THE DECISION USEFULNESS OF CASH-FLOW STATEMENTS BY AUSTRALIAN REPORTING ENTITIES: SOME FURTHER...

19

British Accounting Review (1997) 29, 67–85 THE DECISION USEFULNESS OF CASH-FLOW STATEMENTS BY AUSTRALIAN REPORTING ENTITIES: SOME FURTHER EVIDENCE STEWART JONES* & JANEK RATNATUNGA* Monash University This paper investigates further the findings of a survey on cash-flow reporting presented by Jones et al. (1995). Their study both corroborated and extended on previous UK and US research which demonstrated the decision relevance and utility of the CFS (see for example Lee, 1981; McEnroe, 1989). However, their results were both preliminary and generic. No attempt was made in their paper to examine the combined effects of two or more variables on attitudes and ratings of the decision usefulness capabilities of the CFS by respondents. This analysis will clearly impact on the authors’ conclusions. By examining specific hypotheses and a priori relationships between variables, more rigorous, structured and refined tests of the decision usefulness functions of the CFS can be established. The results of the present study indicate that three independent variables were highly correlated with support for the CFS: firm size; the focus of a firm’s financial reporting responsibility; and the incidence of companies preparing CFSs prior to the introduction of AASB 1026. 1997 Academic Press Limited INTRODUCTION This paper extends the findings of a survey on cash-flow reporting by Jones et al. (1995), which examined the support for cash-flow reporting by respondents who were primarily preparers rather than users.(cf. Lee, 1981; McEnroe, 1989). The findings of Jones et al. indicated overwhelming support by Australian companies to the introduction of compulsory cash-flow statements (CFSs) and the essential requirements of AASB 1026, including some of its more stringent provisions (for example, the direct method of reporting cash flows). Their results also indicated that the CFS was perceived to be relevant across a wide range of decision contexts, including: liquidity and solvency evaluation; * Respectively Associate Professor and Professor at the Syme Department of Accounting, Monash University. The authors would like to thank a number of their colleagues and an anonymous referee for many useful comments on this paper. Correspondence should be addressed to: S. Jones, Syme Department of Accounting, Monash University, P.O. Box 197, Caulfield East, Membourne, Victoria 3145, Australia Received 18 April 1995; revised 16 December 1995; accepted 18 April 1996. 0890–8389/97/010067+19 $25.00/0 ba960037 1997 Academic Press Limited

-

Upload

stewart-jones -

Category

Documents

-

view

213 -

download

0

Transcript of THE DECISION USEFULNESS OF CASH-FLOW STATEMENTS BY AUSTRALIAN REPORTING ENTITIES: SOME FURTHER...

British Accounting Review (1997) 29, 67–85

THE DECISION USEFULNESS OF CASH-FLOWSTATEMENTS BY AUSTRALIAN REPORTING

ENTITIES: SOME FURTHER EVIDENCE

STEWART JONES∗ & JANEK RATNATUNGA∗Monash University

This paper investigates further the findings of a survey on cash-flow reporting presentedby Jones et al. (1995). Their study both corroborated and extended on previous UKand US research which demonstrated the decision relevance and utility of the CFS(see for example Lee, 1981; McEnroe, 1989). However, their results were bothpreliminary and generic. No attempt was made in their paper to examine the combinedeffects of two or more variables on attitudes and ratings of the decision usefulnesscapabilities of the CFS by respondents. This analysis will clearly impact on the authors’conclusions. By examining specific hypotheses and a priori relationships betweenvariables, more rigorous, structured and refined tests of the decision usefulnessfunctions of the CFS can be established. The results of the present study indicate thatthree independent variables were highly correlated with support for the CFS: firmsize; the focus of a firm’s financial reporting responsibility; and the incidence ofcompanies preparing CFSs prior to the introduction of AASB 1026.

1997 Academic Press Limited

INTRODUCTION

This paper extends the findings of a survey on cash-flow reporting by Jones etal. (1995),whichexaminedthesupport forcash-flowreportingbyrespondentswho were primarily preparers rather than users. (cf.Lee, 1981; McEnroe, 1989).The findings of Jones et al. indicated overwhelming support by Australiancompanies to the introduction of compulsory cash-flow statements (CFSs)and the essential requirements of AASB 1026, including some of its morestringent provisions (for example, the direct method of reporting cash flows).Their results also indicated that the CFS was perceived to be relevant acrossa wide range of decision contexts, including: liquidity and solvency evaluation;

∗Respectively Associate Professor and Professor at the Syme Department of Accounting, MonashUniversity. The authors would like to thank a number of their colleagues and an anonymous refereefor many useful comments on this paper.

Correspondence should be addressed to: S. Jones, Syme Department of Accounting, MonashUniversity, P.O. Box 197, Caulfield East, Membourne, Victoria 3145, Australia

Received 18 April 1995; revised 16 December 1995; accepted 18 April 1996.

0890–8389/97/010067+19 $25.00/0 ba960037 1997 Academic Press Limited

. . 68

monitoring and prediction functions; strategic decision making; and per-formance evaluation tasks. The CFS was also perceived to appeal to thedecision-making needs of a wide range of external and internal users.

This paper extends the analysis provided by Jones et al. (1995) by examiningthe decision usefulness of the CFS in the context of three formal hypothesesrelating to: firm size; focus of financial reporting responsibility; and voluntaryCFS preparation practices of respondent companies.

METHODOLOGY AND DEVELOPMENT OF RESEARCHHYPOTHESES

A brief summary of the methodology employed by Jones et al. (1995) is nowprovided. Subjects were 210 representatives of companies listed on the Aus-tralian Stock Exchange. Initially, questionnaires were forwarded to 500 ran-domly selected Australian listed public companies (n=(approximately) 1,200). The instrument developed by the authors comprised 124 questions.Most closed-ended questions were rated on 5-point Likert scales ranging from‘strongly agree’ to ‘strongly disagree’. Questions were grouped into five broadsections: respondent characteristics (e.g., occupation, reporting experience;main financial reporting responsibilities to external and internal users); com-pany characteristics (e.g., company size, industry membership); decision con-texts (i.e., respondents rated 20 decisions contexts that cash flow and fundsstatements were used for); and primary users of CFSs.

A covering letter outlined the purpose of the research and defined the CFSin the context of the definitions, format, and classifications adopted in theAustralian accounting standard AASB 1026 ‘Statement of Cash Flows’. Thesurvey achieved a response rate, after deducting 21 unusable responses, of42% (n=210). Furthermore, tests for non-response error indicated that therespondent group was likely to be representative of the non-respondent group.It should be noted, however, that the same study limitations reported in Joneset al. also apply to this study.1

The survey instrument elicited information from respondents on a numberof key background questions and issues. As previously mentioned, the threevariables above had particular relevance in shedding light on the decisionusefulness of the CFS. It is noted that other independent variables, for ex-ample, financial reporting experience of respondents, respondent occupationand industry background were not strongly correlated with respondent ratingsof the CFS.

The following discussion presents the development of hypotheses and therelevant literature.

The Impact of Firm Size

The study poses the following null hypothesis:Hypothesis 1:

- 69

There are no differences in respondent ratings of the decision usefulness of CFSsby small and large firms.

The significance of the firm size variable has been established in the or-ganization literature in respect of internal financial reporting and decisionfunctions of accounting information (see Emmanuel et al. 1991). Fur-thermore, contemporary positive research (e.g., Watts & Zimmerman, 1986,pp. 234–240, p. 245, pp. 248–256) have emphasized the significance of thefirm size variable in the external reporting arena. This literature is now brieflydiscussed.

Firm Size and the Organizational Control Literature. The organization literaturehas found important explanatory linkages between firm size2 and internalfunctions of accounting information, particularly in performance evaluation.Larger companies are characterized by, inter alia, a decentralized decision-making environment, disaggregation in management structures, differ-entiation in subunits, and bureacratization (Gordon & Miller, 1976, pp. 59–69). These features of organizational structure3 necessitate the developmentand maintenance of more sophisticated accounting information systems andoverall measures of performance to monitor, integrate and control a diverserange of activities. Emmanuel et al. (1991, p. 6, p. 31) observe that accountinginformation is usually the only source of quantitative information that cancombine the results of all the different parts of enterprise activities. Im-portantly, monetary indicators, particularly cash flow and profitability, arecritical because they represent the only way of assessing the results of diverseactivities in terms of a single dimension. These measures are also crucial forevaluating divisional performance in a manner that is compatible with overallcompany performance (Emmanuel et al., 1991, p. 279).4

Given developments in this literature, it was expected in the present resultsthat cash flow information would be rated relatively more highly for decisionmakingby largerfirms.This isowing to, inter alia, a greaterneed foraccountinginformation by larger firms in the monitoring and controlling of decentralizedand diverse activities, and in the assessment of these activities with overallmeasures of company performance.

Firm Size: Implications to Positive Research. The explanatory linkages betweenaccounting policy choices and firm size has been widely advocated in anextensive literature (see, as examples, Ball & Foster, 1981, p. 182; Brown,1994, p. 111). It is not suggested here that the correlations between firm sizeand support for the CFS can be directly linked to the political costs issue.However, the political processes literature indicates that accounting in-formation, such as CFSs, have a significantly greater impact on the resourceallocation decisions of users in respect of larger firms than for smaller firms(see Brown, 1994, pp. 109–110).5 Furthermore, larger firms report to andare, to some extent, at the mercy of a greater concentration of external users

. . 70

possessing potentially unlimited powers to influence the allocation of scarceresources (see Atiase et al. 1988).6 Given that financial statements have greatereconomic consequences for larger firms, larger firms are more likely to besusceptible to various assessments and evaluations of firm performance byexternal users. Hence, larger firms are more likely to be concerned with theinternal monitoring and control of a range of financial performance factors tomeet both the actual and perceived expectations of users. This will cause largerfirms to rely more heavily on internal and external accounting information.

To conclude, if the CFS possesses a high level of decision making relevance,the firm size hypothesis literature would predict that larger firms would ratethe relevance of CFSs more highly than smaller firms.

The Focus of an Entity’s Financial Reporting Responsibility

This study poses the following null hypothesis:

Hypothesis 2:Respondent ratings of the decision usefulness of the CFS are not positivelyassociated with any particular financial reporting focus to users.

An important test of the decision relevance of CFSs relates to the iden-tification of user groups. This notion has been widely advocated in the lit-erature. For instance, the theoretical foundation of Lee’s (1971, 1972a,1972b) support for CFSs is based almost exclusively on the principles of utilityand relevance to users.7

One approach adopted by Jones et al. in identifying potential users was torequest respondents to rate their perceptions of the decision relevance of theCFS for a range of different user groups. The authors report that the greatmajority of respondents perceived the CFS to have a high degree of decisionusefulness, particularly to bankers, managers and institutional investors.

However, this approach is limited because it is entirely perception drivenand does not attempt to establish any connection between ratings of the CFSand a respondent company’s actual users. A more tangible context for in-vestigating the existence of CFS users is to identify those users who are thefocus of an entity’s financial reporting responsibility (see Lee, 1981, p. 132).Jones et al. requested respondents to rate the following users, includingwhether they constituted the primary focus of their company’s financial re-porting responsibility: bankers, non-bank lenders, potential investors, share-holders, parent companies, executives/managers, or other users (e.g.,consumers, employers and suppliers). It is acknowledged that while this ap-proach also relies on respondent perceptions of user needs, a more reliableassessment of an entity’s actual users can nevertheless be made. Furthermore,this information allows us to investigate systematic associations in ratings ofthe decision usefulness of the CFS and a respondent’s reporting focus to users.For instance, will ratings of the decision usefulness of the CFS differ betweenentities who have lenders, as opposed to investors, as the primary focus of

- 71

their financial reporting responsibility? It was anticipated that if respondentsbelieved the CFS to be relevant to users, higher ratings of support for the CFSwould be correlated with entities having a financial reporting focus to a majoruser group. In particular, it was expected that relatively higher ratings of theCFS would be significantly correlated with firms who have lenders as theprimary focus of their reporting responsibility. The literature indicates thatwhile the CFS could be potentially useful to the decision making of diverseuser groups, lenders are consistently rated as the primary user in many studies(see as examples, Lee, 1981; McEnroe, 1989; Jones et al. 1995). Furthermore,it shouldbenotedthatone importantconclusionemanating fromtheempiricalliterature on the users of financial reports is that bankers and loan officers tendtobearelativelymoresophisticatedusergroup,andrelyoncompanyproducedfinancial statements more than other classes of users (see Griffin, 1987, pp.98ff).

It is also instructive to determine whether the CFS is relevant to the in-formation needs of a range of potential user groups. Arguably, the more usersthe CFS satisfies, the more overall relevance the document has for decisionmaking. For instance, if firms differ in their financial reporting focus to users,and yet all rate the decision usefulness of the CFS comparably, then thedecision relevance of the document can be more clearly established.

The Impact of Voluntary CFS Preparation Practices

The study poses the following null hypothesis:

Hypothesis 3There are no significant differences in ratings of the decision usefulness of CFSsby firms having a prior history of preparing CFSs for internal reporting purposesversus firms having no such prior history.

Inferences about the relevance of the CFS for decision making can also bemade with respect to voluntary cash-flow preparation practices of respondentcompanies. Jones et al. reported that a majority of companies were preparingCFSs for internal purposes prior to the introduction of mandatory AASB 1026requirements in 1992. These results imply that the CFS could have, inter alia,a high degree of relevance for internal control and decision purposes withincompanies. Consistent with the agency literature (cf. Watts & Zimmerman,1986) it is assumed that it would not be cost/benefit-effective for firms to incurthe expense of preparing additional internal accounting information havinglittle value for decision making or control purposes. In the absence of anyother satisfactory rationale for voluntary practices, a relationship betweenrespondent ratings of the CFS and voluntary preparation practices was an-ticipated. It was expected that firms who have had a history of preparing aCFS would rate relatively more highly its relevance for various forms ofinternal decisions. Afterall, entities that have voluntarily prepared cash-flowdata, particularly over a number of years, have had greater opportunity to trial

. . 72

the information and are more likely to have greater experience in its use andinterpretation for decision making. This provides another opportunity to testa further dimension of the decision relevance of the CFS.

RESULTS AND DISCUSSION

This section of the paper presents the results relating to the hypotheses out-lined in Section Two. Data were analysed using SPSS for Windows: Release6.0 (Norusis, 1993). While parametric statistics are reported in the body ofthis paper, it is noteworthy that non-parametric statistics for all hypothesistests were consistent with those of parametric equivalents.

Hypothesis 1: Firm Size

The firm size hypothesis was tested by dividing respondent companies intothree categories based on total asset size:8 The first group had a total assetsize ranging between $A0–$A100 million. The second group had total assetsranging between $A101 million–$A600 million, and the third group includedall entities having a total asset size greater than $A601 million.9 For the pur-poses of analysis and ease of description, the first group of entities were des-ignated as small firms, the second as medium-sized firms, and the third groupwere designated as large firms. It is recognised that there is no necessaryagreement in the literature over what constitutes a small, medium or largefirm. These comparisons are essentially arbitrary and must be made in relativeterms. However, the firm size classifications above are justified on the groundsthat the medium total asset size of firms across the entire sample of firmsreported by Jones et al. ranged between $A101–$A300 million. It was con-sidered appropriate to classify entities with less than$A100 million and greaterthan $A600 million as small and large relative to the medium asset size of thepopulation of listed Australian firms.

Application of the one-way ANOVA statistic revealed that respondent rat-ings of the CFS were strongly correlated with firm size. For instance, whencompared to medium- and small-sized firms, large firms tended to rate theCFS as being more relevant across a range of decision contexts. Similar resultswere found when medium size firms were compared with small firms, a findingoften established throughout this section of the results.

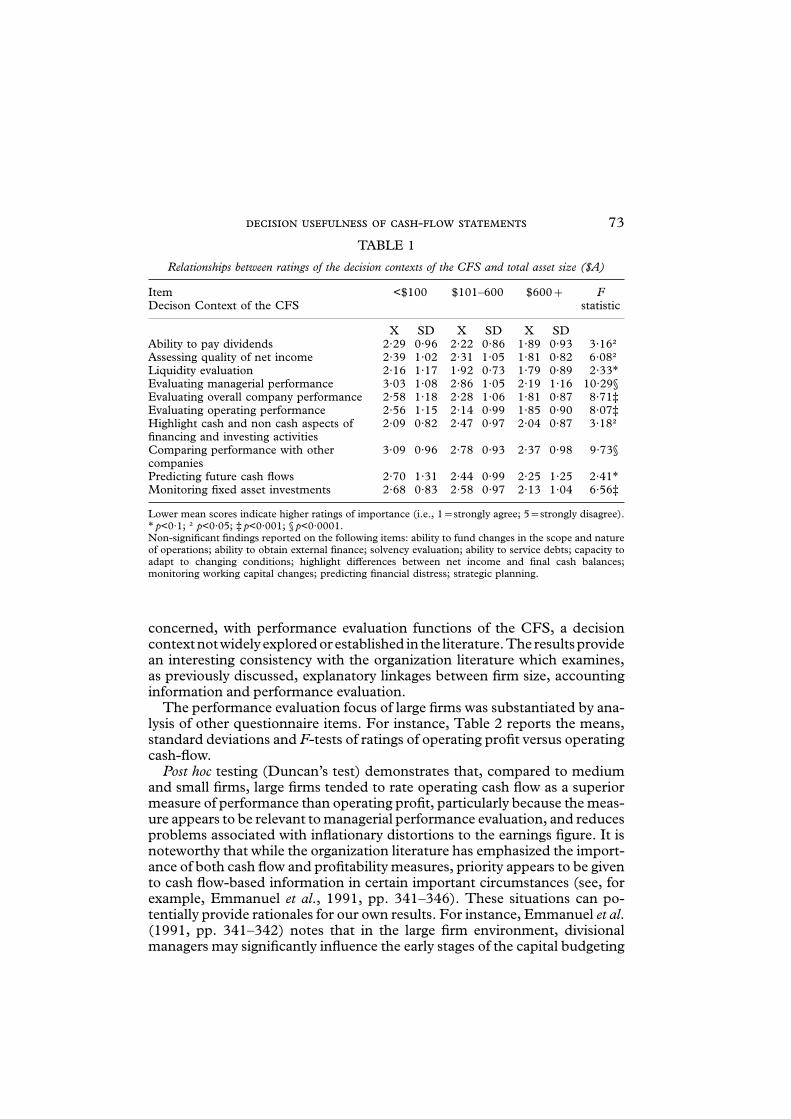

Table 1 displays the means, standard deviations and F-tests of respondentratings of the decision contexts of the CFS and the firm size variable.

The omnibus F-test reveals a number of statistically significant differencesbetween firm size and respondent ratings of decision usefulness functions ofthe CFS. It is noteworthy that the cash-flow literature has tended to stress theimportance of liquidity and solvency evaluation as a primary function of theCFS (see Heath, 1978; Jones et al. 1995). However, the ANOVA resultsreported in Table 1 reveal that large firms appear to be equally, if not more

- 73

TABLE 1

Relationships between ratings of the decision contexts of the CFS and total asset size ($A)

Item <$100 $101–600 $600+ FDecison Context of the CFS statistic

X SD X SD X SDAbility to pay dividends 2·29 0·96 2·22 0·86 1·89 0·93 3·16†Assessing quality of net income 2·39 1·02 2·31 1·05 1·81 0·82 6·08†Liquidity evaluation 2·16 1·17 1·92 0·73 1·79 0·89 2·33∗Evaluating managerial performance 3·03 1·08 2·86 1·05 2·19 1·16 10·29§Evaluating overall company performance 2·58 1·18 2·28 1·06 1·81 0·87 8·71‡Evaluating operating performance 2·56 1·15 2·14 0·99 1·85 0·90 8·07‡Highlight cash and non cash aspects of 2·09 0·82 2·47 0·97 2·04 0·87 3·18†financing and investing activitiesComparing performance with other 3·09 0·96 2·78 0·93 2·37 0·98 9·73§companiesPredicting future cash flows 2·70 1·31 2·44 0·99 2·25 1·25 2·41∗Monitoring fixed asset investments 2·68 0·83 2·58 0·97 2·13 1·04 6·56‡

Lower mean scores indicate higher ratings of importance (i.e., 1=strongly agree; 5=strongly disagree).∗ p<0·1; † p<0·05; ‡ p<0·001; § p<0·0001.Non-significant findings reported on the following items: ability to fund changes in the scope and natureof operations; ability to obtain external finance; solvency evaluation; ability to service debts; capacity toadapt to changing conditions; highlight differences between net income and final cash balances;monitoring working capital changes; predicting financial distress; strategic planning.

concerned, with performance evaluation functions of the CFS, a decisioncontextnotwidelyexploredorestablished in the literature.The resultsprovidean interesting consistency with the organization literature which examines,as previously discussed, explanatory linkages between firm size, accountinginformation and performance evaluation.

The performance evaluation focus of large firms was substantiated by ana-lysis of other questionnaire items. For instance, Table 2 reports the means,standard deviations and F-tests of ratings of operating profit versus operatingcash-flow.

Post hoc testing (Duncan’s test) demonstrates that, compared to mediumand small firms, large firms tended to rate operating cash flow as a superiormeasure of performance than operating profit, particularly because the meas-ure appears to be relevant to managerial performance evaluation, and reducesproblems associated with inflationary distortions to the earnings figure. It isnoteworthy that while the organization literature has emphasized the import-ance of both cash flow and profitability measures, priority appears to be givento cash flow-based information in certain important circumstances (see, forexample, Emmanuel et al., 1991, pp. 341–346). These situations can po-tentially provide rationales for our own results. For instance, Emmanuel et al.(1991, pp. 341–342) notes that in the large firm environment, divisionalmanagers may significantly influence the early stages of the capital budgeting

. . 74

TABLE 2

Relationships between ratings of operating cash flow vs operating profit (as a performance measure)and total asset size ($A)

Item <$100 $101–$600 $600+ FRelevance of Operating Cash Flow Vs statisticOperating Profit

X SD X SD X SDIt is a more reliable measure of performance 3·59 1·06 3·21 1·12 2·68 1·41 2·41∗because it avoids estimates for accrual anddeferralsIt avoids problems of changing price levels 3·47 0·94 3·24 0·88 2·77 0·94 2·88†which can distort reported earningsIt reduces problems associated with earnings 3·59 0·87 3·26 0·83 2·86 0·91 2·94†variabilityIs a more relevant measure of managerial 3·47 0·87 3·32 1·07 2·54 1·27 4·03†performance than operating profit

Lower mean scores indicate higher ratings of importance (i.e., 1=strongly agree; 5=strongly disagree).∗ p<0·1; † p<0·05. Non-significant findings were reported on the following two items: operating cashflow was not considered superior to operating profit in assessments of overall company performance.Nor was operating cash flow considered a more reliable measure of operating performance.

TABLE 3

Relationships between ratings of users of cash-flow statements and total asset size ($A)

Item <$100 $101–$600 $600+ FUsers of the CFS statistic

X SD X SD X SDManagers 2·26 1·34 1·98 0·89 1·68 0·83 3·83†Bankers 2·03 1·25 1·68 0·76 1·53 0·99 3·73†Investors 2·66 0·84 2·35 0·98 1·89 0·81 3·78†Shareholders 2·66 1·14 2·60 1·24 2·25 0·81 2·46∗Employees 3·62 0·96 3·34 1·03 3·13 0·76 5·22†

Lower mean scores indicate higher ratings of importance (i.e., 1=strongly agree; 5=strongly disagree).∗ p<0·1; † p<0·05. Non-significant findings were reported on the following users: institutional investors,consumers and suppliers.

process. They argue (1991, p. 342) that when this potential to influenceexists, cash flow information can provide a more reliable basis for performanceevaluation. This, the authors claim, will reduce the likelihood of managerssubmitting investment projects incongruent with the firm’s best interests.

Emmanuel et al. (1991,p.342)alsoobserve that cashflowmeasuresbecomeparticularly relevant in the large firm environment during times of inflation,an argument again consistent with results reported in Table 2.10

The firm size variable featured in other relevant areas of the results. Whencompared to medium and small firms, large firms rated the CFS as havingmore overall relevance to perceived users of the CFS. Table 3 displays the

- 75

means, standard deviations and F-tests of respondent ratings of CFS usersand the firm size variable.

Post hoc testing (Duncan’s test) indicates that, when compared to mediumand small firms, large firms rated more highly managers, bankers, investorsand employees as significant users of the CFS. Furthermore, Table 3 indicatesthat shareholders were tending towards significance. These results indicatethat large firms consider, whether this is actual or perceived, CFS informationto be relatively more useful to a number of user groups. It is plausible that theseresults share some important consistencies with the size hypothesis literatureexpounded in the positive literature (Watts & Zimmerman, 1986). For in-stance, this literature presumes that large firms generally have a significantlygreater concentration of users, who rely on financial and other informationprovided by firms for decision making.11 The results reported in Table 3 couldbe so interpreted, not unreasonably, that large firms rate the different classesof users of the CFS more highly than small firms because of greater potentialeconomic consequences associated with its preparation and disclosure.

A consistent pattern in the results on firm size can also be observed onseveral other questionnaire items. For instance, relative to medium and smallfirms, large firms rated operating cash flow as a more important overall meas-ure of an entity’s economic condition and future prospects than operatingprofit [F(2, 204),= 4·66, p=0·001]. Large companies also rated more highlythe significance of operating cash flow relative to other cash-flow measures,including cash flow from investment and net change in cash balance [F(2,204)= 4·14, p=0·002].

Furthermore, compared to medium and small firms, large firms tended torate the CFS considerably more highly for decision making than the fundsstatement. This is because the document was perceived to be: more com-parable between companies [F(2, 203)=4·56, p=0·01]; easier to understand[F(2, 204)=2·19, p=0·021]; easier to interpret [F(2, 203)=2·61, p=0·043]and satisfies the information requirements of a wider range of users [F(2,203)=2·71, p=0·03].

In conclusion, the results of this section establish firm size as a significantdiscriminating variable explaining variation in ratings of the CFS by re-spondent companies. As was previously mentioned, the size hypothesis lit-eraturewouldpredict thataccounting informationhasa relativelymorecriticalrole to play in numerous aspects of the internal and external decision-makingenvironment of larger firms. Many of the findings have consistencies withimportant elements of this literature.

Hypothesis 2: Focus of Financial Reporting Responsibility

It will be recalled that the Jones et al. survey instrument requested respondentsto rate the relevance of the CFS to a number of users, and whether these usersconstituted the primary focus of their financial reporting responsibility. In

. . 76

TABLE 4

Ratings of the decision usefulness of cash-flow statements by firms having a primary financialreporting focus to lenders

Item Lenders OtherDecision Contexts of the CFS

X SD X SDAbility to fund changes in the scope and 1·61† 0·90 1·91 0·95nature of operationsAbility to obtain external finance 1·69† 0·88 2·04 0·95Solvency evaluation 1·82† 0·85 2·14 0·96Ability to service debts 1·75† 0·86 2·10 0·99Assessing quality of net income 2·06∗ 0·95 2·36 1·07Liquidity evaluation 1·82‡ 0·82 2·42 1·31Evaluating managerial performance 2·46§ 1·10 3·17 1·20Evaluating overall company performance 1·99§ 0·92 2·75 1·31Evaluating operating performance 1·97§ 0·86 2·75 1·31Comparing performance with other 2·54§ 1·00 3·13 0·84companiesUseful for predicting future cash flows 2·36† 1·19 2·87 1·33Monitoring fixed assets 2·40∗ 0·99 2·67 0·83

Footnotes in this table denote significance levels of t-test results. Lower mean scores indicate higherratings of importance (i.e., 1=strongly agree; 5=strongly disagree). ∗ p<0·1; † p<0·05; ‡ p<0·001;§ p<0·0001.Non-significant findings were reported on the following decision contexts: ability to pay dividends;capacity to adapt to changing conditions; highlight differences between net income and final cashbalances; highlight cash and non cash aspects of an entity’s investing and financing activities; monitorchanges in financial position; predicting financial distress; strategic planning; monitoring working capitalchanges.

order to facilitate the testing of Hypothesis 2, the initial data collected by Joneset al. had to be collapsed and re-coded.12

The t statistic revealed that the highest ratings of the decision usefulness ofthe CFS was by respondent companies who had either bankers or non-banklenders as the primary focus of their financial reporting responsibility. Thisfinding is broadly consistent with the relevant literature outlined in ‘Method-ology andDevelopment of ResearchHypotheses’. However,many statisticallysignificant results were also observed where respondent companies had eitherparent companies, managers or investors as the major focus of their reportingresponsibility. The results revealed that firms whose major reporting re-sponsibilities were to shareholders had fairly minimal impact on ratings of theCFS by respondents.13

Table 4 displays the means, standard deviations and t-test results of ratingsof the decision contexts of the CFS by firms having a primary reporting focusto lenders.

It is noteworthy that the results reported in Table 4 had very few differenceswith firms having a primary reporting focus to bankers. Because the results are

- 77

very similar, only the results on lenders are reported. These findings clearlyindicate that the relevance of CFSs is not confined to a particular group ofcreditors, such as bankers.

It is noteworthy that Table 4 indicates that, in addition to liquidity andsolvency factors, performance evaluation again surfaces as a relevant decisioncontext in the analysis. While the literature tends to closely associate the lenderfocus with liquidity and solvency evaluation (see Griffin, 1987, p. 100), thepresent results indicate thatAustralianfirmsperceive lenders tohaveabroadereconomic interest in CFS information.

Firmshavingamajorreportingresponsibility tobanksandnon-bank lendersalso rated relatively more highly the relevance of the CFS versus the fundsstatement fordecisionmaking.Thisagain indicates that theCFShasparticularrelevance in a lending context. In particular, the CFS was considered (usingthe example of lenders): more understandable [F(2,203)=2·53, p=0·07);easier to interpret [F(2,203),=4·12, p=0·003]; has less problems with keyterms [F(2,203),=2·18, p=0·011] and provides greater comparability be-tween companies [F(2,204),=2·88, p=0·023].

With respect to the decision contexts of the CFS, firms having a majorreporting focus to either investors, managers or parent companies displayedimportant but differing results when contrasted with the bank and non-banklender focus. In this case, the highest ratings of the decision usefulness of theCFS tended to be concentrated almost entirely on performance evaluationfactors. Table 5 reports the means, standard deviations and t test results offirms having investors as a major reporting focus. Again, because the resultsfor managers and parent companies are very similar to Table 5, they are notdisplayed here.

The results in Tables 4 and 5 signify, among other things, that the CFS isperceived by firms to be especially relevant to a range of user groups onparticular decision items. Furthermore, the decision focus among these usersis not perceived to be dramatically different. The only substantive differenceis that the interest of bankers and non-bank lenders in the CFS appears to bemore broadly based than other users. Essential similarities in the results wereconfirmed in other areas of the analysis. For instance, firms having a majorreporting focus to either bankers, non-bank lenders, investors, managers orparent companies all displayed strong support for reporting cash flows underthe direct method. Using the example of lenders, Table 6 reports the means,standard deviations and t-test results of ratings of the direct method of re-porting cash flows.The results in Table 6 indicate that while the direct methodwas considered more complex, costly and time consuming, the method wasperceived by these firms to: help users understand cash-flow data; facilitatecash-flow analysis; reflect accepted commercial practice; and have a sounderconceptual basis. These results imply that the direct method is perceived byrespondents to satisfy the information requirements of diverse potential users.

Furthermore, operating cash flow was rated as a superior performancemeasure than operating profit by companies having a major reporting focus

. . 78

TABLE 5

Ratings of the decision usefulness of cash-flow statements by firms having a primary financialreporting focus to investors

Item Investors OtherDecision Contexts of the CFS

X SD X SDLiquidity evaluation 1·89§ 0·78 2·68 1·58Evaluating managerial performance 2·62‡ 1·11 3·38 1·29Evaluating overall company performance 2·18§ 1·02 3·08 1·37Evaluating operating performance 2·11§ 0·95 3·10 1·37Capacity to adapt to changing conditions 2·15∗ 1·09 2·49 0·96Comparing performance with other 2·58‡ 1·08 3·08 0·80companiesUseful for predicting future cash flows 2·39§ 1·14 3·20 1·49Helps monitor changes in financial 1·78∗ 0·80 1·99 0·83positionMonitoring fixed assets 2·21∗ 1·01 2·65 0·53

Footnotes in this table denote significance levels of t-test results. Lower mean scores indicate higherratings of importance (i.e., 1=strongly agree; 5=strongly disagree). ∗ p<0·01; † p<0·05; ‡ p<0·001;§ p<0·0001.Non-significant findings were reported on the following decision contexts: ability to fund changes inthe scope and nature of operations; ability to obtain external finance; solvency evaluation; ability to paydividends; ability to service debts; assessing quality of net income; highlight differences between netincome and final cash balances; highlight cash and non-cash aspects of an entity’s investing and financingactivities; predicting financial distress; strategic planning; monitoring working capital changes.

to either bankers, non-bank lenders, investors or managers. In particular,operating cash flow was seen as superior because (using the example of in-vestors): it avoids problems of changing price levels which can distort reportedearnings (t=−2·34, p=0·02); and is a more reliable measure of operatingperformance (t=−2·27, p=0·025).

Inconclusion, the resultsof this section indicate strongassociationsbetweenan entity’s financial reporting focus and ratings of several questionnaire itemsrelevant to establishing the decision usefulness of the CFS. While relativelyhigher ratings of the CFS tended to be associated with a reporting focus toeither bankers or non-bank lenders, several other potential user groups alsofeatured reasonably prominently in different areas of the results. These find-ings are broadly consistent with the initial findings of Jones et al. of whomreported that respondents perceived wide support for the CFS by a variety ofuser groups.

Hypothesis 3: Voluntary CFS Preparation Practices

Jones et al. reported that 57% (n=120) of respondents had been preparing aCFS, for internal reporting purposes, for an average period of 10 years priorto the release of AASB 1026 in 1992. For the purpose of testing Hypothesis

- 79

TABLE 6

Ratings of the direct method by firms having a primary financial reporting focus to lenders

Item Lenders OtherSupport for the Direct Method

X SD X SDDirect method helps users understand 2·33† 0·70 2·58 0·61cash flow dataDirect method facilities cash flow analysis 2·28† 0·66 2·57 0·66Direct method is a better indicator of 2·63∗ 0·75 2·83 0·62solvencyDirect method reflects accepted 2·56‡ 0·64 2·94 0·78commercial practiceDirect method has a sounder conceptual 2·39† 0·62 2·59 0·61basisDirect method is more complex 2·85† 0·82 2·56 1·04Direct method does not emphasise 2·84† 0·68 3·12 0·75changes in components of working capitaluseful for predicting future cash flows

Footnotes in this table denote significance levels of t-test results. Lower mean scores indicate higherratings of importance (i.e., 1=strongly agree; 5=strongly disagree). ∗ p<0·1; † p<0·05; ‡ p<0·001.Non-significant findings were reported on the following questionnaire items: direct method conformsto internal reporting practice and direct method is more costly than indirect method.

3, survey responsesweredivided into twomaingroups: thosecompanieswhichhad never prepared a CFS prior to the requirements of AASB 1026, and thosecompanies which had been preparing CFSs for up to 5 years prior to therelease of AASB 1026. Statistical testing (t-tests) revealed that the strongestsupport for CFSs came from firms who had already been preparing CFSsprior to the requirements of AASB 1026.14 A large number of statisticallysignificant results were found. Table 7 reports the means, standard deviationsand t-test results of this analysis.

Importantly, firms with a history of preparing CFSs invariably rated theCFS more highly on a wide range of decision contexts, including liquidityand solvency factors, performance evaluation factors, and monitoring andprediction decision contexts.

These results indicate that the CFS is likely to have particular relevance forinternal decision making and control functions within firms. This conclusionis reinforced considering that respondent companies who were already pre-paringCFSsprior toregulationoftenranked internalusersas theprimary focusof their reportingresponsibility (i.e.,parentcompanies,managers/executives).

Respondent companies having a history of preparing CFSs prior to theintroduction of AASB 1026 also rated more highly the relevance of CFSs toexternal users when compared with other firms. Table 8 reports the means,standard deviations and t-tests of these results.

. . 80

TABLE 7

Decision usefulness ratings by firms who prepared CFSs prior to the requirements of AASB 1026

Item Up to 5 years Not at allDecision Contexts of the CFS

X SD X SDAbility to fund changes in the scope and nature of 1·51§ 0·76 2·11 1·06operationsAbility to obtain external finance 1·63§ 0·77 2·15 1·04Solvency evaluation 1·76§ 0·79 2·24 1·05Ability to pay dividends 2·03† 0·86 2·43 1·02Ability to service debts 1·75‡ 0·85 2·18 0·99Assessing quality of net income 2·15∗ 0·97 2·39 1·03Liquidity evaluation 1·76§ 0·81 2·41 1·23Evaluating managerial performance 2·45§ 1·02 3·29 1·13Evaluating overall company performance 1·97§ 0·87 2·89 1·23Evaluating operating performance 1·98§ 0·85 2·78 1·24Capacity to adapt changing conditions 2·35∗ 0·96 2·59 1·04Highlight cash and non-cash aspects of an entity’s 2·23∗ 0·88 2·03 0·84investing and financing activities during a periodComparing performance with other companies 2·71† 1·00 3·09 0·95Useful for predicting future cash flows 2·16§ 1·12 3·08 1·22Helps monitor changes in financial position 1·86† 0·76 2·10 0·88Predicting financial distress 1·87‡ 0·86 2·32 1·06Useful for strategic planning 2·02† 0·87 2·40 1·05Monitoring fixed assets 2·29§ 0·89 2·84 0·91

Footnotes in this table denote significance levels of t-test results. Lower mean scores indicate higherratings of importance (i.e., 1=strongly agree; 5=strongly disagree). ∗ p<0·1; † p<0·05; ‡ p<0·001;§ p<0·0001.Non-significant findings were reported on the following decision contexts: highlight differences betweennet income and final cash balances and monitoring capital changes.

TABLE 8

Ratings of the users of CFSs by firms who prepared CFSs prior to the requirements of AASB 1026

Item Up to 5 years Not at allUsers of the CFS

X SD X SDManagers 1·73§ 0·80 2·58 1·41Bankers 1·54§ 0·79 2·27 1·36Institutional investors 2·07‡ 0·96 2·59 1·31Shareholders 2·32§ 0·91 2·87 1·25Employees 3·29† 0·92 3·69 0·94Consumers 3·21† 0·89 3·88 0·86Suppliers 3·08§ 1·05 3·63 1·03

Footnotes in this table denote significance levels of t-test results. Lower mean scores indicate higherratings of importance (i.e., 1=strongly disagree). ∗p<0·1; †p<0·05; ‡p<0·001; §p<0·0001.

- 81

Many other results were consistent with differential ratings of the CFS byfirms having a prior history of preparing CFSs and those that did not. Forinstance, it is noteworthy that firms having a history of preparing CFSs tendedto rate the direct method of reporting cash flows more highly than other firms.In particular, the direct method was seen to: facilitate cash-flow analysis (t=−3·47, p=0·001); have a sounder conceptual basis (t=−3·33, p=0·001);and help users to understand cash-flow data (t=−1·56, p=0·041). Fur-thermore,firmshavingahistoryofpreparingCFSsrated relativelymorehighlythe relevance of the CFS versus the funds statement for decision making.15

The above results were analysed more closely by establishing whether rat-ings of the CFS was a function of the specific number of years firms had beenpreparing CFSs prior to regulatory mandates. Firms that had been preparingCFSs for 1 year prior to the release of AASB 1026 were compared againstfirms who had been preparing CFSs for 2–5 years and for 5–10 years prior toreleaseofAASB1026. It isplausible thatfirmswhichhavevoluntarilypreparedCFSs fora longerperiodof timewillhavegreaterexposureand,hence,possiblybemoreconvincedabout the relevanceof the information fordecisionmaking.The results were consistent with this proposition.16

CONCLUSIONS

The study by Jones et al. (1995) is relevant to the cash-flow literature because itindicates an accelerating international trend, particularly in Australia, towardsthe growing significance of the CFS. Their paper indicated strong support forCFS regulations by Australian reporting entities. However, the relevance oftheir findings is considerably strengthened by the establishment of formalhypotheses which can potentially explain systematic variations in survey re-sponses, as well as test relevant propositions available in the literature. In anattempt to address limitations in their results, as well as extend on their generalfindings, the decision usefulness functions of the CFS was tested in the contextof three specific variables: firm size; financial reporting focus to users; andvoluntary CFS preparation practices. Each of the hypotheses based on thesevariables have been justified as a relevant test of the decision usefulness ofCFSs.

Statistical procedures reveal that the null hypotheses established in‘Methodology and Development of Research Hypotheses’ cannot be reas-onably retained in any of the three instances. The results demonstrate thatsupport for the CFS are strongly correlated with the above variables, par-ticularly in respondent ratings of: performance evaluation and liquidity andsolvency decision contexts of CFSs; the different users of CFSs; the relativeusefulness of CFSs vs funds statements; the direct method of reporting cashflows; and the relative merits of operating cash flow versus operating profit asa performance measure.

The firm size variable, which featured prominently in the present results,

. . 82

has particular significance in contemporary accounting literature. This vari-able has been controlled and operationalized in numerous studies to test amyriad of propositions and relationships pertinent to assessing the relevanceof accounting information and systems on decision making (Watts & Zimm-erman, 1986).

The focus of financial reporting responsibility has special significance forgenerating inferences about a firm’s actual CFS users. The associations es-tablished in this study between ratings of the CFS and a firm’s financial re-porting focus indicates that the CFS has much potential relevance to theinformation requirements of the major user groups.

Finally, firms having a prior history of preparing CFSs consistently ratedthe document as more relevant for decision making across a wide range ofquestionnaire items. These results imply that support for the CFS was afunction of firms having more experience and/or exposure to the preparationand use of cash-flow information. These results again provide evidence thatthe CFS has relevance across a number of internal and external decisionmaking contexts.

While the findings pose no notable inconsistencies to Jones et al. they con-siderably reinforce and extend their basic conclusions concerning the growingrelevance of the CFS in the Australian reporting environment.

N

1. Furthermore, is noted that the homogeneity of the questionnaire and the degree towhich all items measured one factor was established using Cronbach’s alpha. The veryhigh reliability level reported in the study indicates that the instrument was likely to bemeasuring a single factor (Cohen, Montague, Nathanson & Swerdlik, 1988).

2. Obviously, firm size has no obvious interpretation in its own right. Firm size is importantinsofar as it stands as a proxy for other distinguishing features of firms. For instance,Watts & Zimmerman (1986) use firm size as a proxy for greater political and economicconsequences associated with the disclosure practices and measurement choices ofcompanies. In the organization literature, which primarily focuses on the internalfunctions of accounting information, size is a proxy for differences in organizationalstructure, such as decentralization and divisionalization, which can impact on therelevance, design and sophistication of accounting information systems.

3. It is acknowledged, however, that this paper provides no explicit tests of whether theseorganisational features of large firms are present in our own sample. The relationshipsare largely assumed.

4. Merchant (1985, pp.17–18) observes that results control (such as cash flow andprofitability measures) are not only consistent with, but necessary for the implementationof decentralized organisations with largely autonomous division centres. In fact, asnoted by Cave (1980) and Emmanuel et al. (1991), organizational growth is usuallyaccompanied by the introduction of formal accounting measures for planning capitalinvestment and for monitoring the overall financial performance of the firm and itsmultivarious divisions.

5. There is some convincing literature to support this view. For instance, Atiase, Bamber& Freeman (1988) found that large firms are more closely monitored by investors thansmall firms. This observation is implicit in other research findings. Grant (1980) and

- 83

Atiase (1985) observed that voluntary disclosure practices, particularly pre-disclosureof earnings announcements, were significantly greater for larger firms. Freeman (1992)found that investors use accrual and cash flow information to set stock prices in largefirms, but not in small firms (Freeman, 1992, p. 144). Furthermore, the impact onshare prices tends to be greater with the unexpected earnings announcements of largercompanies (see Brown, 1994, p. 44n). It can be concluded that financial disclosuresappear to have relatively greater economic consequences for larger firms.

6. Evidence that larger companies report to a wider range of users has already beensupported in the initial survey results of Jones et al. (1995).

7. Lee (1974, 1978, 1979, 1981) demonstrated the relevance of CFSs to a number ofspecific user groups, including creditors, bankers, employees, managers, and governmentbodies. It is noteworthy that the survey findings of McEnroe (1989) are consistent withthose of Lee (1981).

8. Of course, total asset size is not the only size measure that can be used. Sales turnover,market shares and employee numbers are other possible measures. While the literaturehas not discriminated between the relative merits of different size measures, it is clearthat total assets is the most commonly used measure in the size hypothesis literature(see Watts & Zimmerman, 1986).

9. It should be noted that the survey instrument of Jones et al. (1995) requested respondentsto indicate the size of their firms in terms of a range of values. It was anticipated thatrespondents would not know (or have the information at hand) the exact asset size oftheir companies.

10. The potential superiority of operating cash flows (versus profitability measures) duringtimes of inflation has been described in a number of other decision contexts (see Lee,1993, pp.72ff). Another factor to consider is that the exclusion of arbitrary cost allocationsunder cash flow based information systems provide better approximations of opportunitycost values, and hence better approximations of true economic value (see Lee, 1993,pp. 72–74). Emmanuel et al. (1991, p. 346) note that, in contrast to profitabilitymeasures, cash flow information gives divisional managers ‘better signals as to whatlevel of operations to aim for, which products to produce . . . that will result in activitiescloser to maximising economic value than may be obtained using AIS based on accrualincome’.

11. Afterall, agency relationships between different classes of users, particularly shareholders,managers and lenders, grow more pronounced in the large firm environment (see Watts& Zimmerman, 1986, pp. 180–191; Griffin, 1987). Indeed, there are close relationshipsimplicit in agency theory between firm size, accounting information and the existenceof users groups. For example, a pivotal empirical finding of agency research (see Watts& Zimmerman, 1986, p. 245) is that larger firms tend to choose accounting alternativeswhich reduce current earnings. These practices are intrinsically linked and motivatedby firm perceptions of different users and their decision reactions to financial disclosure(see Watts & Zimmerman, 1986, pp. 180ff).

12. When collecting information on the major financial reporting responsibilities of re-spondents, Jones et al. initially used a five-point Likert scale ranging from ‘stronglyagree’ to ‘strongly disagree’. This complicated the analysis of differences in financialreporting responsibilities, particularly where respondents indicated more than one usergroup as the focus of their reporting responsibility. To simplify the task, the ‘stronglyagree’ and ‘agree’ categories were collapsed into a single ‘yes’ category, and the ‘neutral’,‘disagree’ and ‘strongly disagree’ categories were collapsed into a single ‘no’ category.Where respondents indicated more than one user group, their responses were analysedseparately for each user group.

13. It should be noted that only a very small number of respondent companies indicatedthat the focus of their financial reporting responsibility was to ‘other’ groups (e.g.,consumers). Hence, analysis was not conducted on this variable.

14. Similar results were reported when firms with more than five years experience of

. . 84

preparing CFSs were compared with firms having no prior history of preparing CFSs.15. In particular, the CFS was seen to: provide a greater degree of comparability between

companies (t=−3·28, p=0·001); satisfy the information needs of a wider range ofexternal and internal users [t=−2·07, p=0·039; t=−2·73, p=0·007]; has less problemswith terminology [t=−3·55, p=0·0000]; and key terms [t=4·37, p=0·0000]; and ismore relevant to planning and decision making by companies [t=−3·77, p=0·0000]

16. Compared to firms who had been preparing CFSs for 1 year only or between 2–5 years,it was found that firms who had prepared CFSs between 5–10 years rated significantlymore highly the relevance of the CFS for a large number of liquidity and performanceevaluation tasks. Again, these results tend to confirm that the CFS has decision relevanceextending beyond the traditional focus of liquidity and solvency evaluation (cf. Heath,1978). More importantly, the results tend to reinforce a relationship between a firm’sprior exposure and/or experience in the preparation and use of CFSs and higher ratingsof the relevance of the information for decision making.

R

Atiase, R.K. (1985), ‘Predisclosure information, firm capitalization, and security pricebehavior around earnings announcements’, Journal of Accounting Research, 23 (1), pp.21–36.

Atiase, R.K., Bamber, L. and Freeman, R. (1988), ‘Accounting disclosures based on companysize: regulations and capital markets evidence’ Accounting Horizons, 2 (1), pp. 18–26.

Ball, R. and Foster, G. (1982), ‘Corporate financial reporting: a methodological review ofempirical research’, Journal of Accounting Research, 20 (Supplement), pp. 161–234

Brown, P. (1994), ‘Capital markets-based research in accounting: an introduction’, AccountingResearch Methodology Monograph No. 1, Coopers & Lybrand, Australia.

Cave, R.E. (1980), ‘Industrial organisation, corporate strategy and structure’, Journal ofEconomic Literature, March, pp. 64–92.

Cohen, R.J., Montague, P., Nathanson, L.S. & Swerdlik, M.E. (1988). Psychological Testing:An Introduction to Tests and Measurement California: Mayfield.

Grant, E.B. (1980), ‘Market implications of differential amounts of interim information’,Journal of Accounting Research, 18 (1), pp. 255–268

Emmanuel, C., Otley, D., & Merchant, K., (1991). Accounting for Management ControlLondon: Chapman and Hall.

Freeman, R.N. and Tse, S. ‘An earnings prediction approach to examining intercompanyinformation transfers’, Journal of Accounting and Economics, 15 (4), pp. 509–523.

Gordon, L.A., & Miller, D. (1976). ‘A contingency framework for the design of accountinginformation systems’, Accounting, Organisations and Society, 1, pp. 59–70.

Griffin, P. (1987) Usefulness to Investors and Creditors of Information Provided by FinancialReporting: A Review of Empirical Accounting Research (Connecticut: FASB).

Heath, L.C. (1978), ‘Financial reporting and the evaluation of solvency’, Accounting ResearchMonograph 3, American Institute of Certified Public Accountants.

Jones, S., Romano, C., & Smyrnios, K. ‘An evaluation of the decision usefulness of cashflow statements by Australian reporting entities’, Accounting and Business Research, Spring,25 (98), pp. 115–129.

Lee, T.A. (1971). ‘Goodwill—an example of will-o-the-wisp accounting’, Accounting andBusiness Research, Autumn, pp. 318–328.

Lee, T.A. (1972a). ‘The relevance of accounting information including cash flows’, TheAccountants’ Magazine, January, pp. 30–34.

Lee, T.A. (1972b). ‘A case for cash flow reporting’, Journal of Business Finance, Summer,pp. 27–36.

- 85

Lee, T.A. (1974). ‘Enterprise income: survival or decline and fall?’, Accounting and BusinessResearch, Summer, pp. 178–192.

Lee, T.A. (1978), ‘The cash flow accounting alternative for corporate financial reporting’,in van Dam, C (ed.), Trends in Managerial and Financial Accounting, Martinus Nijhoff,pp. 63–84.

Lee, T.A. (1979), ‘The simplicity and the complexity of accounting’, in Sterling, R.R. andThomas, A.L (eds.), Accounting for a Simplified Firm, Scholars Book Co., pp. 35–55.

Lee, T.A. (1981), ‘A survey of accountants’ opinions on cash flow reporting’, Abacus 17(2), pp. 130–143.

Lee, T.A. (ed.) (1993). Cash Flow Reporting: A Recent History of an Accounting Practice (NewYork: Garland Publishing)

McEnroe, J. (1989). ‘Cash flow accounting revisited: a note on a partial replication of thelee study’, Abacus, 25 (1), pp. 56–60.

Merchant, K.A. (1985), ‘Budgeting and the propensity to create budgetary stock’, Accounting,Organisations and Society, 10 (2), pp. 201–210.

Norusis, M.J. (1993). SPSS for Windows: Advanced Statistics Release 6.0 (Chicago: SPSSInc.)

Watts, R.L. and Zimmerman, J.L. (1978). ‘Towards a positive theory of the determinantsof accounting standards’ The Accounting Review, 53 (1), pp. 112–134.

Watts, R.L. and Zimmerman, J.L. (1986). Positive, Accounting Theory, (New Jersey: Prentice-Hall).

Williamson, O.E., (1970), Corporate Control and Business Behaviour (London: Prentice-Hall).