The Forestry Debate – Where are we? Dr Julian Amos 24 February 2012.

52

The Forestry Debate – Where are we? r Julian Amos 24 February 20

-

Upload

aron-harper -

Category

Documents

-

view

217 -

download

0

Transcript of The Forestry Debate – Where are we? Dr Julian Amos 24 February 2012.

The Forestry Debate – Where are we?

Dr Julian Amos 24 February 2012

The Present Round

OUTLINE

Land Tenure

Wood Supply

More Reserves?Other Options

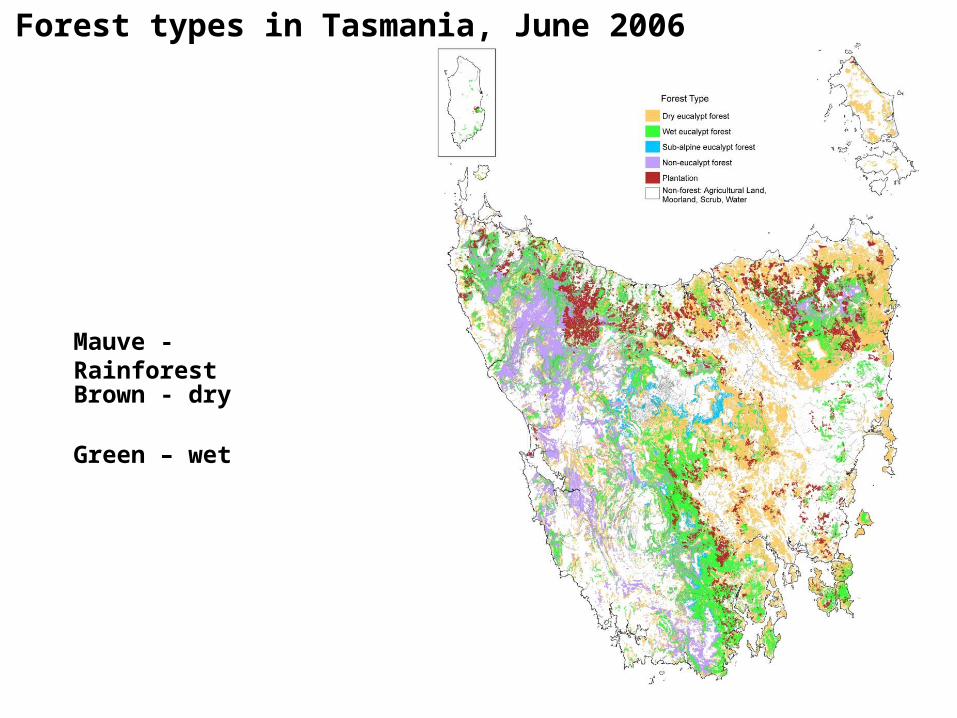

Forest types in Tasmania, June 2006

Brown - dry

Mauve - Rainforest

Green – wet

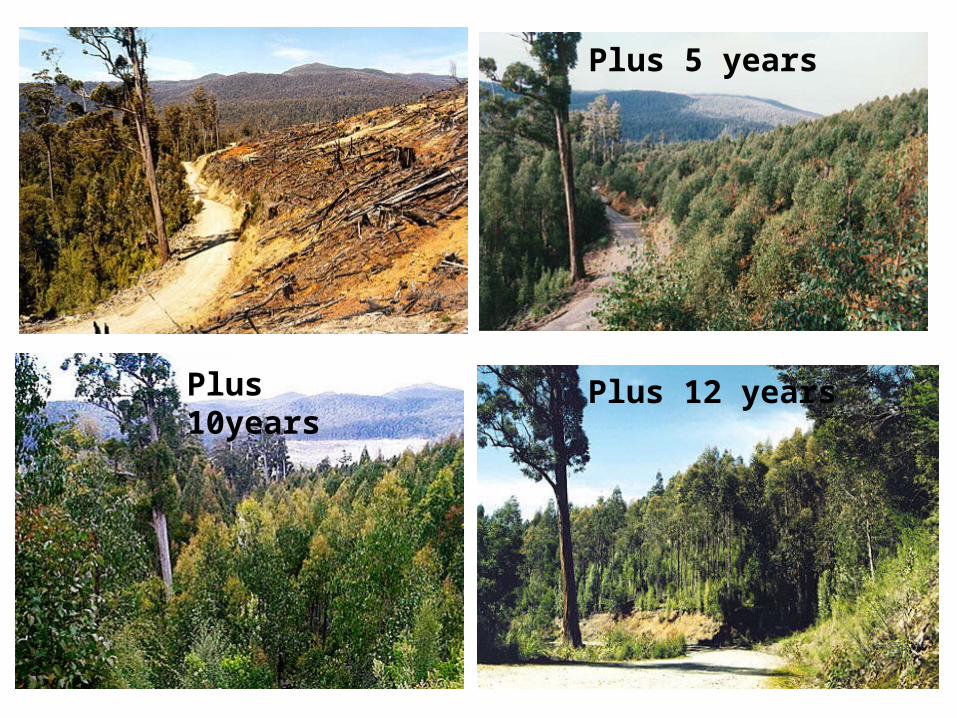

But what they don’t show you…

Clearfelling – Industrial logging???

What they do show you…

Plus 5 years

Plus 10 years

Plus 12 years

Plus 10years

Plus 5 years

Plus 12 years

Reserves - pre 1981

Less than 600,000 ha

Reserves – 1982post GbF

Reserves – 1992post Helsham

Arthur Pieman Conservation Area

Now 2.3 million ha

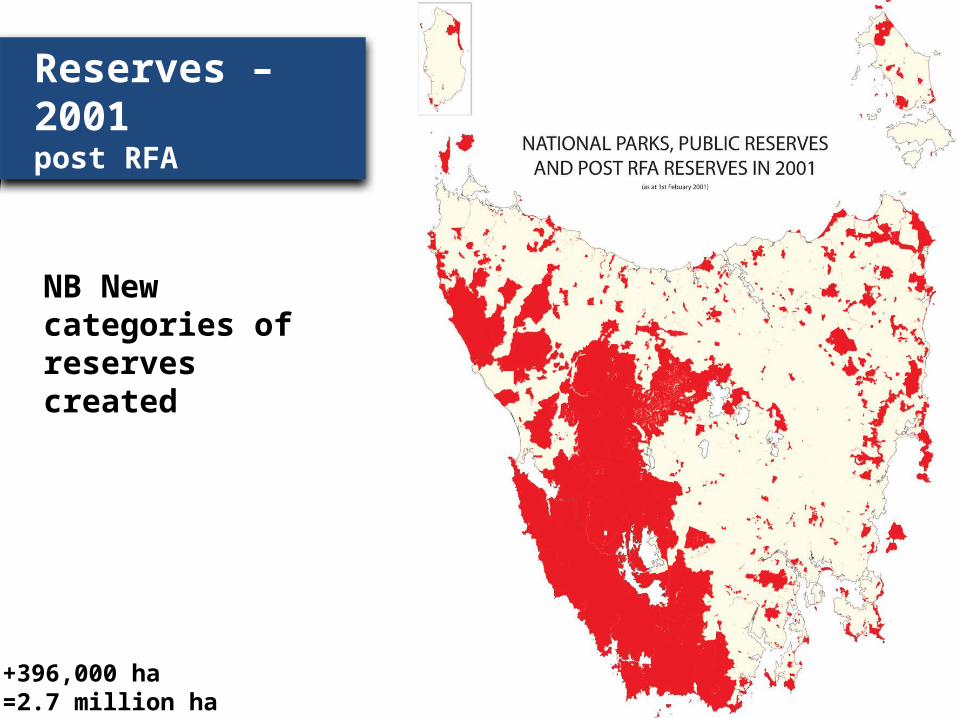

Reserves – 2001post RFA

NB New categories of reserves created

+396,000 ha=2.7 million ha

Reserves – 2005post TCFA

+170,000 ha=2.9 million ha

Reserves – 2011

The Present Round

OUTLINE

Land Tenure

Wood Supply

More Reserves?Other Options

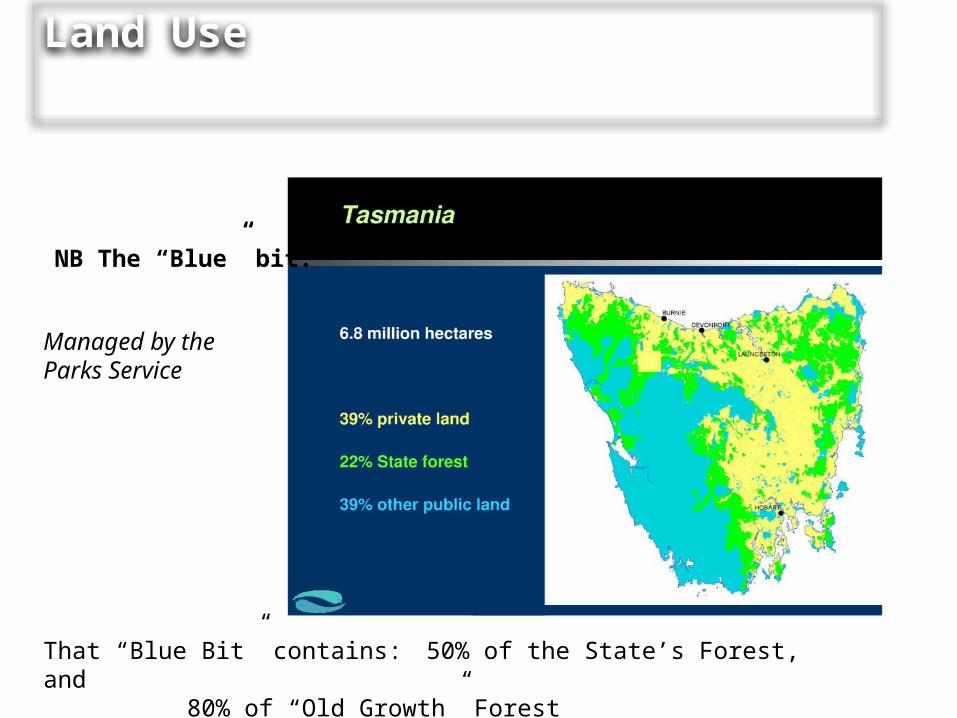

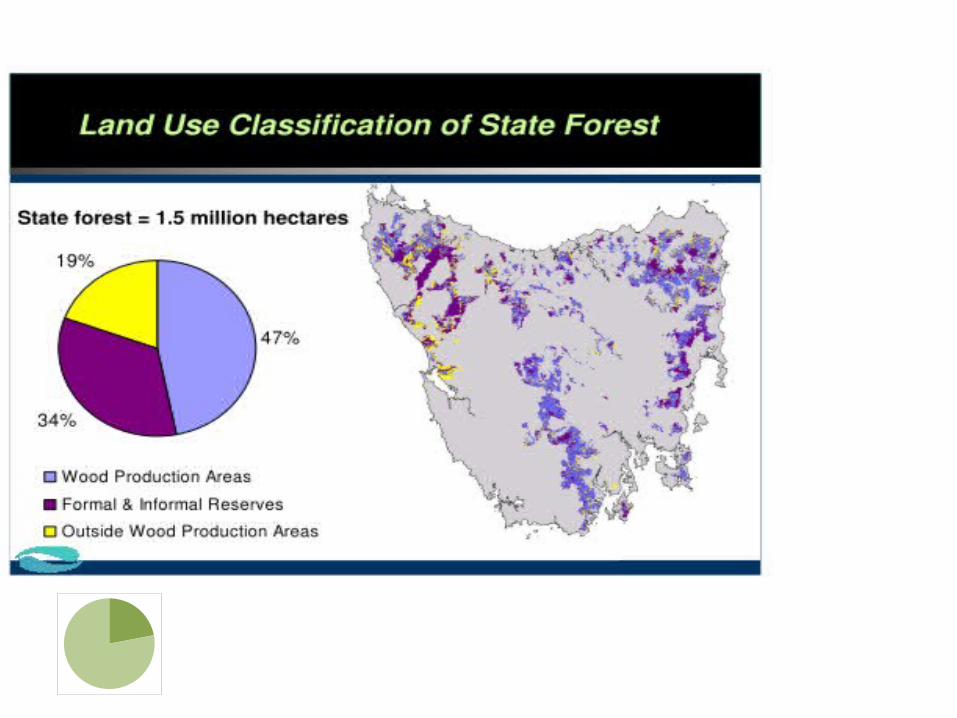

Land Use

NB The “Blue” bit.

That “Blue Bit” contains: 50% of the State’s Forest, and 80% of “Old Growth” Forest

Managed by theParks Service

So, the call to

“Save Tasmania’s Forests”

rings somewhat hollow

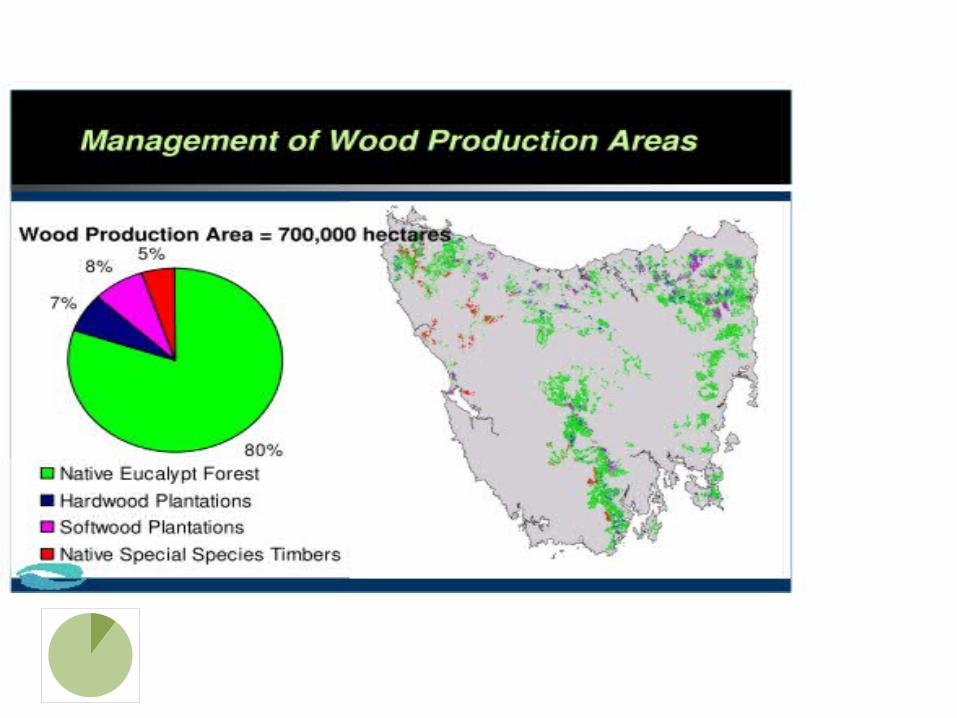

Land Use

Now the “Green” bit.

Remember – it is ONLY50% of all public forest – the other 50% is in the “blue” bit

Managed by Forestry Tasmania

2020

And yet FT had contracts for over 300,000 cub metres per annum!

Predominantly E nitens

2020

Can E nitens do it???

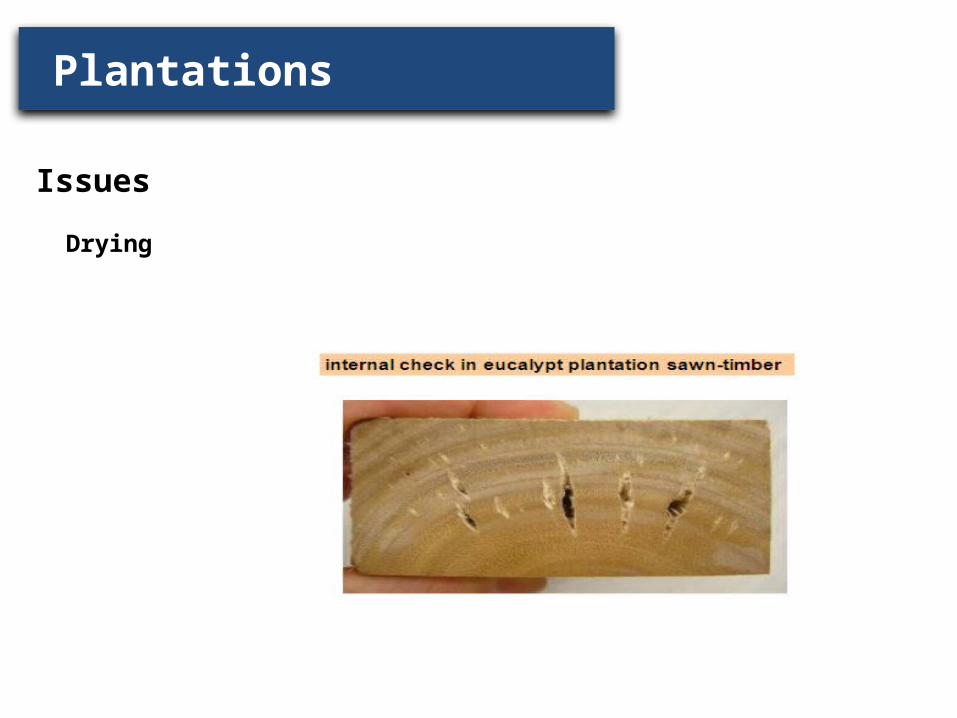

Plantations

• Claimed by green groups to be the answer to supply problems• However:

– 80 to 90% not thinned or pruned• so suitable only for pulpwood and other low grade products

– 10 to 15% is pruned E. nitens• a species unsuitable for solid appearance grade products• E. nitens can be used for engineered products but these products are

expensive to produce in Tasmania – 5% is pruned E. globulus

• if properly managed, is suitable for solid appearance grade products and rotary peeled veneer

Issues

Management

Issues

Drying

Plantations

Plantations

Public and private

Hectarage Public Private

H/wood 53,000 ha 180,000 ha

S/wood 55,000 ha 25,000 ha

The future for private plantations?

Pulp mill?

Issues

Availability

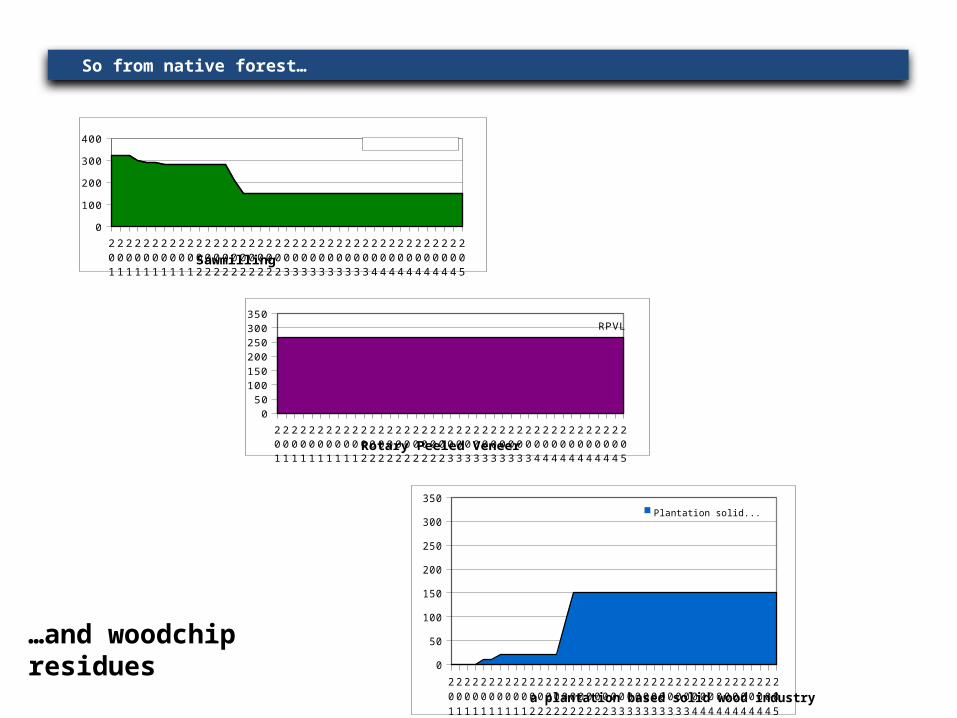

So from native forest…

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

050

100150200250300350

Sawmilling

HQSL Plantatio...

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

0

50

100

150

200

250

300

350RPVL

Rotary Peeled Veneer

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

0

50

100

150

200

250

300

350

a plantation based solid wood industry

Plantation solid wood

…and woodchip residues

The Present Round

OUTLINE

Land Tenure

Wood Supply

More Reserves?Other Options

Since 2010…

The Round Table

The Statement of Principlescompeting claims

guaranteed volumesmore reserved ground

The Kelty Process

The Intergovernmental Agreement2 separate processesinterim -immediate cessation in 430,000 hectares

A Heads of Agreement

An Independent Verification Panel - twice!!!

The Conservation Agreement

permanent-reservation of up to 572,000 hectares

A separate Independent Verification PanelHCV???

The UP TO 572,000 ha earmarked as “HCV”

522,000 ha of State Forest

345,000 ha of production forest177,000 ha of forest reserves

Remember - FT only had 700,000 ha avail for wood production

Reserves - 2011

Approx. 3 million ha

Reserves - 2011 plus proposed new IGA reserves

Proposed new IGA reserves

Plus 572,000 ha=over 3.5 million ha

Reserves - 2013 with state forest

State forest

30 years of reserve growth in Tasmania

And “the Tarkine”?

In 1981…

it didn’t exist.

It first appeared in a TCT document in 1986.

Area presently managedby the Parks Service

(excludes FT’s Forest Reserves)

And it has grown from there…

The current claim:

And with HCV:

Native forest logging stops at 2020

Existing E nitens

An immediate reservation of 572,000 ha of “HCV” Forest - and a full transition out of native forest by 2020

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

0

100

200

300Native forest

Sawmiling - Industry closes

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

050

100150200250300350 Plantation solid wood

Possible development of a new industry

The ENGO view…

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

0

100

200

300 RPVL

Rotary Peeled Veneer

THE ENGO Demand Hectarage

Industry Demand Guaranteed Wood Supply

Are the two in conflict?

The recent bout of protest activity shows that:

The claim for more ground is never-endingThe demand is insatiableThe tactics are deplorableThe level of human suffering is enormous

It is obvious that “peace” is illusory

What’s to be done?

YES

FT have advised they cannot deliver the volumes

The Present Round

OUTLINE

Land Tenure

Wood Supply

More Reserves?Other Options

Next steps?

Future of IGARole of the Signatories (Govts)Role of the ParticipantsRole of the GreensRole of the LegCo

Sanctions Charitable StatusTruth in AdvertisingWorkplace Invasion LegislationTrade Practices Act, ACCC

•conspiracy to incite breach of contract•engaging in activities damaging to trade

and commerce

Reversion to RFA

???

Environmental – what gain, really?

So, what does this all mean for me?

Economy – it was a $1.6b industry

Social - Rural Communities in crisis

Next target?

Markets

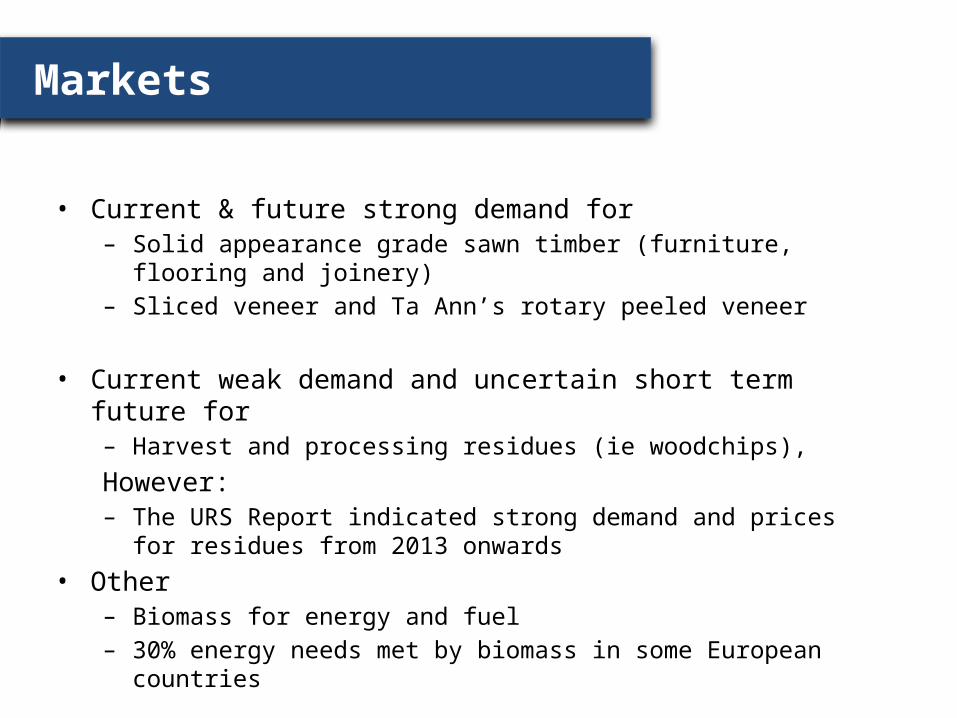

• Current & future strong demand for– Solid appearance grade sawn timber (furniture, flooring and joinery)– Sliced veneer and Ta Ann’s rotary peeled veneer

• Current weak demand and uncertain short term future for– Harvest and processing residues (ie woodchips),

However:– The URS Report indicated strong demand and prices for residues from

2013 onwards• Other

– Biomass for energy and fuel– 30% energy needs met by biomass in some European countries

Threats to markets

Campaigns by green activists in• UN

– Campaigned for extra World Heritage declarations– Continual lobbying in UN-sponsored forums eg Cancun Climate Change Conference

• Japan – Gunns virtually bankrupted– Ta Ann laid off 30% of workforce after 50% of Japanese customers cancelled contracts

in favour of tropical rainforest hardwoods• London

– Ta Ann removed from supplier list for Olympic construction projects• Australia

– Harvey Norman, Corporate Express, Bunnings, Mitre 10 and various other retail outlets– ANZ Bank as a financier

Threats to industry

In the very early rounds of discussions over the Statement of Principles Sean Cadman, for the ACF, said to Glenn Britton - in front of other Industry and ENGO representatives -

“Glenn, if you don’t change your business and agree to our demands we will do you over in the market place and send you broke like we’ve done with Gunns”

Environmental – what gain, really?

So, what does this all mean for me?

Economy – it was a $1.6b industry

Social - Rural Communities in crisis

Next target?

Employment

• Prior to Gunns’ exit – 17,000 to 20,000 direct and indirect– Earnings 1 to 1.2 billion dollars per annum

• Post Gunns’ exit– 8,000 to 9,000 direct and indirect– Earnings 700 million dollars per annum

• Regardless of the outcome of current negotiations– Green and ENGO groups don’t stand to lose or gain

• one job or one dollar– And yet:– – Thousands of industry families stand to lose their livelihoods

causing untold stress and hardship to men, women and children and their regional communities

Environmental – what gain, really?

So, what does this all mean for me?

Economy – it was a $1.6b industry

Social - Rural Communities in crisis

Next target?

High Conservation Value (HCV) Forests

• What are HCV forests?– No internationally accepted definition– Greens use terms such as “old growth” and “wild”– Approx 80% of euc sawlogs in our current production forests are second generation

regrowth, up to 100 years old and emanate from wild fire or previous harvesting

• The initial claim by the greens for HCV forest to be protected included Blackwood forests in Smithton that

– were first harvested in the first half of the 20th century by the first generation Britton family

– were re-harvested in the second half of the 20th century by second generation Brittons

– are currently being harvested for a third time by third and fourth generation family members

• So it is apparent that forests can be harvested productively, contributing major economic and social values to the community and the state while at the same time retaining high conservation values – a win-win surely

Current reserves

• One million hectares of “Old Growth” forests in reserves– average 250 trees per hectare– equating to 250 million trees– which is 10 large old growth trees for each

man, woman and child in Australia

• Half a million hectares of rainforest and re-growth eucalypt forest in reserves– average 250 trees per hectare– equating to 125 million trees– which is 5 large old growth trees for each

man, woman and child in Australia

Environmental – what gain, really?

So, what does this all mean for me?

Economy – it was a $1.6b industry

Social - Rural Communities in crisis

Next target?

The Future

• Pending the outcome of the West Report due 29/2/12

• Impossible to satisfy both– the greens’ demand for 572,000 ha– the industry’s current contractual volumes of suitable wood

• Therefore unilateral State and Federal government decision required which may well satisfy no one

• Real prospect of – continuation of the nonsense we’ve had for the past 30 years – the cessation of all industry costing state and federal governments up to a

further 500 million dollars in compensation to contractors, businesses and their employees

Next target

• Next on the Greens’ agenda, regardless of the monetary and social cost to the taxpayer and the community:– all native forest land previously converted to plantations

is to be rehabilitated back to native forest

– all marginal farm land previously converted to plantations is to be returned to agriculture

• who pays for this? Once again the poor old taxpayer?

Other industry groups– Agriculture?– Aquaculture?– Mining?– Tourism associated with natural landscapes?

Thank you

NOTEThe forestry issue is a 'moving feast' and that obviously as time goes by, more up-to-date information would need to

be considered.