The fiscal impact of lower VAT rates on visitor ......VAT on Visitor Accommodation and Attractions...

56

The fiscal impact of lower VAT rates on visitor accommodation and attractions in the United Kingdom Final Report July 2014 Nevin Associates Ltd Kilgour Spencer Place Trinity Edinburgh EH5 3HF Tel: 0131 552 6089 Mobile: 078 248 29 445 [email protected]

Transcript of The fiscal impact of lower VAT rates on visitor ......VAT on Visitor Accommodation and Attractions...

The fiscal impact of lower VAT rates on visitor accommodation and attractions

in the United Kingdom

Final Report

July 2014

Nevin Associates Ltd Kilgour Spencer Place Trinity Edinburgh EH5 3HF Tel: 0131 552 6089 Mobile: 078 248 29 445 [email protected]

Table of Contents

Glossary of Terms ....................................................................................................................... i Executive Summary .................................................................................................................... ii 1 Purpose and Structure of the Report .................................................................................. 1

1.1 Background and Objectives 1

1.2 Structure of this Report 3

2 The Computable General Equilibrium model analysis, 2012 .............................................. 4 3 Developments elsewhere in the EU since 2011 .................................................................. 6

3.1 Trends in VAT on tourism and hospitality services 6

3.2 Evidence of the Impact of Changes in VAT rates 8

3.3 Conclusions 9

4 The updated fiscal model .................................................................................................. 11

4.1 Introduction 11

4.2 Sector development since 2011 12

4.3 Assumptions driving the DPE fiscal model 14

4.4 How a Reduction in VAT would be passed through – the Base Case 17

4.5 How a Reduction in VAT would be passed through – the Rapid Adjustment Case 17

4.6 Results – The Base Case 18

4.7 The Overall Picture 22

4.8 Key Sensitivities 25

4.9 Results – The Rapid Reduction Scenario 27

4.10 Results – The position after four years 29

5 Conclusions ....................................................................................................................... 31 Annexe 1: VAT Rates applying to Hotels and Amusement Parks in EU Member States, 2007-2013 ......................................................................................................................................... 33 Annexe 2: DPE Fiscal Model Assumptions and Sources .......................................................... 40 Annexe 3: Forecast Outlook for the UK’s Tourism Balance ..................................................... 47 Annexe 4: Fiscal Impact for Accommodation and Attractions ................................................ 49

VAT on Visitor Accommodation and Attractions in the UK i

Glossary of Terms

The following acronyms have been used in this report (in alphabetical order): ABS Annual Business Survey

CGE Computable General Equilibrium DPE Dynamic Partial Equilibrium EU European Union

FTE Full Time Equivalent (job)

GDP Gross Domestic Product GVA Gross Value Added HMRC Her Majesty’s Revenue and Customs HMT Her Majesty’s Treasury ITR International Tourism Receipts OECD Organisation for Economic Co-operation and Development ONS Office of National Statistics SIC Standard Industrial Classification TWER Trade-Weighted Exchange Rate

VAT Value-Added Tax

VAT on Visitor Accommodation and Attractions in the UK ii

Executive Summary

Current Position The visitor accommodation and attractions sector in the UK currently pays VAT at the full standard rate of 20%. Most other member states of the European Union apply a reduced rate. The average rate of VAT applying to visitor accommodation in the EU is 10.8%, and 19 EU member states apply a VAT rate of 10% or less. Industry and political concerns Leading sector operators are concerned that the additional burden of VAT on the UK tourism sector has held back the sector’s development in a highly price-sensitive international market.1 This view is shared by dozens of parliamentarians, many of whom expressed their support for a more competitive VAT rate during a Westminster debate last February. The debate witnessed strong support from MPs for the proposal from Conservative, Labour, Liberal Democrats, Green, SNP, DUP, SDLP, and Alliance parties.

Conclusions Under a "business as usual" VAT scenario, it is likely that the UK's share of the international tourism market will contract. By contrast, a reduction in the VAT rate will stimulate the growth in overseas tourism to Britain, and domestic tourism, helping to increase the taxation base. The impact of a cut in tourism VAT will also be felt by the wider economy. For each £1 spent in the tourism industry, 70p extra is spent in other sectors of the economy. Cutting tourism VAT will therefore not only benefit hotels and tourist attractions, but also the construction industry, the retail sector, the airline companies and so on. Because of the highly price sensitive nature of the sector, lower VAT rates that feed through to lower prices will stimulate higher turnover and employment. This in turn will increase income and corporation tax receipts and reduce benefit payments. Overall, when both the direct and indirect effects of a lower VAT rate are taken into account, our estimates indicate that there will be a net £45 million gain for the Exchequer. The source of these gains is shown in the diagram overpage.

1 In order to assess the full impact of reduced VAT on the sector, Bourne Leisure Group and Merlin

Entertainments Group commissioned a report completed in February 2011 on Tourism Sector VAT: A Report on the Impact of Reduced VAT rates on British Visitor Accommodation, Attractions and the Wider Economy, by Deloitte, Graham Wason and Michael Nevin. The report concluded that lower VAT would feed through to lower prices, stimulating greater demand for accommodation and attractions, increasing the total revenue base on which VAT is levied. In aggregate, the February 2011 analysis estimated that there would be a net fiscal gain to the Exchequer.

VAT on Visitor Accommodation and Attractions in the UK iii

VAT on Visitor Accommodation and Attractions in the UK iii

VAT on Visitor Accommodation and Attractions in the UK iii

VAT on Visitor Accommodation and Attractions in the UK iv

A VAT reduction could help meet the Prime Minister’s goal of raising the expenditure of domestic British tourism from 36% to 50%, as more visitors would choose to stay at home for their vacations rather than travel abroad. Additional spending – from both foreign and domestic tourists – would be circulated and spent in the UK economy and would continue to benefit the Exchequer over a longer period of time By growing the tourism sector, the UK can reduce its balance of payments deficit. In 2011, travel expenditure by non-residents visiting the UK accounted for 4.4% of total UK exports. A VAT reduction for the tourism industry would provide a significant boost to the UK export market – a goal that George Osborne has signalled as a key aspect of the recovery Another indirect benefit to the Treasury would be a reduction in the so-called ‘shadow economy’. The UK tourism industry is populated by a large number of small firms that may choose not to expand or invest in order to keep below the VAT threshold to avoid paying tax. In France, the ‘shadow economy’ has been estimated to have reduced by €720 million a year due to VAT reductions implemented. Another study using the government’s own Computable General Equilibrium (CGE) economic model (conducted by Treasury Advisor Professor Adam Blake) noted that cutting tourism VAT is “one of the most efficient, if not the most efficient, means of generating GDP gains at a low cost to the Exchequer”. This result was reinforced by a number of scenarios run through the CGE model. One scenario envisaged a commitment by the tourism industry to take on an additional 10,000 workers who had previously been long-term unemployed as part of an agreement with the Treasury underpinning a VAT reduction (similar to the French ‘Contrat d’Avenir’). In this scenario, GDP gains peaked at £4 billion per year rather than £3 billion in the base case. There was also a positive fiscal impact for the first 4 years. In summary, a lower VAT rate would represent a "win : win" strategy – helping to stimulate Britain's tourism industry, increase foreign exchange earnings, create additional jobs, and generate a net fiscal gain for Her Majesty's Treasury. On this basis, we believe that the case for lower VAT on tourism services merits further consideration by Her Majesty’s Treasury.

VAT on Visitor Accommodation and Attractions in the UK 1

1 Purpose and Structure of the Report

1.1 Background and Objectives The visitor accommodation and attractions sector in the UK currently pays VAT at the full standard rate of 20%. Most other member states of the European Union apply a reduced rate. The average rate of VAT applying to visitor accommodation in the EU is 10.8%, and 19 EU Member states apply a VAT rate of 10% or less. The additional burden of VAT that the UK tourism sector has to bear relative to its competitors has held back the sector’s development, which operates in a highly price-sensitive international market. In certain parts of the UK, the effects of this competitive disadvantage are particularly acute. For example, in Northern Ireland hotels and attractions paying 20% VAT are faced with direct competition from operators in the Republic of Ireland who are charged VAT at 9%. For this reason, a Parliamentary debate was secured by Margaret Ritchie MP (SDLP) which took place on February 11th 2014. The debate witnessed strong support from MPs for the proposal from Conservative, Labour, Liberal Democrats, Green, SNP, DUP, SDLP, and Alliance parties. In order to assess the wider impact of reduced VAT on the sector, Bourne Leisure Group and Merlin Entertainments Group commissioned a report completed in February 2011 on Tourism Sector VAT: A Report on the Impact of Reduced VAT rates on British Visitor Accommodation, Attractions and the Wider Economy, by Deloitte, Graham Wason and Michael Nevin. This report indicated that most EU Member states levy reduced rates of VAT on visitor accommodation and visitor attractions. This continues to be the case, as shown in Annexe 1 to this report which sets out the rates of VAT that have applied to visitor accommodation and attractions in each Member State of the EU since 2007. This suggests that national governments across the EU recognise that higher tax rates could have the perverse effect of reducing tax yields, because of the negative impact high tax rates would have on inbound tourism. The report accepted that the immediate impact of cutting VAT in the UK from its current rate of 20 per cent to a reduced rate of 5 per cent would be a loss of VAT yields, but concluded that this would be offset by lower prices, stimulating greater demand for accommodation and attractions. This would increase the total revenue base on which VAT is levied. There would be a number of other benefits from lower VAT rates:

higher levels of employment in tourism and related services;

this increase in employment will generate additional income tax receipts and savings in social security payments;

higher expenditure will also generate an increase in profits and corporation tax payments by sector operators;

VAT on Visitor Accommodation and Attractions in the UK 2

higher tourism incomes will feed through to higher expenditure in other sectors of the economy, which in turn will generate further tax receipts.

In aggregate, taking all these indirect effects into account, the February 2011 analysis indicated that, while the Exchequer would suffer an initial net loss in taxation receipts, once the stimulus imparted by lower taxes and prices fed through to higher demand there would be a net fiscal gain to the Exchequer, which would increase year by year over a 10-year period. In Year 4 following a reduction – by which time most of the adjustment to lower VAT rates has occurred – the February 2011 analysis indicated the following impact on tax yields:

Impact on the Exchequer’s Position Value, £ million

(1) Net direct loss of VAT receipts -£1,145.8

(2) VAT Yield on increased turnover at 5% £67.1

(3) VAT Yield on wider base at 5% £33.6

(4) Income and national insurance derived from new jobs & previously unreported (Shadow Economy) jobs

£176.2

(5) Income and national insurance derived from higher wages

£38.5

(6) Savings in social security payments £164.5

(7) Corporation tax from higher margins on current turnover including previously unreported (Shadow Economy) turnover

£90.6

(8) Corporation tax from higher turnover £95.2

(9) Income tax paid on dividends £40.9

Sub-total, direct and indirect fiscal impact -£439.1

(10) Multiplier impact £753.7

Net fiscal impact £314.6

As shown in the Table, the February 2011 analysis estimated a net fiscal gain following a VAT reduction of £315 million p.a. by Year 4 compared to a “no policy change” scenario. These findings were contested by HM Treasury, who, in a collaborative exercise, suggested that the analysis be run through their own Computable General Equilibrium (CGE) Model which assesses the fiscal impact of changes in taxation policy. This exercise was completed in 2012.

VAT on Visitor Accommodation and Attractions in the UK 3

1.2 Structure of this Report

Section 2 of this report summarises the results of the analysis undertaken through the Treasury's CGE Model in 2012, which was carried out by Professor Adam Blake of Bournemouth University, who helped to develop the model and is an authorised user of it (the CGEM is protected under the Official Secrets Act and therefore was not directly available to the Deloitte / Wason / Nevin team). Section 3 summarises developments that have occurred in the VAT regime particularly applying to visitor accommodation and attractions across the EU since the February 2011 report was completed. Section 4 sets out an updated analysis of our Dynamic Partial Equilibrium (DPE) model as applied in 2011, inputting the latest available information on sector turnover, employment and cost structure provided by the Office of National Statistics (ONS). Section 5 sets out the conclusions that emerge from this analysis.

VAT on Visitor Accommodation and Attractions in the UK 4

2 The Computable General Equilibrium model analysis, 2012 The Report on the Impact of Reduced VAT rates on British Visitor Accommodation, Attractions and the Wider Economy was published in February 2011. Consultants who carried out the report met HMT officials in September 2011 to discuss the findings of the report. At this meeting, HMT officials suggested that this impact be modelled using the Treasury’s own Computable General Equilibrium (CGE) model, and that the Campaign could work with Professor Adam Blake of Bournemouth University who built and helps to maintain the CGE model. Permission was granted by HMT for Professor Blake to use the model for the exercise. The analysis was carried out in 2011/12 and a further meeting was held with HMT to discuss the findings of the CGE analysis in September 2012. Unlike the DPE model, the Treasury’s CGE Model does not take account of the potential dynamic effects of a VAT reduction in stimulating sector investment and growth over time. It is a “comparative-static” model, measuring HMT’s fiscal receipts before and after a specified tax change. Nevertheless, the results were broadly consistent with those reported in the February 2011 report, showing a modest net loss to the Exchequer as a consequence of a VAT cut from 20% to 5%. Professor Blake’s conclusion was that reduced VAT on tourism services represents “one of the most efficient, if not the most efficient, means of generating GDP gains at low cost to the exchequer that I have seen with the CGE model”. This result was reinforced by a number of scenarios run through the CGE model. One scenario envisaged a commitment by the tourism industry, as part of a collaborative package similar to the French ‘Contrat d’Avenir’, to take on an additional 10,000 workers who had previously been long-term unemployed as part of an agreement with HMT underpinning a VAT reduction. In this scenario, GDP gains peaked at £4 billion per year, rather than £3 billion in the base case. There was also a positive fiscal impact for the first 4 years and a cumulative fiscal impact over the 2012-2020 period that is only slightly negative at -£151 million, excluding multiplier effects. The DPE and CGE models are constructed in very different ways and comparison between the two is not straightforward. However, the estimated direct fiscal loss to the Exchequer as a result of cutting VAT on visitor accommodation and attractions after four years is quite close – at £479 million in the CGE base case scenario2 compared to £439 million in the DPE model. The composition of this net effect is different in the two models and, in addition, the DPE model estimated a multiplied gain of £754 million for the Exchequer from taxation gains elsewhere in the supply chain which are not included in the CGE model.

2i.e. before additional scenarios such as the ‘Contrat d’Avenir’ scenario involving a commitment to

create 10,000 jobs for those previously long-term unemployed

VAT on Visitor Accommodation and Attractions in the UK 5

Professor Blake and the consultants to the Campaign came to the agreement that “in summary, based on reasonable and plausible assumptions, the modelling exercise seems to support a general case that a reduction of VAT on tourism services would be fairly close to fiscal neutrality.”

VAT on Visitor Accommodation and Attractions in the UK 6

3 Developments elsewhere in the EU since 2011

3.1 Trends in VAT on tourism and hospitality services While HMT have not altered their policy with respect to VAT on tourism and hospitality services, this has not been the case elsewhere in the EU. Total VAT revenue currently generates approximately a fifth of all taxation receipts collected in the EU, and therefore is a core source of revenue for all Member State governments. At EU level, the European Council of Ministers and European Commission have sought to harmonise the regulatory framework applying to VAT, in order to ensure that it is applied consistently across different Member States. The EU does however allow Member states to apply a reduced rate of VAT to labour-intensive services, and Council Directive 2009/47/EC of May 5th 2009 included a list of these services. Visitor accommodation and attractions are included on this list. Of the EU’s 28 Member States, all but one (Denmark) applies at least one reduced rate. These reduced rates are widely used: approximately one-third of all consumption is taxed at reduced rates, with the average reduced rate being between 7.5% and 10.5%. The rates of VAT applying to accommodation and attractions (amusement parks) between 2007 and 2013 are set out as Annexe 1 to this report. The Annexe indicates that the standard rate of VAT has shown a general tendency to rise across the EU as a whole since 2007, as EU governments have sought to reduce their budget deficits, which rose sharply in the aftermath of the global financial crisis of 2007/08. Since 2007, not one Member State has reduced its standard rate. The best that has happened is that the standard rate has remained stable – but this has generally occurred where it was already at a high level, in countries such as Sweden and Denmark, where the standard rate stayed at 25% throughout the period. A number of major EU Member states have increased the standard rate of VAT:

in Italy, the standard rate of VAT has increased from 19% in 2009 to 22% in 2014;

in the Netherlands, the standard rate increased from 19% in 2009 to 22% 2014;

in Spain, the rate increased from 16% in 2009 to 21% in 2014;

and in the UK from 15% in 2009 (a level to which it was temporarily reduced from 17.5%) to 20% in 2014.

Overall, across the EU, over the period from May 2007 to January 2014, the average standard rate of VAT of the 28 EU Member states increased from 19.5% to 21.5%, or by 10.3%.

VAT on Visitor Accommodation and Attractions in the UK 7

However, while there has been a general upward drift in standard VAT rates, recent years have also witnessed a reduction in certain VAT rates applying to price sensitive, labour-intensive sectors. This suggests that national governments are aware of the adverse impact that high VAT rates can have on employment, turnover, and ultimately the taxation base in such sectors. Since the unanimous decision by the Ministers of Finance of the European Union to permit Member states to apply a reduced rate of VAT to catering and restaurants on May 5th 2009, there have been significant VAT reductions on hospitality services across the European Union. In chronological order, the reductions in VAT that have occurred since then which are of particular relevance to accommodation and attractions include the following:

July 1st 2009: France reduced VAT for the restaurant industry from a standard rate of 19.6% to a reduced rate of 5.5% with immediate effect. The reduced rate was adjusted to 7% in 2012, and the President of France increased the rate further to 10% in 2014. While the French President has progressively increased the reduced rate from 5.5% to 10% as a deficit-reduction measure, the French rate remains half of the rate applying in the UK.

December 18th 2009: In Germany, the Bundesrat confirmed the decision of the Bundestag in approving a reduction in the VAT rate for hotel accommodation from 19% to 7% with effect from January 1st 2010. This did not follow directly from the decision by the Council of Ministers in May 2009 to permit a reduced rate of VAT to apply to restaurant and catering services, but was part of the wider trend by EU Governments to apply lower rates of VAT to price-sensitive sectors in order to stimulate a recovery from the recession that followed the financial crisis of 2007/08.

July 1st 2011: In Ireland, the parliament approved a VAT reduction from 13.5% to 9% for room accommodation and restaurants. VAT on tourism in the Republic of Ireland was reduced first during the 1980s which led to a significant increase in tourism. Since then, the rate has gone up and down but has always been at a reduced level. Ireland suffered a greater proportional national debt crisis following the 2007/08 credit crisis than the UK, and reduced government spending and increased taxes, including the standard rate of VAT. However, recognising the potential for job creation and growth through tourism and hospitality, the Irish government further reduced the rate applying to tourism from 13.5% to 9% from 1st July 2011 until the end of December 2013. According to the Irish Hotels Federation (IHF) and the Restaurants Association, over 96% of their members passed on at least some of the decrease in VAT, and more than half of those businesses responding to the IHF survey reported an increase in business compared with the same time last year, with 90 per cent saying that the reduced tourism VAT rate had boosted their business. There was a net increase in the sector of 6,200 jobs (5.7%) between the second quarter of 2011 and the second quarter of 2012, at a time when total employment in Ireland fell overall.

VAT on Visitor Accommodation and Attractions in the UK 8

In late 2013 the Irish Government announced that VAT on tourism would remain at 9% indefinitely.

2013: In Greece, negotiations with the International Monetary Fund and the Euro Group (the European Commission and European Central Bank) on a package of measures to bail out the Greek Government and enable it to continue to service its national debt led to agreement that the government could reduce the VAT rate of restaurant and café services from 23% to 13% from August 1st 2013.

3.2 Evidence of the Impact of Changes in VAT rates

FRANCE. According to INSEE – the Institut National de Statistiques et Etudes Economiques, France’s official office of national statistics – employment in the hotel and restaurant sector increased from 898,100 to 973,100, or by 75,000, between June 30th 2009 and September 30th 2011, which were the first nine quarters following the VAT reduction on restaurant meals from 19.6% to 5.5% on July 1st 2009. Several reports for the National Assembly and the Senate, including Senator Houel’s report, showed that 40% of the VAT decrease was passed through to higher staff remuneration, 23% to price decreases, 20% to investments, and the balance to cash improvements. In addition to the net impact on job creation, President Nicolas Sarkozy declared on television in early 2012 that the VAT decrease had saved 30,000 cafés and restaurants that were struggling financially. On the basis that, on average, each of these small cafés employed three people, this would imply that 90,000 jobs were safeguarded in the sector. On the assumption that there is a sectorial multiplier of 70%, then the 75,000 jobs directly created in the sector would have supported 50,000 jobs further down in the supply chain. On this basis, a total of 215,000 jobs were created or safeguarded by the VAT reduction, being the sum of 75,000 jobs directly created (INSEE), 50,000 jobs indirectly created (through the multiplier effect) and 90,000 jobs safeguarded. It is too early to fully assess the impact of the increase in VAT to 10%, but early indications are that it is having a negative impact on sector employment. GERMANY. A press release issued by the German Hotel Association, DEHOGA, on March 29th 2012 reported the results of a study on the impact of the VAT reduction carried out by the German Institute of Management Tourism (IMT) at the University of Applied Sciences Westkueste, headed by Dr Bernd Eisenstein. This study reported that the decrease in value added tax on January 1st 2010 has resulted in a massive surge in investment. In the two years following the introduction of reduced VAT rates on accommodation, the owners of hotels, guesthouses and bed and breakfasts stated that it had resulted in a significant stimulus. The survey covered 5,000 accommodation businesses, which between them had invested €939.6 million and created over 11,000 new jobs and apprenticeships as a result of the VAT cut, and had also reduced average room rates by 1.6%, during a period of rising demand. Those interviewed stated that they planned to invest a further €827.5 million and hire an additional 6,000 employees later on in 2012.

VAT on Visitor Accommodation and Attractions in the UK 9

IRELAND. In its 2013 budget, the Irish Government extended the 9% VAT rate into 2014 and at the same time reduced travel tax (airport departure tax) to zero, giving the Republic a significant tax advantage over its competitors in the UK in both respects. SPAIN. A counter-example is provided by the experience of Spain. Whereas most EU Member states have sought to maintain a reduced rate of VAT for visitor accommodation and attractions, the Spanish Government, faced with a mounting budget deficit, opted to apply the full VAT rate to theme and amusement parks from September 2012, at the end of the 2012 season. The Spanish association of theme park operators reported that Spanish parks suffered a reduction of nearly 13% in attendance in 2013, even though most operators sought to absorb some of the increase in their pricing structure. The consequence has been a squeeze of profitability, and 7 of the 10 Spanish parks have reduced staff number by an average of 10.2%. The Association stated in March 2014 that, “Since September 2012, when VAT rates were increased in Spain, theme and amusement parks have been clearly discriminated by the Spanish Government, as our activity has not been considered as part of the tourist sector, in which the VAT rate is 10%. Our activity has suffered a VAT increase from 8% to 21% which directly provoked a reduction in the number of visitors of nearly 13% (and some decline in spend per visitor) resulting in a decline in turnover of 17%, and a reduction in employment in most of the parks by an average of 10%. These magnitudes, if they are compared with the record numbers of the tourist sector emphasized by the Spanish Prime Minister in Madrid on January 21st 2014 (arrivals of foreign tourists – 60.4 million, with 250 million hotel nights) clearly leave theme and amusement parks in a situation of marginality and lacking competitiveness, which will be sharpened if the Government applies a VAT reduction to the cultural sector and a positive response is not given to our submissions for lower VAT.”

3.3 Conclusions

The evidence of the impact of changes in VAT across the EU since 2011 confirms several key findings:

Most EU member states apply reduced rates to visitor accommodation and attractions – the UK remains an exception in charging the full rate of VAT to this sector;

More reduced rates have been applied since 2011, and where reduced rates have been introduced, they have been maintained – even where, as in the case of the Republic of Ireland, the government is seeking to reduce the budget deficit. This suggests that the governments that have introduced reduced rates

VAT on Visitor Accommodation and Attractions in the UK 10

believe that they have been effective in stimulating growth and jobs in their tourism sectors;

One exception is Spain, which has applied the full standard rate to theme and amusement parks (although not to tourism services in general), precipitating a sharp downturn in turnover, profitability and jobs, thus eroding the base on which taxation is levied;

Otherwise, EU governments recognise that competitive VAT rates need to be applied to tourism, which is a highly price sensitive and labour-intensive sector.

VAT on Visitor Accommodation and Attractions in the UK 11

4 The updated fiscal model

4.1 Introduction

This section sets out the key assumptions and results of a fiscal modelling exercise to update analysis previously conducted in 2011 of the full fiscal impact of the proposed VAT reduction. As in 2011, the analysis is based on a reduction in VAT from a current standard rate of 20% to a reduced rate of 5%. It should be noted that the reduced 5% rate already applies to certain specific parts of the sector, including static caravans and ski lifts. The same methodology has been applied to undertake this analysis as in the 2011 report, applying a fiscal model which measures not only the direct impact of lower VAT rates, in terms of the direct loss of VAT receipts, but also indirect gains that would accrue to the Exchequer, arising from:

higher turnover as sector demand would be stimulated by lower prices;

greater income and national insurance payments generated by new jobs and higher wages in the sector;

savings in social security payments as a consequence of lower unemployment – with some of the new jobs created in the sector taken up by those previously unemployed;

increased corporation tax payments as a result of higher margins and higher turnover;

increased income taxes paid on dividends generated by the accommodation and attractions sector; and

multiplier impacts from additional taxes generated further down the supply chain for accommodation and attractions.

The assumptions underpinning the model have been updated to take account of the latest information on sector turnover and employment. This is based on official data provided by the Office of National Statistics, drawing on the latest version of their Annual Business Survey, released on November 14th 2013. Thus the updated analysis has been prepared on a like-for-like basis with the earlier 2011 analysis.3

3 The 2011 report was based primarily on 2008 ONS data, which was the latest data available when

that report was prepared, drawing on the ONS, 'Annual Business Inquiry: Section I - Accommodation and food service activities', Release date 15/06/2010. This 2014 report is based primarily on 2012 ONS data, drawing on the ONS, 'Annual Business Inquiry: Section I - Accommodation and food service activities', Release date 14/11/2013.

VAT on Visitor Accommodation and Attractions in the UK 12

4.2 Sector development since 2011

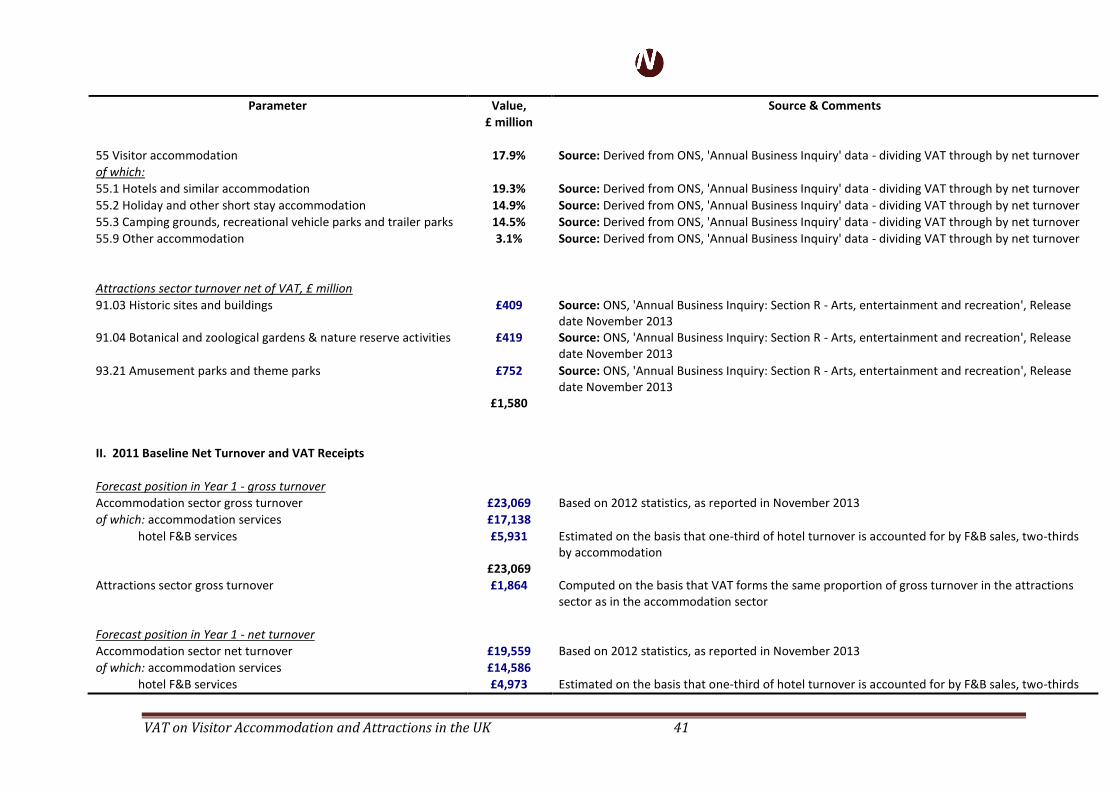

The Office for National Statistics (ONS) has provided data on turnover, jobs and employment costs in the accommodation and attractions sector based on its Annual Business Survey (ABS). It covers the period the years between 2008 and 2012 inclusive (i.e. five years). The accommodation sector comprises the entirety of SIC Code 55. (The Standard Industrial Classification (SIC) is a system for classifying industries by a four-digit code established in the late 1930s). Our definition of the visitor attractions sector for the 2011 study covered the following SIC codes within Section R (arts, entertainment and recreation):

91.03: Historic sites and buildings,

91.04: Botanical and zoological gardens and nature reserves,

93.21: Amusement parks and theme parks. The data provided by the ONS covers:

number of enterprises,

total turnover net of VAT,

approximate Gross Value Added at basic prices,

total employment,

total employment costs and

net capital expenditure. The ONS data also shows the VAT element and gross turnover (= net turnover + VAT) for the accommodation sector. This is not available for the attractions sector, so for the purposes of our analysis we have assumed that the proportion of gross turnover accounted for by VAT is the same for the visitor attractions sector as for the accommodation sector. Trends for each sector are assessed below.

Accommodation

Both net and gross turnover dipped in 2009 compared to 2008, before recovering slightly in nominal terms in 2010 and 2011. However, in real (inflation-adjusted) terms, both showed a decline over the period between 2008 and 2011. For example, net turnover increased in nominal terms from £17,532 million in 2008 to £18,667 million in 2011, or by 6.5%. Over the same four-year period, the UK Retail Price Index increased from 216.8 (in June 2008) to 235.2 (in June 2011), or by 8.5%. Thus, there was a real terms decrease in net accommodation turnover over the period. The same applies to gross turnover, which increased only marginally in money terms from £20.245 million in 2008 to £21.97 million in 2011, representing a decline in real terms.

VAT on Visitor Accommodation and Attractions in the UK 13

However, in the most recent year for which data is available – 2012 – there was a real increase, with net turnover up from £18.667 million to £19.559 million (4.8%), and gross turnover up form £21.97 million to £23.069 million. It is likely that this was driven by both business and leisure demand, and may have been assisted by the Olympics which were held in London. Sector employment, after being static over the period between 2008 and 2010, increased ahead of the upturn in real turnover from 388,000 to 429,000 in 2011, stabilising at that level in 2012. This represents total employment, including part-time employees, although the same pattern is evident in the FTE data. This suggests that accommodation businesses started hiring staff almost immediately they experienced an upturn in business.

Attractions

Going through each of the subsectors in turn: 91.03: Historic Buildings. Net turnover fell quite sharply from £377 million in 2008 to £303 million in 2009. It then recovered in 2010 and more strongly in 2011 (possibly reflecting the staycation effect) before stabilising in 2012. Interestingly, total employment increased from 11,000 to 13,000 in 2009 – i.e. the year of the sharp decline in turnover – since when it has remained steady. 91.04: Botanical Gardens and Zoos: the decline in turnover was more severe and prolonged in this sector than in historic buildings, probably not helped by wet weather in the summer and snows in the winter, falling from £559 million in 2008 to £306 million in 2011, before recovering to £419 million in 2012. The ONS data shows negative gross value-added for the sector in 2011 and 2012 – i.e., it was only surviving with the aid of public subsidies or loss-making equity at macro level. However, total employment did not fall, increasing slightly from 17,000 in 2008 to 19,000 in 2010. 93.21: Amusement and Theme Parks. Turnover increased from £611 million in 2008 to £733 million in 2009, before decreasing sharply to £605 million in 2010 – i.e. the downturn in this sector seems to have occurred one year later than the rest of the accommodation and attractions sector. But amusement and theme parks then recovered strongly in 2011, up to £776 million, before falling back slightly to £752 million in 2012. This may have been due to the "staycation effect" in 2011. Employment has risen gradually from 16,000 in 2008 to 18,000 in 2012.

Conclusions

The statistics for the accommodation and attractions sector are consistent with wider macroeconomic indicators which suggest that a recovery is underway in the UK. Indeed, it could be argued that the attractions and accommodation sector helped to lead the economic recovery, as they started to grow in 2011, one year ahead of the overall economy where recovery commenced in 2012/13.

VAT on Visitor Accommodation and Attractions in the UK 14

4.3 Assumptions driving the DPE fiscal model

All the assumptions driving the DPE fiscal model, and their sources, are set out in Annexe 2 to this report. Key changes in assumptions compared to the 2011 analysis are as follows: 1. Updated net turnover. ONS data indicates that, after allowing for inflation,

turnover in the accommodation sector was flat in real terms over the five years between 2008 and 2013. In the attractions sector, the turnover of historic sites and buildings has fallen slightly, while the turnover of botanical and zoological gardens dropped significantly in both nominal and real terms. The turnover of amusement parks and theme parks has grown strongly. We estimate that one-third of hotel turnover is generated by food and beverage (F&B) sales, to which a 20% standard VAT rate continues to apply. However, not all hotels have restaurants, nor do guesthouses, bed and breakfast establishments, youth hostels, self-catering establishments, etc. ONS statistics indicate that, of total accommodation sector turnover, 76% was accounted for by hotels, most but not all of which have restaurants, and 24% by other forms of accommodation, most of which do not have an F&B offer. On this basis, we estimate that, overall, 25% of total visitor accommodation turnover will not benefit from the VAT reduction, and 75% will.

2. Changes in VAT payments. One striking result that emerges from ONS statistics

is that VAT payments by the accommodation sector have increased much more rapidly than the increase in the sector’s net turnover – with VAT up from £2.7 billion in 2008 to £3.5 billion in 2012, or by 29%, against an increase in turnover of less than 12%. This reflects the increase in the standard rate of VAT to 20%. Overall, VAT payments as a percentage of net turnover increased from 15.5% in 2008 to 17.9% in 2012. The ONS does not report VAT payments made by the attractions sector, so estimates have been imputed by applying the accommodation VAT rate to historic sites, botanical gardens, amusement and theme parks. This gives a total estimate of VAT paid by the attractions sector of £283 million, which is close to the 2011 estimate of £274 million.

3. Personnel expenses and investment as a percentage of sector turnover has

been calculated from the latest ONS data (as in 2011) and are broadly similar to the percentage rates calculated in 2011. One exception is personnel expenses in the attractions sector, which increased from 51% to 62% including payments to subcontractors.

4. Turnover per job in both the accommodation sector and visitor attraction

sector appears to have fallen in real terms based on ONS data over the past five years, although average remuneration per job has increased slightly in the accommodation sector. It has fallen sharply in the attractions sector, on the basis of the ONS data.

VAT on Visitor Accommodation and Attractions in the UK 15

5. The average rate of income tax and National Insurance contributions used in the model has fallen from 36% to 32%, reflecting the reduction in the standard rate of income tax to 20%. The figure of 32% is equal to the 20% standard rate income tax plus 12% employee’s National Insurance (NI). A worker paid the average UK wage of £26,500 would contribute approximately 32% of this wage to the Exchequer in income tax, employees’ NI and employers’ NI.

6. The estimated annual value of Social Security payments paid to the unemployed,

including housing benefit etc has been increased in line with inflation from £7,500 to £8,360 p.a.

The altered values entered into the updated fiscal model are set out in the Table below.

Description 2014 2011 % change

55 Visitor Accommodation net turnover, £m £19,559 £17,510 11.7%

Of which:

55.1 Hotels and similar accommodation £14,920 £13,528 10.3%

55.2 Holiday and other short stay accommodation £1,505 £1,362 10.5%

55.3 Camping grounds, recreational vehicle parks and trailer parks £2,777 £2,438 13.9%

55.9 Other accommodation £357 £182 96.2%

55 Visitor accommodation VAT Payments £3,509 £2,718 29.1%

Of which:

55.1 Hotels and similar accommodation £2,873 £2,197 30.8%

55.2 Holiday and other short stay accommodation £224 £200 12.0%

55.3 Camping grounds, recreational vehicle parks and trailer parks £402 £306 31.4%

55.9 Other accommodation £11 £15 -26.7%

£3,510 £2,718

Visitor accommodation VAT payments as a % of net turnover 17.9% 15.5%

Attractions sector turnover net of VAT, £ million

91.03 Historic sites and buildings £409 £369 10.8%

91.04 Botanical and zoological gardens & nature reserve activities £419 £562 -25.4%

93.21 Amusement parks and theme parks £752 £611 23.1%

£1,580 £1,542

Attractions sector VAT £283 £274

Accommodation sector

Personnel expenses - % of turnover net of VAT 31% 29%

Investment - % of turnover net of VAT 10% 11%

Attractions sector

Personnel expenses - % of turnover net of VAT 62% 51%

Investment - % of turnover net of VAT 12% 16%

VAT on Visitor Accommodation and Attractions in the UK 16

Description 2014 2011 % change

Turnover per job: visitor accommodation sector £47,820 £45,000 6.3%

Turnover per job: visitor attraction sector £30,980 £35,000 -11.5%

Average remuneration per job: visitor accommodation sector £14,145 £12,400 14.1%

Average remuneration per job: visitor attraction sector £15,800 £15,600 1.3%

Average rate of income tax & National Insurance 32.0% 36.0%

Social security payments - average per person unemployed p.a. £8,360 £7,500 11.5%

Since the original report was presented in 2011, it has been pointed out that one source of tax revenue was omitted from it, which is included in HMT’s own CGE model, namely business rates. In 2012/13, £26.1 billion was paid business rates across the UK, representing approximately 1.67% of UK GDP at £1,570 billion. However, HM Government’s supply use tables indicate that the proportion of turnover paid in rates by the visitor accommodation sector is significantly higher than this, at approximately 6% of value-added, reflecting the sector’s “property intensive” cost structure. In order to compute the likely gain to the Exchequer from business rates, a business rates factor has been incorporated into the fiscal model at 1.67% of increased turnover, which we regard as a conservative estimate, being lower than would be implied by the supply use tables. It is calculated on the basis of the overall proportion of business rates in total UK GDP. It is assumed that the adjustment in rates will occur in line with the adjustment in sector turnover, rather than lagging behind it, for the following reasons: a/ A lagged response would be based on the assumption that sector operators wait until demand turns upwards before commissioning new capacity. b/ An alternative model would be based on investment driving an upturn in turnover, which occurs in innovative sectors and where a sector has historically underinvested. Reports on the impact of lower VAT on hotel accommodation in Germany, introduced in January 2010, suggest that this is what has happened there. The reduction in VAT rates fed through to higher investment ahead of an increase in demand, and higher investment in turn helped to drive an increase in hotel sector turnover, through increased capacity and enhanced quality. c/ The question is whether investment would lead or lag an upturn in turnover in the UK. The most reasonable assumption, in the absence of other information, is that it would broadly match the gradual adjustment in turnover, in part because it is possible that an agreement in the form of a "Contract of the Future" could underpin any decision by HMT to reduce VAT, and could include a commitment by operators to utilise some of the VAT reduction for greater investment.

VAT on Visitor Accommodation and Attractions in the UK 17

4.4 How a Reduction in VAT would be passed through – the Base Case The point made in [c] above, regarding the likely pass-through of lower VAT, is consistent with the assumptions made regarding the allocation of a VAT reduction, which are the same in the updated model as in the previous 2011 model. Overall, the base case fiscal model assumes that a 15 per cent reduction of VAT from 20 per cent to 5 per cent will feed through as follows:

60 per cent of the reduction will feed through in lower prices;

10 per cent will be used to recruit more workers and pay higher wages;

3 per cent will be allocated to training;

22 per cent will be allocated to investment; and

5 per cent will be allocated to higher profit after investment. These adjustments will not happen instantaneously. The evidence from countries that have reduced VAT indicates that it may take 3 to 4 years for a full pass-through of reduced VAT to lower prices. Initially, some operators may seek to retain the VAT reduction and hold their prices at a constant level. However, the evidence from Ireland and France indicates that some operators in a price-sensitive market will take the lead in reducing prices in an effort to increase their market share. This in turn will force an adjustment by competing operators in order to protect their sales. On the basis of the international evidence, the base case model assumes the following adjustment path:

30% of the total price adjustment occurs in Year 1 following the VAT cut;

70% in Year 2;

90% in Year 3; and

100% in Year and thereafter.

4.5 How a Reduction in VAT would be passed through – the Rapid Adjustment Case An alternative scenario posits that the Base Case is too conservative, in two regards:

1. The assumption that only 60% of the VAT cut gets passed through, whereas Copenhagen Economics, in their report for the European Commission on labour-intensive services4 concluded that full pass-through will be achieved.

2. The assumption that it would take 4 years to reach that position, compared to 2-3 years in Copenhagen Economics’ analysis.

Accordingly, we have also modelled a "rapid adjustment" scenario, where:

75% of the VAT reduction will pass through to lower prices, and

the full price adjustment will take a total of three years, with 50% of the full adjustment occurring in Year One, 80% in Year Two, and 100% by Year Three and thereafter.

4 Study on reduced VAT applied to goods and services in the Member states of the European Union.

Final Report by Copenhagen Economics, Thursday, 21 June 2007. http://ec.europa.eu/taxation_customs/resources/documents/taxation/vat/how_vat_works/rates/study_reduced_vat.pdf

VAT on Visitor Accommodation and Attractions in the UK 18

Such a scenario could occur if industry leaders gave a positive commitment to government that they would seek to pass at least 75% of the VAT reduction through in lower prices. The evidence from one country where such an agreement was entered into – Finland – is that it was honoured in practice, and consumers did indeed benefit from significantly lower prices as a result of a reduced VAT rate. Further reassurance could be provided by a Government commitment to retaining the lower rate of VAT provided that the reduction was passed through in lower prices, subject to review after three or four years.

4.6 Results – The Base Case Based upon these assumptions, the "comparative static" results indicate a net annual gain to the Exchequer from a VAT reduction of £45 million. A direct loss of VAT yields of £1.558 billion is offset by indirect gains from higher yields from income and corporation tax, savings in social security payments, a smaller shadow economy and multiplier effects. These indirect gains generate additional tax revenues of £1.603 billion in total. The net gain of £45 million compares to a net gain of £68 million computed in the 2011 model. The comparative 2014 and 2011 figures are shown in the Table below.

2014 2011

(1) Net direct loss of VAT receipts (£1,558.4) (£1,234.0)

(2) VAT Yield on increased turnover at 5% £85.0 £69.6

(3) VAT Yield on wider base at 5% £37.3 £33.6

(4) Income and national insurance derived from new jobs & previously unreported (Shadow Economy) jobs

£181.0 £161.6

(5) Income and national insurance derived from higher wages £49.9 £44.7

(6) Savings in social security payments £205.1 £155.2

(7) Corporation tax from higher margins on current turnover including previously unreported (Shadow Economy) turnover

£108.3

£86.1

(8) Corporation tax from higher turnover £85.7 £70.1

(9) Income tax paid on dividends £39.0 £32.9

(10) Business rates £28.4 -

(11) Multiplier impact £783.6 £656.8

Net fiscal impact £45.0 £67.6

VAT on Visitor Accommodation and Attractions in the UK 19

The Table above is based on a simple “before” and “after” comparison. In reality, transition to a post-VAT reduction equilibrium will not be instantaneous. There will be lags in the adjustment process:

firstly, it takes time for operators to pass through the VAT reduction in lower prices, and

secondly, it takes further time for consumers to respond to lower prices. The evidence from the French VAT reduction on restaurant meals in July 2009, and the German VAT reduction on hotel accommodation in January 2010, indicates that the first response of many operators will be to retain the proceeds of any VAT cut in higher profits. However, this is not an equilibrium position. Some operators will attempt to gain market share by reducing their prices, and this will provoke a competitive response from other operators, so tending to reduce prices over a period of approximately two years after a VAT reduction. Once operators begin to reduce their prices, it will take time for consumers to adjust their purchasing patterns in response to lower prices. The evidence from econometric analysis of the path of adjustment in tourism expenditure after a change in prices suggests the response time from consumers may take between 18 and 24 months. However, it is possible that this consumer response lag may be getting shorter, reflecting more efficient information flows as a result of the growth of the Internet, and a tendency for holidaymakers to book their holidays closer to the date of departure than 10 or 20 years ago, when holidays were often booked many months in advance. Taking these factors into account, we have estimated that 30 per cent of the total impact of a VAT reduction will be felt in the first year following the reduction, rising to 70 per cent in the second year, 90 per cent in the third year and 100 per cent by Year 4. The implication of this is that the full indirect and multiplied impact of a VAT reduction will take time to feed through, with the result that the Exchequer may suffer net losses in the years immediately following a VAT cut, because the loss of yield is not immediately offset by indirect and multiplied gains generated by the demand stimulus. However, once the effects of the VAT cut begin to feed through in lower prices and higher demand, the indirect gains from VAT deriving from a higher revenue base start to offset the direct loss of VAT yield. By Year 3 the net receipts to the Exchequer are greater than under a "no VAT change" scenario. Indirect fiscal gains are projected to increase over time compared with a no change baseline, because a VAT cut will provide a stimulus to the entire sector, as was seen in the Republic of Ireland following the VAT reduction there in the mid-1980s, and is currently being witnessed in France and Germany.

VAT on Visitor Accommodation and Attractions in the UK 20

Overall, the fiscal balance is approximately neutral after two to three years, and the Exchequer makes a net gain over a ten-year period, as shown in the chart below.

-£1,000.0

-£500.0

£0.0

£500.0

£1,000.0

£1,500.0

-1 0 1 2 3 4 5 6 7 8 9 10

Pre-cut Year ofCut

Post-Reduction Path of Adjustment

£ m

illio

n

Net fiscal impact (undiscounted)

From the chart, it will be seen that the Exchequer makes progressively greater gains compared to a "business as usual" scenario over time, because of the dynamic stimulus that lower VAT would give to sector growth and both domestic and inbound tourism. This would increase the UK's taxation base, not only for VAT, but also for income and corporation tax. The detailed year-by-year adjustment path is given in the Table overpage. It shows that, while the VAT cut would result in a net loss of revenues to the Exchequer in the first two years following the reduction, considered over the period as a whole a VAT reduction would generate a positive Net Present Value of £275 million in the first five years, and £3,862 million over the ten-year period.

VAT on Visitor Accommodation and Attractions in the UK 21

Pre-cut Year of Cut

Year -1 0 1 2 3 4 5 6 7 8 9 10

(1) Net direct loss of VAT receipts £0.0 £0.0 -£1,527.2 -£1,496.5 -£1,466.2 -£1,436.5 -£1,407.1 -£1,378.2 -£1,349.8 -£1,321.7 -£1,294.1 -£1,266.9

(2) VAT Yield on increased turnover at 5% £0.0 £0.0 £25.5 £59.5 £76.5 £85.0 £85.0 £85.0 £85.0 £85.0 £85.0 £85.0

(3) VAT Yield on wider base at 5% £0.0 £0.0 £11.2 £26.1 £33.6 £37.3 £37.3 £37.3 £37.3 £37.3 £37.3 £37.3

(4) Income and national insurance derived from new jobs &

previously unreported (Shadow Economy) jobs£0.0 £0.0 £64.1 £146.1 £191.8 £219.3 £228.5 £237.5 £246.5 £255.3 £263.9 £272.5

(5) Income and national insurance derived from higher wages £0.0 £0.0 £15.0 £34.9 £44.9 £49.9 £49.9 £49.9 £49.9 £49.9 £49.9 £49.9

(6) Savings in social security payments £0.0 £0.0 £79.1 £178.5 £236.6 £274.0 £290.5 £306.9 £323.0 £338.8 £354.4 £369.8

(7) Corporation tax from higher margins on current turnover

including previously unreported (Shadow Economy) turnover£0.0 £0.0 £205.0 £109.4 £98.4 £95.8 £95.8 £95.8 £95.8 £95.8 £95.8 £95.8

(8) Corporation tax from higher turnover £0.0 £0.0 £33.5 £75.5 £100.2 £116.2 £123.5 £130.8 £137.9 £145.0 £151.9 £158.7

(9) Income tax paid on dividends £0.0 £0.0 £14.2 £32.2 £42.4 £48.7 £51.0 £53.3 £55.6 £57.8 £60.0 £62.2

(10) Additional business rates £0.0 £0.0 £11.1 £25.0 £33.2 £38.5 £40.9 £43.3 £45.7 £48.0 £50.3 £52.6

(11) Multiplier impact £0.0 £0.0 £284.8 £647.3 £852.3 £978.2 £1,025.1 £1,071.2 £1,116.6 £1,161.4 £1,205.5 £1,248.9

Net fiscal impact (undiscounted) £0.0 £0.0 -£783.7 -£161.9 £243.7 £506.3 £620.4 £732.8 £843.5 £952.5 £1,059.9 £1,165.6

Check total £0.0 £0.0 -£783.7 -£161.9 £243.7 £506.3 £620.4 £732.8 £843.5 £952.5 £1,059.9 £1,165.6

Net fiscal impact (discounted) -£764.4 -£152.4 £221.4 £443.8 £524.8 £598.1 £664.3 £724.0 £777.4 £825.0

Cumulative fiscal impact (undiscounted) £0.0 £0.0 -£783.7 -£945.6 -£701.9 -£195.5 £424.9 £1,157.7 £2,001.1 £2,953.6 £4,013.5 £5,179.1

Cumulative fiscal impact (discounted) -£764.4 -£916.8 -£695.4 -£251.6 £273.2 £871.3 £1,535.6 £2,259.6 £3,037.0 £3,862.0

Additional jobs directly created 0 0 9,463 21,346 28,294 32,759 34,741 36,694 38,617 40,512 42,378 44,217

Total Direct Jobs Impact 0 0 15,771 35,577 47,156 54,598 57,902 61,157 64,362 67,520 70,630 73,694

Multiplied Jobs 0 0 10,567 23,836 31,595 36,580 38,794 40,975 43,123 45,238 47,322 49,375

Total Direct and Multiplied Jobs Impact 0 0 26,338 59,413 78,751 91,178 96,696 102,131 107,485 112,759 117,953 123,069

First 5 years First 10 Years

Net Present Value , £ mill ion £275 £3,862

Economic Rate of Return, % 12.8% 41.2%

Post-Reduction Path of Adjustment

VAT on Visitor Accommodation and Attractions in the UK 22

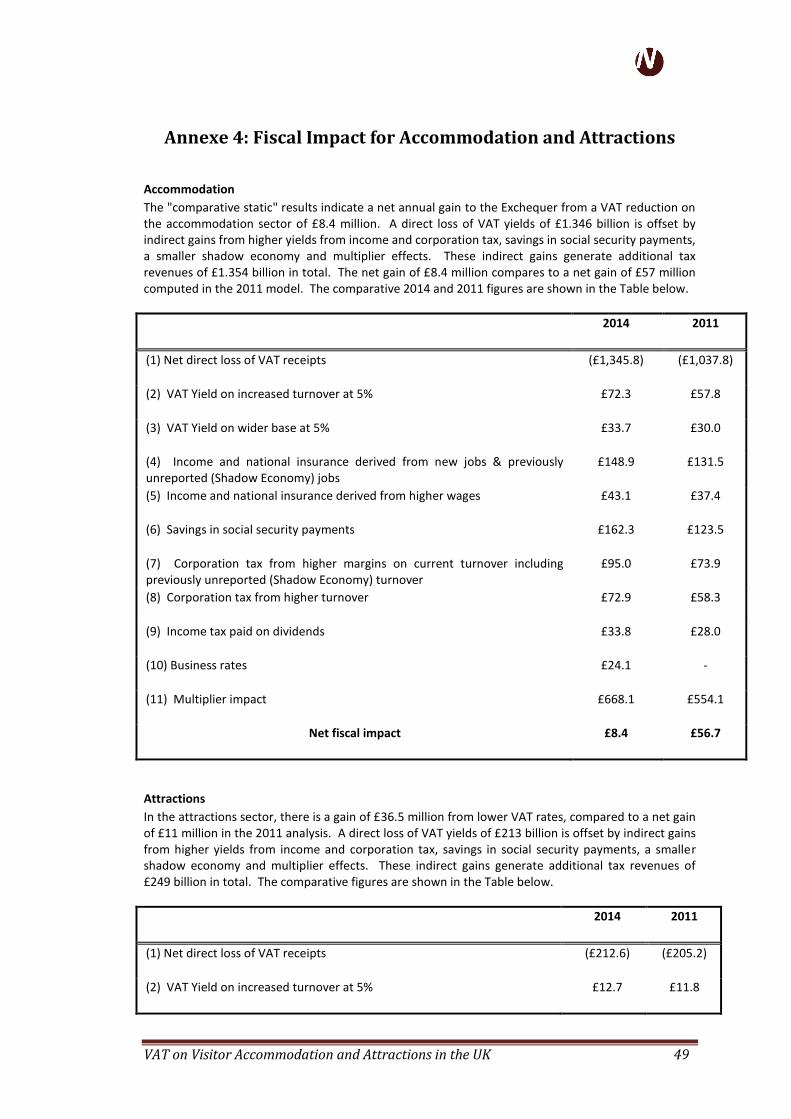

4.7 The Overall Picture In total, on a comparative-static basis, the Exchequer would achieve a net gain of £45 million p.a. by reducing VAT on accommodation and attractions. Of this amount, £8.5 million will be generated by visitor accommodation, and £36.5 million by visitor attractions. The results for accommodation and attractions considered separately are set out in Annexe 4. The source of the gains excluding business rates, as computed in the DPE fiscal model, is shown in the chart overpage.

The chart illustrates the full direct and indirect fiscal impact of lower tourism VAT as follows:

lower tourism VAT is passed through in lower prices to the consumer;

over time, as a consequence, tourism demand – from both domestic and foreign visitors – goes up;

tourism supply rises to meet this demand – generating extra wages and profits in the tourism sector;

this leads to a positive direct economic contribution to UK GDP, and extra tax revenue from income and corporation taxes, along with savings in benefit payments to workers who secure jobs in tourism services, who were previously unemployed;

tourism businesses buy more services from suppliers – an indirect effect, captured through the multiplier, generating extra tax revenue from suppliers;

in addition, people who work in the sector will spend their extra wages in non-tourism businesses – an induced effect, also captured through the multiplier, and generating extra tax revenue from those businesses.

VAT on Visitor Accommodation and Attractions in the UK 23

VAT on Visitor Accommodation and Attractions in the UK 23

VAT on Visitor Accommodation and Attractions in the UK iii

VAT on Visitor Accommodation and Attractions in the UK 24

The multiplier The last two effects – the indirect effect of greater purchases from suppliers, and the induced effect of spending by workers in the accommodation and attractions sector on incomes and jobs in other sectors – are captured through the multiplier. Our estimate of the multiplier impact of a reduction in taxes is based on Oxford Economics’ estimate of a tourist multiplier of 1.7 in their study of the economic contribution of the UK hospitality industry for the British Hospitality Association (Hospitality: driving local economies, 2010). A more recent estimate by Deloitte, in their 2012 report for VisitBritain, Tourism: Jobs and Growth (2014), estimates a Gross Value Added (GVA) multiple of 2.8 – i.e., each £1 of value directly added by tourism for the UK economy generates £1.80 of indirect or multiplied value-added further down the supply chain. Deloitte estimate that tourism’s direct contribution to the UK economy is currently worth £58 billion per annum in direct GVA, with an indirect contribution of just under £69 billion, with the sector supporting 3.1 million jobs in total. The impact on lower VAT on overseas and domestic tourism We estimate that approximately half of the increased fiscal revenues to the Exchequer will be generated by overseas tourists, who currently account for approximately 45% of all expenditure on visitor accommodation in the UK. In addition, some of the increase in tax receipts will be generated by UK residents who would otherwise have travelled abroad on holiday. Thus, overall, the effect of a lower VAT rate will be to increase the base upon which taxation is levied, and the UK’s net foreign exchange earnings from tourism. In a speech on 17th August 2010, the Prime Minister, David Cameron, challenged the travel industry to raise British residents’ holiday expenditure within the UK from 36% to 50%, and correspondingly reduce the proportion spent abroad from 64% to 50%. In the succeeding two years, the proportion of domestic tourism expenditure by UK residents did indeed increase to just over 40% of all tourism expenditure by UK residents, thus moving in the direction that the PM wished. However, the “staycation” effect witnessed in 2011-2013 may be a temporary phenomenon. There is some evidence that the proportion of total tourism expenditure by UK residents on holidays overseas is beginning to rise once more in 2014, driven by underlying economic recovery and the appreciation of the £ Sterling against both the euro and the dollar. There is a risk that, under a "no VAT change" scenario, the proportion of total tourism expenditure by UK residents abroad will continue to rise. This would have a negative impact on the UK's external Tourism Balance, which measures the difference between the UK’s receipts from international visitors and expenditure by UK residents on visits abroad.

VAT on Visitor Accommodation and Attractions in the UK 25

The Tourism Balance improved from a deficit of £20.5 billion in 2008, when UK residents spent £36.8 billion on visits abroad against earnings of £16.3 billion from overseas visitors to Britain, to:

£13.7 billion in 2011;

£13.8 billion in 2012; and

£13.9 billion in 2013, when outbound spend by UK residents was £34.9 billion against inbound receipts of £21.0 billion.

A reduction in VAT, by encouraging more UK residents take their holidays at home and more overseas visitors to come into the UK, could help to sustain the improvement in the UK’s Tourism Balance and strengthen the UK’s taxation base.

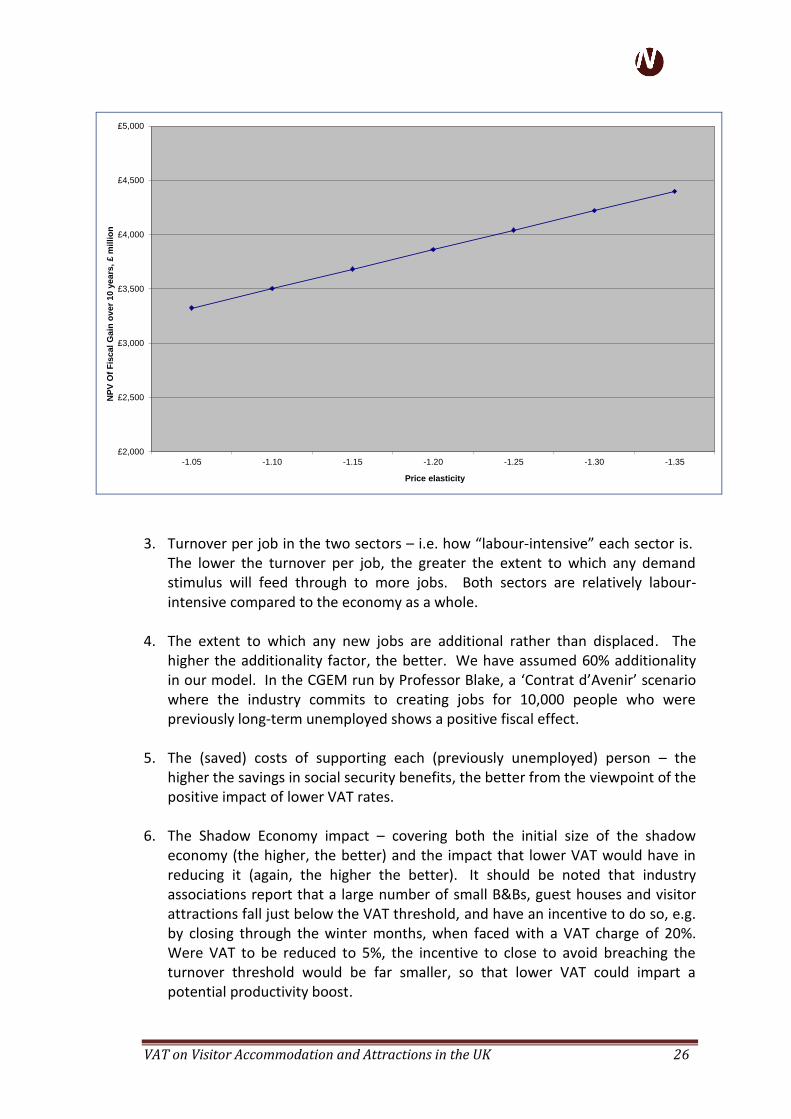

4.8 Key Sensitivities The assumptions that drive the overall fiscal impact are as follows: 1. The assumptions made regarding the pass-through of the VAT reduction, and in

particular how much of the reduction is passed through in lower prices – the more, the better.

2. The estimated price sensitivity of demand – or the extent to which any price

reduction stimulates an increase in demand – the higher, the better. A series of sensitivity tests were run to estimate the Net Present Value (NPV) of a VAT reduction in terms of the net fiscal gains to the Exchequer over a ten-year time horizon, assuming a price elasticity of demand ranging from -1.00 (the low case, under which a 5% reduction in prices feeds through to a 5% increase in sales) to -1.35 (the high case, under which a 5% reduction in prices feeds through to a 6.75% increase in sales).

The results are shown in the chart overpage, and indicate that the NPV to the Exchequer would be £3.3 billion with a price elasticity of demand (Epd) of -1.05, rising to £4.4 billion with an Epd of -1.35. So even in the low case, the results would be positive from the Exchequer’s viewpoint.

VAT on Visitor Accommodation and Attractions in the UK 26

£2,000

£2,500

£3,000

£3,500

£4,000

£4,500

£5,000

-1.05 -1.10 -1.15 -1.20 -1.25 -1.30 -1.35

NP

V O

f F

isc

al

Ga

in o

ve

r 1

0 y

ears

, £

mil

lio

n

Price elasticity

3. Turnover per job in the two sectors – i.e. how “labour-intensive” each sector is. The lower the turnover per job, the greater the extent to which any demand stimulus will feed through to more jobs. Both sectors are relatively labour-intensive compared to the economy as a whole.

4. The extent to which any new jobs are additional rather than displaced. The

higher the additionality factor, the better. We have assumed 60% additionality in our model. In the CGEM run by Professor Blake, a ‘Contrat d’Avenir’ scenario where the industry commits to creating jobs for 10,000 people who were previously long-term unemployed shows a positive fiscal effect.

5. The (saved) costs of supporting each (previously unemployed) person – the

higher the savings in social security benefits, the better from the viewpoint of the positive impact of lower VAT rates.

6. The Shadow Economy impact – covering both the initial size of the shadow

economy (the higher, the better) and the impact that lower VAT would have in reducing it (again, the higher the better). It should be noted that industry associations report that a large number of small B&Bs, guest houses and visitor attractions fall just below the VAT threshold, and have an incentive to do so, e.g. by closing through the winter months, when faced with a VAT charge of 20%. Were VAT to be reduced to 5%, the incentive to close to avoid breaching the turnover threshold would be far smaller, so that lower VAT could impart a potential productivity boost.

VAT on Visitor Accommodation and Attractions in the UK 27

The chart below measures the relationship between HMT’s fiscal gains over 10 years and percentage reduction in the size of the Shadow Economy, which is the value of sector turnover falling outside the VAT regime, whether legally – as in the case of businesses that fall below the VAT threshold – or otherwise. It indicates that the net fiscal impact is quite sensitive in response to changes in the size of the Shadow Economy.

£0

£500

£1,000

£1,500

£2,000

£2,500

£3,000

£3,500

£4,000

£4,500

£5,000

5% 10% 15% 20% 25% 30% 35% 40%

% reduction in the Shadow Economy with VAT at 5% rather than 20%

NPV of fiscal gain over 10 years, £m

4.9 Results – The Rapid Reduction Scenario Under the rapid reduction scenario, it is assumed that more of the VAT cut is passed in lower prices – 75%, compared to 60% of the base case – and that full adjustment occurs within three years. On this basis, the "comparative static" results indicate a small net loss to the Exchequer from a VAT reduction of £18 million. A direct loss of VAT yields of £1.558 billion is offset by indirect gains that generate additional tax revenues of £1.540 billion in total – i.e. slightly lower than in the base case. The comparative figures for the Base Case and the Rapid Reduction scenario are shown in the Table below.

Base Case Rapid Reduction

(1) Net direct loss of VAT receipts (£1,558.4) (£1,558.4)

(2) VAT Yield on increased turnover at 5% £85.0 £83.7

(3) VAT Yield on wider base at 5% £37.3 £37.3

(4) Income and national insurance derived from new jobs & previously unreported (Shadow Economy) jobs

£181.0 £179.2

(5) Income and national insurance derived from higher wages

£49.9 £31.2

VAT on Visitor Accommodation and Attractions in the UK 28

Base Case Rapid Reduction

(6) Savings in social security payments £205.1 £201.7

(7) Corporation tax from higher margins on current turnover including previously unreported (Shadow Economy) turnover

£108.3

£81.8

(8) Corporation tax from higher turnover £85.7 £84.3

(9) Income tax paid on dividends £39.0 £38.6

(10) Business rates £28.4 £27.9

(11) Multiplier impact £783.6 £775.0

Net fiscal impact £45.0 -£17.7

The Table above is based on a simple “before” and “after” comparison. On the face of it, the results that there is a lesser net gain to the Exchequer than under the Base Case seems counter-intuitive. However, it arises as a result of lower investment, and a lower enhancement in sector wages – and as a result, the net gain from corporation tax and from income tax on higher wages is much lower under a scenario where 75% of any VAT reduction is passed through in lower prices. As shown in table:

The gain in income tax and National Insurance receipts from higher wages is £31.2 million under the rapid adjustment scenario, compared to £49.9 million in the Base Case – i.e. £18.7 million less, while

The gain in corporation tax receipts from higher margins falls from £108.3 million to £81.3 million – i.e. £27 million less.

If 75% of a VAT cut is passed through in lower prices, there is less scope to use part of the reduction for enhanced wages and working conditions, or for greater margins. And if margins are less, there is less funding available for greater investment. On the assumptions in the model, greater investment would stimulate greater sales – so lower investment results in a loss in sales growth compared to the Base Case. This tends to counter the beneficial demand stimulus provided by lower prices. One implication could be that, if a "Contract for the Future" were agreed between the government, the industry, and union representatives, it might be better to agree a balanced allocation of any VAT reduction, to include greater investment and enhanced working terms and conditions, rather than insisting that all of the reduction be passed through in lower prices. In terms of the dynamic response to a VAT reduction, the rapid reduction scenario shows the initial fiscal loss to HMT is less, and the balance becomes positive, more rapidly than under the Base Case, and the Exchequer makes a net gain over a ten-year period, as shown in the chart below.

VAT on Visitor Accommodation and Attractions in the UK 29

-£800.0

-£600.0

-£400.0

-£200.0

£0.0

£200.0

£400.0

£600.0

£800.0

£1,000.0

£1,200.0

-1 0 1 2 3 4 5 6 7 8 9 10

Pre-cut Year ofCut

Post-Reduction Path of Adjustment

£ m

illio

n

Net fiscal impact (undiscounted)

From the chart, it will be seen that the Exchequer makes progressively greater gains compared to a "business as usual" scenario over time, because of the dynamic stimulus that lower VAT would give to sector growth and both domestic and inbound tourism. Considered over a 10-year period, a VAT cut under the rapid reduction scenario would generate a positive Net Present Value of £515 million in the first five years compared to £275 million in the Base Case – i.e. the Treasury recovers its investment more quickly than in the base case. Over 10 years, the NPV is £3,892 million, compared to £3,862 million in the Base Case.

4.10 Results – The position after four years In Year 4 following a reduction – by which time most of the adjustment to lower VAT rates has occurred – the analysis indicates the following impact on tax yields:

Impact on the Exchequer’s Position Base Case Rapid Reduction

2011, £m

(1) Net direct loss of VAT receipts -£1,436.5 -£1,436.5 -£1,145.8

(2) VAT Yield on increased turnover at 5% £85.0 £83.7 £67.1

(3) VAT Yield on wider base at 5% £37.3 £37.3 £33.6

(4) Income and national insurance derived from new jobs & previously unreported (Shadow Economy) jobs

£219.3 £217.4 £176.2

VAT on Visitor Accommodation and Attractions in the UK 30

Impact on the Exchequer’s Position Base Case Rapid Reduction

2011, £m

(5) Income and national insurance derived from higher wages £49.9 £31.2 £38.5

(6) Savings in social security payments £274.0 £270.5 £164.5

(7) Corporation tax from higher margins on current turnover including previously unreported (Shadow Economy) turnover

£95.8 £76.9 £90.6

(8) Corporation tax from higher turnover £116.2 £114.9 £95.2

(9) Income tax paid on dividends £48.7 £48.3 £40.9

(10) Additional business rates £38.5 £38.1 -

Sub-total, direct and indirect fiscal impact -£471.8 -£518.2 -£439.1

(10) Multiplier impact £978.2 £969.6 £753.7

Net fiscal impact £506.4 £451.4 £314.6

VAT on Visitor Accommodation and Attractions in the UK 31

5 Conclusions

The central conclusions of this report may be summed up as follows: 1. The UK charges a comparatively high rate of VAT on visitor accommodation and

attractions. The UK is one of only four EU member states that charges the full standard rate of VAT on visitor accommodation, and the British VAT rate is almost twice the average rate on accommodation applying across the European Union. The differential is less acute in the case of attractions, but the UK rate of 20% applying to amusement parks is still 27% higher than the current EU average of 15.7%.

2. The high VAT rate imposed on accommodation and attractions represents a

significant competitive disadvantage to the British tourist industry compared to its European competitors.

3. The government appears to not accept this, citing the UK’s good tourism

performance in recent years. While it is true that UK tourism performed relatively well in the years between 2011 and 2013, when the very substantial deficit on the UK's Tourism Balance fell, this could be a purely temporary phenomenon reflecting domestic economic recession and a weak £, which may be reversed in 2014 and beyond.

4. Under a "business as usual" VAT scenario, it is likely that the UK's share of the

international tourism market will continue to contract. By contrast, a reduction in the VAT rate will stimulate the growth in overseas tourism to Britain, and domestic tourism, helping to increase the taxation base.

5. Because of the highly price sensitive nature of the sector, lower VAT rates that

feed through to lower prices will stimulate higher turnover and employment. This in turn will increase income and corporation tax receipts and reduce benefit payments. Overall, when both the direct and indirect effects of a lower VAT rate are taken into account, our estimates indicate that there will be a net £106 million gain for the Exchequer. This gain would increase year-or-year over a 10-year horizon, because of the dynamic gains that would accrue to the sector compared to a Business as Usual scenario where VAT continues to be levied at 20%.

6. In summary, a lower VAT rate would represent a "win-win" strategy – helping to

stimulate Britain's tourism industry, increase foreign exchange earnings, create additional jobs, and generate a net fiscal gain for Her Majesty's Treasury. On this basis, we believe that the case for lower VAT on tourism services merits further consideration by Her Majesty’s Treasury.

VAT on Visitor Accommodation and Attractions in the UK 32

VAT on Visitor Accommodation and Attractions in the UK 33

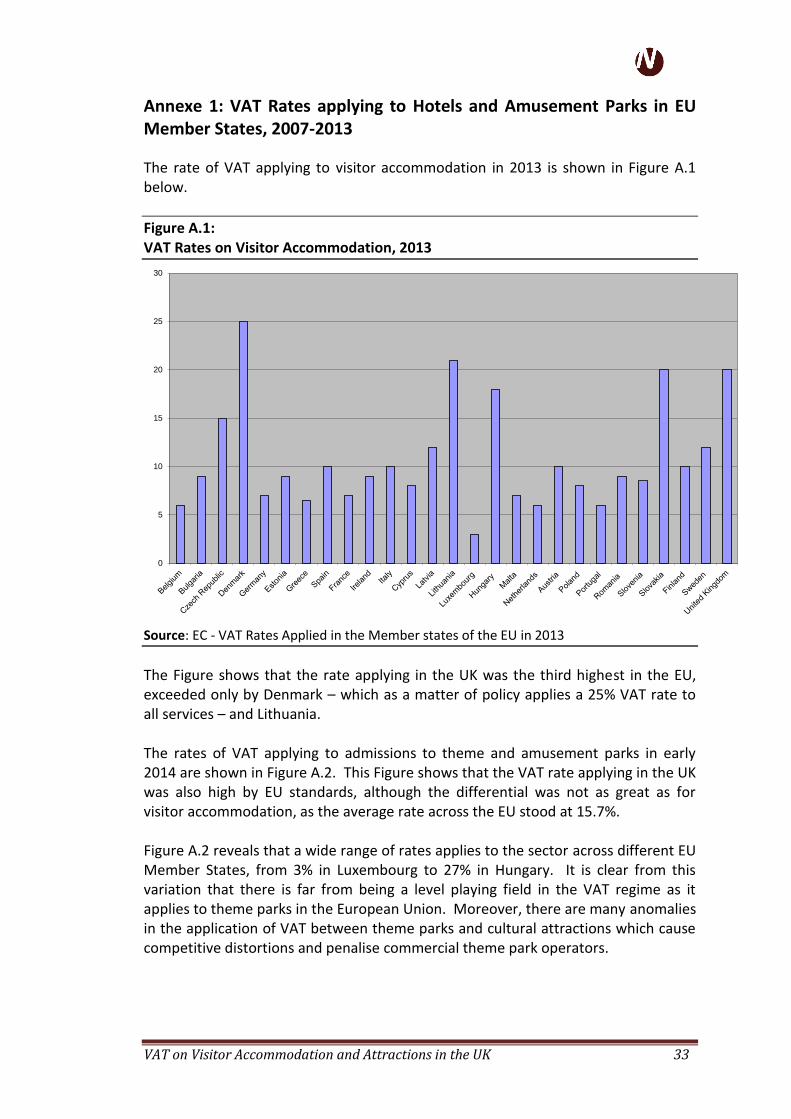

Annexe 1: VAT Rates applying to Hotels and Amusement Parks in EU Member States, 2007-2013

The rate of VAT applying to visitor accommodation in 2013 is shown in Figure A.1 below.

Figure A.1: VAT Rates on Visitor Accommodation, 2013

0

5

10

15

20

25

30

Source: EC - VAT Rates Applied in the Member states of the EU in 2013

The Figure shows that the rate applying in the UK was the third highest in the EU, exceeded only by Denmark – which as a matter of policy applies a 25% VAT rate to all services – and Lithuania. The rates of VAT applying to admissions to theme and amusement parks in early 2014 are shown in Figure A.2. This Figure shows that the VAT rate applying in the UK was also high by EU standards, although the differential was not as great as for visitor accommodation, as the average rate across the EU stood at 15.7%. Figure A.2 reveals that a wide range of rates applies to the sector across different EU Member States, from 3% in Luxembourg to 27% in Hungary. It is clear from this variation that there is far from being a level playing field in the VAT regime as it applies to theme parks in the European Union. Moreover, there are many anomalies in the application of VAT between theme parks and cultural attractions which cause competitive distortions and penalise commercial theme park operators.

VAT on Visitor Accommodation and Attractions in the UK 34

Figure A.2: VAT Rates on Admissions to Amusement Parks in EU Member States, January 2014

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

EU Average @ January 2014 = 15.7%

Source: EC - VAT Rates Applied in the Member states of the EU as at 13 January 2014

The Table below shows the standard rate (in the right-hand column) and also the rate of VAT applying to accommodation and amusement park operators between 2007 and 2013.

The Evolution of VAT Rates across the EU, 2007-2013 (in alphabetical order by Member State)

Member State Year Hotels Amusement parks

Standard Rate

Austria 2013 10 10 20

2012 10 10 20

2011 10 10 20

2010 10 10 20

2009 10 10 20

2008 10 10 20

2007 10 20 20

Belgium 2013 6 6 21

2012 6 6 21

2011 6 6 21

2010 6 6 21

2009 6 6 21

2008 6, ex 6 21

VAT on Visitor Accommodation and Attractions in the UK 35

Member State Year Hotels Amusement parks

Standard Rate

2007 6, ex 6 21

Bulgaria 2013 9 20 20

2012 9 20 20

2011 7%, 20% 20 20

2010 7%, 20% 20 20

2009 7%, 20% 20 20

2008 7%, 20% 20 20

2007 7%, 20% 20 20

Cyprus 2013 8 5 18

2012 8 5 15

2011 5 15 15

2010 5 15 15

2009 8 15 15

2008 8 15 15

2007 15

Czech Republic 2013 15 15 21

2012 14 14 20

2011 10 10 20

2010 10 10 20

2009 9 9 19

2008 5 5 19

2007 5 5 19

Denmark 2013 25 25 25

2012 25 25 25

2011 25 25 25

2010 25 25 25

2009 25 25 25

2008 25 25 25

2007 25 25 25

Estonia 2013 9 20 20

2012 9 20 20

2011 9 20 20

2010 9 20 20

2009 5 18 18

2008 5 18 18

2007 18

Finland 2013 10 10 24

VAT on Visitor Accommodation and Attractions in the UK 36

Member State Year Hotels Amusement parks

Standard Rate

2012 9 9 23

2011 9 9 23

2010 8 8 22

2009 8.5 8 22

2008 8 8 22

2007 8 8 22

France 2013 7 7%, 19.6% 19.6

2012 7 7%, 19.6% 19.6

2011 5.5 5.5% 19.6% 19.6

2010 5.5 5.5% 19.6% 19.6

2009 5.5 5.5% 19.6% 19.6

2008 5.5 5.5% 19.6% 19.6

2007 5.5 5.5% 19.6% 19.6

Germany 2013 7 19 19

2012 7 19 19

2011 7 19 19

2010 7 19 19

2009 19 19 19