The Enron Affair EMBA 21 Program, 2003 Prof. L.J. Brooks.

30

The Enron Affair EMBA 21 Program, 2003 Prof. L.J. Brooks

-

date post

19-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of The Enron Affair EMBA 21 Program, 2003 Prof. L.J. Brooks.

The Enron Affair

EMBA 21 Program, 2003Prof. L.J. Brooks

L.J. Brooks, Rotman School of Management, University of Toronto 2

Overview Management was:

out of control, and engaged in self-dealing manipulating transactions & financial

reports Company imploded - Chap. 11 in Dec. 2001 Investors misled, pensions lost Executives plead the 5th, poor memory,

ignorance, incompetence Outrage Auditor savaged, profession to be changed

L.J. Brooks, Rotman School of Management, University of Toronto 3

Enron Stock Chart

Source: www.globe investor.com

Weekly Prices 1997- 2002

L.J. Brooks, Rotman School of Management, University of Toronto 4

Enron’s Business (10K-2000) Transportation and distribution Wholesale services

Commodity sales & services, risk management products, plants, etc

Retail energy services - gas, electricity Broadband services

Nationwide fiber-optic network - build, market, etc.

Corporate and other operation of water, renewable energy, and clean

fuels plants plus other corporate activities

L.J. Brooks, Rotman School of Management, University of Toronto 5

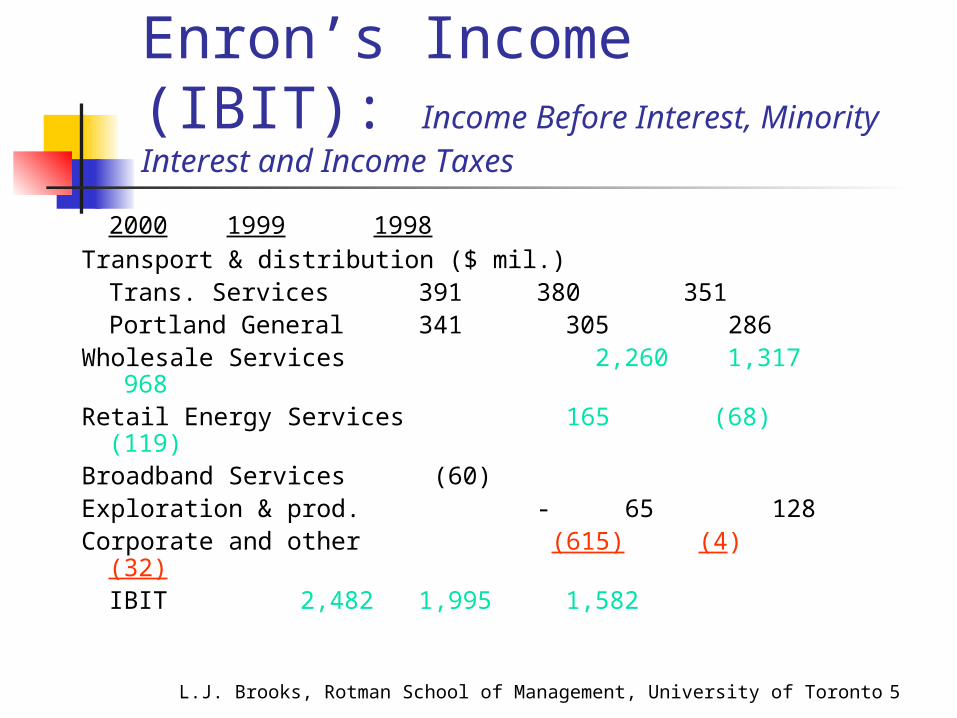

Enron’s Income (IBIT): Income Before Interest, Minority Interest and Income Taxes

2000 1999 1998Transport & distribution ($ mil.)

Trans. Services 391 380 351Portland General 341 305 286

Wholesale Services 2,260 1,317 968Retail Energy Services 165 (68) (119)Broadband Services (60)Exploration & prod. - 65 128Corporate and other (615) (4)

(32)IBIT 2,482 1,995 1,582

L.J. Brooks, Rotman School of Management, University of Toronto 6

Enron’s Wholesale Services

…creation of networks involving selective asset ownership, contractual access to third-party assets and market-making activities. 10K p.36.

…uses portfolio and risk management disciplines, including offsetting or hedging transactions, to manage exposures to market price movements (commodities, interest rates, foreign currencies and equities).

10K p.37. …sells interests in certain investments and

other assets to improve liquidity and overall return, 10K p.37

L.J. Brooks, Rotman School of Management, University of Toronto 7

Enron’s Financial Data2000 19991998

Revenues (in Billions) 100.8 40.1 31.3

Operating income (Millions) 1,953 802 1,378IBIT 2,482 1,995 1,582Net Income before Cumulative

Accounting Changes 979 1,024 703Net Income 979 893 703

EPS (in dollars) - basic 1.22 1.17 1.07

- diluted 1.12 1.10 1.01

L.J. Brooks, Rotman School of Management, University of Toronto 8

Enron’s Financial Data2000 1999

Current assets (Billions) 30.4 7.3Investments, other 23.4 15.4Property, plant, equip, net 11.7 10.7

Total Assets 65.5 33.4Current liabilities 28.4 6.8Long-term Debt 8.6 7.2Deferred credits and other 13.8 6.5Shareholders’ Equity 11.5 9.6

Total Liab. & Shareholders’ Equity 65.5 33.4

L.J. Brooks, Rotman School of Management, University of Toronto 9

Enron’s Changing Risk Profile

Early By Risk 1990’s 2000 Level

Pipelines, distribution networks LowRetail energy LowPower generation LowOil and gas exploration Med.Alternative energy M/HHedging transactions HighCommodity trading transactions HighBroadband optical fiber networks V.

High

Related party transact. (SPEs/Partnerships) ???

L.J. Brooks, Rotman School of Management, University of Toronto 10

Corporate Governance

Role of the Board of Directors - traditional strategic objectives - set or approve appoint CEO, approve other officers company policies and procedures:

set or approve ensure dissemination and compliance

laws, regulations, & expectations of society ensure monitoring and compliance act as ethical conscience (Dey Report & CICA)

L.J. Brooks, Rotman School of Management, University of Toronto 11

Role of the Board of Directors, cont’d

“to supervise, direct or oversee”…”day-to-day management must be delegated to others” Dey Report (1994)

5 core functions (CICA/TSE, 2001): Choosing the CEO and ensuring the team is sound Setting the broad parameters the management team

operates within Coaching the CEO and team Monitoring and assessing the performance of the CEO,

setting the CEO’s compensation and approving the team’s Providing assurance to shareholders and stakeholders

about the integrity of the corporation’s financial performance, incl. Quarterly Reports.

L.J. Brooks, Rotman School of Management, University of Toronto 12

Audit Committee must:(CICA/TSE, 2001)

Provide assurance that external auditors: are independent are satisfied accounting estimates and judgments are

sound and in accord with GAAP Develop sufficient rapport with external and

internal auditors, and management to facilitate Approve mandate of internal audit group, and

ensure it has adequate resources to ensure an effective internal control framework and culture

Disclose mandate

L.J. Brooks, Rotman School of Management, University of Toronto 13

Enron’s Governance StructureWas Short Circuited

BoardKen Lay: Chair; Co-chair ZZZAudit, Compensation Cees.

ManagementLay, Skilling: CEO

Fastow, CFO; KoppersCausey, CAO; Buy, CRO

Watkins; Kaminsky; McMahon

Company Policies

Code of Conduct

Internal Audit ?

Whistleblowers ?

AuditorArthur

Andersen

Outside Law Firm

Consultant: Arthur Andersen

MissingSuspended

Compliance

GuidanceFinan.

ReportsSPEs

© L. Brooks

L.J. Brooks, Rotman School of Management, University of Toronto 14

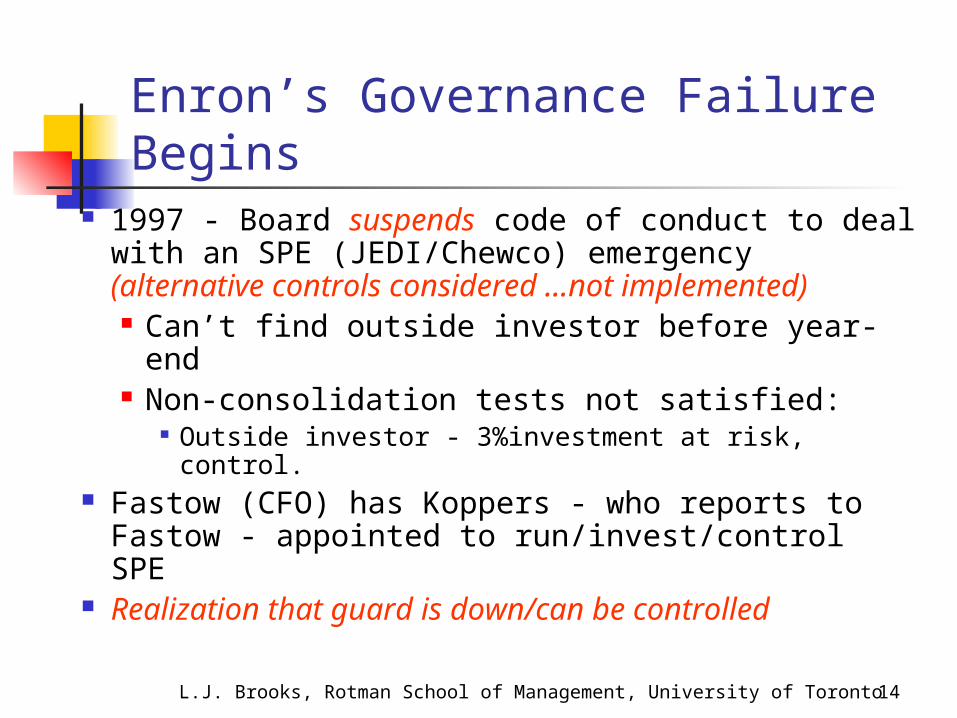

Enron’s Governance Failure Begins

1997 - Board suspends code of conduct to deal with an SPE (JEDI/Chewco) emergency (alternative controls considered …not implemented) Can’t find outside investor before year-end Non-consolidation tests not satisfied:

Outside investor - 3%investment at risk, control. Fastow (CFO) has Koppers - who reports to

Fastow - appointed to run/invest/control SPE Realization that guard is down/can be

controlled

L.J. Brooks, Rotman School of Management, University of Toronto 15

Chewco/JEDI Kopper/Dodson Dodson

LP/GP Big/Little

SONR River $11.4

GP LP

$11.4 ENRON Chewco

$132 LP

Barclays GP $240 JEDI

$240 + $11 +132 = $383

© I. Wiecek

3% Calculation

L.J. Brooks, Rotman School of Management, University of Toronto 16

Select Enron SPEsPurpose Issues

Chewco/JEDI Syndicatedinvestment

Off balance sheet liabilities ($628 million), revenues recognized early

LJM Provided marketfor assets

Artificial profits Equity overstated($1.2 billion)

LJM1/Rhythms Investment“hedge”

Unrecognized losses($508 mill. ‘97-’00)

LJM2/Raptors Investment“hedge”

Unexpected losses ($544 million)

L.J. Brooks, Rotman School of Management, University of Toronto 17

Governance Failure Allows Fastow to control SPE transactions:

Sales of assets at inflated prices (False gains) False hedging of losses on Enron investments

(Falsely keeps losses off Enron Income Stat.) Exorbitant payments to Fastow & helpers Hiding of SPE debt ultimately to be borne by

Enron Fastow to create more SPEs (LJMs…) Manipulation of accounting disclosure

L.J. Brooks, Rotman School of Management, University of Toronto 18

Partial Impact

Payments to Fastow & helpers Invest._ Return Other

Fastow $25,000 $4.5 mil in 2 mo. $30 mil+stock options+Koppers 125,000 10 mil (incl. $2 mil in fees

friend)2 others 5,800 1 mil

Manipulated transactions in Q3 & Q4, 1999Asset sales, plus 1 hedge $229 profit of $570 before tax

and 549 after tax (~50%)

L.J. Brooks, Rotman School of Management, University of Toronto 19

Enron’s Ethical Culture Code suspended, alternate controls ignored Bogus trading floor for visiting analysts California energy market manipulation Whistleblowers/doubters came forward

(to), but Co-chair Baxter (Lay) resigned, 32 mil. …

suicide? Kaminsky (Fastow) …….. ignored McMahon (Fastow)...transferred …now CEO Sharon Watkins (Lay)… Enron’s law firm

found no problem …fox in the chicken coup

L.J. Brooks, Rotman School of Management, University of Toronto 20

Stock Proceeds, 10/98 to 11/01

Lou Pal Chairman, Enron Accelerator $353.7 mill.Ken Lay Chairman 101.3Rebecca Mark-Jusbasche Director 79.5Ken Harrison Director, Portland General Electrics 75.2Kenneth Rice Chairman, Enron Broadband 72.8Jeffrey Skilling Director (former CEO) 66.9Mark Frevert Vice Chairman 50.3Stanley Horton Global Chairman 45.5Joseph Sutton Vice Chairman 40.1J. Clifford Baxter Vice Chairman 35.2Joseph Hirco CEO, Enron Broadband 35.2Andrew Fastow Chief Financial Officer 30.5

Source: The Washington Post Company, January 27, 2002, A10.

L.J. Brooks, Rotman School of Management, University of Toronto 21

Arthur Andersen’s Culture Emphasis on revenue generation, not on

quality assurance Final full year of fees: $52 million; $25

mil. Audit and 27 other services Previous largest fine $7 million Audit partner can veto Quality Assurance

partner – only Big 5 firm Post-AA work, alumni Franchise risk parameters? Shredding … Retention policy … optics

L.J. Brooks, Rotman School of Management, University of Toronto 22

Arthur Andersen’s Troubles

Losses to Job AAClient Problem Missed, Date Shareholders Losses Fine

WorldCom $4.3 billion overstatement of earnings, announced on June 25, 2002 $179.3 billion 17,000 N.A.

Enron Inflation of income, assets, etc., Bankrupt Dec. 2, 2001 $66.4 billion

6,100 N.A.

Global Candidate for bankruptcy Crossing $26.6 billion 8,700

Waste Overstatement of income Management by $1.1 billion, 1992-6 $20.5 billion 11,000 $7 mil.

Sunbeam Overstatement of 1997 income by $71.1 million, then bankruptcy $4.4 billion 1,700

Baptist Books cooked, Foundation largest nonprofit $570 million 165 of Arizona bankruptcy ever

Source: Primarily Business Week, August 12, 2002, 54

L.J. Brooks, Rotman School of Management, University of Toronto 23

Governance After Enron Dec. 2, 2001 – bankruptcy, outrage, crisis of

credibility, political and regulatory action accelerated

Canada - April 2002: TSE adopts most recommendations of Joint TSE/CICA Report of Nov. 2001, OSC watching US

US - SEC, NYSE, Nasdaq, President and Congress/Senate race to put forward proposals

March-June, 2002, Arthur Andersen shredding trial

June 26, 2002 - WorldCom announces 4.3 bil. Sarbanes-Oxley Act, July 30, 2002 SEC, + CICA/ICD initiatives - Audit Committee

L.J. Brooks, Rotman School of Management, University of Toronto 24

TSE Rule Changes, April, 2002, to be effective Dec. 31, 2002

Board approval of strategic plan - risks, opportunities Provide Board mandate:

Limits for Board and management; Provisions for shareholder feedback

Communications Policy - dealings with analysts and investors Disclosure on directors: related, composition, minority New Directors: full board participation in determination of skill

sets Assessments:

Board assessments - responsibility for and frequency CEO assessments

Directors meetings without management present Audit Committee:

all financially literate, at least one expert Charter of powers and responsibilities Source: Canadian Governance Review, April/May

2002

L.J. Brooks, Rotman School of Management, University of Toronto 25

Sarbanes-Oxley Act of 2002 (SOx)Worldwide coverage… new Directors’ needs: Competencies - recruitment & training

Role & new governance responsibilities Financial literacy Understanding

Strategy, policies, business model, internal control & compliance

Mandatory Whistleblower programs - anonymous CFO codes, Company codes disclosed (SEC)

No executive personal loans/arrangements

L.J. Brooks, Rotman School of Management, University of Toronto 26

Sarbanes-Oxley Act, July 30, 2002

Broad coverage, some to come – SEC, … Interesting coverage:

Audit Committees - anonymous whistleblowing process

Code of Ethics for senior financial officers No material misstatements or omissions Public Company Accounting Oversight Board Conflicts of Interest in audit services

Source Financial Reporting Release, PricewaterhouseCoopers, August 2002

L.J. Brooks, Rotman School of Management, University of Toronto 27

Emerging Governance Trends

Independence of Directors …judgement, role Chair//CEO, Audit Committee, unrelated …

Clarification of responsibilities of Directors, Officers, Audit Committee charters - oversight, strategies, compliance, internal culture, ethics, tone at the top, broader risk management, competencies (financial

literacy/financial expertise), performance measures Greater transparency

CEO, CFO sign-off certification of annual and quarterly fin. statements, compensation, stock options approved, additional disclosures… risks, internal control, earlier insider trade reporting

Independence of Auditors…not some consulting services

L.J. Brooks, Rotman School of Management, University of Toronto 28

Audit Committee key … must

Understand key business operations Understand comprehensive risk

management model and reports Examine key/large transactions Ensure compliance with good policies Ensure fair presentation

Who wants this risk?How much should the members be

paid?© L. Brooks

L.J. Brooks, Rotman School of Management, University of Toronto 29

New Governance IssuesFor directors and senior officers:

Director’s Responsibilities Financial literacy Guidance and control systems Ethics risk management Comprehensive risk management

How important is reputation, public interest,…

L.J. Brooks, Rotman School of Management, University of Toronto 30

Enron Case Discussion

Group discussion: What ethical problems caused the

Enron fiasco? Who was responsible? How could the problems have been

prevented? Class discussion and debrief