The constitutional and legal basis of public finance

22

THE CONSTITUTIONAL AND LEGAL BASIS OF PUBLIC FINANCE IN THE PHILIPPINES

-

Upload

masahiro-kobayashi -

Category

Law

-

view

4.583 -

download

2

Transcript of The constitutional and legal basis of public finance

THE CONSTITUTIONAL AND LEGAL BASIS OF PUBLIC

FINANCE IN THE PHILIPPINES

What is a legal basis? the justification for or reasoning behind

something.

A law based explanation how or why things are carried out in a certain manner

the underlying support or foundation for an idea, argument, or process.

What are the main aspects of Public Finance Administration Taxation

Budgeting

Accounting and Auditing

What is Taxation? Taxation is the inherent power of the

sovereign, exercised through the legislature, to impose burdens upon subjects and objects within its jurisdiction for the purpose of raising revenues to carry out the legitimate objects of government.

What is the essence of Taxation? The power of taxation proceeds upon

the theory that the existence of a government is a necessity; that it cannot continue without means to pay its expenses; and that for those means it has the right to compel all citizens and property within its limits to contribute.

Theoretical Basis of Taxation Life Blood Theory of Taxation

Social Contract Theory

Benefit Received Principle

Sources of Taxation Constitution Special laws or Statutes NIRC Administrative Rules and Regulations Administrative Rulings and Opinions Judicial Rulings or Jurisprudence

Kinds of taxes1. Income Tax2. Estate and donor's taxes3. Value-Added tax4. Other percentage taxes5. Excise taxes6. Documentary Stamp taxes7. Such other taxes as are or hereafter may

be imposed and collected by the Bureau of Internal Revenue

Limitations of the Power to Tax Limitation means a legally specified period

beyond which an action may be defeated or a property right is not to continue

Two Classes of tax limitations

Inherent Limitations

Constitutional Limitations

Constitutional Limitations Due process of law (sec. 1Art. III) Rule of uniformity and equity in taxation (sec 28(1)Art VI) No imprisonment for non-payment of poll tax (sec. 20, Art III) Non-impairment of obligations and contracts (sec 10, Art III) Prohibition against infringement of religious freedom (Sec 5, Art III) Prohibition against appropriations for religious purposes (sec 29,

(2) Art. VI) exemption of all revenues and assets of non-stock, non-profit

educational institutions used actually, directly, and exclusively for educational purposes from income, property and donor’s taxes and custom duties (sec. 4 (3 and 4) art. XIV.)

Concurrence by a majority of all members of Congress in the passage of a law granting tax exemptions. (Sec. 28 (4) Art. VI.)

Inherent Limitations Purpose. Taxes may be levied only for public

purpose; Territoriality. The State may tax persons and

properties under its jurisdiction; International Comity. the property of a foreign

State may not be taxed by another. Exemption. Government agencies performing

governmental functions are exempt from taxation Non-delegation. The power to tax being

legislative in nature may not be delegated. (subject to exceptions)

The process of Taxation Taxation is a Legislative function since a Statute is required to

enable the Executive branch to initiate tax collection. However, it is the Executive department who issues the

recommendations to Congress regarding the effectiveness of the tax statutes.

All aspects of tax policy formulation and implementation is principally handled by the Department of Finance.

The Secretary of Finance is the key recommendatory position to the President when it comes to concerns about the tax policies.

With such, the Executive formulates its recommendations to the Congress for it legislate statutes which will be implemented by the Department of Finance through the Bureau of Internal Revenue and the Bureau of Customs.

What is Budgeting? In general, a government budget is the

financial plan of a government for a given period, usually for a fiscal year, which shows what its resources are, and how they will be generated and used over the fiscal period. The budget is the government's key instrument for promoting its socio-economic objectives.

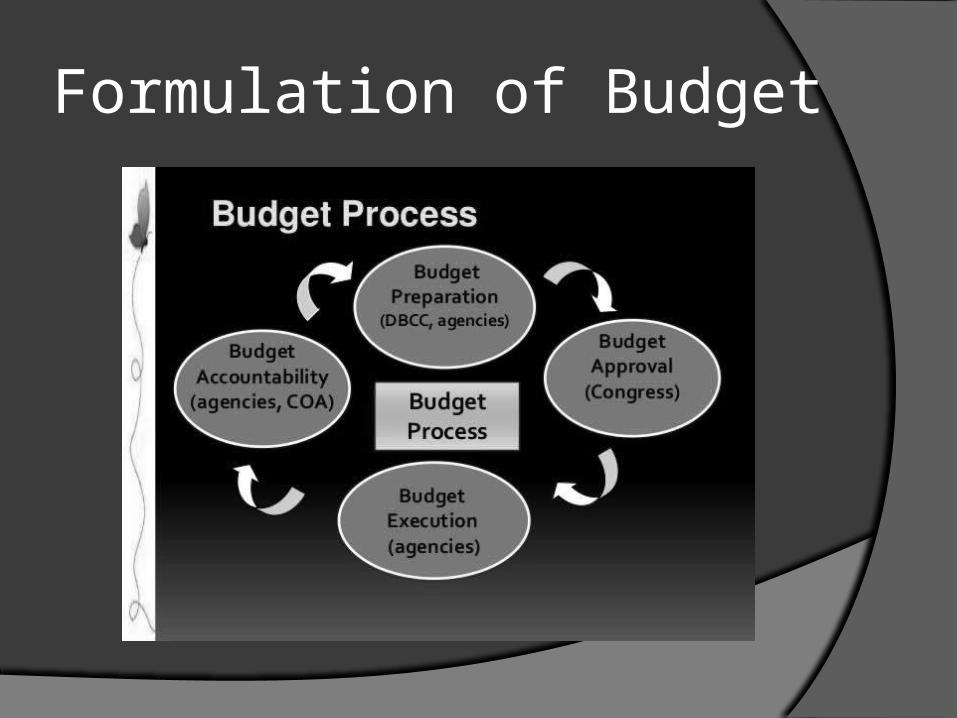

Formulation of Budget

Constitutional Basis of Budgeting Section 24, Article VI, which states that all appropriations, revenue

or tariff bills increase of the public debt, bills of local application and private bills shall originate in the House of Representatives, but the Senate may propose or concur with amendments

Section 25 (1), Article VI, states that the Congress may not increase the appropriations recommended by the President for the operation of the government as specified in the budget. The form, content, and manner of preparation of the budget shall be prescribed by law.

Section 25 (2), Article VI states that no provision or enactment shall be embraced in the General Appropriations Bill unless it relates specifically to some particular appropriation therein. Any such provision or enactment shall be limited in its operation to the appropriations to which it relates.

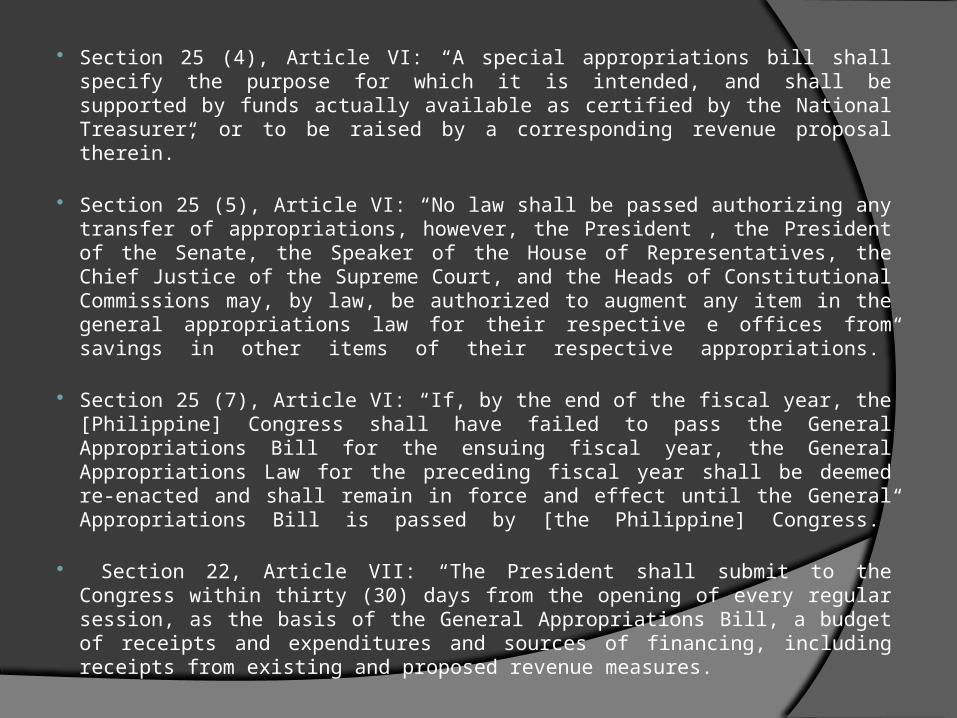

Section 25 (4), Article VI: “A special appropriations bill shall specify the purpose for which it is intended, and shall be supported by funds actually available as certified by the National Treasurer, or to be raised by a corresponding revenue proposal therein.”

Section 25 (5), Article VI: “No law shall be passed authorizing any transfer of appropriations, however, the President , the President of the Senate, the Speaker of the House of Representatives, the Chief Justice of the Supreme Court, and the Heads of Constitutional Commissions may, by law, be authorized to augment any item in the general appropriations law for their respective e offices from savings in other items of their respective appropriations.”

Section 25 (7), Article VI: “If, by the end of the fiscal year, the [Philippine] Congress shall have failed to pass the General Appropriations Bill for the ensuing fiscal year, the General Appropriations Law for the preceding fiscal year shall be deemed re-enacted and shall remain in force and effect until the General Appropriations Bill is passed by [the Philippine] Congress.”

Section 22, Article VII: “The President shall submit to the Congress within thirty (30) days from the opening of every regular session, as the basis of the General Appropriations Bill, a budget of receipts and expenditures and sources of financing, including receipts from existing and proposed revenue measures.

Restrictions on Budgeting The President has exclusive right to propose a budget. Congress can only reduce or reallocate appropriations in the

proposed budget. The President can use a line-item veto. The previous year’s budget is automatically “re-enacted” if

the budget is not passed prior to the start of the fiscal year. The President can impose restrictions on the disbursement

of funds appropriated by Congress. The President can augment any appropriations from savings

in other appropriations. Highest allocation to Education Separation of Church and State Special Funds are for Special funds only

Accounting and Auditing Accounting is defined as "the art of recording,

classifying and summarizing, in a significant manner and in terms of money, transactions and events which are, in part at least of a financial character and interpreting the results thereof." Its primary function is to measure and communicate financial and business data as it gives meaning to financial reports by explaining the results of transactions in terms of profit and loss and current financial positions.

Auditing on the other hand is the examination of information by a third party than the preparer or user with the intention of establishing its reliability, and the reporting of the results of this examination with the expectation of increasing the usefulness of the information of the user.

Justification of Accounting and Auditing (COA) The Commission has the power, authority and

duty to examine, audit and settle all accounts and expenditures of the funds and properties of the Philippine government. Towards that end, it has the exclusive authority to define the scope, techniques and methods of its auditing and examination procedures. It also may prevent and disallow irregular, unnecessary, excessive, extravagant or unconscionable expenditures, or uses of government funds and properties

Constitutional Provision and Legal BasisArticle IX (D), Section 2 of the 1987

Constitution is the prime basis of accounting and auditing of public finance.

The Audit Code of the Philippines (P.D. 1445)

ReferencesBooks

Hector De Leon, Text Book on Philippine 1987 ConstitutionHector De Leon, The Law on Income TaxationLeonor M. Briones, Philippine Public Fiscal Administration, Fiscal Administration Foundation Inc.

Mandaluyong, 1996

Online References

http://www.gov.ph/the-philippine-constitutions/the-1987-constitution-of-the-republic-of-the-philippines

http://www.gov.ph/1987/07/25/executive-order-no-292http://www.transparencyreporting.net/index.phphttp://hrepreflibrarian.wordpress.com/2013/03/07/the-budget-process-the-philippine-congress/https://ideas.repec.orghttp://www.oecd.org/countries/philippines/48170279.pdfhttp://www.dbm.gov.phhttp://www.lawphil.net/administ/coa/coa.htmlhttp://tax71.blogspot.com/2009/06/limitations-on-power-of-taxation.html