THE EFFECT OF BUDGET DEFICIT ON INTEREST … · deficit financing is the issue of government...

14

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai (in partnership with The Journal of Developing Areas, Tennessee State University, USA) ISBN 978-0-9925622-3-6 370 THE EFFECT OF BUDGET DEFICIT ON INTEREST RATES IN SUB-SAHARAN AFRICA COUNTRIES: A PANEL VAR APPROACH Ikechukwu Kelikume Lagos Business School, Pan-Atlantic University, Lagos, Nigeria ABSTRACT The 2007-2008 global economic crisis and the recent effects of declining global oil prices has led most countries in sub- Saharan Africa to respond by borrowing massively from both domestic and international market to fund the day to day running of the home country. The effects of borrowing and increased deficit financing raises the age old question of the linkage between government deficit financing and domestic interest rates. Notable amongst the issue raised by increasing deficit financing is the issue of government borrowing crowding out private sector investment. Though there are theories, which link budget deficit and interest rate, however, there is no consensus on the relationship between them. This study, therefore, examine the effect of government deficit financing on interest rates. The study made use of the panel Vector Auto regression techniques on dataset collected from 18 countries across Sub-Saharan Africa (SSA) over the period 2000 to 2014. The results obtained for this study showed that interest rate initially responded negatively to rising budget deficit which negates the conventional Keynesian proposition which states that government deficit reduces the stock of loanable funds and subsequently crowds out private sector investment. Subsequently, the result shows that interest rate became neutral or insensitive to rising government budget deficit. The findings lend credence to the Ricardian Equivalence theory, which emphasizes the neutrality of budget deficit on interest rate. It was also found that interest rate response positively to exchange rate, inflation, and money supply. The policy implication of this study is that Sub-Saharan African economies can increase government borrowing without concerning itself with rising domestic interest rate. JEL Classifications: E4, H6 Keywords: Budget Deficit, Interest Rate, Panel VAR, SSA Corresponding Author’s Email Address: [email protected] INTRODUCTION Budget deficit occurs when the government spending exceed its tax revenue. There have been cases of large government budget deficit since the late 1970s and this has generated controversial issue among economists. Notable of the issues is that the high interest rate in the past years is attributable to the government deficit budget. Though there are theories, which link budget deficit and interest rate, however, there is no consensus on the relationship between them. The Conventional Keynesian preposition (CKP) is of the view that budget deficit results in the reduction of loanable funds thus, leading to a rise in the interest rate and crowding out of private sector investment. The CKP further presupposes that reduced loan able funds will cause net foreign investment to fall in an open economy since domestic savings now attract higher rates of return and investing abroad is less attractive. Hence, budget deficit according to the CKP, raise both domestic and foreign interest rates, causing decline in net foreign investment. Some authors’ work such as Laumas (1989), Dua (1993), and Bovenberg (1998) tend to lend credence to the CKP. The Ricardian Equivalent Hypothesis (REH), on the other hand, emphasized on the neutral effect of budget deficit on interest rate, that is, government budget deficit has no impact on macroeconomic variables. The Ricardian argument is based on the premise that an increase in government budget deficit is equivalent to a future increase in tax liabilities and therefore, budget deficits do not have any impact on macroeconomic variables. Some of the authors whose studies conforms to the REH include Barro (1987), Evans (1987), Darrat (1990), Findlay (1990), and Ostrosky (1990). Fiscal policy in most sub-Saharan countries has remained expansionary, which has resulted to vulnerability to external shocks. Over one-third of the sub-Saharan Africa countries have been experiencing fiscal deficit after the global financial crisis of 2007 (Punam et al., 2011) and this has led to the accumulation of public debt by oil exporters, middle-income, and low-income countries in sub-Saharan Africa countries. For instance, the rate of change in public sector debt between 2007 and 2012 in the oil exporting countries in sub-

Transcript of THE EFFECT OF BUDGET DEFICIT ON INTEREST … · deficit financing is the issue of government...

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

370

THE EFFECT OF BUDGET DEFICIT ON INTEREST RATES

IN SUB-SAHARAN AFRICA COUNTRIES: A PANEL VAR

APPROACH

Ikechukwu Kelikume

Lagos Business School, Pan-Atlantic University, Lagos, Nigeria

ABSTRACT

The 2007-2008 global economic crisis and the recent effects of declining global oil prices has led most countries in sub-

Saharan Africa to respond by borrowing massively from both domestic and international market to fund the day to day

running of the home country. The effects of borrowing and increased deficit financing raises the age old question of the

linkage between government deficit financing and domestic interest rates. Notable amongst the issue raised by increasing

deficit financing is the issue of government borrowing crowding out private sector investment. Though there are theories,

which link budget deficit and interest rate, however, there is no consensus on the relationship between them. This study,

therefore, examine the effect of government deficit financing on interest rates. The study made use of the panel Vector Auto

regression techniques on dataset collected from 18 countries across Sub-Saharan Africa (SSA) over the period 2000 to 2014.

The results obtained for this study showed that interest rate initially responded negatively to rising budget deficit which

negates the conventional Keynesian proposition which states that government deficit reduces the stock of loanable funds and

subsequently crowds out private sector investment. Subsequently, the result shows that interest rate became neutral or

insensitive to rising government budget deficit. The findings lend credence to the Ricardian Equivalence theory, which

emphasizes the neutrality of budget deficit on interest rate. It was also found that interest rate response positively to

exchange rate, inflation, and money supply. The policy implication of this study is that Sub-Saharan African economies can

increase government borrowing without concerning itself with rising domestic interest rate.

JEL Classifications: E4, H6

Keywords: Budget Deficit, Interest Rate, Panel VAR, SSA

Corresponding Author’s Email Address: [email protected]

INTRODUCTION

Budget deficit occurs when the government spending exceed its tax revenue. There have been cases of large

government budget deficit since the late 1970s and this has generated controversial issue among economists.

Notable of the issues is that the high interest rate in the past years is attributable to the government deficit

budget. Though there are theories, which link budget deficit and interest rate, however, there is no consensus on

the relationship between them. The Conventional Keynesian preposition (CKP) is of the view that budget deficit

results in the reduction of loanable funds thus, leading to a rise in the interest rate and crowding out of private

sector investment. The CKP further presupposes that reduced loan able funds will cause net foreign investment

to fall in an open economy since domestic savings now attract higher rates of return and investing abroad is less

attractive. Hence, budget deficit according to the CKP, raise both domestic and foreign interest rates, causing

decline in net foreign investment. Some authors’ work such as Laumas (1989), Dua (1993), and Bovenberg

(1998) tend to lend credence to the CKP. The Ricardian Equivalent Hypothesis (REH), on the other hand,

emphasized on the neutral effect of budget deficit on interest rate, that is, government budget deficit has no

impact on macroeconomic variables. The Ricardian argument is based on the premise that an increase in

government budget deficit is equivalent to a future increase in tax liabilities and therefore, budget deficits do not

have any impact on macroeconomic variables. Some of the authors whose studies conforms to the REH include

Barro (1987), Evans (1987), Darrat (1990), Findlay (1990), and Ostrosky (1990).

Fiscal policy in most sub-Saharan countries has remained expansionary, which has resulted to

vulnerability to external shocks. Over one-third of the sub-Saharan Africa countries have been experiencing

fiscal deficit after the global financial crisis of 2007 (Punam et al., 2011) and this has led to the accumulation of

public debt by oil exporters, middle-income, and low-income countries in sub-Saharan Africa countries. For

instance, the rate of change in public sector debt between 2007 and 2012 in the oil exporting countries in sub-

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

371

Saharan Africa countries include Chad 26%, Nigeria 12.7%, and Angola 21.4%. For the middle-income

countries, the rate of change in public sector debt in Senegal was 23.5%, South-Africa 25.4%, Ghana 31%, Cape

Verde 73.9% Mauritius 56.2%, Lesotho 50.6% while for low income earner include Malawi 41%, Tanzania

40.6%, Sierria Leone 43.2 and Ethiopia 43.5% (International Monetary Fund, 2013).

Despite this trend, the impact of budget deficit on interest rate still remains controversial and

inconclusive as many studies came up with diverse findings. This, therefore, has motivated the study to examine

the effects of budget deficit on interest rate in sub-Saharan Africa countries. The major innovation of this study

is the methodology adopted as well as its scope

This paper is structured into five sections. The first section is this part which introduces the topic.

Section two examines the empirical literature while section three presents the methodology and data source.

Section four discusses the results of findings while section five which is the last part presents the conclusion.

LITERATURE REVIEW

Several studies abound on the relationship between government budget deficit and interest rate. Empirical

findings as regards the relationship are however, conflicting and inconsistence. Mukhtar & Zakaria (2008) in

their study of the budget deficits and interest rate in Pakistan and tested the conventional crowding-out

prepositions against the Ricardian deficit neutrality. They found that budget deficits have no significant effect

on nominal interest rate, thus lending credence to the Ricardian view. Caporale, Pittis & Prodromidis (2013)

research, on the other hand, examined the relationship between budget deficits and interest rates in the US

economy using cointegration and causality approach and found a positive relationship between budgets deficit

and interest rates in both short-run and long-run.

Bovenberg (1998) empirical investigation of the long-term interest rates in the United States noted that

fiscal deficits results in increase in real long-term interest rates. The study, on the bases of both theoretical and

empirical evidence, asserts that neither the response of national capital mobility nor private savings has

prevented budget deficits from raising interest rates. On the contrary, Chen (2011) study of budget deficits and

interest rates for Japan found that a higher government deficit as a percentage of GDP leads to a lower long-term

interest rates in Japan. Meanwhile, Darrat (1990) study on structural Federal deficits and interest rates using

causality and co-integration test failed to establish the existence of causal relationship between structural federal

deficits and interest rates. In addition, it was found that there was no co-integration between structural deficits

and corporate rate, implying that there is lack of long-run relationship between the two variables. This result,

therefore, cast a doubt on the crowding-out effects of budget deficits preposition by the CKP. In the same vein,

Odionye & Uma (2013) a long-run relationship between budget deficit and interest rate in Nigeria. The result,

however, indicate the existence of a long-run relationship between budget deficit and interest rate, hence,

lending the credence to the Keynesian preposition.

Laubach (2009) study of interest rate effects of budget deficits concluded that the effect of government

deficits on interest rates is significant. The outcome of the study noted that a one percent point increase in

projected deficit-to-GDP ratio would result in a rise in the long-term interest rates by approximately 25 points.

Aisen & Hauner (2009) explored the interaction between budget deficits and interest rates in both the advanced

and emerging economies using the generalize method of moment (GMM). The overall findings revealed that

there is a positive and significance relationship between budgets deficit and interest rates. Also, Cebula (2003)

study of budget deficits and interest rates in Germany revealed that there exists a long-run relationship between

budget deficits and the nominal interest rate.

Laumas (1989) investigated the effects of anticipated and unanticipated effect of budget deficit on

interest rates and found that the impact of both variables, anticipated and unanticipated budget deficits, on

interest rates are statistically significant. In the same vein, Dua (1993) conducted a study on the relationship

between interest rates, government purchases, and budget deficits. The outcome of the study showed that the

movements in both expected and actual deficit have significant impact on long-term interest rates. On the

contrary, Evans (1987) carried out a study on interest rates and expected future budget deficits in the United

States and found no evidence that current, past, and expected budget deficits are related to interest rates. Pandit

(2005) examined the impact of fiscal deficit on long-term nominal interest rate in Nepal. The findings of the

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

372

study revealed that the impact of fiscal deficit on long-term nominal interest rates is insignificant, thus, lending

credence to the outcome of Evans (1987). Pandit findings, however, differ from that of Evans, as the study

observed a positive relationship between fiscal deficits and long-term interest rates.

Kormendi & Protopapadakis (2004) investigated the impact of budgets deficits on cash account deficits

and real interest rates by testing the conventional preposition against the Ricardian view. They found no

evidence of a positive effect of both current and expected budget deficits on real interest rates. In the same vein,

Dvorný (2006) examined the impact of budget deficit on interest rates in Czech in bid to testing the predictions

of the three paradigms, Keynesian, neoclassical and the Ricardian. The results of the study showed that there is a

negative relationship between budget deficit and interest rate in the short-run, hence, validating the Ricardian

preposition. However, Gale & Orszag (2004) conducted a study on budget deficits, national saving, and interest

rates with the view of testing the Ricardian and the non-Ricardian models. They found that projected future

budget deficits affect long-term interest rates while the current deficits do not.

Cebula (2012) investigation of the causality between primary budget deficits and the ex ante real long-

term interest rate in the United States using error correction model (ECM) estimation suggests a bi-directional

relationship exist between primary budget deficit and ex ante real long-term interest rate yield. Also, Cebula

(1991) study on Federal budget deficits and the term structure of real interest rates in United States using 2SLS

estimation of quarterly data noted that budget deficits increases the slope of the yield curve. On the contrary,

Hussain & Saaed (2014) study on the relationship between budget deficits and macroeconomics variables in

United Arab Emirates, using the granger causality technique, found that there is no directional causality between

budget deficits and nominal effective exchange rates.

The foregoing empirical literature signal that the relationship between budget deficit and interest rate is

yet inconclusive, that is, deficit budgets either increase, decrease, or do not have any effect on interest rate. It is

believed that the outcome of this study, in addition to previous studies, will offer a lucid relationship between

the two variables, particularly as it relates to the sub-Saharan countries.

METHODOLOGY

Sources of Data and Description

The study used secondary data sourced from the World Bank Development Indicators (WDI) and International

Financial Statistics of the International Monetary Fund (IMF). The dataset used for the study comprises of

annual data on 18 sub-Saharan countries over the period of 2000-2014. These countries include Angola,

Botswana, Cape Verde, Congo, Dr Congo, Equatorial Guinea, Gambia, Kenya, Lesotho, Mozambique, Namibia,

Nigeria, Sierria Leone, Sao Tome, South-Africa, Seychelles, Zambia, and Uganda. The rationale for using these

selected countries out of the 44 countries in sub-Saharan Africa is because of the availability of data on the

selected variables. The choice of variables for this study include real interest rate (RIR), budget deficits as a

ratio of GDP (BDGDP), inflation (INF), money supply as a percentage ratio of the GDP (M2GDP), and

exchange rate to US Dollar (EXR). The selected variables are consistence with empirical studies carried out by

(Mukhtar & Zakaria, 2008; Laubach, 2009; Odionye & Uma, 2013; Caporale et al., 2013).

Panel Unit Root Test and Cointegration analysis

The study first employed the panel unit root test to examine the properties of the data. Panel unit root test helps

to investigate the presence of a unit root. It is important to note that the first generation of panel unit-root test,

which include Hadri (2000) and Im et al. (2003), assumed cross sectional independence among panel units.

However, the second generation test, which includes Smith et al. (2004); and Pesaran (2007), relax the

assumption of cross-sectional independence and allowed for variety of dependence across the different units. In

investigating the presence of panel unit root of the 18 sub-Saharan countries, the study used Levin, Lin & Chu

or LLC (2002); Im, Pesaran and Shin or IPS (2003); ADF-Fisher Chi-square; PP – Fisher Chi-square and the

Hadri test.

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

373

Impulse Response Function and Variance Decomposition

The impulse response function (IRF) gives information on the response of an endogenous variable to one of the

innovations. It traces the effects on present and future values of the endogenous variable of one standard

deviation shock to one of the innovations. However, IRF does not show the extent in which the shock in variable

affects the other. Hence, the estimation of the variance decomposition (VDC) becomes important. The VDC

separates the variation in an endogenous variable into component shocks to the VAR. Hence, VDC offers

information on the relative importance of each random innovation in affecting the variables in the VAR. The

study also employed inverse roots of AR graph to test the stability of the estimated PVAR and the reliability of

the IRF. PVAR is said to be stable when the polynomial roots are within the circle.

Panel Vector Autoregressive Model

Vector Autoregressive (VAR) methodology is appropriate for this study given the lack of an a priori theory

regarding the relationship between the variables of the model. Also the choice of panel VAR approach rest on its

suitability in incorporating time variation in the coefficients and in the variance of the shocks (Canova &

Ciccarelli, 2013). The methodology is based on a framework that permits variables to be entered as endogenous

within a system of equations, where the short run dynamic relationships could be subsequently identified

(Koutsomanoli-Filippaki & Mamatzakis, 2009). The VAR also assist in investigating the underlying causal

relationships between the key variables: interest rates and budget deficit. In this way, it is possible to have one-

way causality, running from budget deficit to interest rate or vice versa. It is also possible to have a bi-

directional one. The Panel VAR is specified as follow:

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

∑

Where:

RIR = Real interest rate

BDGDP = Budget deficit as a percentage of GDP

LOG (EXR) = Log of exchange rate in US Dollar

INF = Inflation rate

M2GDP = Money Supply as a percentage of GDP

= Stochastic error term called impulses or innovations or shocks in VAR.

= Country and year respectively

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

374

RESULTS

Descriptive Statistics

Table 1 depicts the results of the descriptive statistics of the variables in the 18 selected sub-Saharan Africa

countries. The results show that the averages real interest rate (RIR) prevalence in the selected countries is 9

percent while the maximum real interest rate is 40 percent. The budget deficit as a percentage of the GDP has an

average of -0.14 and a maximum average value of 128.11. The results also indicate that the average exchange

rate is 4.301. The results further reveal that the average inflation (INF) rate in sub-Saharan countries is 11.7

percent while the maximum inflation rate is 152.5 percent. The money supply as a percentage of the GDP

(M2GDP), which represents financial deepening, shows an average of 38.59 and the maximum level of 110.7.

TABLE 1: DESCRIPTIVE STATISTICS

Mean St-dev Min Max

RIR 9.114 10.293 -42.310 40.190

BDGDP -0.139 12.208 -17.980 128.110

LOG(EXR) 4.301 2.465 1.280 9.855

INF 11.783 17.285 -9.620 152.560

M2GDP 38.598 23.357 6.010 110.770

Source: Author’s Computation and EViews 9 Output

Table 2 reports the outcome of the panel unit root test for each variable. On the bases of the principles of Levin,

Lin & Chu or LLC (2002); Im, Pesaran and Shin or IPS (2003); ADF-Fisher Chi-square; PP – Fisher Chi-square

and the Hadri test, The results reveal that none of the variables, except M2GDP, possesses unit root or common

root at 1% and 5% level of significance. Thus, the variable possesses the properties of stationarity, that is, they

are integrated of order zero I[0]. As a result of this, the issue of testing for panel cointegration would not be

relevant for this study.

TABLE 2: PANEL UNIT ROOT TEST

RIR: lag 1 BDGD: lag 1

Method Statistic Prob.** Statistic Prob.**

Levin, Lin & Chu t* -4.85921 0.0000 -20.1120 0.0000

Im, Pesaran and Shin W-stat -4.1490 0.0000 -3.09309 0.0010

ADF - Fisher Chi-square 82.8768 0.0000 55.1454 0.0067

PP - Fisher Chi-square 147.572 0.0000 60.0426 0.0019

Hadri Z-stat 2.4867 0.0000 5.2170 0.0000

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

375

LOG(EXR):

lag 1 INF: lag 1

Method Statistic Prob.** Statistic Prob.**

Levin, Lin & Chu t* -2.8425 0.0022 -40.1035 0.0000

Im, Pesaran and Shin W-stat -1.2273 0.1099 -11.6693 0.0000

ADF - Fisher Chi-square 47.0710 0.1025 83.6556 0.0000

PP - Fisher Chi-square 78.2571 0.0001 133.646 0.0000

Hadri Z-stat 9.7562 0.0000 7.3620 0.0000

D(M2GDP):

lag 1

Method Statistic Prob.**

Levin, Lin & Chu t* -6.9049 0.0000

Im, Pesaran and Shin W-stat -5.0097 0.0000

ADF - Fisher Chi-square 87.5921 0.0000

PP - Fisher Chi-square 162.368 0.0000

Hadri Z-stat 8.5149 0.0000

Source: Author’s Computation and EViews 9 Output

Table 3 depicts the results of the optimum lag selection criteria. The panel VAR selection criteria was estimated

in bid to determining the optimum lag length to be adopted in estimating the panel VAR (Anetor et al., 2016).

All the information criteria, that is, the Sequential modifies LR test statistics (LR), Final prediction error (FPE),

Akaike information criterion (AIC), Schwarz information criterion (SC), and the Haanan-quinn information

criteria (HQ), suggest the optimum lag length of 1.

TABLE 3: PVAR OPTIMUM LAG SELECTION CRITERIA

Lag LogL LR FPE AIC SC HQ

0 -1285.828 NA 1.63e+08 33.09815 33.24922 33.15862

1 -1008.009 512.8959* 249635.0* 26.61562* 27.52204* 26.97848*

2 -995.2173 21.97565 344113.1 26.92865 28.59043 27.59389

3 -980.0126 24.17152 451326.2 27.17981 29.59695 28.14744

4 -962.5936 25.45858 569688.3 27.37419 30.54669 28.64420

Source: Author’s Computation using EViews 9. *indicates lag order selected by the criterion at 5 percent level

of significance.

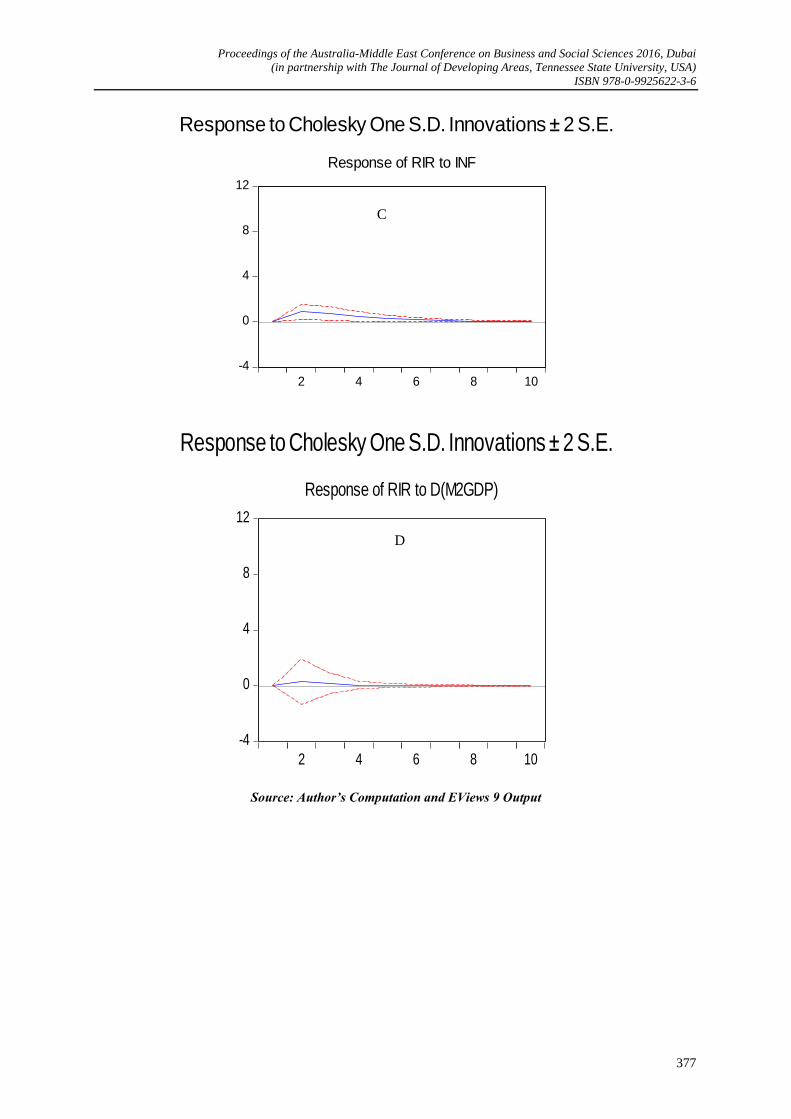

Figure 1 shows the IRFs derived from the estimated panel VAR equations above. The horizontal axis of the

IRFs indicates the number of periods that have passed after the impulse has been given. The vertical axis, on the

other hand, measures the responses of the variables. It is important to emphasize that explanation will be

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

376

focused on the response of the real interest rate (RIR) due to the shocks in other variables. Panel A IRF depicts

the response of RIR to a shock in budget deficit as a percentage of GDP (BDGDP) in the period of 10 years. It

shows that a shock in BDGDP results in a negative impact on RIR in the first-five period and subsequently

produces neutral effect on RIR as shown by the graph i.e. lying on the origin. It can be inferred from this results

that budget deficits in sub-Saharan Africa countries have negative impact on the interest rate in the short-run

(Dvorný, 2006) and subsequently have no effect on the interest rate in the long-run (Evans, 1987; Kormendi &

Protopapadakis, 2004; Pandit, 2005; Mukhtar & Zakaria, 2008). Panel B shows that a one percent innovation in

exchange rate LOG(EXR) produces a positive effects on real interest rate (RIR). This suggests that currency

appreciation in sub-Saharan Africa countries give rise to increase in interest rate. In the same vein, Panel C

indicates that a shock in inflation lead to rise in interest rate. Panel D reveals that a one percent innovation in

M2GDP results in a positive effects in RIR.

FIGURE 1: IMPULSE RESPONSE FUNCTIONS GRAPH

-4

0

4

8

12

2 4 6 8 10

Response of RIR to BDGDP

Response to Cholesky One S.D. Innovations ± 2 S.E.

-4

0

4

8

12

2 4 6 8 10

Response of RIR to LOG(EXR)

Response to Cholesky One S.D. Innovations ± 2 S.E.

A

B

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

377

-4

0

4

8

12

2 4 6 8 10

Response of RIR to INF

Response to Cholesky One S.D. Innovations ± 2 S.E.

-4

0

4

8

12

2 4 6 8 10

Response of RIR to D(M2GDP)

Response to Cholesky One S.D. Innovations ± 2 S.E.

Source: Author’s Computation and EViews 9 Output

C

D

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

378

Figure 2 reports the inverse roots of the panel VAR. The graph to investigate if the panel VAR and the IRFs are

stable and reliable. The panel VAR and the IRFs are said to be stable if the polynomial roots fall within the

circle. Hence, the inverse of the AR characteristics polynomial suggests that the panel VAR is stable and the

IRFs are reliable.

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Figure2: Inverse Roots of AR Characteristic Polynomial

Source: Author’s Computation and EViews9 Output

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

379

Figure 3 depicts the residual trends of the endogenous variables. The results are appears consistence with the

IRFs outcomes. For instance, a cursory look at the BDGDP trend vis-à-vis the RIR shows that an upsurge of

BDGDP results in slight negative respond in RIR. However, a comparative of LOG(EXR), INF, and

D(M2GDP) with the trend in RIR is similar, that is, they almost have the pattern of movement. These patterns of

movement suggest a positive relationship.

FIGURE 3: RESIDUAL TRENDS OF ENDOGENOUS VARIABLES

-60

-40

-20

0

20

40

1 -

03

1 -

08

2 -

07

2 -

12

3 -

10

4 -

05

5 -

09

7 -

06

8 -

04

8 -

09

9 -

04

10

- 1

1 1

1 - 0

7 1

2 - 0

4 1

2 - 0

9 1

3 - 0

9 1

4 - 0

4 1

4 - 0

9 1

5 - 0

4 1

5 - 0

9 1

6 - 0

4 1

6 - 0

9 1

7 - 0

4 1

7 - 0

9 1

8 - 0

5 1

8 - 1

0

RIR Residuals

-40

0

40

80

120

160

1 -

03

1 -

08

2 -

07

2 -

12

3 -

10

4 -

05

5 -

09

7 -

06

8 -

04

8 -

09

9 -

04

10

- 1

1 1

1 - 0

7 1

2 - 0

4 1

2 - 0

9 1

3 - 0

9 1

4 - 0

4 1

4 - 0

9 1

5 - 0

4 1

5 - 0

9 1

6 - 0

4 1

6 - 0

9 1

7 - 0

4 1

7 - 0

9 1

8 - 0

5 1

8 - 1

0

BDGDP Residuals

-.6

-.4

-.2

.0

.2

.4

1 -

03

1 -

08

2 -

07

2 -

12

3 -

10

4 -

05

5 -

09

7 -

06

8 -

04

8 -

09

9 -

04

10

- 1

1 1

1 - 0

7 1

2 - 0

4 1

2 - 0

9 1

3 - 0

9 1

4 - 0

4 1

4 - 0

9 1

5 - 0

4 1

5 - 0

9 1

6 - 0

4 1

6 - 0

9 1

7 - 0

4 1

7 - 0

9 1

8 - 0

5 1

8 - 1

0

LOG(EXR) Residuals

-30

-20

-10

0

10

20

30

40

1 -

03

1 -

08

2 -

07

2 -

12

3 -

10

4 -

05

5 -

09

7 -

06

8 -

04

8 -

09

9 -

04

10

- 1

1 1

1 - 0

7 1

2 - 0

4 1

2 - 0

9 1

3 - 0

9 1

4 - 0

4 1

4 - 0

9 1

5 - 0

4 1

5 - 0

9 1

6 - 0

4 1

6 - 0

9 1

7 - 0

4 1

7 - 0

9 1

8 - 0

5 1

8 - 1

0

INF Residuals

-30

-20

-10

0

10

20

30

1 -

03

1 -

08

2 -

07

2 -

12

3 -

10

4 -

05

5 -

09

7 -

06

8 -

04

8 -

09

9 -

04

10

- 1

1 1

1 - 0

7 1

2 - 0

4 1

2 - 0

9 1

3 - 0

9 1

4 - 0

4 1

4 - 0

9 1

5 - 0

4 1

5 - 0

9 1

6 - 0

4 1

6 - 0

9 1

7 - 0

4 1

7 - 0

9 1

8 - 0

5 1

8 - 1

0

D(M2GDP) Residuals

Source: Author’s Computation and EViews9 Output

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

380

Table 4 depicts the variance decompositions (VDCs), which shed more light to the IRFs results. The results

shows that 1.2% of budget deficit (BDGDP) forecast error variance of interest rate (RIR) after ten year period,

while exchange rate (LOG(EXR)) accounts for 1% of the variation in RIR. In the case of inflation (INF), the

VDCs report reveals that INF accounts for about 2% variation in RIR, while money supply (D(M2GDP))

accounts for just 0.1%. This implies that the predominant source of variation of RIR in sub-Saharan Africa

countries is INF follow by BDGDP.

TABLE 4: VARIANCE DECOMPOSITION OF REAL INTEREST RATE (RIR)

S.E. RIR BDGDP LOG(EXR) INF D(M2GDP)

1 9.281812 100.0000 0.000000 0.000000 0.000000 0.000000

2 9.670613 97.60658 1.119488 0.360925 0.827397 0.085605

3 9.725819 96.63390 1.234418 0.641670 1.374629 0.115380

4 9.745660 96.24703 1.233674 0.794702 1.606468 0.118129

5 9.754993 96.07950 1.231385 0.876656 1.694500 0.117963

6 9.759652 95.99845 1.230502 0.925079 1.728090 0.117881

7 9.762266 95.95281 1.230000 0.957695 1.741629 0.117868

8 9.763981 95.92241 1.229624 0.982537 1.747567 0.117863

9 9.765284 95.89898 1.229312 1.003390 1.750464 0.117855

10 9.766388 95.87891 1.229039 1.022147 1.752060 0.117844

Source: Author’s Computation using EViews 9

Table 5 depicts the panel VAR granger causality test. The outcome of the test reveals that budget deficit

(BDGDP) does not granger cause the interest rate (RIR) because the p-value = 0.1923 exceeds 0.05. Thus, the

null hypothesis that BDGDP does not granger cause RIR cannot be rejected. In the same vein, the p-value of

exchange rate (LOG(EXR)) is also greater than 0.05, which implies that the null hypothesis that LOG(EXR)

does not granger cause RIR cannot be rejected. However, inflation (INF) has a p-value = 0.0077, which is less

than 0.05. This outcome suggests that INF is significant. Hence, the null hypothesis that INF does not granger

cause RIR is rejected. This outcome further suggests that there is a unidirectional causality between INF and

RIR that is, INF causes RIR. The panel VAR granger causality test further indicate that money supply

(D(M2GDP)) does not granger cause RIR. These results substantiated the outcomes of the IRFs and VDCs,

particularly the VDCs, that inflation is a key determinant of interest rates in the sub-Saharan Africa countries.

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

381

TABLE 5: VAR GRANGER CAUSALITY/BLOCK

EXOGENEITY WALD TESTS

Dependent variable: RIR

Excluded Chi-sq Df Prob.

BDGDP 1.700126 1 0.1923

LOG(EXR) 2.219173 1 0.1363

INF 7.113418 1 0.0077

D(M2GDP) 0.121654 1 0.7272

All 11.44921 4 0.0220

Dependent variable: BDGDP

Excluded Chi-sq Df Prob.

RIR 0.104252 1 0.7468

LOG(EXR) 0.197318 1 0.6569

INF 0.317457 1 0.5731

D(M2GDP) 0.447216 1 0.5037

All 1.157881 4 0.8850

CONCLUSION

The study examined the effects of budget deficits on interest rates in 18 countries in sub-Saharan Africa over the

period of 2000 to 2014 using panel VAR approach. The outcome of the panel VAR analysis, in terms of IRFs,

VDCs, and causality, revealed some interesting findings. From the IRFs, it was found that the interest rate

initially responded negatively to budget deficit and subsequently, there was a neutral reaction of interest rate to

budget deficit. It was also noted that interest rate reacted positively to exchange rate. The same applies to

inflation and money supply, interest rate responded positively to money supply and interest rate. The VDCs,

however, showed that inflation rate accounts more for the variation in interest rate vis-à-vis other variables. The

panel VAR granger causality test revealed that inflation mainly granger cause interest rate. This, therefore

implies that inflation rate provide much explanation for interest rate.

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

382

REFERENCES

Aisen, A & Hauner, D 2009, ‘Budget deficits and interest rates: a fresh perspective’, Applied Economics, vol.

45, no. 17, pp. 2501-2510.

Anetor, FO, Ogbechie, C, Kelikume, I, & Ikpesu, F 2016, ‘Credit Supply and Agricultural Production in

Nigeria: A Vector Autoregressive (VAR) Approach’, Journal of Economics and Sustainable

Development, vol. 7, no.2, pp.131-143.

Barro R 1987, ‘Government Spending, Interest Rates, Prices, and Budget Deficits in the United Kingdom 1701-

1918’, Journal of Monetary Economics, vol.20, no.2, September, pp. 221-47.

Bovenberg, LA 1998, ‘Long – Term Interest Rates in the United States: An Empirical Analysis’, IMF Staff

Papers, 35, no.2, June, pp. 382-90

Canova, F & Ciccarelli, M 2013, ‘Panel Vector Autoregressive Models: A Survey’, Working Paper Series, no

1507/January

Caporale, GM, Pittis, N, & Prodromidis, K 2013, ‘Budget Deficits and Interest Rates: A Cointegration and

Causality Analysis’, Revista Brasileira de Economia de Empresas, vol.4, no.1

Cebula, RJ 1991, ‘A note on federal budget deficits and the term structure of real interest rates in the United

States’, Southern Economic Journal, pp. 1170-1173.

Cebula, RJ 2003, ‘Budget deficits and interest rates in Germany’, International Advances in Economic

Research, vol. 9 no.1 pp. 64-68.

Cebula, RJ 2012, ‘A contemporary investigation of causality between the primary government budget deficit

and the ex ante real long term interest rate in the US’, PSL Quarterly Review, vol. 55, no.223.

Chen, Y 2011, ‘A study of budget deficits and interest rates for Japan: evidence from an extended loanable

funds model’, Journal of International and Global Economic Studies, vol. 4, no. 1, pp. 11-27.

Cheug, BS 1998. The Causality between Budget Deficits and Interests Rates in Japan: An Application of Time

Services Analysis, Applied Economic Letters, 5, no.7, July pp.419-22.

Darrat, AF 1990, ‘Structural Federal Deficits and Interest Rates: Some Causality and Cointegration Tests’,

Southern Economic Journal, vol. 56, no.3, January pp.752-59.

Dua, P 1993, ‘Interest Rates, Government Purchases and budget Deficit: A forward-looking model’, Public

Financial Quarterly

Dvorný, Z 2006 ‘Budget Deficit and Interest Rates’, Prague Economic Papers, vol. 2006, no.1, pp. 3-13.

Evans, P 1987, ‘Do Budget Deficits Raise Nominal Interest Rates?’, Journal of Monetary Economics vol. 20,

no.2 September, pp.281-300.

Findlay, DW 1990, ‘Budget Deficits, Expected Inflation and Short-term Real Interest Rates: Evidence for the

United States’, International Economic Journal, vol.4, pp. 41-53.

Gale, WG & Orszag, PR 2004, ‘Budget deficits, national saving, and interest rates’, Brookings Papers on

Economic Activity, vol. 2004, vol.2, pp.101-210.

Hadri, K 2000, ‘Testing for Stationary in Heterogeneous Panel Data’, Econometric Journal, vol.3, no.2,

P.14861.

Hussain, MA & Saaed, AA 2014, ‘The relationship between budget deficits and macroeconomics variables in

United Arab Emirates: an empirical investigation’, Journal of Emerging Trends in Economics and

Management Sciences, vol.5, no. 5, P.449

Im KS, Pesaran MH, Shin Y 2003, ‘Testing for unit roots in heterogeneous panels’, Journal of Econometrics,

vol.115, no.1, pp.53-74.

International Monetary Fund 2013, ‘Regional Economic Outlook: Sub-Saharan Africa’, May

Kormendi, RC & Protopapadakis, A 2004, ‘Budget Deficits, Current Account Deficits, and Interest Rates: The

Systematic Evidence on Ricardian Equivalence’, Center for Society and Economy, Business School,

University of Michigan.

Koutsomanoli-Filippaki, A & Mamatzakis, E 2009, ‘Performance and Merton-type default risk of listed banks in

the EU: a panel VAR approach;, Journal of Banking & Finance, vol. 33, no. 11, pp.2050-2061.

Laubach, T 2009, ‘New evidence on the interest rate effects of budget deficits and debt’, Journal of the

European Economic Association, vol.7, no.4, pp.858-885

Proceedings of the Australia-Middle East Conference on Business and Social Sciences 2016, Dubai

(in partnership with The Journal of Developing Areas, Tennessee State University, USA)

ISBN 978-0-9925622-3-6

383

Laumas, GS 1989, ‘Anticipated Federal Budget Deficits, Monetary Policy and the Rate of Interest’, Southern

Economic Journal, vol.56, no.2 October, pp.375-82.

Levin A, Lin CF, & Chu C 2002, ‘Unit root tests in panel data: Asymptotic and finite-sample properties’,

Journal of Econometrics, Vol. 108, no.1, pp.1-24

Mukhtar, T & Zakaria, M 2008, ‘Budget deficits and interest rates: an empirical analysis for Pakistan’, Journal

of Economic Cooperation, vol. 29, no 2, pp.1-14.

Odionye, JC & Uma, KE 2013, ‘The Relationship between Budget Deficit and Interest Rate: Evidence from

Nigeria’, European Journal of Business and Social Sciences, vol.2, no.1, pp.158-167.

Ostrosky, AL 1990, ‘Federal Government Budget Deficits and Interest Rates: Comment’, Southern Economic

Journal, 56, 802-803.

Pandit, R 2005, ‘The Impact of Fiscal Deficit on Long-term Nominal Interest Rate in Nepal’, Economic Review,

Occasional Paper, vol.17.

Pesaran, M.H., (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of

Applied Econometrics, 27(2), 265-312.

Punam, CP, Korman, V, Angwafo, M & Buitano, M 2011, ‘An analysis of issues shaping Africa’s economic

future’, Africa’s Pulse Newsletter, 3, 81684.

Smith, V, Leybourne, S, Kim, TH, & Newbold, P 2004, ‘More Powerful Panel Unit Root Tests with an

Application to the Mean Reversion in Real Exchange Rates’ Journal of Applied Econometrics, vol.19,

no.2, P.14770