The economics of airline financial performance and wider ...

23

The economics of airline financial performance and wider economic benefits 6 th April 2018, Paris Brian Pearce, Chief Economist, IATA www.iata.org/economics

Transcript of The economics of airline financial performance and wider ...

The economics of airline

financial performance

and wider economic

benefits

6th April 2018, Paris

Brian Pearce,

Chief Economist, IATA

www.iata.org/economics

Outline

• Why is the airline industry suddenly profitable?

• After decades of investor capital destruction

• Is the change widespread?

• Have the underlying economics of the industry changed?

• Why is the emergence of protectionism such a threat?

• How does air transport bring economic benefit?

• Users

• Wider economic benefits• Come from the people, goods, capital and ideas we carry between cities

• Rather than the jobs required to run the service (with some exceptions)

Airlines have suddenly become profitable (for their equity investors)

Source: IATA Economics using data from McKinsey, The Airlines Analyst, IATA forecasts

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

% o

f in

vest

ed c

apit

alReturn on capital invested in airlines and their cost of capital

Cost of capital (WACC)

Return on capital (ROIC)

After decades of investor value destruction

Source: IATA Economics using data from McKinsey, The Airlines Analyst, IATA forecasts

-40

-30

-20

-10

0

10

20

30

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

US$

bill

ion

Difference between investing in airlines and investing in similar assets elsewhere

And widespread airline failures

Source: HSBC report – early 2014 situation. Since then Monarch and airberlin have failed

European LCCs

Planet

duo

nexus

Air Wales

ThomsonflyNordic

airlink

flyforbeans.com

clickair

Atlas-blue

myair

flyglobespan

GoDebonair

mytravellite

dba

Basiqair

jetmagic

Iceland Express

AerArann

Aerlingus

Ryanair

Monarch

easyJetflybe Transavia

Eurowingsairberlin

WIZZ

Voloteavueling

SkyExpress

Norwegian

Pegasus

Jet2

snowflake

flyecoSkyeurope

Hamburg airlines

Helvetic

VBIRDVirginExpress

EUjet

FlyMe

buzz

Volareweb

Maersk Air

Air Finland

Flying Finn

Kiss

GetJet

Aeris

Smart Wings

centralwings

fly gibraltar

HLXLTU

Air polonia

flybaboo

flywest

Viking

SterlingCimber

Air Turquoise

Germania

air lib express

Clickair

WindJet

Failed Survived

But improvement has been very uneven across the industry

Source: IATA Economics using data from IATA and The Airline Analyst

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015 2016

EBIT

ad

just

ed f

or

op

erat

ing

leas

es a

s %

inve

sted

cap

ital

Return on invested capital

Industry average

North America

Europe

Asia PacificLatin America

Middle East

Weighted Average Cost of Capital

Balance sheet remain highly leveraged in some regions

Source: IATA Economics using data from The Airline Analyst

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016

Deb

t ad

just

ed f

or

op

erat

ing

leas

es/E

BIT

DA

RAdjusted net debt/EBITDAR

Latin America

Asia Pacific

Industry average

Europe

North America

Middle East

Investment grade

There has always been a paradox at the heart of air transport

Source: McKinsey presentation to IATA

2015-18: 9.7%

Technology continues to cut costs dramatically

Source: Lee

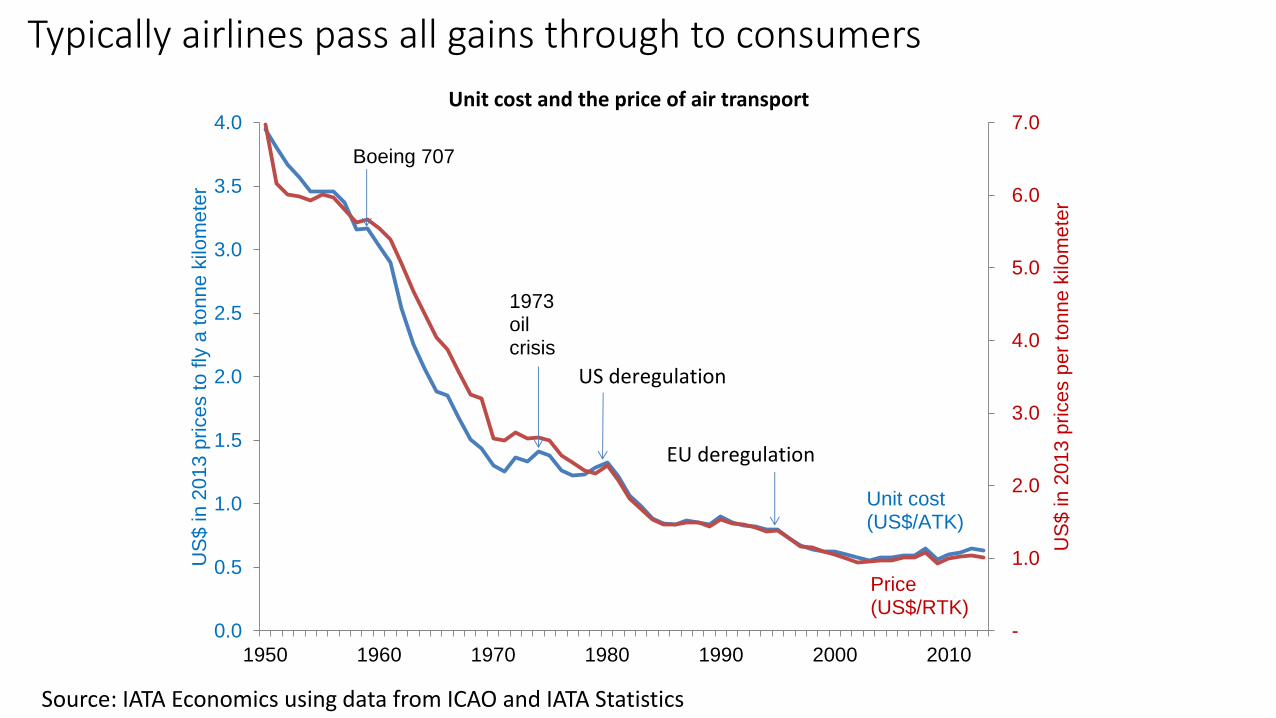

Typically airlines pass all gains through to consumers

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1950 1960 1970 1980 1990 2000 2010

US

$ in

20

13

price

s p

er

ton

ne

kilo

me

ter

US

$ in

20

13

price

s t

o f

ly a

to

nn

e k

ilom

ete

r

Unit cost and the price of air transport

Price(US$/RTK)

Unit cost(US$/ATK)

US deregulation

EU deregulation

Boeing 707

1973 oil crisis

Source: IATA Economics using data from ICAO and IATA Statistics

In fact prices have fallen further than costs forcing up breakeven loads

45%

50%

55%

60%

65%

70%

1970 1975 1980 1985 1990 1995 2000 2005 2010

% A

TK

s

Breakeven and actual load factors

Breakeven load factor

Load factor achieved

+15%points

Source: IATA Economics using data from ICAO and IATA Statistics

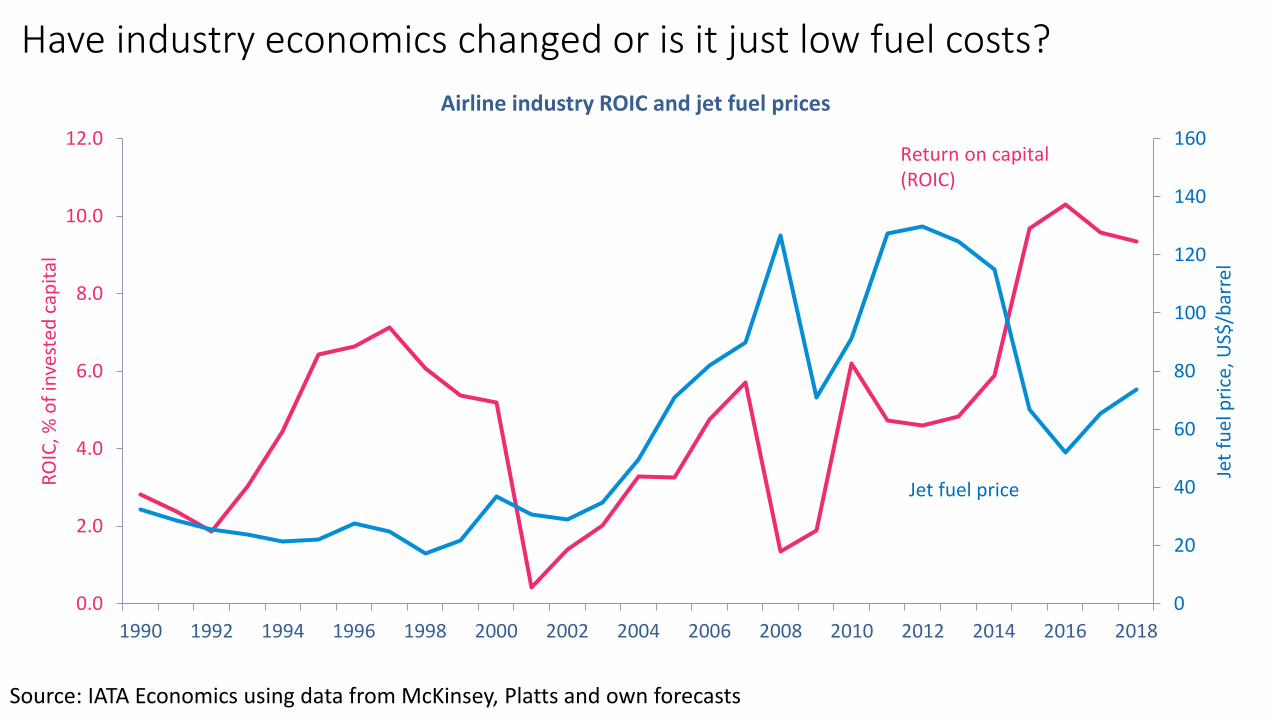

Have industry economics changed or is it just low fuel costs?

0

20

40

60

80

100

120

140

160

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Jet

fuel

pri

ce, U

S$/b

arre

l

RO

IC, %

of

inve

sted

cap

ital

Airline industry ROIC and jet fuel prices

Return on capital (ROIC)

Jet fuel price

Source: IATA Economics using data from McKinsey, Platts and own forecasts

The underlying economics of air transport

• Perishable

• Fixed costs high

• Barriers to entry low

• Competitive advantages hard to defend

• Aircraft are a platform to serve many markets

• Economies of scale in aircraft size but business travelers want frequency and flexibility

• Few scale economies in fleet size but economies of density in networks

OUTCOME:

• Prices pushed down towards variable costs,

• But ways need to be found to cover fixed costs:• Differential pricing, sequential use of coupons, non-refundable tickets….and now ancillaries

• Network density economies through merger prevented by bilateral and O&C regulation barriers:• Leading to code shares, alliances and now ATI JVs and equity partnerships on international markets

Improvement in performance pre-dates fall in fuel costs

Source: IATA Economics using data from ICAO, IATA Statistics, IATA forecasts

55

57

59

61

63

65

67

69

71

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

% A

TKs

Breakeven and achieved weight load factors

Load factor achieved

Breakeven load factor

Airlines are sweating assets as well as improving margins

Source: IATA Economics using data from ICAO, McKinsey, The Airline Analyst, IATA forecasts

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Cap

ital

pro

du

ctiv

ity,

rev

enu

e/in

vest

ed c

apit

al, U

S$

Op

erat

ing

mar

gin

, % r

even

ue

Components of return on capital

Capital productivity

Operating margin

Wide variety of successful business models

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.00 0.50 1.00 1.50 2.00 2.50

EBIT

mar

gin

, ad

just

ed E

BIT

/rev

enu

e

Capital productivity ($ revenue per $ invested capital)

2015 ROIC = adjusted EBIT/revenue * revenue/invested capital

WALMART

PFIZER

Allegiant

Lufthansa

Easyjet

Southwest

Alaska

Spirit

Ryanair

Jazeera

Delta

IAG

AF-KLM

Hawaiian

AMR JAL

Qantas

United

Thai

Volaris

Mesa

Spring

Air CanadaPIA

GOLKorean

SIA

Air China

Cathay

Aeromexico

JetBlue

LATAMANA

Increasing return on capital (ROIC)

Comair

Source: IATA using data from The Airline Analyst IATA Economics www.iata.org/economics

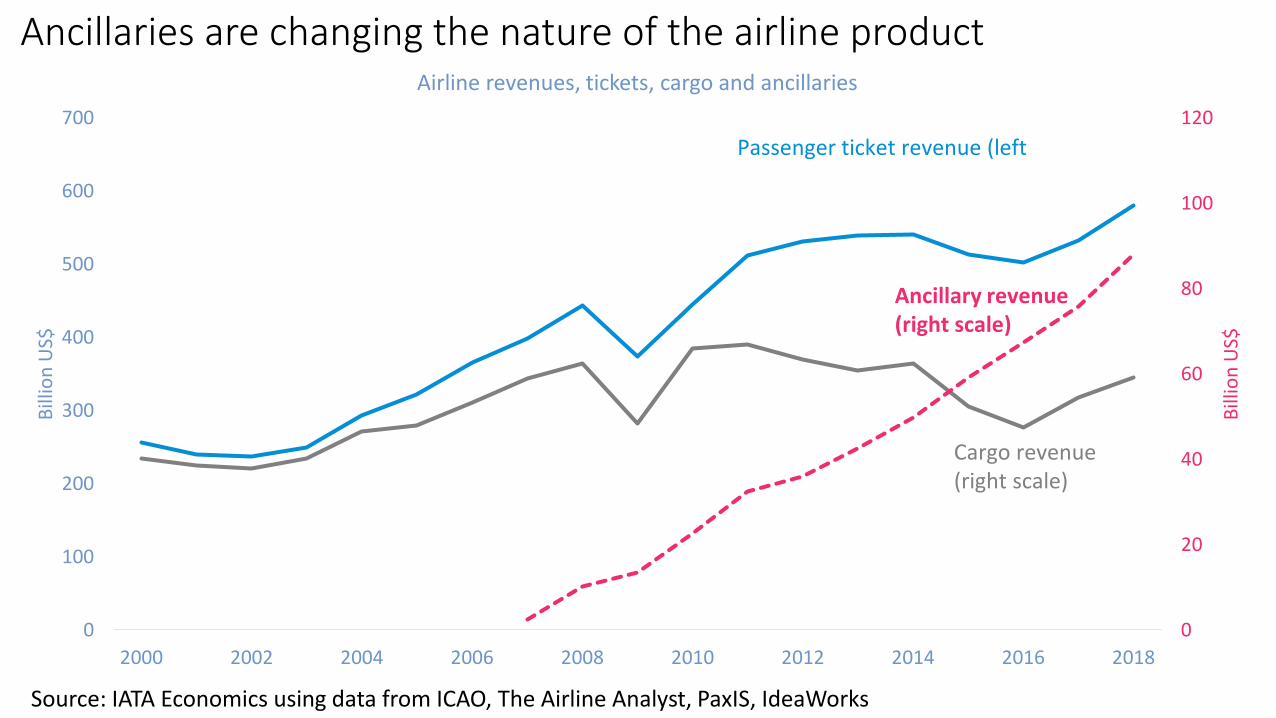

Ancillaries are changing the nature of the airline product

Source: IATA Economics using data from ICAO, The Airline Analyst, PaxIS, IdeaWorks

0

20

40

60

80

100

120

0

100

200

300

400

500

600

700

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Bill

ion

US$

Bill

ion

US$

Airline revenues, tickets, cargo and ancillaries

Passenger ticket revenue (left

Cargo revenue (right scale)

Ancillary revenue (right scale)

Consolidation important but not simply because of size

Source: IATA Economics using data from IATA and The Airline Analyst

-

5

10

15

20

25

30

35

40

45

-10% 0% 10% 20% 30% 40% 50%

Inve

sted

cap

ital

, $ b

illio

n

Return on invested capital, %

Return on invested capital versus invested capital, 2016

American

United

Delta

Allegiant

Air ChinaChina SouthernChina Eastern

Lufthansa

FedexSouthwest

IAGRyanair

AlaskaIcelandic

Korean Turkish

CathaySingapore

AF-KLMLATAM

Emirates (2015)

Qatar (2015)

JVs doing better job than code shares/alliances to get density economies

Source: Lufthansa

Protectionism (or the new ‘localism’) is a major threat

10

12

14

16

18

20

22

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

% o

f G

DP

Share of goods trade (exports+imports) in global GDP

Global financial

crisis

Source: IATA Economics using data from Netherlands CPB

Benefits to consumers (and economy) arise from cheap city connections

Source: IATA Economics using data from ICAO, Boeing, OAG, SRS Analyser

0.50

1.00

1.50

2.00

2.50

3.00

3.50

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

22000

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

US$

/RTK

in 2

01

4U

S$

Nu

mb

er o

f u

niq

ue

city

-pai

rs

Unique city-pairs and real transport costs

Unique city pairs

Real cost of air transport

Wider economic benefits

• Often measured by the jobs and GVA in the supply chain, through I-O models• Economic footprint is a useful description

• But it measures cost not benefit• Do labor productivity gains really mean lower wider economic benefits?

• Economic benefits generated by connecting cities at lower cost• Air transport network is an infrastructure asset, a bridge between cities

• Boosting the productive capacity of an economy

• Generating flows of people, goods, capital, ideas, competitive pressure

• Raising productivity through agglomeration, gains from trade

• Higher GDP from the supply-side, in economies close to full capacity

• Demand-side/spending flows do matter where economies/regions under-developed

• More research and evidence required!