The Effect of Quantitative Easing on Irish Businesses

33

THE EFFECT OF QUANTITATIVE EASING ON IRISH BUSINESSES Student: Daniel Flanagan Student Number: C11419868 Student: Ben O’Connor Student Number: 11336376 Student: Cian O’Brien Student Number: C11398546 Student: Mark Draper Student Number: C11421778 Student: Daniel Connell Student Number: C11705359 1

-

Upload

ben-oconnor -

Category

Documents

-

view

7 -

download

1

description

In depth analysis into the effect of the recently announced quantitative easing program on Irish businesses

Transcript of The Effect of Quantitative Easing on Irish Businesses

THE EFFECT OF QUANTITATIVE

EASING ON IRISH BUSINESSES

Student: Daniel Flanagan

Student Number: C11419868

Student: Ben O’Connor

Student Number: 11336376

Student: Cian O’Brien

Student Number: C11398546

Student: Mark Draper

Student Number: C11421778

Student: Daniel Connell

Student Number: C11705359

Word Count:

1

Declaration

I hereby certify that this material, which I now submit for assessment as a continuous

assessment project in Financial Services on the course DT365/4 BSc (Business and

Management) Year 4, is entirely my own work and has not been submitted in whole

or in part for assessment for any academic purpose other than in fulfillment for that

stated above.

Signed: ………………………..……..……………….………… Date:……………………

Daniel Flanagan

Signed: ………………………..……..……………….………… Date:……………………

Ben O’Connor

Signed: ………………………..……..……………….………… Date:……………………

Cian O’Brien

Signed: ………………………..……..……………….………… Date:……………………

Mark Draper

Signed: ………………………..……..……………….………… Date:……………………

Daniel Connell

2

TABLE OF CONTENTS

INTRODUCTION.............................................................................................................4

WHAT IS QUANTITATIVE EASING?............................................................................4

WHERE HAS QUANTITATIVE EASING BEEN APPLIED BEFORE?.............................5

Japan......................................................................................................................5

America..................................................................................................................5

United Kingdom.....................................................................................................5

EUROPE’S ADOPTION OF QUANTITATIVE EASING...................................................6

EXCHANGE RATE MOVEMENT...................................................................................6

Positive Effects for Irish Businesses of a Weaker Euro.........................................8

Negative Effects for Irish Businesses of a Weaker Euro........................................9

QUANTITATIVE EASING’S EFFECT ON STOCK MARKETS.....................................10

EFFECT OF LOW INTEREST RATE AND INCREASED CREDIT AVAILABILITY........12

NEGATIVE EFFECTS OF LOW INTEREST RATE..........................................................14

Financial Instruments..........................................................................................14

Bonds Reduced In Value......................................................................................14

POSITIVE EFFECTS OF LOW INTEREST RATE............................................................15

Lower Cost of Borrowing.....................................................................................15

Increased Consumer Spending.............................................................................15

REACTION BY IRISH BUSINESSES TO LOW INTEREST RATES..................................15

RISKS...........................................................................................................................16

CONCLUSION...............................................................................................................18

REFERENCES...............................................................................................................19

3

INTRODUCTION

In January 2015, Mario Draghi announced a quantitative easing package worth

€1.1 trillion in order to help Europe in the fight against increasing deflation levels and

stagnant growth. The stimulus package will run through to September 2016 in an

attempt to boost inflation, make europe more competitive and to hopefully increse

growth.

This article seeks to examine quantitative easing and its previous uses, along

with the anticipated exchange and interest rate movement and their effect on Irish

businesses. Furthermore, the effects of quantitative easing on stock markets will be

reviewed along with the potential risks of implementing the quanitative easing

programme.

WHAT IS QUANTITATIVE EASING?

Quantitative easing is adopted when consumer spending is low and there are

signs of deflation. The aim of quantitative easing is to reduce long term interest rates

so to encourage spending (Walker, 2015).

Quantitative easing is when the central bank produces money electronically

and pumps it into the economy. The central bank generally purchases government

bonds from private sector firms such as high street banks, insurance companies,

pension funds and non-financial companies (Bank of England, 2015). For example by

purchasing from high street banks, it will increase the levels of cash reserves in the

high street banks. By increasing the cash reserves the high street banks will be able to

lend more which will encourage customers to spend, thus stimulating economic

growth.

As the bank purchases the assets the available supply drops. This causes the

price to increase which reduces the yield thus causing returns to drop. The drop in

return encourages investors to sell their assets and re-invest in other high return

investments therefore increasing the price of these assets too (Bank of England,

2015). This causes long term interest rate to drop and encourages households and

businesses to spend (Walker, 2015).

4

WHERE HAS QUANTITATIVE EASING BEEN APPLIED

BEFORE?

Japan

Japan was the first to implement QE in 2001 because their economy was

experiencing high levels of deflation. The Bank of Japan decided in 2001 to launch

their QE programme after their failed attempt to reduce deflation and the collapse of

global IT industry (Bowman, Cai, Davies, and Kamin, 2011). Between 2009 and 2012

the BOJ purchased ¥187 trillion worth of assets. According to Fawley and Neely

(2013) the BOJ focused their purchasing on short and long term government bonds.

Since April 2013 the BOJ has acquired another ¥84 trillion worth of government

bonds (Allen, 2015). So there are no results yet whether QE has been successful for

the Japanese economy.

America

Since the financial crisis in 2008 the Federal Reserve (FED) has practised

quantitative easing four times (QE1, QE2, Operation Twist and QE3). To date the

FED has spent over $3 trillion on government sponsored enterprise debt, mortgage

back debt and long term treasury debt (Fawley and Neely, 2013). According to

Walker (2014) America’s QE programme has reduced interest rates for households

and businesses, helped with job creation and prevented the US slipping into another

recession. However according to Prof Martin Feldstein of Harvard University there is

a worry that by pumping large amounts of money into an economy it can lead to

higher inflation (cited in Walker, 2014).

United Kingdom

According to Joyce (2012) there was a risk that Consumer Price Index

inflation wasn’t going to reach the 2 per cent target set by the British government.

With the risk present the Bank of England’s Monetary Committee announced their

QE plan to purchase assets and reduce the bank rate by 0.5 per cent. The Bank of

England focused on purchasing medium and long term government gilts (Mortimer-

Lee, 2012) and by 2010 the BOE altered their focus and purchased government bonds

(Joyce, 2012). According to Allen (2015) the BOE has said that QE easing has had a

positive effect on increasing the price of bonds and shares along with increasing jobs.

5

However there is now a worry of deflation as inflation currently rests at 0.5 per cent

(Allen, 2015).

EUROPE’S ADOPTION OF QUANTITATIVE EASING

With low economic growth and inflation dropping below zero in December

2014 the Europe Central Bank (ECB) finally announced their QE programme at the

start of this year (BBC, 2015). They are going to spend €50 billion a month for the

next 19 months on government bonds and €10 billion on asset backed securities (The

Economist, 2015). The ECB are not going to purchase Greek bonds until the Greek

government reaches an agreement on the debt they owe to the other euro zone

partners (RTE, 2015).

It is expected that the ECB’s QE programme will give a strong signal to the

markets that they are taking action to restore inflation to 2 per cent and is also

expected to cause the euro to weaken making European products cheaper on

international markets (The Economist, 2015). However it is not expected to have the

same impact as the FED’s and the BOE’s QE programmes because the markets have

been expecting the announcement for some time (The Economist, 2015).

EXCHANGE RATE MOVEMENT

Mortimer-Lee (2012) clarifies that one market that is clearly distorted by

quantitative easing is the foreign-exchange market. De Grauwe (2015) describes how

the recently announced quantitative easing programme should have a substantial

influence on the exchange rate of the euro. He states that ‘by increasing the supply of

money base the ECB will contribute to a further weakening of the euro vis-à-vis other

currencies such as the dollar, the pound and the yuan, thereby increasing exports and

boosting inflation’ (De Grauwe 2015). Similarly, Krugman (2008) explains that an

increase in the euro zone’s money supply causes a depreciation of the euro. Also vice

versa a decrease in the euro zone’s money supply causes an appreciation of the euro.

He clarifies that the interest rate is the mechanism responsible for causing the

devaluation of a currency. The increase in the euro zone’s money supply reduces

interest rates in the euro zone therefore reducing the expected return on euro deposits.

This invariably leads to a capital outflow which causes a depreciation of the euro. We

have already seen this occur in the euro zone as the euro has fallen sharply against

6

other currencies, namely the dollar and the pound sterling. Kenourgios et al. (2015)

found that there was a depreciation of the euro and an increase of its volatility before

and after the ECB's announcements of the implementation of a quantitative easing

programme. They explain that markets were anticipating the actions of the ECB and

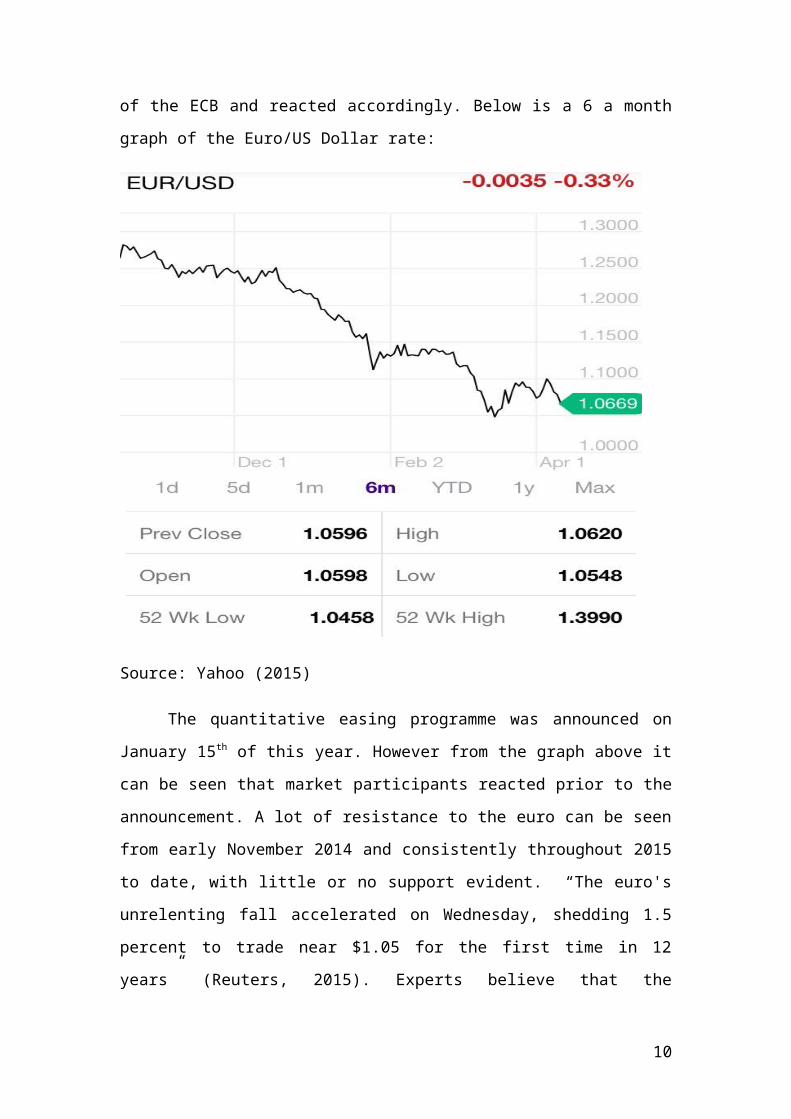

reacted accordingly. Below is a 6 a month graph of the Euro/US Dollar rate:

Source: Yahoo (2015)

The quantitative easing programme was announced on January 15 th of this

year. However from the graph above it can be seen that market participants reacted

prior to the announcement. A lot of resistance to the euro can be seen from early

November 2014 and consistently throughout 2015 to date, with little or no support

evident. “The euro's unrelenting fall accelerated on Wednesday, shedding 1.5 percent

to trade near $1.05 for the first time in 12 years” (Reuters, 2015). Experts believe that

the euro/dollar rate will move to parity by end of the year stating “U.S. bank Morgan

Stanley has forecast that the euro will sink below parity with the dollar before the end

of this year” (Reuters, 2015).

7

Source: Yahoo (2015)

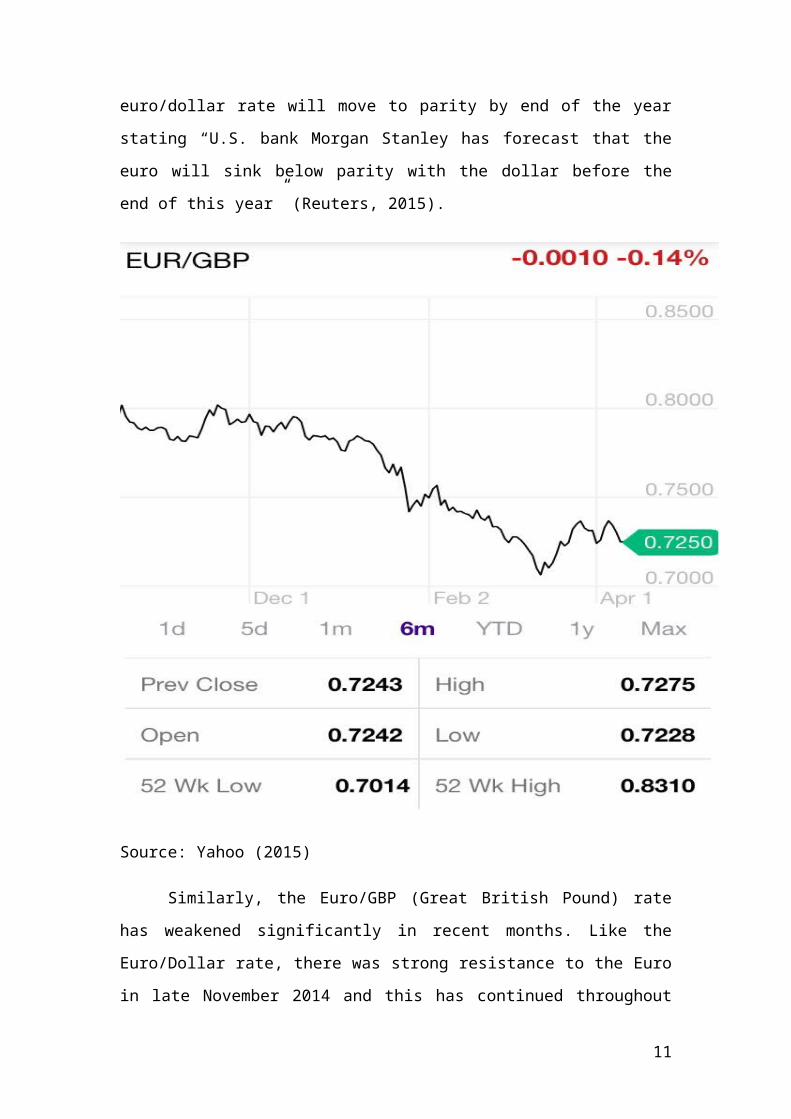

Similarly, the Euro/GBP (Great British Pound) rate has weakened significantly

in recent months. Like the Euro/Dollar rate, there was strong resistance to the Euro in

late November 2014 and this has continued throughout 2015. “The Euro struck a

seven-year low against sterling at 70.145 pence EURGBP and an 18-month low of

128.29 yen EURJPY” (Reuters, 2015).

Positive Effects for Irish Businesses of a Weaker Euro

Labonte (2015) explains that quantitative easing encourages exchange rate

depreciation that causes exports to rise and imports to fall. This is especially good

news for Irish businesses as Ireland are an export-orientated country. The weaker euro

should drive export-orientated growth to non-euro markets. Our main trading partners,

8

namely the U.S. and the U.K., will benefit hugely from the weaker euro. According to

Power (2015) 64% of our goods produced are exported to non-euro markets. He also

identifies that over the past year the euro has lost approximately 24% of its value

against the dollar and over 16% against sterling. This means that Irish exporters will

receive a massive competitiveness boost as a direct result of the weak euro.

Power (2015) also explains that the agri-food sector could receive a timely

boost from the weaker euro. Ireland exports 85% of its food to more than 160

countries worldwide and the agri-food sector accounts for more than 10% of total

Irish exports (Teagasc 2015). Britain accounts for 38% of exports from the agri-food

sector so the weaker euro should increase agricultural exports to Britain and other

non-euro markets.

Colgan (2015) identifies the tourism sector as one that should incur substantial

growth in 2015 as a result of quantitative easing. The Irish tourism sector should reap

massive benefits from the weaker euro as British and American tourists will see this

as a great time to travel to Ireland.

Strauss and Gordon (2015) explain that essentially companies with high U.S.

dollar revenues will gain most from the weaker euro. They state that “given the euro’s

fall has been sharpest against the dollar, companies with significant US or dollar-

denominated sales, such as pharmaceuticals, would eventually be among the biggest

beneficiaries” (Strauss & Gordon, 2015)

Negative Effects for Irish Businesses of a Weaker Euro

Although the weaker euro increases our competitiveness, it will inflate the

price of imports. Importers will have to give away more euros to import goods from

non-euro markets. Power (2015) explains that Ireland imports more goods from

Britain than they export to them. He shows that in 2014, merchandise imports from

Britain totalled €17.3bn while exports only totalled €13.4bn. However, the weaker

euro may act as a stimulant for domestic growth as consumers and businesses may

look to purchase indigenous goods instead of importing foreign goods. This is

positive news for smaller businesses who only operate on a domestic level.

The weaker euro may have a negative impact on the airline industry, as the

price of fuel will be highly inflated due to the weaker euro. Strauss and Gordon

(2015) explain that low-cost airlines that buy fuel in dollars but have no dollar

revenues could be among the worst affected. However Ryanair has stated that it has

9

locked in its capital-expenditure requirements through September 2017 at a rate of

$1.35 to the euro and is nearly fully hedged for all of its fuel requirements.

Overall, the devaluation of the euro as a result of the recently announced

quantitative easing programme should act as a stimulant for growth by increasing our

competitiveness on a global stage. This because Ireland are an export orientated

economy, most Irish business should benefit from quantitative easing. Larger

multinational companies who operate in non-euro markets will reap the most benefits,

whilst smaller scale exporters and other businesses should also benefit.

QUANTITATIVE EASING’S EFFECT ON STOCK MARKETS

As quantitative easing involves a massive bond-buying programme.

Inevitably, yields on such bonds will decline forcing investors to look elsewhere for

higher returns. “With government debt now carrying a negative yield thanks to QE,

it’s no surprise that investors are throwing themselves headlong into equities to try

and find some income” (Hunter and Chisholm, 2015).

Investors will have to move higher up the risk curve to get a satisfactory

return. This means bond investors will look to equities for higher yields and therefore

stock markets will appreciate in value as a result of this. “As investors attempt to

rebalance their portfolios away from gilts towards more risky assets, the additional

compensation investor’s demand for the risk of holding equities (the so-called equity

risk premium) should fall. This will put further upward pressure on equity prices”

(Joyce et al., 2011).

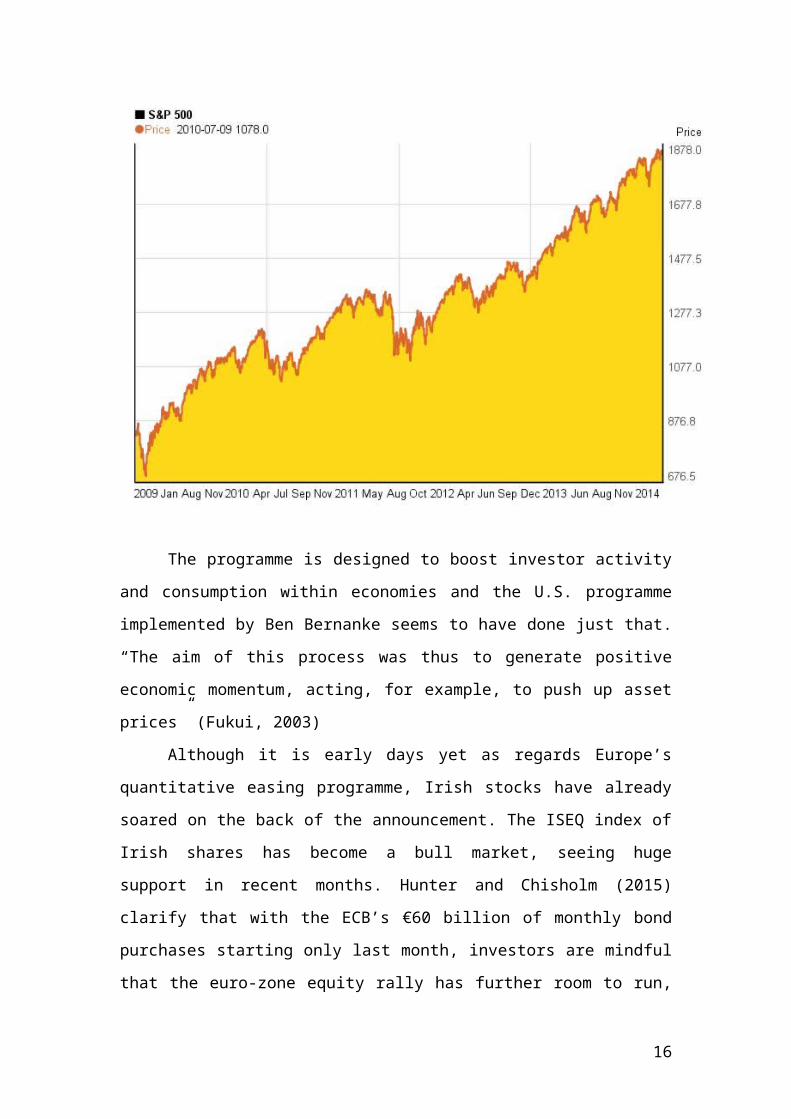

Quantitative easing and stock markets are said to have a positive correlation.

Below is a graph of the S&P 500, a market consisting of the top 500 companies in the

U.S. This snapshot shows a 5 year period immediately after the Federal Reserve’s

announcement a quantitative easing programme in late 2009. It can be seen here that

there was substantial support in the market for equities and therefore share prices

soared. The S&P 500 remained a bull market throughout the duration of the

quantitative easing programme. There were minor blips as you can see a strong

resistance in the market in mid-2011 when the then head of the Federal Reserve, Ben

Bernanke, announced a tapering back of the asset buying programme which caused

significant volatility in the market.

10

The programme is designed to boost investor activity and consumption within

economies and the U.S. programme implemented by Ben Bernanke seems to have

done just that. “The aim of this process was thus to generate positive economic

momentum, acting, for example, to push up asset prices” (Fukui, 2003)

Although it is early days yet as regards Europe’s quantitative easing

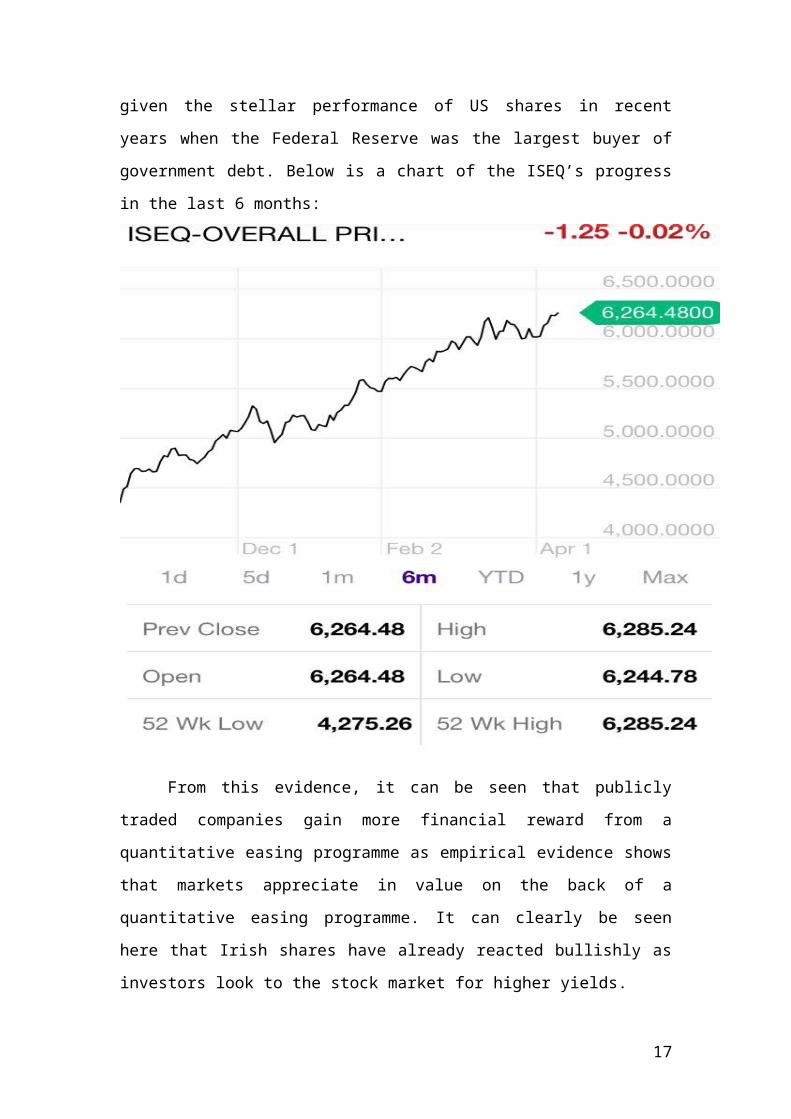

programme, Irish stocks have already soared on the back of the announcement. The

ISEQ index of Irish shares has become a bull market, seeing huge support in recent

months. Hunter and Chisholm (2015) clarify that with the ECB’s €60 billion of

monthly bond purchases starting only last month, investors are mindful that the euro-

zone equity rally has further room to run, given the stellar performance of US shares

in recent years when the Federal Reserve was the largest buyer of government debt.

Below is a chart of the ISEQ’s progress in the last 6 months:

11

From this evidence, it can be seen that publicly traded companies gain more

financial reward from a quantitative easing programme as empirical evidence shows

that markets appreciate in value on the back of a quantitative easing programme. It

can clearly be seen here that Irish shares have already reacted bullishly as investors

look to the stock market for higher yields.

EFFECT OF LOW INTEREST RATE AND INCREASED CREDIT

AVAILABILITY

One effect of introducing QE is that interest rates remain at extremely low

levels. This means that businesses with cash deposits will get lower returns on its

money than previously thought. This leaves a number of options for businesses. A

business will now have to enter into riskier investments in order to achieve the same

12

return on its cash deposits. As outlined in the graphs below the ECB marginal lending

rate and the 10-year government bond yield rates are at historically low rates.

Source: CSO (2015)

13

Source: CSO (2015)

Negative Effects of Low Interest Rate

Financial Instruments

Financial instruments in which a business may have used that depend on a

deposit rate will now have to revalued downwards as they will not get the same return

for its bank deposits. Money market instruments which involve calculations based on

deposit interest rates will now be changed due to QE lowering the deposit rate in

banks, therefore giving Irish businesses less return through interest.

Bonds Reduced In Value

The yield on bonds is at such a level that the real return created through the

interest rate is actually negative (Deloitte, 2015). The low bond yields induced by QE

effects businesses as it poses an asset allocation problem to pension and fund

managers. Previously a certain amount of a fund would be allocated to bonds as they

were a safe asset with predictable returns, but now with yields approaching negative

these funds have to be allocated elsewhere (Deloitte, 2015).

14

Positive Effects of Low Interest Rate

Lower Cost of Borrowing

One positive effect of having a low interest rate for Irish businesses is that the

cost of borrowing is also lower. This could act as a catalyst for Irish business to

expand and increase capital expenditure through the use of extremely low interest

rates.

Further with the ECB purchasing bonds from the government, and if banks

choose to sell its bonds they will have more cash to lend out. This means that it’s

easier for an Irish business to gain access to funds in a liquid market.

Increased Consumer Spending

Due to a lower return from deposits in banks for households this could

positively affect Irish businesses due to increased consumption in the Irish economy.

The hope of this cash injection into the European economy by the ECB is that it will

increase consumer spending. Due to the lower interest rates in combination with

lending becoming more accessible to consumers, spending could be seen to increase if

you are of the view that the reason for low consumption in the marketplace is a supply

side issue. There is considerable debate amongst academics whether this is the case.

Reaction By Irish Businesses To Low Interest Rates

The thinking behind the large QE package is that the low interest rates will

encourage companies to start investing and spending more in economies due to the

ease of access to credit and the historically low interest rates. There is considerable

debate to this view though among economists. Lo and Rogoff (2014) and Pasani-

Ferry and Jean (2013) are of the view that companies are deleveraging after a period

of high leveraging. They argue that due to this deleveraging cycle, businesses are not

looking to expand and take advantage of the low interest rates resulting from a QE

programme. Businesses instead are looking to repair its balance sheet, as there is a

debt overhang from the recession (Lo and Rogoff, 2014).

The assumed manner that businesses will react to the QE, and therefore low

interest rates is increase borrowing. The ECB takes a view that there is a liquidity

problem in the market i.e. it is a supply side issue of funds, but according to Wyplosz

(2014) it is a demand side issue. Wyplosz (2014) therefore thinks that businesses will

not react to low interest rates by increasing spending as they are still in a period of

15

recovery in which the phrase has been coined a ‘balance sheet recession’ by Richard

Koo. This is where businesses are not looking to maximise their profits, but instead

are looking to repair their balance sheet after it was severely damaged during the

recession.

Businesses may look to capitalise on the low interest rates resulting from the

QE programme and spend money now, fearing an increase in interest rates in the

future. It is difficult to say for certain, given the disagreement going on amid

academics whether or not this will mean that Irish businesses will truly benefit from

the low interest rates and increase spending. Irish businesses may simply go on and

continue to repair their balance sheets and not look to maximise profits.

RISKS

Where there is an upside with regards to QE, there must be a downside too.

Quantitative Easing has only been around for a very short period of time, so the risks

haven’t been observed to the level they should be. QE is essentially tailor-made to suit

an economy that is experiencing challenges. The ECB in comparisons to the US and

Japan are unique as they operate a single monetary policy over eighteen different

economies within the Eurozone, which all have their own distinct challenges

(Deloitte, 2015). When the US began QE it was crisis driven but as time passed it

became orderly and thought-out, and they are a wonderful example as learning by

doing (Blinder, 2010).

So with regards the Central Bank, what problem will they face with QE? The

answer is none, as they are obliged to hit certain levels of inflation which are seen as

being modest. However, when inflation levels get unsustainable, the central bank will

need to tighten monetary policy (Deloitte, 2015). The growth of the central bank’s

balance sheet will become an issue if a T Bill defaults which is unlikely to happen,

but is still a major risk. A major risk for the growing Irish economy at this moment in

time is the danger of a double dip recession. This occurred in England in the back end

of 2011 due to bank credit growth contracting by record amounts. This led the UK

economy into a double dip recession in 2012, seeing this occur only a few years ago

will lead to major worries for Irish businesses (Lyonnet & Werner, 2012).

A peculiar risk for the Irish economy to take in to account is that QE might

work too well. For instance it is difficult for the central bank to judge whether or not

16

they are using the right amount of QE. If the size of QE is not correct, there is a threat

of the central bank providing too much stimulus meaning the economy could grow at

a faster rate than it should be (Mortimer-Lee, 2012). With Ireland after going through

one of its worst ever recessions and housing crisis in its history, QE may add to the

woes of the past. As it signifies substantial risk to the stability of the bond market and

brings about volatility. If this volatility is to occur, the consequences on mortgages,

corporate borrowings and government re-financing would be liable to confine growth

(Quantitative easing: Implications for bond market volatility, 2012). If this transpires

the Irish economy will be back where it was seven years ago. Quantitative easing also

forces investors to move into riskier investments. With this materialising another

recession could be on the cards for Ireland (ECR Research, 2015).

As Ireland is a part of the Eurozone, there might be conflicting objectives

between the Irish central bank and the ECB. This is highly likely to occur between

one of the eighteen economies within the Eurozone (Deloitte, 2015). It might be for

the reason they feel the need to exit QE at a certain time and the ECB don’t deem it

appropriate at that moment in time to leave QE behind (Mortimer-Lee, 2012). If this

emerges it might put ideas into other central banks minds and the whole programme

could all go into disarray as one economy can create a domino effect for others to

follow.

Nonetheless one of the biggest risks that might come with QE that will affect

businesses in Ireland is that commodity prices might increase to unsustainable levels.

According to Palley the “Dollar exchange rate depreciation increases commodity

prices indirectly via the expected inflation effect, and directly because it increases

global commodity demand by making dollar priced commodities cheaper in the rest of

the world” (2011, p12). This would have a huge effect on Irish businesses as the cost

of transport will rise considerably, along with the cost of exporting goods rising

significantly too. As stated in the New York Times, Mr. Draghi’s only objective

officially is to drive inflation towards the central banks goal of below 2 percent. If

inflation becomes too low or even worse outright deflation occurs; companies’ profits

will be cut, wages will decrease and unemployment will rise significantly (Ewing,

2015).

17

CONCLUSION

The major quantitative easing package annonced January 2015 has been

implemented in order to stimulate growth in the eurozone economy. The above article

has analysed the positive effects of the stimulus programme on Irish businesses, along

with potential negative efects and associated risks.

As the ECB have committed to the mass purchase of eurozone government

bonds, this has increased the money supply within the european economy and

provides governments with more money to spend on both the private and public

sector. Similarly, the asset buying programme has provided banks with more money

available to lend, which may act as a catalyst for Irish businesses to expand and

increase capital expenditure on the back of lower borrowing rates. However, as a

result of the major debt overhang from the recession it may be feared that banks may

not be willing to lend or companies are not looking to expand and take advantage of

low interest rate but instead seek to deleverage balance sheets.

The QE annoncement has encouraged exchange rate depreciation which is

especially good news for Irish businesses as Ireland are an export oriented country.

The weaker euro has lead to a massive increase in competitiveness for Irish exporters,

although it will also negatively inflate the price of all imports. However this may also

be deemed positive, particularly for small Irish businesses, as it may act as a stimulant

for domestic growth.

The quantitative easing has also negatively effected the yields on government

bonds which has forced investors to move higher up the risk curve in order to increase

returns. Investors may look to equities, corporate bonds or property for the higher

yield they require, hence stimulating growth in the economy through the circulation of

money and increased consumption. As stock markets continue to appreciate in value

and investement rises this may increase consumer confidence and finally lead to

Ireland and Europe creating sustainable growth.

The impact of quantitative easing should have many positive effects for Irish

businesses, however this programme does not come without its risks. Early signals are

positive but the programme has only just begun. The programme is being

implemented across 18 different econmoies which will provide their own distinct

challenges. Also there is a chance that QE could create bubble like conditions if too

much stmulus is pumped into Europe. Ireland needs to be particularly careful of ths

18

and needs to ensure that the the economy is structurally sound with no imbamlances

like we have seen before.

To conclude, the impact of quantitative easing should have many positive

effects on Irish businesses in the short run. However problems may arise when

tapering back measures are announced and it will be interesting to see if Ireland and

indeed Europe will be able to stand on its own feet once quantitatoive eassing has

finished.

REFERENCES

1. Allen, K. (2015). Quantitative easing around the world: lessons from Japan, UK

and US. The Guardian. Retrieved 5th April 2015 from

http://www.theguardian.com/business/2015/jan/22/quantitative-easing-around-the-

world-lessons-from-japan-uk-and-us

2. Anonymous Author. (2012). Quantitative easing: Implications for bond market

volatility. Journal of Risk Management in Financial Institutions. 5 (4), pp.368-

371.

3. BBC News, (2015). What is quantitative easing? BBC News. Retrieved the 13th

April 2015 from http://www.bbc.com/news/business-15198789

4. Blinder, A. S. (2010). Quantitative Easing: Entrance and Exit Strategies (Digest

Summary). Federal Reserve Bank of St. Louis Review, 92(6), pp.465-479.

5. Bowman, D., F. Cai, S. Davies, and S. Kamin (2011): “Quantitative Easing and

bank lending: evidence from Japan,” Discussion Paper 1018, Board of Governors

of the Federal Reserve System (U.S.). Retrieved the 5th April 2015 from

http://www.federalreserve.gov/pubs/IFDP/2011/1018/ifdp1018.pdf

6. Colgan, P (2015). What quantitative easing means for Ireland. UTV Ireland.

Retrieved 7th April 2015 from http://utv.ie/Blogs/2015/03/09/What-quantitative-

easing-means-for-Ireland-33182

7. De Grauwe, P. (2015). The sad consequences of the fear of QE. The Economist.

Retrieved the 9th April 2015 from

http://www.economist.com/blogs/freeexchange/2015/01/quantitative-easing-and-

euro-zone.

19

8. Deloitte. (2015). Quantitative Easing Problem or Solution? Retrieved 11th April,

2015 from

http://www2.deloitte.com/ie/en/pages/deloitte-private/articles/quantitative-

easing.html

9. ECR Research. (2015). The dangers and drawbacks of Quantitative

Easing. Retrieved the 7th April 2015 from http://www.ecrresearch.com/world-

economy/dangers-and-drawbacks-quantitative-easing.

10. Ewing, J (2015). Eurozone Takes on Quantitative Easing, and Its Risks. New

York Times. Retrieved the 14th April 2015 from:

http://www.nytimes.com/2015/01/30/business/international/eurozone-takes-on-

quantitative-easing-and-its-risks.html?_r=0

11. Fawley, B. W., & Neely, C. J. (2013). Four stories of quantitative easing. Federal

Reserve Bank of St. Louis Review, 95(1), pp.51-88

12. Financial Interest Rates by Month – ECB Marginal Lending Rate. (n.d). Central

Statistics Office website. Retrieved the 11th April 2015 from

http://www.cso.ie/px/pxeirestat/Statire/SelectVarVal/Define.asp?

maintable=FIM08

13. Financial Interest Rates by Month – Government 10 Year Bonds. (n.d). Central

Statistics Office website. Retrieved the 11th April, 2015 from

http://www.cso.ie/px/pxeirestat/Statire/SelectVarVal/Define.asp?

maintable=FIM08

14. Hunter M. & Chisholm J., (2015) European stocks reach 15-year high. Financial

Times. Retrieved the 14th April 2015 from:

http://www.ft.com/intl/cms/s/0/8f489a3c-df63-11e4-a6c4-

00144feab7de.html#axzz3XMtKvAL5

15. Joyce, M. (2012): “Quantitative easing and other unconventional monetary

policies: Bank of England conference summary,” Bank of England Quarterly

Bulletin, 52, pp.48–56

16. Joyce, M., Lasaosa, A., Stevens, I., & Tong, M. (2011). The financial market

impact of quantitative easing in the United Kingdom. International Journal of

Central Banking, 7(3), pp.113-161.

17. Kenourgios, D., Papadamou, S., & Dimitriou, D. (2015). On quantitative easing

and high frequency exchange rate dynamics. Research in International Business

and Finance, 34, pp.110-125.

20

18. Krugman, P. R. (2008). International economics: Theory and policy, 8/E. Pearson

Education India.

19. Labonte, M., (2015). Monetary policy and the Federal Reserve: current policy and

conditions. Congressional Research Service, Library of Congress.

20. Lo, S. H., & Rogoff, K. (2015). Secular Stagnation, Debt Overhang and Other

Rationales for Sluggish Growth, Six Years On. Bank for International

Settlements, Working Papers No 482. Retrieved the 11th April 2015 from

http://www.bis.org/publ/work482.pdf

21. Lyonnet, V., & Werner, R. (2012). Lessons from the Bank of England on

‘quantitative easing’and other ‘unconventional’monetary policies. International

Review of Financial Analysis, 25, pp.94-105.

22. Mortimer-Lee, P. (2012). The effects and risks of quantitative easing. Journal of

Risk Management in Financial Institutions, 5(4), pp.372-389.

23. Palley, T. I. (2011). Quantitative easing: a Keynesian critique. investigación

económica, pp.69-86.

24. Pasani-Ferry, J., Jean, S., Hauschild, H., Kawai, M., Fan, H. and Park, Y. C.

(2013). Deleveraging and global growth a call for coordinated macroeconomic

policies. Paper based on Asia Europe Economics Forum Conference. Retrieved

11th April, 2015 from

http://www.bruegel.org/publications/publication-detail/publication/778-

deleveraging-and-global-growth/

25. Power, J. (2015). Weak euro will help economic recovery. The Irish Examiner.

Retrieved the 7th April 2015 from:

http://www.irishexaminer.com/business/features/weak-euro-will-help-economic-

recovery-318139.html.

26. Reuters. (2015). Morgan Stanley says dollar parity beckons for euro by Q4.

Reuters. Retrieved the 13th April 2015 from:

http://www.reuters.com/article/2015/04/13/markets-forex-euro-

idUSL5N0XA0Z420150413.

27. RTE News, (2015). ECB to begin QE programme on 9th March. RTE News.

Retrieved the 13th April 2015 from http://www.rte.ie/news/2015/0305/684618-ecb

28. Strauss. D and Gordon. S (2015). Big European groups expect boost from weak

euro. The Financial Times. Retrieved 13 April 2015 from

21

http://www.ft.com/intl/cms/s/0/b93f5088-4f03-11e4-a1ef-

00144feab7de.html#axzz3XMtKvAL5.

29. Teagasc, (2015). Agri-food. Retrieved the 9th April 2015 from

http://www.teagasc.ie/agrifood/.

30. The Bank of England, (2015). What is Quantitative Easing? Retrieved 4th April

2015 from http://www.bankofengland.co.uk/monetarypolicy/pages/qe/default.aspx

31. The Economist, (2015). Better late than never. The Economist. Retrieved 13 April

2015 from http://www.economist.com/news/finance-and-economics/21640371-

policy-will-help-less-so-other-big-economies-better-late

32. Toshihiko, F. (2003), “Challenges for Monetary Policy in Japan,” Speech at the

Spring Meeting of the Japan Society of Monetary Economics, on the occasion of

its 60th anniversary, on June 1 2003.

33. Walker, A. (2014). Has quantitative easing worked in the US? BBC News.

Retrieved the 5th April 2015 from http://www.bbc.com/news/business-29778331

34. Wyplosz, C. (2014). Recent ECB Actions. The European Parlement. Retrieved

11th April, 2015 from

http://www.europarl.europa.eu/document/activities/cont/201409/20140917ATT89

229/20140917ATT89229EN.pdf

35. Yahoo. (2015). Yahoo Finance. Retrieved the 13th April 2015 from

https://uk.finance.yahoo.com/.

22