The Colder War Chapter 9

of 12

-

Upload

caseyresearch -

Category

Documents

-

view

215 -

download

0

Transcript of The Colder War Chapter 9

-

7/21/2019 The Colder War Chapter 9

1/12

Chapter 9

The Putinization

of Uranium

On Friday, March 11, 2011, nature struck.

A monster, magnitude 9.0 earthquake grabbed the seabed 40

miles northeast of Honshu, in Japan. It tossed the entire island eight

feet eastward and shifted the earths axis by more than four inches. The

shock generated tsunami waves that reached elevations of 130 feet andinundated areas six miles inland. Hundreds of thousands of people ed.

Nearly 16,000 bodies were recovered and another 2,500 still are missing.

Lying in the tsunamis path were generators that fed the Fukushima

Daiichi nuclear power plants cooling system. They were disabled, and

the cooling system stopped. Reactor core meltdowns followed. On the

International Nuclear and Radiological Event Scale, it was a Level 7

disaster, matched only by Chernobyl.

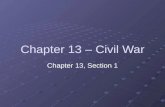

In the aftermath of Fukushimawhose cleanup will take decadesthe spot price of uranium yellowcake has dropped more than 60 percent,

to $28 per pound (see Figure 9.1), and the stock prices of uranium miners

123

-

7/21/2019 The Colder War Chapter 9

2/12

124 T H E C O L D E R WA R

$20

$30

$40

$50

$60

$70

$80

8-12-2009

2-12-2010

8-12-2010

2-12-2011

8-12-2011

2-12-2012

8-12-2012

2-12-2013

8-12-2013

2-12-2014

Uranium,US$perPound

Fukushima Disaster

Figure 9.1 Spot Uranium PriceSOURCE: S&P Capital IQ. Casey Research 2014.

have plunged between 60 and 85 percent. Japan shut down all 52 of its

other reactors for safety evaluations. South Korea followed suit for its 23

reactorsalthough most have now been returned to service.

Fukushima rousted antinuclear protestors out of bed around the

world. For them, the earthquake revealed nuclear power to the world for

the terrible idea it had been all along. Germany announced it would shut

down all 17 of its reactors, permanently, by 2022. It seemed that many

other countriesperhaps all of themwould be closing their nuclearpower plants as well.

Well, not so fast.

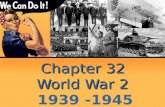

No one followed Germanys lead. Today, no fewer than 71 new

plants are under construction, in more than a dozen countries, with

another 163 planned and 329 proposed. (See Figure 9.2.) Many coun-

tries without nuclear power soon will build their rst reactor, including

Turkey, Kazakhstan, Indonesia, Vietnam, Egypt, Saudi Arabia, and sev-

eral of the Gulf emirates.While many countries with nuclear power plants declared a time-

out to reassess safety practices, almost all are staying with what they

have. Uranium is still the only fuel that can produce base-load electricity

-

7/21/2019 The Colder War Chapter 9

3/12

Figure

9.

2

NuclearReactorsWorldwide

125

-

7/21/2019 The Colder War Chapter 9

4/12

126 T H E C O L D E R W A R

economically and without exhaling greenhouse gases and other unwel-

come hydrocarbons.

In the United States, which hasnt opened a nuclear power plant

since 1977, six new units are scheduled to come online by 2020, fourfrom license applications made since mid-2007. The country is the

worlds biggest producer of nuclear energy, accounting for more than

30 percent of the worldwide total. Its 65 nuclear plants (housing just

over 100 reactors) generate 20 percent of U.S. electricity.

France is the country most dependent on uranium; 75 percent of

its electricity comes from nuclear power. China, whose urban residents

are choking on pollution from coal-red plants, is now on a nuclear-

construction fast track. It already has 17 reactors in operation, and 29

more are being built. The country wants a fourfold capacity increase by

2020. India has 20 plants and is adding seven more. Several countries

in Africa, where more than 90 percent of the population goes without

electricity, have begun to explore the possibility.

New facilities are going to be safer, too, especially after Fukushima

exposed the vulnerabilities of older designs. Though the containment

systems at Fukushima were far more robust than the buckets that held theChernobyl reactors, they were 40 years old, several generations behind

todays containment engineering and materials. Fukushima would soon

have been a candidate for decommissioning.

Long-Term Shortage

While Germany may be able to get by without nuclear power plants(although its carbon footprint is spreading, and its already fudging by

importing nuclear-generated electricity from France), none of the other

countries using or readying for nuclear power can. Theres just no alter-

native. That means the demand for uranium will rise as both the worlds

economy and its discomfort over fossil fuels grow. And that means prots

and political leverage for any country that might dominate the uranium

industry.

The World Nuclear Association predicts demand growth of 33 per-cent from 2010 to 2020 and similar growth in the 10 years that follow. In

2011, the world consumed 160 million pounds of yellowcake uranium.

-

7/21/2019 The Colder War Chapter 9

5/12

The Putinization of Uranium 127

32%

19%12%

12%

11%

7%

3% 2% 2%

Russia

Kazakhstan/UzbekistanNiger/Gabon

Australia

Canada

South Africa/Namibia

European Union

Other

United States

Figure 9.3 EU-27 Sources of Uranium, 2010SOURCE: Energy Information Administration. Casey Research 2012.

By 2024, just 10 years from now, it will be chewing through 200 million

pounds annuallyif its available.

At the same time, a supply crunch is building. In 2012, the world

consumed 25 percent more uranium than came out of its mines, a short-

fall of 40 million pounds (at current long-term prices, about $1.8 billionworth). The decit is likely to rise to 55 million pounds by 2020. Ura-

nium mines are few and far between. Only 20 countries have even one,

and half of global production comes from just 10 mines in six countries.

(Sources for the European Union are shown in Figure 9.3.)

In the United States, 100 reactors are burning fuel from 43 million

pounds of uranium per year to produce electricity. Supply from U.S.

mines is about 4 million pounds, or only 9 percent of whats needed to

keep those plants running.Heres another way of looking at it: The estimated needs of U.S.

nuclear power plants between now and 2021 come in at around 275 mil-

lion pounds of yellowcake.The countrys entire inventoryamounts to only

120 million pounds.

In the long run, more mining is the only answer. But a new uranium

mine is more difficult to bring into production than any other kind of

resource. Given the engineering challenges, environmental and safety

requirements, and strict permitting, it takes 10 years, minimum, to getfrom decision to production. New mines are not coming online quickly

enough to meet expected growth in consumption. And the worldalready

-

7/21/2019 The Colder War Chapter 9

6/12

128 T H E C O L D E R W A R

is using more than it digs out of the ground. In fact, it has been doing

so for the past 20 years.

If every uranium mine proposed in the past decade were approved,

built, and commissioned on schedule, suppliesmightbe able to keep up.But current uranium prices are too low to entice any company to build

those potential mines, and any risk taker that might decide to gamble on

rising prices would face the separate risk of regulatory delay. Getting the

permits to build a uranium mine is not like standing in line for an hour

at the Department of Motor Vehicles. You have to stand in many lines

for many years while you wait for decision makers to nd the courage

to confront the radiation bogeyman.

A shortage is coming, and Putin is preparing to turn it into a cash

register and also into a tool of geopolitics. Controlling in-the-ground

resources is just part of Putins plan. Understanding the whole plan

requires a brief detour.

Science Lesson

The uranium fuel cycle starts with digging uranium-bearing ore out ofthe ground and then subjecting it to a chemical process that extracts the

uranium oxides (chiey U3O8). The dried product is a powder called

yellowcake. You can guess the color.

Of the uranium atoms in a pile of yellowcake, more than 99 per-

cent are U-238, a barely radioactive isotope that cannot sustain a chain

reaction for a power plant, bomb, or any other purpose. Virtually all the

rest of the uranium atoms, about 0.7 percent, are U-235 (the number

difference indicating three fewer neutrons), which is a somewhat more

radioactive isotope that in quantities of just a few pounds can sustain a

chain reaction. U-235 has that capability because when an atom of the

stuff splits, it ings out neutrons with just the right velocity for splitting

any other U-235 atoms they encounter. Its like one drunk starting a

ght that spreads through an entire barroom.

To turn the yellowcake into something useful, enough of the U-

238 must be separated out so that the concentration of U-235 in theremaining material is:

3 to 10 percent for use in a commercial nuclear power plant 20 percent for use in certain types of research and medical reactors

-

7/21/2019 The Colder War Chapter 9

7/12

The Putinization of Uranium 129

20 to 90 percent for use in the compact power plants of submarines 90 percent for use in weapons

Moving from the 0.7 percent U-235 concentration provided by

nature to something higher begins with introducing uorine to the ura-

nium oxides. That produces uranium hexauoride (UF6), which at room

temperature is a gas.

Next, the uranium hexauoride gas is pumped through a system that

exploits the slight weight difference between an atom of U-235 and an

atom of U-238 (whose greater weight comes from its three additional

neutrons). There are half a dozen clever techniques for doing this, butonly two are in commercial use. One is to spin the gas through a series

of ultra-high-speed centrifuges. The other is to pump the gas through a

series of ultrane lters.

With either technique, each step in the series yields two streams of

gas, one slightly higher in U-235 and one slightly lower in U-235 than

the gas that went into the step. After the gas has passed through many

centrifuges or through many lters, the process ends with two tanks

of uranium hexauoride. One contains the desired concentration ofU-235, and one contains U-238 with traces of U-235 well below

natures 0.7 percent. The contents of that second tank are referred to

as tails. For easier long-term storage, the tail gas may be reconverted to

a uranium oxide.

For fuel, the nal step is fabrication. The enriched gas (with the

desired concentration of U-235) is chemically processed into uranium

dioxide powder. The powder is compressed into pellets, heated until it

coalesces into a ceramic, and then bundled into rod-shaped fuel assem-

blies tailored for a particular kind of reactor.

The current uranium enrichment capacities of several nations is

shown in Figure 9.4.

Short-Term Fixes

An adequate supply of uranium is available today to fuel the worldsreactors only because a secondary supply is lling the gap between usage

and primary supply from mines. Most of that secondary supply involves

Russia.

-

7/21/2019 The Colder War Chapter 9

8/12

130 T H E C O L D E R WA R

40%

23%

20%

15%

2%

Russia

Germany/Netherlands/UK

France

China

United States

Figure 9.4 Current Uranium Enrichment Capacity Casey Research 2014.

When the USSR collapsed, Russia inherited over 2 million pounds

of weapons-grade uranium and vast, underused facilities for han-

dling and fabricating the material. Starting in 1993, the two were

brought together under the Megatons to Megawatts agreement between

Russia and the United States. Over the 20 years that followed, 1.1 mil-lion pounds of Russian warhead-grade uranium (90 percent U-235),

equivalent to 20,000 nuclear warheads, was blended down to 33 mil-

lion pounds of reactor-grade uranium (3 percent U-235) by diluting it

with tailsenrichment in reverse. The resulting product was sold to the

United States.

Megatons to Megawatts helped to ll the supply gap for two decades

but now is history. Its expiration in November 2013 marked the end to

24 million pounds of annual uranium supply, 55 percent of what theUnited States had been using.

During the Megatons to Megawatts period, Russia operated a sepa-

rate stream of secondary production. It put its excess enrichment capacity

to work on other peoples tails. In the 1990s and early 2000s, Russia

accepted boatloads of ready-to-process tails from major players like

Areva (Canadian) and Urenco (a European consortium). Today that

sideline also is history.

The United States now contributes to secondary supply in a modestway. During the Megatons era, the United States also was converting

unwanted warhead material to fuel. But only one American company,

-

7/21/2019 The Colder War Chapter 9

9/12

The Putinization of Uranium 131

7% 4%

42%11%

Russia

United States

18%

France

Canada

18%

United Kingdom

China

Figure 9.5 Uranium Conversion Capacity Casey Research 2014.

WesDyne International, has facilities for downblending weapons-grade

uranium to fuel grade, and its capacity is less than 18,000 pounds per

year. (Russias capacity is more than ve times that.) (See Figure 9.5.)

So while the United States has plenty of warhead uranium to feed

downblending plants, it doesnt have much plant capacity to feed it into.

To speed things up, it would have to send the material to Russia for

conversion to fuel. Imagine the screaming if any U.S. politician proposed

handing nuclear warhead material to Mr. Putin.

Today Russia is producing enriched uranium from its own stockpile

of tails, in addition to enriching the output from Russian mines. As a

producer of uranium ore, Russia is in sixth place; however, when the

former Soviet states combine their production, Kazakhstan, Uzbekistan,

and Russia make up almost half the global uranium production. As aproducer of enriched uranium, Russia is number one. It supplies over

40 percent of the worlds enriched uranium, mostly to power plants.

Putins Uranium Superstore

Russia now ranks sixth in the world for mine production of uranium.

On top of that, Putin carries a lot of clout in neighboring Kazakhstan,a member of the Common Economic Space (CES) customs union and

the worlds top primary uranium producer, with 38 percent of the total.

-

7/21/2019 The Colder War Chapter 9

10/12

132 T H E C O L D E R W A R

So Russia already has its hands on 47 percent of the worlds primary

production.

Control over so much capacity for mining and enrichment makes

Putin the go-to source for countries desperate to secure long-term sup-plies of reactor fuel. In 2012, for example, Russia signed an agree-

ment with Japanwhich, despite Fukushima, cant afford to give up on

nuclear powerthat guarantees the availability of uranium enrichment

services for Japanese utilities.

Russia will continue supplying the United States as well, but this

time on Russian terms. The Megatons agreement didnt let Russia sell

directly to American utilitiesonly to the U.S. Enrichment Corpora-

tion (USEC), at a set, below-market price. And the only product eligible

was downblended warhead uraniumnothing from new mine produc-

tion. It was because of those and other restrictions that Russia made no

effort to extend Megatons past 2013.

In 2012, Tenex, Russias nuclear fuel exporter, reached six-year

deals to supply more than $1 billion worth of reactor fuel to four

American utilities. It has also contracted to provide enrichment services

to USEC for nine years. Annual deliveries under the USEC contractshould be about half of those under Megatons. There is no price ceiling,

and there are no conditions on where the uranium comes from.

Putin has also captured long-term customers for Russian uranium

in countries where Rosatom, Russias state nuclear utility, is building

reactors.

Rosatom is a giant in the global nuclear sector. The company builds

more nuclear power plants worldwide than anyone else, with construc-

tion currently under way in China, Vietnam, India, and Turkey. The21 projects now on Rosatoms order book are worth $50 billion. Iran

plans to buy at least eight new nuclear reactors, and the Russians are

ready to build and operate the projects and supply the fuel. While the

United States dithers over Ukraine, Putin is cementing more long-term

contracts into place.

Moreover, many of those new facilities come with a life-of-plant

fuel supply contract, such as the one Rosatom recently signed with

Bangladesh for its rst nuclear power plant. Putin understands the mean-ing of full-service provider.

-

7/21/2019 The Colder War Chapter 9

11/12

The Putinization of Uranium 133

Rosatom also handles $3 billion per year of Russian uranium exports

to other customers. One-fth of the material goes to the Asia-Pacic

region, a market growing so quickly that Rosatom is building a new

uranium products transportation hub at Vladivostok, Russias largestPacic port.

The Ultimate Source

Putin has been locking up mine production outside of Russia. In mid-

2010, AtomRedMetZoloto (ARMZ, an arm of state-owned Rosatom)

boosted its stake in Uranium One, one of the largest publicly traded

uranium producers in the world, from 17 percent to 51 percent. At the

time, ARMZ wanted to use Uranium One as a public vehicle to attract

investors for its expansion plans.

That notion evaporated when Fukushima killed investor interest

in uranium. Thus, in 2013, it acquired all of the remaining shares in

Uranium One for $1.3 billion and took the company private at over

100 percent premium to the market price of the shares at the time. Thetiming was right.

Uranium One is a major producer, with 16 million pounds per

year. Through the acquisition, Russia picked up mining operations in

Australia, Canada, Kazakhstan, South Africa, Tanzania, and even the

United States, where it will now produce more uranium each year than

all American mining companies combined.

Russia has signed uranium exploration and development agreements

with Japan, France, India, South Korea, and Canada. ARMZ is alreadyinvolved in joint production projects with Kazakhstans state-owned

Kazatomprom, the worlds largest producer of uranium.

Russia has also been courting Namibia, which possesses 5 percent

of the worlds known uranium reserves. It is already a big producer and

is expected to become the number two yellowcake exporter by 2018,

after Kazakhstan.

Egypt has a place in Putins plan as well. After a 2013 meeting

with then-President Mohamed Morsi, it was announced that the twocountries would resume cooperation in peaceful nuclear projects,

-

7/21/2019 The Colder War Chapter 9

12/12

134 T H E C O L D E R W A R

including construction of nuclear power plants. Cairo wants 4 gigawatts

of nuclear generating capacity by 2025, enough to power about 3 million

homes. Egypt also invited Moscow to cooperate in the joint develop-

ment of uranium mines. Given the benets to Egypt, the agreements arelikely to survive Morsis overthrow.

Going to School in Mongolia

Russia is willing to go pretty far to get what it wants. Though Putin shies

away from waging war over resourcespreferring to let other countries

do the dirty work, then step in for a share of the spoils, as in Iraqhes

not shy about economic warfare. Consider events in Mongolia, one of

those bordering nations, like Ukraine, that Russia proprietarily considers

part of its near-beyond.

Russia was the rst developer of Mongolias 7,500-acre Dornod

deposit. The Soviets and then the Russians mined it from 1988 to 1995,

with a workforce that peaked near 10,000. Russia spent $150 million on

developing the site but then abandoned it in 1995, during the turbulenttime when the money supply from Moscow had all but dried up.

Despite leaving, Russia never lost its sense of entitlement for

Dornod.

The project sat idle until 2003. Then the Mongolian government

opened it to Western mining interests. It was snapped up by a small

Canadian company, Khan Resources, which took a majority stake and

also took on the Mongolian government as a partner.

Then Khan got clipped by Putin.In January 2009, Russia and Mongolia announced a joint venture for

uranium extraction. Next, in January 2010, the Mongolian parliament

bestowed upon the Mongolian government a 51 percent share in every

project in which the Mongolian government had an investment. That

included Dornod. Thus Khan lost control of the project through a no-

compensation expropriation; that is, they were robbed.

The matter is now entombed in international litigation. Whatever

Khan recovers in the legal ght, if anything, will go to the lawyersanother dead client for dinner.