The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role...

11

Cont ents list s ava ilable at ScienceDirect Management Accounting Research j ou r nal hom e p a g e: www.elsevier.com/locate/mar Theeffectsof incentivesubjectivityandstrategy communication onknowledge-sharing andextra-role behaviours MandyM.Cheng a,∗ ,RodneyCoyte b a School of Acc ounting, TheUnivers ity of New South Wal es, NSW 2052 , Aust ralia b The Uni vers ity of Syd ney Bus ine ss Sch ool, NSW 2006, Aus tral ia articleinfo Keywords: Extra-role behaviours Knowl edge shari ng Incentive scheme Performance manag ement syste ms abstract Thisstudyexaminestheeffectsof performancemeasurement systemdesignonemployees’ willingnesstoshareknowledgeandtheirgeneraltendencytopursueextra-rolebehaviours. Two ke y d es i gnissuesareexamined, namely, incentiveschemesubjectivityandcom- municatingthevalueof human-basedintangibleassetsthrougha strategymap.Usinga controlledexperiment wefoundthatemployeesaremorewillingtoshareknowledgewith a co- wor ker(evenif itmeansdivertingresourcesawayfromincentivisedareas)under a sub jec tiv eweightingschemethan aformula-basedscheme. Inaddition, wefoundan interaction effectwherethecommunicationof thestrategicvalueof human-basedintangi- ble ass ets increasesemployees’ generaltendencytopursueextra-rolebehavioursundera subjectiveweightingscheme, butdecreasesthistendencyundera formula-b asedscheme. Our stu dycontributestotheperformancemanagement literatureandhas impli cationsfor practi ce by pro vid ingempirical evidencedemonstratinghowthedesignof performance measurement systemscanmotivatediscretionarybehaviours inrelationtoperformance areasthatarenotrecognisedby t heformalincentivescheme. ©2013ElsevierLtd.Allrightsreserved. 1. Introduc ti on As th e us e of mu lt ip le perf o rm anc e m eas ur es gain s gr eater populari ty in cont empo rary pe rf ormanc e me a- surement systems, there is an on-going discourse on the meri ts of us ing su bj ec ti ve we ight ing vers us formul a- based weightin g sch eme s in evaluating and compensatin g empl oyee s. Subj ecti vity in perfo rmanc e meas urement can take many forms, for exampl e, by al lowi ng supe rvis ors to make subjective perf ormance ratings or gi vi ng them dis- cretion over the size of bonus pools. The current study focuses on al lowi ng subj ec ti vi ty over pe rf ormance mea- sure we ight ing when supe rvis ors determine empl oyees’ ∗ Corres ponding author. Tel. : +61 2 9385 6343; fax: +61 2 9385 5925. E-mail addre sses: [email protected] (M.M.Cheng), [email protected] (R. Coyte) . comp en sati on. Pr ior li te rature sugg es ts that while sub- jective weighting schemes suffer from problems such as favourit is m, comp ress ion bi as es and leni ency bi as es (e.g. Itt ner etal., 200 3; Moers,200 5), theyalsohave a numberof advan tage s over formu la-b ased ince ntiv e sche mes, such as allowing firms to exp loit non-c ontra ctibl e infor matio n and to mi ti gate dysf unct ional behavi ours induced by incom- plet e perf ormance measures (e.g . Bai man and Raj an,1995; Bake r et al ., 1994). Wecontribute to this lit era ture by examinin g the eff ect of su bj ec ti ve we ighting ve rsus formula-based incentive schemes on indi vi dual s’ wi ll ingness to share knowledge with a co-wor ker, an d on their tend en cy to pursue ex tr a- role beh avi ours (i. e. des ira ble discre tio nar y act ivities tha t are not exp licit ly recog nise d by the forma l rewa rd scheme). Because of the purported competitive advantage and organisational learni ng benefits derived from kno wl edg e- sh ari ng and e xtr a -ro le be hav io urs (e .g . Burney et al., 1044-5 005 /$ – see front mat ter © 201 3 Elsevier Ltd . All rig hts res erv ed. http://dx.doi.org/10.1016/j.mar.2013.07.003

-

Upload

hector-guzman -

Category

Documents

-

view

5 -

download

0

description

the effect of incentive subjectivity

Transcript of The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role...

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 1/11

Contents lists available at ScienceDirect

Management Accounting Research

j o u r n a l h o m e p a g e : w w w. e l s e v i e r. c o m / l o c a t e / m a r

The effects of incentive subjectivity and strategycommunication on knowledge-sharing and extra-rolebehaviours

Mandy M. Cheng a , , Rodney Coyte b

a School of Accounting, The University of New South Wales, NSW 2052, Australiab The University of Sydney Business School, NSW 2006, Australia

a r t i c l e i n f o

Keywords:Extra-role behavioursKnowledge sharingIncentive schemePerformance management systems

a b s t r a c t

Thisstudy examines the effects of performance measurement system design on employees’willingness to share knowledge and their general tendency to pursue extra-role behaviours.Two key design issues are examined, namely, incentive scheme subjectivity and com-municating the value of human-based intangible assets through a strategy map. Using acontrolled experiment we found that employees are more willing to share knowledge witha co-worker (even if it means diverting resources away from incentivised areas) undera subjective weighting scheme than a formula-based scheme. In addition, we found aninteraction effect where the communication of the strategic value of human-based intangi-ble assets increases employees’ general tendency to pursue extra-role behaviours under asubjective weighting scheme, but decreases this tendency under a formula-based scheme.Our study contributes to the performance management literature and has implications forpractice by providing empirical evidence demonstrating how the design of performancemeasurement systems can motivate discretionary behaviours in relation to performanceareas that are not recognised by the formal incentive scheme.

© 2013 Elsevier Ltd. All rights reserved.

1. Introduction

As the use of multiple performance measures gainsgreater popularity in contemporary performance mea-surement systems, there is an on-going discourse onthe merits of using subjective weighting versus formula-based weighting schemes in evaluating and compensatingemployees. Subjectivity in performance measurement cantake many forms, for example, by allowing supervisors tomake subjective performance ratings or giving them dis-cretion over the size of bonus pools. The current studyfocuses on allowing subjectivity over performance mea-sure weighting when supervisors determine employees’

Corresponding author. Tel.: +61 2 9385 6343; fax: +61 2 9385 5925.E-mail addresses: [email protected] (M.M. Cheng),

[email protected] (R. Coyte).

compensation. Prior literature suggests that while sub- jective weighting schemes suffer from problems such asfavouritism, compression biases and leniency biases (e.g.Ittneret al., 2003; Moers,2005 ), theyalsohave a number of advantages over formula-based incentive schemes, such asallowing rms to exploit non-contractible information andto mitigate dysfunctional behaviours induced by incom-plete performance measures (e.g. Baiman and Rajan, 1995;Baker et al., 1994 ).

We contribute to this literature by examining the effectof subjective weighting versus formula-based incentiveschemes on individuals’ willingness to share knowledgewith a co-worker, and on their tendency to pursue extra-role behaviours (i.e. desirable discretionary activities thatarenot explicitly recognised by theformal reward scheme).Because of the purported competitive advantage andorganisational learning benets derived from knowledge-sharing and extra-role behaviours (e.g. Burney et al.,

1044-5005/$ – see front matter © 2013 Elsevier Ltd. All rights reserved.http://dx.doi.org/10.1016/j.mar.2013.07.003

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 2/11

. . , .

2009; Chow et al., 2000 ), it is important to better under-stand how performance incentive schemes affect thesebehaviours.

In addition, the performance incentive scheme is onlyone aspect of the overall performance management sys-tem ( Otley, 1999 ). It is often recommended that a rmshould clearly communicate its strategic objectives to itsemployees to encouragegoalalignment behaviours. In par-ticular, Kaplan and Norton (2004) argue that managersshould use a strategy map to illustrate and explain to theiremployees how a rm’s intangible assets, including its

human capital (i.e. knowledge, skills and value), have thepotentialto accomplish their strategicgoals. Thesecondaryaim of this study is to examine whether communicat-ing the strategic role of a rm’s human-based intangibleassets (HIA) moderates the effect of the rm’s incentiveschemes on employees’ knowledge-sharing and extra-rolebehaviours.

Examining the effect of these two performance mea-surement system design choices on employees’ knowledgesharing (i.e. the willingness of individuals to share theknowledge acquired or created with others) and extra-role behaviours is important for a number of reasons. First,knowledge sharing underliesknowledge development and

exploitation within a rm, and is widely recognised as akeybasisfor competitiveadvantage( Nonaka and Takeuchi,1995;Spender, 1996;Teece,2000; Vera-Mu nozet al., 2006;Grant, 2010 ) and organisational learning ( Senge, 1990;Huber, 1990; Chenhall, 2005 ). Yet evidence demonstratingthe effectiveness of directly rewarding employees on theirknowledge-sharing behaviours has been mixed (e.g. Wolfeand Loraas, 2008; Bock et al., 2005 ). With the exception of a number of studies that examine the inuence of culture(e.g. Chow et al., 1999, 2000 ) and group-based incentives(e.g. Taylor, 2006 ), there is generally limited accountingresearch on how management accountants can inuenceknowledge sharing. Findings from this study add to our

understanding in this area by demonstrating that subjec-tiveweighting schemesaremorelikely thanformula-basedschemes to induce knowledge sharing.

Second, not all performance areas can be reliablymeasured and therefore formally incorporated into anemployee’s incentive scheme. Increased complexity and acontinuously changing environment mean that employeesare often relied upon to do the “right thing” to the benetof their rm, in any particular decision-making situation,even though that particular dimension of their work taskmay not be formally recognised in the incentive scheme.Indeed, a number of recent studies have found that suchextra-role behaviours have positive implications on both

individual and rm level performance (e.g. Burney et al.,2009; Podsakoffet al., 2009 ). Thus, understandinghowper-formance management system design affects individuals’willingnesstoengagein extra-role behaviours is alsohighlyimportant.

This study reports an experiment where we manip-ulated the type of incentive scheme (formula-basedversus subjective) and investigated whether the strate-gic value of a rm’s HIA is explicitly communicated toemployees via a strategy map. We argue that these twoperformance measurement system aspects will shift the

perceived costs and benets associated with engagingin knowledge-sharing and extra-role behaviours. Consis-tent with our expectations, we found that employeeswere more willing to share their knowledge with a co-worker (at the expense of pursuing their incentivisedactivities) under a subjectiveweighting scheme thanundera formula-based scheme. We also found an interactioneffect, which indicated that using a strategy map toillustrate the link between a rm’s HIA and its overallstrategic goal increased employees’ tendency to pur-sue extra-role behaviour under a subjective weighting

scheme, but decreased this tendency under a formula-based scheme.

Our study makes a number of contributions to theaccounting literature. First, while prior analytical stud-ies have discussed and modelled the importance of using“implicit contracts” in the form of subjectivity in designingincentive schemes (e.g. Budde, 2007; Baiman and Rajan,1995; Baker et al., 1994 ), our study provides experimen-tal evidence that subjectivity in compensation weightingencourages knowledge sharing and also positively impactson employees’ general tendency to perform extra-rolebehaviours. Importantly, our study shows that employeescanbemotivatedto pursuethese desirablebehaviourseven

in the absence of direct and specic performance meas-ures on these areas,by changingthe waythe compensationschemeis designedandthe way strategic goalsarecommu-nicated.

Second, despite the importance of understandingemployees’ tendency to share knowledge and performextra-role behaviours, empirical studies on the inuenceof performance measurement systems on these behaviourshave been limited. We contribute by providing evidenceon the role of incentive system design, and therefore thepotential role of the management accountant, in encour-aging knowledge-sharing behaviour. Further, Burney et al.(2009) recently showed that providing employees with a

performance management system incorporating a validstrategic causal model enhances individuals’ willingnessto perform organisation citizenship behaviour. Our studycomplements their survey research by highlighting thepotential moderating role of incentive scheme design inthese relationships.

Third, while the strategy map is considered a criti-cal part of a strategic performance management system(e.g. Banker et al., 2009; Cheng and Humphreys, 2012;Kaplan and Norton, 2004 ), it has so far received verylittle attention in the accounting literature. Our studycontributes to this small but growing literature by exam-ining the effect of using the strategy map to communicate

the strategic value of HIA on managers’ effort allocationbehaviour.

The rest of the paper is structured as follows. In Sec-tion 2 we present a set of hypotheses, rstly concerningknowledge-sharing behaviour, and secondly, individuals’general tendency to perform extra-role behaviour. Next,Section 3 outlines the experimental design and process,followed by Section 4, which presents our results; nally,Section 5 concludes and discusses the implications of ourndings, and thefuturedirections suggested by thestudy’slimitations.

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 3/11

. . , .

2. Hypothesis development

2.1. The effect of subjective versus formula-basedincentive schemes on knowledge sharing

The inclusion of multiple performance measures in anincentive scheme is one attempt to overcome the limita-tionof using a single,nancial-based performance measureto (control and) evaluate an agent’s performance (e.g.Datar et al., 2001; Feltham and Xie, 1994 ). Despite theincorporationof multipleperformancemeasures,however,

incentive contractsoftenremain incomplete. Manyaspectsof an agent’s (e.g. the employee being evaluated) perfor-mance are not explicitly contractible due to the lack of veriable and reliable measures, even though these per-formance aspects may be observed by the principal (e.g.the supervisor) by “walking around the ofce or factory”or through informal communication channels ( Baiman andRajan, 1995; Baker et al., 1994 ).

A major example of a difcult-to-contract performanceaspect is knowledge sharing by employees. Knowledgesharing refers to the willingness of individuals in an orga-nisation to share with others the knowledge they havecreated or acquired ( Bock et al., 2005; Gibbert and Krause,

2002 ). More recently, Wolfe and Loraas (2008) enhanceunderstanding of such behaviour, arguing that individu-als differentiate between sharing proprietary knowledge(i.e. knowledge that separates them from other employ-ees) and general organisational knowledge (i.e. knowledgethat does not distinguish an individual from other employ-ees).

Knowledge sharing can be formal, such as establish-ing IT-based knowledge databases where employees cancontribute their ideas. It can also occur more infor-mally, through employees’ discussion and interaction (e.g.when sharing their experience relating to dealing with aparticular type of clientproblem, strategy solution or oper-

ational improvement approach). While neitherapproachtoknowledge sharing is amenable to precise measurement,the latter, more informal approach to knowledge sharing isparticularly difcult to quantify. The supervisor can oftenonly identify such behaviours through other channels, forexample, via dialogue with employees and direct observa-tions.

Even if knowledge-sharing behaviours were readilyquantiable, prior research has found that attempts todirectly compensate knowledge sharing via a formalincentive scheme may be problematic or even counter-productive. Bock etal. (2005) , f or example,found a negativerelationship between anticipated extrinsic rewards and

knowledge-sharing intention. Bock et al. (2005) arguethat this result might be attributed to the destruction of individuals’ intrinsic motivation to share knowledge byextrinsic reward. Another, less direct, approach to encour-aging knowledge sharing among employees is throughgroup-based incentive schemes. A number of accountingstudieshaveshown thatgroup-based incentives encourageknowledge-sharing and helping behaviours between teammembers (e.g. Drake et al., 1999; Taylor, 2006 ). These stud-ies,however, typicallyfocus on scenarioswhere employeesengage in tasks with a high degree of interdependency,

and are working in teams. 1 It is unclear whether group-based incentives are appropriate beyond assembly linesand team work contexts. Group-based incentives alsohave limitations, including the potential for opportunisticbehaviours, such as social loang ( van der Heijdenmet al., 2009; Fisher et al., 2005 ). In this study, we proposethat, in the absence of a direct and explicit link betweenknowledge-sharing behaviour and compensation, the typeof incentive schemes (formula-based versus subjectiveweighting) will impact on employees’ willingness to shareknowledge.

Specically, an incentive scheme can vary in terms of the level of subjectivity involved. Subjectivity can take theform of exibility over performance weighting, discretionover adjusting the bonuses upward or downward, the useof subjective ratings, andexibility in includingjob dimen-sions ( Ittner et al., 2003 ). In this study, we are interestedin comparing a subjective weighting scheme, where thesupervisor has discretion over the weighting of variousperformance dimensions, with a formula-based scheme,where the supervisor must evaluate thesubordinate basedon pre-determined weights.

We propose that employees are more willing toshare knowledge if they are working under a subjective

weightingscheme than a formula-based incentive scheme.Economic theories argue that agents/employees are moti-vated by self-interest. This suggests that, in general, agentswill allocate effort to the pursuit of a particular activity if the perceived personal benets in doing so outweigh theperceivedcosts. Wherethere is no incentivefor knowledgesharing, the perceived personal benets will mainly com-prise intrinsic rewards, such as the satisfaction of assistingco-workers, anenhancedsenseof self-worth, andanexpec-tation of reciprocity (e.g. Bock et al., 2005; Wolfe andLoraas, 2008 ). The perceived personal costs include thetime and effort involved, which could have been spent onother incentivisedactivities. Thehigher these costsrelative

to the perceived benets, the less willing the employee toengage in knowledge-sharing behaviour.

Under a formula-based scheme, the cost of knowledgesharing is highly salient. Because incentives are based on apre-determined formula where no subjectivity regardingthe relative weights of each performance dimension isallowed, the supervisor does not have any discretion toadjust the weights of different performance dimensionsto take into account the knowledge-sharing activity. Thismeans that anytime/effortspentawayfrom improvingoneof the incentivised activities is likely to reduce a manager’sopportunity to obtain a bigger nancial reward.

In contrast, a subjective weighting scheme effectively

incorporates an implicit contract where the supervisorhas an opportunity to moderate any distortion createdby explicit contracts ( Baker et al., 1994 ). For example,if an employee’s knowledge-sharing activity results in

1 In Drake et al. (1999) participants worked on a Lego assembling taskwith each workerin theteambuilding onthe work ofthe previousworker.Taylor’s (2006) task involved participants locating spreadsheet errorstogether in groups; each member of a group received a spreadsheet withsimilar types of errors, such that group members canhelp each other withtheir problems.

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 4/11

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 5/11

. . , .

theories (e.g. Adams, 1965 ) predict that individuals judgetheir relationships with thermas a series of “give or take”interactions. Any dissatisfaction with the exchange rela-tionship willresult in negativebehavioural responses, suchas workplace deviance behaviours (e.g. intentionally arriv-ing late to work, taking undeserved breaks) ( Bordia et al.,2008; Restubog et al., 2008 ). We posit that employees willsee the act of sharing knowledge under a formula-basedscheme as an unfair exchange, because their potentialcontribution to the organisation is penalised rather thanrewarded. Thus, we expect that under a formula-based

scheme, communicating the strategic value of HIA willactuallyreduce employees’ willingness to shareknowledgewith their co-workers. Instead, it will cause employees toallocate relatively greater effort to other incentivised per-formance areas, the importance of which are also mademore salient by the strategy map. This leads to our secondhypothesis:

H2. The introduction of a strategy map that communi-cates how the rm’s human-based intangible assets cancontribute to its strategic goals will increase employees’willingness to share knowledge with a co-worker undera subjective weighting incentive scheme, but decreasesemployees’ willingness to share knowledge with a co-worker under a formula-based incentive scheme.

2.3. Incentive schemes, communication of the strategic value of HIA, and extra-role behaviours

In addition to knowledgesharing, wealso examine indi-viduals’ more general tendency to engage in extra-rolebehaviours. Extra-role behaviour, also known as ‘organ-isational citizenship behaviour’, refers to a discretionaryactivity not directly or explicitly recognised by the for-mal reward system and which promotes the efcient andeffective functioning of the rm ( Organ, 1988; Podsakoff

et al., 2000 ).2

Extra-role behaviours “involve helping oth-ers with, or preventing the occurrence of, work relatedproblems” ( Podsakoff et al., 2000 , p. 516). Such activitiesgo beyond the minimum requirements of the employee’swork and thus take on a ‘voluntary avour ’ (e.g. Burneyet al., 2009; Podsakoff et al., 2000 ). Examples of extra-role behaviours include helping other employees whohave a heavy workload or have been absent, and listen-ing to colleagues’ problems and worries and offering tohelp. 3

In this study, we propose that the two aspects of aperformance measurement system, the type of incentivescheme and the communication of the strategic value

of HIA, will also affect individuals’ general tendency topursue extra-role behaviours. However, the magnitude of these effects on individuals’ general tendency to pursue

2 While the two terms are often seen as interchangeable, extra-rolebehaviouris a broader conceptthan organisational citizenship behaviour;the latter may also include in-role behaviours ( Vey and Campbell, 2004 ).

3 In thisstudy we focus on individuals’ tendency to engage in ‘helpingbehaviour’ – a prominent example of extra-role behaviour that is oftenconsidered as the most important form of extra-role behaviours (refer toPodsakoff et al., 2000 f or a comprehensive review).

extra-role behaviours differs when compared with knowl-edge sharing for two reasons.

First, ndings from prior literature suggest that theimpact of economic incentives on individuals’ generaltendency to pursue extra-role behaviours is likely tobe smaller than the incentive impact on knowledge-sharing behaviour. Wolfe and Loraas (2008) suggestedthat, because sharing proprietary knowledge representsan act of giving up ‘economic rents’, the intention toshare proprietary knowledge is more likely to be gov-erned by economic concerns than the intention to share

knowledge generally available to all employees (whichis more likely to be inuenced by social concerns). Inthe current context, performing extra-role behavioursin general is less likely to be seen as being associatedwith giving up economic rents, compared with sharingvaluable business knowledge (our variable of interest inH1 and H2). As such, the general tendency to performextra-role behaviours may be less sensitive to whethera subjective weighting or a formula-based scheme is inplace.

Second, in the absence of a clear communication of the strategic value of HIA to employees, the function of extra-role behaviours in the achievement of their rm’s

strategic goals is likely to be seen as weaker than thelink between knowledge sharing and the rm’s strategicgoals. If this is the case, then the effect of communi-cating the importance of HIA via a strategy map willhave a greater effect on individuals’ general tendencyto perform extra-role behaviours than their willingnessto engage in knowledge sharing. By highlighting thestrategic importance of HIA, a strategy map can increaseemployees’ awareness that activities directed towardsimproving the work of other employees have signi-cance for the rm, thereby establishing a stronger linkbetween extra-role behaviours and valuable rm out-comes.

To summarise, past literature indicates that the effectof the type of incentive schemeon individuals’ tendency toperform extra-role behaviours is likely to be smaller, whilethe moderating role of a strategy map that communicatesthe importance of HIA is likely to be more signicant. Thedirection of these impacts, however, is expected to be thesameas the impact of these two performancemanagementsystem aspects on knowledge-sharingbehaviour. To inves-tigatetheextenttowhichthesetwoaspectsofperformancemanagement systems inuence individuals’ general ten-dency to perform extra-role behaviours, we formally testthe following two hypotheses which are parallel to H1 andH2:

H3. Managers’ tendencyto perform extra-role behavioursis higher under a subjective weighting incentive schemethan a formula-based incentive scheme.

H4. The introduction of a strategy map that communi-cates how the rm’s human-based intangible assets cancontribute to its strategic goals will increase employ-ees’ tendency to perform extra-role behaviours undera subjective weighting incentive scheme, but decreasesemployees’ willingness to perform extra-role behavioursunder a formula-based incentive scheme.

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 6/11

. . , .

3. Research method

3.1. Research design

We test theproposed hypotheses usinga 2 × 2 between-subject controlled experiment. The two independentvariables are type of incentive scheme (formula-basedscheme versus subjective weighting scheme) and whetherthe strategic value of HIA is communicated to employ-ees using a strategy map (presence versus absence of communication).The dependent variables are participants’reported willingness to share knowledge with a co-workerand to perform extra-role behaviours in a ctitious consul-ting rm (discussed in Section 3.2 ).

3.2. Research task and dependent variables

Participants assumed the role of a management con-sultant at a consulting rm, Alpha Consulting. Participantswere told that the overall goal of Alpha Consulting wasto increase fee revenue and, in line with this goal, theirmonthly performance would be evaluated based on fourperformance areas: billable hours, billable rates, dollarvalue of future work requested by clients, and client’sevaluations. 4 Using a scenario similar to Chow et al. (2000) ,participants were told that, over the last few years, theyhad built up substantial knowledge and expertise aboutIndustry X, such as a list of useful contacts and relevantbenchmark information. To measure the rst dependentvariable,willingnessto shareknowledge,participantswereasked whether they were willing to spend their time shar-ing this knowledge with a new colleague, Jones, in anotherdepartment (Tax Advisory Department) of Alpha Consul-ting, who was given a portfolio of tax clients in Industry X.It was made clear that although Jones came from a differ-ent department (Tax Advisory), and therefore was not indirect competition with the role assigned to participants,theamountof time spenton sharing this knowledge wouldresultin a delay to oneof theclientprojects theparticipantsaimed to start this month and would also lower the num-ber of billable hours for the participant in this month. Ourscenario therefore suggests potential costs to knowledgesharing.

To measureour second dependent variable,generalten-dency to perform extra-role behaviours, participants werealso asked to respond to six questions based on Williamsand Anderson’s (1991) OCB-Iscale. Specically, these ques-tions ask participants to indicate the extent to which theyarewillingto help co-workers when they have been absent,help co-workerswith heavyworkload,taketimeto listentoco-workers’ problems, go out of their way to help new co-workers, take a personal interest in co-workers, and passalong information to co-workers.

4 These fourwork dimensions are common focuses of business consul-ting rms. ‘Billable hours’ measures the ‘volume’ effect of getting clientwork,and ‘billingrates’ isindicative of thelevel of the expertisecontractedby theclientand whether the consulting work is of sufciently high qual-ity todemand higherprices.Both‘dollarvalueof futureworkrequested byclients’ and ‘clients’ evaluations’ are forward looking measures that indi-cate the potential for creating more volume in the future and the abilityto charge higher prices (rates) by satisfying clients.

After the dependent variables were measured, partic-ipants completed a post-test questionnaire that includedtwo manipulation check questions and a demographicsurvey. The manipulation check questions asked partici-pants to indicate (a) whether the performance incentivescheme at Alpha Consulting involved explicit weights, and(b) whether the participants received a diagram depictingthe company’s strategic goals.

3.3. Independent variables

To manipulate the rst independent variable, type of incentive scheme, participants in the formula-based incen-tive scheme (“formula-based scheme”) treatment weretold that, for the purpose of monthly performance eval-uation, explicit weights were assigned to each of the fourperformance areas (25% each). 5 The weighted rating wasthen used as a basis for determining monthly bonuses.Further, the supervisor was not allowed any subjectiv-ity or exibility in the weighting process. In contrast,participants in the subjective incentive scheme (“sub- jective scheme”) treatment were told that no explicitweights were assigned to each performance area, and thattheir supervisor was allowed the exibility to make a

subjective judgement on their performance rating basedon their overall achievements on these four areas (seeFig. 1 ).

For the second independent variable, we manipulatedwhether the communication of the strategic value of HIA via a strategy map is present or absent. Consis-tent with prior literature such as Banker et al. (2004)we provided participants in the “HIA communicationpresent” treatment with a diagram illustrating the link-ages between Alpha Consulting’s strategic objectives;whereas the diagram was omitted in the “HIA commu-nication absent” treatment. Specically, participants inthe “HIA communication present” treatment received a

diagram (i.e. a simple strategy map) explicating howthe actions of the consultants at Alpha Consulting cancreate rm value, for example, by building the rm’sand their expertise (see Fig. 2 ). Because the interest of the current study lies in the effect of communicatingto employees the links between the rm’s HIA and itsultimate goal of increasing fee revenue, we provided par-ticipants with a very basic strategy map that fulls thisrole. 6

The strategy map was also carefully designed to ensurethat the importance of HIA was highlighted but withoutexplicitly referring to knowledge-sharing and extra-rolebehaviours. Further, the strategic objectives shown in the

5 Equal weights were used to avoid any unintentional signalling aboutpriorities between relativeperformance dimensionsthat couldhave inu-encedparticipants( Edmisterand Locke,1987 ). However, in futurestudies,differential weightings may be used to examine the impact of higher orlower weights on the performance dimensions most directly related toknowledge sharing behaviour.

6 We acknowledge that a strategy map based on Kaplan and Norton’s(2004) balanced scorecard framework usually contains more comprehen-sive strategy information and links. However, given our research interest,we decided to provide participantswith a simplemap that focuseson thelinks between HIA and the ctitious rm’s ultimate strategic goals.

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 7/11

. . , .

Subjective incentive scheme

The overall goal of Alpha Consulting is to increase its fee revenue from clients. Inline with this, your performance as a management consultant at Alpha Consulting isevaluated based on the following four areas :

• Billable hours (total number of work hours you charged to clients this month);• Average billing rate you charged to your clients this month ($);• Total revenue from new project work requested by your clients this month; and• Evaluations by your clients (based on survey ratings of your performance this month).

Your supervisor evaluates your performance on the above four areas against othermanagement consultants. Each month your supervisor is allowed the flexibility tomake a subjective judgement based on your overall achievements in these fourareas. The average of the monthly evaluation ratings you receive from yoursupervisor will determine your annual bonus.

Formula-based incentive scheme

The overall goal of Alpha Consulting is to increase its fee revenue from clients. Inline with this, your performance as a management consultant at Alpha Consulting isevaluated based on the following four areas :

Monthly performance area: AssignedWeighting

(1). Billable hours (total number of work hours you charged to clients thismonth);

25%

(2). Average billing rate you charged to your clients this month ($); 25%

(3). Total revenue from new project work requested by your clients this

month;

25%

(4). Evaluations by your clients (based on survey ratings of your performancethis month).

25%

Total 100%

Each month, your supervisor evaluates your performance on the above four areasagainst other management consultants. Your supervisor is required to evaluate yourmonthly performance based on the explicit weights assigned to each performancearea as indicated above. No subjectivity or flexibility is allowed in this process. Theaverage of the monthly evaluation ratings you receive from your supervisor willdetermine your annual bonus.

Fig. 1. Incentive scheme manipulations.

strategy map were consistent with the four performancedimensions in the incentive scheme for consultants. 7

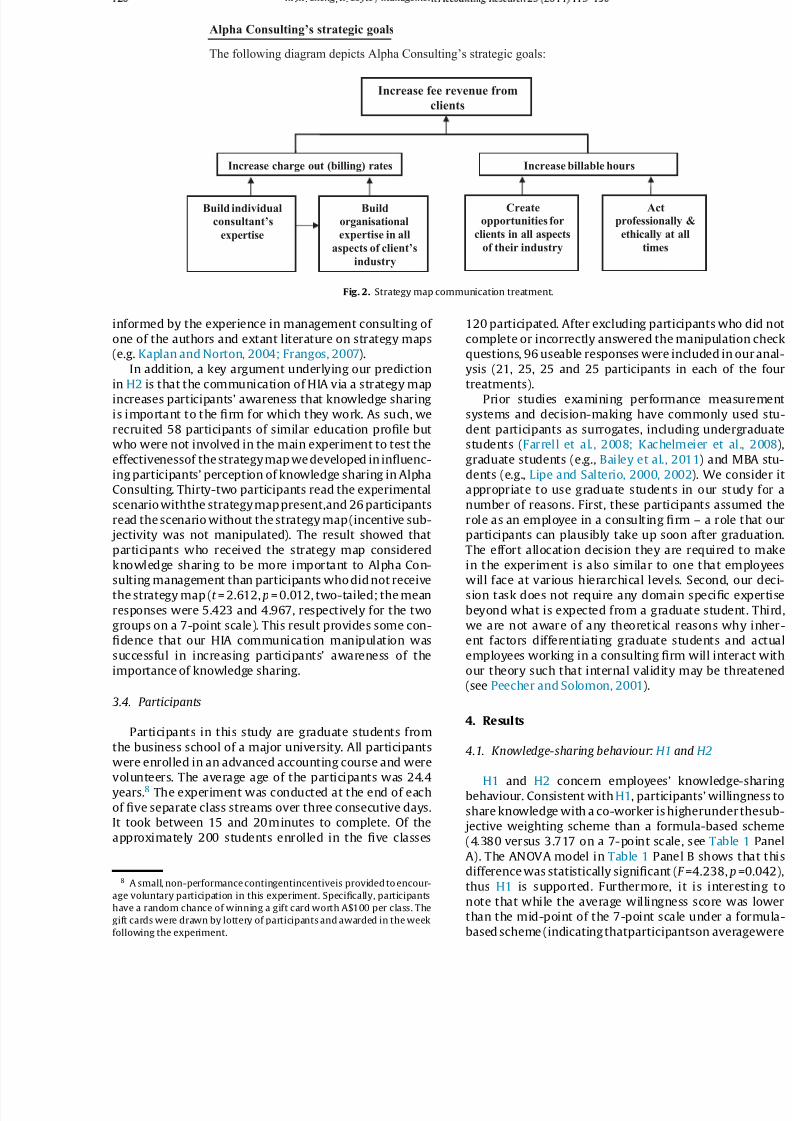

7 Specically, the strategy map (see Fig. 2 ) shows that increased feerevenue – the overall goal of the rm– is driven by increasing charge-outrates and billable hours. The right side of the strategy map shows thatthe volume of work, represented by the objective ‘increases in billablehours’, can be achieved through creating more opportunities for clientsin an ethical and professional manner. The left side of the strategy mapshowsthe ‘quality’effect; buildingindividual andorganisationalexpertise

Although rudimentary, the strategy map reects a keyfocus of consulting rms in practice and its design was

arekeysto inuencing theabilityof theconsultantsand therm to chargehigherbilling rates.Thus, consistentwith theliterature from practice,thestrategy map highlights how HIA, including knowledge (expertise), skills(developingnew opportunities), and value (acting professionally and eth-ically), cancontribute to therm’sstrategic goals (see Kaplan and Norton,2004 ).

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 8/11

. . , .

Alpha Consulting’s strategic goals

The following diagram depicts Alpha Consulting’s strategic goals:

Increase fee revenue fromclients

Increase billable hoursIncrease charge out (billing) rates

Createopportunities for

clients in all aspectsof their industry

Actprofessionally &

ethically at alltimes

Build individualconsultant’s

expertise

Buildorganisationalexpertise in all

aspects of client’sindustry

Fig. 2. Strategy map communication treatment.

informed by the experience in management consulting of one of the authors and extant literature on strategy maps(e.g. Kaplan and Norton, 2004; Frangos, 2007 ).

In addition, a key argument underlying our predictionin H2 is that the communication of HIA via a strategy mapincreases participants’ awareness that knowledge sharingis important to the rm for which they work. As such, werecruited 58 participants of similar education prole butwho were not involved in the main experiment to test theeffectivenessof thestrategymap wedeveloped in inuenc-ing participants’ perception of knowledge sharing in AlphaConsulting. Thirty-two participants read the experimentalscenario withthe strategymap present,and 26 participantsread the scenario without the strategy map (incentive sub- jectivity was not manipulated). The result showed thatparticipants who received the strategy map consideredknowledge sharing to be more important to Alpha Con-sulting management than participants who did not receivethe strategy map (t = 2.612, p = 0.012, two-tailed; the meanresponses were 5.423 and 4.967, respectively for the twogroups on a 7-point scale). This result provides some con-dence that our HIA communication manipulation wassuccessful in increasing participants’ awareness of theimportance of knowledge sharing.

3.4. Participants

Participants in this study are graduate students fromthe business school of a major university. All participantswere enrolled in an advanced accounting course and were

volunteers. The average age of the participants was 24.4years. 8 The experiment was conducted at the end of eachof ve separate class streams over three consecutive days.It took between 15 and 20minutes to complete. Of theapproximately 200 students enrolled in the ve classes

8 A small, non-performance contingentincentiveis provided to encour-age voluntary participation in this experiment. Specically, participantshave a random chance of winning a gift card worth A$100 per class. Thegift cards were drawn by lottery of participants and awarded in the weekfollowing the experiment.

120 participated. After excluding participants who did notcomplete or incorrectly answered the manipulation checkquestions, 96 useable responses were included in our anal-ysis (21, 25, 25 and 25 participants in each of the fourtreatments).

Prior studies examining performance measurementsystems and decision-making have commonly used stu-dent participants as surrogates, including undergraduatestudents ( Farrell et al., 2008; Kachelmeier et al., 2008 )graduate students (e.g., Bailey et al., 2011 ) and MBA stu-dents (e.g., Lipe and Salterio, 2000, 2002 ). We consider itappropriate to use graduate students in our study for anumber of reasons. First, these participants assumed therole as an employee in a consulting rm – a role that ourparticipants can plausibly take up soon after graduation.The effort allocation decision they are required to makein the experiment is also similar to one that employeeswill face at various hierarchical levels. Second, our deci-sion task does not require any domain specic expertisebeyond what is expected from a graduate student. Third,we are not aware of any theoretical reasons why inher-ent factors differentiating graduate students and actualemployees working in a consulting rm will interact withour theory such that internal validity may be threatened(see Peecher and Solomon, 2001 ).

4. Results

4.1. Knowledge-sharing behaviour: H1 and H2

H1 and H2 concern employees’ knowledge-sharingbehaviour. Consistent with H1, participants’ willingness toshare knowledge with a co-worker is higherunder thesub- jective weighting scheme than a formula-based scheme(4.380 versus 3.717 on a 7-point scale, see Table 1 PanelA). The ANOVA model in Table 1 Panel B shows that thisdifference was statistically signicant ( F =4.238, p =0.042),thus H1 is supported. Furthermore, it is interesting tonote that while the average willingness score was lowerthan the mid-point of the 7-point scale under a formula-based scheme (indicating thatparticipantson averagewere

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 9/11

. . , .

Table 1Willingness to engage in knowledge-sharing behaviour.

Formula-basedscheme

Subjectiveweighting scheme

Row average

Panel A: Descriptive statistics a

HIA communication present 3.680(1.725 )N = 21

4.360(1.630 )N = 25

4.020(1.696 )N = 50

HIA communication absent 3.762(1.640 )N = 25

4.400(1.225 )N = 25

4.109(1.449 )N = 46

Column average 3.717(1.669 )N = 46

4.380(1.427 )N = 50

4.063(1.575 )N = 96

Source SS df MS F p

Panel B: ANOVA modelIncentive scheme subjectivity 10.365 1 10.365 4.238 0.042HIA communication 0.089 1 0.089 0.036 0.849Incentive scheme subjectivity a HIA communication 0.010 1 0.010 0.004 0.948Error 225.010 92 2.446

a 7-Point scale, where a larger number indicates stronger willingness to share information with a colleague.

unwilling to engage in knowledge sharing); participantsgiven a subjective weighting scheme were, on average,willing to share knowledge with their co-worker (the aver-

age of 4.380 was signicantly higher than the mid-pointof 4.00, t = 1.883, p = 0.033, one-tailed). This further showsthat the nature of the incentive schemes has substantialimpact on employees’ knowledge-sharing behaviour.

H2 predicts an interaction effect where using a strat-egy map to communicate howthe rm’s HIA contributes toits strategic goals will increase employees’ willingness toshare knowledge under a subjective scheme, butdecreasesthis willingness under a formula-based scheme. As we arepredicting a specic form of interaction, using contrasttesting is more appropriate than the use of the omnibus F -test ( Bucklessand Ravenscroft, 1990 ). Given thedirectionalprediction, we used a one-tailed test. A planned interac-

tion contrast between incentive scheme design and thecommunication of HIA was, however, insignicant ( p >0.1,one-tailed), and therefore H2 was not supported.

4.2. Extra-role behaviours: H3 and H4

Our next two hypotheses concern employees’ generaltendency to perform extra-role behaviours. As discussedearlier, we adopted the OCB-I scale ( Williams andAnderson, 1991 ) for our study, which comprises a set of six questions. The Cronbach’s Alpha for these six questionswas acceptable at 0.770; thus, we used theaverage of these

six questions as our dependent variable to test H3 and H4(the descriptive statistics are shown in Table 2 Panel A).

H3 predicts that employees’ tendency to performextra-role behaviours is higher under a subjective incen-tive scheme than a formula-based incentive scheme. Theinsignicant main effect in the ANOVA model in Table 2Panel B does not support our prediction. Table 2 Panel A,however, shows that in the presence of communication of thestrategicrole of HIA,the general tendencyof individualsto perform extra-role behaviours was higher under a sub- jective scheme than a formula-based scheme (4.433 versus

3.884). A subsequent t -test conrms that this differenceis marginally signicant ( t = 1.626, p = 0.056 one-tailed). Incontrast, the difference was not signicant when commu-

nication was absent. Our nding thus provides only partialsupport to H3 . This weaker result, compared with H1, maybe explained by monetary incentives having greater effectin inuencing individuals’ tendency to perform an activitythat requires giving up economic rents (e.g. sharing pro-priety knowledge) than performing extra-role behavioursthat do not require giving up economic rents ( Wolfe andLoraas, 2008 ). That is, the type of incentive schemeis likelyto have less effect on extra-role behaviours than its effecton sharing proprietary knowledge.

H4 predicts an interaction effect where the presenceof a strategy map communication increases employees’tendency to perform extra-role behaviours if they are

given a subjective weighting scheme, but lowers thistendency if employees are given a formula-based incen-tive scheme. Table 2 Panel A provides initial support tothis hypothesis. As shown in Table 2 Panel B, under asubjectiveschemeparticipants’ tendencyto perform extra-role behaviours was higher in the HIA communicationpresent treatment than without HIA communication treat-ment (4.433 versus 3.907). The reverse was true undera formula-based incentive scheme: the responses werehigher when HIA communication was absent than whenit was present (4.207 versus 3.884). A planned interactioncontrast showed that the interaction effect was signicant( p = 0.04, one-tailed), thus H4 w as supported.

5. Conclusion and discussions

This study investigates whether employees’ willing-ness to share their knowledge with co-workers, and theirgeneral tendency to perform extra-role behaviours areimpacted by two aspects of a performance managementsystem. First, by the nature of the incentive scheme,specically, whether subjectivity is allowed in weightingemployees’ performance on multiple areas, or whether

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 10/11

. . , .

Table 2General tendency to perform extra-role behaviours.

Formula-basedscheme

Subjectiveweighting scheme

Row average

Panel A: Descriptive statistics a

HIA communication present 3.884(1.070 )N = 20

4.433(1.191 )N = 25

4.189(1.160 )N = 45

HIA communication absent 4.207(1.054 )N = 25

3.907(1.393 )N = 25

4.057(1.232 )N = 50

Column average 4.063(1.061 )N = 45

4.170(1.310 )N = 50

4.119(1.194 )N = 95

Source SS df MS F p

Panel B: ANOVA modelIncentive scheme subjectivity 0.366 1 0.366 0.258 0.613HIA communication 0.242 1 0.242 0.170 0.681Incentive scheme subjectivity a HIA communication 4.243 1 4.243 2.992 0.087Error 129.057 91 1.418

a 7-Point scale, where a larger number indicates stronger willingness to perform extra-role activities.

weighting is based on an inexible formula; and second,by communicating the importance of HIA in driving rmperformance. Prior research indicates the former repre-

sents an important design choice for the managementaccountants responsible for implementing a performancemanagement system. In addition, recent,mainly normativeliterature, argues forcefully for the importance of the lat-ter, and specically, to use the strategy map as a meansof aligning HIA with strategic objectives. The implica-tions of these design choices for knowledge-sharing andextra-role behaviours, both of which have the potential toenhance competitiveness through intangible asset devel-opment, previously have not been adequately examined inthe accounting literature.

Our results provide evidence that design choices of performance management systems inuence employee

behaviours inactivities thataffectHIAdevelopment. Inpar-ticular, our nding that a subjective weighting scheme canincrease employees’ willingness to shift their effort fromincentivised work activities to sharing knowledge witha co-worker is important. It indicates there is potentialto encourage this desired behaviour even where it is notpossible to precisely specify a measure of an employee’sknowledge-sharing performance. This is important inpractice as well, for the quantity and quality of knowledgecannot be directly speciedor measured.Much knowledgesharing will take place in day-to-day interaction aroundwork activities and will not always be planned in advance,making direct control and supervision problematic. The

results demonstrate subjectivity in an incentive weightingscheme is positive for encouraging knowledge sharing.Further, our result shows that using a strategy map to

communicate to employees the importance of HIA furtherimproves employees’ general tendency to perform extra-role behaviours under a subjective weighting scheme, butcan potentially ‘back-re’ under a formula-based scheme.This is an important nding as it highlights that although astrategy map may communicate strategic objectives and,by implication, desired behaviour, its effect on behaviourwill depend on other factors. The creation of conicting

signals by the inclusion of a strategy map (which helpsto highlight the importance of extra-role behaviours)with a formula-based incentive scheme (which effectively

punishes extra-role behaviours), exacerbates this negativeinuence.While caution is required in interpreting the lack

of statistical signicance in H2, our study alerts us tothe potential differential impacts of the two perfor-mance management systems investigated in relation toknowledge-sharing and extra-role behaviours. One plau-sible explanation for the differential effects relates tothe nature of these activities. In the knowledge-sharingscenario inourexperiment, individualshave to give uppro-prietary information that was collected and built up overtime, whereas engaging in general extra-role behaviours,such as helping a co-worker with a heavy workload, is not

context specic and the costs of doing so may be seen asless salient. As a result, the nancial consideration (andtherefore the role of the incentive scheme) is greater withrespect to knowledge sharing than engaging in extra-rolebehaviours. Our nding that the moderating role of com-municating the strategic value of HIA is signicant onlywith respect to extra-role behaviours may be similarlyexplained. It is likely that compared with knowledge shar-ing, general extra-role behaviours, which are directed athelping co-workers, are seen as less valuable. It requiresa strategy map, explicitly highlighting the link betweenHIA,including expertiseandprofessionalism, and therm’sstrategic goals to encourage individuals to recognise the

value of such activities.Our research contributes to the management account-ing research by providing experimental evidence thatsubjectivity in incentiveschemes has benets with respectto knowledge-sharing and extra-role behaviours. Further,despite the fact that the strategy map is often pro-posed as an important part of a strategic performancemeasurement system (e.g. Kaplan and Norton, 2004 ), itseffects on practice have received only limited attentionfrom the accounting research literature. Our nding con-tributes to our understanding of the strategic value of

7/21/2019 The Effects of Incentive Subjectivity and Strategy Communication on Knowledge-sharing and Extra-role Behaviours

http://slidepdf.com/reader/full/the-effects-of-incentive-subjectivity-and-strategy-communication-on-knowledge-sharing 11/11

. . , .

HIA. Past research tends to focus on examining howperformance management system design can motivateemployees’ in-role activities; little attention has beenpaid to extra-role behaviours (with the recent exceptionof Burney et al., 2009 ). Yet, such behaviours have beenfound to be important to organisational successes in thepsychology literature (e.g. Podsakoff et al., 2009 ). Our nd-ings show that management accountants can play a rolein motivating employees to perform such value-addingactivities.

Our study has several limitations. First, while our nd-

ings on H4 are consistent with our argument that thecombination of a formula-based scheme and a strategymap can result in a perception of an ‘unfair exchange’between the individual and the organisation (while theopposite is likely under a subjective weighting scheme),we did not directly test the mediating role of perceivedfairness. Our ndings though are supported by a recentstudy by Johnson et al. (2009) , which shows that employ-ees perceive a performance evaluation scheme as fairerif it takes into account employees’ organisational citizen-ship behaviours. Second, a contrasting argument to ourproposed H2 is that subjectivity in performance evalu-ation may negatively impact on procedural fairness and

therefore employees’ willingness to contribute to theorganisation through knowledge sharing. While we didnot measure procedural fairness in our study, we donot expect this factor to have signicant impact on ourresults because participants in the study did not receiveany indication (e.g. performance feedback) that wouldsuggest biased performance evaluation Third, our exper-iment focuses on one period only; it is likely that theimpact of subjectivity will become more apparent overtime, as employees learn whether their supervisor ful-ls their ‘implicit contract’ and uses his/her discretion toensure that employees’ knowledge-sharing and extra-roleefforts are not penalised. Related to this, our experiment

examines the behavioural intentions of business graduatestudents rather than the actual behaviours of employees.Although we are not aware of any theoretical reasons whygraduate students would respond to our stimulus differ-ently to professionals/employees, experienced employeesare more likely to have encountered both favourable andunfavourable performance evaluations, and in the role of both the evaluatees and the evaluators. It is possible thatsuch encounters will impact on individuals’ responses totheir effort allocation decisions. We see this as an interest-ing future research avenue.

A number of research avenues are also apparent.For example, future studies may examine whether other

types of subjectivity in incentive schemes (e.g. subjec-tive ratings versus objective measures) also impact onemployees’ knowledge-sharing behaviour and their ten-dency to perform extra-role behaviours. Also, futureresearch may investigate the extent to which the super-visor’s characteristics, such as reputation, managementstyle and competence, and employees’ perception of the evaluation system, such as distributive and proce-dural fairness, may moderate the impact of subjectivityon employees’ behaviours. Finally, future research mayadopt a multi-period design to investigate how multiple

interactionsbetweensupervisors andemployees willinu-ence employees’ general tendency to perform extra-rolebehaviours.

References

Adams, J.S., 1965. Inequity in social exchanges. In: Berkowitz, L. (Ed.),Advances in Experimental Social Psychology, vol. 2. Academic Press,New York, pp. 267 –299.

Bailey, W.J., Hecht, G., Towry, K.L., 2011. Dividing the pie: the inuence of managerialdiscretion extent on bonus pool allocation. Contemporary

Accounting Research 28 (5), 1562 –1584.Baiman, S., Rajan, M.V., 1995. The informational advantages of discre-

tionary bonus schemes. The Accounting Review 70 (4), 557 –579.Baker,G.P.,Gibbons,R., Murphy,K.J.,1994. Subjectiveperformancemeas-

ures in optimal incentive contracts. Quarterly Journal of Economics109 (4), 1125 –1156.

Banker, R.D. , Chang, H., Pizzini, M.J., 2004. The balanced scorecard: judgmental effects of performance measures linked to strategy. TheAccounting Review 79 (1), 1 –12.

Banker, R.D., Chang, H., Pizzini, M.J., 2009. The judgmental effects of strategy maps in balanced scorecard performance evaluation, SSRNWorking Paper.

Blau, P.M., 1964. Exchange and Power in Social Life. Wiley, New York.Bock, G.-W., Lee, J.-M., Zmud, R., 2005. Behavioural intention formation

in knowledge-sharing: examining the roles of extrinsic motivators,social-psychologicalforces, and organizational climate. MIS Quarterly29(1), 87 –111.

Bordia, P., Restubog, S.L.D., Tang, R.L., 2008. When employees strike back:investigating mediating mechanisms between psychological contractbreachand workplace deviance. Journal of Applied Psychology 93 (5),1104 –1117.

Buckless, F.A., Ravenscroft, S.P., 1990. Contrast coding: a renementof ANOVA in behavioral analysis. The Accounting Review 65 (4),933 –945.

Budde, J., 2007. Performance measure congruity and the balanced score-card. Journal of Accounting Research 45, 515 –539.

Burney, L.C., Henle, C., Widener, S., 2009. A path model exam-ining the relations among strategic performance measurementsystem characteristics, organizational justice, and extra- and in-role performance. Accounting, Organizations and Society 34 (3-4),305 –341.

Cheng, M.M., Humphreys, K.A., 2009. The Effect of Causal Chain Illustra-tionon Managers’Assessment of Perceived StrategicContribution andWillingness to Approve a Capital Investment. University of New South

Wales Working Paper. In: Presented at 2009 Accounting, Behaviouraland Organizations Conference.Cheng,M.M., Humphreys,K.A., 2012. The differential improvementeffects

of thestrategy map and scorecardperspectives on managers’strategic judgments. The Accounting Review 87 (3), 899 –924.

Chenhall, R., 2005. Integrative strategic performance measurement sys-tems, strategic alignment of manufacturing, learning and strategicoutcomes: an exploratory study. Accounting, Organizations and Soci-ety 30, 395 –422.

Chow, C., Deng, F.J., Ho, J.L., 2000. The openness of knowledge sharingwithin organizations: a comparative study of the United States andthe People’s Republic of China. Journal of Management AccountingResearch 12, 66 –95.

Chow,C., Harrison,G.L., McKinnon,J.L., Wu, A.,1999. Culturalinuencesoninformal information sharing in Chinese and Anglo-American organi-zations: an exploratory study. Accounting, Organizations and Society24, 561 –582.

Coyte,R., 1995. TheRoleofManagementAccountingintheEmergingTeamApproach to Work, International Federation of Accountants. Finan-cialand ManagementAccounting Committee,Study No. 5, September,International Federation of Accountants New York.

Coyte, R., 2005. Strategy, Teams and Resource Consciousness. Universityof New South Wales, Sydney (PhD Dissertation).

Datar, S., Kulp, S., Lambert, R., 2001. Balancing performance measures. Journal of Accounting Research 39 (1), 75 –92.

Drake, A.R., Haka, S.F., Ravenscroft, S.P., 1999. Cost system and incentivestructure effects on innovation, efciency, and protability in teams.The Accounting Review 74, 323 –345.

Edmister, R.O., Locke, E.A., 1987. The effects of differential goal weightson theperformance of a complex nancial task. PersonnelPsychology40 (3), 505 –517.