The Economy in the Environment – basic concepts The Holistic View.

77

The Economy in the Environment – basic concepts The Holistic View

-

date post

22-Dec-2015 -

Category

Documents

-

view

216 -

download

2

Transcript of The Economy in the Environment – basic concepts The Holistic View.

The Economy in the Environment – basic concepts

The Holistic View

The Cowboy Economy

• Circular flow between firms and consumers

• Seemingly perpetual• Success measured by

the amount of stuff moving through

• Reckless, romantic, not realistic

The Spaceship Economy• Expanding system

boundaries• Limited reservoir of

materials on earth• Economy uses inputs

from the environment and emits waste

• Must limit throughput• Limits to growth?

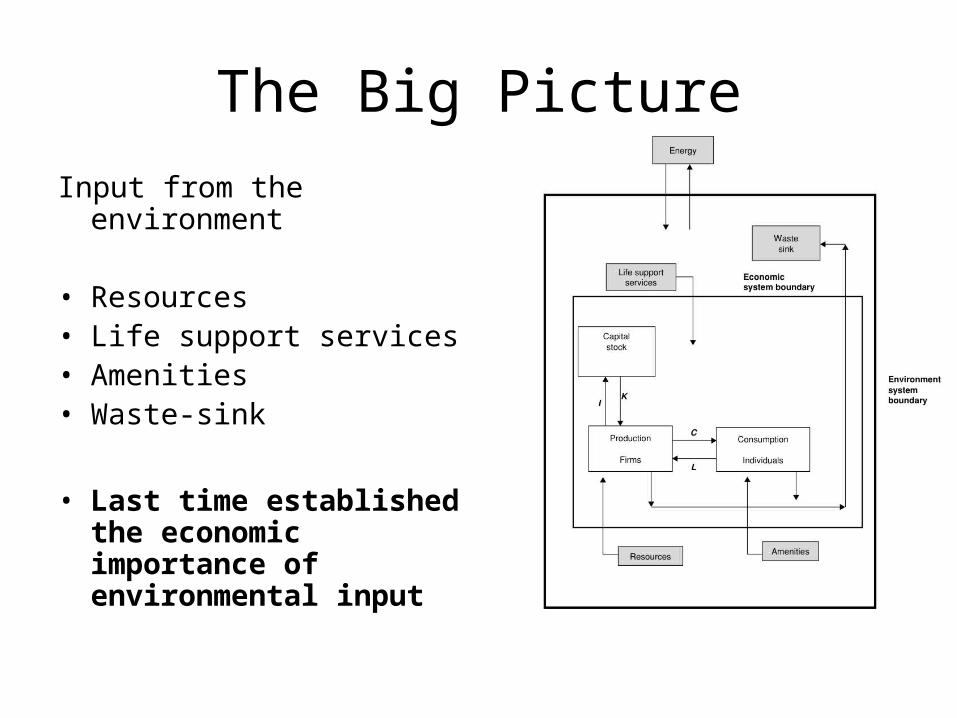

The Big Picture

Input from the environment

• Resources• Life support services• Amenities• Waste-sink

• Last time established the economic importance of environmental input

The Big Picture

• Continually trying:– Not to overwhelm regenerative capacity of the

environment– Not to overwhelm the waste-assimilative

capacity of the environment

First - a few concepts

• Thermodynamics• Matter = energy and materials

• Energy = ability to do work

• Entropy = unavailable bound energy - represents level of chaos or disarray. Can also measure the quality of energy.

First - a few concepts

• Systems: Two or more entities that interact

• Open system: Exchanges energy and materials with its surroundings

• Closed system: Exchanges only energy with its surroundings.

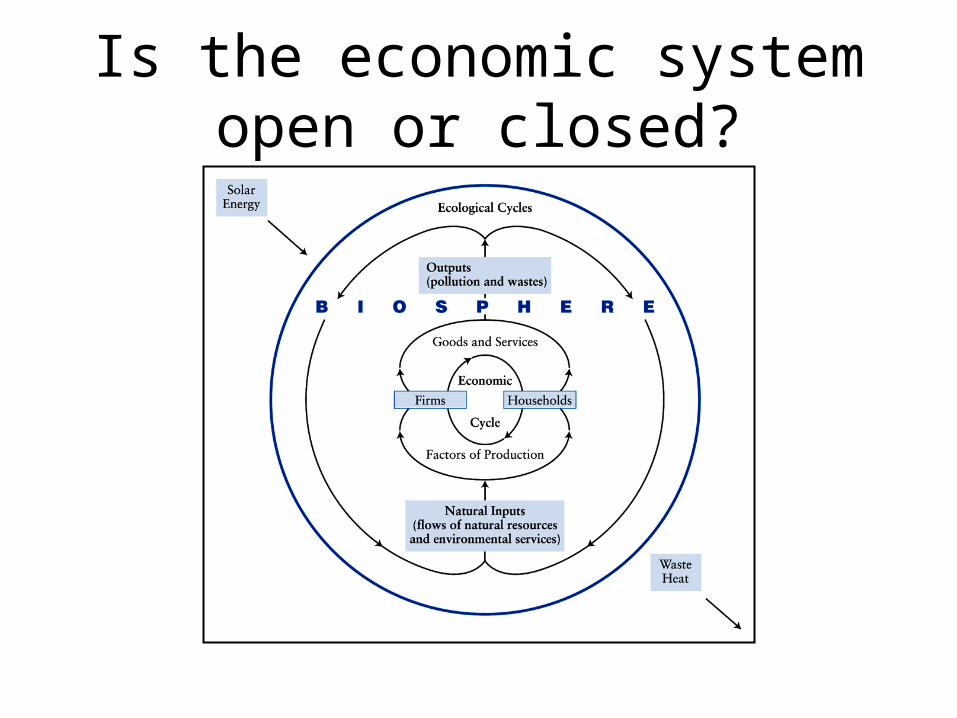

Is the earth open or closed?

Is the economic system open or closed?

Laws of Thermodynamics

The first law:

• Matter (energy or materials) can neither be created nor destroyed

Implications:

• Whatever comes in will come out (implies waste)

• Economic processes simply rearrange things

Laws of Thermodynamics

Second law:The entropy law• All processes require energy - and as they

do they reduce the quality of the energy used - increasing entropy in the universe

• The arrow of time: over time we always will see an increase in entropy

• Energy cannot be recycled - continually goes from a high quality state to a low quality state

Laws of thermodynamics

• Implications for the earth as a whole– A closed system, and thus

quantity of materials is constant

– Constant flux of energy into the system

– Energy cannot be recycled but materials can

– No process is 100% efficient

– Implications for economic systems?

Natural Capital

• Capital: A stock that yields a flow of goods and services into the future

• Natural capital: Those stocks in nature that provide goods and services into the future

• Example: A fish stock (capital) yields a flow of goods (harvested fish) into the future

Natural Capital

• Two types:– Renewable or active capital

• Providing extractable renewable resources, and provide services without being extracted (ex. Waste assimilation).

– Nonrenewable or passive capital• Inactive (passive). Provide no services until

extracted. Ex. Fossil fuels

– Perpetual resources - only provide flow services and have no stock counterpart

Stocks and flows

The Big Picture

• Resources: – Flow resources– Stock resources

• Nonrenewable• Renewable

Stock resources

• Non-renewable

• Depletable, scarce (if used)

• Resources vs. reserves– Economic feasibility

• Provide services only if extracted

Non-Renewable Resources

Non-Renewable Resources

• Rate of regeneration is slower than extraction

• St = St-1 + Gt - Et

Where:

Gt = 0

• Example: Fossil fuels - Others?

Economic theory of nonrenewable resources

• Describes the optimal extraction path for non-renewable resources– Hotelling principle

• By definition scarcity increases as extracted which should increase price– Has it?

Economics of non-renewable resources

• Optimal extraction rule: Extract such that rent rises at the rate of interest

• What happens if interest rates increase? Extract more? Less?

Economic theory of non-renewable resources

– Prices increase over time

– Extracted quantity declines over time

– Total size of the resource declines over time

– All true in reality?

Economic theory of non-renewable resources

• More realistic picture• U-shaped price path

– Technology– Scarcity– Shown by Slade 1982

Economic theory of non-renewable resources

• Is it possible to use non-renewable resources and be sustainable?

• Why/why not?

• If yes, how?

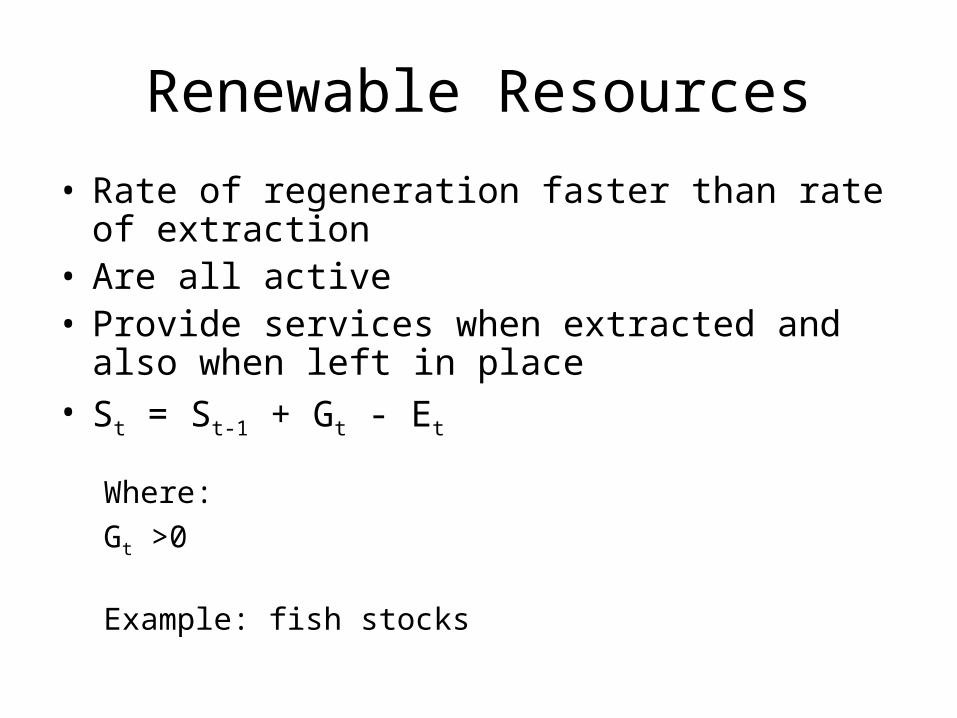

Renewable Resources

• Rate of regeneration faster than rate of extraction• Are all active• Provide services when extracted and also when

left in place• St = St-1 + Gt - Et

Where:

Gt >0

Example: fish stocks

Renewable resources - Population dynamics

• Population: a group of individuals belonging to the same species

• Population dynamics: The dynamics of population growth and how populations interact

• Crucial for the management of renewable resources

Renewable ResourcesPopulation growth

• Focus on G• Exponential growth• Characterizes

anything that can grow without limit

• Pt = Pt-1*(1+r)• Doubling time:

LogN2 =r*DT0.693 = r*DTDT = 70/r

Renewable ResourcesPopulation growth

• Logistic or density dependent growth

• Upper limit to the ultimate size

• Determined by carrying capacity– What defines CC?

• Growth curve u-shaped

Growth determined by:

Pt = Pt-1 + r*(CC - Pt-1)/CC

Renewable resources

Original Equation

• St = St-1 + Gt - Et

• Extraction affects stock size.

• Sustainable yield: extraction equal to growth

• G=E

Renewable resources

• Maximum sustainable yield (MSY)

• Complex dynamics - stock possibly grows drastically with decreased harvest

Renewable Resources

Equilibrium and stability

• Do populations ever reach an equilibrium?

• Are growth curves ever smooth?

• Can populations be stable without an equilibrium?

Renewable Resources

• A) Dampened oscillations - falling amplitude

• B) Constant oscillations - constant amplitude

• C) Exploding oscillations - increasing amplitude - collapse

Renewable resources

Population interactions

• No species lives in isolation

• Predator prey (Lotka Volterra)

• Competition

• Symbiosis

Renewable resources

• Resiliency - ability of a system to bounch back after a disturbance

• What determines resiliency?– Diversity?– Keystone species?

• The rivets analogy

The Big Picture

• Waste: definition

“Unwanted” byproducts of economic activity

• Conservation of matter - always waste into the environment

Waste

• Accumulation of waste

• St = St-1 + W - D– W: inflow– D: assimilation

• Function of S

• D = d*S

• With d from 0-1

• Recycling or reuse possible, intercepts flow

• Industrial symbiosis

Waste

Damage relationships• Biomagnification

– Increasing concentration as going up food-chain

– DDT

• Synergy: Two pollutants interact and create something worse - e.g. smog

Waste

Damage relationships• Dose response

curves– Relationship between

exposure and damage

• Thresholds• Lagged response

Amenity services

• Pleasure of going to a park

• Pleasure to run in a forest

• Simply knowing that nature exists

Amenity services

• Sustainable amenity service

• Relationship between the quality of the service and the number of visitors

Life Support Services

• Services that make human life possible– Purification of air and

water– Stabilization and

moderation of climate– Nutrient cycling– Pollination of plants

Interactions

• Various services interact e.g.– Inflow of fossil fuels

creates an outflow of carbon

– Increasing temperatures, affecting other services

Summary

• Various services received from nature

• Valuable (33 trillion $)

• Very complex dynamics– Non-linear movements– Lags– Thresholds– Interactions

• Creates massive Uncertainty

Threats to Sustainability

• Resource depletion• Waste accumulation• Loss of resiliency

• What to do?• Why those threats?

Classical causes of Environmental degradation!

Markets and efficiency

• Market:

• Is a system in which buyers and sellers of something interact.

• Something is exchanged in return for money

• Illustrates individual preferences

Demand and Supply

Demand function:• Describes the relationship

between the quantity the buyers buy and price of the product

• Inverse relationship• Qd = 30 - 6P • Maximum price – choke

price• Usually not linear

Elasticity

• Describes how quantity changes as price changes.

1=elastic

0=inelastic

Elasticity

• Elasticity of demand (Ed)• Elasticity of supply• Cross elasticity of demand or supply• Income elasticity (IE)

• Inferior goods (IE negative, Ed negative)• Normal goods (IE positive, Ed negative)• Luxury goods (IE positive, Ed positive)

Supply function

• Describes the relationship between the quantity that sellers are ready to sell and price

• Upward sloping

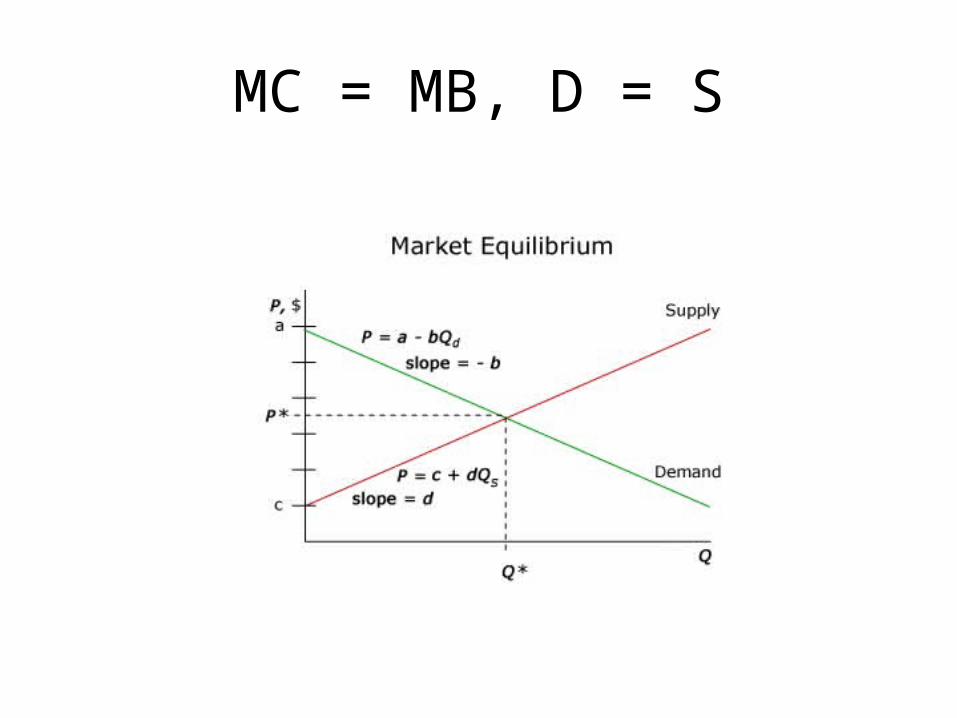

Market equilibrium

• Bringing together buyers and sellers

• At the market equilibrium D=S, and giving the market price

• Illustrates efficient allocation of resources

Markets and Efficiency

• Economics: Allocation by economic agents of scarce resources among alternative competing ends.

• Three questions:– What ends to economic agents desire

• (what to produce and how much)

– What limited scarce resources do economic agents need to attain those ends

• How to produce this?

– What ends do get priority and how to share this among society

Welfare economics

Answer: Maximize utility

Utility

• What people want, and the benefit from getting it, expressed via preferences

• Increases via ever increasing provision of goods and services

Maximum utility = maximum social welfare

Preferences

• Expressed through the market by what goods and services people are willing to give up (read money) to get sth else

• Willingness to pay

Allocative Efficiency

• Adam Smith – Invisible hand

• First theorem of welfare economics– Pareto efficient allocation (optimality)

• Efficient allocation when noone can be made better of at the cost of others

• Noone can gain at the cost of others+• Only holds under “perfect markets”

Conditions for efficient allocation (“perfect markets”)

• Competitive market– Price takers

• Rational behavior

• Full information

• Full inclusion

• Marginal benefit (MB) = marginal cost (MC)

MC = MB, D = S

Market failure

• When allocative efficiency is not achieved• Conditions for a perfect market:

– Full (complete) inclusion of all goods and services (all traded in markets), nothing external

– Full (complete) information– Rational behavior– Competitive markets (price takers)– Property rights allocated – consumer sovereignty

Public goods

• Public vs private goods• Public goods: Used collectively by society• Pure PG are non-rivalrous and non-excludable

(pure vs. impure)– Non-rivalrous: consumption by one does not affect

consumption by another• Crowding

– Non-excludable: agent cannot be prevented from consuming and using it

– Market does not handle allocation of such goods

Management concepts

• Open access

• Private property– Exclusive – Functional ownership

• Common property – “the commons”

Externalities

• Externality– The unintended and uncompensated side-

effects of one agents activities on another– Beneficial, or harmful

• Positive externality (beneficial)– Ex. Orchards and the bee farmer

• Negative externality (harmful)– Ex. Pollution affects a surrounding community

Internalizing Externalities

How to intervene to ensure effective allocation?

• Coase theorem– Private property rights– Issues

• High transaction costs• Number of agents

• Intervention– Piguvian taxes (e.g.)– Subsidies

Application of the Coase Theorem

External costs in the Automobile industry

External costs with tax

Enter the Environment

• Nature/natural services– Non-market good

• Rarely enter welfare functions, often excluded from economic decision-making

• Services received free of charge

– External to the market• Provide positive externalities• Affected by negative externalities

– Property rights hard to define• Many cases considered public goods

Classical Causes of Environmental Degradation

• Exclusion of the environment indicates market failure– Markets cannot allocate the environment

efficiently– Agents (that operate based on price), do not

have the means to allocate this resource effectively

• Result: We overuse natural capital, extract too much and emit too much waste

Tragedy of the Commons

• A group of herdsmen that all have to use common grazing lands. That is the grazing lands are all used in common and are the resource in question.

• The herdsmen must use the grazing-lands to fatten their cattle - and thus they want to keep as many cattle on the grazing lands as possible.

• Grazing lands are a renewable resource = overuse means degradation.

Tragedy of the Commons

• Assume:– Profit maximization

• Based on weight of each cattle times N

– Rational behavior• Maximize profits, (minimize cost)

Tragedy of the Commons

• Profits = P*Q• Costs = C*Q/N

• Profits private• Costs are shared by all

=> More cattle added until Commons are ruined

Tragedy of the Commons

• Can “Commons” Management ever work?– Strength of norm

• Technology• Prices• Outsiders

What to do?

• Get the market to internalize the environment

• When?– In the presence of market failure

• How?– Property rights– Market intervention

• Policy

Sustainability = efficient markets?

• Correcting market failure does not guarantee sustainability

• Intergenerational equity

• Exclusion of “non-productive” natural capital

• Neoclassical perspective vs. Sustainability perspective

The Economy and the Environment

• Economic Planner – maximize economic utility, economic growth, income

• Environment excluded from framework

• Relationship between the environment and income e.g.the EKC (later)

• But, what is economic growth? (next time)

Next time

What is economic growth?