ISO 26000 and social audit expert training folder Sept final

Upload

horace-curtisCategory

view

217download

1

The Expert in Tax Education

The Expert in Tax Education

How to Survive an Audit

How to Survive an Audit

Developed by Alan L Pinck, EA

Presented by XXXX

Summer 2014

The Process

• Recognizing that there is an audit is the first step

• There are 3 basic types of audits:

Field, Office and Correspondence

• The letter the taxpayer receives tells you what type of audit you are facing

• Understanding the process is key to being successful

2205-A The Field Audit

• Issued by the Revenue Agent (RA) this is the more complex type of audit

• This audit will be held where the records are

• The audit will take at least a couple of days and some RA’s will want to schedule 2 consecutive days at once

3572 The Office Audit

• Issued by a Tax Compliance Officer (TCO)

• Audit is conducted in the IRS office

• Generally limited to a few items

• Letter will say what is being audited

• Audit generally takes only a few hours to complete if well organized

CP 2000 Correspondence Audit

• Letter is generated at the service center

• The most common type of audit

• Generally pertains to unreported income or deduction that is not on record at the IRS

• Letter will give 30 days to respondPractice tip; If the audit is for something that needs

to be done in person request a change of venue.

Power of Attorney

• In order to speak on the taxpayers behalf while under audit a Power of Attorney needs to be filed

• Form 2848 is what you will need to fill out, have the taxpayers sign and fax it to the auditor

Contacting the Auditor

• Review the initial letter to be sure you understand what the audit is about

• Call the auditor and discuss the case as well as set up an appointment.

• Ask for an Information Document Request (IDR)

• Be sure to allow enough time for you and your client to organize the requested documents

Meeting the Auditor

• The auditor will ask if the taxpayer is aware of their rights and did they receive Pub. 3498

• Next will be a series of questions about the taxpayer

• Last will be producing the documents to support the items on the return in question

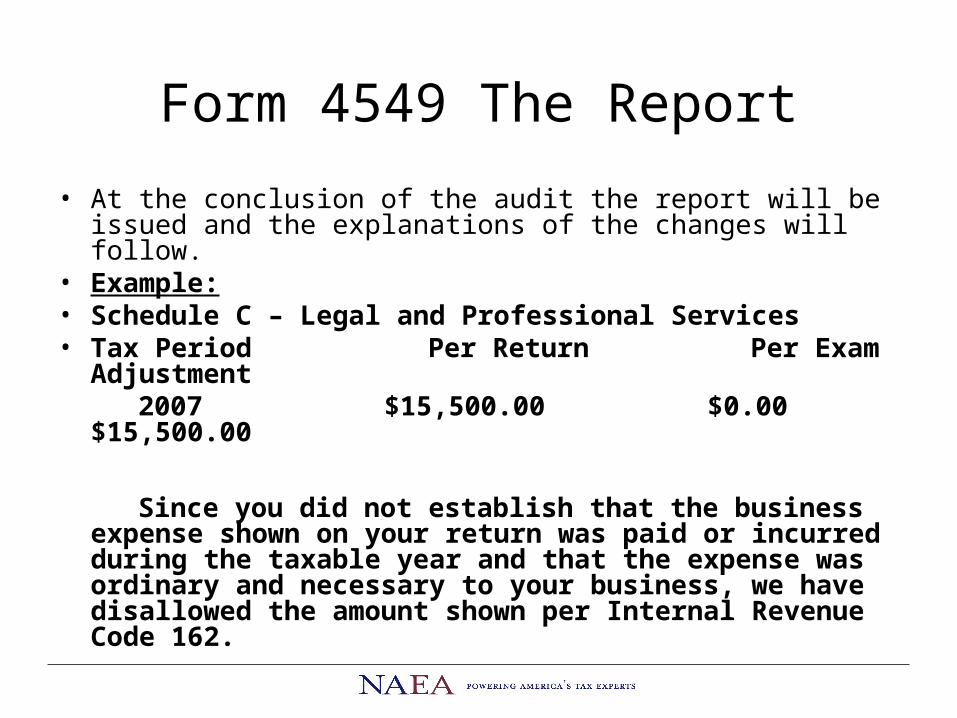

Form 4549 The Report

• At the conclusion of the audit the report will be issued and the explanations of the changes will follow.

• Example:• Schedule C – Legal and Professional Services• Tax Period Per Return Per Exam

Adjustment 2007 $15,500.00 $0.00 $15,500.00

Since you did not establish that the business expense shown on your return was paid or incurred during the taxable year and that the expense was ordinary and necessary to your business, we have disallowed the amount shown per Internal Revenue Code 162.

Representation Toolbox

• Now that you understand the process let’s discuss the things you need in your “Toolbox” in order to be comfortable with what you are doing.

Engagement Letter

• Be sure to spell out what it is that you will be doing and what the Taxpayer is responsible for

• Clearly define the fee and payment method

Power Of Attorney

• You cannot speak for your client with out the POA on file with the IRS

• Include all open years on the POA. It makes your ability to represent more effective if the audit expands to another year

Audit Interview Sheets

• The first part of the audit is Q&A, be sure you know who you are representing

• An income probe is always part of the process so be sure to get that information

• No matter how many questions I think to ask, the auditor will come up with more

• Be sure to update your interview sheet regularly

Organized Records

• If you want to get the audit closed fast then be well prepared

• Organize the records in the same order as they appear on the IDR

• Include a total page spreadsheet or calculator tape to each category

Acceptable Backup

• The receipt and the form of payment• If a credit card is used be sure to show the

Taxpayer is the holder of the card• When a receipt is from a store such as

Costco it will be needed.• When no receipt is present it will be at the

auditors discretion to allow• Note; though they want original receipts the

auditors understand that originals do not hold up well, and will accept copies in most cases

Mileage Log

• Whether claiming standard mileage rate or actual expenses a mileage log is needed

• The more detail the better; who where and why

• The total mileage driven will also need to be supported, have repair receipts available to show the odometer reading

Let the Auditor Set the Pace

• The auditor will let you know what they want and in what order

• They may not always ask for everything that you prepared so be patient

• The more organized and complete the documents are the less likely that they will look at everything

Do Not Let the Auditor Control the Audit

• We are playing in their ball park but we still are able to control the action

• When dealing with an aggressive auditor be on your toes

• Be sure to let them know that you are both there to be sure that a properly filed return is the end result

Never Take it Personally

• Remember you are representing the return• If you prepared it you did so using your

expertise and their information• If you did not prepare it then you have no

reason to be defensive, you are simply using the information you have been provided

• The auditor will generally leave the door open to look into other areas of the tax return that are not initially under audit. Do not provide that incentive.

Follow-up Information

• When more documentation is requested there is generally only 10-15 days to provide it

• Gather and present the information timely• Do not be surprised to see at the bottom of

the IDR “Other information may be requested during the course of the audit”

• To help prevent this have everything the first time and be well organized

Handling a Disagreement

• Try to state your position with the auditor• Request a managers conference• Take the case to Appeals • Petition Tax CourtNote: if there is a balance due, it continues to accumulate interest until it is paid. To

stop the interest from compounding, the taxpayer is entitled to post a cash bond by sending in the tax payment and requesting it be held as a bond. When the taxpayer prevails the bond will be fully refunded, unless taxpayer only partially prevails, in which case the refund will be adjusted accordingly. Prepayment is a consideration if the taxpayer plans on appealing an issue that might not win completely. With the lengthy appeals process, a lot of interest could accrue.

Finishing the Case

• If you and the taxpayer agree with the findings sign the 4549 and send it back to the auditor

• If the taxpayer cannot pay the balance due in full be sure to send the report back anyway, and they will be billed for the balance

• Note; even though the report will give the taxpayers options in making payments I recommend they wait for the bill and set it up through the collections unit

Finishing With the Client

• Review the findings and be sure they understand what happened

• Inform the client that the IRS will notify the state when there is a change so they need to amend their state returns accordingly

• Return the taxpayers supporting documents

• Collect the balance of your fee

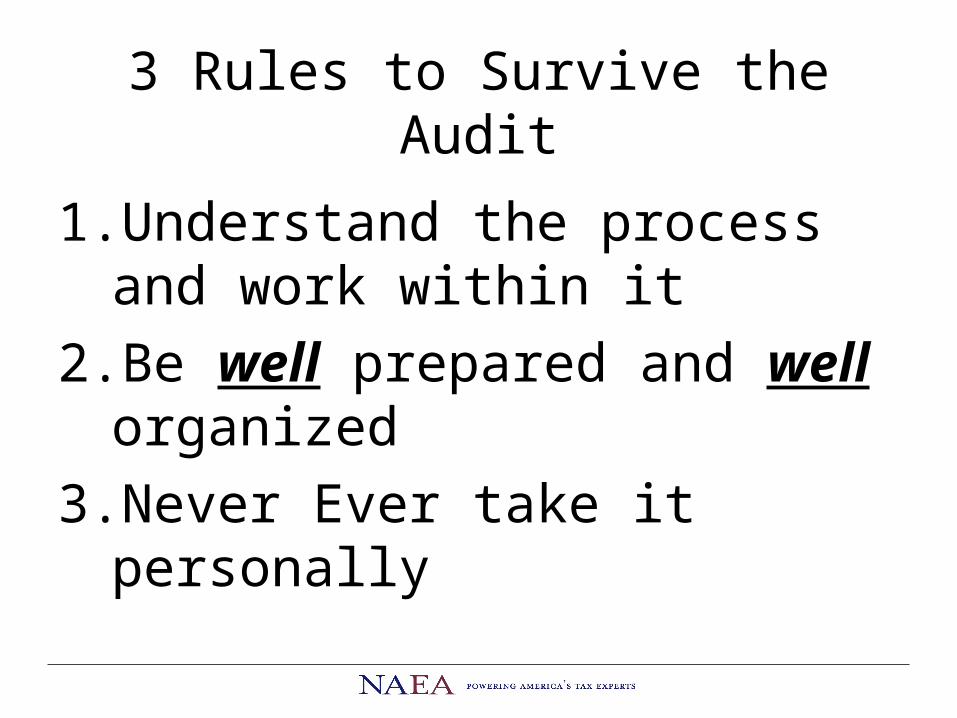

3 Rules to Survive the Audit

1. Understand the process and work within it

2. Be well prepared and well organized

3. Never Ever take it personally

Presentation developed by Alan L. Pinck, EA

Alan Pinck, EA is currently the NAEA Education Committee chair and has previously held board positions including president of the Mission Society of Enrolled Agents. He has taught at the CSEA Super Seminar and teaches a Part 2 SEE preparation class. His practice in the San Francisco Bay area specializes in personal and business tax return preparation as well as audit representation. Pinck serves as an instructor for Level 2 and the Graduate Level in Representation.

A. Pinck & Associates

2021 The Alameda Suite 280

San Jose, CA 95126

(408) 298-7199

www.apincktax.com

NAEA created this educational program as part of its firm commitment to providing up-to-date, convenient continuing education that focuses on the issues that members identify as top priorities. Members are invited to suggest further areas of study or to submit presentations by contacting [email protected].

National Association of Enrolled Agents1730 Rhode Island Ave, NW Ste 400Washington, DC 20036Toll free: 855-880-NAEAwww.naea.org