STATEMENT OF Congressional Budget Office Committee on the Budget

The Foundations of the

Congressional Budget

Office

Barry AndersonOECD

Meeting of OECD Parliamentary Budget Officials

Rome, February 26-27, 2009

1

Outline

• A Note About Me

• Origins of CBO

• CBO’s Potential Value

• Fundamental Characteristics of CBO

• Additional Characteristics

• CBO’s Core Functions

• CBO’s Other Functions

• A Few Significant Events in CBO’s Past

• Implications of CBO for Other Countries

2

A Note About Me:

Experience in Both

the US Congress & the White House (as well as in IMF & OECD)

3

Office of Management & BudgetGeneral Accounting Office

Congressional Budget Office

ORIGINS OF CBO

• Budgetary Dominance of President Nixon

• Other Factors• Budgetary Weakness of Congress

4

Budgetary Dominance of

President Nixon

• Impoundment• Creation of a More Powerful

OMB• Monopoly on Budget

Information

5

Other Factors

• Deficits without War or Recession

• Complexity• Long Term Perspective• Gimmicks

6

Budgetary Weakness of

Congress

• No Budget Process• Creation of Budget

Committees• Separation of Powers: CBO vs.

OMB• Precedents of GAO, CRS, OTA

7

One Early View of CBO:

Like A Sewer

―What the House wanted [when CBO was created] was

basically a manhole in which Congress would have a billor something and it would lift up the manhole cover andput the bill down it, and 20 minutes later a piece of paperwould be handed up, with the cost estimate, the answer,on it. No visibility, [just] some kind of mechanism downbelow the ground level doing this...non-controversial[work], the way the sewer system [does].‖

8

CBO’s POTENTIAL VALUE

• Eliminate Executive’s Information Monopoly

• Simplifies Complexity

• Promotes Transparency

• Enhances Credibility

• Promotes Accountability

• Improves Budget Process

• Serves Both Majority & Minority

• Provides Rapid Responses9

CBO’s Value Changed

• CBO’s Value at its Creation in 1975

– More Information for the Congress relative to the President

• CBO’s Value Beginning About 1980

– More Information for the Minority Party relative to Majority

10

FUNDAMENTAL

CHARACTERISTICS of CBO

• Nonpartisan (not Bipartisan)– Directors have been more technical than political

– Staff has been technical

– A strong esprit de corps has developed

• Independent

• Objective

• Informed

• Serve Both Majority & Minority

• Transparent (Everything on the Internet)

• Understandable (Subway test)

11

ADDITIONAL CHARACTERISTICS

• Put core functions in law

• CBO does not make recommendations; GAO does

• Serve Committees, not Members

• Meet with anyone, but strive for balance

• Is physically separate from legislature

• Avoid limelight

• Is responsive and timely

12

Characteristics of a

Good CBO Director

• Most importantly: unbiased

– A good start: takes a position contrary to those who supported him

• Avoid recommendations, but if you make them, do them orally, not in writing

• Be willing to take on unpopular issues

– This can help Members by giving them an excuse not to take on the issues themselves

• Establish a rapport with Budget Committee Chairmen

– Talk with Members, not to them

– Brief Members first, especially if news is bad

• Avoid the limelight

• Avoid the perks of power 13

CBO’s CORE FUNCTIONS

I. Economic Forecasts

II. Baseline Estimates

III.Analysis of President’s Budget Proposals

IV. Medium Term Analysis

14

I: Economic Forecasts

• Objective– Not a function of policy proposals - not ―dynamic‖

– Not based on wishful thinking - no rosy scenario

– Not a means to an end - for example, interest rates, & oil & crop prices are forecasts, not targets

• Conservative - allows for better-than-forecasted performance to reduce deficits/debt

• “Centrist”, based on:– Panel of experts

– Private forecasters

– The Fed

15

II: Baseline Estimates

• Projections, not Predictions

• ―Centrist‖ Economic Forecast

• Current Law Basis, including

– ―Spend Out‖ of Enacted Legislation

– Termination of Expiring Legislation

• Medium Term Focus

• Replaces Previous Year & Executive Baselines

16

III: Analysis Of President’s Budget

Proposals

• An objective budgetary assessment

– A technical review - not a programmatic evaluation

• Enhances credibility – both of government as a whole and of the President’s forecasts

17

IV: Medium Term Analysis

• Forces government to look beyond one year

• Estimates medium term economic and fiscal impacts of policy proposals

• Important to take account of Fiscal Risks:– Guarantees

– Pension liabilities

– Contingent liabilities

– PPPs

• Provides basis for Long-Term Analysis18

CBO’s OTHER FUNCTIONS

• Analysis of proposals

• Options for spending cuts

• Analysis of mandates (regulatory analysis)

• Economic analyses

• Tax analyses

• Long term analysis

• Policy briefs

19

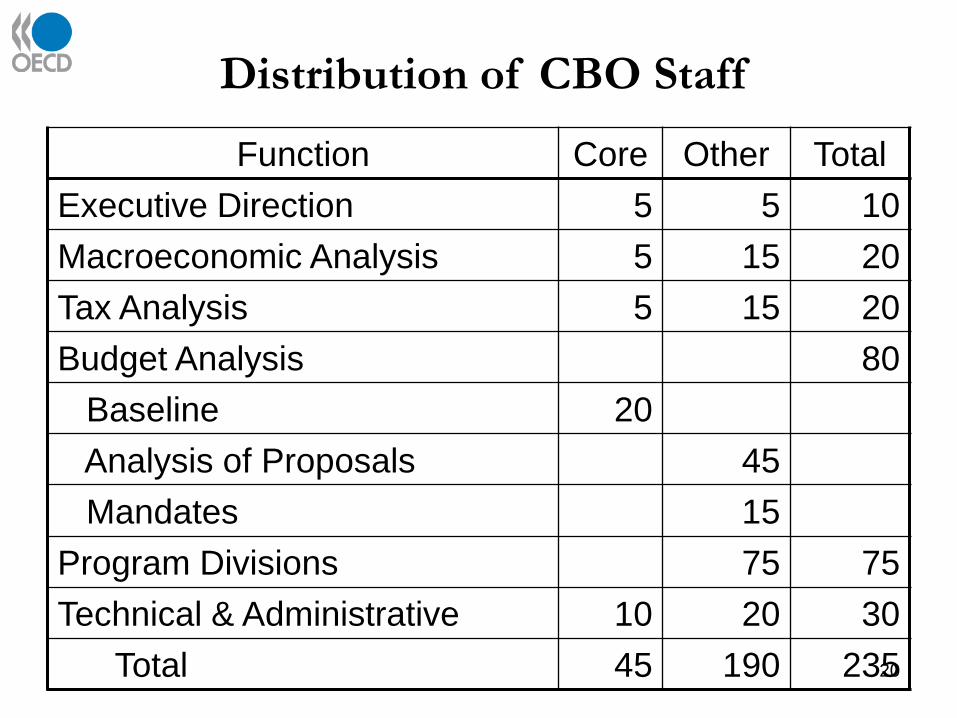

Function Core Other Total

Executive Direction 5 5 10

Macroeconomic Analysis 5 15 20

Tax Analysis 5 15 20

Budget Analysis 80

Baseline 20

Analysis of Proposals 45

Mandates 15

Program Divisions 75 75

Technical & Administrative 10 20 30

Total 45 190 23520

Distribution of CBO Staff

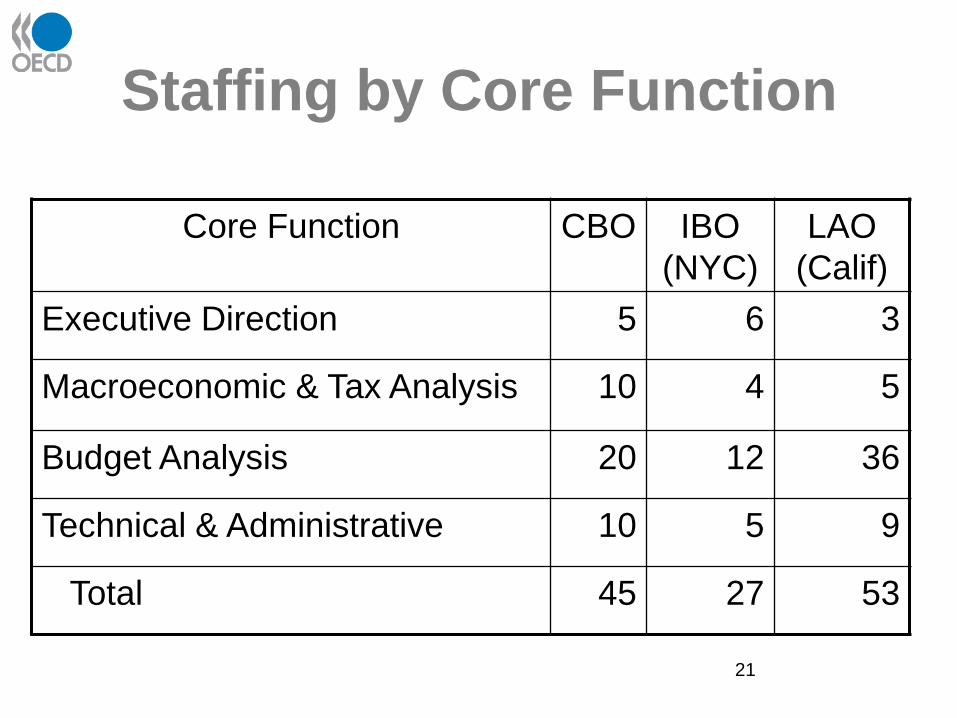

Staffing by Core Function

21

Core Function CBO IBO

(NYC)

LAO

(Calif)

Executive Direction 5 6 3

Macroeconomic & Tax Analysis 10 4 5

Budget Analysis 20 12 36

Technical & Administrative 10 5 9

Total 45 27 53

A FEW SIGNIFICANT EVENTS IN

CBO’S PAST• 1975: Rivlin establishes CBO’s independence with help of

the Minority Budget Chairman

• 1980: Gramm-Rudman & the Reagan economic assumptions help establish CBO’s objectivity

• 1990: the Budget Enforcement Act enhances CBO’s role

• 1994: Reischauer & Clinton Care—CBO’s finest hour

• 1997: O’Neill (Blum) undoes a deal—CBO’s lowest point

• 2001: Crippen (Anderson)—a $5.6T surplus projection

• 2003: Crippen (Anderson)—a $2.4T deficit projection

• 2003: Holtz-Eakin takes a stand against dynamic scoring

• 2009: New CBO Director Elmendorf estimates that only 20% of the stimulus would impact 2009

22

IMPLICATIONS of CBO for

OTHER COUNTRIES• Legislatures need an independent source of

information and analysis to improve theirparticipation in budget preparation.

• A nonpartisan, independent, objectiveanalytic unit such as CBO can providetransparent, clear, & accurate informationwithout polarizing relations betweenexecutive and legislature.

• Successful creation of such a unit is noteasy: in particular, it demands balance in apolitical environment.

23

Acronyms Used in This

Presentation• CBO: Congressional Budget Office

• CRS: Congressional Research Service

• Fed: The Federal Reserve Board

• GAO: Government Accountability Office

• IBO (NYC): New York City’s Independent Budget Office

• IMF: International Monetary Fund

• LAO (Calif): California’s Legislative Analysts Office

• OECD: Organization for Economic Cooperation and Development

• OMB: Office of Management and Budget

• OTA: Office of Technology Assessment

• PPPs: Public-Private Partnerships24