CHAPTER 9 MUTUAL FUNDS (UNIT TRUSTS, OEICS, INVESTMENT TRUSTS)

Upload

agustin-edgingtonCategory

view

215download

0

The Coordination Gap—Ordering Relationships in Multi-Participant Trusts

Stephen E. Parker, Managing Director, J.P.Morgan Private Bank404.926.2504, [email protected]

February 3, 2011

©2007-10 Duncan Associates A&C, P.C. and Anita M. Sarafa All rights reserved.

2

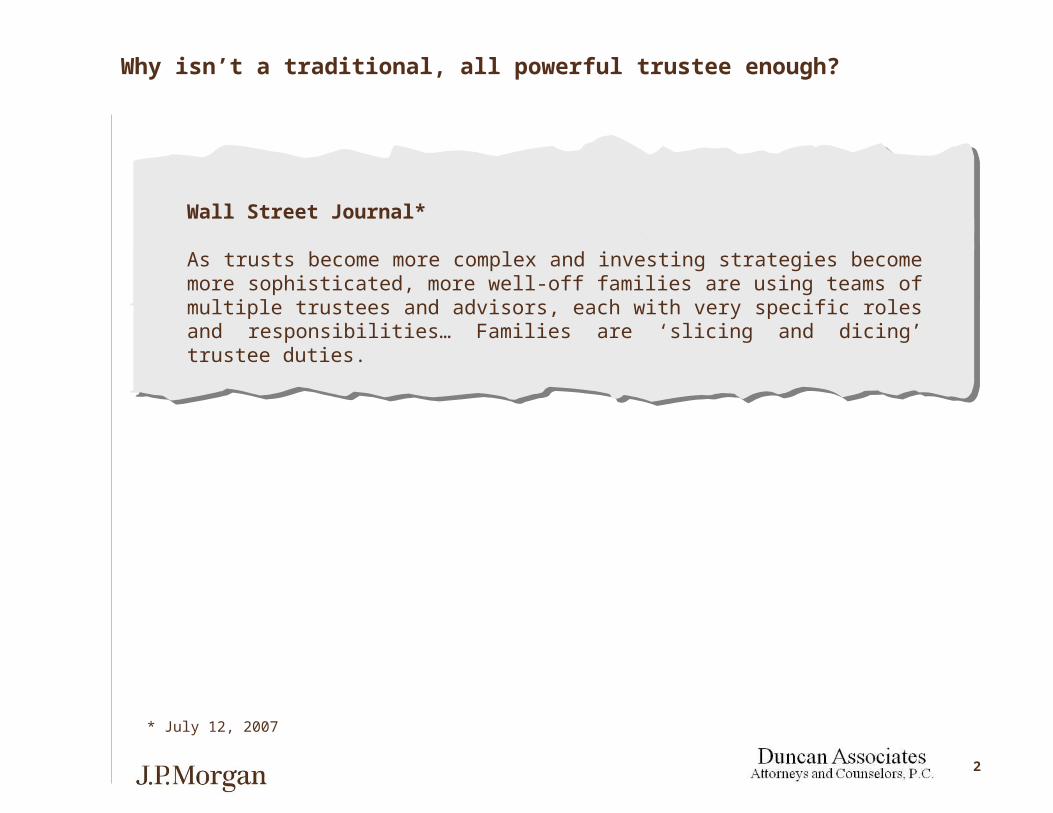

Why isn’t a traditional, all powerful trustee enough?

Wall Street Journal*

As trusts become more complex and investing strategies become more sophisticated, more well-off families are using teams of multiple trustees and advisors, each with very specific roles and responsibilities… Families are ‘slicing and dicing’ trustee duties.

* July 12, 2007

3

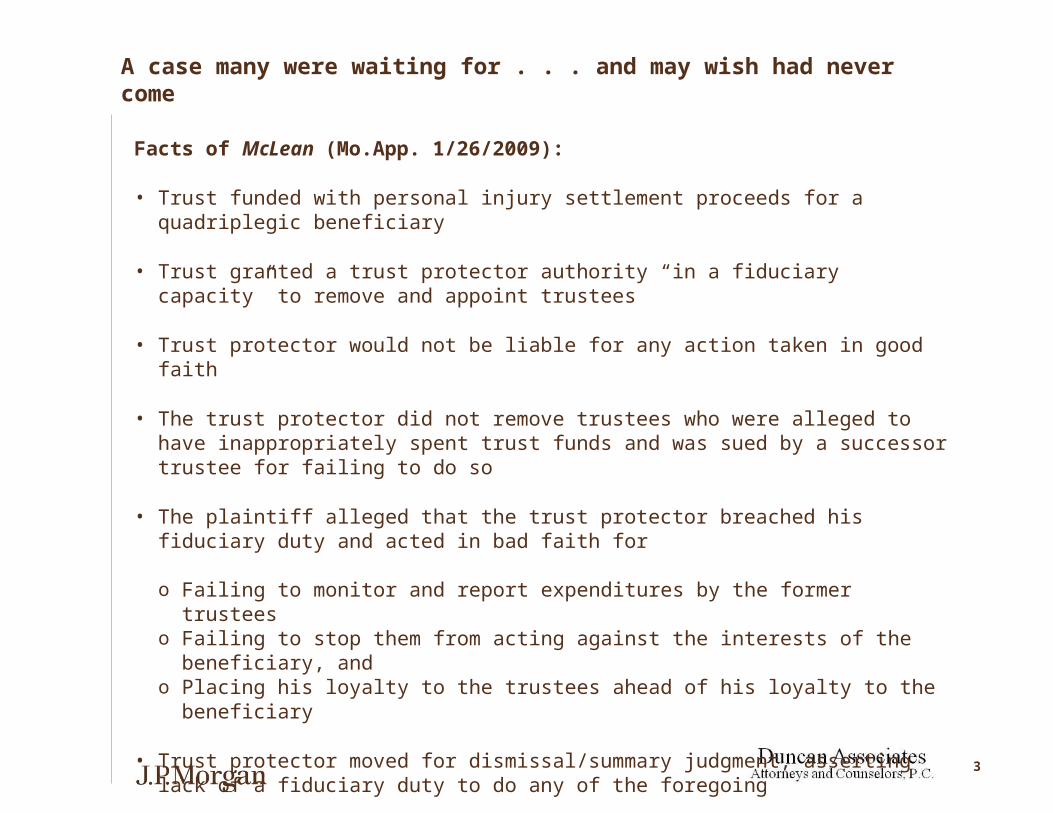

Facts of McLean (Mo.App. 1/26/2009):

• Trust funded with personal injury settlement proceeds for a quadriplegic beneficiary

• Trust granted a trust protector authority “in a fiduciary capacity” to remove and appoint trustees

• Trust protector would not be liable for any action taken in good faith

• The trust protector did not remove trustees who were alleged to have inappropriately spent trust funds and was sued by a successor trustee for failing to do so

• The plaintiff alleged that the trust protector breached his fiduciary duty and acted in bad faith for

o Failing to monitor and report expenditures by the former trusteeso Failing to stop them from acting against the interests of the beneficiary, ando Placing his loyalty to the trustees ahead of his loyalty to the beneficiary

• Trust protector moved for dismissal/summary judgment, asserting lack of a fiduciary duty to do any of the foregoing

• Trial court granted summary judgment for the trust protector

A case many were waiting for . . . and may wish had never come

4

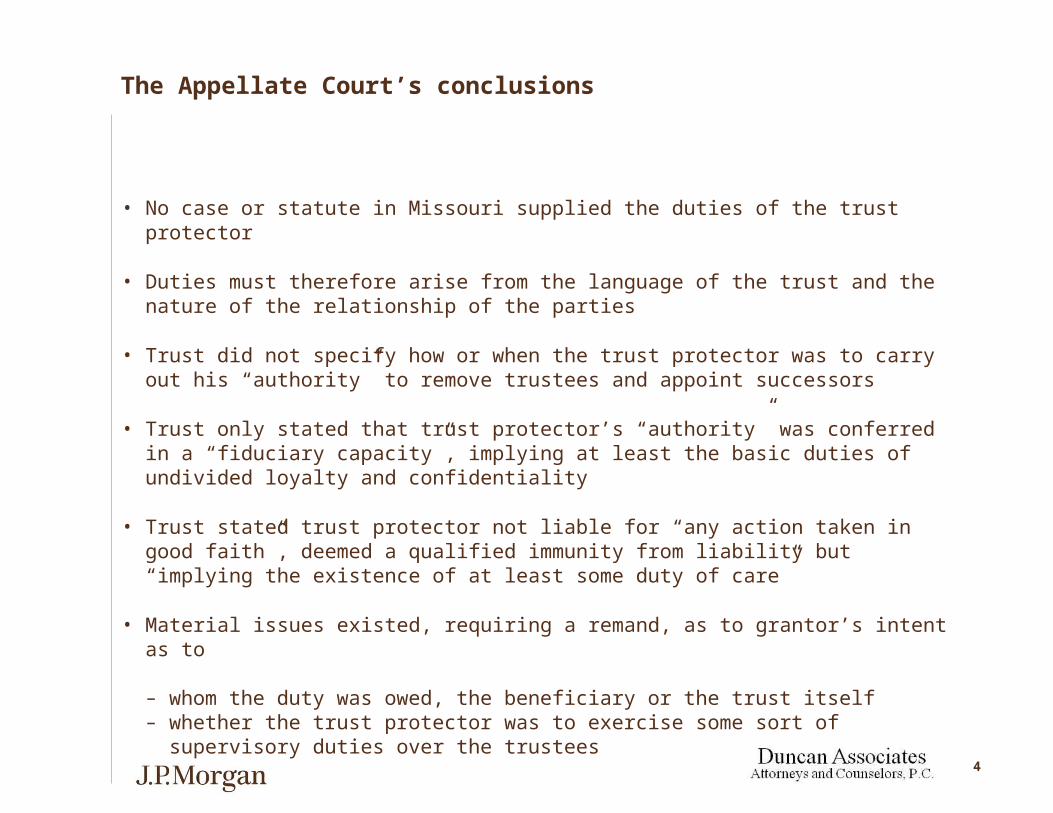

• No case or statute in Missouri supplied the duties of the trust protector

• Duties must therefore arise from the language of the trust and the nature of the relationship of the parties

• Trust did not specify how or when the trust protector was to carry out his “authority” to remove trustees and appoint successors

• Trust only stated that trust protector’s “authority” was conferred in a “fiduciary capacity”, implying at least the basic duties of undivided loyalty and confidentiality

• Trust stated trust protector not liable for “any action taken in good faith”, deemed a qualified immunity from liability but “implying the existence of at least some duty of care”

• Material issues existed, requiring a remand, as to grantor’s intent as to – whom the duty was owed, the beneficiary or the trust itself– whether the trust protector was to exercise some sort of supervisory duties

over the trustees

The Appellate Court’s conclusions

5

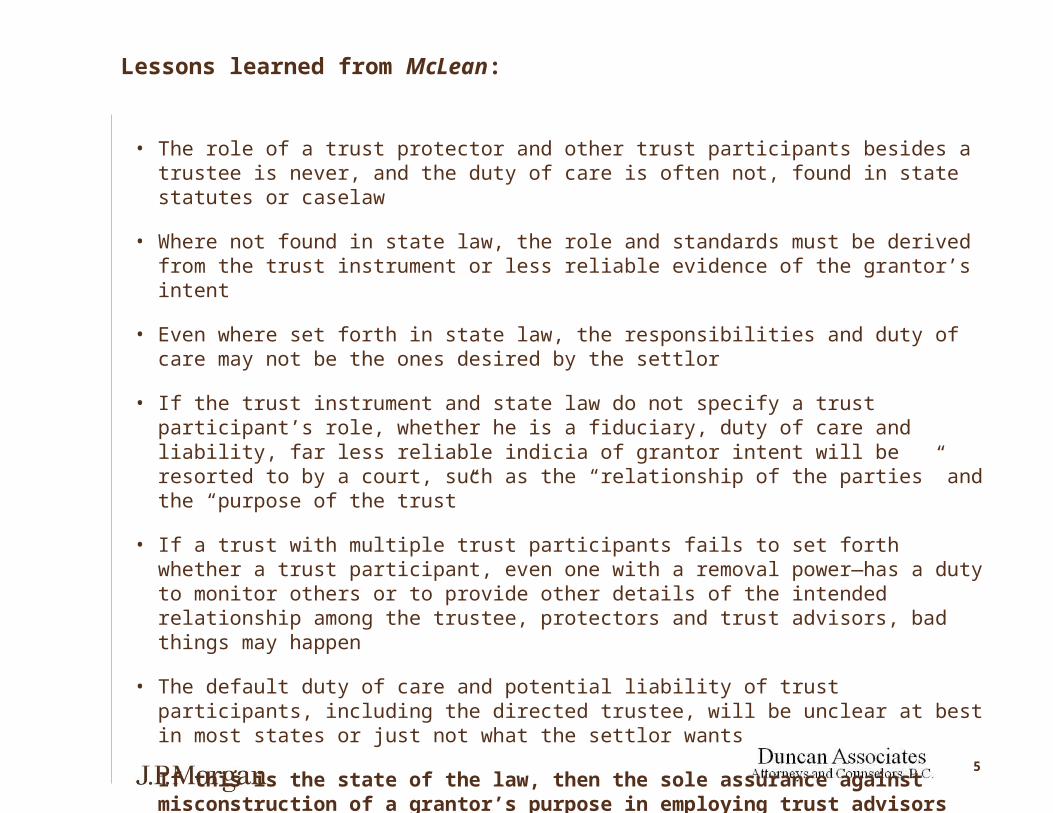

• The role of a trust protector and other trust participants besides a trustee is never, and the duty of care is often not, found in state statutes or caselaw

• Where not found in state law, the role and standards must be derived from the trust instrument or less reliable evidence of the grantor’s intent

• Even where set forth in state law, the responsibilities and duty of care may not be the ones desired by the settlor

• If the trust instrument and state law do not specify a trust participant’s role, whether he is a fiduciary, duty of care and liability, far less reliable indicia of grantor intent will be resorted to by a court, such as the “relationship of the parties” and the “purpose of the trust”

• If a trust with multiple trust participants fails to set forth whether a trust participant, even one with a removal power—has a duty to monitor others or to provide other details of the intended relationship among the trustee, protectors and trust advisors, bad things may happen

• The default duty of care and potential liability of trust participants, including the directed trustee, will be unclear at best in most states or just not what the settlor wants

If this is the state of the law, then the sole assurance against misconstruction of a grantor’s purpose in employing trust advisors and trust protectors is a clear understanding of that purpose that can only be derived from carefully drafted trust provisions governing all trust participants' actions and duties.

Lessons learned from McLean:

6

Why the trend toward multi-participant trusts?

• Desire to assign specialized roles for fiduciaries has a long history (co-trustee legacy)

• Modern trust statutes grant trustees more authority and flexibility

• Sophisticated investment and financial management may require multiple experts

• Many families desire to retain significant decision-making functions

• Trustee risk management may encourage bifurcating trustee role

• Use of dynasty and other long-term trusts requires adaptability

• Emergence of dynamic, flexible trust laws in leading states

• Philosopher King shortage

• Control the family business, family office, private trust company or portfolio companies with an advisor committee or family council instead of a single individual or institutional trustee

7

Our goals . . .

• Review the problems that can arise with multiple trust participants

• Identify the characteristics of a manageable multi-participant trust

• Review the current state of the law, focusing on uncertainties and gaps

• Demonstrate the essential role of knowledgeable and careful draftsmanship

• Provide drafting suggestions for creating a manageable, surprise-free multi-participant trust

8

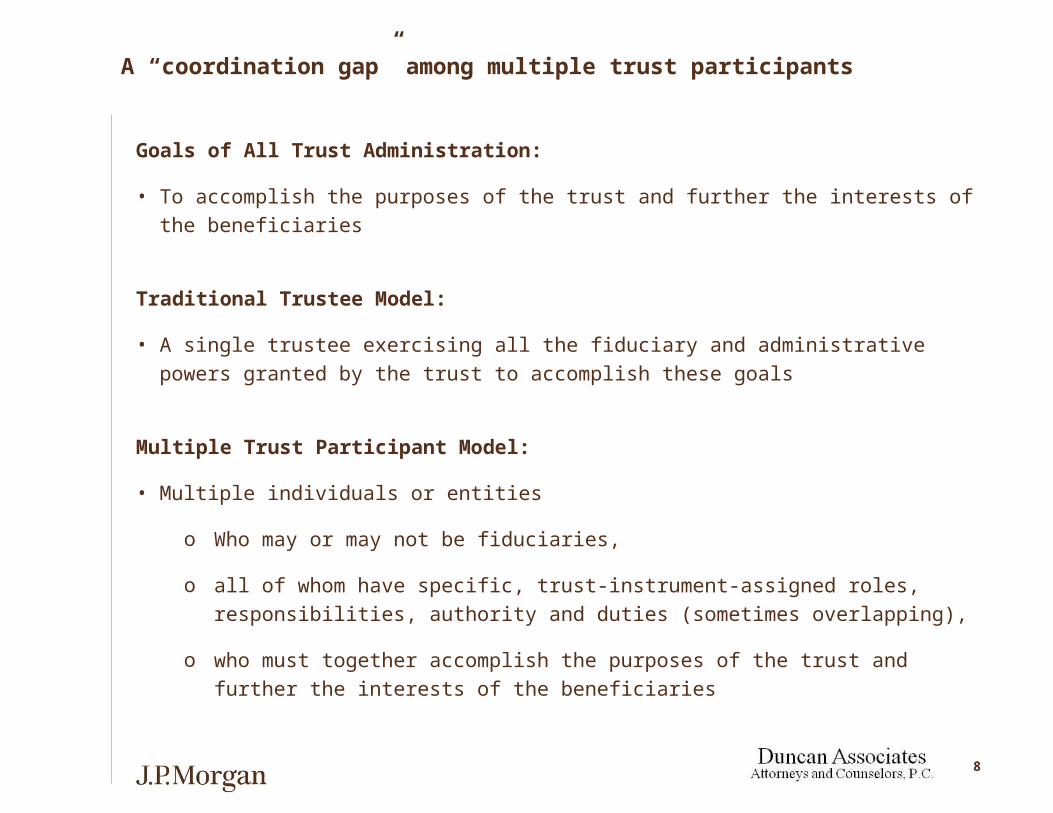

A “coordination gap” among multiple trust participants

Goals of All Trust Administration:

• To accomplish the purposes of the trust and further the interests of the beneficiaries

Traditional Trustee Model:

• A single trustee exercising all the fiduciary and administrative powers granted by the trust to accomplish these goals

Multiple Trust Participant Model:

• Multiple individuals or entities

o Who may or may not be fiduciaries,

o all of whom have specific, trust-instrument-assigned roles, responsibilities, authority and duties (sometimes overlapping),

o who must together accomplish the purposes of the trust and further the interests of the beneficiaries

9

Who are the various trust participants?

• Full trustee/Co-trustees

• Directed trustee

• Trust advisor

o Investment advisor/investment committeeo Distribution advisor/distribution committee

• Trust protector

o Trustee removero Trustee appointero Trust amender

10

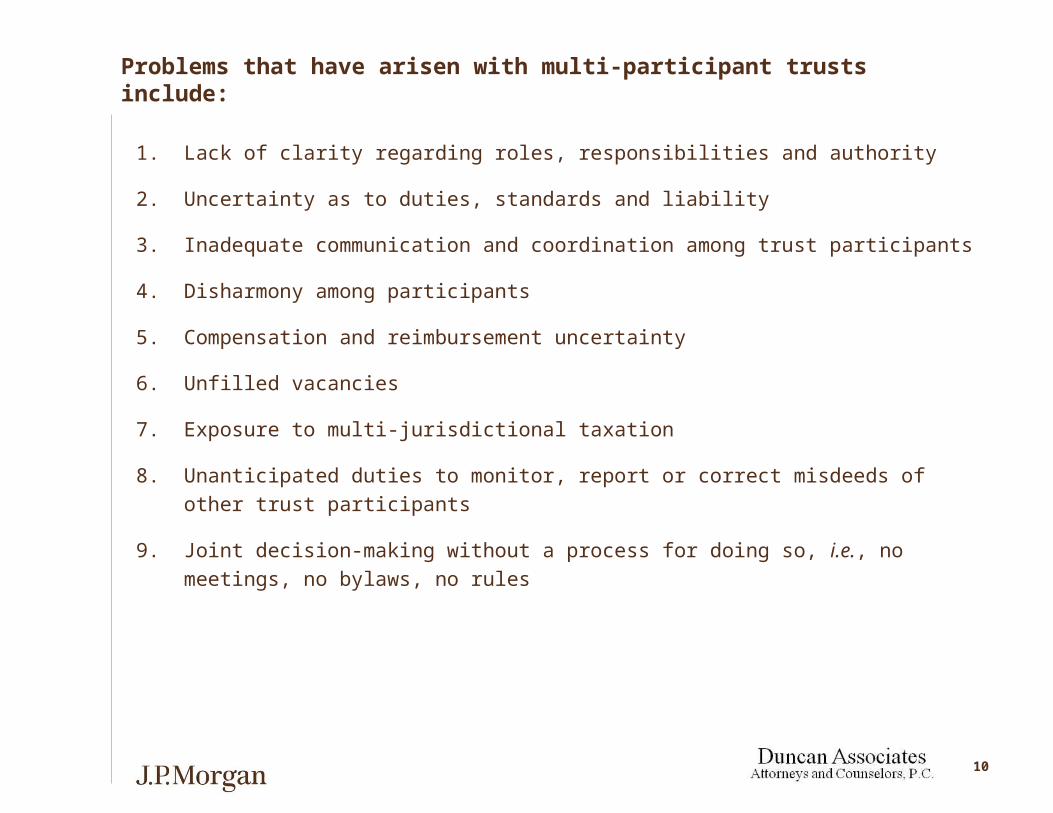

Problems that have arisen with multi-participant trusts include:

1. Lack of clarity regarding roles, responsibilities and authority

2. Uncertainty as to duties, standards and liability

3. Inadequate communication and coordination among trust participants

4. Disharmony among participants

5. Compensation and reimbursement uncertainty

6. Unfilled vacancies

7. Exposure to multi-jurisdictional taxation

8. Unanticipated duties to monitor, report or correct misdeeds of other trust participants

9. Joint decision-making without a process for doing so, i.e., no meetings, no bylaws, no rules

11

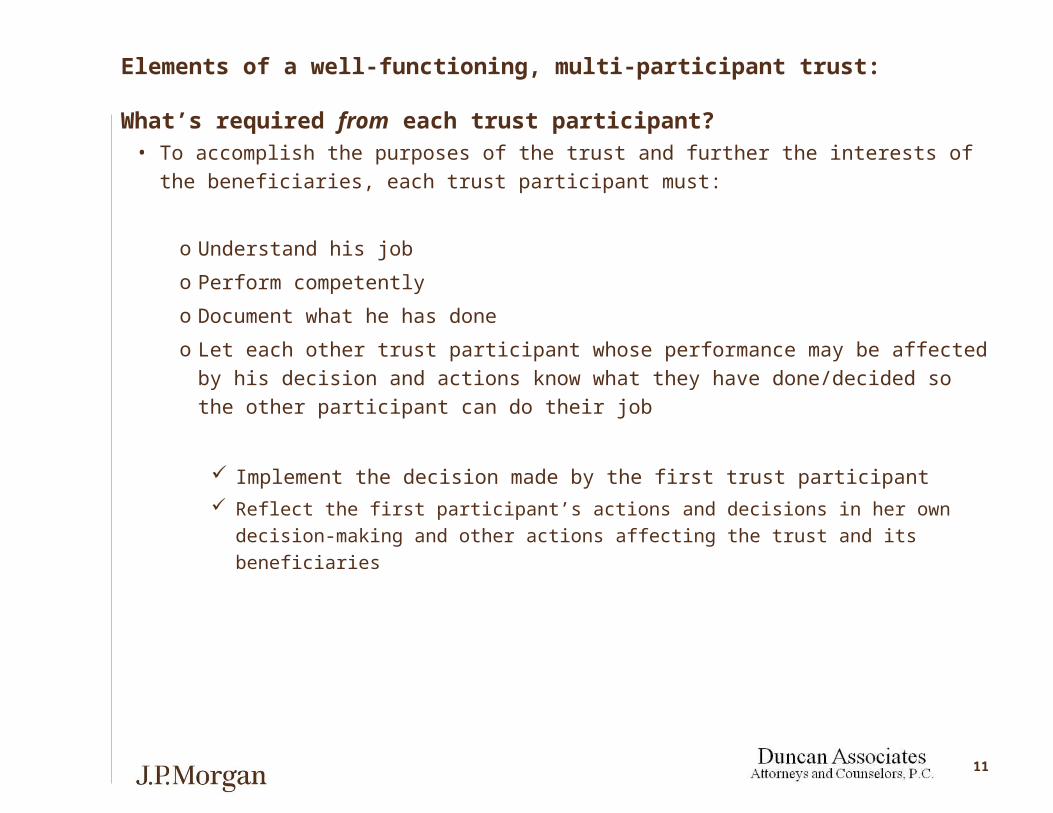

Elements of a well-functioning, multi-participant trust: What’s required from each trust participant?

• To accomplish the purposes of the trust and further the interests of the beneficiaries, each trust participant must:

o Understand his job

o Perform competently

o Document what he has done

o Let each other trust participant whose performance may be affected by his decision and actions know what they have done/decided so the other participant can do their job

Implement the decision made by the first trust participant Reflect the first participant’s actions and decisions in her own decision-making

and other actions affecting the trust and its beneficiaries

12

Elements of a well-functioning, multi-participant trust: What’s required for each participant’s ability to fulfill her function?

• Communication among the trust participants (e.g., actions they have taken)

• Coordination among the trust participants (e.g., speaking with a consistent voice if possible, investing and liquidating assets according to liquidity needs, taking a consistent view as to the meaning of trust provisions)

• Filling vacancies and assuring performance of absent participant’s functions

• Time limits for a trust participant to vote on, consent to or veto an action and certainty as to when a decision has actually been made

• Means for determining where a trust is being administered and the applicable law of administration and tax laws, especially when trust participants are residing or acting in multiple states

• Expeditious and competent out-of-court resolution of participant disagreements

13

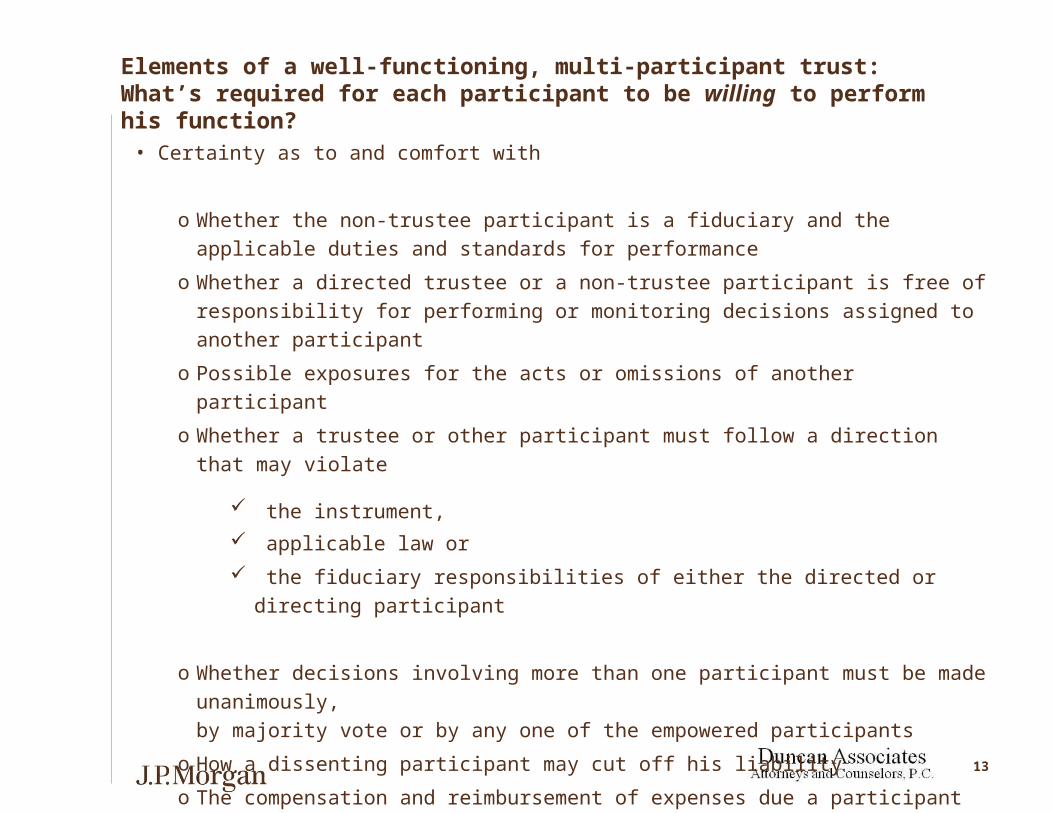

Elements of a well-functioning, multi-participant trust: What’s required for each participant to be willing to perform his function?

• Certainty as to and comfort with

o Whether the non-trustee participant is a fiduciary and the applicable duties and standards for performance

o Whether a directed trustee or a non-trustee participant is free of responsibility for performing or monitoring decisions assigned to another participant

o Possible exposures for the acts or omissions of another participant

o Whether a trustee or other participant must follow a direction that may violate

the instrument, applicable law or

the fiduciary responsibilities of either the directed or directing participant

o Whether decisions involving more than one participant must be made unanimously, by majority vote or by any one of the empowered participants

o How a dissenting participant may cut off his liability

o The compensation and reimbursement of expenses due a participant

14

Are non-trustee trust participants fiduciaries?

Common Law

• Little difficulty concluding that co-trustees and directed trustees are fiduciaries at common law

• Cases, treatises, and restatements also conclude that a person empowered to control a trustee is a fiduciary if the power is for the benefit of the beneficiaries

• Rights, duties, and liabilities depend on circumstances

Statutory Law

• Unless otherwise provided in the instrument:

o UTC §808: Anyone with a power to direct the trustee for someone else’s benefit is a fiduciary and has fiduciary duties

o Non-Conforming UTC States: Trust advisors and protectors are fiduciaries to the extent of the powers, duties, and discretions granted (e.g., NH and WY)

o Non-UTC States: If a person is given authority to direct, consent to, or disapprove a fiduciary’s decision, such advisors are considered to be fiduciaries (e.g., DE and SD)

15

Co-trustees under common law

Role, responsibilities and decision-making same as single trustee

• Decision-making: Historically, unanimity required. Restatement (Third) reversed prior versions, sanctioning a majority

• Allocation of responsibilities: Trust terms can give exclusive control over an area of trust administration to one co-trustee. Others have no duty to participate unless “reason to believe” a breach of trust will be committed

Compensation and reimbursement

• Ordinarily the same as for single trustees

Liability

• Generally joint and several liability

• Not liable for breach by a co-trustee, except in particular circumstances (e.g., improperly delegated)

• Inactivity not a defense

• Dissenting co-trustee ordinarily protected

16

Co-trustees under statutory law

Role, responsibilities and decision-making

• UTC states (23 states):

o Cannot be passive

o Must exercise reasonable care to prevent a co-trustee from committing a serious breach of trust and compel redress

o Decision-making by majority rule

o Remaining co-trustee (or majority) can act if one co-trustee is unavailable

o May not delegate to another trustee functions settlor expected trustees to perform jointly

o Non-UTC states and non-conforming UTC states:

o Some states require unanimity in decision-making; others by majority rule

o Many non-UTC states have similar provisions to UTC

o Inter-trustee delegation authority varies:

• DE: ministerial powers only

• IL: all rights, powers, and duties

o Explicit duty to inform co-fiduciaries about trust administration and other material information in NH

17

Co-trustees under statutory law (cont.)

Compensation and reimbursement

• UTC §708(a) provides for reasonable compensation

Liability

• UTC §703(c) provides a co-trustee is generally not liable for acts of another trustee

• Requirement to consult among all co-trustees before majority decision

• Some statutes make co-trustee liable for negligently permitting wrongful act

• Dissenting trustee protected under UTC and some non-UTC states if gives written notice to co-trustees and not a “serious breach”

• Some non-UTC states like MI and NY relieve dissenting trustee of liability only with prompt written dissent

Vacancies

• UTC §704(b) provides a vacancy need not be filled if at least one co-trustee remains in office

18

Directed trustees under common law

Role, responsibilities and decision-making

• Directed trustee has duty to follow directions of power holder

o Exceptions:

• Direction violates trust terms

• Trustee suspects violation of power holder’s fiduciary duty

o Little case law on directed trustee’s duty or authority to supervise actions of trust advisor

o Some authority that general fiduciary duties linger such as to keep informed, to investigate, and to warn beneficiaries

• Rollins

• Duemler

• Enron

• Worldcom

Compensation

• Not addressed

Liability

• Generally liability is limited on directed action

o Exception: If directed trustee “has reason to suspect” violation of fiduciary duty

19

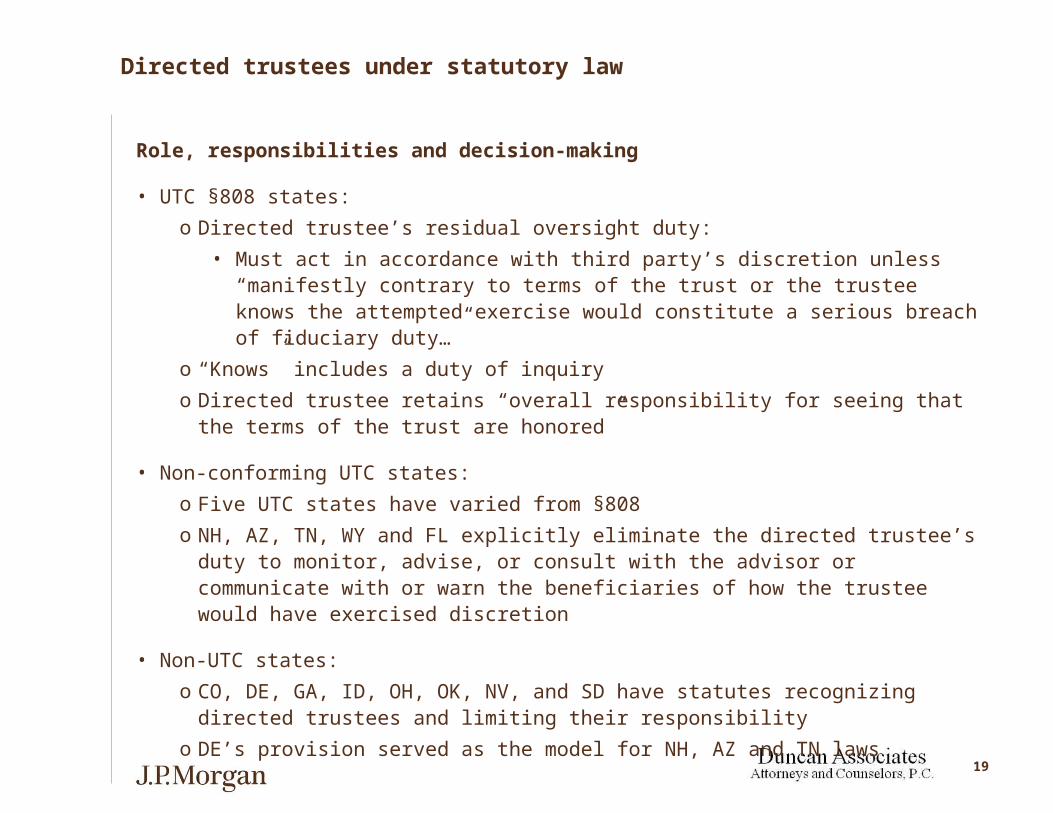

Directed trustees under statutory law

Role, responsibilities and decision-making

• UTC §808 states:

o Directed trustee’s residual oversight duty:

• Must act in accordance with third party’s discretion unless “manifestly contrary to terms of the trust or the trustee knows the attempted exercise would constitute a serious breach of fiduciary duty…”

o “Knows” includes a duty of inquiry

o Directed trustee retains “overall responsibility for seeing that the terms of the trust are honored”

• Non-conforming UTC states:

o Five UTC states have varied from §808

o NH, AZ, TN, WY and FL explicitly eliminate the directed trustee’s duty to monitor, advise, or consult with the advisor or communicate with or warn the beneficiaries of how the trustee would have exercised discretion

• Non-UTC states:

o CO, DE, GA, ID, OH, OK, NV, and SD have statutes recognizing directed trustees and limiting their responsibility

o DE’s provision served as the model for NH, AZ and TN laws

20

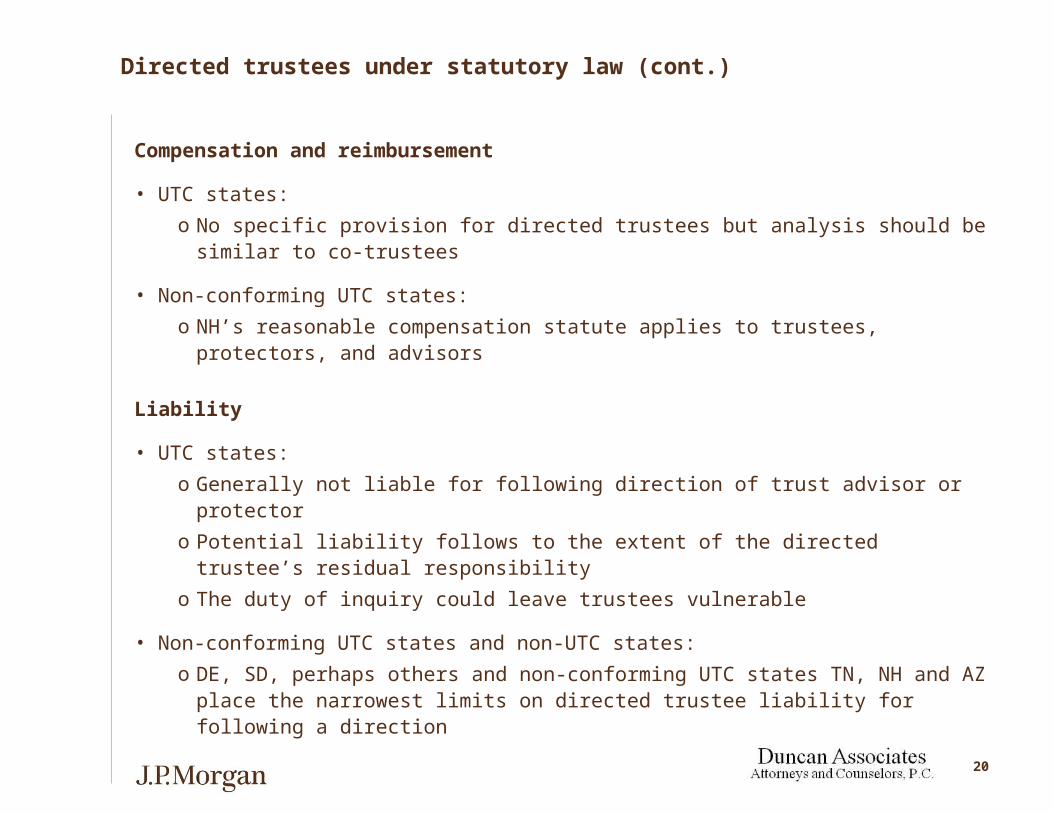

Directed trustees under statutory law (cont.)

Compensation and reimbursement

• UTC states:

o No specific provision for directed trustees but analysis should be similar to co-trustees

• Non-conforming UTC states:

o NH’s reasonable compensation statute applies to trustees, protectors, and advisors

Liability

• UTC states:

o Generally not liable for following direction of trust advisor or protector

o Potential liability follows to the extent of the directed trustee’s residual responsibility

o The duty of inquiry could leave trustees vulnerable

• Non-conforming UTC states and non-UTC states:

o DE, SD, perhaps others and non-conforming UTC states TN, NH and AZ place the narrowest limits on directed trustee liability for following a direction

21

Investment advisors/investment committees under common law

Role, responsibilities and decision-making

• Role and responsibilities same as a full trustee with regard to investing and managing the assets

• Standard of reasonable care, skill, and caution

• Duty to diversify unless trust provides otherwise

• Other fiduciary duties likely to apply (e.g., duty of loyalty)

Compensation and reimbursement

• Generally not addressed

Liability

• Subject to same liabilities as trustee with regard to investment function (e.g., open to claims of mismanagement, failure to diversify)

• Liability for breach of general fiduciary duties (e.g., duty of care)

22

Investment advisors/investment committees under statutory law

Role, responsibilities and decision-making

• UTC states:

o Any person with a power to direct, other than a beneficiary, is a fiduciary and subject to fiduciary duties

• Non-conforming UTC states and non-UTC states:

o A few states outline powers and duties that may be granted to a trust advisor (e.g., SD, NH, NV, and WY)

• Compensation and reimbursement

o Not specifically addressed, except in NH (reasonable)

Liability

• UTC states:

o UTC §808(d) provides that a holder of a power to direct is liable for fiduciary breach

o Liability for breach of specific authority granted and breach of general fiduciary duties

• Non-conforming UTC states and non-UTC states:

o Some states provide default powers for “trust advisors” (WY) or “trust investment advisors” (SD), others only illustrative powers (NH and ID)

o NH excludes liability for other participant’s decisions

Vacancies

• NH vests trustee with power to act on behalf of advisor until vacancy filled. Thirty day grace period before liability. Trustee may petition court to fill vacancy

23

Discretionary distribution advisors/discretionary distribution committees under common law

Role, responsibilities and decision-making

• Although there is little case law, the role and responsibilities probably the same as a full trustee with regard to distribution decisions (e.g., duty of impartiality)

• Other general fiduciary duties likely to apply (e.g., duty of care)

Compensation and reimbursement

• Generally not addressed

Liability

• Subject to same liabilities as trustee with regard to discretionary decisions (e.g., open to claims of improper distributions)

• Liability for breach of general fiduciary duties

24

Discretionary distribution advisors/discretionary distribution committees under statutory law

• UTC and other states with trust advisor statutes do not distinguish discretionary distribution advisors from other trust advisors, other than SD

• SD and NV have specific statutes outlining powers and discretions of a distribution trust advisor

25

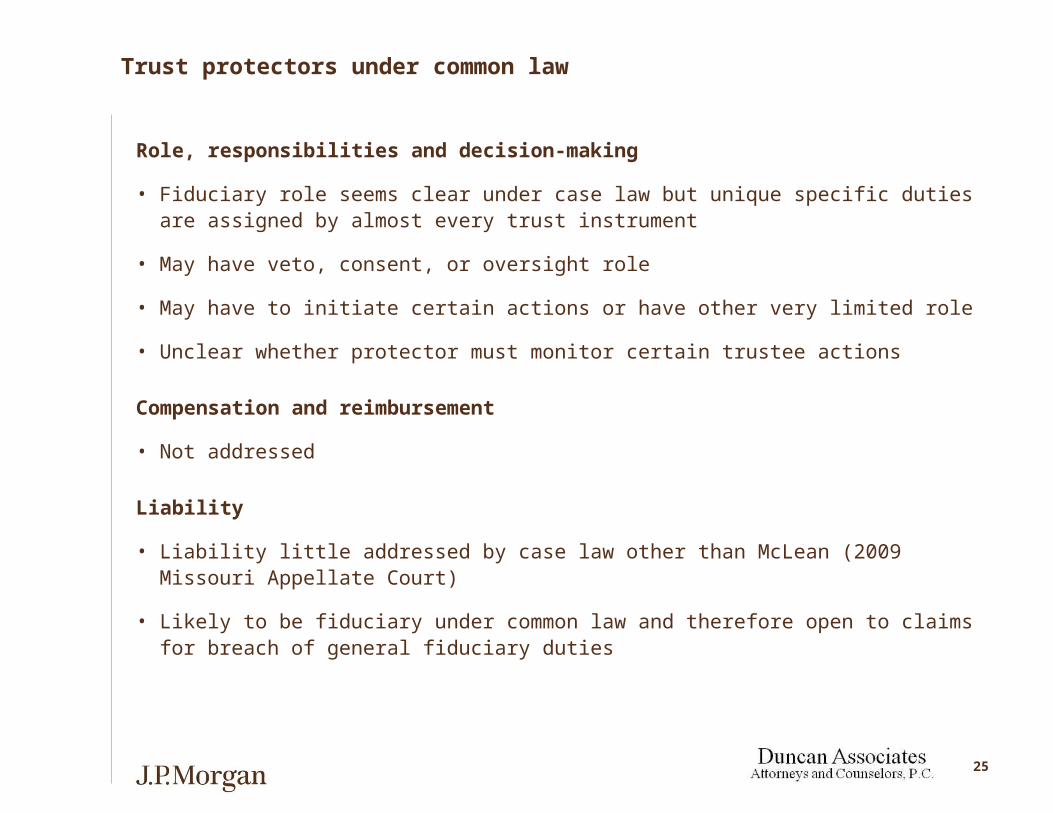

Trust protectors under common law

Role, responsibilities and decision-making

• Fiduciary role seems clear under case law but unique specific duties are assigned by almost every trust instrument

• May have veto, consent, or oversight role

• May have to initiate certain actions or have other very limited role

• Unclear whether protector must monitor certain trustee actions

Compensation and reimbursement

• Not addressed

Liability

• Liability little addressed by case law other than McLean (2009 Missouri Appellate Court)

• Likely to be fiduciary under common law and therefore open to claims for breach of general fiduciary duties

26

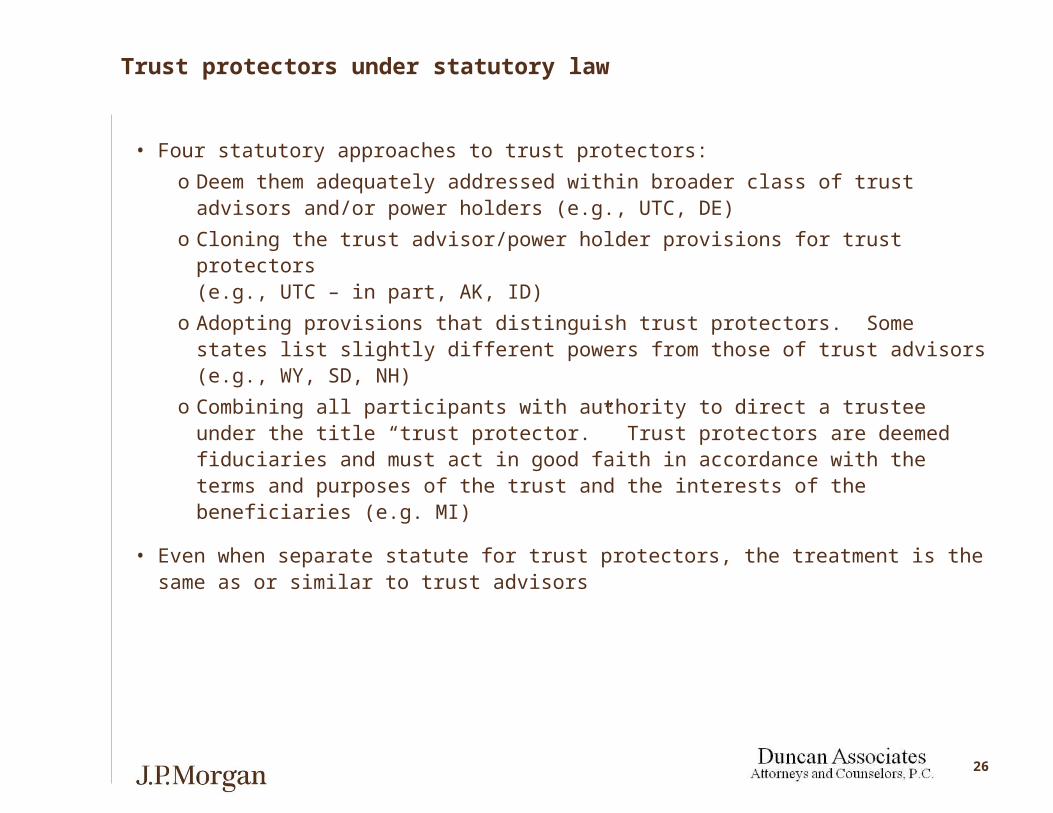

Trust protectors under statutory law

• Four statutory approaches to trust protectors:

o Deem them adequately addressed within broader class of trust advisors and/or power holders (e.g., UTC, DE)

o Cloning the trust advisor/power holder provisions for trust protectors (e.g., UTC – in part, AK, ID)

o Adopting provisions that distinguish trust protectors. Some states list slightly different powers from those of trust advisors (e.g., WY, SD, NH)

o Combining all participants with authority to direct a trustee under the title “trust protector.” Trust protectors are deemed fiduciaries and must act in good faith in accordance with the terms and purposes of the trust and the interests of the beneficiaries (e.g. MI)

• Even when separate statute for trust protectors, the treatment is the same as or similar to trust advisors

27

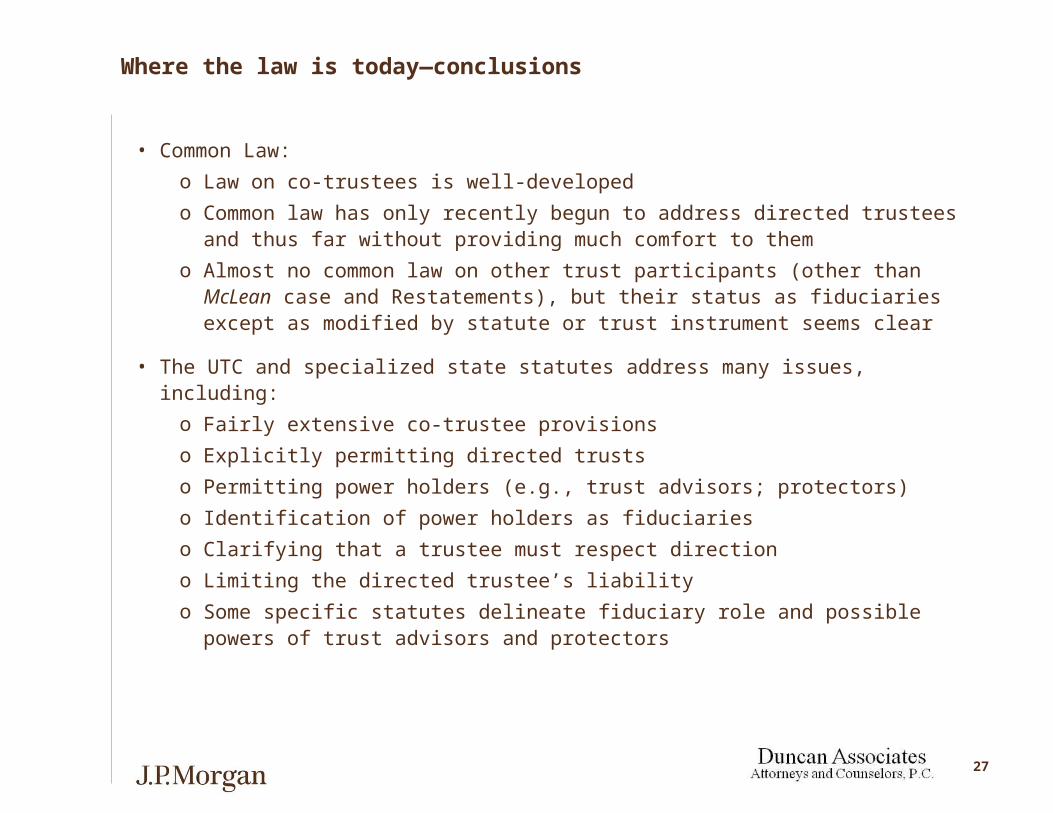

Where the law is today—conclusions

• Common Law:

o Law on co-trustees is well-developed

o Common law has only recently begun to address directed trustees and thus far without providing much comfort to them

o Almost no common law on other trust participants (other than McLean case and Restatements), but their status as fiduciaries except as modified by statute or trust instrument seems clear

• The UTC and specialized state statutes address many issues, including:

o Fairly extensive co-trustee provisions

o Explicitly permitting directed trusts

o Permitting power holders (e.g., trust advisors; protectors)

o Identification of power holders as fiduciaries

o Clarifying that a trustee must respect direction

o Limiting the directed trustee’s liability

o Some specific statutes delineate fiduciary role and possible powers of trust advisors and protectors

28

Where the law is today—conclusions (cont.)

• The holes—what even the best state statutes do not cover at all, or at a sufficient level to provide certainty (though NH, AZ, TN and DE come closest):

o Residual fiduciary duties of directed trustees with respect to power holders

o Explicit provisions addressing the duties of power holders

o No explicit duty on trust participants to co-operate

o No explicit duty on trust participants to even communicate (other than NH; DE has duty but only upon request of trust participants)

o Mechanism for filling vacancies in the office of non-trustee participants (other than NH)

o Compensation and reimbursement of expenses for non-trustee participants (other than NH)

o Determination of incapacity of non-trustee participants

o Treatment of dissenting participant

o Mechanism for dealing with disagreements between trust participants

29

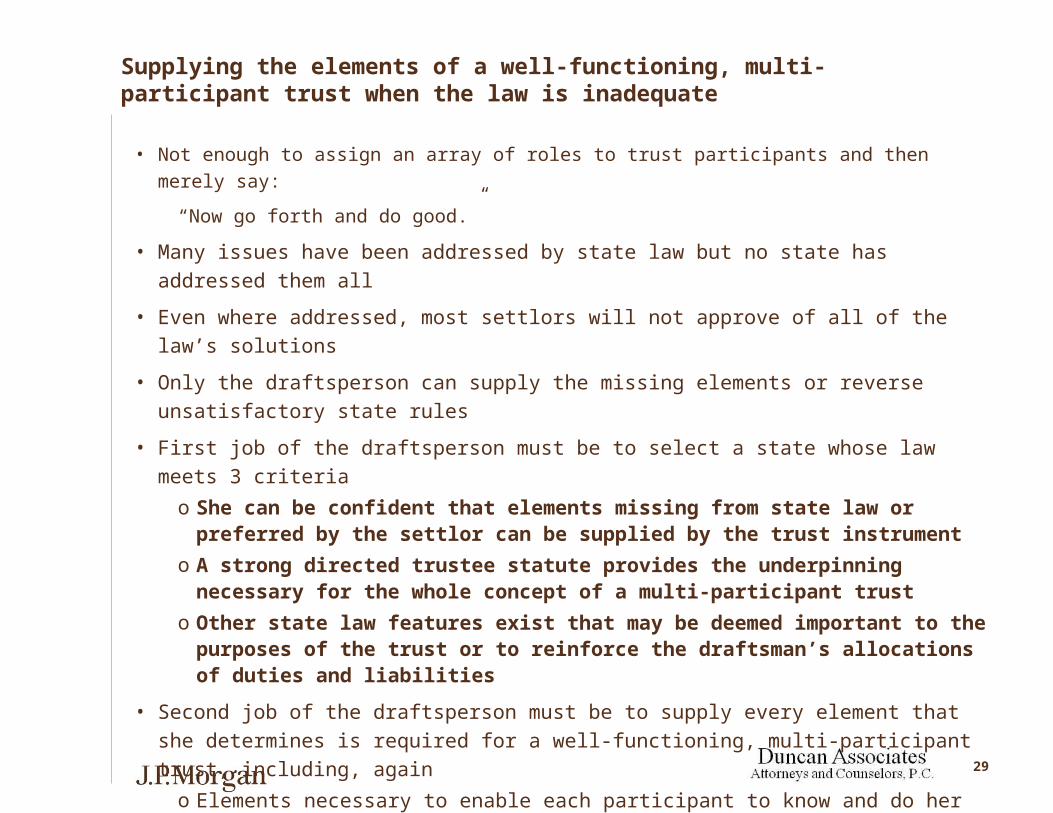

Supplying the elements of a well-functioning, multi-participant trust when the law is inadequate

• Not enough to assign an array of roles to trust participants and then merely say:

“Now go forth and do good.”

• Many issues have been addressed by state law but no state has addressed them all

• Even where addressed, most settlors will not approve of all of the law’s solutions

• Only the draftsperson can supply the missing elements or reverse unsatisfactory state rules

• First job of the draftsperson must be to select a state whose law meets 3 criteria

o She can be confident that elements missing from state law or preferred by the settlor can be supplied by the trust instrument

o A strong directed trustee statute provides the underpinning necessary for the whole concept of a multi-participant trust

o Other state law features exist that may be deemed important to the purposes of the trust or to reinforce the draftsman’s allocations of duties and liabilities

• Second job of the draftsperson must be to supply every element that she determines is required for a well-functioning, multi-participant trust, including, again

o Elements necessary to enable each participant to know and do her job

o Elements necessary to induce the participants to accept their appointments

o Perhaps create and assign the job of trust coordinator

30

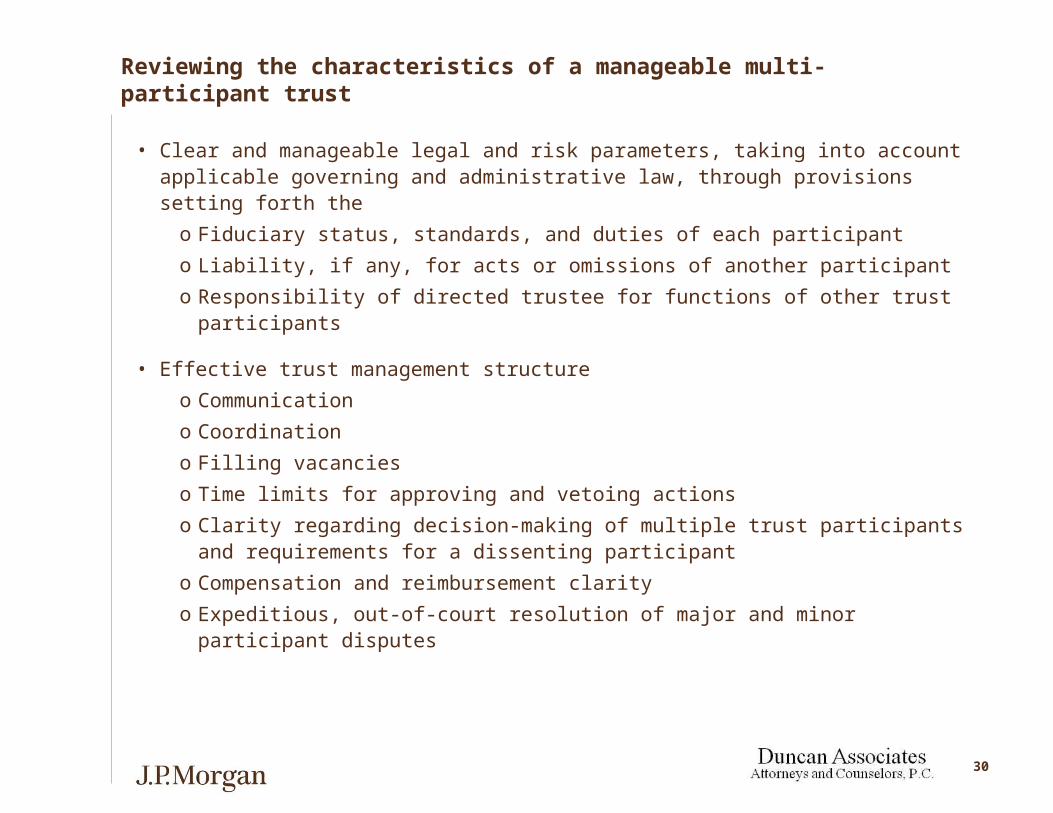

Reviewing the characteristics of a manageable multi-participant trust

• Clear and manageable legal and risk parameters, taking into account applicable governing and administrative law, through provisions setting forth the

o Fiduciary status, standards, and duties of each participant

o Liability, if any, for acts or omissions of another participant

o Responsibility of directed trustee for functions of other trust participants

• Effective trust management structure

o Communication

o Coordination

o Filling vacancies

o Time limits for approving and vetoing actions

o Clarity regarding decision-making of multiple trust participants and requirements for a dissenting participant

o Compensation and reimbursement clarity

o Expeditious, out-of-court resolution of major and minor participant disputes

31

Coordination generally requires a coordinator

• Consider creating a “managing directed trustee” (“MDT”) to forge a team out multiple trust participants

• Family office (“FO”)/Private Trust Company (“PTC”) management of multiple participants provide templates for the MDT

o FOs can create formal, fiduciary support (agency) agreements for the participants (the model)

o All responsibilities other than discretionary decisions assigned in the trust delegated to FO

o FO “tees up” those decisions, records them, implements them

o PTC performs same functions—by bringing the participants under its corporate umbrella and hierarchical management structure—with maximum coordination of all participants (the ideal)

o Key for both FO model and PTC ideal: actual ability to coordinate trust participants’ actions

• An MDT if similarly given the authority to coordinate the activities of all participants, can set and advance the agenda for a multi-participant trusts by using that authority to:

o Provide each participant material information about the trust’s assets, distributions, expenses and beneficiaries

o Set guidelines for timely decision-making by participants with critical trust powers

o Notify each participant when he has a decision to make; inquire whether he has made it and record the decision

o Identify who must implement each participant decision

o Assure that persons responsible for implementing a decision are aware it was made and what it was

o Assure and coordinate regular communication with the beneficiaries and settlor

o Temporarily perform vacant participant roles and taking steps to see vacancy filled

32

Coordinator’s responsibility must be for process, not results

• The MDT’s liability must, by state law or trust instrument,

o Be limited to the administrative processes it actually undertakes

o Exclude responsibility for whether another participant actually makes a decision, the quality of that decision or even acts or responds when requested to do so by the MDT

• Progressive state laws can protect the MDT from liability for the actions of other participants to a certain extent, but the draftsperson must

o Build on the state directed trust laws, especially those that authorize the directed trustee to confirm, record and report actions without assuming responsibility for trust outcomes

o Limit the MDT’s role to administrative actions that are within its authority and capability

o Ensure that the directed trustee has the authority to meet its process responsibilities

o Assure that the directed trustee/MDT has no liability for results dependent on the actions of others

• The MDT is likely to be a corporate trustee or a PTC but it can also be a professional advisor, family office (as “managing advisor” but not trustee) or an individual with the requisite skills

33

Other drafting points for creating a manageable multi-participant trust

• Defining who is and who is not a fiduciary

o Current law considers various trust participants to be fiduciaries

o Specific waiver of the status as a fiduciary is needed to avoid the presumption

o In some state’s, a court’s interpretation of a waiver still uncertain, others prohibit it in part (e.g., Michigan)

• Information sharing

o Other than NH and a limited implementation by DE, no statutes or case law address necessity for information-sharing among participants

o Draftsperson may want to establish guidelines requiring necessary information to be supplied

o Consider

• Type of information

• Timing of information-sharing

o Some information-sharing may have limits, e.g., deliberations regarding discretionary decision-making

34

Further limiting liability of trust participants?Exculpation, indemnification, or neither?

• Directed trustee liability for following a direction is limited under many state statutes absent a finding that attempted exercise is:

o Manifestly contrary to the terms of the trust or

o Would constitute a serious breach (UTC Standard)

o Or willful misconduct (DE) (willful misconduct defined in 2010 to mean intentional wrongdoing not mere negligence, gross negligence or recklessness)

• Power-holder’s liability is generally not addressed. Draftsperson and settlor need to consider drafting limits if desired

• Consider use of an entity (such as an LLC) for a trust participant to act if liability exposure needs to be limited

• Consider errors and omissions insurance policy purchases by the trust

• Do consider the need to balance protection of participants with competent performance of trust functions when considering exculpation/exoneration/indemnification

o Exculpation clauses should be drafted in as appropriate

• Some common and statutory law limits usefulness

• Will not protect against bad faith, reckless indifference to interests of beneficiaries, liability for a trustee’s profit from a breach or abuse of a fiduciary or confidential relationship

• Some cases completely reject as “contrary to public policy”

o Indemnification can also be a remedy

35

Vacancies, succession, incapacity

• Goal is to avoid a hiatus in an area of trust decision-making if a participant resigns, dies, is incapacitated or is removed

• Problem of vacancies not generally addressed in the law (other than NH). Must solve with good drafting.

• Issues that should be covered:

o Succession of multiple trust participants

o If vacancy not filled, give trustee or other trust participant power to appoint a successor or direct they petition a court to fill vacancy

o Consider vesting the trustee or another participant with the powers held by the former trust participant until a new participant is appointed

o Suspend liability for a period of time is role is being temporarily filled by trustee or another trust participant

o Require notice to all participants of resignation

o Provide when vacancies need not be filled

o Vest successors with all necessary powers

o Consider waiving liability for acts and omissions of predecessor

o Consider tax sensitive powers and possible prohibitions on who can act

• Incapacity

o Identify how incapacity will be determined and what the consequences are

36

Where do we go from here?

• Trend toward multi-participant trusts is likely to continue

• Watch for more developments on the legislative front because this is a rapidly evolving area of trust law

• Practitioners and advisors need to have a broad understanding of many issues involving multiple trust participants to draft their ways over, under, around and through them

• Careful drafting must fill in where even the best statutes are silent, or ambiguous, or where the settlor wants different terms

• Think of the trust participants as part of an organization when drafting coordination and communication clauses

o Consider whether you can rely on participants to “go forth and do good.”

37

Stephen E. Parker is a member of J.P. Morgan’s national Wealth Advisory Group and is responsible for tax and estate planning strategy for the firm’s Private Banking clients in the Southeast region.

Prior to joining J.P. Morgan Private Bank, Steve spent 13 years in the private practice of law and was most recently a partner in the Family Wealth Planning Department of Cohen, Pollock, Merlin and Small.

Steve is an attorney, admitted to practice in Georgia, and is a member of the American and Georgia Bar Associations. He is also a member of the Georgia Fiduciary Law Section Legislation Committee, a member of the Planned Giving Advisory Board for both Emory University and the Community Foundation for Greater Atlanta, and a Board member of the Georgia Planned Giving Council. His specific areas of expertise include wealth transfer, closely held business and international tax planning. He is a frequent lecturer on estate planning and tax topics.

Mr. Parker received a BSBA, magna cum laude, from Washington University in St. Louis (1989), and a J.D., with distinction, from Emory University School of Law (1992).

Stephen E. Parker, Wealth AdvisorJ.P.Morgan Private Bank

38

Anita Sarafa joined JPMorgan Private Bank in 2000, where she is a Managing Director in the Wealth Advisory Group. She provides high-net-worth individuals and families throughout the Midwest with integrated wealth management advice on how to tax-efficiently hold, manage and transfer their wealth.

In addition to serving as a Wealth Advisor, Anita acted as the Fiduciary Manager for the Midwest region, overseeing trust and estate administration from 2000 to 2002. Prior to joining JPMorgan Private Bank, Anita was with the Chicago-based law firm of Winston & Strawn for 11 years, practicing in the Trust & Estates Group. She was admitted into the partnership in 1998. Anita is the current Vice President of the Chicago Estate Planning Council and a member of the Ravinia Festival Planned Giving Advisory Committee, American Bar Association, and Chicago Bar Association. She speaks frequently on topics related to tax planning, charitable giving and estate planning. Anita has also been featured in Business Week, the Wall Street Journal, Dow Jones, the Chicago Tribune, CLTV and other local and national media.

Anita graduated from the University of Michigan with a B.A. in Political Science. She received her Juris Doctor from Boston University School of Law in 1989. While at Boston University, Anita was an editor of the Probate Law Journal for the National College of Probate Judges.

Anita Sarafa, Wealth AdvisorJ.P.Morgan Private Bank

39

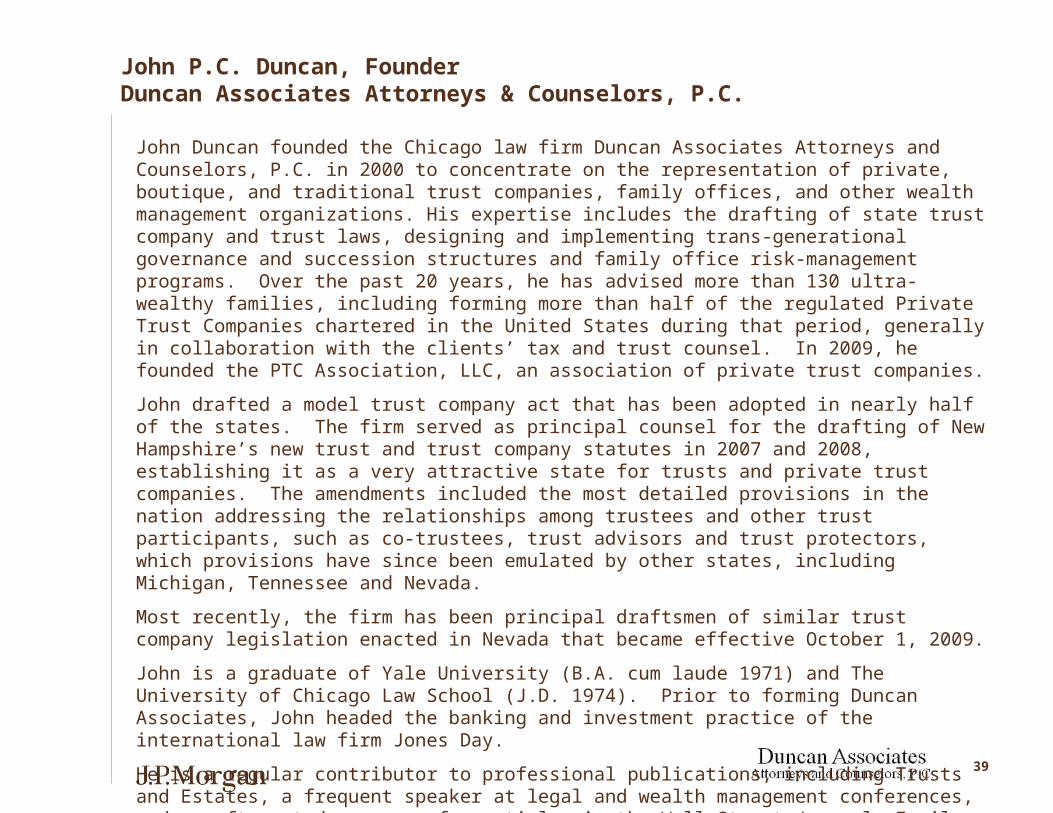

John Duncan founded the Chicago law firm Duncan Associates Attorneys and Counselors, P.C. in 2000 to concentrate on the representation of private, boutique, and traditional trust companies, family offices, and other wealth management organizations. His expertise includes the drafting of state trust company and trust laws, designing and implementing trans-generational governance and succession structures and family office risk-management programs. Over the past 20 years, he has advised more than 130 ultra-wealthy families, including forming more than half of the regulated Private Trust Companies chartered in the United States during that period, generally in collaboration with the clients’ tax and trust counsel. In 2009, he founded the PTC Association, LLC, an association of private trust companies.

John drafted a model trust company act that has been adopted in nearly half of the states. The firm served as principal counsel for the drafting of New Hampshire’s new trust and trust company statutes in 2007 and 2008, establishing it as a very attractive state for trusts and private trust companies. The amendments included the most detailed provisions in the nation addressing the relationships among trustees and other trust participants, such as co-trustees, trust advisors and trust protectors, which provisions have since been emulated by other states, including Michigan, Tennessee and Nevada.

Most recently, the firm has been principal draftsmen of similar trust company legislation enacted in Nevada that became effective October 1, 2009.

John is a graduate of Yale University (B.A. cum laude 1971) and The University of Chicago Law School (J.D. 1974). Prior to forming Duncan Associates, John headed the banking and investment practice of the international law firm Jones Day.

He is a regular contributor to professional publications, including Trusts and Estates, a frequent speaker at legal and wealth management conferences, and an oft-quoted resource for articles in the Wall Street Journal, Family Wealth Report, Registered Rep and other national and local media.

John P.C. Duncan, FounderDuncan Associates Attorneys & Counselors, P.C.

40

Disclaimers

Duncan AssociatesAttorneys and Counselors, P.C.

Any discussion of U.S. tax matters contained herein, including attachments, is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with Duncan Associates Attorneys and Counselors, P.C. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

JPMorgan Chase & Co.

JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein is not intended or written to be used, and cannot be used in connection with the promotion, marketing or recommendation by anyone unaffiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.