THE CONSUMER FINANCIAL PROTECTION BUREAU: FAIR LENDING AT WORK JUNE 2012 Tim Lambert Senior Counsel,...

16

THE CONSUMER FINANCIAL PROTECTION BUREAU: FAIR LENDING AT WORK JUNE 2012 Tim Lambert Senior Counsel, Office of Fair Lending and Equal Opportunity Consumer Financial Protection Bureau Note: This document was used in support of a live discussion. As such, it does not necessarily express the entirety of that discussion nor the relative emphasis of topics. FAIR LENDING AT WORK 1

-

Upload

eleanor-josephine-adams -

Category

Documents

-

view

216 -

download

2

Transcript of THE CONSUMER FINANCIAL PROTECTION BUREAU: FAIR LENDING AT WORK JUNE 2012 Tim Lambert Senior Counsel,...

FAIR LENDING AT WORK 1

THE CONSUMER FINANCIAL PROTECTION BUREAU:FAIR LENDING AT WORK

JUNE 2012

Tim Lambert

Senior Counsel, Office of Fair Lending and Equal Opportunity

Consumer Financial Protection Bureau

Note: This document was used in support of a live discussion. As such, it does not necessarily express the entirety of that discussion nor the relative emphasis of topics.

FAIR LENDING AT WORK 2

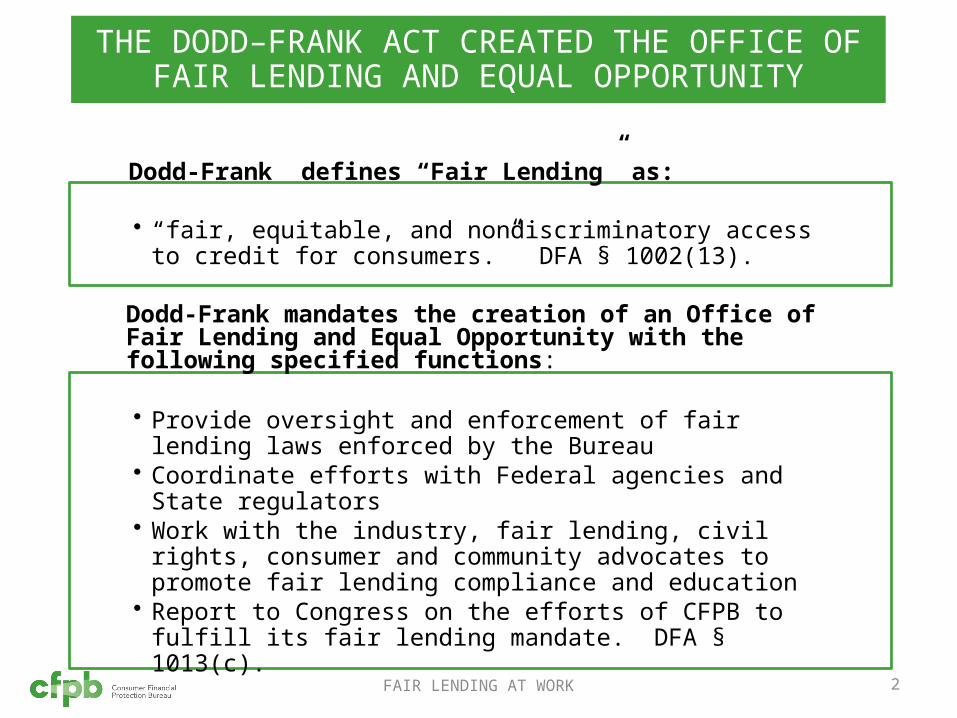

• “fair, equitable, and nondiscriminatory access to credit for consumers.” DFA § 1002(13).

Dodd-Frank defines “Fair Lending” as:

• Provide oversight and enforcement of fair lending laws enforced by the Bureau

• Coordinate efforts with Federal agencies and State regulators

• Work with the industry, fair lending, civil rights, consumer and community advocates to promote fair lending compliance and education

• Report to Congress on the efforts of CFPB to fulfill its fair lending mandate. DFA § 1013(c).

Dodd-Frank mandates the creation of an Office of Fair Lending and Equal Opportunity with the following specified functions:

THE DODD–FRANK ACT CREATED THE OFFICE OF FAIR LENDING AND EQUAL OPPORTUNITY

FAIR LENDING AT WORK 3

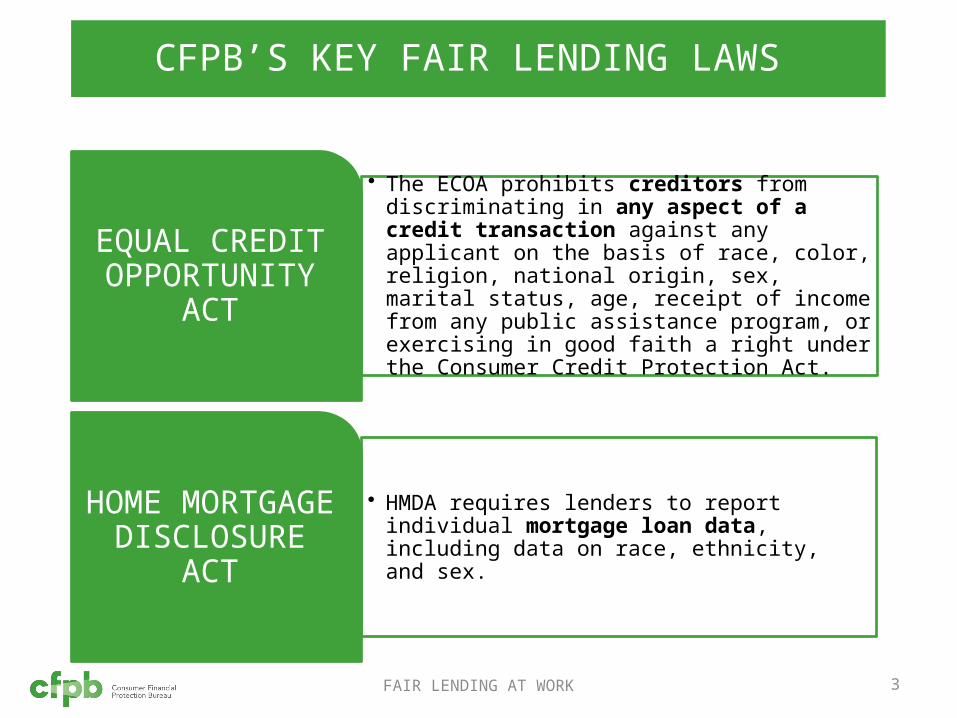

CFPB’S KEY FAIR LENDING LAWS

• The ECOA prohibits creditors from discriminating in any aspect of a credit transaction against any applicant on the basis of race, color, religion, national origin, sex, marital status, age, receipt of income from any public assistance program, or exercising in good faith a right under the Consumer Credit Protection Act.

EQUAL CREDIT OPPORTUNITY

ACT

• HMDA requires lenders to report individual mortgage loan data, including data on race, ethnicity, and sex.

HOME MORTGAGE

DISCLOSURE ACT

FAIR LE NDING AT WORK 4

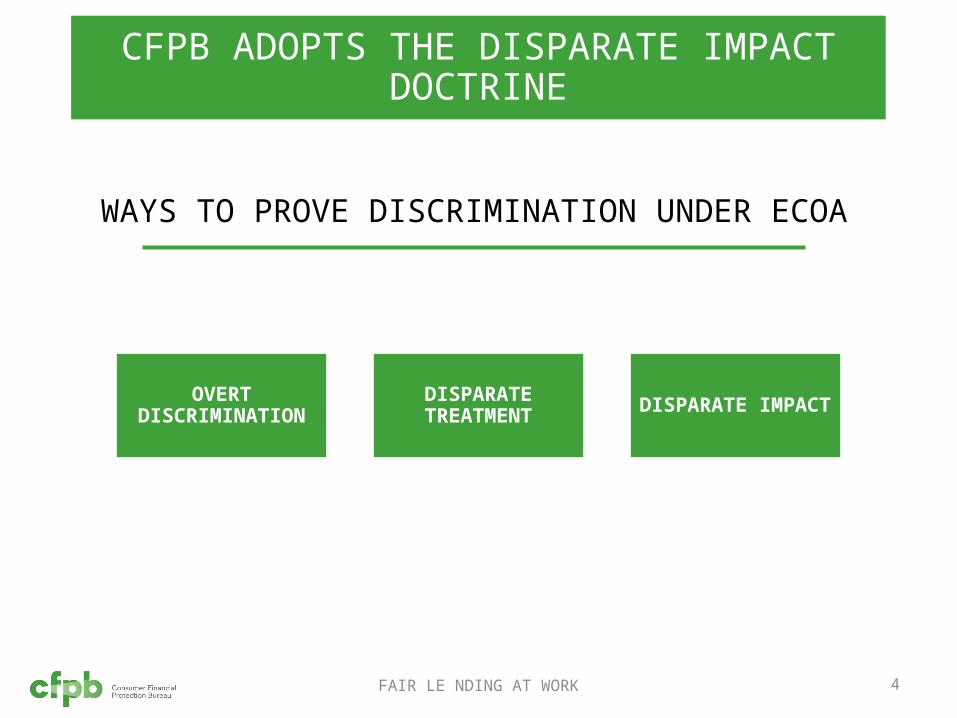

CFPB ADOPTS THE DISPARATE IMPACT DOCTRINE

WAYS TO PROVE DISCRIMINATION UNDER ECOA

OVERT DISCRIMINATION

DISPARATE TREATMENT

DISPARATE IMPACT

FAIR LENDING AT WORK 5

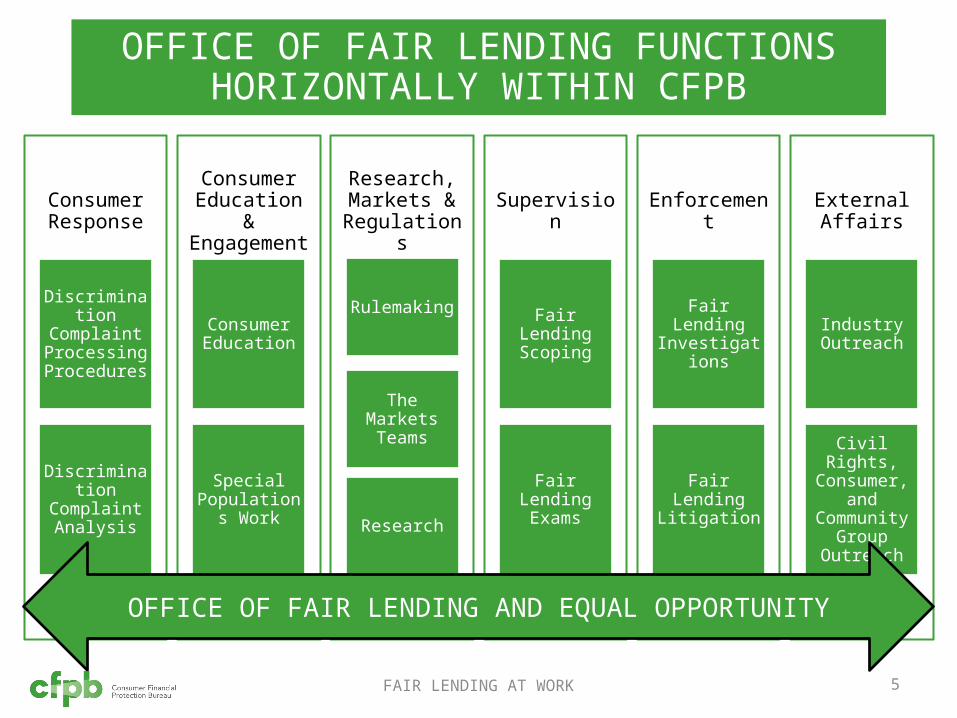

Consumer Response

Discrimination Complaint Processing Procedures

Discrimination Complaint

Analysis

Consumer Education & Engagement

Consumer Education

Special Populations

Work

Research, Markets &

Regulations

Rulemaking

The Markets Teams

Research

Supervision

Fair Lending Scoping

Fair Lending Exams

Enforcement

Fair Lending Investigations

Fair Lending Litigation

External Affairs

Industry Outreach

Civil Rights, Consumer, and

Community Group

Outreach

OFFICE OF FAIR LENDING AND EQUAL OPPORTUNITY

OFFICE OF FAIR LENDING FUNCTIONS HORIZONTALLY WITHIN CFPB

FAIR LENDING AT WORK 6

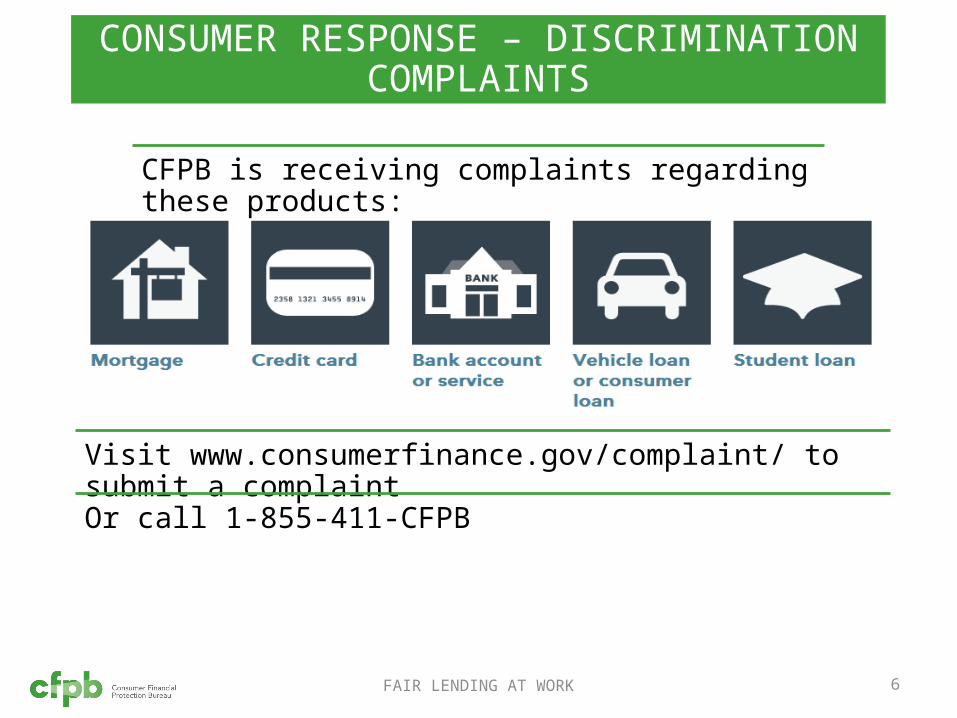

CONSUMER RESPONSE – DISCRIMINATION COMPLAINTS

Visit www.consumerfinance.gov/complaint/ to submit a complaint

Or call 1-855-411-CFPB

CFPB is receiving complaints regarding these products:

FAIR LENDING AT WORK 7

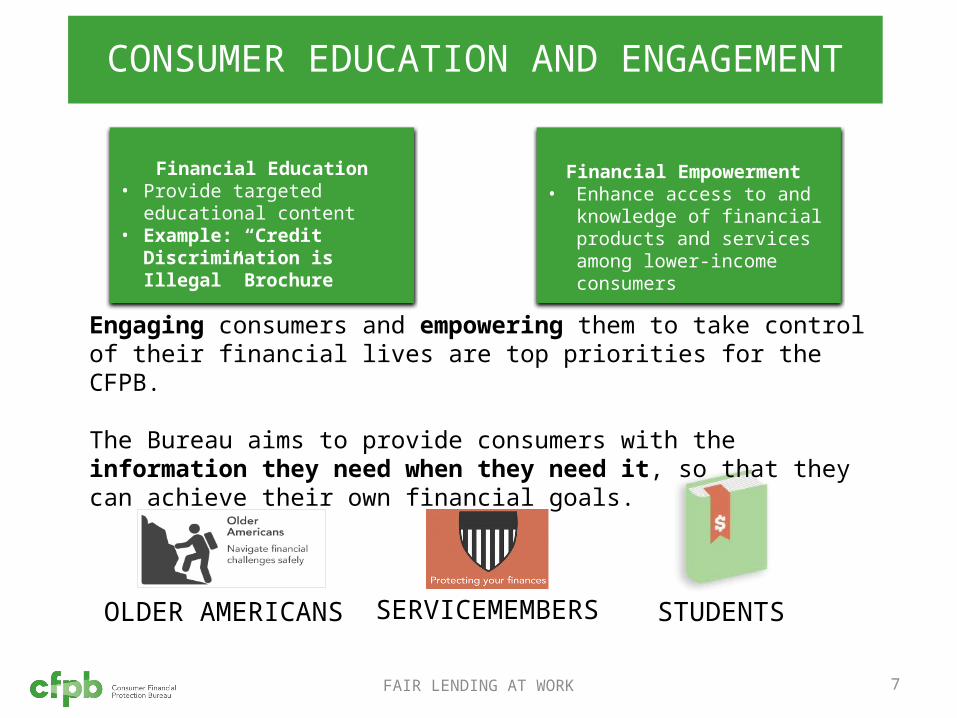

CONSUMER EDUCATION AND ENGAGEMENT

OLDER AMERICANS SERVICEMEMBERS STUDENTS

Engaging consumers and empowering them to take control of their financial lives are top priorities for the CFPB.

The Bureau aims to provide consumers with the information they need when they need it, so that they can achieve their own financial goals.

Financial Education• Provide targeted

educational content• Example: “Credit

Discrimination is Illegal” Brochure

Financial Empowerment • Enhance access to and

knowledge of financial products and services among lower-income consumers

FAIR LENDING AT WORK 8

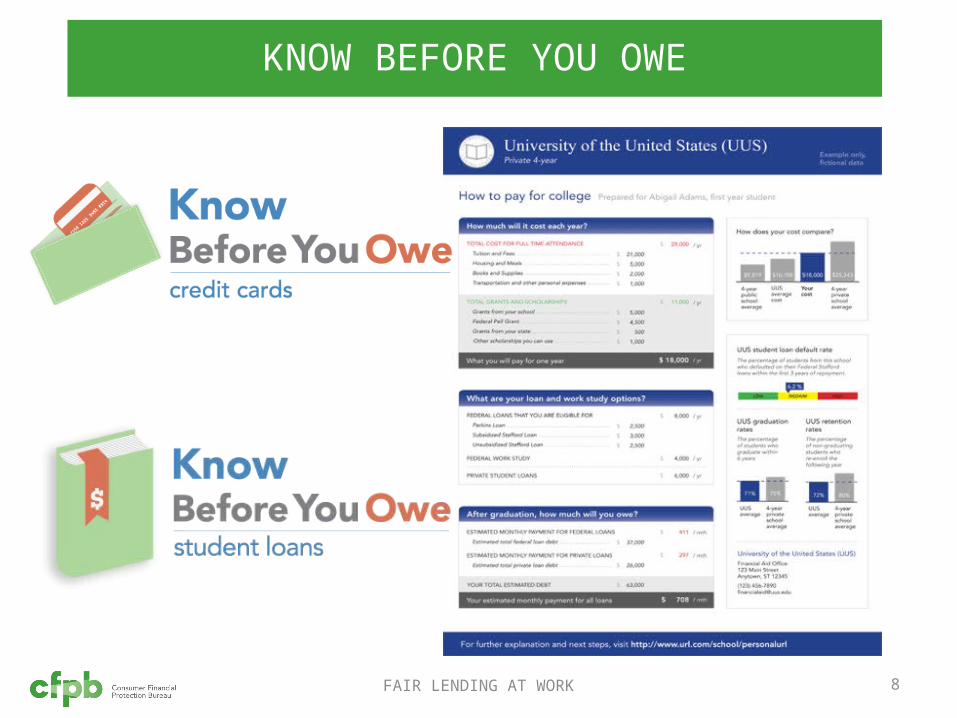

KNOW BEFORE YOU OWE

FAIR LENDING AT WORK 9

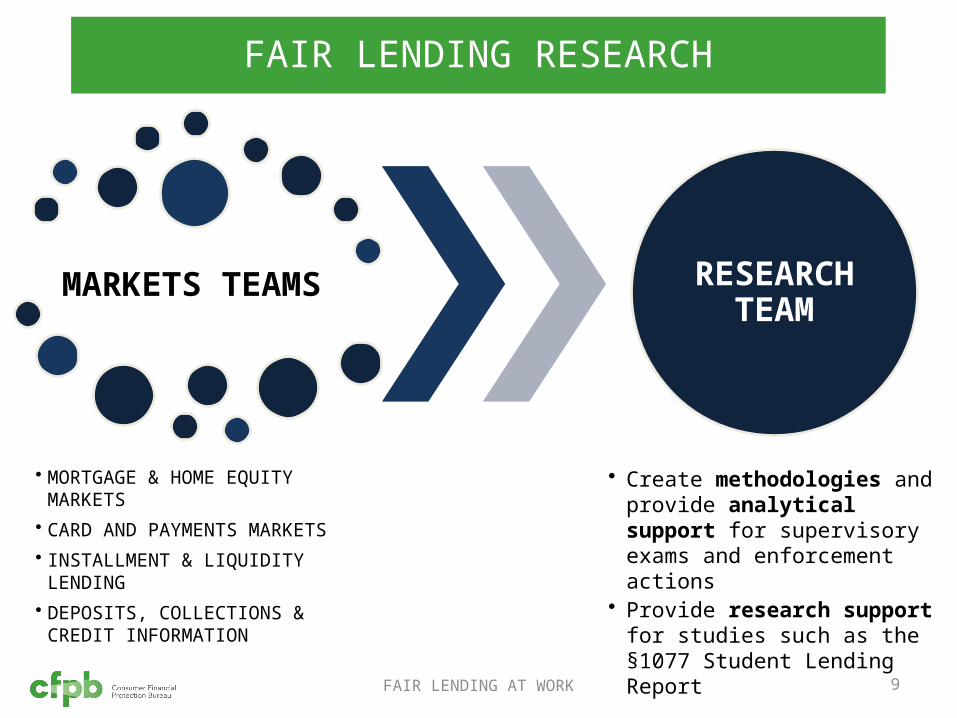

FAIR LENDING RESEARCH

MARKETS TEAMS

• MORTGAGE & HOME EQUITY MARKETS

• CARD AND PAYMENTS MARKETS

• INSTALLMENT & LIQUIDITY LENDING

• DEPOSITS, COLLECTIONS & CREDIT INFORMATION

RESEARCH TEAM

• Create methodologies and provide analytical support for supervisory exams and enforcement actions

• Provide research support for studies such as the §1077 Student Lending Report

FAIR LENDING AT WORK 10

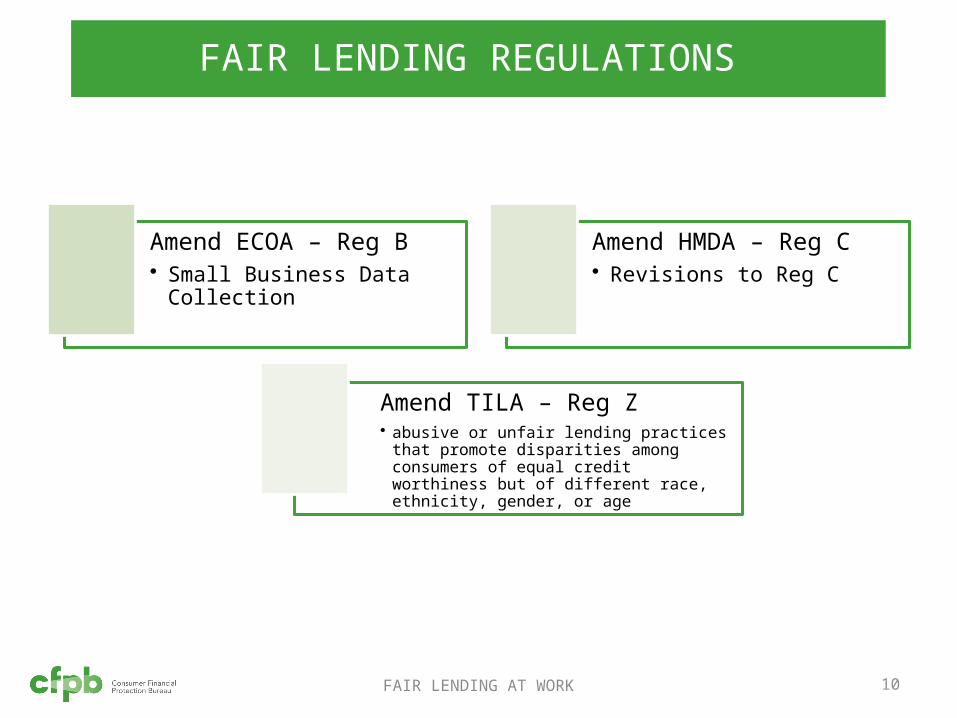

Amend ECOA – Reg B • Small Business Data

Collection

Amend HMDA – Reg C • Revisions to Reg C

Amend TILA – Reg Z• abusive or unfair lending practices that

promote disparities among consumers of equal credit worthiness but of different race, ethnicity, gender, or age

FAIR LENDING REGULATIONS

FAIR LENDING AT WORK 11

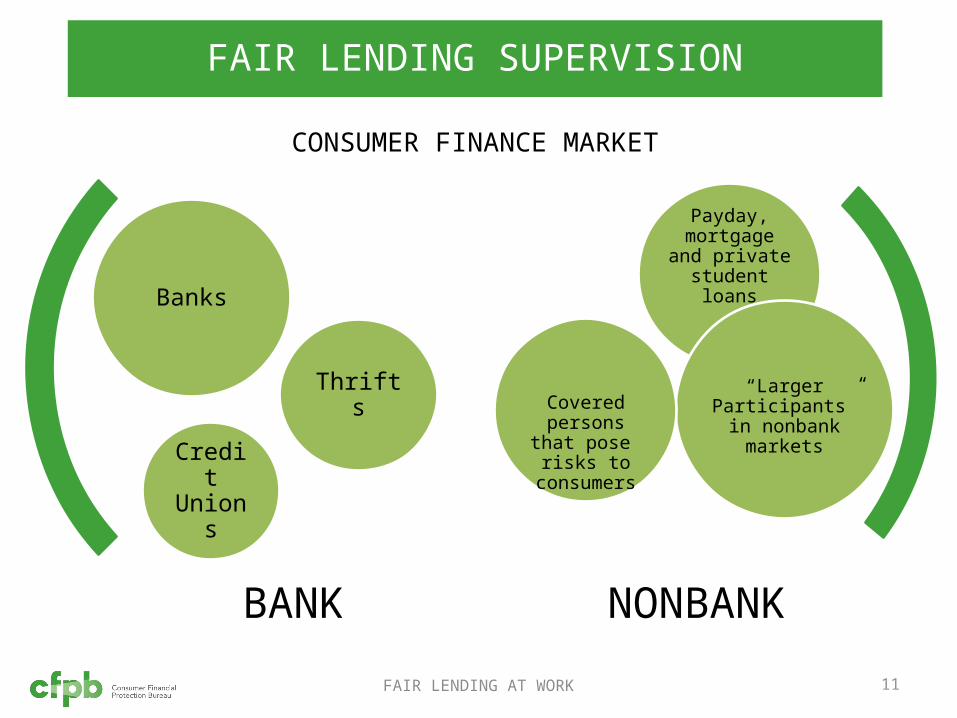

FAIR LENDING SUPERVISION

NONBANK

Payday, mortgage and

private student loans

“Larger Participants” in nonbank

markets

Covered persons

that pose risks to

consumers

Banks

Thrifts

Credit Unions

BANK

CONSUMER FINANCE MARKET

FAIR LENDING AT WORK 12

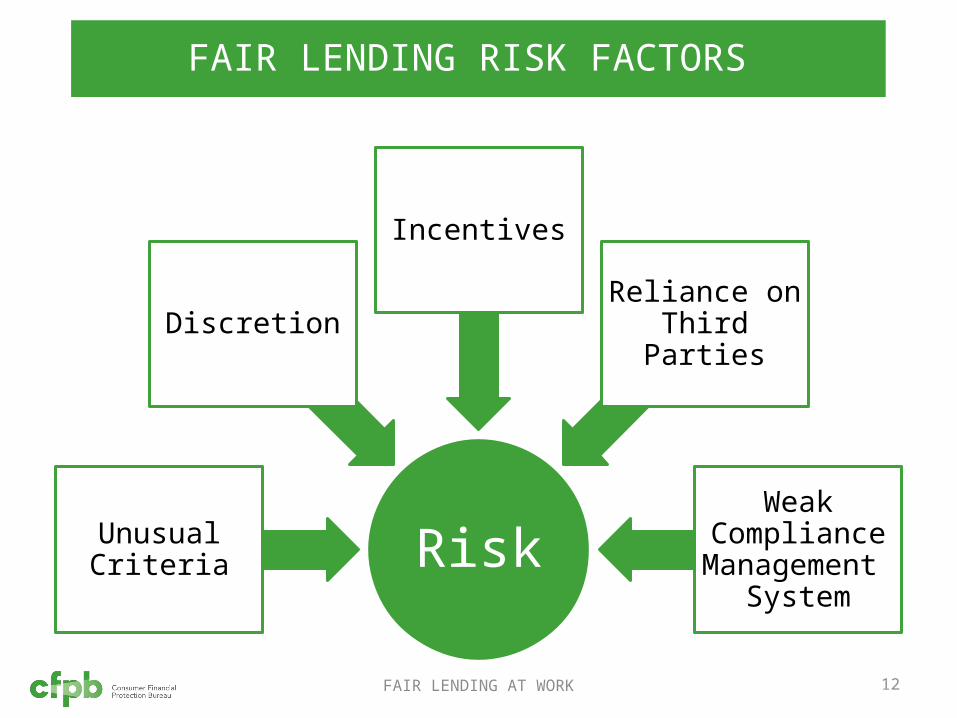

RiskUnusual Criteria

Discretion

Incentives

Reliance on Third Parties

Weak Compliance

Management System

FAIR LENDING RISK FACTORS

FAIR LENDING AT WORK 13

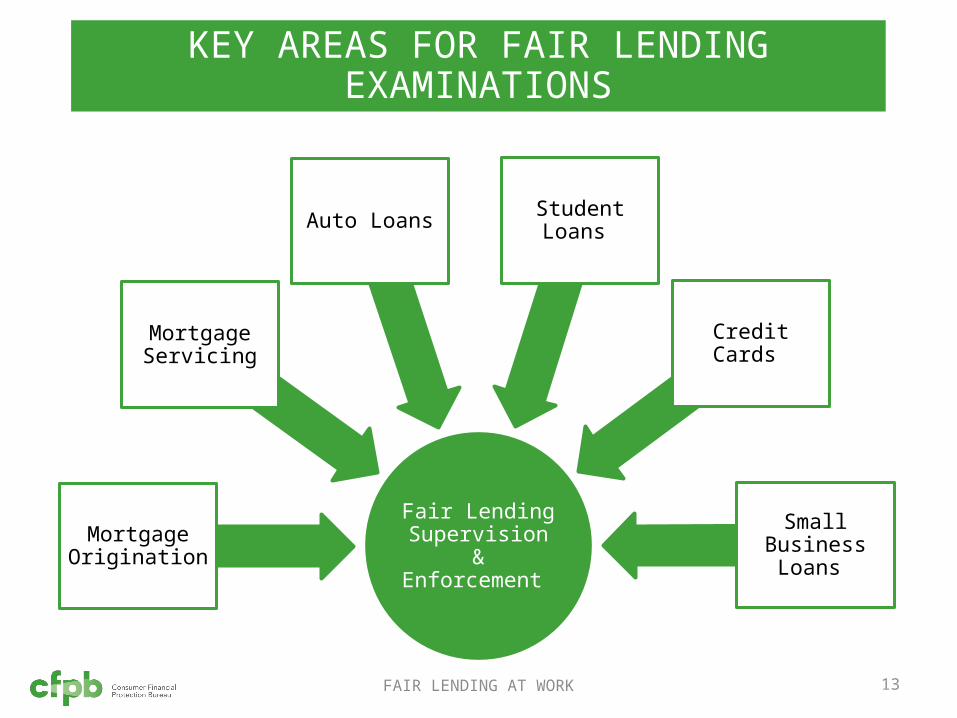

Fair Lending Supervision & Enforcement

Mortgage Origination

Mortgage Servicing

Auto Loans Student Loans

Credit Cards

Small Business Loans

KEY AREAS FOR FAIR LENDING EXAMINATIONS

FAIR LENDING AT WORK 14

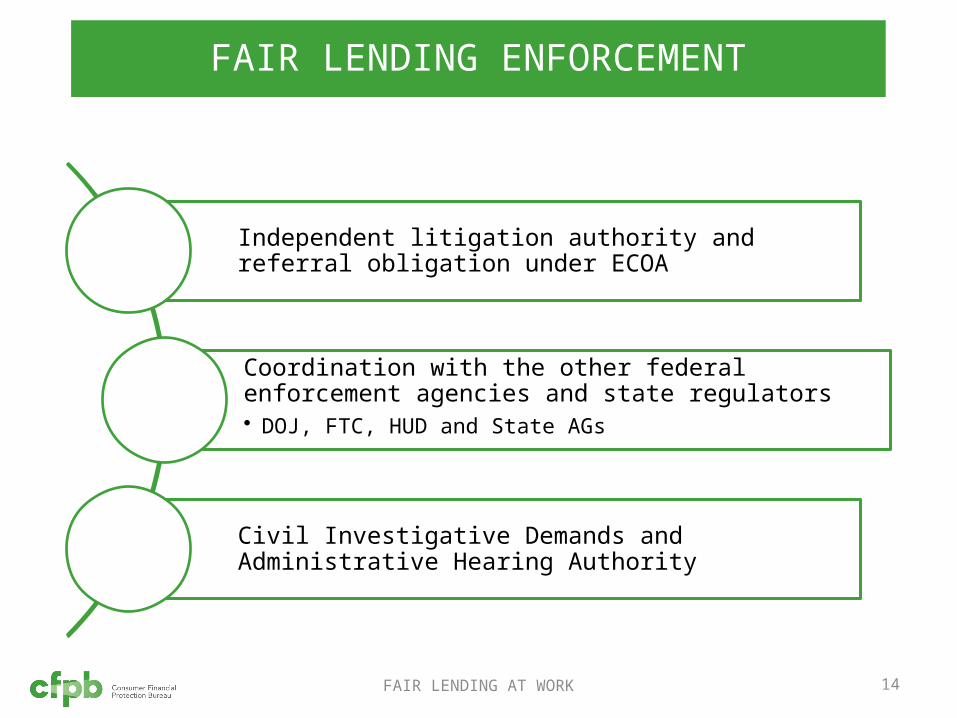

FAIR LENDING ENFORCEMENT

Independent litigation authority and referral obligation under ECOA

Coordination with the other federal enforcement agencies and state regulators• DOJ, FTC, HUD and State AGs

Civil Investigative Demands and Administrative Hearing Authority

FAIR LENDING AT WORK 15

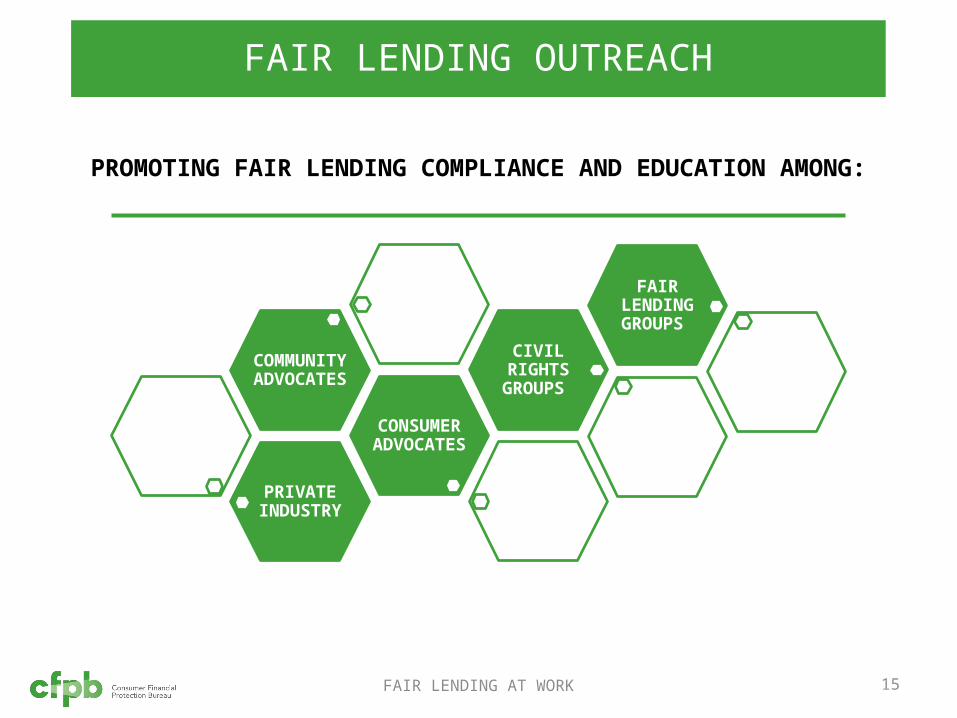

FAIR LENDING OUTREACH

PRIVATE INDUSTRY

CONSUMER ADVOCATES

COMMUNITY ADVOCATES

CIVIL RIGHTS GROUPS

FAIR LENDING GROUPS

PROMOTING FAIR LENDING COMPLIANCE AND EDUCATION AMONG:

FAIR LENDING AT WORK 16

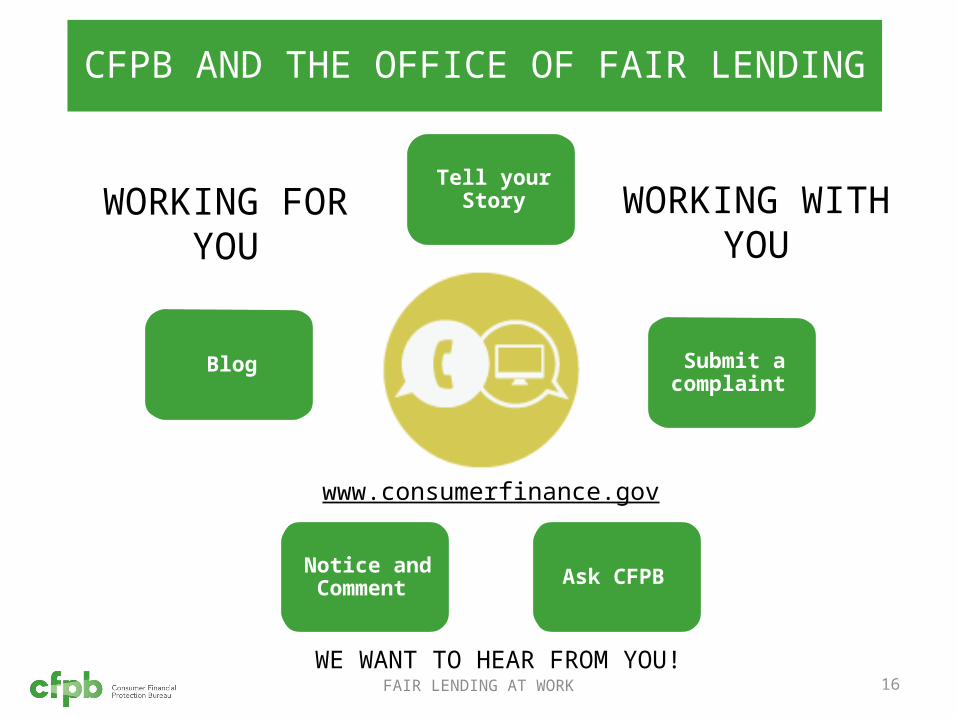

Tell your Story

Submit a complaint

Ask CFPB Notice and Comment

Blog

www.consumerfinance.gov

WE WANT TO HEAR FROM YOU!

CFPB AND THE OFFICE OF FAIR LENDING

WORKING FORYOU

WORKING WITHYOU