The Economics of Corporate Securities Fraud · The Economics of Corporate Securities ... Corporate...

31

The Economics of Corporate Securities Fraud CES Lecture 1 Tracy Wang April, 2013

-

Upload

nguyencong -

Category

Documents

-

view

222 -

download

3

Transcript of The Economics of Corporate Securities Fraud · The Economics of Corporate Securities ... Corporate...

The Economics of Corporate Securities Fraud

CES Lecture 1

Tracy Wang

April, 2013

Outline

• Lecture 1: Conceptual and empirical foundation for understanding corporate securities fraud

• Lecture 2: Determinants of corporate fraud incentive and implications for securities market regulation

• Lecture 3: Consequences of fraud and securities market regulation

Outline of Lecture 1

• Information asymmetry and institutional design in securities market

• The economics approach to corporate fraud

• The empirical framework for analyzing fraud

Corporate Securities

• What is a corporate security?

– It is essentially a claim on the corporation’s future cash flows.

• What is the value of a security?

– It is the expected discounted future cash flows entitled to the security owner.

– Information to form sensible expectation.

– Information to assess risk in order to set a reasonable discount rate.

Corporate Securities Market

Issuer Underwriter

(financial intermediary)

Primary market

investors

Securities and Exchange Commission (regulator)

Corporate Securities Market

• Why do we need the underwriter and the SEC in the middle?

• Information asymmetry---the seller knows more about the goods than the buyer – The “lemons” problem

– Particularly severe in the securities market

– Can the seller credibly certify the quality of its own securities?

– Certification of reputable intermediaries and oversight of regulators

Akerlof’s Lemons Problem • Consider a stylized market for used cars in which two equally likely

types of cars exist:

Car Type Full Information Value

Good $3,000

Lemon $1,000

• Assume that the used car owners have the full information about their cars, but potential buyers can not discern car types. How much are buyers willing to pay (fair market value)?

• Less information buyers have relative to sellers, ____ the market valuation of products

• Suppose that car owners have the option to sell or to hold onto their cars. What will happen to the market for used cars?

• What can a reputable specialized used car dealer do to this market?

Akerlof’s Lemons Problem

• Consequences of information asymmetry:

– Undervaluation

– Market dominated by low-quality products

– Market breakdown, no trade

• Will voluntary information disclosure by the issuer help resolve the information problem?

– Credibility

• Will investors freely offer to pay what they think the firm is worth?

– Undervaluation as a protection from information risk

• Think about the role of the SEC and the underwriter

9

Akerlof’s Lemons Problem

The Role of the SEC

• Securities Act of 1933 mandates the registration of public securities

– The issuer files a registration statement with the SEC

• Audited financial statements

• A complete description of business: projects, prospects, possible risks, etc.

• Purpose of registration

– The same document goes to investors as prospectus

• The role of the law and the SEC in mitigating the information problem

– Mandatory disclosure vs. voluntary disclosure

– Threat of litigation against fraud 10

11

Sample Prospectus/Registration Statement: FaceBook 2012

Table of Contents: 1. Prospectus summary 2. Risk factors (24 pages of discussion) --- If we fail to retain existing users or add new users…. --- Majority of revenue comes from advertising. The loss of advertisers... --- Ability to monetize in mobile products is unproven…

3. Special note regarding forward-looking statements and industry data 4. Use of proceeds 5. Dividend policy 6. Principal stockholders 7. Selected Consolidated financial data 8. Management’s discussion and analysis of financial condition and results of operations 9. Management & executive compensation 10. Related party transactions 11. Letter from the CEO

The Role of Financial Intermediaries

• Certify the quality of the issuer’s securities

– Reputation on the table

• Help generate information

– About the securities for potential investors

– About the market demand for the issuer

– During the underwriting process and after securities are issued (analyst coverage).

• Set the price of the security to clear the market

– It is the underwriter, not the issuer, who sets the value

13

In 2004, Google used Dutch auction to sell shares “directly” to investors. In 2011, Facebook considered going Dutch as well. In history, fewer than 30 companies went public using the Dutch auction mechanism. Why? Because for Dutch auction to work, the company needs to be very well known, highly regarded by regular investors, and solidly profitable. Most companies, however, need to be “sold” by underwriters.

The Role of Financial Intermediaries

Corporate Securities Market • Information asymmetry is the most important issue in

financial markets.

• A healthy and vibrant financial market requires a continuous flow of high quality information. – Relevant, truthful

• The entire institutional design in the securities markets centers around the infor. asymmetry problem. – SEC: protect outside investors and minority investors – Financial intermediaries: facilitate infor. exchange

• Greece’s sovereign debt

Corporate Securities Fraud

• Do firms’ insiders have incentive to withhold relevant information to outsider investors?

– Mandatory and periodical information disclosure

• Do firms’ insiders always have incentive to truthfully disclose relevant information?

• Securities fraud: intentional misreporting of material financial information

Corporate Securities Fraud • The “psycho” approach to crime (including white-

collar crime) – Crimes cannot result from rational behavior

• The “ethics” approach to crime – Intrinsic cost of engaging in illegal behavior

• The “economics” approach to crime – People are utility maximizers and thus respond to

economic incentives (economic benefits and costs). – People are forward looking. They try their best to

anticipate the uncertain consequences of their actions.

Corporate Securities Fraud • The different approaches are not mutually

exclusive. – The preference in the utility function can be broad

– Heterogeneous preferences

• Gibson et al. “Preferences for truthfulness: Heterogeneity among and within individuals” (AER forthcoming) – When there is an economic cost for telling the truth

and no economic cost for lying, 32% of participants choose to tell the truth.

– Participants’ incentive to tell the truth does respond significantly to varying economic cost of truth-telling.

Gary Becker’s Work

• Many decisions in life can reflect rational economic decision making.

– Illegal behaviors and crimes

– Investment in human capital: education, accumulation of skills and knowledge.

– Family: marriage, divorce, child care, relations among family members

– Discrimination against minorities

Economics of Securities Fraud

Decision to commit fraud

Economic benefits

Economic costs

Prob. of being detected

Penalty upon detection

Benefits from Fraud

• Managers’ personal benefit – Compensation

– Job security

• Benefit for current shareholders (at the cost of other investors) – Getting financing at better terms

– Acquisition using overvalued equity

– Selling overvalued securities

– Gaining competitive advantages in the product market

Cost of Committing Fraud

• Deterrence of detection

– Do fraud committers respond more to an increase in the prob. of detection or to an increase in the penalty upon detection?

– Implication for the utility function of fraud committers.

– Implication for optimal provision of deterrence.

Cost of Committing Fraud

• Costs to the private parties upon detection – Managers: being fired, reputation loss, monetary

penalty, jail terms – Investors: loss of security value, loss of future cash

flow, monetary penalty paid by the firm – Investors: resources used up to commit fraud, to

conceal fraud, and to clean up after detection (real operations may be distorted)

• Costs to the society – Negative externalities: fraud is not just a wealth

transfer

Empirical Framework

• Challenge: Partial observability of fraud

– We only observe frauds that are committed and later detected

– Shared by other white-collar crimes: tax evasion, corruption and bribery, etc.

Empirical Framework

Do not commit fraud

Commit fraud

Not detected

Detected

P(F)

1-P(F)

P(D|F)

1-P(D|F)

Prob.(Detected Fraud) = Prob.(Fraud Commission)*Prob.(Detection | Commission)

Observed

Empirical Framework

• Since the fraud detection process is not perfect, the probability of detected fraud can substantially underestimate the probability of fraud. • The realized probability of detected financial fraud is

only about 4%.

• Equating P(F*D) to P(F) can lead to incorrect assessment of corporate or public policies that are designed to combat fraud.

• Need to separate P(F) from P(D|F) in order to examine the deterrence of detection.

Empirical Framework • Wang (JLEO, 2011):

– Fraud commitment:

– Fraud detection:

– Detected fraud:

– The error terms u and v are assumed to follow a bivariate normal distribution.

26

iii

iiiDi

iiiFi

DFZ

DvxD

FuxF

,

*

,

*

Unobserved

Observed

).,,(10,1)0,0()0()0(

);,,(1,1)1()1(

,,0

,,

iDiFiiiiii

iDiFiiiii

xxDFPDFPDFPZP

xxDFPDFPZP

Ni

iDiFiiDiFi

z

i

z

i

xxzxxz

ZPZPLii

,..,1

,,,,

01

),,(1ln1),,(ln

0log1log),,(

Identification • The F* and D* equations cannot have exactly the same

set of explanatory variables. – Anticipatable detection risk: Deterrence of detection

• some variables that affect detection risk (and can be anticipated) should also affect incentive to commit fraud, in the opposite direction.

– Unanticipatable detection risk: Detection occurs after the commission of fraud. • There are factors that affect detection ex post but cannot be

anticipated at time of fraud commission

• The explanatory variables exhibit adequate variation in the sample – Continuous variables are better than indicator variables.

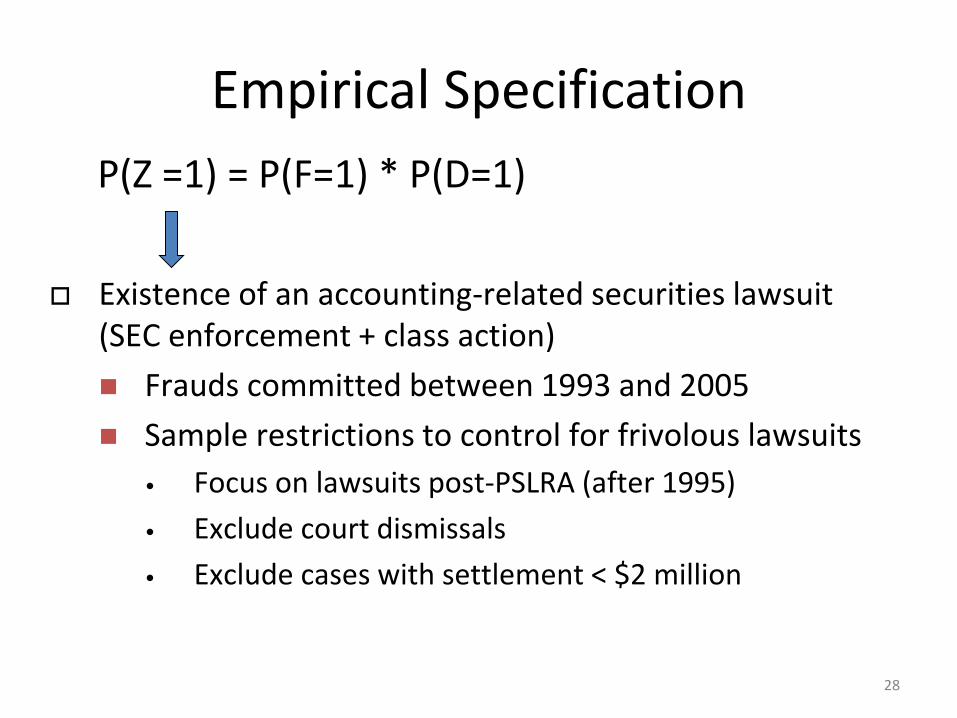

Empirical Specification

P(Z =1) = P(F=1) * P(D=1)

28

Existence of an accounting-related securities lawsuit (SEC enforcement + class action)

Frauds committed between 1993 and 2005

Sample restrictions to control for frivolous lawsuits

• Focus on lawsuits post-PSLRA (after 1995)

• Exclude court dismissals

• Exclude cases with settlement < $2 million

P(Z =1) = P(F=1) * P(D=1)

29

Industry boom/bust

Profitability

External financing need

Leverage

Insider equity incentives

Firm investment

Institutional monitoring

Firm size, age, sector

Firm investment

Institutional monitoring

Firm size, age, sector

Abnormal industry litigation

Unexpected performance shock

Abnormal return volatility

Abnormal stock turnover

Deterrence of detection; Ex-ante detection risk, may deter fraud.

Key identification condition: detection occurs after fraud commitment; Ex-post detection risk, cannot be anticipated at time of fraud commission.