THE EMPIRICAL FOUNDATIONS OF ARBITRAGE...

42

Jouxnal of Fhmtial Economics ‘?I (3958) 213-254. North-Holland THE EMPIRICAL FOUNDATIONSOF THE ARBITRAGE PRICING THEORY* David ha. MODEST Received 0ctober 1985, &nal version received January 1988 The arbitrage pricing theory (APT) developed by Ross (1976,1977) is a major attempt to overcome the problems with testzbility’ and anomalous euqkical evidence that have plagued the static and iktertemporal capital asset pricing models (CAPMs). The main assumption of the theory is that the returns of a large (in the limit infinite) number of assets can be broken into two components: nondiver&able, systematic rislc,which can be measured as exposure to a small number of common factors, and idiosyncratic risk, which *We are grateful to the Faculty Research Fund of the Columbia Business School and i&z Institute for Quantitative Research iz Finance for their support and to Wayne Ferson and Allan Kleidon for comments on earlier drafts. We owe a special debt of gratitude to Jay Shauken (the refer) for signikantly improving the paper through his incisive comments and for pointing out severai errors in earlier drafts. The usual disclaimer applies. ‘The model does not resolve all empirical ambiguities of the type discuss4 in Roll (1977). Jtn particular, !Shanken (1982,198Sa) has emphasized that the absence of riskless arbitrage opportuni- ties coupled with the linear factor model for security returns does not place sufficiently precise restrictions on expected returns. In section 2 we address this i$nt further and sqecify a set of additional assumptions, that is sufficient to perform preci§e statistical tests. 0304405X/88,/,93.50 0 1,988, Ekevier Science Publishers B.V. (North-

Transcript of THE EMPIRICAL FOUNDATIONS OF ARBITRAGE...

Jouxnal of Fhmtial Economics ‘?I (3958) 213-254. North-Holland

THE EMPIRICAL FOUNDATIONS OF THE ARBITRAGE PRICING THEORY*

David ha. MODEST

Received 0ctober 1985, &nal version received January 1988

The arbitrage pricing theory (APT) developed by Ross (1976,1977) is a major attempt to overcome the problems with testzbility’ and anomalous euqkical evidence that have plagued the static and iktertemporal capital asset pricing models (CAPMs). The main assumption of the theory is that the returns of a large (in the limit infinite) number of assets can be broken into two components: nondiver&able, systematic rislc, which can be measured as exposure to a small number of common factors, and idiosyncratic risk, which

*We are grateful to the Faculty Research Fund of the Columbia Business School and i&z Institute for Quantitative Research iz Finance for their support and to Wayne Ferson and Allan Kleidon for comments on earlier drafts. We owe a special debt of gratitude to Jay Shauken (the refer) for signikantly improving the paper through his incisive comments and for pointing out severai errors in earlier drafts. The usual disclaimer applies.

‘The model does not resolve all empirical ambiguities of the type discuss4 in Roll (1977). Jtn particular, !Shanken (1982,198Sa) has emphasized that the absence of riskless arbitrage opportuni- ties coupled with the linear factor model for security returns does not place sufficiently precise restrictions on expected returns. In section 2 we address this i$nt further and sqecify a set of additional assumptions, that is sufficient to perform preci§e statistical tests.

0304405X/88,/,93.50 0 1,988, Ekevier Science Publishers B.V. (North-

214 B.N Lehmann and D. M. Modest, Empirical basis of the a&rage pricing theory

em be eliminated in large weW.iversified portfolios. This assumption, com- b&d tith the presumption that investors prefer more to less, leads to an approtiate theory of expected returns through the preclusion of riskless arbitrage opportunity.

Unfortunately, the apparent simplicity of the AFT conceals serious dish- cultis associated with its implementation. In particular, the theory cannot be tested without a strategy for measuring thecommon factors. Most investiga- tors have turned to factor analysis to measure these common factors implicitly. This approach exchanges the problem of identif@g tie factors o priori for the computational problems of performing maximum4ikelihood factor analysis on large cross-sections using conventional software pa&ages.

As a consequence, most previous researchers have performed factor analysis on relatively small cross-sections. This resolution of the problem of common factor measurement can adversely aff&ct tests of the APT’ in two ways. First, the use of small cross-sections can yield imprecise estimates of the common factors because the reliability of these estimates is low with small cross-sec- tions. Second the reliance on a small number of securities in the analysis nHkes it dif&u’lt to confront the theory with the anomalies that have proven puzzling in the CAPM context. Both problems can lead to tests of the APT that reject the theory when it is true or fail to reject rt when it is false.’

In this paper we remove some of the empirical ambiguity s~urrounding the .*. APT by performing more comprehensive tests than have previously been feasible. In the next section, we review the basic theory of the APT and its different formulations. The third section contains a brief literature review and a detailed description of our tests. in the fourth section, w’c de&be our procedure for forming basis portfolios to mimic the common factors and the impact of measurement error in the basis portfolios on our tests. The fifth section presents our empirical results. Among the most striking results are: (i) rejection of the hyp&esis that our basis portfolios span the mean-variance frontier of listed equities on the New York and American Stock Exchanges, (ii) evidence that the APT can explain the dividendyield and own-variance anomalies where the usual CAPM market proxies fail, and (iii) a distinct inability of the APT to explain the relation between firm size and average returns- The final section is devoted to concluding remarks.

2. T&e APT

ROSS (1976,1977) argued that the key intuition underleg the CAPM was the distinction between systematic and unsystematic riik. Ross noted that systematic risk need no: be adequately represented by a single common factor such as the return on the market and instead assumed that asset returns tie

5 N Lehmann and D. M. Modest, Empirical basis oj th? at&rage pricing theory 215

generated by a hear K-factor model:

In (l), R, is the return on asset i between dates t - 1 and t, Ei is the asset’s expected return, & is the realization of the kth common factor (normalized to have a zero population mean), bik is the sentitivity of the return of asset i to the kth common factor (called the factor loading), and Eit is tLe idiosyn- cratic return on the ith asset, which is assumed to have zero mean and finite variance, and to be suf&iently independent across securities so that idiosyn- cratic risk can be eliminated in large, well-diversified portfolios.

Ross and many subsequent authors have proven that the absence of riskless arbitrage opporuunities implies that expected returns must satisfy (approxi- mately):

(2)

as the number of assets satisfying the factor model (1) tends toward infinity where A, is the intercept of the pricing relation and X, is the risk premimn cm the kth common factor, k= l,..., K.

The approxir&e pricing relation given by (2) should price most assets with negligible error but, unfortunately, need not price all assets arbitrarily well. If the pricing errors for most assets were not trifling, one could construct zero net investment arbitrage portfolios that are riskless and earn nonzero profits. Unfortunately, the same argument cannot be used to guarantee that all assets will be priced correctly, since arbitrage portfolios must place appreciable weight on a small INdEi u nf assets to exploit a few signScant pricing deviations- These portfolios, in general, wii not be well-divers&d and need

u not have negligible total risk.2 As a consequence, the central risk-expected return relation of the APT

given by (2) is not testable without further assumptions, since a small number of assets could be priced arbitrarily badly.3 Not surprisingly, many investiga- tors have examined the circumstances in which the pricing errors for all assets under consideration are negligible. Chamberlain (1983, corollary I, pa 1315) provided the conditions required to transform the approximate pricing relation (2) into an exact pricing relation - the e&tence of a riskv well-diversified portfolio on the mean-variance efficient frontier of the assets under considera-

28ti1arly, assets.

these heuristic arguments can fail when applied to a large but finite number of

‘This point is made by Shanken (1982) and is a focus of the exchange between 5 -;bvig and Ross (1985) and Shanken (1985a).

tion is both mceswy and sufikient for exact factor pricing.4 Note that the requirement for exact factor pricing on a large subset of traded assets whose returns follow a factor structure (i.e., that there exist a well-div~ed portfolio of these assets on their mean=variance efkient frontier) does not preclude the existence of nontraded assets, such as human capital, or traded assets whose returns do not satisfy a linear factor model.

Since Ross% approximate pricing relation is not testable, our tests must be considered joint tests of Ross’s basic theory plus the additional assumptions requked to turn (2) into an exact factor pricing relation. In addition, as discussed in section 3, the empirical formulation of our tests requires us to construct po&*oKos to mimic the factors that span the factor space and do not contain any idiosyncratic risk, As a conseclue any rejection of the APT could reflect a fail= of the exact factor pricing version of the theory or of our inability to construct r&able estimates of the common factors.

The .APT has several formulations that follow from the diversikation possibilities arising when portfolios are formed from large (in the limit infinite) cross-sections of securities that satisfy a linear factor structure. As noted by Chamberlain (1983), the principal distinction among exact factor pricing models is whether the entire mean-variance frontier is well-diversified or whether only one potiolio on the frontier is welldiversified. This in turn depends ;~lh whether the limiting minimum variance potiolio of riw assets contains (i) no risk (i.e., no factor 0~ idiosyncratic risk), (ii) both factor and idiosyncratic risk, or (iii) only .U factor. Each case yields a difkrent formula- tion of the 4UT.

These three possibilities regarding the risk of the limiting minimum vatiance portfolio lead to three possible exact factor pricing versions of the APT’. If it is possible to construct a limi*Gng portfolio that costs a dollar and whose returns do nat vary, then the pricing intercept A, in (2) corresponds to the riskless rate (IQ). M**reover, in this case, there exists a well-diversified mean-variance efficient portfolio of *he K basis portfolios that with the riskless asset (i.e., the limiting riskless portfolio of these risky mts) spans the mean-vtince efficient fkontier of the individual assets - although the K basis portfolios by themselves do not spzm the frontier.

‘Using Chamberlain’s terminology, a sequence of portfolios is omsiderd well-diver&xl if in the limit (as the number of assets in the portfolio goes to infmity) the idiosyncratic variance of the sequence of portfolios tends to zero. ‘3 k, en and Ingersoll (1983), COMOr (1984), Dybvig (1983), Grinblatt and Titmm (1983), and !&a&en (198%) provide equilibrium conditions under which the pricing deviations for all assets will be small.

‘Huberman aud Kandel(1987) refer to the former circumstance as spanning of the efficient frontier and the latter as intersection of the eikient frontier.

It is not possible to form a limiting portfolio [from an infinite subset of securities whose ret- satisfy (1)) whose returns do not vary if, under an appropriate normalization of the factor spaeV the factor loadings on one of the factors are identical for all but a tite number of securities. Put diff~&rent,ly~ *&is inability to form a limiting riskless portfolio arises when a vector of one lies approximat&y in the cohunn space of the factor loading matrk This would occur, for instance, if most security returns are equally a@&cted by unexpected &anges in some mal3xBonomk variable asGlWorinfla= tion.

Inthiscase,~~aretwoversionsoftheApT,dependi~onwhetherthe limiting minimum variance potiolio is welbdivaed and contains ody factor risk or whether it is not w&divers&d and, neaCe, also contains some idiosyncratic risk, In the former c8se, the entire &an-&ce eflkient set will be welldiversi6ed and the K basis portfolios will span the frontier, given exact factor pricing. Under this formulation, the pricing intercept A, will be zero.

However, if the &3iting minimum variance portfolio is not ~e&diversiEed and, hens con’aias some idiosyncratic risk, the K basis span the frontier. In these circumstan~althoughalinear K basis portfolios will be mean-variance e&ient and well-diversikd, its orthogonal partner (Le., its a!Bociated minimum varian4x& zero beta portfolio) will contain idiosyncratic risk and hence the entire mean-variance frontier will not be welldivers&d. Under this formulation, there is no restriction on the pricing interpret A,.

Since A, could equal the riskless rate, these intercepts cannot be used to distinguish this model from the limiting riskless asset case dkussed above. Moreover, it is not poss&le to form a riskless portfolio with finitely many linearly independent securities even if the limiting minimum variance portfolio is r&less. Ekize, the etiteme of a limiting riskkss minimum variance po?tfolio is without empirical content in finite cross-sections. As a conse- quence, the two empirically distinct models are the spanuing formulation in which A, = 0 and the K basis portfolios span the frontier, and the alternative formulation in which X0 is unrestricted and a portfolio of the K basis portfolios is mean-variance efficient.

2.3. Empirical formulations

Hence we have two exact factor prickg models. If the K basis portfolios span the frontier, then security returns ,s._kF~

3

218 B.N LAmann and D.M. Modest, Empitical basis of tk arbitrage pricing theory

where R,, is the return on the basis portfolio that has unit sensitivity to the kth factor, zero sensitivity to aII other factors, and no idiosyncratic risk. In this case, tests of the APT mean restriction can be performed by regressing the raw secutity returns on a constant and the returns Gf the basis portfoIios and examining whether the constants are significantly different from zero. We sometimes refer to this as the raw-return version of the APT’. In addition, the K basis porafolios span the mean-variance efficient frontier in these cir- cumstances and it follows from RoII (1977) and Huberman and Kandel(l987) that the sum of the factor loadings must equal one. In section 3.3, we formahy discuss our procedures for testing these restrictions.

If the minimum variance portfoIio is not we&diversified, the K basis portfoIio wiII not span the mean-variance frontier of the individual assets and hence the sum of the factor loadings need not equaI one. In these cir- cumstances, individual security returns are described by

where fizt is the return on the minimum variance portfolio orthogonal td the returns of the K basis portfoIios? Thus, tests of the APT mean restriction can be performed by regre&q excess returns (over &) on a constant and the excess returns of the basis portfolios and examining whether the constants are fiigdicantly difkent from zero. We sometimes refer to this as the excess-retum v&sion of the APT.’

3. Hypothesis-testing-

3.1. Previous tests of the APT

Previous tests of the restriction given by (2) forms:* (i) tests for the equ&y

have typically taken three of intercepts across smah subgroups of

securities, (ii) tests for the joint significance of the factor risk premiums in each

%ee also Gibbons, Ross, and Shanken (1987).

‘Pantematively, we could perform such tests using returns in excess of X0 (i.e., E&J). Of course, both X0 and i?,, are unobservable in practice. Our reasons for performing the tests based on (4) are discussed below.

*Among the papers that have examined the implications of the factor-pricing relation are Roll and Ross (3980), Brown and Weinstein (1983), Chen (1983), Dhrymes, Friend, and Gultekin (1984), Dhrymes, Friend, Gultekin, and Gultekin (1985), and Connor and Korajczyk (‘1986). Papers that have examined the K-factor assumption underlying the theory include Gibbons (1986) and Shanken (1987a).

B.N Lehmann and D.M. Modest, Empirical basis of the arbitrage pricing theory 219

subgroup,g and (iii) tests for the si@can~ of nonfactor risk measures in explaining expected returns. Although most of the existing empi&al literature has failed to provide sharp evidence against the theory, this body of work suffers from a serious problem: the tests often lack the power to reject the theory when it is false. Some of the problems with earlier tests stem from the division of the universe of securities into small groups to perform maximum- likelihood factor analysis with Wnventional software packages.

This forced dependence on small cross-sections has two deleterious conse- quences. First, it results in imprecise estimates of the pricing intercept and the factor risk premiums, which make statistid tests particularly susceptible to Type II errors. Second, this practi~ prevents the implementation of tests that have proven useful in the CAPM context, such as the examination of the risk~adj~usted returns on portfolios sorted on the basis of some characteristic such as dividend yield or firm size. Our maximum4ikelihood factor analysis procedure permits us to use many securities in our examination of the APT.

3.2. Testing exact fucttw pricing

We implement +be tests uy estimating the factor loadings and idiosyncratic variances for a large cross-section of securities and using these estimate to construct basis portfolios to mimic realizations of the common factors. Sec- ond, we form portfolios of securities ranked on characteristics such as firm size, dividend yield, and own variance. We then regress the returns of the sorted portfolios on the corresponding basis portfolio returns and a constant. The usual F test for the hypothesis that the intercepts for each portfolio are jointly insigniucantly Werent from zero provides a test of exact factor pricing.

To guard against potential power dithculties caused by possible nonlineari- ties of the dividend yield, own variance, and size effects, we consistently perform this test on five, ten, and twenty sorted portfolios. In addition, we use similar procedures to test the mean- var&na &&iCY & -&e ~aJly-ly_wei$#@d

and valueweighted CRSP indices. The failure to reject the APT and simulta~ neous rejection of the mean-variance efficiency of the usual market proxies suggest that our tests have power against reasonable alternatives.

3.2.1. The test statistic

Fomdy, our tests are as follows. Let a,, be the vector of excess returns on the sorted characteristics portfolios when the K basis portfolios do not&sFan the mean-variance frontier and be the corresponding raw returns when there

‘This involves the additional assumption that investors are risk-averse. Unfortunately, the sample rotation of the factors may got be the same across different factor analysis runs. Consequently, there is no prediction that the factor risk pretiums should be equal across groups w&e kior ioadings may correspond to different rotations of the factor space.

220 B. N L.ehmmn and B. &L. X&s~~ &qvirica! busis of the arbitrage pricing theoy

is spanning. Similarly, let a,, be the corresponding vectors of excess or raw returns on the basis portfolios (where appropriate), which are assumed to be perfectly correlated with the factors. Consider the fitted multivariate regression of &,, on 8,1 and a constant:

where ap is tie estimated constant term vector, 3 is the estimated factor loading matrix, and gPt is the fitted residual vector. If there is exact factor p&in% the basis portfolios are measured without error, and we observe fizt when appropriate, kP should be statistically insignificantly different from zero. On the assumption that &,, md 1, are jointly norm&y distributed random vectors, &e usual F statistic for testing this hypothesis is

(6)

where fiP is the sample residual covariance matrix of &, h, is the vector of sample mean returns on the basis portfolios, and e,,, is the sample covariance matrix of their returns.

3.2.2. On the cmsttuction of excess tetwns

To construct our orthogonal portfolio we choose the N portfolio weights Use so that they

mi.nwjDwrj s.t. w$bk = 0, Qk, and w$,, = 1, @%f

where bk is the kth cohunn of the factor loading matrix diagonal matrix consisting of the estimated variances of disturbances.‘*

B and D is the the idiosyncratic

The assumption that our orthogonal portfolio perfectly mimics the returns on the true minimum-variance orthogonal portfolio can fail to hold for several rasons. If the conjiructed orthogonal portfolio were free of ‘excess’ idiosyn- cratic risk but not factor risk, then the use of its ~-eturn 1?,*1 in computing excess returns [i.e., replacing R,, with 82 in (4)] would still lead to valid tests

‘*This is ptisely the portfolio for the intercept that is produced by the Fama-MacBeth style cros~sectional regression on a constant and the factor loadings. Note that it will not be possible to solve this programming problem in the population if Bak = dpl, that is when the ~&niting minimum-variance portfolio contains no idiosyncratic risk and the basis portfolios spank the mean-variance &Sent frontier.

B. N Lehmann and D. M. Modest, Empirical basis of the arbitrage pricing theory 221

of the APT mean restriction while using its mean return E&] would not? If, on the other hand, the orthogod portfolio were free of factor risk but some ‘excess’ idiosyncratic risk remained, it would be appropriate to construct the excess returns in relation to R,*,] rather than the actual retwns, since the mean return would quai h, in this case.

In practice, it seems likely that the orthogonal portfolios will contain negligible ‘excess’ idiosyncratic risk when they are well=diversSed portfolios constructed from large cross+ections. However, since the orthogonal po~-Vinc are constructed to have weights orthogonal to the estimated factor loadings (but not necessarily orthog~=zl to the true loadings), some factor risk is likely 10 remain - biasing these ~&folios’ mean returns even as the number c;’ secur5ti.e-s in the cross=section grows large - leading to inference problems if the mean return on the orthogonal portfolio is used to construct excess returns?* Co nsequently, the results presented below for exact factor pricing without spanning are based on excess returns computed in relation to the actual returns on the orthogonal portfolio.13 In additioq we report summary s’tatistics for the orthogonal portfolios and their relationship to one-month Treasury bill returns.

3.3. Tests for q?anrai?lg

Pn sections 2.2 and 2.3, we noted that distinctions among exact factor pricing versions of the APT hinge on whether the K basis portfolios span the mean-variance frontier of the individual assets. As previously noted, it follows

‘ITo see thig asspe that actual purity returns are generated by a one-factor model: Rit = R:c + BicR,* - R,,) + i&r where R,, is the return on the @ctor@isider the mulatjon regression coefficients (at and bf ) from ~UIU@ the regression: R, - R, = a,? + b,+ ( R,, - Rz) + Zit, where i?;Y, is the ret= on a proxy ‘orthogonal’ pcrtfolio wKch contains some factor risk but no idiosyn&atic risk, i.e., Rz = (1 - v)R,, + &,,,. Since Bit - 83 = (fli - r)(R,,,, - R,,) + Zfr a@d _Rmr --_jQ = (1 - y)(i?,, - R,,). it is my to ShOW tbt b: =COV(Ri, - 82, R,,-- k,*,)/

“ar(Rm, - Rz) = (pi - y)\(l - y) (which Is a b&ed estimate of pi U&SS y = 0), but that 4r = E[Rit - R$] - b,*Qfimt - &I = 0. Note that subtracting the mean retum on the orthogonal portfolio would lead to biased tests since b? would be an unbiased estimate of & but El&] + A0 ?ice the portfolio contains some factor r&k.

12The i&ition behind th& result is clearest in the one-factor case. Consider Fama-B&Beth style cross-sectional regressions of inditiduaI securitjr returns on a constant and the estimated factor loadings. As is well knom measurement error in the independent variable (the estimated factor loadings) will unambiguously bias tie slope term (the estiated return on the factor) toward zero and the constant term (the estimated return on the orthogonal portfolio) away from zero. However, as the c:oss-section grows large, idiosyncratic risk will be eliminated in the p~flf~lio mimicking the retum on the factor. H ace, wMe &&is basis portfoliu return will II& have a sensitivity of one to the factor because of the bias, it ti in the limit be perfectly correlated with the factor* which is all that is needed to test the mean restriction. Unfortunately, since the bias in the regression coefficients does not disappear in the limit, inferences regarding the mean return on the orthogonal portfolio remain problematic.

?paS a c&k on this assumption, selected results are presew.3 for the excess-return tests, w&&e th sample mean retwn on the or%ogonal portfolio is used to construct excess retums.

229 B. N Lehmann and D. M. Mudest, Empirical basis cf the arbitrage pricing theory

from Roll (1977) and Huberman and Kandel(l987) that spanning implies that the sum of the factor loadings must equal one, and hence that Br, = c,.

As a consequence, the spanning versus no-spanning dichotomy can be examined by testing whether the-sum of t@e coefficients in either (3) or (4) is unity. On the assumption that R,, and R, are jointly normally d&?buted random vectors, the usual F statistic for testing this hypothesis is

where again fiP is the matrix of estimated portfolio factor loadings and fiP is the sample residual covariance matrix of the regression residuals. We perform this test on both the excess-return and raw-return regressions to guard against possible digerences in the two test formulations -both specifications are appropriate under the null hypothesis that BI, = B,, and there is exact factor pricing.

The aualysis in section 3 presupposes the existence of basis portfolios that are perfectly correlated tith the common factors underlying security returns. In this section, we discuss the construction of basis portfolios designed to mimic the realizations of the common factors and the impact of measurement erro: h the estimated factor loatigs and in the basis portfolios on our tests. The construction of basis portfolios is a two-step procedure. In step one, the sensitivities to the common factors are estimated for a collection of individual securities. In the second step, these estimated factor loadings are used to form the basis portfolios.

The primary assumption of the APT is that security returns are generated by a K factor linear structure. Given the structure in (1) combined with the assumptions E[$#,] = 0 and I@$#“] = 0 (a a positive definite symmetric matrix) and the normalization of the factors so that E!!8t] = 0 and E&8;] = 1, the covariance matrix of security returns, 2, can be written as 27 = B.?? -+ $2. Theoretically, the APT places no restrictions on Q other than the requirement that the off-diagonal elements be sufficiently sparse so that the residual risks are diversifiable (in the limit) and, hence, security returns satisfy au approxi- mate factor structure.i”

14The formal requirement is t&t the e’ ~gecv&es cf D remain bounded as N + 00.

B. N Lehmann and D. M. Modest, Empirical basis of the arbitrage pricing theory 223

Chamberlain and Rothschild (1983) have shown that consistent estimates of the factor loa&ngs can be obtained from the eigenvectors associated with the K largest ezgenvalues of the matrix T-2, where T is any arbitrary positive- deiknite mat& with eigenvalues bounded away from zero and i&&y. Stan- dard maximum likelihood fector zplar*;m (m Jyw \mder the normahty assumption) is numericak qa I +tivalent to calc$aring the largest K eigenvectors of the matrix T-!S, where T is set equal to D, which is a diagonal matrix consisting of the estimated residual variances and S is the sample covariance matrix.r5 Al- though this is a conceptually simple exercise, it is computationally infeasible to obtain these estimates by iteratively solving the tit-order conditions when the number of securities being analyzed is substantial. We employ a signifkantly cheaper alternative: the EM algorithm of Dempster, Laird, and Rubin (1977) applied to factor analysis in Rubin and Thayer (1982).

A variety of methods can be used to construct portfolios to mimic the factors. The niost commonly used procedure involves treating the factor sensitivities &) in (1) as explanatoq variables, gi, - Ei as the dependent variables, and *the factor realizations (I&J as parameters to be estima%d, and running cross-sectional regressions perid by period along the lines of Fama and IMacBeth (1973). Given the true factor loa&ngs (B) and the true idiosyn- cratic covariance matrix (a), the generalized least squares version of this estimator [i.e., portfolio weights given by (B12-1B)-1M2-1] provides the minimum-variance linear unbiased estimate of the factors. In practice, all APT applications that we are aware of replace Q with a diagonai matrix consisting of estimates of the idiosyncratic variances, thereby ignoring the .ofMiagonal elements. Hence, the procedure is more accurately referred to as a weigh&d least squares (WLS) procedure.

Unfortunately, the true factor loadings and the *&ue idiosyncratic covariance matrix are not known and estimates must be used in constructing these portfolios. The presence of this measurement error reduces the population correlation between these WLS basis portfolios and the common factors and, in fact, alternative basis portfolio formation techniques may have higher

“Formally, this involves maxim@@e likelihood function: S(ZiS) = (-- NT/2)ln(2rrr) - (T/2)lx@( - $Xr_,(& - @‘P(R, - R). Principal components involves calculating the corre- sponding eigenvectors of the matrix T-IS with T set equal to a~ identity matrix. Asymptotically, both methods provide the same estimated factor loading up to an arbitrary rotation. Unfor- tunately, the relative small-sample properties of the two estimation procedures are unknowrz, assuming only an approximate factor structure holds. Connor and Korajczyk (1986) prove the consistency of the factor estimates (as N + GU) of the principal components estimator. A similar proof can be used to show the consistency of maximum likelihood factor analysis with T set equal to a diagonal matrix of estimated idiosyncratic variances with elements bounded away from zero and intinity.

224 B. N Lehmann D.&i. Mdest, basis of arbitrage pricing

population correlation with the common factors? This is possible because the WLS procedure tends to give greater weight to security returns associated with large estimated factor loadings and typically downweights those with small loading estimates. This is appropriate in the absence of measurement error, since the returns of securities with large factor loadings are more informative about fhictuations in the common factor the WLS ;++hg prw

dure is less approtxiate when the sample loadings reflect measurement error in addition to the t&e loadings.

We employ a method we refer to as the minimum idbsyncratic risk procedure

as an aluznative to the WLS potiolio formation procedure. In particular, our procedure involves choosing the portfolio weights 7 which solve

min w;Dwi s.t. w-

w;bk =O,Vj#k, and +=l, J

where 1c(i’bi is unrestricted.17 These portfolios are similar to the WLS ones in that they minim&e the sample idiosycratic variance of the basis portfolios subject to the constraint that the weights be orthogonal to the sample loadings of the factors not being mimicked [i.e., w;bk = 0, Vj i k].‘8 ‘I%~ d8brence between the two procedures lie in the requirement that the WLS portfolios have a sample loading of unity on the factor being mimicked (before normal= ization to unit net-investment), whereas the minimum idiosyncratic risk portfolios must simply cost a dollar. As a consequence, the minimum idiosyn- cratic risk procedure largely ignores the information in the factor loadings: a

16’Ihis is formally shown fcs the case of a single common factor in Lehmann and Modest (1985). One other problem with the WLS procedure is that in factor model estimation it is conventional to normalixe the factors so that they are uncorrelated ad have unit variances and to normal& the factor loadings so that B’D’IB 2s &god. lfhis practice yields typical factor loading estknates that are much less than one - on the order of 0.001 to 0 9901 in daily data A.: a co~uence, the WLS procedure must place large positive and negative weights on at least some see&ties to ensure both that 9% = 1 and $bk = 0, Vj # k. For instance, we have found that the WLS procedure coupkd with the conventional normalization of the factor model typically produces portfolio weights in excess of 100% in absolute vale, yielding poorlydiversified reference portfolios. The evidence presented in Lehmann and Modest (1985) suggests that the minimum idiosyncratic risk procedure dkussed below performed at least as well as (and usually better than) its competitors.

“This minimum idiosyncratic risk estimator for the jth factor is D-LB*[B4’D-‘B*J-iej, where B* =(b,q...r . . . bk), 1 is a vector of ones in the jth cohrmn and ei is a vector of zeros except for a one in the jth position fn large crossIsections, this procedure can be shown to produce valid mimicking portfolios in the sense of proposition 1 of Huberman, Kandel, and Stambaugh (1987). A proof is available upon request.

‘*As pointed out by Litzenberger and Ramaswamy (1979) and Rosenberg and Marathe (1979), the WLs estimator is equivalent to choosing the N portfolio weights q (to mimic the jth factor) so that they min w/D9 subject to qbk - 0, Vj + k, and BJ%~ - 1, Vj - k, and then normalizing the weights ?5 “&c they sum to one,

B. N Lehmann ad D. M. Mod&t, Empirical b&s of the erbitmge prizing theory 225

bad decision in the absence of meassurement error and a potentially choice in its presence.19

We emphasize that the distinction between the minimum idiosynaatic risk procedure and the WLS method affects only the results obtained for the raw-fetum verson of the model *muse of our use of constructed orthogonal portfolios to create excess returns. Wt mte the excess returns on the mimicking portfolios by subtracting the retbm on the orthogonal portfolio from the returns on the minimum idiosyncratic tisk potiolios. These excess returns are identical (up to a factor of proporti,?nality) to the coefficients obtained from the WLS cross-sectional regression 3 individual security re- turns on the factor loadings and a ve$.? ;c cG< : : : a-- T’ -.s e&e rs&s &&&d

for the excess+etm version of the *,~2ld on the Merences in these procedureP

4.3. On the impact oj?n4wsure~dnt en-or

A critical assumption in our tests of exact factor pricing is that the bak portfolios span the factor space and contain no idiosyncratic risk, an assump- tion that is literally correct only as the number of securities in the cross-section tends toward infinity. To the extent that this assumption is violated, the intercepts in (5) will be biased away from zero when the APT is true, yielding F statistics that are biased toward rejection. Fortunately, although measure- ment error in the estimated factor loadings will tend to lead to biased estimates of the individual factors, linear combinations of the K bask pw+- folios will still tend to span the factor space. Furthermore, as long as the basis portfolio weights are we&diversified (i.e., of order l/N), the basis portfolios will contain minimal idiosyncratic risk. 21 Hence9 in the limit, the use of the K basis nortfolios leads to valid tests of the APT mean restriction even in the presence of measurement error in the factor loadings.

We eschew an alternative strategy that would partially mitigate the effecd of measurement error in the estimated factor loadings. In particular, we-could have estimated the basis portfolio returns by straightfonvard application of the Fama-MacBeth style cross-sectional regresfiions (at each date t) of the

19The two strategies yield basis portfolios with very different diversification properties in actual practice. The average sum of squared basis portfolio weig#.s (per factor) using the minirn~um. idiosyncratic risk procclure is 0.016 for the five-factor modd, 0.022 for the ten-factor rn~&A, and 0.025 for b&e fiftce&~_ctor model, GE c&c to -the minimum attainable sum of 0.00213. By contrast, the corresponding averages for the WLS procedure coupled with the conventional normalization of the factor model are 0.659, 72.689, and 2SS.234p clearly far from the minimum attainable. Footnote 16 discusses why this occurs.

2oSee Lehmann and Modest (1985) for a detailed analysjs of this equivalence in the one-factor case. This relation between the two procedures, however, dims not obtain when measured riskless rates are used instead of the constructed orthogonal portfoE returns.

“a two-factor example is available on request.

226 B.N Lehmann and D.M. Modest, Empirical basis of the arbitrage pricing theoly

sorted portfolio returns on a constant md their estimated factor loadings. The analog to hp in (5) could then be computed from the time series mean of the portfolio residuals. This approach would tend to alleviate the measurement error problem discuss,, -u..+ @A ahave. since the measurement error in the factor loadings of the sorted portfolios should be much smaller than the typical error in the loadings of the individual securities as long as the portfolios are well-diversified and not formed on the basis of their sample loadings.

Vv’e forego this seemingly superior statistical procedure because it involves estimating the factor risk premiums using the portfolios formed from well- known emtGrical anomalies. Suppose that the APT is false and we construct the test stitistics in this revised fashion. The cross-sectional regressions will choose estimates of the factor risk premiums that minim& the weighted sum of squared residuals (i.e., tend to fit the anomalies). This, in turn, will tend to make the F statistic small, and hence can cause a failure to reject the null hypothesis when it is false. In our procedure, we estimate the factor risk premiums from the whole sample of securities underlying the factor analysis, a sample that is not biased with regard to firm size, dividend yield, or own variance. These premiums are then used to estimtite “iP and to test its significance.

5. I. Data considerations

The CRSP files provide both daily and monthly equity returns. The poten- tial benefit associated with the use of daily data in the estimation of variances a9.d covariances is enormous, since the precision of these parameter estimates hinges on the frquency of observation. Of course, daily data has the well- known probiems of asynchronolus trading, which bias the estimates of second moments, and the bid-ask spread, which bias the estimates of first moments. Moreover, daily data provide no advantage when estimatiag mean returns whose precision depends on the length of tl& estimation interval.

In choosing an observation frequency, we opt for a comprotise solution. Following Roll and Ross (1980) and most subsequent empirical investigators, we estimate out factor models fd>r security returns with daily data, since we surmise that the ga’ %n in precisioii offsets the thin trading biases in the estimation of covariance matrices .** We test the theory and its various aspects, however, using weekly returns data, formed by compounding daily returns

%s a ret UfUS.

check, we also pfesd t results based on factor models estimated with weekly arnd monthly

B. N Luhmann and D. M. Modest, Empirical basis of the arbitrage pricing theory 227

from Wednesday k~ Tuesday. 23 Consequently, basis portfolio returns are computed by multiplying the portfolio weights by the corresponding weekly

returns on individual securities. The weekly returns on the CRSP qua,@- weighted and value-weighted indices are compttted by compound&g th&

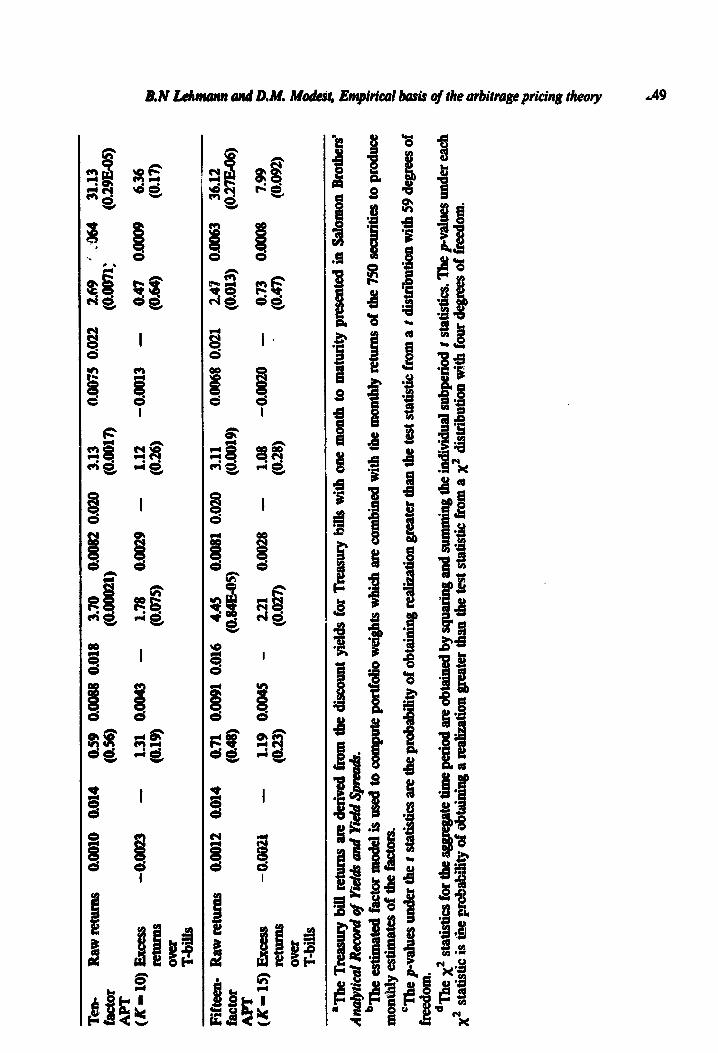

daily returns in the same fashion. Thus our market proxies contain both New York Stock Exchange (NYSE) and American Stock Exchange (AMEX) securi- ties. Excess returns, when needed, are computed in relation to the orthogonal portfolio returns. All of the relevant test statistics are constructed with these weekIy returns with one exception.” The tests comparing the returns on the orthogonaI portfolios and Treasury bibs are performed with monthly data, since ‘Zeasury bills with one week to maturity are not actively traded and hence reliable weekly interest rates cannot be obtained.

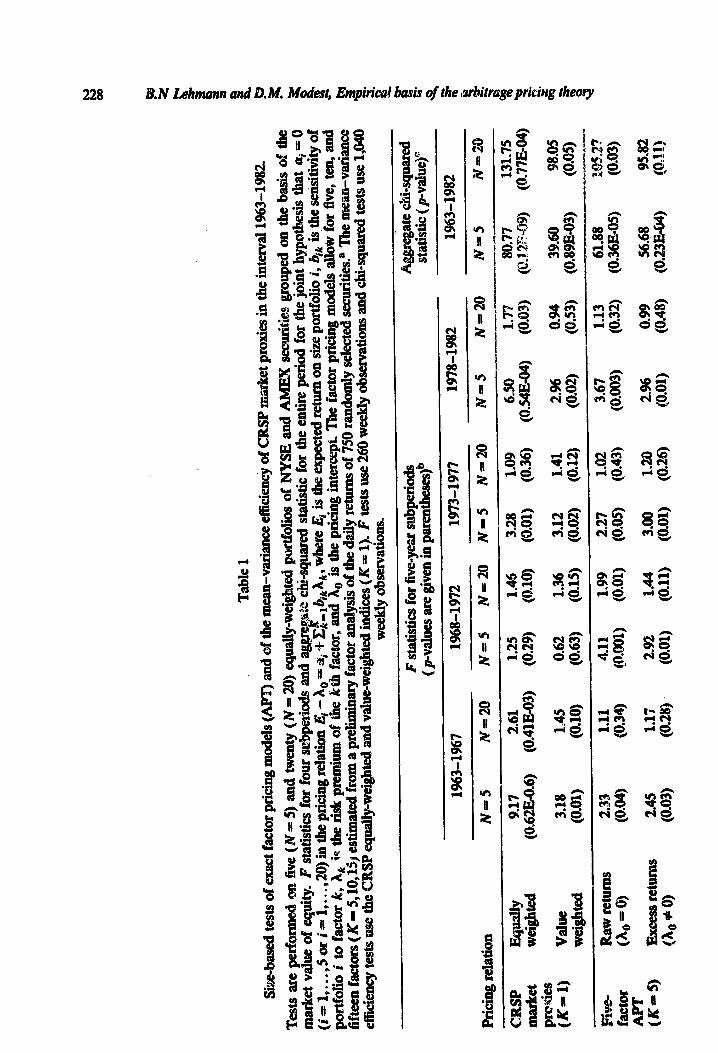

Two other important choices involve the length of the estimation interval and which firms to include in our ample. We assume stationarity over five-year subperiods and divide the time interval covered by the CRSP daily returns fi3e into four periods: 1963-1967, 1968-1972, 1973-1977, and 1978-1982. Within each period, we exclude securities that are not continu- ously listed or which have missing returns and ignore the possible selection bias inherent in this strategy. The remaining securities number 1,001, 1,359, 1,346, and 1,281 in the four periods. The number of daily observations in these samples totals 2,259, 1,234, 1,263, and 1,264, respectively, and there are 260 weekly observations in each five-year period. The CRSP daily file (with few exceptions) lists securities in alphabetical order. We randomljf reorder the securities in each subperiod to guard against any biases induced by the natural progression of letters (IBM, International Paper, etc.). The usual sample ~variance mmix of these security returns provides the basic input to our subsequent anr~ysis. Bach period we estimate five-,, ten-, and fifteen-factor models using the first 750 securities in 3ur randomly reordered data file.

5.2. Tests of t!k APT mean restriction

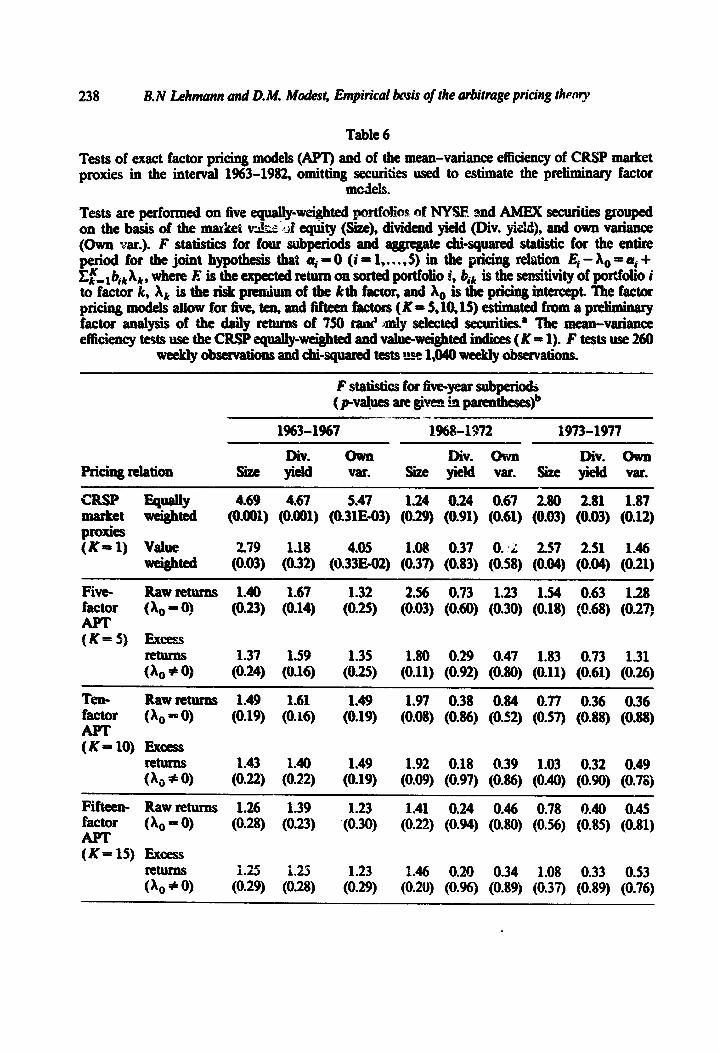

Our strategy for testing the AFT involves examining the ability to the theory to account for well-documented empirical anomalies that provide the basis for rejecting the mean-variance efficiency of the usual market proxies. ‘rabies 1 through 6 provide tests based on three such anomalies: firm size, dividend

23T~ be more precise, our weeks begin on the fitst trading day after Tuei ‘J (usually Wednesday) and end on the last trading day prior to Wednesday (usually Tuesday). We made this choice because &there are fewer trading holidays on Tuesdays and Wednesdays and to mitigate biases caused by the day-of-the-week eflrect.. Also, it was sometimes necessary to drop observations at the beginning and end of our fiveaye= subperiods to insure that within each subperiod our weeks began on Wednesdays and ended on Tuesdays.

“We i&Fated rmost of our tests SB zxx&E~ ,a +I ta and verified that the conclusionis reported hc1=e are robust with respect to this choice. We report the weekly results because of the potential gain associated with more pwdbcl estimation of the residual covariance matrix.

228 1% N khtnann ad D.iU. Mode@, Empirica! basis of the arbitrage pri&g theory

I I

, I

,

r r c

5 Y

I

B. N khmmn lad D. M. Mdest, Empirical basis of the arbitrage pric@g thewy 229

Tab

le 2

Siz

e-ba

sed

test

s of

exa

ct f

acto

r pr

icin

g m

odel

s (A

PT

) us

ing

diff

eren

t fac

tor

esti

mat

es a

nd o

f th

e m

ean-

vari

ance

eff

icie

ncy

of C

USP

mar

ket p

roxi

es in

th

e in

terv

al 1

963-

1982

.

Tes

ts a

re p

erfo

rmed

oti

tie

qu

ail

y-w

e&k&

d po

rtfo

tios

of

NO

SE a

nd A

ME

YC

secu

riti

es g

roup

&

_- o

n th

e ba

sis

of t

he m

arke

t val

ue o

f eq

uity

. F

stat

isti

cs

for

four

sub

peti

ods

and

aggr

egat

e cl&

squa

red

stat

isti

c fo

r th

e eh

e pe

riod

for

the

join

t hy

poth

esis

tha

t ui

= 0

(i

= 1,

. . .

,5)

in’ t

he p

rici

ng r

elat

ion

Ei -

X

0 =

ai +

Z&

lbjh

X,;

whe

re I

$ is

the

exp

ecte

d re

turn

OIP &e portfallio

i, 6ik is

the

seu

siti

vity

of

port

folio

i t

o fa

ctor

k,

X,

is t

he r

isk

prem

itim

of

thz

k*&

fact

or,

and

a0 i

s th

e pr

icin

g in

ter&

@. T

he f

acto

r pr

icin

g m

odel

s al

low

for

fiv

e an

d te

n fa

ctor

s (K

= $

10)

esti

mat

ed f

rom

a p

relim

inar

y an

alys

is o

f th

e w

eek

ly a

nd

mon

thly

ret

urns

of

750

rand

omly

sel

ecte

d se

curi

ties

.~ T

he m

ean-

vari

ance

eff

icie

ncy

test

s us

e th

e C

RSP

equ

ally

-wei

ghte

d an

d va

he~

wei

ghte

d in

dice

s (K

= 1

). F

tes

ts u

se 2

60 w

eekl

y ob

serv

atio

ns a

nd c

i&sq

ua~&

tes

ts v

m 1

,040

wee

kly

ob3?

:rva

tidn

s.

Pri

cing

rel

atio

n

.

1963

-l&

7

We&

y M

oz~t

bly

F s

tati

stic

s for

five

-yea

r sub

peri

ods

(p-v

alue

s ar

e gi

ven

in p

aren

th~5

5s)~

1968

-197

2 19

73-1

977

W&

ly

Mon

thly

W

eek

ly

Mon

thly

Agg

rega

te &

i-sq

uar

ed

stat

isti

c (p

-val

ue)”

1978

-198

2 -

196=

82

-I.

Wee

kly

M

a&&

y#

&..y

r.

r -

- ..

_.-

MO

KlU

ii~

’ C

RSP

J%

dY

9.17

9.

17

1.25

1.

25

3.28

3.

28

6.50

6.

50

80.7

7 80

.77

mar

La

W4figbd

(0.6

2E-O

.6)

(0.6

2E-0

6)

(0.2

9)

(0.2

9)

(0.0

1)

(0.0

1)

(O.S

4E-0

4)

(OS

4E-0

4)

(O.l

2E-0

9)

(O.l

2E-0

9)

prox

ies

(K-=

1)

va

lue

3.18

3.

18

0.62

0.

62

3.12

3.

12

2.96

2.

96

39.6

0 39

.60

Wt?igh!d

(0.01)

(O+

Ol)

(0

.63)

(0

.63)

(0

.02)

(O

&2)

(0

.02)

(0

.02)

(0

.89E

-03)

(0

.89E

-03)

Fiv

e R

aw r

etur

ns

3.32

3.

29

3.79

2.

00

4.32

3.

31

4.82

4.

04

81.2

5 63

.20

fact

or

(%I

= 0

) (0

.64E

-02)

(0

.68E

-02)

(0.

2SE

-02)

(0

.08)

(0

.86E

-O 3;

(W6E

-02)

(0

.31E

-03)

(O

.lS

E-0

3) (

0.24

E-0

8)

(0.2

3E-0

5)

(K-5

) E

xces

sret

urns

3.

10

3.47

3.

07

2.80

3.

61

2.83

4.

21

2.32

69

.95

57.1

0 (A

, #

0)

(0.9

9E82

) (0

.48E

-02)

(0

.01)

(0

.02)

(0

.36E

-02)

(0

.02)

(O

.llE

-02)

(0

.04)

(0

.19E

-06)

(0

.2O

E-0

4)

Ten

- R

aw r

etur

ns

4.58

28

0 3.

30

1.77

3.

45

2.47

3.

52

3.49

74

.25

52.6

0 fa

ctor

(A

, =

0)

(0.5

2E-0

3)

(0.0

2)

(0.6

7E-0

2)

(0.1

2)

(0.4

9E-0

2)

(0.0

3)

(0.4

4E-0

2)

(0.4

7E-0

2)

(0.3

4E-0

7)

(0.9

3E-0

4)

AP

T

(K=

lO)

Exc

egsr

etur

ns

.t 3

7 3.

36

3.72

2.

89

4.20

2.

26

3.38

2.

99

73.8

5 57

.50

(A,

+ 0

) (0

.4&

2)

(0.5

9E-0

2) (

0.29

E-0

2)

(0.0

1)

(O.l

lE-0

2)

(0.0

5)

(0.5

7E-0

2)

(0.0

1)

(0.4

2E-0

7)

(0.1

7E-0

4)

‘The

es

tim

ated

fac

tor

mod

el i

s us

ed t

o co

mpu

te p

ortf

olio

wei

ghts

whi

ch a

re c

ombi

ned

wit

h th

e w

eek

ly r

etur

ns o

f th

e 75

0 se

curi

ties

to p

rodu

ce

wee

kly

est

imat

es o

f th

e fa

cto=

bE

ach

F st

atis

tic is

for

the

test

of

the j

oint

hyp

othe

sis t

hat

ui =

0 in

the

app

ropr

iate

pric

ing

rela

tion

. For

the

AP

I’ te

sts,

the

~~

~ah

te is t

he p

roba

bili

ty

of o

btai

ning

a r

eali

zati

on g

reat

er th

an t

he t

est s

tati

stic

from

an

F di

stri

buti

on w

ith

N n

umer

ator

deg

rees

of

free

dom

and

235

- K

- N

den

omin

ator

de

gree

s of

free

dom

. For

the

CR

SP

mea

n-va

rian

ce e

ffic

ienc

y tes

ts, t

he p

-val

ue i

s th

e pr

obab

ilit

y of

obt

aini

ng a

rea

liza

tion

grea

ter t

han

the

test

sta

tist

ic

from

an

F di

stri

buti

on w

ith

N -

1 n

umer

ator

deg

rees

of

free

dom

and

235

- N

den

omin

ator

deg

rees

of

free

dom

. ‘E

ach

x2 s

tati

stic

for

the

ste

ti

me

peri

od is

N t

imes

the

sum

of

the

four

sub

peri

od F

sta

tist

ics.

The

pval

ue u

mbe

r ee&

x2

%id

ic

is t

he

prob

abil

ity

of o

bWun

g a

real

izat

ion

grea

ter t

han

the

test

sta

tist

ic fr

om a

x2

dist

ribu

tion

wit

h de

gree

s of

free

dom

equ

al t

o 20

whe

n N

= 5

and

80

whe

n N

= 2

0 fo

r th

e A

PT

test

s and

wit

h de

gree

s of

free

dom

equa

l to

16 w

hen

N =

5 a

nd 7

6 w

hen

N =

20

for

the

CR

SP

mea

n-va

rian

ce e

ffic

ienc

y tes

ts.

Tab

le 3

Siz

e-ba

sed

test

s of

exa

ct f

acto

r pr

icin

g m

odel

s (A

PT

) an

d of

the

mea

n-va

rian

ce e

ffic

ienc

y of

CR

SP

mar

ket

pro

ties

in

the

inte

rval

L96

3A98

2,

excl

udk

g Ja

nuar

y ret

ums.

Tes

ts a

re p

e&m

ed

0~ t

ie

(N =

5)

and

twen

ty (

N =

39)

qy_TMeighted

port

foli

os o

f W

SE

an

d A

ME

X s

ecm

itk

s gr

oupe

d on

the

bas

is o

f th

e m

ark

et v

alue

of

equi

ty.

F st

atis

tics

for

four

sub

peri

ods

and

te &

i-sq

uare

d statistic for

the

enti

re p

erio

d fo

r th

e jo

int

hypo

thes

is t

hat

ai =

0

(i=

l,..

.,

Sor

i==

l,...

, 20

) in

the

p&&

g re

lati

sn E

i ag

gry

- A

, = U

i + x

k_lb

ikX

k, w

here

Ei i

s the

exp

ecte

d re

turn

011

S&

po

rtfo

lio

i, b

ik is

the

sea

sitit

ity

of

poti

olio

i

to f

acto

r k

, A

, is

the

ris

k p

rem

ium

of

the

kth

fac

tor,

and

X,

is t

he p

rici

ng in

terc

ept.

me

fact

or p

rici

ng m

odel

s al

low

for

fiv

e, te

n, a

nd

fift

een

fact

ors (

K =

$10, 15

) est

imat

ed fr

om a

pre

lim

imuy

fac

tor a

naly

sis o

f th

e da

ily

ret~

tns o

f 75

0 ra

ndom

ly se

lect

ed se

curi

tka

The

mea

n-va

rian

ce

effi

cien

cy te

sts

use

the

CR

SP

equa

lly-

wei

ghte

d and

val

uew

eigh

ted

indi

ces (

K =

1).

F t

ests

use

260

wee

kly

obs

erva

tion

s and

&i-

squa

red

test

s us

e 1,

040

wee

kly

0bs

erva

tkM

UL

Pri

cing

rela

tion

F s

tati

stic

s fez

five

-yea

r sub

peri

odsb

A

ggre

gate

&i-

squa

red

(~V

a&E

!s ar

e gi

vez

k p

SeA

!ses

) st

atis

tic (

p-va

lue)

=

1963

01%

7 19

68-1

972

1973

-197

7 19

78-1

982

h%3-

1982

N=

=5

Iv=

20

N=

5 N

=2O

N

=S

N

=20

N=j

N=

20

N=

S

N--

20

-ZR

$P

prox

ies

W=

1)

W&

Y

6.15

1.

94

0.26

1.

40

0.87

0.

76

4.44

1.

36

46.8

3 10

3.77

W

iSig

htd

(O

.lO

EA

I3)

(0.0

1)

(0.9

1)

(0.1

3)

(0.4

8)

(0.7

5)

(0.0

02)

(0.1

5)

(0.7

2E-0

4)

(0.0

2)

Val

ue

1.98

I.

08

0.20

1.

51

1.56

1.

01

2.38

0.

79

30.5

7 83

.35

Wei

gh

ted

(0

.10)

(0

.37)

(0

.94)

(0

.09)

(0

.19)

(0

.45)

(0

.05)

(0

.72)

(0

.06)

(0

.26)

Fiv

e-

Raw

ret

urns

1.

37

0387

2.

01

1.54

1.

47

0.93

3.

56

I.13

42

.08

89.4

2 I;

?‘,*

= 0

) (0

.24)

(0

.6q

@08

) (0

.07)

(0

.20)

(0

.55)

(O

*OW

(0

.32)

(0

.003

) (0

.22)

W=

5)

E

xces

s ret

urns

1.

76

OH

1.

22

1.12

2.

12

1.12

3.

45

1.07

42

.76

84.8

9 &

#

0)

(0.1

2)

(O* W

(0

.30)

(0

.33)

(O

-06)

(0

.33)

(0

.005

) (0

.39)

(0

.002

) (0

.33)

T-0

R

aw re

turu

s 20

6 0.

95

1.68

1.

37

0.89

0.

78

2.22

0.

n 34

.24

77.5

5 fa

ctor

(A

0 = 0

) (O

-07)

(0

.53)

(0

.14)

(0

.14)

(0

.49)

(0

.73)

(0

.05)

(0

.74)

(0

.03)

(0

.56)

= (K

=

10)

Exc

essr

etur

us

1.81

0.

88

1.80

1.

26

1.12

0.

87

2.29

0.

78

35.1

4 75

.66

(ho

# 0

) (0

.11)

(0

.61)

(0

.11)

(0

.12)

(0

.35)

(0

.63)

(0

.05)

(0

.74)

(0

.02)

(0

.62)

Fif

teeu

- R

aw M

ums

206

0.85

1.

01

1.17

0.

87

0.70

2.

52

0.92

32

.26

72.7

9 fa

ctor

(h

o =

0)

(090

7)

(0.6

5)

(0.4

1)

(0.2

8)

(0.5

0)

(0.8

2)

(0.0

3)

(0.5

7)

(0*0

4)

(0.7

0)

(K=

lS)

Exc

ess r

etur

us

1.89

0.

81

1.23

1.

04

1.08

0.

74

2.21

0.

78

32.9

6 67

.47

(X0 #

0)

(0.1

0)

(0.7

1)

(0.2

9)

(0.4

1)

(0.3

7)

(0.7

8)

(0.W

(0

.73)

(0

*04)

(0

.84)

‘The

est

imat

ed fa

ctor

mod

el is

use

d to

com

pute

porG

otio

wei

ghts

whi

ch a

re c

ombi

ned w

ith

the

wee

kly

retu

ms o

f th

e 75

0 se

curi

ties

to p

rodu

ct

wee

kly

esti

mat

es of

the

fact

ors.

bE

ach

F st

atis

tic is

for t

he te

st of

the j

oiut

hyp

othe

sis th

at a

, = 0

in

the

appr

opri

ate p

rici

ng re

lati

ort.

For

the A

PT

test

s, th

e p-v

alue

is th

e pro

babi

ity

of o

btai

&g

a C

gr

catc

r tha

u th

e te

st st

atis

tic f

rom

au F

&&

ibuh

n w

ith

N n

umer

ator

degr

ees o

f fr

eedo

m au

d 26

0 - X

- iV

deuo

min

aiw

r de

gree

s of f

reed

om. F

or th

e CIU

P m

ean-

vari

auce

effi

cien

cy test

s, th

e p-v

alue

is th

e pro

babi

lity

of o

btai

niug

a re

ahza

tior

t gtea

ter t

hau

the

test

stat

isti

c fr

om a

u F

&tr

ibut

ion

wit

h N

- 1

uum

erat

or de

gree

s of f

reed

om au

d 26

0 - N

deu

omiu

ator

degr

ees o

f fre

edom

. %

a&

x2 s

tati

stic

for

the

aggr

egat

e tim

e per

iod i

s N

ti

mes

the

sum

of

the

four

subp

erio

d F s

tati

stic

s. Th

e p-

valu

e und

er e

ach

x2 s

tati

stic

is t

he

prob

abil

ity o

f ob

taiu

iug a

rea

liza

tiou

grea

ter t

hau

the

test

stat

isti

c fro

m a

x2

dist

ribu

tion

wit

h de

gree

s of

free

dom

equa

l to

20 w

hen

N =

5 a

nd 8

0 w

hen

N =

20

for t

he A

PT

test

s aud

wit

h deg

rees

of fr

eedo

m eq

ual t

o 16

whe

n N

= 5

and

76

whe

n N

= 2

0 fo

r the

CR

!W ux

au-v

aria

ucc e

tRci

eucy

test

s.

Tab

le 4

test

s of

exa

ct f

acto

r pr

icin

g m

odel

s (A

PT

) an

d of

the

mea

n-va

rian

ce e

ffic

ienc

y of

CR

SP

mar

ket

pro

xies

in

the

inte

rval

19

63-1

982.

Tes

ts a

re p

erfo

rmed

OR

five

(N

= 5

) an

d tw

enty

(N

= 2

0) e

qual

ly~

wei

ghte

d por

tf&

os

of N

YS

E a

nd A

ME

X s

ec~

niti

es gr

oupe

d on

the

bas

is o

f di

vide

~~

&y.

i&!.~

F s

tati

stic

s fo

r fo

ur s

ubpe

riod

s ad

aggr

egat

e &i-

squa

red

stat

isti

c fo

r th

e en

tire

per

iod

for

the j

oint

hyp

othe

sis

that

ai =

0 (

i =

1,.

. . ,5

or

i=

,...

,20)

ia

the

pzic

ing

rela

tion

Ei -

X

0 =

Ui +

Zf-

lb,X

, 9 w

here

Ei

is th

e ex

pect

ed n

etw

n

OII

div

iden

d-yi

eld

pott

foli

o i,

bik

is t

he

sen

siti

vity

Of

port

foli

o i

ta fa

ctor

k, A

, is

the r

isk p

rem

ium

of

the

kth

fac

tor,

and

X0

is t

he p

rici

ng in

terc

ept.

The

fac

tor

pric

ing

mod

els

allo

w f

or f

ive,

ten,

and

fi

ftee

n fa

ctor

s (#

= 5

, IO

, 15)

est

imat

ed fr

om a

pre

lim

inar

y fac

tor a

naly

sis o

f th

e da

ily

retu

rns o

f 75

0 ra

ndom

ly se

lect

ed se

curi

ties

! T

he m

ean-

vari

ance

ef

icie

ncy

test

s us

e th

e C

RS

P eq

~~

IIy~

w@

hted

and

valu

e-w

eigh

ted i

ndim

(K

= 1

). F

tes

ts us

e 26

0 w

eek

ly o

bser

vati

ons a

nd &

i-sq

uare

d te

sts

use

1,04

0 w

eek

ly o

bser

vati

ons.

-r

F

stat

isti

cs fo

r fi

ve-y

ear s

ubpe

riod

s A

ggre

gate

chi~

squa

red

(~~

a&s

are

give

n in

par

enth

eseQ

c st

atis

tic

( pqv

alue

)d

, 1%

3-19

67

1968

-197

2 19

73-1

977

1978

-198

2 19

63-1

982

Pri

cing

rela

tion

N

=5

N=

20

N=

5 N

=20

N

=5

N=

20

N=

5 N

=20

N

=s

Iv=

20

CR

SP

E

qual

ly

9.54

2.

40

0.96

0.

55

3.43

x.

21

7.58

2.

56

86.0

8 12

7.78

m

ark

et

Weig

hte

d

(0.3

3M)

(0.0

01)

(0.4

3)

(0.9

4)

(0.0

09)

(0.2

5)

(0.8

8E=

O5)

(0

.5lE

=O

3)

(O.l

SE

~lO

) (O

.l9E

-03)

pr

oxie

s &

x=

l>-

V&

R

2.18

1.

13

0.26

0.

44

2.64

1.

03

2.46

1.

02

30.1

5 68

.72

=&

*@i

(MU

) (0

.32)

(0

.90)

(0

.98)

(0

.04)

(0

#43

) (0

.05)

(O

-44)

(0

.02)

(0

.71)

Fiv

e-

Raw

re&

cns

1.47

0,

91

1.70

x.

11

1.56

0.

80

0.77

0.

69

27.4

8 70

.11

fW

(X0

e 0)

(s

.20)

(0

.57)

(0

.14)

(0

.35)

(0

.17)

(0

.71)

(0

.57)

(O

-84)

(0

.12)

(0

.78)

W=

5)

E

xces

s ret

urns

1.

44

0.92

0.

80

0.62

1.

76

0.73

1.

20

0.77

25

.99

61.0

1 (h

.0 f

0)

(0.2

1)

(0.5

6)

(0.5

5)

(0.8

9)

(0.1

2)

(0.7

9)

(0.3

1)

(0.7

5)

(0*1

7)

(0.9

4)

Ten

- R

aw r

etur

ns

2.67

1.

19

1.10

0.

96

0.85

0.

55

1.58

0.

70

31.0

1 67

.87

fact

or

(A,

= 0)

(0

.02)

(0

.26)

(0

.36)

(0

.52)

(0

.52)

(0

94)

(0.1

7)

(0.8

3)

(0%

) (0

.83)

(K= 1

0)

Exc

ess

retu

rns

2.44

1.

12

0.58

0.

54

0.97

0.

55

I.12

0.

67

25.5

4 57

.69

(&I

if 0

) (0

.04)

(0

.33)

(0

.72)

(0

.95j

(0

~4)

(0.9

4)

(0.3

5)

(0.8

5)

(0.1

8)

(099

7)

Fif

teen

- R

aw r

etur

ns

2.65

1.

15

0.64

0.

75

1.07

0.

54

1.56

0.

68

29.6

2 62

.32

fact

or

(k,

= 0)

(0

.02)

(0

.30)

(0

.67)

(0

.77)

(0

.38)

(0

.95)

(0

.17)

(O

-85)

(0

‘08)

(0

.93)

(K=15)

Eluxssretums 2

.51

1.12

0.

48

0.52

1.

15

0.51

1.

05

0.64

25

.96

55.5

9 (&

I +

Oj

(0.0

3)

(0.3

3j

(0=7

9)

(O*%

j (0

.33)

(0

0%)

(0.3

9)

(0.8

8)

(0.1

7)

(0.9

8)

“The

Grs

t por

tfol

io i

s an

equ

ally

-wei

ghte

d po

rtfo

lio o

f th

ose

stoc

ks t

hat p

aid

no d

ivid

ends

k

the

prec

edin

g pe

riod

. The

rem

aini

ng fo

ur o

r ni

nete

en

port

folio

s ar

e eq

ually

-wei

ghte

d po

tiol

ios

of t

he r

emai

ning

stoc

ks r

anke

d by

the

ir d

itid

end

yiei

d.

bThe

est

imat

ed f

acto

r m

odel

is

used

to

com

pute

por

tfol

io w

eigh

ts w

hich

are

com

bine

d w

ith t

he w

eekl

y re

turn

s of

the

750

sec

urit

ies

to p

rodu

ce

wee

kly

esti

mat

es o

f th

e fa

ctor

s.

‘Eac

h F

sta

tist

ic is

for

the

test

of

the j

oint

hyp

othe

sis

that

q =

0 in

the

app

ropr

iate

pric

ing

re&

&on

. For

the

AH

’ te

sts,

the

p_V

atue

is t

he p

roba

biht

y of

obt

aini

ng a

rea

lizat

ion

grea

ter t

han

the

test

sta

tist

ic f

rom

an

F d

istr

ibut

ion

with

N n

umer

ator

deg

rees

of

fr&

om

and

260

- K - N d

enom

inat

or

degr

ees

of f

reed

om* F

or t

he C

RSP

mea

n-va

rian

ce e

ffic

ienq

f tes

ts, t

he p

evab

te is

the

pro

babi

lity

of o

btai

ning

a r

ealiz

atio

n gr

eate

r tha

n th

e te

st s

tati

stic

fr

om a

n F

dis

trib

utio

n w

ith _

W Y 1

num

erat

or d

egre

es o

f fr

eedo

m a

nd 2

60 -

N d

enom

inat

or d

egre

es o

f fr

eedo

m.

dEac

h x2

sta

tist

ic f

or t

he a

ggre

gate

tim

e pe

riod

is N

tim

es t

he s

um o

f th

e fo

ur s

ubpe

riod

F s

tati

stic

s. T

he p

-val

ue u

nder

eac

h x2

sta

tist

ic i;

i; th

e pr

obab

ility

of

obta

inin

g a

r&Ji

zati

on gr

eate

r tha

n th

e te

st s

tati

stic

fro

m a

x2

dist

ribu

tion

with

deg

rees

of

free

dom

equ

al t

o 20

whe

n N

= 5

and

80

whe

n N

= 2

0 fo

r th

e A

PT

’ tes

ts a

nd w

ith d

egre

es o

f fr

eedo

m eq

ual t

o 16

whe

n N = 5

and

76

whe

n N

= 2

0 fo

r th

e C

RSP

mea

n-va

rian

ce e

ffic

ienc

y te

sts.

Tab

le 5

0wn

wu

ian

F’-b

ased

te

sts o

f ex

act

fact

or p

rici

ng m

odel

s (A

PT

) and

of

the

mea

n-va

rian

ce e

ffic

ienc

y of

Cm

P

mar

ket

pro

xies

in t

he in

terv

al 1

963-

1982

.

Tat

s ar

e pe

rfor

med

on

five

(N

= 5

) an

d tw

enty

(N

= 2

0) e

quaU

y=w

eigh

ted po

rtfo

lios

of

NY

SE

an

d A

ME

X

secu

riti

es g

rou

ped

on

the

basi

s of

ow

xwar

hce

. F

stat

isti

cs fo

r fo

ur w

bpek

ds

and

qgre

g at

e ch

i~sq

uare

d sta

tist

ic fo

r th

e en

tire

p&

od

for

the j

oint

hyp

othe

sis

that

ai =

0 (

i =

1,.

. . ,5

or

i--

l ,.

..,2

O)i

nthe

pric

ingr

elat

i~

Ei-

$j=

$d_Z

kp1

ik

k,

Q x

w

here

Ei

is th

e ex

geC

&d M

Urn

On O

W!k

V&

B

PO

dOfi

O

is

bik

& &

e S#

Zd~

V@

Of

pa

rtfo

lio

i

t0

fact

or k

, xk

is

the

risk

pre

rmut

u of

the

kth

fac

tor,

and

ho

is t

he p

rici

ng in

terc

ept.

The

fac

tor

pik

ing

mod

els

aNow

for

five

, ten

, and

fi

ftee

n fa

ctor

s (K

= S

,lO

, 15)

est

imat

t fr

om a

pre

lim

imuy

fac

tor a

na@

is o

f th

e da

ily

retu

ms

of 7

50 ra

ndom

ly s

elec

ted

secu

ritk

~~

The

mea

n-va

rian

ce

effi

cien

cy te

sts

use

the

CR

SP

equa

Uy=

wei

ghte

d and

valu

e-w

eigh

ted i

ndic

es (K

=

1). F

tes

ts us

e 26

0 w

eek

ly o

bser