED::• TRAVEL & ENTERTAIMENT—Carte

Blance, Diners Club and American Express are the most widely used entertainment credit cards. A yearly membership fee is charged for use of these credit cards and it is higher than the annual fee charge by bank cards. These are used for motels, hotels, restaraunts etc.

USES OF CREDIT

• HOW/WHAT CREDIT CARDS USED::• OIL COMPANY CARDS—such as

Texaco, Chevron, Shell and Stinker Stations issue their own unique credit cards. Many oil companies that it costs them way too much to offer credit. So they have left that to credit card companies which is their specialties.

USES OF CREDIT

• HOW/WHAT CREDIT CARDS USED::• RETAIL STORE CARDS—many retail

stores are now carrying their own cards. They carry the name of the department or retail store involved. These are usually very high interest and are referred to as the “single-purpose” credit cards.

USES OF CREDIT• CONSUMER LOANS

• INSTALLMENT LOANS—is one in which you agree to make a certain amount of monthly payment.

• SINGLE PAYMENT LOANS—you don’t pay anything until the end of the loan period.

• PROMISSORY NOTE—is a written promise to pay based on the “debtor’s” excellent credit reating.

• COLLATERAL—is a security deposit. Something of value is put against the loan so in the event it isn’t repaid the company can acquire the property.

• SECURED LOAN—is simply some type of property that is put up against the loan.

• COSIGNER—is someone who signs on additionally to a loan and promises to pay if the person who is first on the loan does not.