The Cost of Capital, Corporation Finance, and the Theory of Investment: Comments

29

COURSE TITLE: SEMINAR IN FINANCE COURSE CODE: MPH 622 Presentation on The cost of capital, corporation finance, and the Theory of Investment: Comment by: David Durand Massachusetts Institute of Technology Published in: The American Economic Review, Vol. XLIX, No. 4, September 1959, pp. 639-55. 16 th April, 2011

-

Upload

sudarshan-kadariya -

Category

Economy & Finance

-

view

306 -

download

3

Transcript of The Cost of Capital, Corporation Finance, and the Theory of Investment: Comments

COURSE TITLE: SEMINAR IN FINANCE COURSE CODE: MPH 622

Presentation on

The cost of capital, corporation finance, and the Theory of Investment: Comment

by:

David DurandMassachusetts Institute of Technology

Published in: The American Economic Review, Vol. XLIX, No. 4, September 1959, pp. 639-55.

16th April, 2011

Presentation Outline The cost of capital, corporation finance, and the Theory of

Investment

Prof. David Durand

The Cost of Capital, Corporation Finance, and the Theory of Investment: Reply

Franco Modigliani and Metron H. Miller

The Cost of Capital, Corporation Finance, and the Theory of Investment: Comment

Dowson E. Brewer and Jocab B. Michaelsen

The Cost of Capital, Corporation Finance, and the Theory of Investment: Reply

Franco Modigliani and Metron H. Miller

Background

MM 1958 have articulated three propositions that contradict widely accepted beliefs against traditional view of capital structure.

The Proposition I is the basic, which states, in a perfect market, the total value of all outstanding securities of a firm is independent of its capital structure.

Back…..

Assumptions for Proposition I

i) Arbitrage is possible between securities in an equivalent return class

ii) A firm falls into none of the standard ownership categories but is a sort of hybrid

iii) Exclude risk, and iv) A long-run equilibrium in which stocks sell at

book value. Comment: unrealistic

Objective: To expose the difficulties of justifying MM proposition I.

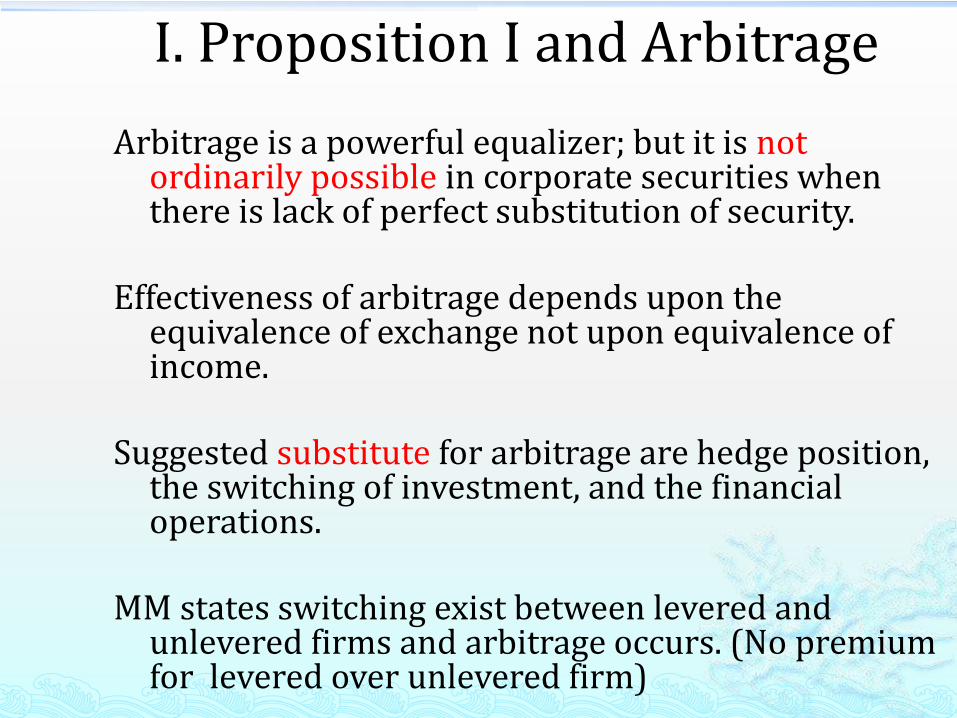

Arbitrage is a powerful equalizer; but it is not ordinarily possible in corporate securities when there is lack of perfect substitution of security.

Effectiveness of arbitrage depends upon the equivalence of exchange not upon equivalence of income.

Suggested substitute for arbitrage are hedge position, the switching of investment, and the financial operations.

MM states switching exist between levered and unlevered firms and arbitrage occurs. (No premium for levered over unlevered firm)

I. Proposition I and Arbitrage

1950 1959

S&P bond Return 2.60% 4.30%

Dividend Yield 5.35% 3.90%

Earnign Yield 8.10% 5.40%

Opportunity Bond finance Sell bonds

Investors have the opportunity of borrowing on personal account. But, only a limited opportunity for most investors.

In practice, those who seek to reduce capital cost by adjusting capital structure must ascertain conditions in the current market, and act rapidly to exploit them.

II. Market Imperfections: Restrictions on Margin Buying

Produced comments on the grounds

MM visualize a highly competitive market

If market deviates it provides an opportunity for profit but whom?

Bond issue requires time to arrange

Why discriminate against the corporations?

Legal issues on margin buying. Margin buying permitted small investors but restrict many of the largest investors.

III. The Risks of Margin Buying

MM’s no additional risk of switching does not apply in a world of high risk.

All bonds are assumed to yield a constant income regardless of the issuer but which is also doubtful.

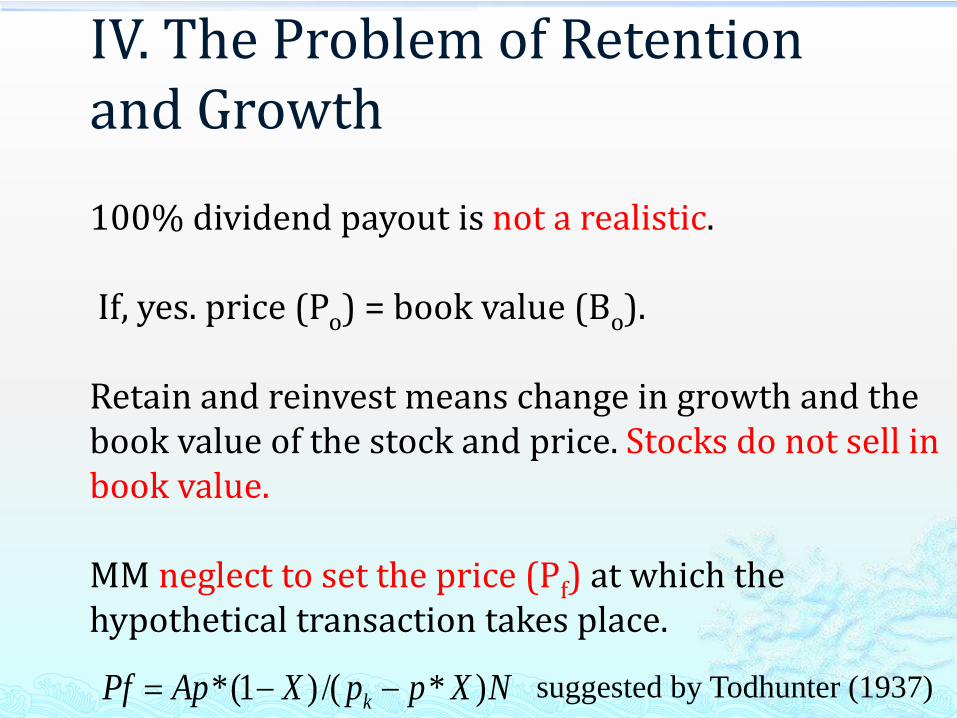

IV. The Problem of Retention and Growth

100% dividend payout is not a realistic.

If, yes. price (Po) = book value (Bo).

Retain and reinvest means change in growth and the book value of the stock and price. Stocks do not sell in book value.

MM neglect to set the price (Pf) at which the hypothetical transaction takes place.

NXppXApPf k )*/()1(* suggested by Todhunter (1937)

The regression results in table-1 showed that the successive reductions in the RSS as addition of earning, and dividend payout ratio.

Table-2 another regression price/book on earning/book and dividend/earning shows that the reduction in RSS is significant.

Based on these results, it is concluded that dividend policy exerts an influence on stock prices and the cost of capital.

V. Problems of Empirical Analysis The empirical analysis on capital structure encounters bunch of obstacles like

Lack of reliable and pertinent data like price quotations, dividend rates, earnings

Difficulties of assembling a sample of corporations.

Type of analysis

Homogenous stock groups, etc.

The cost of capital, corporation finance, and the Theory of Investment: Reply

by:

Franco Modigliani and Metron H. Miller

Carnegie Institute of Technology

Published in: The American Economic Review, Vol. XLIX, No. 4, September 1959, pp. 655-59.

Reply

Reply on comments by David Durand and J.R. Ross.

J.R. Ross - MM apologized for their failure to adjust explicitly the definition of a “class” when introducing debt.

D. Durand - MM believed that further elaboration of the model and approach on four issues.

Reply

I. The Ability of Investors and Speculators to Enforce Proposition I:

MM argued for the comments on arbitrage is semantic, and describes the features of arbitrage - the simultaneous purchase and sale and perfect substitutes.

Further defined the use of other words like “switch”, “hedge”, “home-made”, “imperfections” and “noise” and paved the way to support original paper.

Reply

II. The Role of Financial Operations by Corporations:

Durand raised the issue on Proposition I and regarding MM’s support for the market imperfection.

MM defend that it offers no support whatever for the traditional U-shaped cost-of-capital curve (traditional view).

MM clarify on the queries like “gained by whom? How?” as “he means by the cost of capital” and the process described with examples.

Imperfections - MM concluded that the interpretations of Durand are different from them.

Reply

III. Dividends, Growth Opportunities and the Theory of Share Prices:

Based on the issued raised by Durand MM tried to sketch out the theory of share prices and stated that formal proof will be postponed to a forthcoming paper.

Reply

IV. The Effect of Dividends on Stock Prices: The Empirical Findings and Their Interpretation:

As MM only sketch out the pricing theory and formal proof on the theory of prices remains for the next paper.

MM propose the original conclusion i.e. in a world of perfect markets and rational behavior, firm's dividend policy, other things equal, will have no effect either on the value of the firm or its cost of capital.

The cost of capital, corporation finance, and the Theory of Investment:

Comment

by:

Dowson E. Brewer and Jocab B. MichaelsenUniversity of California

Published in: The American Economic Review, Vol. LV, No. 3, June 1965, pp. 516-24.

Comment

Optimum capital structure exists (traditional view) vs. arbitrage operations will make the market value of the firm independent of its capital structure (MM 1958).

The purpose of the study is to show that the implications of the relationship between i) The expected yield on a firm's shares and its debt-

equity ratio; and

ii) The weighted average of the expected yields on a firm's shares and bonds and its debt-equity ratio.

I. Implications of the Alternative Views in

the Absence of Corporate Income Taxes

All MM propositions are based on Proposition I. However, MM failed to recognize that Proposition I also implies the bond-yield function(r = Pk - (i -pk)S/D).

In the absence of taxes, the MM’s a linear horizontal relationship whereas the traditional view implies a U-shaped

II. Implications of the Alternative Views in

the Presence of the Corporate Income

Tax

In the presence of the corporate income tax, MM distinguish alternative views in two reasons.

First, the relationship between the weighted average cost of capital and debt-equity ratios are similar for both views under the tax.

Second, and perhaps more important, the tax provides an incentive for rational managers to use debt.

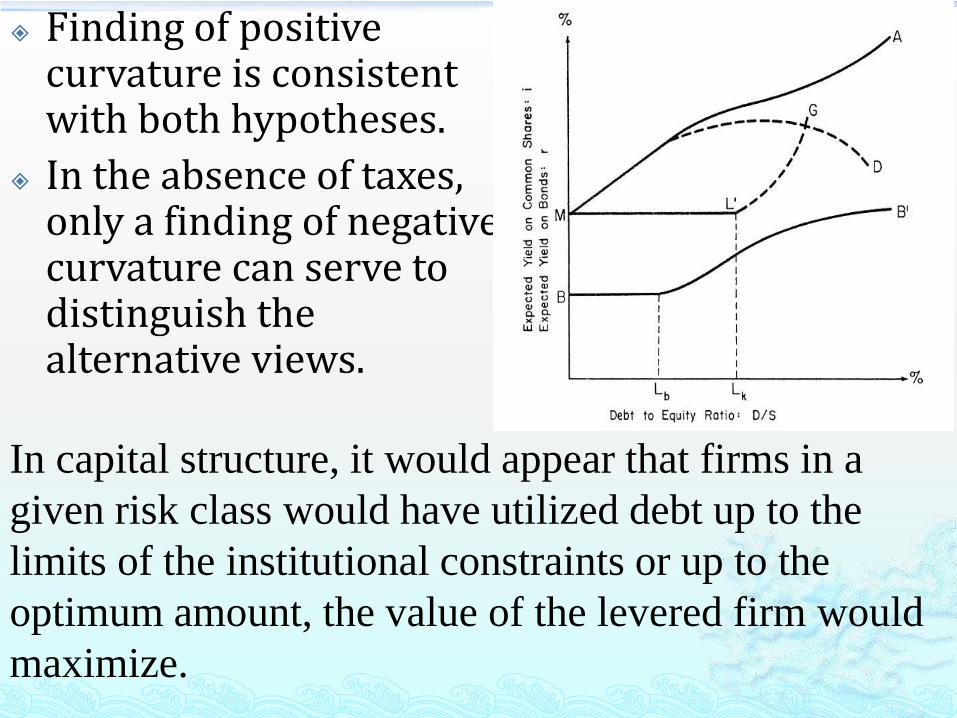

Finding of positive curvature is consistent with both hypotheses.

In the absence of taxes, only a finding of negative curvature can serve to distinguish the alternative views.

In capital structure, it would appear that firms in a

given risk class would have utilized debt up to the

limits of the institutional constraints or up to the

optimum amount, the value of the levered firm would

maximize.

The cost of capital, corporation finance, and the Theory of Investment: Reply

by:

Franco Modigliani and Merton H. MillerMassachusetts Institute of Technology and University of Chicago

Published in: The American Economic Review, Vol. LV, No. 3, June 1965, pp. 524-27.

Reply

Issue 1

Brewer and Michaelson (BM)’s comments are mostly in favor of MM’s work. Except,

No precise definition of “risk aversion.”

MM defended that risk aversion is implied by pk >riskless r, and the concept of risk aversion may perhaps have some heuristic value.

Reply

Issue 2

MM convinced that BM have sound ground in derivation of shape of the share-yield curve, given or bond-yield curve.

However, puzzled as to why they think their discussion of the curvature properties?

Reply

Issue 3

MM defend on measure of the value of the tax saving on debt. They blamed commenter's for misunderstanding of what is meant by the “certainty” of the tax deduction for interest payment.

With this justification, MM stated that their assumption is far better than that implied by Brewer and Michaelsen’s.

Overall Conclusion

Despite the rigorous analysis and presentation of the original articles as well as comments forwarded by different researchers, It seems that MM’s work is very much strong and wholeheartedly appreciable.

The issues raised as comments may be beyond the scope of MM’s study but they provide a platform to discuss the issues and complexities in pioneer work.

Thank you.