THE DESIGN AND ADOPTION OF GREEN BANKING … FOR ENVIRONMENT PROTECTION: LESSONS FROM BANGLADESH ......

19

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016 1 THE DESIGN AND ADOPTION OF GREEN BANKING FRAMEWORK FOR ENVIRONMENT PROTECTION: LESSONS FROM BANGLADESH S M Mahfuzur Rahman & Suborna Barua Department of International Business, University of Dhaka, Bangladesh ABSTRACT Bangladesh Bank, the central bank of Bangladesh and a forerunner in pursuing environment-friendly banking, designed a structured three-phase Green Banking Guideline and instructed the scheduled banks to implement it by 2013. This paper aims to present a comprehensive picture about where the country stands in terms of adopting green banking practices. Examining 42 of total 54 scheduled banks of Bangladesh, the study finds that most banks are trapped in the lower boundaries of the performance greed. The state owned banks rank low in performance while the foreign banks have considerably better achievements. The paper also identifies a number of reasons for the banks‟ poor performance and proposes corrective measures. The lessons may be useful for redesigning banking practices around the world to save environment. JEL Code: E5, G2, G18, Q56 Key Words: Environment-friendly Banking, Sustainable Business Strategy, Green Finance, Climate Change, Sustainable Development, Social Responsibility. Corresponding Author’s Email Address: [email protected] INTRODUCTION Global warming and climate change are now having direct impact on biodiversity, agriculture, forestry, dry land, water resources and human health. Bangladesh is one of the most vulnerable countries facing the impacts of climate change and therefore, has the concern in environmental degradation. The country recognizes the fact that the role of the banking sector is very crucial in growth and development activities and therefore, the banks must come forward to play more effective role in mitigating the environmental degradation. Bangladesh Bank has taken the role of a leader in initiating green banking and it is expected that green banking would be a major instrument through which banks can substantially contribute to serve the purpose. As banks comprise major source of finance to the industrial sector, they need to scrutinize that their financing is not used in or does not lead to any activity that cause environmental damage. Green banking requires that financial and business policies are not hazardous to environment and that the banks help to protect environment. Bangladesh Bank has come up as a pioneer in promoting the idea of green banking and has developed a three-phase Green Banking Policy Framework in 2011 (BRPD Circular No.02 dated 27 February 2011) and instructed all scheduled commercial banks of the country to implement the policies in the time period from 2011 to 2013 (Bangladesh Bank, 2011). The phasing of implementation of the 19 policies included in the Green Banking Framework is: Phase I – Policy 1.1 to 1.9 (by 31 December 2011), Phase II – Policy 2.1 to 2.7 (by 31 December 2012) and Phase III – Policy 3.1, 3.2 and 4.0 (by 31 December 2013). However, the experience from on-site and off-site supervision of Bangladesh Bank shows that banks scheduled before 2013 will require more time for implementing Green Banking Policy and therefore time frame for 47 banks (scheduled before 2013) for implementation of green banking activities under Phase-II and Phase-III has been extended to 31 December 2014 and 30 June 2015 respectively (GBCSRD Circular No. 08, 24 December 2013). Based on these circumstances, it has now become relevant to study on how the banks have performed in accomplishing the tasks. As of now, two studies, in the book - “Green Banking in Bangladesh; Environmental Risk Management in Banking” edited by Chowdhury and Habib (2014) and published by Bangladesh Institute of Bank Management (BIBM), examined the status and impact of green banking initiatives of Bangladesh Bank. Both these studies appear to present a partial scenario. In reference to the existing literatures, the current study is more comprehensive and expected to generate new findings through: (i) covering whole three years of given timeframe, (ii) studying larger number of sample banks, (iii) applying more robust parameters and measurement approach for

Transcript of THE DESIGN AND ADOPTION OF GREEN BANKING … FOR ENVIRONMENT PROTECTION: LESSONS FROM BANGLADESH ......

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

1

THE DESIGN AND ADOPTION OF GREEN BANKING

FRAMEWORK FOR ENVIRONMENT PROTECTION:

LESSONS FROM BANGLADESH

S M Mahfuzur Rahman & Suborna Barua

Department of International Business, University of Dhaka, Bangladesh

ABSTRACT

Bangladesh Bank, the central bank of Bangladesh and a forerunner in pursuing environment-friendly banking,

designed a structured three-phase Green Banking Guideline and instructed the scheduled banks to implement it by

2013. This paper aims to present a comprehensive picture about where the country stands in terms of adopting green

banking practices. Examining 42 of total 54 scheduled banks of Bangladesh, the study finds that most banks are

trapped in the lower boundaries of the performance greed. The state owned banks rank low in performance while the

foreign banks have considerably better achievements. The paper also identifies a number of reasons for the banks‟

poor performance and proposes corrective measures. The lessons may be useful for redesigning banking practices

around the world to save environment.

JEL Code: E5, G2, G18, Q56

Key Words: Environment-friendly Banking, Sustainable Business Strategy, Green Finance, Climate Change,

Sustainable Development, Social Responsibility.

Corresponding Author’s Email Address: [email protected]

INTRODUCTION

Global warming and climate change are now having direct impact on biodiversity, agriculture, forestry, dry land,

water resources and human health. Bangladesh is one of the most vulnerable countries facing the impacts of climate

change and therefore, has the concern in environmental degradation. The country recognizes the fact that the role of

the banking sector is very crucial in growth and development activities and therefore, the banks must come forward

to play more effective role in mitigating the environmental degradation. Bangladesh Bank has taken the role of a

leader in initiating green banking and it is expected that green banking would be a major instrument through which

banks can substantially contribute to serve the purpose. As banks comprise major source of finance to the industrial

sector, they need to scrutinize that their financing is not used in or does not lead to any activity that cause

environmental damage. Green banking requires that financial and business policies are not hazardous to

environment and that the banks help to protect environment.

Bangladesh Bank has come up as a pioneer in promoting the idea of green banking and has developed a

three-phase Green Banking Policy Framework in 2011 (BRPD Circular No.02 dated 27 February 2011) and

instructed all scheduled commercial banks of the country to implement the policies in the time period from 2011 to

2013 (Bangladesh Bank, 2011). The phasing of implementation of the 19 policies included in the Green Banking

Framework is: Phase I – Policy 1.1 to 1.9 (by 31 December 2011), Phase II – Policy 2.1 to 2.7 (by 31 December

2012) and Phase III – Policy 3.1, 3.2 and 4.0 (by 31 December 2013). However, the experience from on-site and

off-site supervision of Bangladesh Bank shows that banks scheduled before 2013 will require more time for

implementing Green Banking Policy and therefore time frame for 47 banks (scheduled before 2013) for

implementation of green banking activities under Phase-II and Phase-III has been extended to 31 December 2014

and 30 June 2015 respectively (GBCSRD Circular No. 08, 24 December 2013).

Based on these circumstances, it has now become relevant to study on how the banks have performed in

accomplishing the tasks. As of now, two studies, in the book - “Green Banking in Bangladesh; Environmental Risk

Management in Banking” edited by Chowdhury and Habib (2014) and published by Bangladesh Institute of Bank

Management (BIBM), examined the status and impact of green banking initiatives of Bangladesh Bank. Both these

studies appear to present a partial scenario. In reference to the existing literatures, the current study is more

comprehensive and expected to generate new findings through: (i) covering whole three years of given timeframe,

(ii) studying larger number of sample banks, (iii) applying more robust parameters and measurement approach for

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

2

assessing the level of green banking policy implementation, and finally (iv) exploring the specific reasons for partial

compliance of the Green Banking Guideline (GBG) by the scheduled banks. Therefore, the present study is an

attempt to meet the literature gap and explore in a wider detail the status of green banking policy implementation by

the banking sector of the country after whole three years of target timeline and identify areas where Bangladesh

Bank can now focus on for improvement in its efforts.

REVIEW OF LITERATURE

The Concept of Green Banking

“Green” in green banking principally indicates banks‟ environmental accountability and environmental

performances in business operation (Bai, 2011). Therefore, the term “Green Banking” generally refers to banking

practices that foster environmentally responsible financing practices and environmentally sustainable internal

processes. A green bank is also called ethical bank, environmentally responsible bank, socially responsible bank, or

a sustainable bank, and is expected to consider all the social and environmental issues (Habib, 2010; Goyal and

Joshi, 2011). It means eco-friendly or environment-friendly banking to stop environmental degradation to make this

planet more habitable (Azam, 2012). The approach to green banking varies from bank to bank. A survey of more

literatures reveals a few more different interpretations of green banking and can be summarily presented below.

Author (s) Definition of Green Banking

Schultz (2010) It means promoting environment-friendly practices and reducing carbon footprint

from banking activities.

Singh and Singh (2012)

Green banking signifies encouraging environment-friendly practices and

plummeting carbon footprint by banking activities through various environment-

friendly acts.

Thombre (2011)

Green banking is functioning like a normal bank, which considers all the social and

environmental/ecological factors with an aim to protect the environment and

conserve natural resources.

Bahl (2012) Green banking is a kind of banking conducted in selected area and technique that

helps in reduction of internal carbon footprint and external carbon emissions.

The Purpose of Green Banking

The broad objective of the green banks is to use resources with responsibility, avoid waste and give priority to

environment and society (Habib, 2010). Bihari (2011) elucidated that green banking includes promoting social

responsibility where banks consider before financing a project whether it is environment-friendly and has any future

environmental implications. Green banking is a concept of shifting banks‟ objectives from “profit only” to “profit

with responsibility”. For example, Verma (2012) stated that Indian banks are gradually coming to realize that there

is need for a shift from the „profit, profit and profit motive to „planet, people and profit‟ which in fact establishes the

rationale for green banking (Figure 1).

FIGURE 1. THE COVERAGE OF GREEN BANKING

Adopted from Presentation of Setijawan E. (2014)

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

3

It is now no denying an argument that, to save the planet and the people in combination with profit taking motives,

green banking calls for dealing with environment-friendly approach of banks in their external activities and

environmentally responsible in their internal operations.

The Directions of Green Banking Activities

Green banking allows banks mobilize money, invest safely and channel the money to productive activities free from

deterioration of standard of living and environment. It facilitates and promotes the achievement of sustainable

development of banking and finance (Sahoo & Nayak, 2008; Goyal and Joshi, 2011). Bhardwaj and Malhotra (2013)

stated that although banks might not directly pollute environment, they might have clients doing or would be doing

so in future. Although Schmidheiny and Zorraquin (1996) observed that banks are not hindering the achievement of

sustainability outright, Jeucken and Bouma (1999) argued that their role might hamper sustainable development

because (1) they choose shorter term payback periods in contrast to long-term investment needed for sustainable

development, and (2) investments incorporating environmental side-effects usually have lower rate of return in

short-term. Therefore, sustainable investments are unlikely to find sufficient funding within traditional banking. The

most likely solution to the problem is to repackage cost and pricing structure, the regulatory and legal framework in

a way that profit-driven banks will generate only green financing and investments (Arnsperger, 2012).

Thompson and Cowton (2004) concluded that banks may be supportive through environmental disclosure

practice either voluntarily or required by regulation. In order to explain the banks‟ activities towards sustainability,

Jeucken (2010) identified four stages: defensive, preventive, offensive and sustainable banking where ethical

banking and green banking are also subsets of sustainable banking. From a broader perspective, banks can be green

through bringing improvement in six main spheres: investment management, deposit management, housekeeping,

recruitment and development of human capital, corporate social responsibility, and consciousness of the clients and

general mass (Rahman et al., 2013). Cogan (2008) found that (a) banks are increasingly discussing climate change

related business opportunities, (b) 28 of the 40 banks he studied disclosed their account of greenhouse gas emissions

from operations, and (c) investment banks were taking a leading role in supporting carbon trading mechanisms and

introducing new risk management products. Based on the experience of sustainable banking case studies,

International Finance Corporation (IFC) (2007) stated that (i) individual banks had to devise their own business case

for sustainable banking, (ii) reputation and branding had become the top reason for many banks and (iii) the benefits

outweighed the costs, and social and environmental risk management improved the quality of a bank‟s portfolio and

lowered insurance liabilities and compensation claims.

The Tools of Green Banking

Encouraging environmentally accountable investments and lending must be the prime responsibilities of banks

(Thombre, 2011). Banks should play a pro-active role to oblige industries for mandated investment for

environmental management, use of appropriate technologies and management systems (Masukujjaman and Aktar,

2013). Thus banks can act as an ethical organization by disbursement of loans only to those organizations, which

have environmental concerns (Muhamat et al., 2010; Gyoal & Joshi, 2011; Thombre, 2011). In addition, conversion

of internal operations of banks through renewable energy, process automation and reducing carbon footprint are also

vital (Millat et al., 2012). Green banking requires that the financial institutions should encourage projects which take

care: (i) sustainable development and use of natural renewable natural resources, (ii) protection of human health,

bio-diversity, efficient production and use of energy, and (iii) pollution prevention and waste minimization,

pollution controls (Biswas, 2011). Such approach necessarily calls for initiatives to (a) reinforce the awareness of

employees and other stakeholders on the subject of sustainability, (b) upgrade the tools used by institutions, and (c)

improve the transparency in disclosing socio-environmental information (Lins et al., 2008). There can be a number

of specific tools including but not limited to Carbon Credit business, Green Credit and Investment, Green

Mortgages, Green Credit Cards, Green Deposit Accounts, Mobile Banking, Online Banking, Waste Management,

and Roof Gardening (Dharwal & Agarwal, 2013; Islam & Das, 2013).

Acceptability of Green Banking

Environmental reputation is no doubt an important factor for economic success of the banks today. According to a

recent study by Javelin Strategy and Research, around 43% of customers polled preferred banks with green

initiatives (Green Wiki, 2013). Interestingly, an experience of top five Romanian banks suggests that banks with

higher rating and total assets were also better accountable socially and environmentally (Cosmin, 2008). Now-a-

days, increasing number of customers of many conventional banks request for green financial products and

investment opportunities (Arnsperger, 2012), and many of them also want to be familiar as “doing good” to

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

4

environmental concerns among Citizens. Therefore, mainstream banks do not want to miss out the “greening” of

customer preferences (Münchow et al., 2011). Even stock market investors also are now equally concerned and they

are ready to act against institutions not complying with environmental norms (Gupta, 2003; Goldar, 2007). It is

mentionable that enthusiasm of financial institutions and markets is a primary driver to move towards sustainability

supportive financing (Rahman, 2014).

The Risk and the Impact of Green Banking

Many businesses may be exposed to the risk that they might have to bear direct or indirect cost of environment

protection initiatives (e.g. stringent regulatory compliance requirement) taken by stakeholders (Bhardwaj &

Malhotra, 2013). In the United Kingdom, the breach of terms of the license given by integrated pollution prevention

control would lead to prohibition, financial penalties and enforcement notice against the polluting companies

(Bhardwaj & Malhotra, 2013). A study finds that the European Union had to incur a loss of 14 billion pound and

200 million working days due to the productivity losses and medical costs arising out of only air pollution (Stavros,

2005). Such negative impact is also evident on banks‟ own performance too. Some classic studies found that

environmental performance is highly correlated with financial performance and banks suffer from financial risk due

to lack of environmental considerations in business practice (Hamilton, 1995; Blacconiere & Pattern, 1994). Such an

example is the enforcement of The Comprehensive Environmental Response, Compensation, and Liability Act

(CERCLA) in USA in 1980s due to which many banks were outright held responsible for the environmental

degradation by their clients and banks had to pay for the remedial measures. Thus, it is essential for banks to

consider environmental issues while investing in companies or advise clients to do so in their business (Sahoo &

Nayak, 2008). However, Arnsperger (2012) stated that many organizations including banks that have already

“greened” their products and/or processes are doing quite well financially.

Green Banking Initiatives at the Global Level

In the context of sustainable growth especially in emerging economies, banking management system based on

sustainable principles is a provocation of these days (Raluca, 2012). There have been a number of initiatives to make

financial institutions more environmentally responsible. In the Earth Summit 1992, the United Nations Environment

Program (UNEP) initiative on the environment and sustainable development was established in order to initiate

interactions between UNEP and Financial Institutions and their joint efforts. In another effort, IFC‟s environmental

unit was established in 1991 for reviewing each project for environmental assessment. In 2002, global NGOs created

a coalition named „BankTract‟ to promote sustainable finance in the commercial sector which has been endorsed by

more than 200 organizations. In 2003, a group of banks along with IFC initiated Equator Principle that is accepted

by 46 financial institutions of 16 countries with operation in more than 100 countries as of now. IFC along with the

Financial Times also initiated „Sustainable Banking Award‟ since 2006. The number of banks applying was up by

more than 100% compared to the previous year's 48 banks from 28 countries. International Standards Organization

14000 is also another global initiative which is a series of voluntary compliance standards for environmental

practices (Murray et al., 1997).

European banks seem to be leaders in the international green market compared to other continents as a

whole and have developed a unique environmental philosophy (Papastergiou & Blanas, 2011). Rosenfeld (2007)

studied two major banks of Sweden and found that they were well aware about global greening efforts and were

interested in doing eco-friendly banking. However, Greek banks were fragmentary on this issue demonstrating low

compliance (less than 50% score) with the Global Reporting Initiative (GRI) and the Deloitte Touché Tohmatsu

(DTT) guidelines (Evangelinos, 2009).

In USA, Socially Responsible Investment (SRI) funds are so highly acclaimed that SRI assets there

amounted to $2.29 trillion in 2005 (Starogiannis, 2006). Going further, the Dutch government has made formal

request to banks to devise their operation towards achieving sustainable development. Recently, India is also giving

greater importance to sustainable banking and many are focusing on environment-friendly investment projects

(Pulicheri & Rajashekhar, 2013). The State Bank of India (SBI) is the first bank in the country to put money into

generation of green power through windmills (Dharwal & Agarwal, 2013) while more than 20 banks have already

initiated green products (Nath et al., 2014). However, as found by Rajput et al. (2013), implementing green banking

in India encounters numerous challenges such as fear of business loss to peers, lack of central bank‟s mandate, lack

of interest of customers and investors, complex reporting framework, insufficient budget for training, and lack of

skilled manpower etc.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

5

It must be noted that most international initiatives are voluntary in nature and are meant to promote a

common good of a better ecosystem. Voluntary commitment has its shortcoming in a competitive market.

The Green Banking Initiative in Bangladesh

For developing countries like Bangladesh, environmental sustainability and climate change resilience are key

elements of inclusive socioeconomic development (Rahman, 2013). In Bangladesh, in addition to lending, internal

banking operations have considerably increased the carbon discharge due to their massive use of energy through

lighting, air-conditioning, electrical equipment etc. (Rahman et al., 2013). Bangladesh Bank is quite concerned on

the environmental degradation situation and therefore has been providing continuous support and directions to all

scheduled banks (Khan, 2012). Bangladesh Bank issued a circular for the scheduled banks of the country asking

them to adopt green strategic planning for 2013 and beyond (BRPD Circular No.02 dated 27 February 2011). Banks

are asked to integrate internal green banking operation and external green financing practices. As Millat et al. (2012)

reported Bangladesh Bank has instructed all scheduled banks to formulate comprehensive policies for green lending

and investment after rigorous and adequate analysis of environmental risks incorporating national environmental

rules and acts.

According to a recent study Ullah (2012), along with GBG, Bangladesh Bank also extends technical

assistance. The study, based on a very small sample of 4 banks, observes that state-owned banks demonstrate nearly

zero compliance with the GBG, continue to finance harmful projects, and have achieved little in introducing

paperless banking while private banks have better compliance. These and some other dimensions of green banking

in Bangladesh have been discussed in the works of Rashid (2010), Schultz (2010), Fenn (2012), and Millat (2012).

Along with the GBG enacted by Bangladesh Bank, two comprehensive studies were conducted and

published by Bangladesh Institute of Bank Management in a book edited by Chowdhury & Habib (2014). The first

study found that as of June 2011, among 25 surveyed banks about 80 to 85% were still in planning stage, about 75%

banks had green finance schemes although many did not finance even a single project, some 32% of the banks had

some promotional and customer awareness efforts on their green activities while about 50% had no training

initiatives. The study also revealed that most of the banks were scattered and at early planning stage in having in-

office green initiatives. The second study in mid-2013 on 20 selected commercial banks found substantial progress

and revealed that 92% of the banks had some initiatives of utilizing their green finance fund but fall far short in

Climate Risk Fund (19% had no such allocation, 72% could not utilize allocated fund). However, all banks

developed own green banking policy and separate green banking cell but in-house environment management

initiatives were still in a very limited scale. The study shows although 75% of them developed one or two sector

specific environmental guidelines, only 11% of the fund for green marketing was utilized and merely 2 trainings per

bank were organized in 2012.

Moreover, a recent Bangladesh Bank Quarterly Review Report on Green Banking published in December,

2013 records a notable progress of banks in almost every aspect of the green banking with evidence of some

improvements in the overall scenario in the quarter ending in December, 2013. A latest picture of green banking

activities by banks in December 2013 has been presented below (Table 1).

TABLE 1. GREEN BANKING ACTIVITIES AT A GLANCE (DECEMBER, 2013)

Subject March-

2013

June-

2013

September-

2013

December-

2013

No. of Rated Projects 8117 8063 7615 8188

No. of Rated Projects Financed 6733 7238 6152 7554

Amount Disbursed against Rated Projects (Taka in

Million) 338926.03

433501.

31 404099.46 391062.77

No. of Branches Powered by Solar Energy 228 248 253 311

No. of ATM/SME Unit Offices Powered by Solar Energy 183 184 185 189

No. of Online Branches 3714 3988 4060 4496

Utilization of Green Finance (Taka in Million) 70326.45

86848.8

3 84978.55 105971.66

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

6

Utilization of Climate Risk Fund (Taka in Million) 20.56 103.82 15.41 175.63

Utilization of Green Marketing, Training and

Development (Taka in Million) 34.88 35.73 45.96 50.46

Source: Quarterly Review Report on Green Bangladesh, December 2013, Bangladesh Bank

It should be noted that Bangladesh Bank, is one of the global forerunners in bringing green banking policy guideline

in a so structured and formal way. Therefore, the findings of this study may substantially help the financial services

regulators of other countries in introducing and implementing the green banking or environment-friendly banking

policy smoothly.

OBJECTIVE OF THE STUDY

The study primarily aims at finding out the status of green banking policy implementation by the commercial banks

operating in Bangladesh and identifying the factors leading to success and failure of the banks in green banking so

that some ideas can be generated for planning future interventions of Bangladesh Bank to ensure more effective

green banking activities. In other words, the objectives of this study are:

- To look into how the green banking policies of Bangladesh Bank are implemented in practice and thus

incorporate into „Strategy‟ by the scheduled banks of the country;

- To understand the factors leading to success and failure of the scheduled banks in implementing the

Bangladesh Bank‟s green banking policies;

- To identify areas of further intervention for better implementation of the policies.

METHODOLOGY OF THE STUDY

The key approach of this present study is to measure the progress of the banks in Bangladesh in implementation of

the Bangladesh Bank‟s Green Banking Guideline (GBG). The assessment is made primarily by using the following

criteria: (i) bank-wise weighted average progress level across all policies of the GBG and (ii) policy-wise level of

progress across all banks.

Bank-Wise Weighted Average Progress Level across All Policies

To measure the level of progress in implementing the GBG, „percentage score‟ has been assigned policy-wise. There

are 19 policies in the GBG – Phase I: policies 1.1 to 1.9, Phase II: policies 2.1 to 2.7 and Phase III: policies 3.1, 3.2

and 4.0. The policy no. 4.0 is basically a post-implementation routine activity namely „Reporting Green Banking

Practices on Quarterly Basis‟ and the major Green Banking Policies in Phase I, II, and III are shown in Chart - A.

For each of these individual policies, each of the banks under examination is rated out of „100%‟ compliance level

based on “on the field observation and experience” in a bank. Later, bank-wise weighted average level of progress

( ) has been calculated combining all 19 policies by using the following formula:

∑

Where, n = number of policies, = weighted average score of a given bank

= wight for policy I, = score assigned for policy i

The weighted average overall progress result for each bank has then been used to test two important aspects: (a)

Category-wise weighted average overall progress, (b) Overall weighted average progress by bank type (state owned,

private, and foreign). As the three-year period to implement all three phases of GB guideline set by the Bangladesh

Bank has already passed, banks are expected to achieve full progress level by 2013. Based on the importance of the

policies and necessity for implementation in banking operation, weights have been assigned. The weight structure is

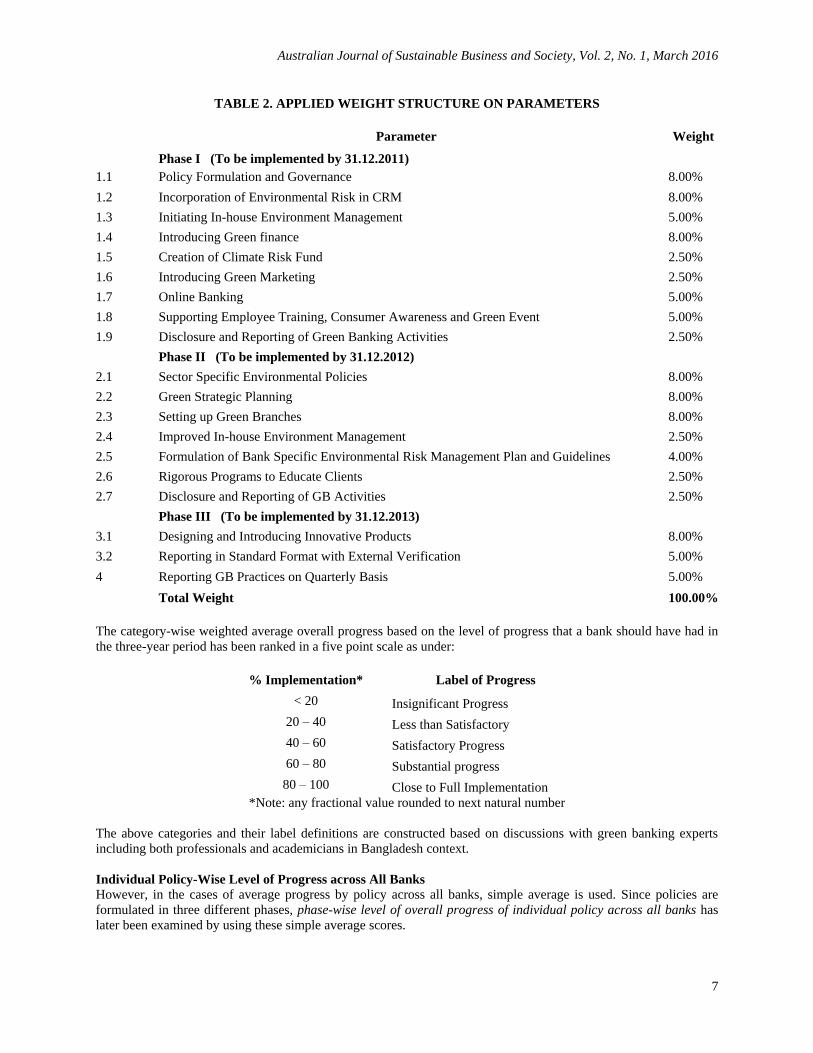

shown below in Table 2.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

7

TABLE 2. APPLIED WEIGHT STRUCTURE ON PARAMETERS

Parameter Weight

Phase I (To be implemented by 31.12.2011)

1.1 Policy Formulation and Governance 8.00%

1.2 Incorporation of Environmental Risk in CRM 8.00%

1.3 Initiating In-house Environment Management 5.00%

1.4 Introducing Green finance 8.00%

1.5 Creation of Climate Risk Fund 2.50%

1.6 Introducing Green Marketing 2.50%

1.7 Online Banking 5.00%

1.8 Supporting Employee Training, Consumer Awareness and Green Event 5.00%

1.9 Disclosure and Reporting of Green Banking Activities 2.50%

Phase II (To be implemented by 31.12.2012)

2.1 Sector Specific Environmental Policies 8.00%

2.2 Green Strategic Planning 8.00%

2.3 Setting up Green Branches 8.00%

2.4 Improved In-house Environment Management 2.50%

2.5 Formulation of Bank Specific Environmental Risk Management Plan and Guidelines 4.00%

2.6 Rigorous Programs to Educate Clients 2.50%

2.7 Disclosure and Reporting of GB Activities 2.50%

Phase III (To be implemented by 31.12.2013)

3.1 Designing and Introducing Innovative Products 8.00%

3.2 Reporting in Standard Format with External Verification 5.00%

4 Reporting GB Practices on Quarterly Basis 5.00%

Total Weight 100.00%

The category-wise weighted average overall progress based on the level of progress that a bank should have had in

the three-year period has been ranked in a five point scale as under:

% Implementation* Label of Progress

< 20 Insignificant Progress

20 – 40 Less than Satisfactory

40 – 60 Satisfactory Progress

60 – 80 Substantial progress

80 – 100 Close to Full Implementation

*Note: any fractional value rounded to next natural number

The above categories and their label definitions are constructed based on discussions with green banking experts

including both professionals and academicians in Bangladesh context.

Individual Policy-Wise Level of Progress across All Banks

However, in the cases of average progress by policy across all banks, simple average is used. Since policies are

formulated in three different phases, phase-wise level of overall progress of individual policy across all banks has

later been examined by using these simple average scores.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

8

Data Sources

The study carried out intensive survey of 42 scheduled banks (out of total 56, 75% sample coverage) operating in

Bangladesh where each bank (Table 3) was studied for 15 days separately during March 2014.

TABLE 3. BANKS AND THEIR WEIGHTED AVERAGE PROGRESS LEVEL ACROSS ALL POLICIES

Domestic Private Commercial Banks

Bank Name % Progress Bank Name %

Progress Bank Name

%

Progress

AB 62 EXIM 63 Premier 37

Al Arafah 55 First Security 70 Prime 60

Bank Asia 71 IBBL 45 Pubali 43

Basic 42 IFIC 44 Shahjalal 47

BCBL 15 Jamuna 29 SIBL 48

BRAC 74 Mercantile 75 Southeast 61

City 34 MTBL 73 Standard 37

DBBL 40 NBL 35 Trust 67

DBL 47 NCC 36 UCB 61

EBL 64 One Bank 35 Uttara 55

State Owned Banks % Progress Foreign Commercial

Banks

%

Progress

Agrani 33 Alfalah 33

BDBL 22 HSBC 62

BKB 25 CITI N A 77

Janata 64 CBCL 48

Rupali 29 SBI 58

Sonali 38 SCB 85

Source: Author Constructed from Survey Findings

Among the banks, 30 are Domestic Private Commercial Banks, 6 are State Owned Banks, and 6 are

Foreign Commercial Banks. Based on the data explored, necessary descriptive and tabular analysis has been made to

assess the status of green banking policy implementation, and develop insights on the reasons for success/failure in

the process of implementation. Apart from this field level data, secondary information has been collected from

banks‟ annual reports and their green banking reports periodically submitted to the central bank. The GBG and its

related materials have been accumulated from the Green Banking division of Bangladesh Bank.

GREEN BANKING PRACTICES: ANALYSIS AND RESULTS

Overall Implementation of GB Policy

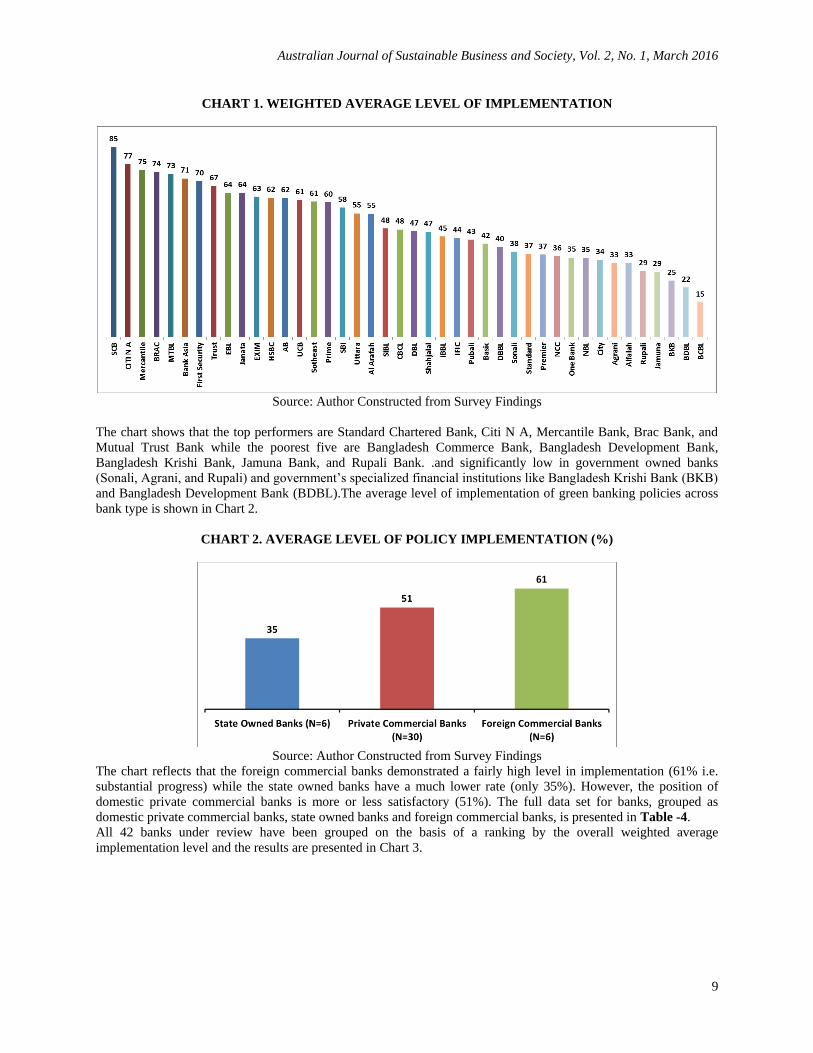

The level of overall implementation is presented in Chart 1 showing the bank-wise weighted average score

combining all 19 policies and their weights, and the position of the 42 surveyed banks in a descending order of the

score for implementation.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

9

CHART 1. WEIGHTED AVERAGE LEVEL OF IMPLEMENTATION

Source: Author Constructed from Survey Findings

The chart shows that the top performers are Standard Chartered Bank, Citi N A, Mercantile Bank, Brac Bank, and

Mutual Trust Bank while the poorest five are Bangladesh Commerce Bank, Bangladesh Development Bank,

Bangladesh Krishi Bank, Jamuna Bank, and Rupali Bank. .and significantly low in government owned banks

(Sonali, Agrani, and Rupali) and government‟s specialized financial institutions like Bangladesh Krishi Bank (BKB)

and Bangladesh Development Bank (BDBL).The average level of implementation of green banking policies across

bank type is shown in Chart 2.

CHART 2. AVERAGE LEVEL OF POLICY IMPLEMENTATION (%)

Source: Author Constructed from Survey Findings

The chart reflects that the foreign commercial banks demonstrated a fairly high level in implementation (61% i.e.

substantial progress) while the state owned banks have a much lower rate (only 35%). However, the position of

domestic private commercial banks is more or less satisfactory (51%). The full data set for banks, grouped as

domestic private commercial banks, state owned banks and foreign commercial banks, is presented in Table -4.

All 42 banks under review have been grouped on the basis of a ranking by the overall weighted average

implementation level and the results are presented in Chart 3.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

10

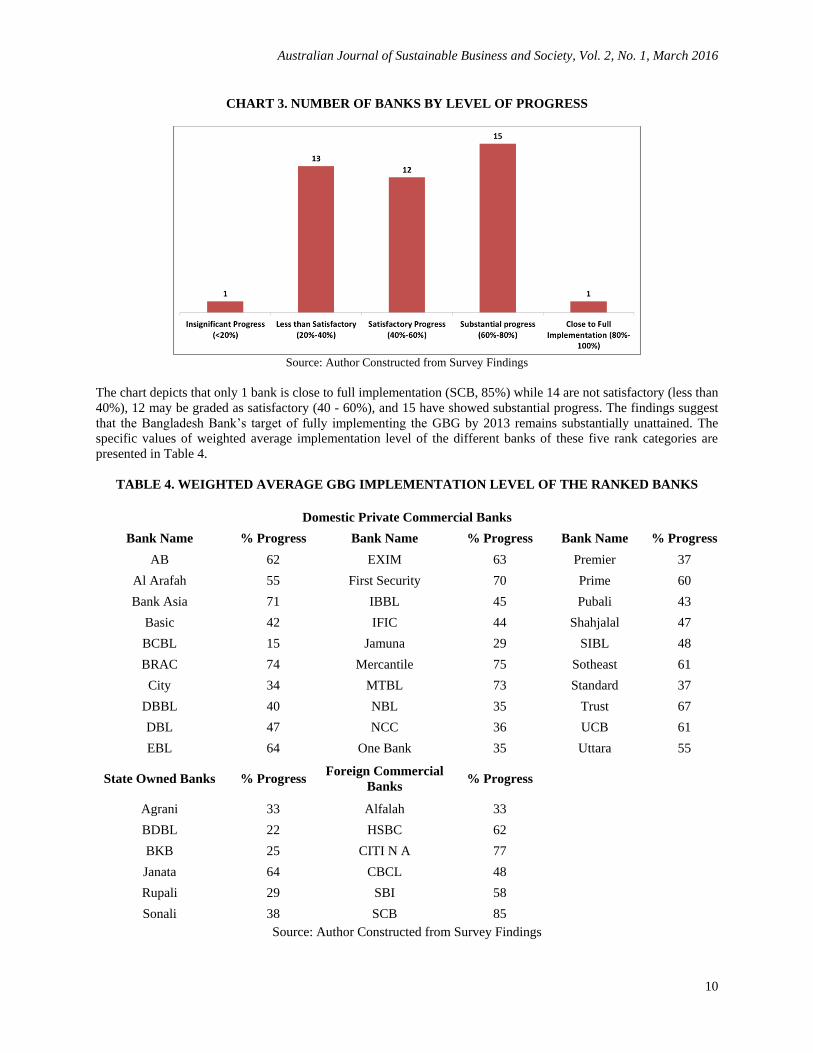

CHART 3. NUMBER OF BANKS BY LEVEL OF PROGRESS

Source: Author Constructed from Survey Findings

The chart depicts that only 1 bank is close to full implementation (SCB, 85%) while 14 are not satisfactory (less than

40%), 12 may be graded as satisfactory (40 - 60%), and 15 have showed substantial progress. The findings suggest

that the Bangladesh Bank‟s target of fully implementing the GBG by 2013 remains substantially unattained. The

specific values of weighted average implementation level of the different banks of these five rank categories are

presented in Table 4.

TABLE 4. WEIGHTED AVERAGE GBG IMPLEMENTATION LEVEL OF THE RANKED BANKS

Domestic Private Commercial Banks

Bank Name % Progress Bank Name % Progress Bank Name % Progress

AB 62 EXIM 63 Premier 37

Al Arafah 55 First Security 70 Prime 60

Bank Asia 71 IBBL 45 Pubali 43

Basic 42 IFIC 44 Shahjalal 47

BCBL 15 Jamuna 29 SIBL 48

BRAC 74 Mercantile 75 Sotheast 61

City 34 MTBL 73 Standard 37

DBBL 40 NBL 35 Trust 67

DBL 47 NCC 36 UCB 61

EBL 64 One Bank 35 Uttara 55

State Owned Banks % Progress Foreign Commercial

Banks % Progress

Agrani 33 Alfalah 33

BDBL 22 HSBC 62

BKB 25 CITI N A 77

Janata 64 CBCL 48

Rupali 29 SBI 58

Sonali 38 SCB 85

Source: Author Constructed from Survey Findings

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

11

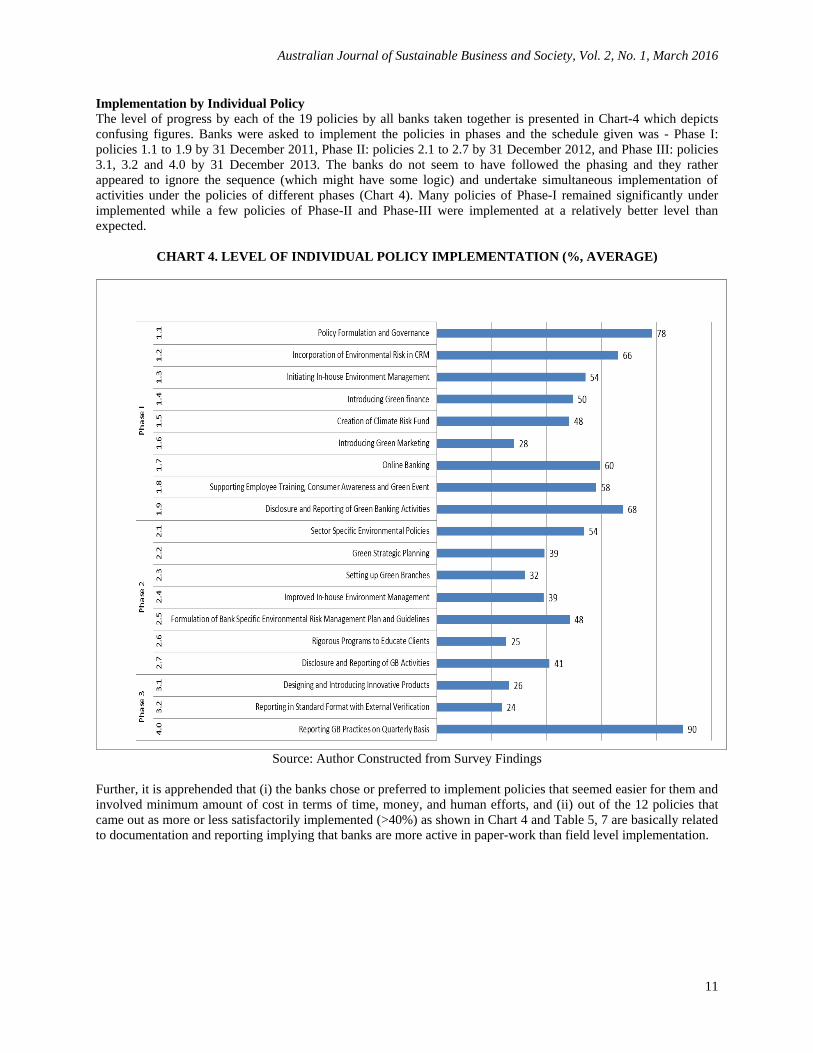

Implementation by Individual Policy

The level of progress by each of the 19 policies by all banks taken together is presented in Chart-4 which depicts

confusing figures. Banks were asked to implement the policies in phases and the schedule given was - Phase I:

policies 1.1 to 1.9 by 31 December 2011, Phase II: policies 2.1 to 2.7 by 31 December 2012, and Phase III: policies

3.1, 3.2 and 4.0 by 31 December 2013. The banks do not seem to have followed the phasing and they rather

appeared to ignore the sequence (which might have some logic) and undertake simultaneous implementation of

activities under the policies of different phases (Chart 4). Many policies of Phase-I remained significantly under

implemented while a few policies of Phase-II and Phase-III were implemented at a relatively better level than

expected.

CHART 4. LEVEL OF INDIVIDUAL POLICY IMPLEMENTATION (%, AVERAGE)

Source: Author Constructed from Survey Findings

Further, it is apprehended that (i) the banks chose or preferred to implement policies that seemed easier for them and

involved minimum amount of cost in terms of time, money, and human efforts, and (ii) out of the 12 policies that

came out as more or less satisfactorily implemented (>40%) as shown in Chart 4 and Table 5, 7 are basically related

to documentation and reporting implying that banks are more active in paper-work than field level implementation.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

12

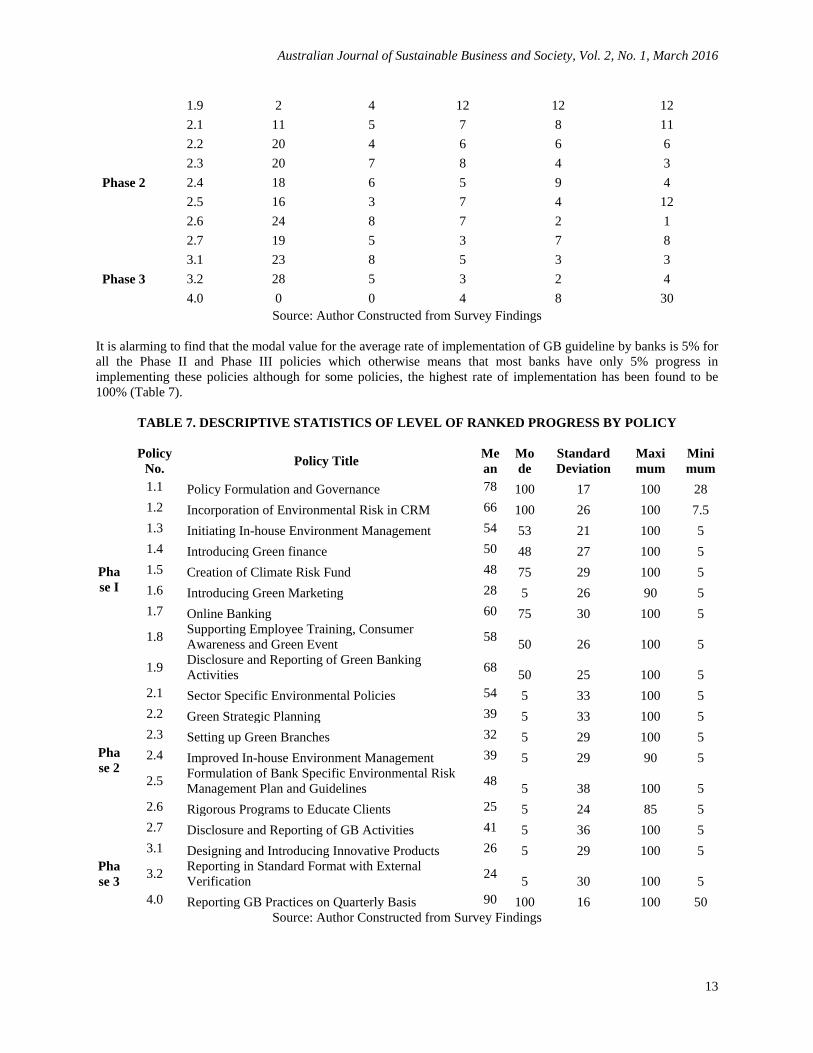

TABLE 5. INDIVIDUAL POLICY-WISE AVERAGE IMPLEMENTATION

Policy

No. Policy Title

Average %

Implementatio

n

4.0 Reporting GB Practices on Quarterly Basis 90

1.1 Policy Formulation and Governance 78

1.9 Disclosure and Reporting of Green Banking Activities 68

1.2 Incorporation of Environmental Risk in CRM 66

1.7 Online Banking 60

1.8 Supporting Employee Training, Consumer Awareness and Green Event 58

1.3 Initiating In-house Environment Management 54

2.1 Sector Specific Environmental Policies 54

1.4 Introducing Green finance 50

2.5 Formulation of Bank Specific Environmental Risk Management Plan and

Guidelines 48

1.5 Creation of Climate Risk Fund 48

2.7 Disclosure and Reporting of GB Activities 41

2.2 Green Strategic Planning 39

2.4 Improved In-house Environment Management 39

2.3 Setting up Green Branches 32

1.6 Introducing Green Marketing 28

3.1 Designing and Introducing Innovative Products 26

2.6 Rigorous Programs to Educate Clients 25

3.2 Reporting in Standard Format with External Verification 24

Source: Author Constructed from Survey Findings

However, the banks did not perform well even in documentation and reporting as evidenced by the fact that their

progress in implementation of disclosure and reporting of Green Banking Activities and Green Strategic Planning is

only around 40%. Observations in phase-wise comparison of GBG policies against the categories of progress as

defined suggest that most banks show relatively good progress in implementing Phase - I policies while

“Insignificant” or “Less than Satisfactory” implementation rate for Phase - II and Phase - III policies (Table 6) and

there are banks with even as low as 5% or lower level of progress of different policies.

TABLE 6. LEVEL OF RANKED PROGRESS BY INDIVIDUAL POLICY

Insignificant

Progress

Less than

Satisfactory

Satisfactory

Progress

Substantial

progress

Close to Full

Implementation

Policy No. <=20 > 20 - 40 > 40 - 60 >60 - 80 >80 - 100

Phase I

1.1 0 1 4 15 22

1.2 4 4 9 13 12

1.3 3 7 15 13 4

1.4 8 8 12 7 7

1.5 10 5 12 10 5

1.6 24 9 3 3 3

1.7 6 6 7 13 10

1.8 5 6 12 12 7

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

13

1.9 2 4 12 12 12

Phase 2

2.1 11 5 7 8 11

2.2 20 4 6 6 6

2.3 20 7 8 4 3

2.4 18 6 5 9 4

2.5 16 3 7 4 12

2.6 24 8 7 2 1

2.7 19 5 3 7 8

Phase 3

3.1 23 8 5 3 3

3.2 28 5 3 2 4

4.0 0 0 4 8 30

Source: Author Constructed from Survey Findings

It is alarming to find that the modal value for the average rate of implementation of GB guideline by banks is 5% for

all the Phase II and Phase III policies which otherwise means that most banks have only 5% progress in

implementing these policies although for some policies, the highest rate of implementation has been found to be

100% (Table 7).

TABLE 7. DESCRIPTIVE STATISTICS OF LEVEL OF RANKED PROGRESS BY POLICY

Policy

No. Policy Title

Me

an

Mo

de

Standard

Deviation

Maxi

mum

Mini

mum

Pha

se I

1.1 Policy Formulation and Governance 78 100 17 100 28

1.2 Incorporation of Environmental Risk in CRM 66 100 26 100 7.5

1.3 Initiating In-house Environment Management 54 53 21 100 5

1.4 Introducing Green finance 50 48 27 100 5

1.5 Creation of Climate Risk Fund 48 75 29 100 5

1.6 Introducing Green Marketing 28 5 26 90 5

1.7 Online Banking 60 75 30 100 5

1.8 Supporting Employee Training, Consumer

Awareness and Green Event 58

50 26 100 5

1.9 Disclosure and Reporting of Green Banking

Activities 68

50 25 100 5

Pha

se 2

2.1 Sector Specific Environmental Policies 54 5 33 100 5

2.2 Green Strategic Planning 39 5 33 100 5

2.3 Setting up Green Branches 32 5 29 100 5

2.4 Improved In-house Environment Management 39 5 29 90 5

2.5 Formulation of Bank Specific Environmental Risk

Management Plan and Guidelines 48

5 38 100 5

2.6 Rigorous Programs to Educate Clients 25 5 24 85 5

2.7 Disclosure and Reporting of GB Activities 41 5 36 100 5

Pha

se 3

3.1 Designing and Introducing Innovative Products 26 5 29 100 5

3.2 Reporting in Standard Format with External

Verification 24

5 30 100 5

4.0 Reporting GB Practices on Quarterly Basis 90 100 16 100 50

Source: Author Constructed from Survey Findings

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

14

The average level of implementation of the Bangladesh Bank‟s policies of different phases is shown in Chart 5. The

chart shows that although Phase-I policies were scheduled to be fully implemented within 31 December 2011, the

actual implementation rate was only 57% and yet this has been the highest rate of implementation. The

implementation rate of policies of Phase-II (scheduled to be implemented by 31 December 2012) was 40% and that

for policies under Phase-III with (scheduled to be done by 31 December 2013) was only 47%.

CHART 5. AVERAGE LEVEL OF IMPLEMENTATION (%) BY PHASE

Source: Author Constructed from Survey Findings

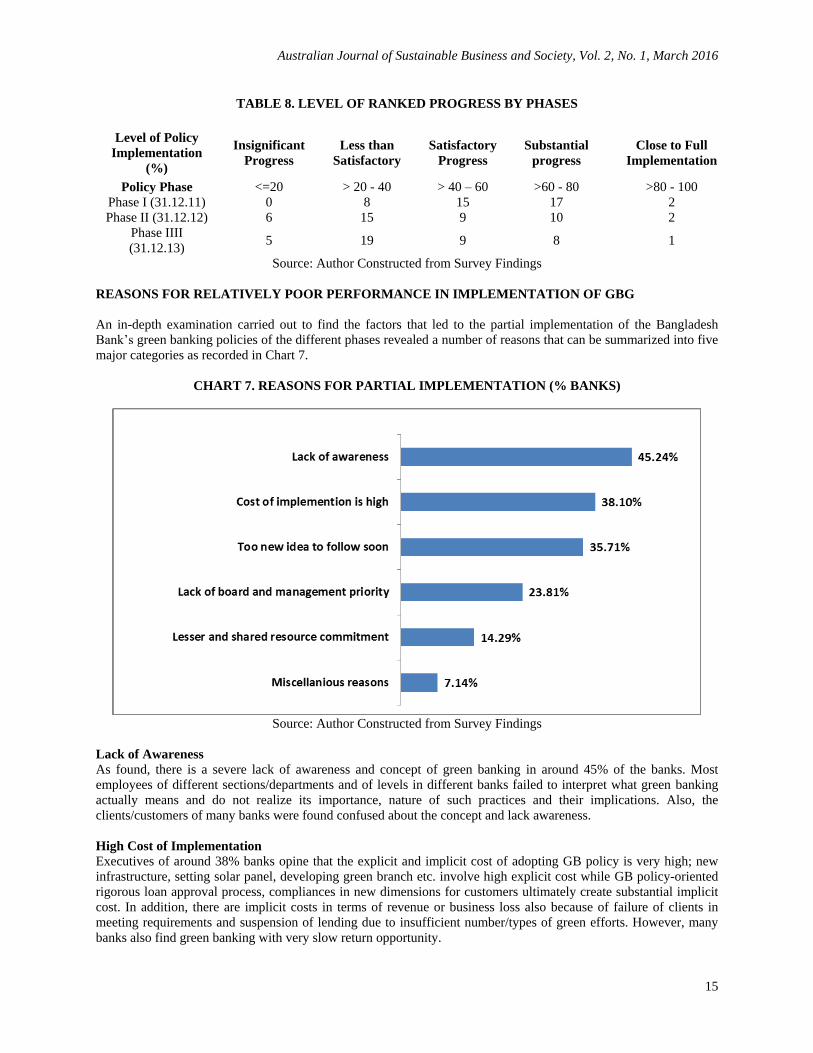

It has been further observed that as time has elapsed in implementing the GBG policies by phases (Chart 6).

CHART 6. NUMBER OF BANKS AND LEVEL OF PROGRESS BY PHASE

Source: Author Constructed from Survey Findings

The number of banks ranked “less than satisfactory” category (>20% and 20–40% implementation rate) grew

substantially higher. At the same time, the number of banks ranked “satisfactory” and “substantial progress”

categories has decreased significantly. This implies that most banks have failed to maintain the pace of

implementation of GBG regardless of phase. Moreover, instead of implementing the policies phase by phase, they

selected their course at their own choice leading to a failure in meeting the time bound targets of achievement. The

result is also shown in Table 8.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

15

TABLE 8. LEVEL OF RANKED PROGRESS BY PHASES

Level of Policy

Implementation

(%)

Insignificant

Progress

Less than

Satisfactory

Satisfactory

Progress

Substantial

progress

Close to Full

Implementation

Policy Phase <=20 > 20 - 40 > 40 – 60 >60 - 80 >80 - 100

Phase I (31.12.11) 0 8 15 17 2

Phase II (31.12.12) 6 15 9 10 2

Phase IIII

(31.12.13) 5 19 9 8 1

Source: Author Constructed from Survey Findings

REASONS FOR RELATIVELY POOR PERFORMANCE IN IMPLEMENTATION OF GBG

An in-depth examination carried out to find the factors that led to the partial implementation of the Bangladesh

Bank‟s green banking policies of the different phases revealed a number of reasons that can be summarized into five

major categories as recorded in Chart 7.

CHART 7. REASONS FOR PARTIAL IMPLEMENTATION (% BANKS)

Source: Author Constructed from Survey Findings

Lack of Awareness

As found, there is a severe lack of awareness and concept of green banking in around 45% of the banks. Most

employees of different sections/departments and of levels in different banks failed to interpret what green banking

actually means and do not realize its importance, nature of such practices and their implications. Also, the

clients/customers of many banks were found confused about the concept and lack awareness.

High Cost of Implementation

Executives of around 38% banks opine that the explicit and implicit cost of adopting GB policy is very high; new

infrastructure, setting solar panel, developing green branch etc. involve high explicit cost while GB policy-oriented

rigorous loan approval process, compliances in new dimensions for customers ultimately create substantial implicit

cost. In addition, there are implicit costs in terms of revenue or business loss also because of failure of clients in

meeting requirements and suspension of lending due to insufficient number/types of green efforts. However, many

banks also find green banking with very slow return opportunity.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

16

Too New an Idea to Implement Fast

The employees and management in around 36% of the banks studied have reported that they perceive green banking

as a completely new concept and therefore more time is needed to be familiar with and conversant in the concept

and adopt it in practice. According to their view, more time is needed to understand the impacts of green banking

and therefore to adopt it properly in practice for a sustainable future of the economy.

Less Priority by the Board and Management

Officers in charge of green banking activities in a number of banks (around 24%) have reported that the top

management is reluctant in green banking and they do not concentrate on, even put a very low priority. The bank

executives are busy with other regular banking operations and usually avoid spending time and energy in complying

with the GBG activities put forward by Bangladesh Bank. Due to lesser priority, funds go more to the traditional

projects and even if some green banking concepts are considered in some lending as well as in internal functions of

the banks, the fund allocated remains small and the process become unnecessarily complex and lengthy.

Lack of Resources/Shared Commitment of Resources

Around 14% of the banks have been found having no dedicated employees or assigned employees with “charge” for

green banking activities/division. The concept of green banking services among bank officers continue to get low

priority and are therefore, not recognized as responsible or high profile job. Too often, the activities are assigned to

employees performing below average in their regular desks and their work in green banking is poorly monitored. In

addition, employees assigned with the “charge” of green banking activities are also transferred from one desk to

another and therefore, frequently changed. In many cases, the green banking policy implementation activities are

distributed to multiple departments creating operational complexity and fragmentation of the process and progress.

Apart from the major reasons explained above, banks also indicated few other reasons such as broadening

range of services by banks because of adopting green banking created additional pressure on the time and work load

of the bank employees and also, some banks consider that the Bangladesh Bank‟s GBG and the requirements of

international standards are difficult to simultaneously comply, and therefore, there should be a mechanism for

addressing the issue, especially in the interest of foreign banks operating in Bangladesh and the relatively large

national banks operating abroad.

CONCLUSION

The study finds that performance of banks in Bangladesh GBG implementation is not very satisfactory although a

substantial progress was expected at the end of the three phase period in December 2013. A recent Bangladesh Bank

report on green banking records that the performance of scheduled banks has not been very impressive but the banks

did fairly well in terms of use of funds allocated for the purpose in the last few quarters (Bangladesh Bank, 2013).

The findings of the present study on the phase-wise implementation data show that the implementation of the 19

policies in three phases remained fragmented and policies related to paper-work or desk-based work have been

implemented quickly while field level implementation related policies are less prioritized by the scheduled banks.

Moreover, it is evident that state-owned banks are the worst performers with the lowest implementation level of the

GBG while foreign banks are the top performers and the domestic private banks are in the second place. This

finding on state-owned and private banks confirms the findings of Ullah (2012) using on around 10 times larger

sample size and a more rigorous and differentiated method. However, evaluation of foreign commercial banks is a

completely new addition by this study in this context.

This study also finds the level of GBG compliance for each of the policy separately some of which were

studied by Habib et al. (2011) and Habib et al. (2013). The findings of this current study closely support the earlier

findings by Habib et al. (2013) as of mid-2013 in terms of very limited advancement in: in-house environmental

activities, actual financing to environment-friendly projects, green marketing and branches, climate risk fund

creation, and training and awareness initiatives. The better progress in paper-work based works such as policy

governance, environmental risk incorporation in CRM, regular disclosure and reporting framework also support the

findings of the above mentioned earlier studies by Habib et al. (2011; 2013) but this study generates more new

findings and has used more rigorous method to assess the compliance level following „policy-by-policy‟ approach.

Moreover, unlike Habib et al. (2011; 2013), this study also sheds light on reasons for failure to comply with GBG.

The banks have reported a number of factors causing partial implementation of GBG. Among them, lack of

awareness, high implementation cost, unfamiliarity of the concept, and relatively poor utilization of human

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

17

resources are consistent with findings by Rajput et al. (2013), and few more have been added newly by this study

(i.e. less prioritization by board and management, conflicting regulatory requirements).

Therefore, a range of education and awareness campaign should be organized by Bangladesh Bank and

scheduled banks for employees and customers. Moreover, separate dialogue sessions should be arranged by

Bangladesh Bank with the boards and top managements of the scheduled banks, and instruct them to place top

priority on green banking activities. Bangladesh Bank may also periodically examine the resources committed for

GBG implementation in the scheduled banks that can ensure self-sufficient green banking divisions in banks.

Moreover, Bangladesh Bank has to initiate education and training programs to convince the boards or top

management on the implicit benefits of green banking compared to its costs. Benefits in terms of environmental

sustainability in the long certainly will best protect the society, community, economy and the country as a whole.

Therefore, for suitable existence of the future earth, a sacrifice today is needed, and this has to be properly

communicated to the scheduled bank authorities.

REFERENCES

Arnsperger, C 2014, „Social and Sustainable Banking and the Green Economy project Part I: A Hypothetical

Diachronic Scenario‟, Paper for the 2014 Annual Conference of the Society for the Advancement of Socio-

Economics (SASE), Chicago, IL.

Azam, S 2012, „Green Corporate Environment Thru' Green Banking and Green Financing‟, The Financial Express

July 04, Viewed on March 2014, Available at_

http://www.thefinancialexpressbd.com/more.php?news_id=135391&date=2012-07-04

Bahl, S 2012, „Role of Green Banking in Sustainable Growth‟, International Journal of Marketing. Financial

Services and Management Research, vol. 2, no. 1, pp. 27-35.

Bai, Y 2011, Financing a Green Future. MS thesis: Lund, Sweden, IIIEE Theses 2011: 02, Accessed on 15

September, 2012 from:

http://lup.lub.lu.se/luur/download?func=downloadFile&recordOId=2203222&fileOId=220322

Bangladesh Bank 2011, BRPD Circular No. 02. dated: 27 February, 2011. Accessed:

http://www.bb.org.bd/mediaroom/circulars/gbcrd/dec242013gbcrd08e.pdf on June 2013

Bangladesh Bank 2013, GBCSRD Circular No. 08. dated: 24 December, 2013, Accessed in April, 2014 from

www.bb.org.bd/mediaroom/circulars/gbcrd/dec242013gbcrd08e.pdf

Bangladesh Bank 2013, Quarterly Review Report on Green Banking Activities of Banks and Financial Institutions.

Green Banking and CSR Department, Retrieved in April 2014 from www.bangladesh-

bank.org/.../greenbanking/greenbanking_dec2013.pdf

Bhardwaj, BR, & Malhotra, A 2013, „Green Banking Strategies: Sustainability through Corporate

Entrepreneurship‟, Greener Journal of Business and Management Studies, vol. 3, no. 4, pp. 180-193.

Bihari, SC 2011, „Green Banking-Towards Socially Responsible Banking in India‟, International Journal of

Business Insights and Transformation, October 2010- March 2011 Issue, vol. 4, no. 1, pp. 82-87.

Biswas, N 2011, „Sustainable Green Banking Approach: The Need of the Hour‟, Business Spectrum, vol. 1, no. 1,

pp. 32-38.

Blacconiere, W, & Pattern, D 1994, „Environment Disclosure, Regulatory Costs and Changes in Firm Values‟,

Journal of Accounting and Economics, December Issue, vol. 18, no. 3, pp. 357-377.

Chowdhury, TA, & Habib, SMA (eds.) 2014, Green Banking in Bangladesh; Environmental Risk Management in

Banking, Bangladesh Institute of Bank Management (BIBM), Dhaka, Bangladesh, ISBN: 978-984-33-

8352-5.

Cogan, DG 2008, „Corporate Governance and Climate Change: The Banking Sector‟, A Ceres Report, January,

RiskMetrics Group Inc., New York. Accessed in June 2015 at

http://www.un.org/ga/president/62/ThematicDebates/gpicc/cgccbs.pdf

Cosmin, J, Mihaela, B, & Irina-Eugenia, I 2008, „Corporate Social Responsibility in the Romanian Banking Sector‟,

Economic Sciences Series; Issue II –Economy and Business Administration, Volume XVII: 620-625,

Oradea University Publishing House, Romania.

Dharwal, M, & Agarwal, A 2013, „Green Banking: An Innovative Initiative for Sustainable Development‟,

ACCMAN Institute of Management Article, Retrieved from

www.accman.in/images/j11/Green_Banking__(2).doc

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

18

Dogarawa, AB 2006, „An Examination of Ethical Dilemmas in the Nigerian Banking Sector‟, Department of

Accounting, Ahmadu Bello University, Zaria, Electronic copy available at:

http://ssrn.com/abstract=1621054

Evangelinos, KI, Skouloudis, A, Nikolaou, IE & Filho, WL 2009, „An Analysis of Corporate Social Responsibility

(CSR) and Sustainability Reporting Assessment in the Greek Banking Sector‟, Professionals’ Perspectives

of Corporate Social Responsibility, Springer Berlin Heidelberg, pp. 157-173.

Fenn, K 2012, „All about Green Banking‟, Private Climate Change, Accessed in February 2013 at

http://www.preventclimatechange.co.uk/green-banking.html

Goldar, BN 2007, „Impact of Corporate Environmental Performance or Profitability and Market Value: A case

Study of Indian Firms‟, Paper presented in National Conference on Expanding Freedom: towards Social

and Economic Transformation in Globalized World, April, Institute of Economic Growth, Delhi.

Goyal, KA, & Joshi, V 2011, „A Study of Social and Ethical Issues In Banking Industry‟, International Journal of

Economics and Research, vol. 2, no. 5, pp. 49-57.

Green Wiki 2013, Green Banking. Available from http://green.wikia.com/wiki/Green_Banking, Accessed in

December 2013.

Gupta, S 2003, „Do Stock Market Penalize Environment-Unfriendly Behavior? Evidence from India‟, Delhi School

of Economics - Working Paper Series, India, no.-116.

Habib, SMA 2010, „Green Banking: A Multi-Stakeholder Endeavour‟, The Daily Star 07 August, Available at

<http://archive.thedailystar.net/newDesign/news-details.php?nid=149676>

Habib, SMA, Ullah, MS, & Rahman, T 2014, „An Impact Evaluation of Green Initiatives of Bangladesh Bank‟, in

Green Banking in Bangladesh; Environmental Risk Management in Banking, eds TA Chowdhury, & SMA

Habib, Bangladesh Institute of Bank Management (BIBM) – Dhaka, pp. 93-136, ISBN: 978-984-33-8352-

5.

Habib, SMA, Ullah, MS, Rahman, T, Zareen, A, & Faisal, N 2014, „Development of Green Banking in Bangladesh:

Status and Prospects‟ in Green Banking in Bangladesh; Environmental Risk Management in Banking, eds

TA Chowdhury, & SMA Habib, Bangladesh Institute of Bank Management (BIBM) – Dhaka, pp. 93-136,

ISBN: 978-984-33-8352-5.

Hamilton, JT 1995, „Pollution as News: Media and Stock Market Reactions to the Toxics Release Inventory Data‟,

Journal of Environmental Economics and Management, vol. 28, no. 1, pp. 98–113.

International Finance Corporation 2008, Banking on Sustainability - Financing Environmental and Social

Opportunities In Emerging Markets. Available at:

http://firstforsustainability.org/media/IFC%20Banking%20on%20Sustainability.pdf

Islam, MS & Das, PC 2013, „Green Banking practices in Bangladesh‟, IOSR Journal of Business and Management,

vol. 8, no. 3, pp. 39 – 44.

Jeucken, M & Bouma, JJ 1999, „The Changing Environment of Banks‟, GMI Theme Issue; GMI-27, Autumn.

Jeucken, M 2010, Sustainable Finance and Banking - The Finance Sector and the Future of the Planet. Routledge.

Khan, MTA 2012, „Green Banking: Go Green Think Green‟, The Daily Star World Environment Day Special June

05. Retrieved in November 2013 from

http://archive.thedailystar.net/suppliments/2012/environment/pg1.htm

Lins, C, Wajnberg, D, Steger, U, & Ionescu, A 2008, Corporate Sustainability in the Brazilian Banking Sector.

International Institute for Management Development, Rio De Janerio. Accessed on November 2013 at:

http://www.imd.org/research/publications/upload/WP_2008_07_Steger_Lins_Wajnberg_Ionescu_Somers_

Level_1.pdf

Masukujjaman M & Aktar S 2013, „Green Banking in Bangladesh: A Commitment towards the Global Initiatives‟,

Journal of Business and Technology (Dhaka), volume VIII, issues 1 and 2, January-June and July-

December.

Millat, KM, Chowdhury, R, & Singha, EA 2012, Green Banking in Bangladesh Fostering Environmentally

Sustainable Inclusive Growth Process. Bangladesh Bank, Dhaka, Bangladesh. Accessed from:

http://www.bangladesh-bank.org/pub/special/greenbankingbd.pdf

Muhamat, AA, Jaafar, MN, & Azizan, NBA 2011, „An Empirical Study on Banks' Clients' Sensitivity towards the

Adoption of Arabic Terminology amongst Islamic Banks‟, International Journal of Islamic and Middle

Eastern Finance and Management, vol. 4, no. 4, pp. 343–354.

Münchow, S, Hummel, K, Jauerneck, D, & Scheschonck, K 2011, Geschäftspolitik von ethisch respektive sozial

orientierten Banken im Vergleich zu herkömmlichen renditeorientierten Banken (German, Translation:

Business Policy of Ethically Respectively Socially Oriented Banks in Comparison to Traditional Profit-

Oriented Banks). GRIN Verlag (German, Translation: GRIN Publication). Available at:

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

19

http://www.grin.com/de/e-book/184405/geschaeftspolitik-von-ethisch-respektive-sozial-orientierten-

banken-im

Murray, BC, Kelly, SJ, & Ganzi, JT 1997, „Review of Environmental Risk Management at Banking Institutions and

Potential Relevance of ISO 14000‟, Research Training Institute Working Paper, RTI Project Number 5774-

4, North Carolina.

Nath, V, Nayak, N, & Goel, A 2014, „Green Banking Practices – A Review‟, International Journal of Research in

Business Management (IMPACT Journal), vol. 2, no. 4, pp. 45-62.

Papastergiou, A, & Blanas, G 2011, „Sustainable Green Banking: The Case of Greece‟, Management of

International Business and Economics Systems (MIBES) Conference.

Pulicheri, V, & Rajashekhar, S 2013, „Green Banking Services for Sustainability‟, International Journal of Research

in Computer Application & Management, vol. 3, no. 11, pp. 132-135.

Rahman, A 2010, Financial Services at People’s Doorstep. Governor‟s Speech at the Bangladesh Bank, Accessed

on January 2014 at www.bangladesh-bank.org/governor/speech/may282010gs.pdf

Rahman, A 2013, Talking Points of Bangladesh Bank Governor. 3GF Round Table on Green Investment: A Road

Map to Scale Up Investments, Global Green Growth Forum, Denmark (October 22).

Rahman, A 2014, Bangladesh Bank Governor Speech on Socially Responsible Financing. Asian Institute of

Technology, March.

Rahman, MM, Ahsan, MA, Hossain, MM, & Hoq, MR 2013, „Green Banking Prospects in Bangladesh‟, Asian

Business Review, vol. 2, no. 4, pp. 59-63.

Rajput, N, Kaura, R, & Khanna, A 2013, „Indian Banking Sector towards a Sustainable Growth: A Paradigm Shift‟,

International Journal of Academic Research in Business and Social Sciences, vol. 3, no. 1, pp. 290-304.

Raluca, DO 2012, „Pathways to Sustainable Banking Management‟, The Journal of the Faculty of Economics, vol.

1, no. 2, pp. 545-550.

Rashid, M 2010, „Green Banking Comes to Focus‟, The Daily Star 17 September, Accessed: August 7, 2012 at

http://archive.thedailystar.net/newDesign/news-details.php?nid=154690

Rosenfeld, E, & Tchapi, PD 2007, Environmental Concerns and Banking Sector in Sweden. Master Degree Project

in Finance (Spring Term), School of Technology and Society, University of Skodev.

Sahoo, P, & Nayak, BP 2008, „Green Banking in India‟, Institute of Economic Growth Discussion Paper Series,

University of Delhi, no. 125, New Delhi, India.

Schmidheiny, S & Zorraquin, FJ 1996, Financing Change: The Financial Community, Eco-efficiency and

Sustainable Development. Mass: MIT Press, Cambridge.

Schultz, C 2010, „What is the Meaning of Green Banking?‟ Green Bank Report, vol. 2, pp. 127-131. Accessed on

May, 2013 from: http://greenbankreport.com/green-bank-deals/what-is-the-meaning-of-green-banking/

Setijawan, E 2014, Green Banking Initiative; Enhancing Banking Role to Support Sustainable Development

(Country: Indonesia). International Labor Organization, Retrieved in March 2014 from

http://apgreenjobs.ilo.org/resources/green-banking-initiative-enhancing-banking-role-to-support-

sustainable-development/at_download/file1

Singh, H & Singh, BP 2012, „An Effective & Resourceful Contribution of Green Banking towards Sustainability‟,

International Journal of Advances in Engineering Science and Technology, vol. 1, no. 2, pp. 41-45.

Starogiannis, D 2006, „What is Environmental Responsibility of Banks‟, UNEP FI Conference, June.

Stavros, D. 2005, Speech on European Commission meeting on Responsible for Environment. Brussels.

Thombre, KA 2011, „The New Face of Banking‟, Green Banking. Research Paper – Commerce, vol. 1, no. 2, pp. 1-

4.

Thompson, P and Cowton CJ 2004, „Bringing the Environment into Bank Lending: Implications for Environmental

Lending‟, British Accounting Review, vol. 36, pp. 197–218.

Ullah, MM 2013, „Green Banking in Bangladesh-A Comparative Analysis‟, World Review of Business Research,

vol. 3, no. 4, pp. 74 – 83.

Verma, MK 2012, „Green Banking: A Unique Corporate Social Responsibility of Indian Banks‟, International

Journal of Research in Commerce & Management, vol. 3, no. 1, pp. 110-114.

![Total Quality Management (TQM) Adoption in Bangladesh ... · forming cutting, making and trimming (CMT) activities [2] [10]. Therefore, this indus- ... Cost of poor quality of Bangladesh](https://static.fdocuments.in/doc/165x107/5f01fd8f7e708231d40208b3/total-quality-management-tqm-adoption-in-bangladesh-forming-cutting-making.jpg)