THE COMPETITIVE POSITION OF THE UK DAIRY INDUSTRY IN EUROPE

11

over the transition from traditional methods to today’s technology. He has given us a paper which I am sure will be even more interesting to read than it has been to listen to, partly because there is so much in it that it requires to be read to be appreciated in full. I have known Professor Crossley since before he was a Professor, and in those days, of course, he was in the hard world of commerce, before he sailed into the relatively still waters of university life. Although he was not the first holder of the title of Professor of Dairying, he was in fact the first active Professor of Dairying, and those of us who have had the opportunity to see the development of the work of that Chair since active work began, immediately after the war, realize just how much influence Professor Crossley has had, not merely in giving advice to all sorts of people, and also media, but in training so many of those who have come up into the industry, and, as you have said your- self, so many who are now authorities in their own field; and they, many of them, were put on this road by Professor Crossley. His talk today must, for many of us older people, have brought back a great many memories of development, and I think the thing which impressed me most, listening to him, is to realize that, in almost every one of these fields of development which he has briefly surveyed, he himself has played an important part, and this is something which perhaps younger people will not know out of their own experience, but I hope it is something that they will bear in mind when they come to read this paper. So, on behalf of the members of the Society, Professor Crossley, may I express our thanks for your paper. BY JAMES MORTON Managing Director, Milk Marketing Board The importance of equality between EEC countries to provide for fair competition is emphasized and the gap between UK and other Community producers in costs and returns examined. Comparisons are made of climatic conditions, herd size, genetic quality of the dairy herd, utilization of artificial insemination for breed- ing, yields achieved/cow and the provision of dairy husbandry services, such as herd yield prediction from computerized records. The need for improvements in animal health in the UK, particularly eliminating brucellosis and controlling mastitis, is stressed. Transport and bulk collection of milk, standardization, retail distribution and the economics of processing and manufacturing are discussed. Tables indicate the level and trends in consumption of milk and dairy products, which are more encouraging in the UK than elsewhere in the Community. The need to improve the application of basis research findings is mentioned, as is the desirability of closer links between the industry and the Ministry. The author concludes that the UK industry has a competitive advantage that all involved in it should strive to maintain. It must be clear to everyone who reads the press, and it is certainly clear to all of us who are here to-day, that the dairy industry in the United Kingdom is at present struggling. By contrast with our difficult situation, milk production in the rest of the EEC was expanding slightly in the first six months of this year. Some countries were increasing rapidly - the Netherlands by 3.9 per cent ard the Irish Republic by as much as 7.4 per cent compared with the same period in the year before. In the face of figures like these, what future can there be for the dairy industry in this country? The future is still bright; make no mistake about that. You may think that only an incurable optimist could make such a statement at the present time; that is why I think it is well worth while to take 14 Journal of the Society of Dairy Technology, Vol. 29, No. 1, January, 1976

-

Upload

james-morton -

Category

Documents

-

view

213 -

download

1

Transcript of THE COMPETITIVE POSITION OF THE UK DAIRY INDUSTRY IN EUROPE

over the transition from traditional methods to today’s technology. He has given us a paper which I am sure will be even more interesting to read than it has been to listen to, partly because there is so much in it that it requires to be read to be appreciated in full.

I have known Professor Crossley since before he was a Professor, and in those days, of course, he was in the hard world of commerce, before he sailed into the relatively still waters of university life. Although he was not the first holder of the title of Professor of Dairying, he was in fact the first active Professor of Dairying, and those of us who have had the opportunity to see the development of the work of that Chair since active work began, immediately after the war, realize just how much influence Professor Crossley has had, not merely in giving advice to all sorts of people, and also media,

but in training so many of those who have come up into the industry, and, as you have said your- self, so many who are now authorities in their own field; and they, many of them, were put on this road by Professor Crossley.

His talk today must, for many of us older people, have brought back a great many memories of development, and I think the thing which impressed me most, listening to him, is to realize that, in almost every one of these fields of development which he has briefly surveyed, he himself has played an important part, and this is something which perhaps younger people will not know out of their own experience, but I hope it is something that they will bear in mind when they come to read this paper.

So, on behalf of the members of the Society, Professor Crossley, may I express our thanks for your paper.

BY JAMES MORTON

Managing Director, Milk Marketing Board

The importance of equality between EEC countries to provide for fair competition is emphasized and the gap between UK and other Community producers in costs and returns examined. Comparisons are made of climatic conditions, herd size, genetic quality of the dairy herd, utilization of artificial insemination for breed- ing, yields achieved/cow and the provision of dairy husbandry services, such as herd yield prediction from computerized records. The need for improvements in animal health in the UK, particularly eliminating brucellosis and controlling mastitis, is stressed. Transport and bulk collection of milk, standardization, retail distribution and the economics of processing and manufacturing are discussed. Tables indicate the level and trends in consumption of milk and dairy products, which are more encouraging in the UK than elsewhere in the Community. The need to improve the application of basis research findings is mentioned, as is the desirability of closer links between the industry and the Ministry. The author concludes that the UK industry has a competitive advantage that all involved in it should strive to maintain.

It must be clear to everyone who reads the press, and it is certainly clear to all of us who are here to-day, that the dairy industry in the United Kingdom is at present struggling. By contrast with our difficult situation, milk production in the rest of the EEC was expanding slightly in the first six months of this year. Some countries were increasing rapidly - the Netherlands by 3.9 per cent ard the Irish Republic by as much as 7.4

per cent compared with the same period in the year before.

In the face of figures like these, what future can there be for the dairy industry in this country? The future is still bright; make no mistake about that.

You may think that only an incurable optimist could make such a statement at the present time; that is why I think it is well worth while to take

14 Journal of the Society of Dairy Technology, Vol. 29, No. 1, January, 1976

a cool and realistic look at the comparative strengths and weaknesses of our dairy industry, compared with those of the rest of the European Community. We should have no false modesty in recognizing that in many ways we are ahead of the rest of Europe - there is a danger at this time of too much despondency. Nobody is more aware than the Milk Marketing Board of the difficult time that farmers and indeed all engaged in dairying have gone through in recent years. Nevertheless, we will do ourselves no good if we lead Government and others to believe that we are incapable of recovery and that expansion in milk production is not something that this country can afford to pay for. There is no doubt in my mind that the industry both can and would expand given reasonable terms. But I would not like you to go away from here believing that, if only we could get the cash, we could relax and everything else would come right. Our com- petitors, as most of us here know, are working hard to improve the productivity of their indust- ries and we must do the same; in some respects they are ahead of us, and one of the things that I want to do in presenting this paper is to draw attention to those aspects of the industry where we have to work particularly hard to ensure that dairying in the UK remains in the forefront of dairying in the EEC. But before turning to these issues, it is necessary to spend a little time analys- ing why milk production went into decline and what the chances are of reversing the trend.

The parity issue Until mid 1973 the industry seemed all set for expansion, but then along came the explosion in world prices of feeding stuffs, due to relatively poor harvests in many parts of the world and the purchase by Russia of most of the reserve grain stocks of the United States. The oil crisis arrived at much the same time, pushing up costs of many important farm inputs, particularly fertilizers and fuel. Farmers were, therefore, faced with an unprecedented rise in prices, but unfortunately, Government response to the situation was, to quote the NFU President, ‘too little and too late’. What we in the industry had hoped would only be a minor hiccough in the expansion programme has turned out to be very much more severe. The weather too has not helped, particularly in the south of the country, with farmers initially unable to turn herds out to grass as early as normal, followed aggravatingly by a great sum- mer for tourists but not so good for cows. The weather has certainly been an added blow, but even with a normal season dairy farmers would have been struggling. Essentially, this is because milk producers have now had two years when costs have raced ahead of returns, so that they have had to pay as much for inputs as their com-

petitors in other Community countries without getting the equivalent price for their milk. Be- cause of the failure of successive governments to react promptly to the situation, the industry is desperately short of cash and has been pushed into a decline. I do not think for one moment that the decline is irreversible, but before we can halt the trend and get back on to the path of expansion it is essential that we are put into a position of parity with producers in the rest of the Community.

The recent change in the green pound rate means a guaranteed price, from 1st November, of 40*02p/gal for the UK or 37*04p/gal for the 1975/76 year as a whole. By comparison, the Community target price, if the green pound were fully devalued, is equivalent to 44*35p/gal for milk of 3.7 per cent butterfat-as is known average quality in the UK is a little above this level. So we are still well behind on the price paid for milk, but there are other factors to take into account. For example, we are convinced that at the end of transition we could earn, if Government permits it, a significant premium over the target price from our large liquid market.

It is often forgotten that there are other aspects of returns and costs, quite apart from the milk price itself, where we are suffering compared with competitors in other European countries. The value of calves and young stock sold from dairy herds is an important factor in total farm income. In September, the average price in England and Wales for first quality Friesian bull calves was almost €30/head; by comparison, farmers in the Netherlands were realizing about €73 /head, in West Germany about €67/head and in France €77-€88 a head. We also lagged behind on the fat steer and heifer prices. For cull cows the price in England and Wales in September was €13,65/live cwt; in Italy it was €28.18; West Germany €27.07 and over €40.00 in France. By the end of transition it is not unreasonable to hope that the dairy farmer in the United King- dom will be doing significantly better from his sales of stock,

Parity between EEC countries in conditions and returns from milk production means so many things. We need to be sure one country does not have a hidden advantage over another. This is a highly complex field and includes the policies of individual countries in such things as income tax liability of farmers; the way VAT is handled; subsidized credit, availability of grants, policies regarding service houses and so on. I t is up to Government to ensure that the dairy industry in the UK fares no worse than our European friends. We have been given every assurance that Government will stand by the ‘Food from our own Resources’ White Paper. Taking a leaf out

Journal of the Society of Dairy Technology, Vol. 29, No. 1 , January. 1976

C

1s

of other Europeans' books and devising means to encourage investment on the farm would be one of the most positive steps that could be taken at the present time. The main theme of this paper is to consider whether, given reasonable parity, the dairy industry can compete and com- pete effectively with other EEC countries. I hope most of us here are in no doubt that we can, but it does no harm to look at some of our strengths and weaknesses. It is a vast subject and on many areas it is difficult to obtain information and make valid comparisons. Of necessity it is not possible to go into any aspect in depth but instead to paint a rather broad picture.

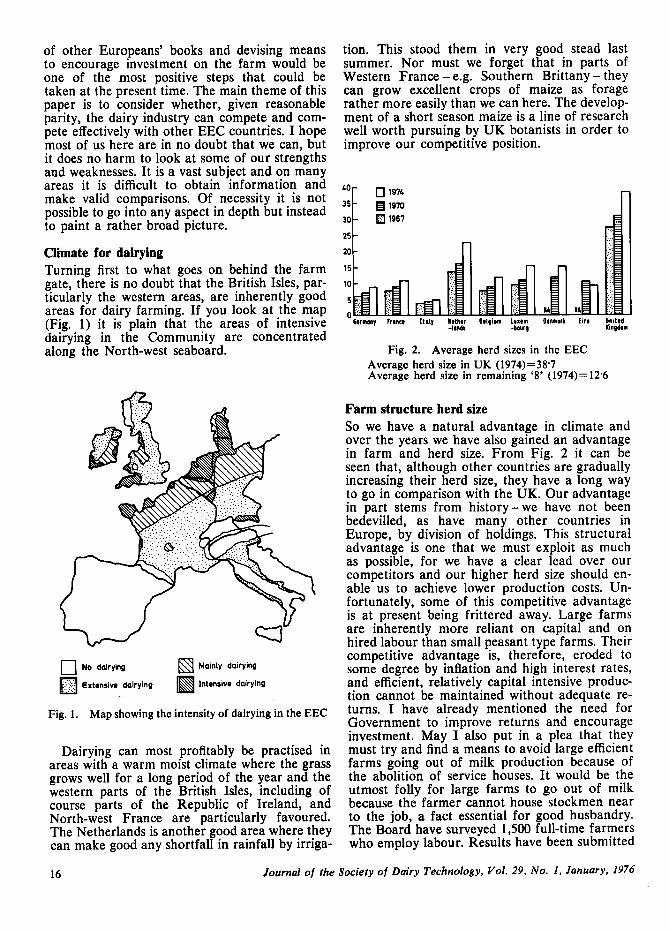

Climate for dairying Turning first to what goes on behind the farm gate, there is no doubt that the British Isles, par- ticularly the western areas, are inherently good areas for dairy farming. If you look a t the map (Fig. 1) it is plain that the areas of intensive dairying in the Community are concentrated along the North-west seaboard.

0 No dairying Moinly dairying

Extensive dairying Intensive dairying

Fig. 1. Map showing the intensity of dairying in the EEC

Dairying can most profitably be practised in areas with a warm moist climate where the grass grows well for a long period of the year and the western parts of the British Isles, including of course parts of the Republic of Ireland, and North-west France are particularly favoured. The Netherlands is another good area where they can make good any shortfall in rainfall by irriga-

tion. This stood them in very good stead last summer. Nor must we forget that in parts of Western France - e.g. Southern Brittany - they can grow excellent crops of maize as forage rather more easily than we can here. The develop- ment of a short season maize is a line of research well worth pursuing by UK botanists in order to improve our competitive position.

6arnnny frnnoi 1101y l i t b a r Bil(lun Lu:m Otnnnrk I l r i United 4rnk -bow9 Kingdom

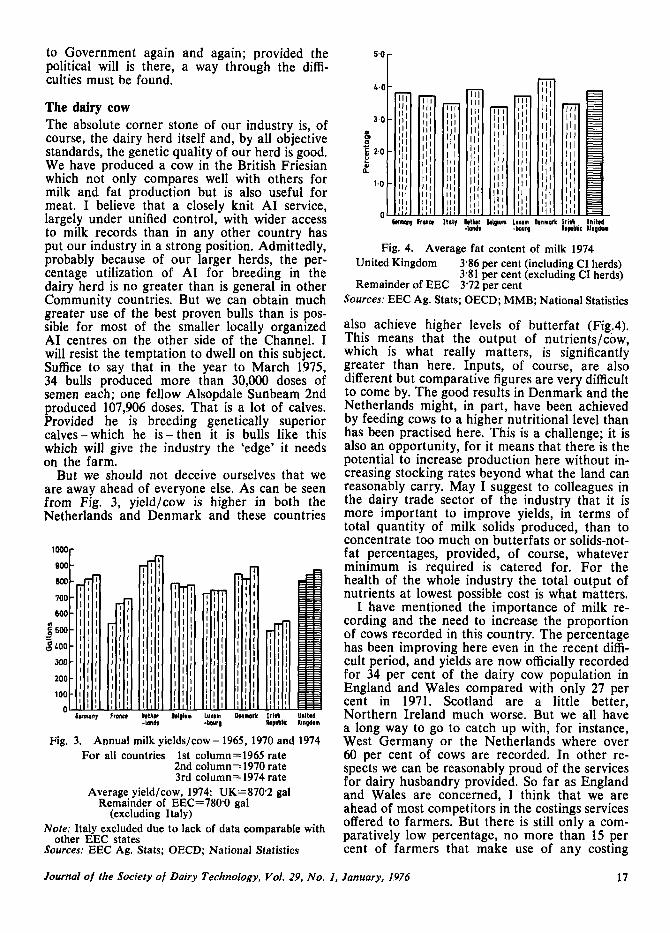

Fig. 2. Average herd sizes in the EEC Average herd size in UK (1974)=38.7 Average herd size in remaining '8' (1974)= 12.6

Farm structure herd size So we have a natural advantage in climate and over the years we have also gained an advantage in farm and herd sue. From Fig. 2 it can be seen that, although other countries are gradually increasing their herd size, they have a long way to go in comparison with the UK. Our advantage in part stems from history-we have not been bedevilled, as have many other countries in Europe, by division of holdings. This structural advantage is one that we must exploit as much as possible, for we have a clear lead over our competitors and our higher herd size should en- able us to achieve lower production costs. Un- fortunately, some of this competitive advantage is at present being frittered away. Large farms are inherently more reliant on capital and on hired labour than small peasant type farms. Their competitive advantage is, therefore, eroded to some degree by inflation and high interest rates, and efficient, relatively capital intensive produc- tion cannot be maintained without adequate re- turns. I have already mentioned the need for Government to improve returns and encourage investment. May I also put in a plea that they must try and find a means to avoid large efficient farms going out of milk production because of the abolition of service houses. I t would be the utmost folly for large farms to go out of milk because the farmer cannot house stockmen near to the job, a fact essential for good husbandry. The Board have surveyed 1,500 full-time farmers who employ labour. Results have been submitted

16 Journal of the Society of Dairy Technology, Vol. 29, No. 1. January, 1976

to Government again and again; provided the political will is there, a way through the diffi- culties must be found.

6wmonr franc8 Irths B8Il)mm Luarm Ommor

The dairy cow The absolute corner stone of our industry is, of course, the dairy herd itself and, by all objective standards, the genetic quality of our herd is good, We have produced a cow in the British Friesian which not only compares well with others for milk and fat production but is also useful for meat. I believe that a closely knit A1 service, largely under unified control, with wider access to milk records than in any other country has put our industry in a strong position. Admittedly, probably because of our larger herds, the per- centage utilization of A1 for breeding in the dairy herd is no greater than is general in other Community countries. But we can o'btain much greater use of the best proven bulls than is pos- sible for most of the smaller locally organized A1 centres on the other side of the Channel. I will resist the temptation to dwell on this subject. Suffice to say that in the year to March 1975, 34 bulls produced more than 30,000 doses of semen each; one fellow Alsopdale Sunbeam 2nd produced 107,906 doses. That is a lot of calves. Provided he is breeding genetically superior calves- which he is- then it is bulls like this which will give the industry the 'edge' it needs on the farm.

But we should not deceive ourselves that we are away ahead of everyone else. As can be seen from Fig. 3, yield/cow is higher in both the Netherlands and Denmark and these countries

rish Unitad

700

600

g 500 d - $400

300

200

100 n

Fig. 4. Average fat content of milk 1974 United Kingdom 3.86 per cent (including CI herds)

3.81 per cent (excluding CI herds) Remainder of EEC 3.72 per cent

Sources: EEC Ag. Stats; OECD; MMB; National Statistics

also achieve higher levels of butterfat (Fig.4). This means that the output of nutrients/cow, which is what really matters, is significantIy greater than here. Inputs, of course, are also different but comparative figures are very difficult to come by. The good results in Denmark and the Netherlands might, in part, have been achieved by feeding cows to a higher nutritional level than has been practised here. This is a challenge; it is also an opportunity, for it means that there is the potential to increase production here without in- creasing stocking rates beyond what the land can reasonably carry. May I suggest to colleagues in the dairy trade sector of the industry that it is more important to improve yields, in terms of total quantity of milk solids produced, than to concentrate too much on butterfats or solids-not- fat percentages, provided, of course, whatever minimum is required is catered for. For the health of the whole industry the total output of nutrients at lowest possible cost is what matters.

I have mentioned the importance of milk re- cording and the need to increase the proportion of cows recorded in this country. The percentage has been improving here even in the recent diffi- cult period, and yields are now officially recorded for 34 per cent of the dairy cow population in England and Wales compared with only 27 per cent in 1971. Scotland are a little better, Northern Ireland much worse. But we all have a long way to go to catch up with, for instance, West Germany or the Netherlands where over 60 per cent of cows are recorded. In other re- spects we can be reasonably proud of the services for dairy husbandry provided. So far as England and Wales are concerned, I think that we are ahead of most competitors in the costings services offered to farmers. But there is still only a com- paratively low percentage, no more than 15 per cent of farmers that make use of any costing

Journal of the Society of Dairy Technology, Vol. 29, No. 1, January, 1976 17

services. The strength of the services available to dairy farmers is, in my view, twofold. First, they have been introduced to meet the commer- cial needs of farmers and they are operated on a commercial basis. New services can be introduced where the need exists; in marketing jargon the art is to introduce the service before the farmer knows the need is there. The second strength lies in the fact that many of the services are con- trolled by the one management. This permits use of computerized data right across the board. Once, for instance, a milk record is in the com- puter it can be used in a host of ways by sister services. Probably the most exciting example is a service known as Herd Management Control by which using a statistical technique a cow’s annual lactation curve can be ‘drawn’ based on age, previous lactation, time of calving etc. Put all the curves together and herd production for the year ahead can be predicted and plotted; per- formance can be monitored all the time against prediction. It is a sophisticated tool of manage- ment-a budgeting procedure if you like. It is vital that the industry continues to lead in developments such as Herd Management Control.

Another important field includes new services to cover pregnancy diagnosis and heat syn- chronization - services so important where aver- age herd size is large. We lead the competition in this field.

Animal health The health of our dairy herd is another factor of vital economic importance. Here our situation, by comparison with other countries of the Com- munity, is rather patchy. The wisdom of Govern- ments in the past has kept this country clear of foot-and-mouth disease. This is of great benefit to our export trade in livestock. We are free of bovine tuberculosis. So too are Denmark and the Netherlands but some other EEC countries have a long way to go.

On the other hand, with the exception of Northern Ireland, we have not done so well on brucellosis. Denmark and the Netherlands are already clear of this disease whilst nearly 40 per cent of the dairy herd in England and Wales has yet to be accredited. To my mind we are not going ahead fast enough. The Board and the NFU have for some time now been pressing the Ministry to speed up the eradication programme and to improve incentives. The longer we delay on this the more we give advantage to the Dutch and Danes.

Control of mastitis is another area in which we cannot be satisfied with our present position. Sub- clinical mastitis is the major disease of present day dairy herds, causing losses in milk volume and quality which we can ill afford combined with a reduced life for our dairy cows. Denmark and

the Netherlands have made the most strenuous efforts to eliminate the disease. In Denmark the Government has subsidized mastitis control measures since 1964 and the number of herds with a cell count in excess of 500,000 has declined from about 39 per cent in 1968 to 20 per cent in 1972. The Netherlands have also organized a National Mastitis Control Scheme with state and industry services operating in partnership. In 1971 only about 5 per cent of the milk supplied in churns and 1 per cent of the milk collected by tanker contained more than one million cells/ml. Whilst it is true that a great deal of useful work has already been done by the NIRD, the Milk Marketing Boards and the other advisory ser- vices in this country, this is really an area where we need to do more.

Transport and bulk collection Turning now to the far side of the farm gate, we in the Board have little doubt, both from what we have seen abroad ourselves and from the comments of those who have come to visit us, that in arrangements for moving milk from farm to dairy and rationalization of milk fields, we are ahead of most of our competitors. We have, of course, an advantage in the larger average size of pick up. We have also had more success than other countries in rationalizing milk fields and making the most economic use of vehicles. In terms of volume of milk collected/vehicle a day, only the Netherlands with their very intensive pattern of milk production can match us. We also seem to be ahead in the development of bulk collection and refrigeration of milk on the farm. Scotland is already almost 100 per cent bulk, England and Wales now about 85 per cent and Northern Ireland not far behind. National statis- tics for other countries are not easy to come by but they are certainly not up with the UK at present, although I suspect our advantage may be comparatively short-lived because all the major European dairying countries are now going over to bulk collection as fast as they can. One note- worthy difference with other European countries is that in the UK the Milk Marketing Board’s specification for farm vats requires faster cooling rates than in the other EEC countries. We con- sider this important to get milk down in tem- perature quickly, so that there is adequate time for tankers to get in two runs between first and second milking. If the average herd size in other EEC countries increases, as I am sure it must, I suspect this slower rate of cooling may eventually cause them some difficulty.

Quality control Once the milk arrives at the dairy methods of quality control, and the effect that these have on

18 Journal of the Society of Dairy Technology, Vol. 29, No. 1, January, 1976

production costs at the farm are certainly im- portant. On hygienic quality there seems to me a basic difference of philosophy between ourselves and other EEC countries. Our view is essentially that the same standard of marketability should apply to all milk eventually destined for human consumption in some form irrespective of whether it is to be sold liquid or manufactured. If we are to compete on an equal footing, it is important that producers here should not be put at a competitive disadvantage by being asked to meet higher standards than their counterparts across the Channel.

We cannot be selective here about which milk goes to manufacturing and which to the liquid market, everything must be suitable for the liquid market. May I pose the question - a controversial one - of whether there is a danger of insisting on too perfectionist standards. Please do not think I am advocating allowing producers to get away with slovenly production methods. Far from it, but what I do think is that standards should be realistic in relation to public health, consumer acceptance and, last but not least, the economics of milk production. In these hard times, we must not forget that time is money on the farm and that if a farmer has to spend longer preparing his cows for milking this inevitably increases his costs. The key question is whether the dairy is prepared to pay sufficient money to justify these extra costs and, of course, the dairy can only afford to do so if, in its turn, it can obtain suffici- ent extra revenue from improved quality of products or liquid milk. If I say more the bacteriologists in the audience will probably con- sider me a suitable subject for germ warfare so I had better move rapidly on to the question of compositional quality.

Our producer payments system is on the basis of total solids, whereas in most of the rest of the Community producers are paid on butterfat, in a few cases butterfat and protein. Our method of payment certainly places a higher value on the SNF fraction of milk than is usual across the Channel; this could well be a good thing, par- ticularly in view of the recognition by nutrition- ists of the value of protein. Another major difference between ourselves and all other con- tinental countries is that at present milk is sold by the marketing boards to dairies at a uniform price, regardless of compositional quality varia- tion. This undoubtedly reduces our marketing and administrative costs and makes life simpler for all concerned. Whether or not we shall be able to maintain this small competitive advan- tage, in view of the threat of standardization still hanging over the industry, is another matter. Milk processing and Liquid market Once the milk has arrived at the dairy the opera-

tions of our industry are of course very different from most of those in the other EEC countries. To start with the majority of the milk goes to the liquid market. This should certainly be an advantage to the UK because this market is pro- tected to some extent by the costs of transporting milk across the Channel or the Irish Sea, al- though we will eventually have to face up to the threat of imports of liquid milk when the various regulations are amended.

Dairymen in other EEC countries, and even Commission officials, often look upon us as old fashioned because we are still packaging non- standardized milk in glass, and delivering it to the doorstep. It can be argued that this system does in fact give us a competitive advantage. To start with, processing costs for packaging milk in glass are lower than the costs for packaging in cartons or any other non-returnable container. The glass bottle is the most acceptable container so far as the consumer is concerned, provided it is delivered to the door. Our present system of household delivery helps us to maintain high levels of per capita consumption. As can be seen from Tables 1 and 2 (p. 20) both the trend and the level of liquid consumption in this country has been very much more encouraging than anywhere in the Community except Italy, where they scarcely drank any milk to start with anyhow, and the Republic of Ireland. Selling milk ‘as it comes from the cow’, rather than standardized, is also to my mind, a competitive advantage, not the reverse, although I am afraid that not all Com- mission officials would agree, and the question of whether we shall have to standardize or not still hangs in the balance. One thing is certain; the case against standardization has been well put. Excellent work has been done in Brussels by both the DTF and Board people.

The issue now exercising the minds of many of us is whether it will be possible to maintain the home delivery service in the future in the face of possible competition from the shops. Let me say first that I think it is absolutely right that we should do everything we possibly can to maintain the home delivery service. We have no quarrel with the sale of groceries on the rounds if this helps to improve profitability for the dairyman. The better the service given to the consumer the better the chance of maintaining home delivery. It seems that in Scotland one of the major factors leading to the increase in shop sales has been the lower quality of the service on the rounds. This is a lesson that I trust we in England and Wales will heed. But, just as we at the producer end must do everything we can to increase efficiency in milk production, so should the retail trade at its end of the business. The shop trade won’t go away; if supermarkets don’t get what they want from UK suppliers they will look overseas. But

Journal of the Society of Dairy Technology, Yol. 29, No. I , January, 1976 19

TABLE 1 EEC consumption/head In 1974. In gallons of whole milk equivalent at 3.7 per cent BF

Skimmed* Total and whole Ranked

Whole semi-skimmed Condensed Cream milk by milk milks Yoghurt Butter Cheese milk 35 %fat equivalent consumption

~~~~~ _____ _ _ _ _ _ _ ~ _ _ _ _ ______ ~ _ _ _ _

Germany 12.5 3.6 1 s o 7 *4 19.1 4-1 2.3 46.4 5 France 14.2 0.7 1 -6 9.8 25.1 1 *o 0.6 52.3 3 .. -

2.6 18.9 nta nla 32.9 9 2.7 16-7 5.9 1 *4 45.3 6 Netherlands 15.8 4.0 2.8

Belgium 13.7 2.3 0.8 9 s o 15.6 2.3 0.8 42.2 8 Luxembourg 18.6 - 1 -0 7.7 12.0 1 *o 4.0 44.3 7

Italy 11.4 3 *2 nla

United Kinidom 39.5 - 0.4 8 *8 9 -9 1 -7 1 *4 61 *7 2 Denmark 15.7 8.8 2.5 8 *9 16.7 nla 4.9 48 *7 4 Eire 44.2 - 0.1 12.8 4.4 nla 2.1 63 *6 1

*Figures for ‘semi-skimmed and skimmed milks’ are for total volume consumed, without adjustment to whole milk equivalent at 3.7 per cent butterfat. The data are included to give an idea of the relative importance of skimmed and semi-skimmed fnilks in the various countries, but the whole milk equivalent is included under butter or cream - the volumes shown under Skimmed and semi-skimmed milks’ are therefore not added into the ‘Total whole milk equivalent’ column.

TABLE 2 Trends in consumption/head - 1965 to 1974 percentage change

Whole All li uid Condensed Total dairy milk mik Yoghurt Butter Cheese milk products

Germany France Italy Netherlands Belgium Luxembourg United Kingdom Denmark Eire

% % -28.8 -16.1 -15.7 -11.4

na + 8.6 -38.4 -22.8 -26.6 -15.5 - 10.7 -10.7 - 2-2 - 2.2 -44.2 - 17.2 - 4.7 - 4.7

% +181*3 + 89.7

na + 5.6 +117*6 + 51.6

na $404.3

na

% - 16.5 + 6.8 $31.6 -40.9 - 3.6 -26.0 - 3.4 - 14.9 -18.5

% + 42.5 +26*1 +31-4 $25.0 $78.8 + 14.3 + 28.3 + 12.4 + 52.9

% - 14.5 + 6.3

na + 1-0 $32.3 - 14.3 -11.8

na na

% - 18.3 - 4.8

na -29.1 - 14.9 - 9.1 - 0.9 -32.3 - 4.9

the best safeguard, surely, to the delivery service is to ensure that it is operated at as low a cost as is compatible with reasonable profits. Nothing can be taken for granted, whether it is frequency of delivery, rationalization or any aspect where there is a possibility of containing costs. I know that the DTF and the dairy companies are well aware of the problems and the need for continu- ous study in this vital area of operation. The producers too are vitally interested. Although the margin between the price of milk for manu- facture and for the liquid market will narrow, there will still be powerful economic reasons for keeping the liquid market as strong as possible - we have, therefore, a keen vested interest. My North East friends will not agree, but perhaps it is not altogether a bad thing that we are meeting a little competition in the North East of England from over the Scottish border at the present time. We have to face facts, however unpalatable they may be. My personal hope and aim is that, first by maintaining standards on the rounds, the amount of trade that moves into the shops will not be very large, and second, where milk is sold in shops it will continue to be British.

Products and manufacture As we get further and further towards the end of the transition, manufacturing milk, at least in terms of the return it earns, becomes more and more important to producers. Comparisons with other countries in the efficiency of manufacturing operations are exceedingly difficult, but we can say that the industry has been restructured so that manufacturing capacity is, in the main, well sited geographically and many of the smaller units have been replaced by large modern manu- facturing creameries. A great deal of money has been spent by dairy companies. The only trouble at present is finding the milk to put through the new plants. In 1973, at the peak of the production cycle, the index of manufacture for the year as a whole, taking May as a 100, was 60 per cent. Everywhere else in the Community, apart from the Republic of Ireland, where there is an ex- treme pattern of seasonality of milk production, the utilization of manufacturing plant was signifi- cantly better. In Germany the ratio of average to peak month was 79 per cent; in Denmark 75 per cent; Holland 72 per cent; France 73 per cent. Since that time, of course, our position has

20 Journal of the Society of Dairy Technology, Vol.’29. No. I . January, 1976

worsened. Milk production has gone down, whilst manufacturing capacity has increased, because the industry invested to deal with an expected ex- pansion in milk production which so far has not come about. This is a competitive disadvantage and the only cure is an expansion of milk pro- duction. If we do obtain this expansion, as we must, our market situation should be encouraging to the home manufacturer. As can be seen from the self-sufficiency ratios in Table 3, we are a long way off producing all the dairy products

TABLE 3 UK percentage self sufticiency by product

Product 1972173 1974175

Liquid milk 100 Cream 94 Butter 23 Cheese 57 Whole milk powder 77 Condensed milk 103 Chocolate crumb 78 Other milk products 100

Total 59 -

100 95 1 1 67 89 108 75

100

54 -

~ ~~~~

necessary to supply the home market. Although we must expect a contraction in the market for butter because of price increases as we go through to the end of the transitional period, the outlook for the cheese market is encouraging. But, as I said before, i t all comes to a question of whether the milk is going to be available to the manufacturers. Farmers have shown in the past that given reasonable encouragement they will produce what is needed. They will do so again when the encouragement is forthcoming.

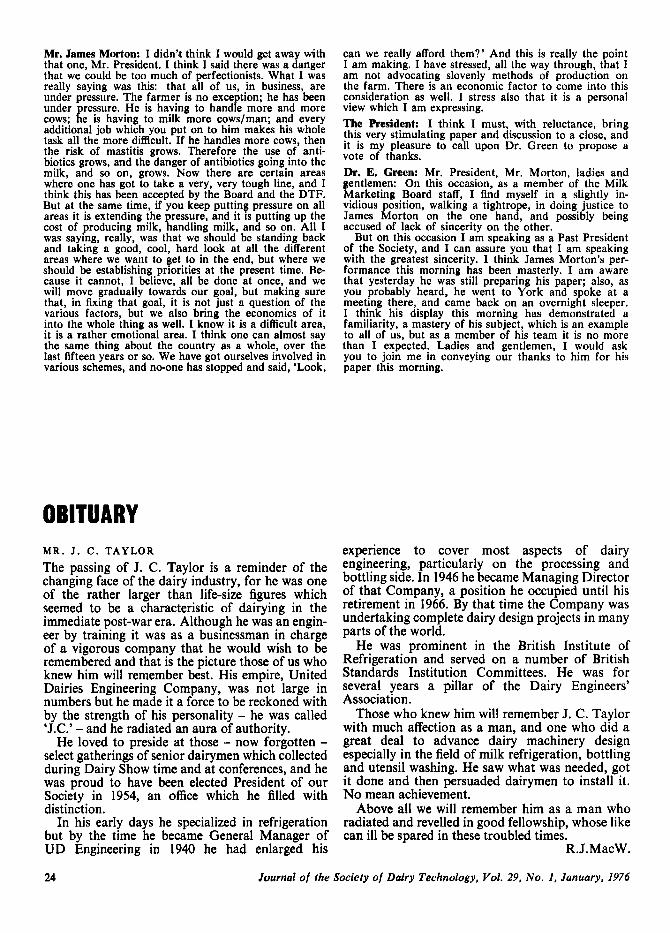

The figures in Table 4 concerning butter im- ports show how severely the balance of payments in this country must have suffered as a result of

the cut back in production and the consequent surge in imports. It also shows the way that the UK butter market has been ‘gifted’ to other countries in the Community.

Organizational structure Having thus, all too briefly, looked at the com- petitiveness of individual facets of the industry from farm to consumer, I would like to consider for a moment the organizational structure of the industry in this country, compared with the rest of the Community. It seems to me that we have the great advantage in this country of having an industry that is not too fragmented and which has become accustomed to working together. The producer and the trade sides of the industry do of course have their differences, but in general the working relationships seem to be very good and long may this continue. In the UK of course, the private dairy trade plays a very much larger part than in any other European country where producer and co-operatives tend to predominate. I would not think that this gives other EEC countries any competitive edge over us, and what does seem to be the advantage of our type of organization is that we can take decisions at a national level. The advantage of this for breeding and production has been mentioned earlier in the paper. On the industry side, the discussions that we have between the Board, the DTF and indi- vidual manufacturers have enabled us to avoid for instance the wasteful duplication of plant which seems to have occurred in some other countries. For example, there is no doubt that there has been very wasteful competition in Ger- many between dairies servicing the liquid market, largely because an excess of UHT capacity was installed. But one aspect of organizational struc- ture where perhaps we have something to learn

TABLE 4 UK production and imports (tons)

Butter: Home production and imports 1969 1972 1973 1974 1975

First six months

UK production 55,600 93,400 94,800 52,163 29,500 (estimate) Imports into the UK

EEC-West Germany - 240 2,783 35,589 28,964 France 2.632 2.445 3.781 30.675 21.376 - ...~~..

Netherlands ii&i 20;390 60;766 108;913 50;910 Belgium/Lux. - 7,379 4,880 10,976 5,168 Denmark 92,880 70,409 73,170 98,415 42,406 Irish Republic 23,680 35,844 38,539 35,977 18,978

Total 130,853 136,707 183,919 320,545 167,802 New Zealand 189,814 116.161 129,875 120,OS 1 49,833 Other countries 92,589 99,306 20,234 587 116

Total imports 413,256 352,174 334,028 441,183 217,751

Journal of the Society of Dairy Technology, Vol. 29, No. 1, January, 1976 21

from overseas is that of the lixiks between in- dustry and the Ministry of Agriculture. Our Ministry officials are hard working and able men. But I do think that they suffer, and that to some degree we suffer in consequence, from a lack of a really detailed inside knowledge of the industry. By contrast the links that for example the Dutch industry seem to have built up with the o@cials of their Ministry of Agriculture are stronger. With the exception of the Advisory Services, the Ministry here have’ perhaps traditionally looked upon themselves as the referee between the in-, dustry and the public. But in the new ball game of Europe they can no longer be in this position, not in Brussels. Here we must look on them, and I hope that they will look on themselves, as very much of a player, part of the team. Our success as an industry rests very considerably on their shoulders and I would personally like to see a greater exchange certainly of ideas and perhaps of personnel between the Ministry and the in- dustry than takes place at the moment. Research and development Finally, as I am speaking to the Society of Dairy Technology, I would like to say just a few words about the place of research and development. Research and the application of research will be vital to the success of our industry in the future. From personal experience, I know rather more about the farm side of the industry than proces- sing and manufacture. Certainly, on the farm side we have some excellent research institutes and our basic research is very good. As a nation, and I do not think this only applies to agriculture, we are not so good at a plying the findings of r e

established by research that it will pay a farmer handsomely to feed concentrates heavily at the start of a lactation and then cut them down to- wards the end. But the detail of what to do seems to be known to relatively few farmers and I won- der whether, as an industry, we do enough to get the results of our research across $0 that we make the most economic use of the resources available to us. So far as processing and manu- facture is concerned, many of my colleagues feel in some cases that there is a simdar gap between the research scientist and the practical dairy engineer. Certainly I was very concerned, at a recent discussion with the staff of the NIRD, to learn that they found it very difficult to find out what research would really be of benefit to pro- cessors and manufacturers. There is a gap here that needs to be bridged. We might do worse than to look carefully at the situation in Holland where the impression of many of my colleagues is that their research effort is achieving more, in terms of the end result of application in the industry, than is the case here. These are only

search. To take a simp P e example, it is now well

impressions and I may be being unfair. Never- theless, it would do none of us any harm to try to do better.

CONCLUSIONS I am very conscious that I have touched on a great number of subjects superficially, and have not had time to go into any one of them in depth. Nevertheless, I think that it is occasionally necessary to try to look at the subject in the round, however difficult this may be, and I have certainly found it difficult. My conclusion is that we have got an industry that on present form can compete with any in Europe given parity of op- portunity. Government policy is still based on the White Paper ‘Food from our own Resources’. We must all do our utmost to see that this policy is implemented. When Government first issued the White Paper one criticism levelled was that the Community could never allow this country to expand milk production at a time when the Community as a whole was moving into surplus. I would contend that our competitive situation is such that, given parity - and that is paramount -we would be capable of expanding even if milk production in some other EEC countries was forced to contract. Do not forget that, just as we at present have an artificial handicap so others have an artificial advantage. The ‘Green Mark‘ rate of exchange means the German producers are at present receiving prices nearly 10 per cent higher than they should. The other main thought on which I would like to conclude is that, al- though we have I believe this competitive advan- tage, it will only be maintained if all of us in the team, and I must include the Ministry in this, keep trying to improve our efficiency and com- petitive position in the specific areas in which we are involved, whether these be farm, dairy, factory, laboratory, computer room or any other part of our great dairy industry.

DISCUSSION Dr. G. Chsmh: Mr. Morton referred to the differ- ences in the levels of milk recording in the different parts of the United Kingdom and as between the UK and other European countnes. I should therefore like to raise the question of the advantages which he con- siders that those countries that are recording at a higher level enjoy. In Northern Ireland we have a very low level of recording, and find it dif€icult to convince our- selves that we ought to be doing more. Mr. Junes Morton: Dr. Chambers, there are two areas, I think, really. First of all, we need to be recording a sufacient number of stock in order to test a large number of animals, to make sure that our breeding programme i s such that we are making real genetic progress. And we can show this. In England and. Wales we are testing about 150 young bulls a year, which are then-laid off, and on the baeis Of whether th.ey are im- proving milk, weight of fat, weight of protein, confor-

22 Journal of the Society of Dairy Technology, Vol. 29, No. 1, January, I976

mation, about one in six comes back; so you need a scheme, you need a level of recording, which allows you to do that. After that it becomes an area where you really can debate.

If the farmer is recording simply for the sake of re- cording, as some do, then he probably had better not; but provided he is making real use of the records that he is getting (and I do not believe you can feed and manage a herd properly unless you have individual cow records) then he should be recording. You can counter that and say that he can record unofficially. He can, but he does not, in practice, and he has not got the vital information on that recording. So I think, George, you ought to be pushing pretty hard to step up the level of recording in Northern Ireland. Mr. J. Campbell: The speaker started off his address by saying that the most serious problem facing the UK dairy industry at the present time was lack of supplies, and he went on to give us some useful tables, showing, for example, that the self-sufficient ratio in the LJK has fallen from 59 per cent in 1972/73 to something like 54 per cent in 1974/75, and then raised the spectre of an additional 200 gal/cow in places like the Irish Republic and so on, suggesting, perhaps, that these were areas that might fill in this deficit. But that is not my question. He did mention, in fact, and perhaps tossed aside, the possibility of whether we were going in the right direc- tion by encouraging the development of the large herd size in the UK, and saying, possibly, that because of the cost of cattle and so on, we might very well have reached the optimum stage. Well now, we still have only an average herd size of something of the order of 38 cows, and we think that the optimum for a one-man sized unit is about 60 cows. I was wondering, therefore, if he could perhaps take that point just a little further, and suggest in which ways credit facilities might be made available to the UK dairy farmer that would enable him not only to stand still, but to go ahead, because I think there are still tremendous economies to be made in this particular field. Mr. James Morton: I did not really suggest which countries might fill in the deficit-I was just drawing attention gently to the areas where there could be sub- stantial increases in production. A lot of deficits have been filled in by the United Kingdom.

This question of herd size is a terribly interesting one. We were over in Brussels, recently - this was the whole Board, we took the Board over for a day - and we had a very interesting address by Dr. O’Dwyer, who painted very skilfully the world product situation. He then went on to the production end, and he was making the point that, no matter what happened, the Bavarian farmer with his 10 cows was still going to be in business. If there was real pressure he would tighten his belt better than anyone else. I think he was being the devil’s advo- cate, a little bit, but, at the same time, I think it is necessary not just to take for granted that a large herd size is as big an advantage as we previously thought it was, I still believe that it is a very considerable advantage, in that, at the end of the day, the chap who is we!’ organized, and making full use of labour, of facilities, IS the chap who is going to be in business and be competitive.

On the subject of credit, I don’t really feel qualified to comment on this. I did listen to a banker, the other day, debating the relative virtues, of subsidized credit as against capital grants, and he came out, in the end, with the view that the British Government had taken the right decision in opting for capital grants rather than for the alternative which was open to them, of subsidized credit. What I would, personally, like to see, I think, is some form of injection at the moment, at the production end. Whether it should be a headage payment, or what, I don’t know. What has happened is that on the current

milk price, the margin which the producer will get is quite a substantial improvement on what he got last year, but he has built up this deficiency in his cash resources over the last couple of years, because of the low margins which he had, and it is very difficult for the milk price alone to pull them out. That is the reason why some form of injection-it could be a headage payment- would help tremendously if it were made.

If you compare with the beef side, and all the various subsidies which are now available on beef, the calf sub- sidy, the headage payment, and there is another payment, it amounts to something between €40 and €50, and be- cause of this, one is seeing heifers being siphoned away from the dairy market into the beef market. So the precise means of doing it - I put forward one suggestion -but I think the need is very much there. Mr. R. H. Weeks: I did accept the speaker’s a&itude towards future standardization of milk for liquid con- sumption. We know that, especially during some winter months, milk of high fat is being delivered in the pint bottle. We know, at the same time, that the butter plants are idle. Would there be some advantage to the industry and the country, if some of that fat were trans- ferred from the bottle? Mr. James Morton: I didn’t deliberately dodge this one. You know, there are things that I did dodge, but there has been so much discussion, over the last couple of years, in this area, that I probably could leave out a little bit. Our attitude is quite clear. It is the same with the attitude of the DTF that we should continue in this country to sell milk as it comes from the cow. We have a big market, 1,500 million gallons of milk going into the liquid market, which is very important to us, and it is equally important to the Dutchman, the Dane and the others, because if that is eroded then they are going to find it more difficult to sell their butter over here. And therefore the question really is: Why put it at risk? The customer wants milk as it comes from the cow, as far as we know, and as an industry I believe we don’t want to get involved in the capltal investment which would be necessary, and certainly would introduce considerable complications in the handling of the milk from the Euro- pean point of view. We might help with making a little bit more butter, and easing the position on the plants and helping the balance of payments but I doubt if the Europeans want to see more butter produced here from that source. So on balance, all round, our view is very clear-that each country should be allowed to do its own thing; and in this area harmonization is not really necessary.

One of the things which I had in the paper, and skipped over, was a tribute to the work which has been done in Europe by DTF and Board people, in presenting our case, the UK case, for us to continue with milk as it comes from the cow. Whether we shall succeed or not, we don’t know. The debate is now well and truly on, and we should know before too long. The one thing we have got to know pretty soon is whether there is going to be an extension of the derogation. If there isn’t, I don’t know what happens. Mr. W. E. Buck: Mr. President, I have listened to Mr. Morton’s paper with great interest, and I was also very pleased to hear of the remarks about the people in the Ministry, although there was a slight qualification. We feel, some of us, that we are not entirely impartial, or entirely well-informed in some fields, and the field I am thinking of is related to milk quality. Therefore perhaps Mr. Morton will understand that I can do two things: one is to satisfy my curiosity, and also not letting him go by quoting a suggestion and not having someone to bite on it. Could he expand a little when he said perhaps we were being too much of perfectionists in some aspects of milk quality?

Journal of the Sociely of Dairy ’I’erhnology, Vol. 29, No. I , January, 1976 23

Mr. James Morton: I didn’mt think I wuuld get away with that one, Mr. President. I think I said there was a danger that we could be too much of perfectionists. What I was really saying was this: that all of us, in business, are under pressure. The farmer is no exception; he has been under pressure. He is having to handle more and more cows; he is having to milk more cows/man; and every additional job which you put on to him makes his whole task all the more difficult. If he handles more cows, then the risk of mastitis grows. Therefore the use of anti- biotics grows, and the danger of antibiotics going into the milk, and so on, grows. Now there are certain areas where one has got to take a very, very tough line, and I think this has been accepted by the Board and the DTF. But at the same time, if you keep puttink pressure on all areas it is extending the pressure, and it is putting up the cost of producing milk, handling milk, and so on. All I was saying, really, was that we should be standing back and taking a good, cool, hard look at all the different areas where we want to get to in the end, but where we should be establishing priorities at the present time. Be- cause it cannot, I believe, all be done at once, and we will move gradually towards our goal, but making sure that, in fixing that goal, it is not just a question of the various factors, but we also bring the economics of it into the whole thing as well. 1 know it is a difficult area, it is a rather emotional area. I think one can almost say the same thing about the country as a whole, over the last fifteen years or so. We have got ourselves involved in various schemes, and no-one has stopped and said, ‘Look,

OBITUARY M R . J . C. TAYLOR

The passing of J. C. Taylor is a reminder of the changing face of the dairy industry, for he was one of the rather larger than life-size figures which seemed to be a characteristic of dairying in the immediate post-war era. Although he was an engin- eer by training it was as a businessman in charge of a vigorous company that he would wish to be remembered and that is the picture those of us who knew him will remember best. His empire, United Dairies Engineering Company, was not large in numbers but he made it a force to be reckoned with by the strength of his personality - he was called ‘J.C.’ - and he radiated an aura of authority.

He loved to preside at those - now forgotten - select gatherings of senior dairymen which collected during Dairy Show time and at conferences, and he was proud to have been elected President of our Society in 1954, an office which he filled with distinction.

In his early days he specialized in refrigeration but by the time he became General Manager of UD Engineering in 1940 he had enlarged his

can we really afford them?’ And this is really the point I am making. I have stressed, all the way through, that I am not advocating slovenly methods of production on the farm. There is an economic factor to come into this consideration as well. I stress also that it is a personal view which I am expressing. The President: I think I must, with reluctance, bring this very stimulating paper and discussion to a close, and it is my pleasure to call upon Dr. Green to propose a vote of thanks. Dr. E. Green: Mr. President, Mr. Morton, ladies and gentlemen: On this occasion, as a member of the Milk Marketing Board staff, I find myself in a slightly in- vidious position, walking a tightrope, in doing justice to James Morton on the one hand, and possibly being accused of lack of sincerity on the other.

But on this occasion I am speaking as a Past President of the Society, and I can assure you that I am speaking with the greatest sincerity. I think James Morton’s per- formance this morning has been masterly. I am aware that yesterday he was still preparing his paper; also, as you probably heard, he went to York and spoke at a meeting there, and came back on an overnight sleeper. I think his display this morning has demonstrated a familiarity, a mastery of his subject, which is an example to all of us, but as a member of his team it is no more than I expected. Ladies and gentlemen, I would ask you to join me in conveying our thanks to him for his paper this morning.

aspects of dairy the Drocessing and

experience to cover most engineering, particularly on bottling side. In 1946 he became Maiaging Dkector of that Company, a position he occupied until his retirement in 1966. By that time the Company was undertaking complete dairy design projects in many parts of the world.

He was prominent in the British Institute of Refrigeration and served on a number of British Standards Institution Committees. He was for several years a pillar of the Dairy Engineers’ Association.

Those who knew him will remember J. C. Taylor with much affection as a man, and one who did a great deal to advance dairy machinery design especially in the field of milk refrigeration, bottling and utensil washing. He saw what was needed, got it done and then persuaded dairymen to install it. No mean achievement.

Above all we will remember him as a man who radiated and revelled in good fellowshiD. whose like can ill be spared in thesgtroubled time’s:

R.J.MacW.

24 Journal of the Society of Dairy Technology, Vol. 29, No. I , January. 1976