The CIS area corporate credit universe in early 2016 ... · The CIS area corporate credit universe...

34

1 The CIS area corporate credit universe in early 2016: priced to perfection? 12 May 2016 When we took a close look at the CIS area corporate credit space six months ago, our conclusion was that the harsh business environment was forcing many borrowers (particularly, in Russia’s mining sector) to deleverage and strengthen free cash flow generation, paving way to spread compression in future. However, the swift turnaround in sentiment on the back of a recovery in commodity prices and a distinctly more dovish outlook for monetary policy globally have resulted in a euphoria that took spreads back to levels last seen at much higher levels of economic growth, commodity prices and profits. While many companies have used the abundant local market liquidity for further deleveraging, there were notable exceptions. The hunt for yield has driven corporate spreads in the CIS to 12-month lows, often ignoring fundamentals and benefiting the weakest credits disproportionately. We doubt the sustainability of the recent increases in commodity prices and struggle to find value in this environment. Our top picks at present are the strongest credits in this pool that should suffer least once market views on either China’s recovery or US interest rates shift again, in particular Alrosa and Phosagro. In this report we present an overview of the non-financial credit space in the CIS, with a particular focus on Russia’s metals and mining sector, alongside two non-Russian issuers (from Georgia and Ukraine). See inside cover for analyst contacts and disclosures

Transcript of The CIS area corporate credit universe in early 2016 ... · The CIS area corporate credit universe...

1

The CIS area corporate credit universe in early 2016: priced to perfection?

12 May 2016

When we took a close look at the CIS area corporate credit space six months ago, our conclusion was that

the harsh business environment was forcing many borrowers (particularly, in Russia’s mining sector) to

deleverage and strengthen free cash flow generation, paving way to spread compression in future.

However, the swift turnaround in sentiment on the back of a recovery in commodity prices and a

distinctly more dovish outlook for monetary policy globally have resulted in a euphoria that took

spreads back to levels last seen at much higher levels of economic growth, commodity prices and

profits.

While many companies have used the abundant local market liquidity for further deleveraging, there

were notable exceptions. The hunt for yield has driven corporate spreads in the CIS to 12-month lows,

often ignoring fundamentals and benefiting the weakest credits disproportionately. We doubt the

sustainability of the recent increases in commodity prices and struggle to find value in this

environment. Our top picks at present are the strongest credits in this pool that should suffer least once

market views on either China’s recovery or US interest rates shift again, in particular Alrosa and

Phosagro.

In this report we present an overview of the non-financial credit space in the CIS, with a particular focus

on Russia’s metals and mining sector, alongside two non-Russian issuers (from Georgia and Ukraine).

See inside cover for analyst contacts and disclosures

2

TABLE OF CONTENTS

Overview of the CIS area non-financial corporate credits 3

Recent performance of select CIS corporate credits in 2015 4

Severstal 6

NLMK 8

EVRAZ 10

Metalloinvest 12

Norilsk Nickel 14

TMK 16

Polyus Gold 18

Nordgold 20

Alrosa 22

Uralkali 24

Phosagro 26

Eurochem 28

MHP 30

Georgian Oil and Gas Corporation 32

Disclosures 34

All charts data are as of 12 May 2016. Sources for all market charts are Bloomberg and for all company-specific

graphs are corresponding company data.

Norvik Banka Research Sergei Voloboev, Head of Research (London) +44 20 7259 8854

Research contacts: Pavel Specivtsev, Economist (Moscow) [email protected]

We would like to acknowledge the substantial input of Maxim Serous CFA, a consultant for Norvik Banka UK, into

the preparation of this report

Norvik Banka Research is a Trading Name of Norvik Banka UK Ltd, which is Authorised and Regulated by the Financial Conduct

Authority, FRN: 681329. Registered in England and Wales with number 08940522. Registered Office: 46/48 Grosvenor Gardens 1st

Floor, London, SW1W 0EB.

3

Overview of the CIS area non-financial corporate credits in late 2015 and early 2016

We highlight below the key factors influencing non-financial sector credits in Russia and the CIS in 2015-2016.

Abundant liquidity in the local market. The turnaround in commodities in Q1, most notably oil, has led to

sustained currency appreciation in Russia and, to a lesser extent, other CIS states. The ensuing strong rally in

local fixed income markets has helped drive sovereign yields lower, thus boosting demand for corporate debt.

Excess liquidity spilled over to Russia’s local money market, with Sberbank slashing short-term USD deposit

rates to near-zero amid lack of reinvestment opportunities and high quality borrowers. We think this trend

also reflects general lack of demand for foreign currency funding, especially among companies without FX

revenues. A number of companies with large FX mismatch between revenues and liabilities (Evraz, TMK) have

been working to reduce this gap by raising funds in the local bond market and using proceeds to repay FX

debt. Another trend, driven by improved access to liquidity, was to push out debt maturities though Eurobond

buybacks. Both Evraz and TMK have pursued this strategy helping to lift short-term liquidity pressures and

gaining time for dealing with the challenges of high leverage.

Primary Eurobond market has reopend for corporate issuers. This window closed over the winter months

during the period of acute risk off mode triggered by falling commodity prices and uncertainty over FOMC

intentions. However, a rebound in oil and improved investor sentiment have helped to reopen market access

leading to placement of several new issues by Russian borrowers, including Global Ports ($350 mn), Gazprom

(CHF 500 mn), Vimpelcom ($1.2 bn) and B&N Bank ($150 mn). Western sanctions against Russia have

prevented a return to the market by the Russian sovereign and continue to restrict issuance by Russia’s quasi-

sovereign entities. While an early return to the market by the entities affected by the sanctions is unlikely, we

expect to see more Eurobond placements by private sector borrowers provided the current favourable

condiditons persist.

Rapid compression of credit spreads. The abundant liquidity and aggressive hunt for yields have resulted in a

rapid compression of credit spread in the Russian corporate Eurobond space, especially in the riskier segment.

Notably, the spread of Evraz-2020 to Russia-2020 reached a historic minimum in May despite further

increases in the company’s leverage. The spread of Polyus Gold to Russia-2020 was close to a historic average

despite accumulation of significant debt at the parent company’s level following completion of the share

buyback. Given the current tight corporate spreads by historic standards, we see little upside for bond prices

from current levels. Any further spread tightening would require additional increases in oil prices, or lifting of

Western sanctions, in our view.

Divergence in deleveraging trends. Although many companies in our sample continued to pay down debt in

H2 2015, others chose to halt this process (Metalloinvest). Furthemore, Norilsk Nickel announced changes to

its dividend policy which imply an increase in leverage. We also note that during 2015 companies were been

increasingly turning to dividend payments as a key use of their cash flows. This was primarily the result of

scarcity of reinvestment opportunities against the backdrop of weak commodity prices and completion of

modernization programs. We see such a trend in the Metal and Mining sector (NLMK, Severstal) and among

fertilizer producers (Phosagro, Eurochem). At the same time, some companies targeting lower leverage ratios

continued to implement their deleveraging strategy (Evraz, TMK, Alrosa), with varying degrees of success. We

expect deleveraging among the non-financial sector borrowers to continue in 2016 (with certain exceptions),

albeit at a significantly slower pace compared to 2014 and 2015. This should provide support to bond prices in

the current volatile environment (including for commodity prices), in our view.

4

The charts below illustrate spread performance of these issuers over the past 12 months, against UST and CIS sovereigns.

5

RUB flexibility cushioned commodity price declines

The second half of 2015 was marked by significant

declines in commodity prices and an increase in risk

aversion among investors. To make things worse for

many export-oriented companies in the CIS, the pace

of exchange rate adjustment typically lagged those

of commodity price declines. This was particularly

relevant for companies in Kazahstan and Azerbaijan

where the central bank decisions to delay exchange

rate liberalization in the face of falling oil prices have

led to significant deterioration in external accounts

and corporate profitability.

Conversely, for Russia-based exporters, the rapid

pace of RUB depreciation has cushioned the impact

on profits, by supporting the commodity prices in

rouble terms (iron ore prices in RUB are currently in

line with their levels in early 2014, while gold prices

in RUB have effecively doubled).

Despite the strong rebound in commodity prices

since the beginning of the year we see some of the

credits as increasingly vulnerable to further

deterioration in credit quality. We question the

sustainability of the recent recovery in commodity

prices, especially in iron ore and steel segments.

The hunt for yield has driven corporate spreads in

Russian space to 12-month lows, sometimes

ignoring deteriorating fundamentals. Key

beneficiaries of this improved market sentiment

have been the weakest corporate credits. We find it

hard to locate value in this environment and prefer

to focus on the strongest credits (from the BBB-/BB+

category), in particular Alrosa and Phosagro.

Further corporate yield compression in Russia

would require a material repricing of Russia’s

sovereign risk, which we find unlikely without either

lifting of the sanctions, a much higher level of oil

prices, or a proactive structural reform effort (hardly

a realistic possibility before the end of the current

polical cycle in 2018).

6

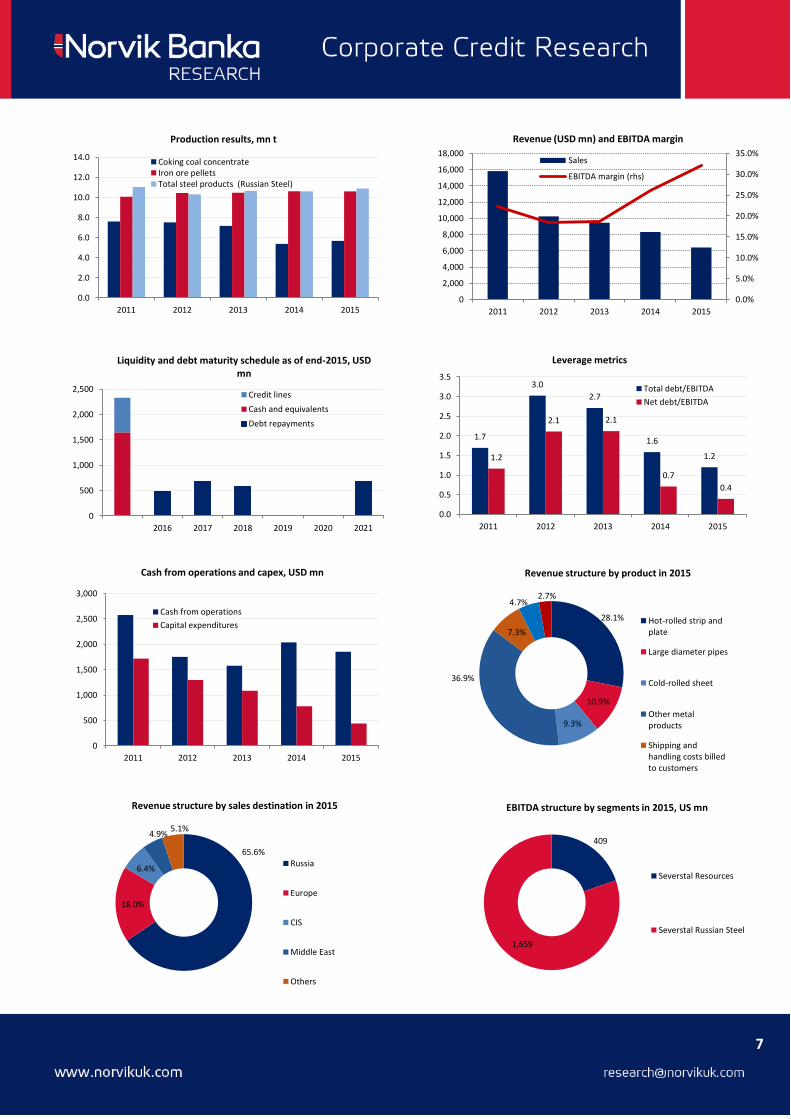

SEVERSTAL

Credit ratings (S&P/Moody’s/Fitch): BB+/Ba1/BB+

Industry: Metals and Mining

Summary

The company remained one of the strongest credits in

Russia’s Metals and Mining space in 2015. Severstal’s credit

profile is supported by low debt, positive free cash flow

generation in the challenging environment, flexible dividend

policy and a comfortable liquidity position. The risks come

mainly from overproduction in global steel markets. Due to

its low cost asset base, we find Severstal to be well

positioned to overcome the industry’s current headwinds.

Company profile

Severstal is a vertically integrated steel producer with assets

based primarily in Russia. The company is 110% self-

sufficient in iron ore and 96% in coking coal (based on 2015

data). With steel production at 11.5 mn t in 2015, the

company is among Russia’s top three steel producers after

NLMK and Evraz. Severstal is controlled by Alexey

Mordashov (79.2%); the remaining shares are in free float.

Debt/financial/liquidity profile

Revenue followed steel prices in H2, declining to $3,059 mn

(H1 2015: $3,337 mn) while sales volumes of steel products

increased by 4.5% YoY. In Q1 2016 sales of steel products

declined by 4% (production was down 2% YoY) as a result of

subdued domestic demand.

EBITDA declined by 21% in H2 2015 to $925 mn from $1,166

mn in H1 2015 as the positive effect of rouble depreciation

was outweighed by a slump in steel prices and inflation

pressures on the cost position. The Q1 2016 financial results

were even weaker, with revenue and EBITDA down 28% YoY

and 55% YoY respectively, due to a decline in sales volumes,

a lower share of high value-added products and weakness in

steel prices. At the same time, Q2 2016 is likely to show and

improvement in QoQ terms thanks to a rebound in steel

prices from multi-year lows in March.

A strong cash flow from operations at $1,093 mn (H1 2015:

$760 mn) was mainly the result of a working capital release

in Q3 2015. Capex remained low at $225 mn, which

supported free cash flow. Apart from debt reduction, the

key use of cash flow remained payment of dividends ($313

mn in H2 2015). The company maintained its dividend policy

which assumes paying 50% of net income as long as net

debt/EBITDA remains below 1.0x and 25% of net income if

net debt/EBITDA exceeds 1.0x.

The company continued to decrease leverage in 2015 as net

debt/EBITDA improved to 0.4x from 0.6x at end-H1 2015 and

0.7x at end-2014. Net debt repayment in H2 was $421 mn

(H1 2015: $558 mn), EBITDA/net interest expense improved

to an impressive 17.2x from 8.6x at end-2014. We expect the

company to maintain a strong credit profile in the next 12

months despite continuing headwinds in the industry.

Severstal’s available liquidity at the end of 2015 amounted

to $2,330 mn, including $1,647 mn of cash and $683 mn in

credit lines, versus short-term debt of $508 mn. 90.1% of

total debt is public and USD-denominated.

On 25 February 2016, 31 miners and 5 rescuers died as a

result of several gas explosions at the Severnaya coal mine in

the town of Vorkuta, in Russia’s Komi Republic. Following

the accident, Severstal paid RUB 163mn ($2.2 mn) to the

affected families and committed to spend another RUB 2 bn

in 2016 to increase safety at Vorkutaugol coal mines. On 6

March 2016, the company decided to flood the mine to stop

the underground fire. Severnaya mine accounted for 27% of

total coal concentrate production of Severstal in 2015.

RISKS

Prolonged weakness in steel prices and demand

Increased protectionism in external markets

Rouble appreciation

Production incidents

IFRS, USD mn 2013 2014 2015 Sales 9,434 8,296 6,396 Sales YoY -8% -12% -23% EBITDA 1,753 2,162 2,048 EBITDA YoY -8% 23% -5% Net income 89 -1,603 603 Net income YoY -89% NA NA Cash from operations 1,578 2,038 1,853 Capital expenditures 1,084 779 439 Free cash flow 494 1,259 1,414 Current ratio 1.9 2.1 2.3 Cash/Short term debt 1.7 2.4 3.2 Short term debt/Total debt 0.13 0.23 0.21 Total debt 4,754 3,429 2,452 Cash 1,036 1,897 1,647 Net debt 3,718 1,532 805 Capex/Depreciation 1.8 1.4 1.2 EBITDA margin 18.4% 24.9% 31.6% Total debt/EBITDA 2.7 1.7 1.2 Net debt/EBITDA 2.1 0.7 0.4 Net interest expense 300 239 117 EBITDA/Net int. expense 5.8 8.6 17.2

7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2011 2012 2013 2014 2015

Production results, mn t

Coking coal concentrateIron ore pelletsTotal steel products (Russian Steel)

0

500

1,000

1,500

2,000

2,500

2016 2017 2018 2019 2020 2021

Liquidity and debt maturity schedule as of end-2015, USD mn

Credit lines

Cash and equivalents

Debt repayments

0

500

1,000

1,500

2,000

2,500

3,000

2011 2012 2013 2014 2015

Cash from operations and capex, USD mn

Cash from operations

Capital expenditures

65.6%

18.0%

6.4%

4.9% 5.1%

Revenue structure by sales destination in 2015

Russia

Europe

CIS

Middle East

Others

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2011 2012 2013 2014 2015

Revenue (USD mn) and EBITDA margin

Sales

EBITDA margin (rhs)

1.7

3.0

2.7

1.6

1.2 1.2

2.1 2.1

0.7

0.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

28.1%

10.9%

9.3%

36.9%

7.3%

4.7% 2.7%

Revenue structure by product in 2015

Hot-rolled strip andplate

Large diameter pipes

Cold-rolled sheet

Other metalproducts

Shipping andhandling costs billedto customers

409

1,659

EBITDA structure by segments in 2015, US mn

Severstal Resources

Severstal Russian Steel

8

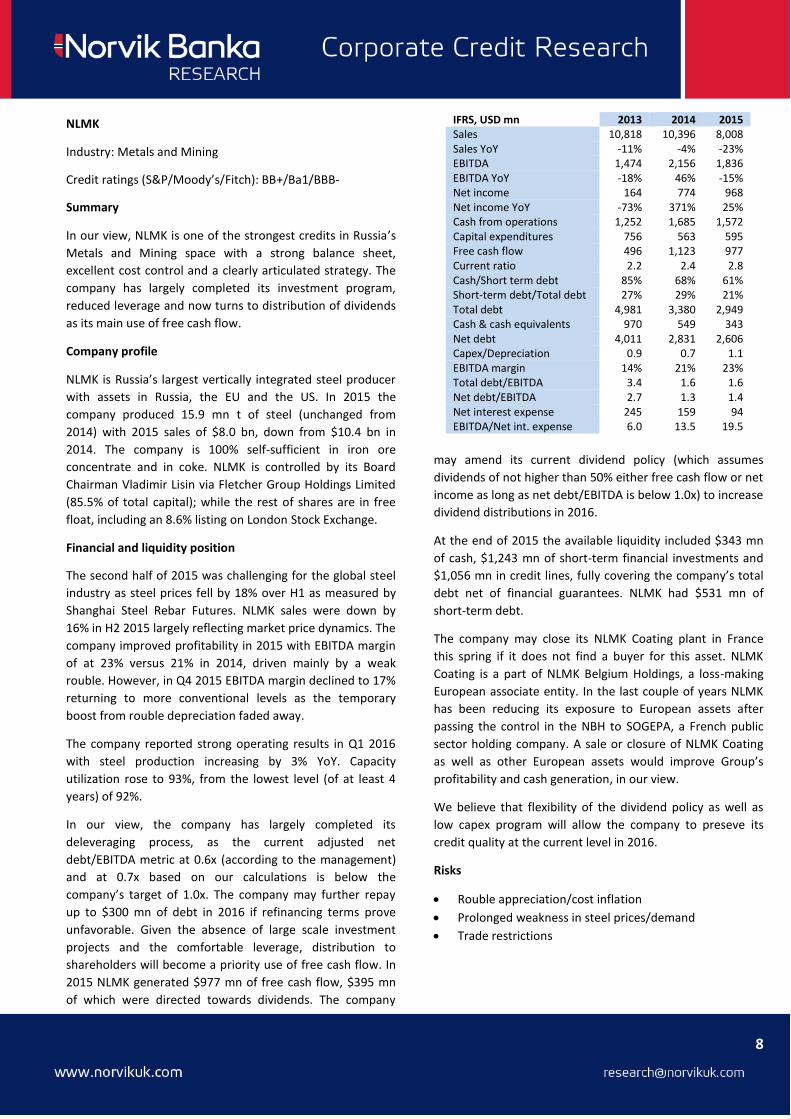

IFRS, USD mn 2013 2014 2015 Sales 10,818 10,396 8,008 Sales YoY -11% -4% -23% EBITDA 1,474 2,156 1,836 EBITDA YoY -18% 46% -15% Net income 164 774 968 Net income YoY -73% 371% 25% Cash from operations 1,252 1,685 1,572 Capital expenditures 756 563 595 Free cash flow 496 1,123 977 Current ratio 2.2 2.4 2.8 Cash/Short term debt 85% 68% 61% Short-term debt/Total debt 27% 29% 21% Total debt 4,981 3,380 2,949 Cash & cash equivalents 970 549 343 Net debt 4,011 2,831 2,606 Capex/Depreciation 0.9 0.7 1.1 EBITDA margin 14% 21% 23% Total debt/EBITDA 3.4 1.6 1.6 Net debt/EBITDA 2.7 1.3 1.4 Net interest expense 245 159 94 EBITDA/Net int. expense 6.0 13.5 19.5

NLMK

Industry: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): BB+/Ba1/BBB-

Summary

In our view, NLMK is one of the strongest credits in Russia’s

Metals and Mining space with a strong balance sheet,

excellent cost control and a clearly articulated strategy. The

company has largely completed its investment program,

reduced leverage and now turns to distribution of dividends

as its main use of free cash flow.

Company profile

NLMK is Russia’s largest vertically integrated steel producer

with assets in Russia, the EU and the US. In 2015 the

company produced 15.9 mn t of steel (unchanged from

2014) with 2015 sales of $8.0 bn, down from $10.4 bn in

2014. The company is 100% self-sufficient in iron ore

concentrate and in coke. NLMK is controlled by its Board

Chairman Vladimir Lisin via Fletcher Group Holdings Limited

(85.5% of total capital); while the rest of shares are in free

float, including an 8.6% listing on London Stock Exchange.

Financial and liquidity position

The second half of 2015 was challenging for the global steel

industry as steel prices fell by 18% over H1 as measured by

Shanghai Steel Rebar Futures. NLMK sales were down by

16% in H2 2015 largely reflecting market price dynamics. The

company improved profitability in 2015 with EBITDA margin

of at 23% versus 21% in 2014, driven mainly by a weak

rouble. However, in Q4 2015 EBITDA margin declined to 17%

returning to more conventional levels as the temporary

boost from rouble depreciation faded away.

The company reported strong operating results in Q1 2016

with steel production increasing by 3% YoY. Capacity

utilization rose to 93%, from the lowest level (of at least 4

years) of 92%.

In our view, the company has largely completed its

deleveraging process, as the current adjusted net

debt/EBITDA metric at 0.6x (according to the management)

and at 0.7x based on our calculations is below the

company’s target of 1.0x. The company may further repay

up to $300 mn of debt in 2016 if refinancing terms prove

unfavorable. Given the absence of large scale investment

projects and the comfortable leverage, distribution to

shareholders will become a priority use of free cash flow. In

2015 NLMK generated $977 mn of free cash flow, $395 mn

of which were directed towards dividends. The company

may amend its current dividend policy (which assumes

dividends of not higher than 50% either free cash flow or net

income as long as net debt/EBITDA is below 1.0x) to increase

dividend distributions in 2016.

At the end of 2015 the available liquidity included $343 mn

of cash, $1,243 mn of short-term financial investments and

$1,056 mn in credit lines, fully covering the company’s total

debt net of financial guarantees. NLMK had $531 mn of

short-term debt.

The company may close its NLMK Coating plant in France

this spring if it does not find a buyer for this asset. NLMK

Coating is a part of NLMK Belgium Holdings, a loss-making

European associate entity. In the last couple of years NLMK

has been reducing its exposure to European assets after

passing the control in the NBH to SOGEPA, a French public

sector holding company. A sale or closure of NLMK Coating

as well as other European assets would improve Group’s

profitability and cash generation, in our view.

We believe that flexibility of the dividend policy as well as

low capex program will allow the company to preseve its

credit quality at the current level in 2016.

Risks

Rouble appreciation/cost inflation

Prolonged weakness in steel prices/demand

Trade restrictions

9

14.4

14.6

14.8

15.0

15.2

15.4

15.6

15.8

16.0

2012 2013 2014 2015

Steel production, mn t

0

500

1,000

1,500

2,000

2,500

3,000

2016 2017 2018 2019 2020+

Liquidity and debt maturity schedule, USD mn

Credit lines

Short-term financial investments

Cash

Debt

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014 2015

Operating cash flow and capex, USD mn

Cash from operations

Capital expenditures

4,366

2,207

809

229 166 47 184

Sales structure in 2015, USD mn

Flat products

Pig iron, slabs and billets

Long products andmetalwareCoke and other chemicalproductsIron-ore and sintering ore

Scrap

Other products

0%

5%

10%

15%

20%

25%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2011 2012 2013 2014 2015

Sales (USD mn) and EBITDA margin

Sales EBITDA margin (rhs)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Mining Russian flatproducts

Russianlong

products

Foreignrolled

products

NBH All other

Profitability of segments in 2015, USD mn

EBITDA

EBITDA margin

3,146

1,603

1,357

684 374

844

Sales geography in 2015, USD mn

Russia

European Union

North America

Middle East, includingTurkey

Asia and Oceania

Other regions

10

IFRS, USD mn 2013 2014 2015 Sales 14,411 13,061 8,767 Sales YoY -2% -9% -33% EBITDA 1,751 2,317 1,430 EBITDA YoY -17% 32% -38% Net income -551 -1,278 -719 Net income YoY 30% 132% -44% Cash from operations 1,314 1,440 1,179 Capital expenditures 902 612 423 Free cash flow 412 828 756 Current ratio 1.2 1.3 1.4 Cash/Short-term debt 87% 143% 277% Short-term debt/Total debt 23% 12% 8% Total debt 8,164 7,300 6,954 Cash 1,576 1,086 1,375 Net debt 6,588 6,214 5,579 Capex/Depreciation 0.9 0.7 0.7 EBITDA margin 12.2% 17.7% 16.3% Total debt/EBITDA 4.7 3.2 4.9 Net debt/EBITDA 3.8 2.7 3.9 Net interest expense 687 564 482 EBITDA/Net int. expense 2.5 4.1 3.0

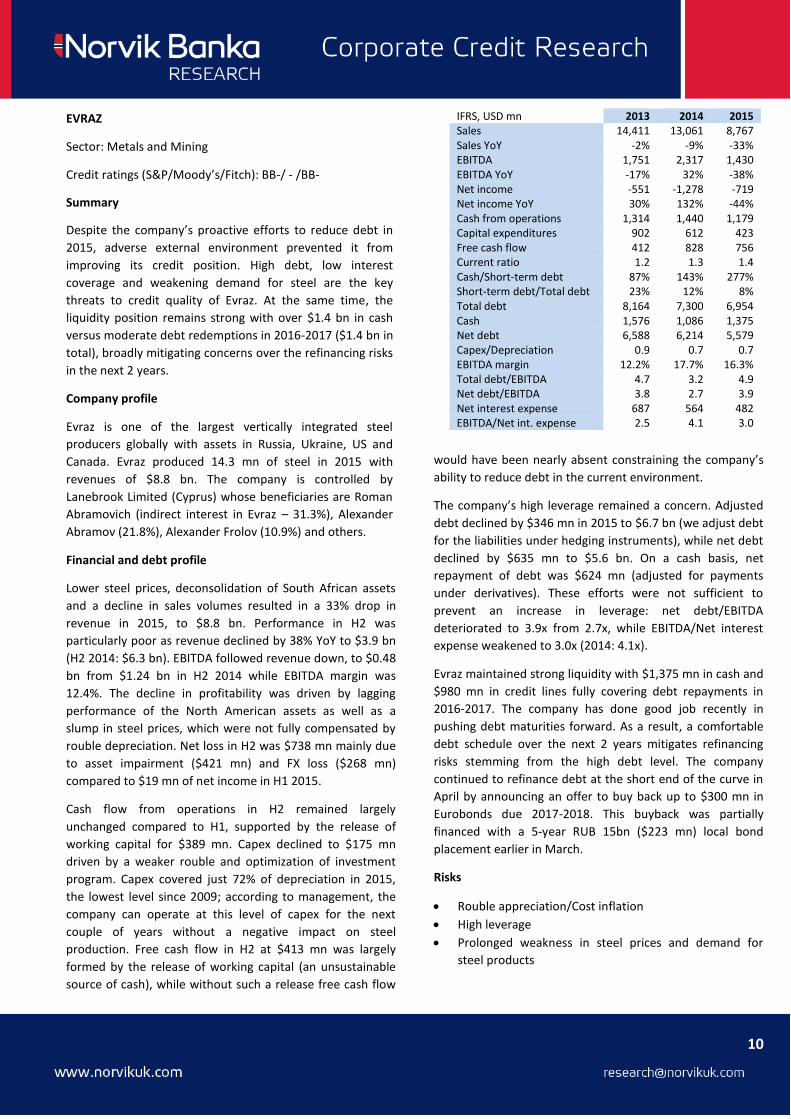

EVRAZ

Sector: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): BB-/ - /BB-

Summary

Despite the company’s proactive efforts to reduce debt in

2015, adverse external environment prevented it from

improving its credit position. High debt, low interest

coverage and weakening demand for steel are the key

threats to credit quality of Evraz. At the same time, the

liquidity position remains strong with over $1.4 bn in cash

versus moderate debt redemptions in 2016-2017 ($1.4 bn in

total), broadly mitigating concerns over the refinancing risks

in the next 2 years.

Company profile

Evraz is one of the largest vertically integrated steel

producers globally with assets in Russia, Ukraine, US and

Canada. Evraz produced 14.3 mn of steel in 2015 with

revenues of $8.8 bn. The company is controlled by

Lanebrook Limited (Cyprus) whose beneficiaries are Roman

Abramovich (indirect interest in Evraz – 31.3%), Alexander

Abramov (21.8%), Alexander Frolov (10.9%) and others.

Financial and debt profile

Lower steel prices, deconsolidation of South African assets

and a decline in sales volumes resulted in a 33% drop in

revenue in 2015, to $8.8 bn. Performance in H2 was

particularly poor as revenue declined by 38% YoY to $3.9 bn

(H2 2014: $6.3 bn). EBITDA followed revenue down, to $0.48

bn from $1.24 bn in H2 2014 while EBITDA margin was

12.4%. The decline in profitability was driven by lagging

performance of the North American assets as well as a

slump in steel prices, which were not fully compensated by

rouble depreciation. Net loss in H2 was $738 mn mainly due

to asset impairment ($421 mn) and FX loss ($268 mn)

compared to $19 mn of net income in H1 2015.

Cash flow from operations in H2 remained largely

unchanged compared to H1, supported by the release of

working capital for $389 mn. Capex declined to $175 mn

driven by a weaker rouble and optimization of investment

program. Capex covered just 72% of depreciation in 2015,

the lowest level since 2009; according to management, the

company can operate at this level of capex for the next

couple of years without a negative impact on steel

production. Free cash flow in H2 at $413 mn was largely

formed by the release of working capital (an unsustainable

source of cash), while without such a release free cash flow

would have been nearly absent constraining the company’s

ability to reduce debt in the current environment.

The company’s high leverage remained a concern. Adjusted

debt declined by $346 mn in 2015 to $6.7 bn (we adjust debt

for the liabilities under hedging instruments), while net debt

declined by $635 mn to $5.6 bn. On a cash basis, net

repayment of debt was $624 mn (adjusted for payments

under derivatives). These efforts were not sufficient to

prevent an increase in leverage: net debt/EBITDA

deteriorated to 3.9x from 2.7x, while EBITDA/Net interest

expense weakened to 3.0x (2014: 4.1x).

Evraz maintained strong liquidity with $1,375 mn in cash and

$980 mn in credit lines fully covering debt repayments in

2016-2017. The company has done good job recently in

pushing debt maturities forward. As a result, a comfortable

debt schedule over the next 2 years mitigates refinancing

risks stemming from the high debt level. The company

continued to refinance debt at the short end of the curve in

April by announcing an offer to buy back up to $300 mn in

Eurobonds due 2017-2018. This buyback was partially

financed with a 5-year RUB 15bn ($223 mn) local bond

placement earlier in March.

Risks

Rouble appreciation/Cost inflation

High leverage

Prolonged weakness in steel prices and demand for

steel products

11

13.0

13.5

14.0

14.5

15.0

15.5

16.0

16.5

17.0

2011 2012 2012 2013 2013

Crude steel production, mn t

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014 2015

Cash flow from operations and capex, USD mn

Cash from operations

Capital expenditures

5,987

2,270

1,068

433

Structure of sales by segments in 2015, USD mn

Steel

Steel, North America

Coal

Other operations

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2011 2012 2013 2014 2015

Sales (USD mn) and profitability

Sales EBITDA margin (rhs)

0

500

1000

1500

2000

2500

2016 2017 2018 2019 2020 2021 2022+

Liquidity and debt maturity schedule, as of end-2015, USD mn

Credit lines Cash Debt

-200

0

200

400

600

800

1,000

1,200

Steel Steel, NorthAmerica

Coal Other Unallocated Eliminations

EBITDA structure by segments in 2015, USD mn

3,104

2,566

1,354

664 815

264

Geography of sales in 2015, USD mn

Russia

Americas

Asia

CIS

Europe

Africa and others

12

IFRS, USD mn 2013 2014 2015 Sales 7,324 6,367 4,393 Sales YoY -11% -13% -31% EBITDA 2,247 2,152 1,434 EBITDA YoY -25% -4% -33% Net income 1,080 66 218 Net income YoY -37% -94% 229% Cash from operations 1,312 1,348 952 Capital expenditures 531 596 417 Free cash flow 781 753 535 Current ratio 3.1 2.5 1.8 Cash/Short term debt 2.75 0.85 0.60 Short term debt/Total debt 3% 14% 16% Total debt 5,965 4,734 4,387 Cash 523 550 824 Net debt 5,443 4,185 3,564 Capex/Depreciation 1.2 1.5 1.7 EBITDA margin 30.7% 33.8% 32.7% Total debt/EBITDA 2.7 2.2 3.1 Net debt/EBITDA 2.4 1.9 2.5 Net interest expense 430 305 191 EBITDA/Net int. expense 5.2 7.1 7.5

METALLOINVEST

Sector: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): BB/Ba2/BB

Summary

The company’s record in terms of deleveraging in H2 2015

was unsatisfactory, in our view. As a result, net debt/EBITDA

increased from 2.0x to 2.5x and will likely increase further to

around 3.0x in H1 2016 which we consider to be a high level

given the numerous risks the company faces. Based on our

interpretation of the recent rebound in iron ore and steel

prices as a temporary phenomenon, Metalloinvest’s

financial results are unlikely to materially improve in 2016

on 2015. The management reiterated a commitment to

reduce debt in 2016, mainly though repayment of $750 mn

due in July. However in absence of a material sustainable

rebound in iron ore prices, the company is unlikely to

generate enough free cash flow to improve its credit profile

compared to end-2015. Thus we see only limited upside for

Metalloinvest-2020s.

Company profile

Metalloinvest is the largest producer of iron ore and one of

the leading steel companies in Russia. Core assets are based

in Kursk, Belgorod and the Orenburg regions of Russia. The

company is controlled by Alisher Usmanov (48%), Vladimir

Skoch (30%) and Farhad Moshiri (10%).

Financial and liquidity position

2015 was a challenging year for mining companies globally

and especially for iron ore producers, as prices fell 40%

during the year. The decline in the company’s revenue was

slightly lower – 31% YoY, to $1,956 mn – supported by

performance of the Steel division. EBITDA followed revenue

lower, declining 49% YoY to $538 mn, while EBITDA margin

in H2 was 27.5%, the lowest level since 2009 as decline in

iron ore price outpaced rouble depreciation. Net loss

amounted to $299 mn driven by a $784 mn FX loss.

The company reported mixed production results in Q1 2016

with the production of iron ore up 4% YoY while the output

of steel declined by 3% YoY. We note the decline in

shipments of steel to the local market by 18% YoY, driven by

increased attractiveness of export destinations alongside

weak local demand.

The cash flow from operations was $319 mn; with $218 mn

of capex this resulted in $101 mn of free cash flow.

Management opted not to reduce debt in H2 by advancing

$321 mn of related party loans (we treat these transactions

as dividend payments), while net proceeds from borrowings

were $487 mn, almost fully reversing the positive trend seen

in H1 2015 (with a net debt repayment of $510 mn).

Such an aggressive debt policy resulted in increased leverage

measured by net debt/EBITDA metric, which rose to 2.5x

from 2.0x at the end of H1 2015. EBITDA/Net interest

expense picked up from 7.1x in 2014 to 7.5x. If iron ore

prices remain at current levels, average iron ore price in H1

16 should be close to the level of H2 15. Under such

assumption Net debt/EBITDA will likely exceed 3.0x.

The company retains a 3.2% stake in Norilsk Nickel, which

could potentially be used to generate additional liquidity. At

the time of writing, these shares were worth around $690

mn. Adjusted for this investment, net debt/EBITDA at end-

2015 would have been 2.0x.

In September 2015 Metalloinvest launched a pellet plant #3

which should increase the Group’s annual EBITDA by some

$25mn according to our estimates. During 2015 the

company continued construction of HBI plant which it plans

to launch in late 2016 – early 2017.

Risks

Prolonged weakness in steel and iron ore prices

Increasing leverage

Rouble appreciation/cost inflation

13

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2011 2012 2013 2014 2015

Production of key products, 000 mt

Iron ore Steel

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2011 2012 2013 2014 2015

Financial leverage metrics

Total debt/EBITDA

Net debt/EBITDA

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013 2014

Operating cash flow and capex, USD mn

Cash from operations

Capital expenditures

43%

3% 2%

3%

16%

22%

10%

Geography of sales in 2015

Russia

Rest of CIS

China

Rest of Asia

Middle East

Europe

Other countries

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

2,000

4,000

6,000

8,000

10,000

12,000

2011 2012 2013 2014 2015

Sales (USDmn) and EBITDA margin, USD mn

Sales

EBITDA margin (rhs)

0

200

400

600

800

1,000

1,200

1,400

1,600

2016 2017 2018 2019 2020 2021

Liquidity and debt maturity as of end-2015, USD mn

Credit linesShort-term deposits

CashDebt

0%

20%

40%

60%

80%

100%

120%

140%

160%

0

200

400

600

800

1,000

Mining Steel Trading All othersegments

EBITDA (USD mn) and EBITDA margin by segments in 2015

Adjusted EBITDA

EBITDA margin

41%

19%

12%

12%

11%

3%

Sales structure by product in 2015

Steel and rolledproducts

Iron ore pellets

Iron ore

Hot briquetted iron

Pig iron

Other revenue

14

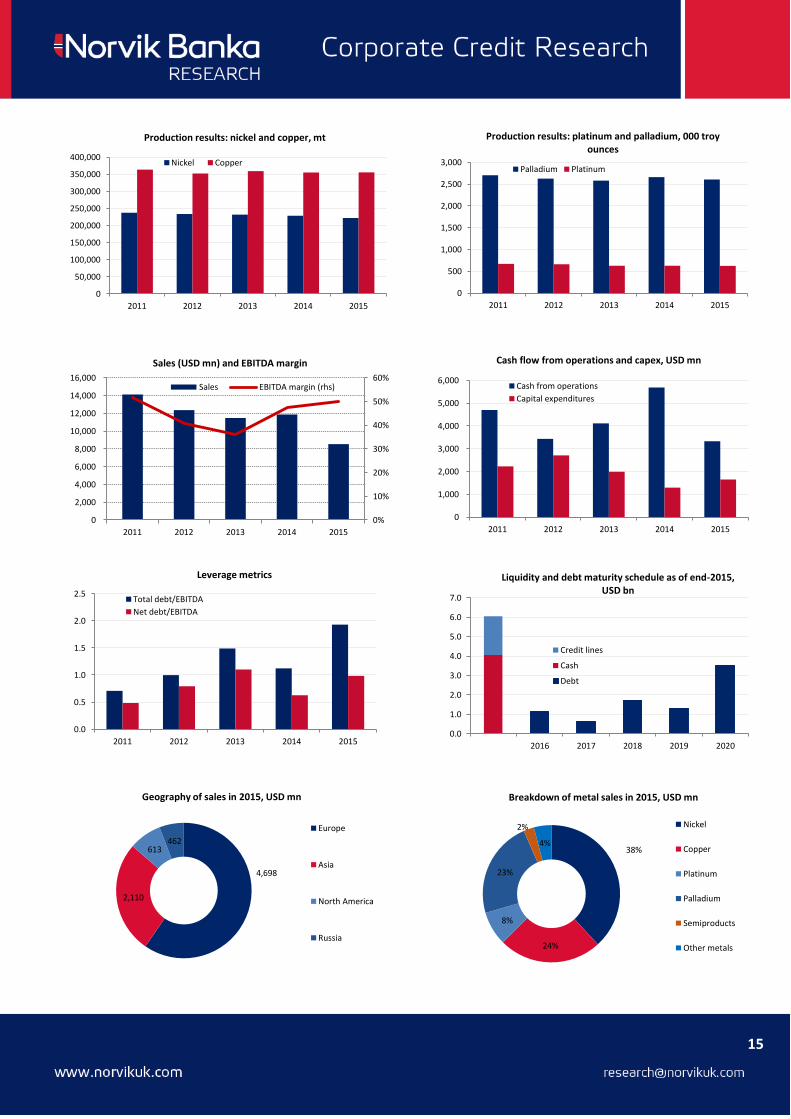

NORILSK NICKEL

Industry: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): BBB-/Ba1/BBB-

Summary

Norilsk Nickel has the highest credit rating in Russia’s

corporate Eurobond space. However, the recent

amendments to its dividend policy indicate that the

management may be targeting materially higher financial

leverage than historical average. The new dividend policy

targets net debt/EBITDA in the range of 1.8-2.2x compared

to the average of 0.9x in the last four years. We see a risk

that the company may lose its investment grade rating from

one or two agencies. Conversely, the company’s credit

profile is supported by its industry-leading position, a low

cost asset base, ample liquidity and positive free cash flow.

Company profile

Norilsk Nickel is a leading global producer of nickel, copper

and platinum group metals. The company recorded sales of

$8.5 bn in 2014 and EBITDA of $4.3 bn. The largest

shareholders are Interros (30%), UC Rusal (28%), Crispian

Investments Limited (6%) controlled by Vladimir Potanin,

Oleg Deripaska and Roman Abramovich respectively.

Metalloinvest holds a further 3% stake, while the rest are in

free float. Key operations are located in Krasnoyarsk and

Murmansk regions of Russia, as well as in Finland

(Harjavalta nickel refinery).

Financial/debt/liquidity profile

H2 financial results were hit by a slump in prices of key

metals: nickel prices declined by 27% versus H1, copper by

17%, platinum by 18% while palladium lost 21%. As a result,

revenue declined by 26% over H1 and by 41% YoY to $3.6

bn. EBITDA was $1.9 bn (-42% H2 over H1) with EBITDA

margin declining to 43.3% after a spike to 55.3% in H1 2015.

Net income was $243mn versus $1,493mn in H1, the decline

was driven by lower revenue and an FX loss of $743mn.

Cash flow from operations in H2 declined by 62% over H1, to

$912 mn (H1 2015: 2,417 mn) driven by lower sales and

profitability as well as large-scale investment in working

capital. However, capex surged 94% in H2 over H1, to $1,091

mn, following implementation of the downstream

reconfiguration program, accelerated development of

Skalisty underground mine and Bystrinsky project entering

final phase of construction. The negative trends in cash flow

and capex resulted in negative free cash flow of $179 mn.

Norilsk increased debt by $2.4 bn in H2 after a relatively

neutral H1 (+$68 mn on a cash flow basis). The surge in debt

and a decline in revenue resulted in weakening of net

debt/EBITDA which increased to 1.0x from 0.6x at the end of

H1 2015. We expect credit quality of the company to

weaken further in 2016 (see below).

The company had comfortable liquidity at the end of 2015:

cash and equivalents of $4.1 bn coupled with $2.0 bn in

credit lines covering debt repayments till 2020.

Following the decline in revenue and EBITDA, the previous

dividend policy assuming payment of 50% EBITDA but not

less than $2bn became unsustainable. The company

introduced a new dividend policy (in April 2016) envisaging

payment of 60% of EBITDA with net debt/EBITDA below 1.8x

and 30% EBITDA with net debt/EBITDA above 2.2x. The

company plans to pay at least $1.3 bn in dividends in 2017

(for 2016 results) not including additional payments from

sales of non-core assets and not less than $1.0 bn in the

following years, up to 2021. In our view these amendments

may result in net debt/EBITDA moving towards a 1.8-2.2x

range. At the same time, despite the changes in dividend

policy, the management reiterated commitment to preserve

the company’s investment grade credit rating.

Risks

An increase in leverage

Declines in key metal prices

Rouble appreciation

IFRS, USD mn 2013 2014 2015 Sales 11,489 11,869 8,542 Sales YoY -7% 3% -28% EBITDA 4,167 5,634 4,285 EBITDA YoY -17% 35% -24% Net income 765 2,000 1,716 Net income YoY -64% 161% -14% Cash from operations 4,115 5,688 3,329 Capital expenditures 1,989 1,298 1,654 Free cash flow 2,126 4,390 1,675 Current ratio 4.5 3.4 2.0 Cash/Short term debt 1.6 4.3 3.6 Short term debt/Total debt 0.20 0.11 0.16 Total debt 6,205 6,330 8,266 Cash 1,621 2,793 4,054 Net debt 4,584 3,537 4,212 Capex/Depreciation 2.3 1.6 3.3 EBITDA margin 36% 47% 50% Total debt/EBITDA 1.5 1.1 1.9 Net debt/EBITDA 1.1 0.6 1.0 Net interest expense 329 233 339 EBITDA/Net interest exp. 12.7 24.2 12.6

15

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2011 2012 2013 2014 2015

Production results: nickel and copper, mt

Nickel Copper

0%

10%

20%

30%

40%

50%

60%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2011 2012 2013 2014 2015

Sales (USD mn) and EBITDA margin

Sales EBITDA margin (rhs)

0.0

0.5

1.0

1.5

2.0

2.5

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

4,698

2,110

613 462

Geography of sales in 2015, USD mn

Europe

Asia

North America

Russia

0

500

1,000

1,500

2,000

2,500

3,000

2011 2012 2013 2014 2015

Production results: platinum and palladium, 000 troy ounces

Palladium Platinum

0

1,000

2,000

3,000

4,000

5,000

6,000

2011 2012 2013 2014 2015

Cash flow from operations and capex, USD mn

Cash from operations

Capital expenditures

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2016 2017 2018 2019 2020

Liquidity and debt maturity schedule as of end-2015, USD bn

Credit lines

Cash

Debt

38%

24%

8%

23%

2%

4%

Breakdown of metal sales in 2015, USD mn

Nickel

Copper

Platinum

Palladium

Semiproducts

Other metals

16

IFRS, USD mn 2013 2014 2015 Sales 6,432 6,009 4,127 Sales YoY -4% -7% -31% EBITDA 927 780 572 EBITDA YoY -8% -16% -27% Net income 433 52 -368 Net income YoY 8% -88% N/A Cash from operations 703 595 684 Capital expenditures 397 293 208 Free cash flow 45 50 205 Current ratio 1.6 1.3 1.3 Cash/Short-term debt 24% 33% 52% Short-term debt/Total debt 11% 24% 21% Total debt 3,694 3,223 2,801 Cash 93 253 305 Net debt 3,600 2,970 2,496 Capex/Depreciation 1.2 1.0 0.8 EBITDA margin 14% 13% 14% Total debt/EBITDA 4.0 4.1 4.9 Net debt/EBITDA 3.9 3.8 4.4 Net interest expense 262 252 271 EBITDA/Net interest exp. 3.5 3.1 2.1

TMK

Sector: Metals and Mining

Credit ratings: (S&P/Moody’s/Fitch): B+/B1 / -

Summary

The company’s credit quality deteriorated in H2 2015 driven

by rouble depreciation, a slump in the US market, increase

in cost of borrowing. At the same time, near-term outlook

looks comfortable with liquidity enough to cover debt

maturities of the next 12 months. However, the company

will have to be more proactive in cost optimization and

capex reduction to reverse the negative trends in credit

quality.

Company profile

TMK is a diversified global steel pipe producer with assets in

Russia, US, Europe, Kazakhstan and the UAE. The company

is the largest steel pipe producer in Russia with

approximately a 25% market share. Around ¾ of total pipe

sales go to the Oil and Gas industry, while the rest are sold

to industrial and construction companies. The company is

controlled by Dmitriy Pumpyanskiy (68% at end-Jan 2016).

Financial and debt profile

A combination of negative factors resulted in a very weak

H2 2015 financial results. Revenue declined 20% over H1 to

$1,830 mn on the back of rouble depreciation and falling

sales volumes by the American segment. EBITDA was 33%

lower YoY at $234 mn (H1 2015: $348 mn) as the company

struggled to keep prices in the Russian market up with

rouble depreciation, while losses in the American segment

remained a drag on the overall Group’s performance (Q4

2015 EBITDA margin was a negative 21%). TMK posted net

loss of $445 mn in H2 mainly due to an FX loss of $147 mn

and impairment of goodwill for $328 mn. Following rouble’s

appreciation and a rebound in oil prices since March,

financial results are likely to improve in Q2 2016,

Cash flow from operations tracked EBITDA lower, down 43%

to $148 mn (H1 2015: $261 mn), however unlike in H1 this

was not supported by the release of working capital. Capex

increased 13% to $110mn remaining at minimum levels

after the completion of the modernization program. Free

cash flow declined to a modest $38 mn (H1 2015: $163 mn)

constraining the company’s ability to deleverage.

The decline in EBITDA has significantly weakened credit

metrics of the company: Net debt/EBITDA increased to 4.4x

(H1 2015: 3.8x), while EBITDA/Net interest expense declined

to 2.1x. (H1 2015: 2.9x). The company did not reduce debt

on a cash flow basis in H2: net debt proceeds were $35mn

versus net debt repayment of $228mn in H1 2015. At the

end of 2015, TMK raised RUB 10bn ($141 mn) from VTB by

selling around 13.2% of share capital. The company

delivered 8% of share capital (treasury shares) with the

commitment to deliver the remaining part in 2016. In our

view the share sale highlights the limited ability of the

company to reduce debt from internally generated cash

flow. Sources of additional cash flow generation remain

constrained: the ability to reduce capex or release working

capital are limited, asset sales are unlikely to improve

leverage, while further sales of shares cannot be a

sustainable source of financing.

Sale of shares to VTB supported liquidity: at the end of 2015

the company had $305 mn of cash and equivalents and

another $528 mn in credit lines versus $575 mn of short-

term debt. The company is unlikely to have any problems

with the refinancing of debt in the next 12 months due to

liquidity surplus in the local market. At the beginning of

April TMK issued RUB 5bn of 5-year local bonds and

simultaneously announced buyback for its Eurobond due

2018 for the total of $200 mn. This should help push

maturities further and to smooth out the debt schedule for

2018, however this will likely increase cost of borrowings.

Risks

FX mismatch between revenue and debt

Increase in cost of borrowings

Rouble depreciation

Refinancing risk

17

0

500

1,000

1,500

2,000

2,500

3,000

2011 2012 2013 2014 2015

Pipe production, 000 mt

Seamless Pipe Welded Pipe

0

100

200

300

400

500

600

700

800

900

2016 2017 2018 2019 2020 2021+

Liquidity and debt maturity schedule as of end-2015, USD mn

Credit facilitiesCashDebt repayment

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015

Cash flow from operations and capex, USD mn

Cash from operations

Capital expenditures

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Adjusted EBITDA margins of the segments

Russia

America

Europe

11.5%

12.0%

12.5%

13.0%

13.5%

14.0%

14.5%

15.0%

15.5%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2011 2012 2013 2014 2015

Revenue (USD mn) and EBITDA margin

Sales

EBITDA margin (rhs)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

3,190 742

196

Revenue by division in 2015, USD mn

Russia

America

Europe

628

-22

31

-100

0

100

200

300

400

500

600

700

Russia America Europe

Adjusted EBITDA by segments in 2015, USD mn

18

IFRS, USD mn 2013 2014 2015 Sales 2,259 2,197 2,159 Sales YoY -14% -3% -2% EBITDA 907 1,011 1,247 EBITDA YoY -31% 11% 23% Net income 143 -182 1119 Net income YoY -85% -227% -715% Cash from operations 422 809 954 Capital expenditures 1384 570 327 Free cash flow -962 239 627 Current ratio 3.2 2.4 11.4 Cash/Short term debt 3.0 13.5 53.7 Short term debt/Total debt 22% 5% 2% Total debt 1,206 2,207 2,683 Cash 809 1,217 2,039 Net debt 397 990 4,294 Capex/Depreciation 6.5 3.1 2.6 EBITDA margin 40% 46% 58% Total debt/EBITDA 1.3 2.2 5.1 Net debt/EBITDA 0.4 1.0 0.5 Net interest expense 48 86 88 EBITDA/Net int. expense 18.9 11.8 14.2

POLYUS

Sector: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): BB-/ - /BB-

Summary

After the completion of a share buyback by entities

controlled by the Kerimov family, Polyus became one of the

most leveraged public companies in Russia. Part of the debt

raised to finance the share buyback remains at parental

level, however we acknowledge that the single source of

cash flow to service and repay this debt is Polyus itself, thus

any deleveraging will be a lengthy process. This means little

upside for company’s credit quality while downside is

relatively high and depends mainly on gold price.

Company profile

Polyus Gold is the largest gold producer in Russia producing

1.75 mn oz of gold in 2015. The company operates 5 mines

and one production site in Siberia and the Far East regions

of Russia, and is the 4th

largest gold company globally by

proven and probable reserves. The company’s operations

are located in Krasnoyarsk, Irkutsk, Magadan regions and

Yakutia. Polyus recorded $2.2bn of sales and $1.2 bn EBITDA

in 2015. The key shareholder is Said Kerimov (over 95%).

Financial and debt profile

Weak gold price performance in H2 2015 was partly offset

by increased gold production which was at 968 Koz (+2.7%

YoY). Revenue declined by 5% YoY to $1’154 mn, while

EBITDA increased by 6.5% YoY to $658 mn with record

EBITDA margin of 58%.

The company’s high profitability was driven by its low cost

position: in 2015 Polyus remained one of the lowest cost

gold producers globally with total cash costs at $424/oz

(2014: $585/oz) and all-in sustaining costs at $610/oz (2014:

$825/oz). As a result the company is highly resilient to

volatility in gold prices.

At the end of 2015, Wandle Holdings and Sacturino Limited

controlled by Said Kerimov, the son of Suleiman Kermov,

completed a share buyback of Polyus Gold International

Limited (Jersey), a former holding company for the group’s

assets. According to public sources, the companies financed

buyback with a loan from VTB for the total of $5.5bn,

virtually all shares bought back were pledged to VTB as a

collateral under the loan. In our view Polyus Gold is the

single asset which will service the debt at the parental level,

thus we adjust Polyus’s debt for the debt held by Sacturino

and Wandle. This transaction transformed Polyus to one of

the most leveraged public corporate borrowers in Russian

corporate eurobond space.

On 11 March 2015 the new holding company JSC Polyus

Gold (Russia) announced share buyback for the total of RUB

255.3 bn buying back shares mainly from parent companies,

which effectively transferred part of the debt accumulated

by parent companies to the balance sheet of Polyus. The

buyback was financed with a US$2.5 bn loan from Sberbank.

We estimate net debt/EBITDA below 3.5x post buyback, the

level set by a covenant in the Eurobond prospectus. Total

adjusted debt of Polyus (including around $8.5 bn of debt at

the parent level) at the end of 2015 was around $11.2 bn,

while adjusted net debt/EBITDA was 7.4x. Given the high

amount of debt relative to cash flow generated by the

company and the lack of transparency regarding the total

amount of debt we consider Polyus to be a very risky play.

The company actively hedges its exposure to gold price risk

by using options which partly mitigates the effects of gold

price volatility on revenue. At the end of 2015 around 48%

of future production was hedged with collars (combination

of call and put options).

Risks

High leverage

Rouble appreciation

Lack of transparency regarding debt held at parent’s

level

Deterioration in corporate governance after delisting

from London Stock Exchange

19

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2011 2012 2013 2014 2015

Refined gold production, koz

0%

10%

20%

30%

40%

50%

60%

70%

0

500

1,000

1,500

2,000

2,500

3,000

2011 2012 2013 2014 2015

Sales (USD mn) and EBITDA margin

Sales EBITDA margin

0

500

1,000

1,500

2,000

2,500

3,000

Liquidity 2016 2017 2018 2019 2020 2020+

Liquidity and debt maturity as of end-2015, USD mn

Undrawn facilities

Cash

Debt repayments

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1,000

1,200

Krasnoyarsk Irkutsk alluvial Irkutsk ore YakutiaKuranakh

EBITDA (USD mn) and EBITDA margin of segments in 2015

Adjusted EBITDA

EBITDA margin (rhs)

0

100

200

300

400

500

600

700

800

Gold production by mine in 2015, koz

0

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013 2014 2015

Cash flow from operations and capex, USD mn

Cash from operations

Capital expenditures

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

0

200

400

600

800

1,000

1,200

2012 2013 2014 2015

Total cash cost and all-in sustaining cost, USD/oz

Total cash cost All-in sustaining cash cost

20

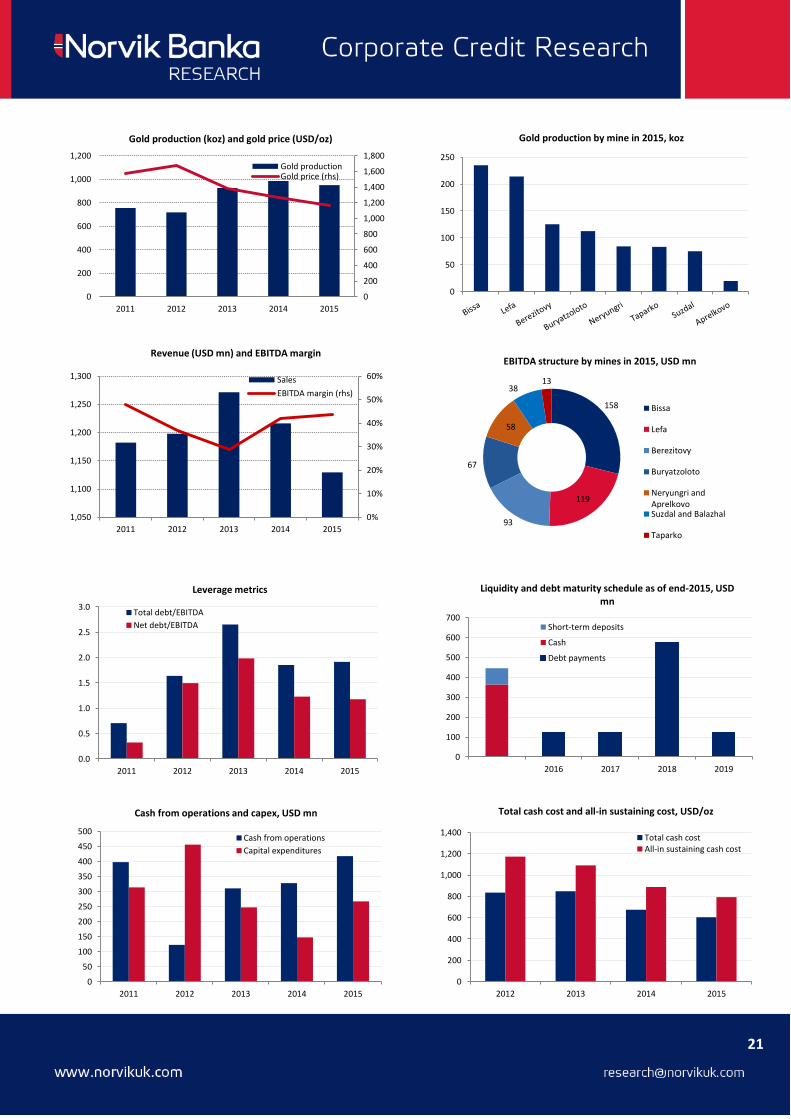

IFRS, USD mn 2013 2014 2015 Sales 1,271 1,216 1,129 Sales YoY 6% -4% -7% EBITDA 365 510 493 EBITDA YoY -18% 40% -3% Net income -199 123 189 Net income YoY NA NA 53% Cash from operations 311 328 418 Capital expenditures 248 148 267 Free cash flow 63 180 151 Current ratio 1.4 3.6 2.0 Cash/Short term debt 0.7 26.3 2.2 Short term debt/Total debt 34% 1% 14% Total debt 968 944 946 Cash 244 318 364 Net debt 724 627 582 Capex/Depreciation 1.1 0.7 1.3 EBITDA margin 29% 42% 44% Total debt/EBITDA 2.7 1.9 1.9 Net debt/EBITDA 2.0 1.2 1.2 Net interest expense 67 67 45 EBITDA/Net int. expense 5.5 7.6 11.0

NORDGOLD

Sector: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): -/Ba3/BB-

Summary

In our view the credit position of Nordgold is supported by

its low cost asset base, geographic diversification as well as a

moderate debt level. The company has a proven track record

of successful commissioning of new mining assets and plans

to launch the new Bouly mine which should increase the

company’s gold production by 12% from 2017. On the other

hand, the company is relatively small and has a highly

concentrated debt maturity schedule (around 60% of its

total debt comes due in 2018). We expect Nordgold to

address this issue in 2016-2017.

Company profile

Nordgold is a gold producer with nine operating mines in

Russia, Kazakhstan, Burkina Faso and Guinea. Nordgold has

proven and probable reserves of 13.0 Moz and produced

950 Koz of gold in 2015. The company is controlled by

Aleksey Mordashov (90%), while the rest of the shares are

listed on the London Stock Exchange.

Financial/debt/liquidity position

Nordgold increased gold output by 2% YoY in Q4: the

company produced 242 thousand ounces (Koz) of gold, total

gold production in 2015 was 950 Koz, in line with production

guidance of 925-985 Koz. Gold production in 2016 is

expected to be in the range of 950-1’010 Koz or 0-4% higher

versus 2015. Q4 revenue was $264 mn or 4% higher YoY

while full-year revenue for 2015 was $1,129 mn or 7% lower

versus 2014. The company reported weak production results

for Q1 2016 with gold production lower by 21% YoY, while

revenue declined by 30% YoY driven by lower production

volumes and weak gold prices. At the current level of

production, total gold output in 2016 should be closer to the

lower bound of the guidance.

The increase in net debt to $584 mn (Q3 2015: $573 mn)

was driven by payment of $13 mn dividend, $3 mn share

buyback and capex related to Bouly mine (Burkina Faso). The

company reiterated plans to start Bouly on schedule in H2

2016 and expects that all-in sustainable cost (AISC) of gold

production at the mine will be around $730/oz. AISC for the

whole company was around $790/oz in 2015 and Nordgold

expects growth to $800-850/oz in 2016 mainly due to cost

pressures.

The company reported $264 mn of revenue (+4% YoY) in the

last quarter of 2015 driven by increased gold sales. However

EBITDA was relatively weak at $69 mn with EBITDA margin

at 26% due to a non-cash impairment of inventory.

Cash flow from operations was at $88 mn with capex at $87

mn driving free cash flow to a modest $1 mn. Net

debt/EBITDA slightly increased to 1.2x from 1.1x at the end

of Q3 2015, while EBITDA/Net interest expense was at a

healthy 11.0x level.

From a liquidity standpoint the company will have to repay

$125 mn in 2016 out of $500 mn loan received from

Sberbank in 2014 which looks easily manageable given the

comfortable liquidity including cash and short-term deposits

for the total of $364 mn. Company debt repayments peak in

2018 at $575 mn when the Eurobond comes due.

The company plans to launch Bouly mine in H2 2016 with

capacity of 120k ounces of gold per year and expects all-in

sustainable cost of $730/oz (Q4 2015: $892/oz for the

company) which should improve cash flow generation and

profitability and will support credit position.

Risks

Exposure to emerging African economies

Concentrated debt schedule in 2018

Prolonged weakness in gold price

Appreciation of local currencies (RUB, KZT, GHS, XOF)

versus USD

21

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

200

400

600

800

1,000

1,200

2011 2012 2013 2014 2015

Gold production (koz) and gold price (USD/oz)

Gold productionGold price (rhs)

0%

10%

20%

30%

40%

50%

60%

1,050

1,100

1,150

1,200

1,250

1,300

2011 2012 2013 2014 2015

Revenue (USD mn) and EBITDA margin

Sales

EBITDA margin (rhs)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014 2015

Cash from operations and capex, USD mn

Cash from operations

Capital expenditures

0

50

100

150

200

250

Gold production by mine in 2015, koz

158

119

93

67

58

38 13

EBITDA structure by mines in 2015, USD mn

Bissa

Lefa

Berezitovy

Buryatzoloto

Neryungri andAprelkovoSuzdal and Balazhal

Taparko

0

100

200

300

400

500

600

700

2016 2017 2018 2019

Liquidity and debt maturity schedule as of end-2015, USD mn

Short-term deposits

Cash

Debt payments

0

200

400

600

800

1,000

1,200

1,400

2012 2013 2014 2015

Total cash cost and all-in sustaining cost, USD/oz

Total cash costAll-in sustaining cash cost

22

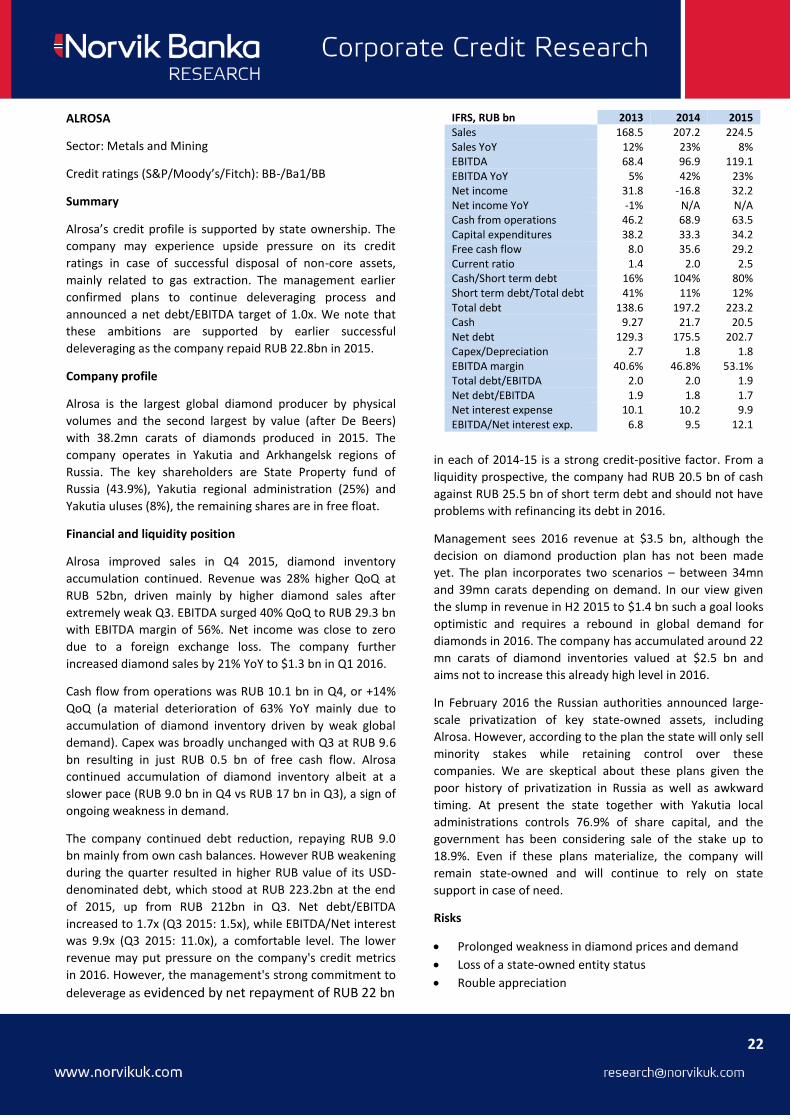

IFRS, RUB bn 2013 2014 2015 Sales 168.5 207.2 224.5 Sales YoY 12% 23% 8% EBITDA 68.4 96.9 119.1 EBITDA YoY 5% 42% 23% Net income 31.8 -16.8 32.2 Net income YoY -1% N/A N/A Cash from operations 46.2 68.9 63.5 Capital expenditures 38.2 33.3 34.2 Free cash flow 8.0 35.6 29.2 Current ratio 1.4 2.0 2.5 Cash/Short term debt 16% 104% 80% Short term debt/Total debt 41% 11% 12% Total debt 138.6 197.2 223.2 Cash 9.27 21.7 20.5 Net debt 129.3 175.5 202.7 Capex/Depreciation 2.7 1.8 1.8 EBITDA margin 40.6% 46.8% 53.1% Total debt/EBITDA 2.0 2.0 1.9 Net debt/EBITDA 1.9 1.8 1.7 Net interest expense 10.1 10.2 9.9 EBITDA/Net interest exp. 6.8 9.5 12.1

ALROSA

Sector: Metals and Mining

Credit ratings (S&P/Moody’s/Fitch): BB-/Ba1/BB

Summary

Alrosa’s credit profile is supported by state ownership. The

company may experience upside pressure on its credit

ratings in case of successful disposal of non-core assets,

mainly related to gas extraction. The management earlier

confirmed plans to continue deleveraging process and

announced a net debt/EBITDA target of 1.0x. We note that

these ambitions are supported by earlier successful

deleveraging as the company repaid RUB 22.8bn in 2015.

Company profile

Alrosa is the largest global diamond producer by physical

volumes and the second largest by value (after De Beers)

with 38.2mn carats of diamonds produced in 2015. The

company operates in Yakutia and Arkhangelsk regions of

Russia. The key shareholders are State Property fund of

Russia (43.9%), Yakutia regional administration (25%) and

Yakutia uluses (8%), the remaining shares are in free float.

Financial and liquidity position

Alrosa improved sales in Q4 2015, diamond inventory

accumulation continued. Revenue was 28% higher QoQ at

RUB 52bn, driven mainly by higher diamond sales after

extremely weak Q3. EBITDA surged 40% QoQ to RUB 29.3 bn

with EBITDA margin of 56%. Net income was close to zero

due to a foreign exchange loss. The company further

increased diamond sales by 21% YoY to $1.3 bn in Q1 2016.

Cash flow from operations was RUB 10.1 bn in Q4, or +14%

QoQ (a material deterioration of 63% YoY mainly due to

accumulation of diamond inventory driven by weak global

demand). Capex was broadly unchanged with Q3 at RUB 9.6

bn resulting in just RUB 0.5 bn of free cash flow. Alrosa

continued accumulation of diamond inventory albeit at a

slower pace (RUB 9.0 bn in Q4 vs RUB 17 bn in Q3), a sign of

ongoing weakness in demand.

The company continued debt reduction, repaying RUB 9.0

bn mainly from own cash balances. However RUB weakening

during the quarter resulted in higher RUB value of its USD-

denominated debt, which stood at RUB 223.2bn at the end

of 2015, up from RUB 212bn in Q3. Net debt/EBITDA

increased to 1.7x (Q3 2015: 1.5x), while EBITDA/Net interest

was 9.9x (Q3 2015: 11.0x), a comfortable level. The lower

revenue may put pressure on the company's credit metrics

in 2016. However, the management's strong commitment to

deleverage as evidenced by net repayment of RUB 22 bn

in each of 2014-15 is a strong credit-positive factor. From a

liquidity prospective, the company had RUB 20.5 bn of cash

against RUB 25.5 bn of short term debt and should not have

problems with refinancing its debt in 2016.

Management sees 2016 revenue at $3.5 bn, although the

decision on diamond production plan has not been made

yet. The plan incorporates two scenarios – between 34mn

and 39mn carats depending on demand. In our view given

the slump in revenue in H2 2015 to $1.4 bn such a goal looks

optimistic and requires a rebound in global demand for

diamonds in 2016. The company has accumulated around 22

mn carats of diamond inventories valued at $2.5 bn and

aims not to increase this already high level in 2016.

In February 2016 the Russian authorities announced large-

scale privatization of key state-owned assets, including

Alrosa. However, according to the plan the state will only sell

minority stakes while retaining control over these

companies. We are skeptical about these plans given the

poor history of privatization in Russia as well as awkward

timing. At present the state together with Yakutia local

administrations controls 76.9% of share capital, and the

government has been considering sale of the stake up to

18.9%. Even if these plans materialize, the company will

remain state-owned and will continue to rely on state

support in case of need.

Risks

Prolonged weakness in diamond prices and demand

Loss of a state-owned entity status

Rouble appreciation

23

0

5

10

15

20

25

30

35

40

45

2011 2012 2013 2014 2015

Production and sales of diamonds, mn carats

Production Sales

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015

Cash from operations and capital expenditures, RUB bn

Cash from operations

Capital expenditures

90%

3% 8%

Sales structure by product in 2015

Diamonds

Gas

Other

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50

100

150

200

250

2011 2012 2013 2014 2015

Sales and profitability

Sales

EBITDA margin

0

200

400

600

800

1,000

1,200

2016 2017 2018 2019 2020

Liquidity and debt maturity (USD mn)

Credit lines

Cash

Debt payments

0

10

20

30

40

50

60

70

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Diamond inventories, RUB bn

98

43

34

24 10

8 7

Geography of sales in 2015, RUB bn

Belgium Russia

India Israel

China UAE

Others

24

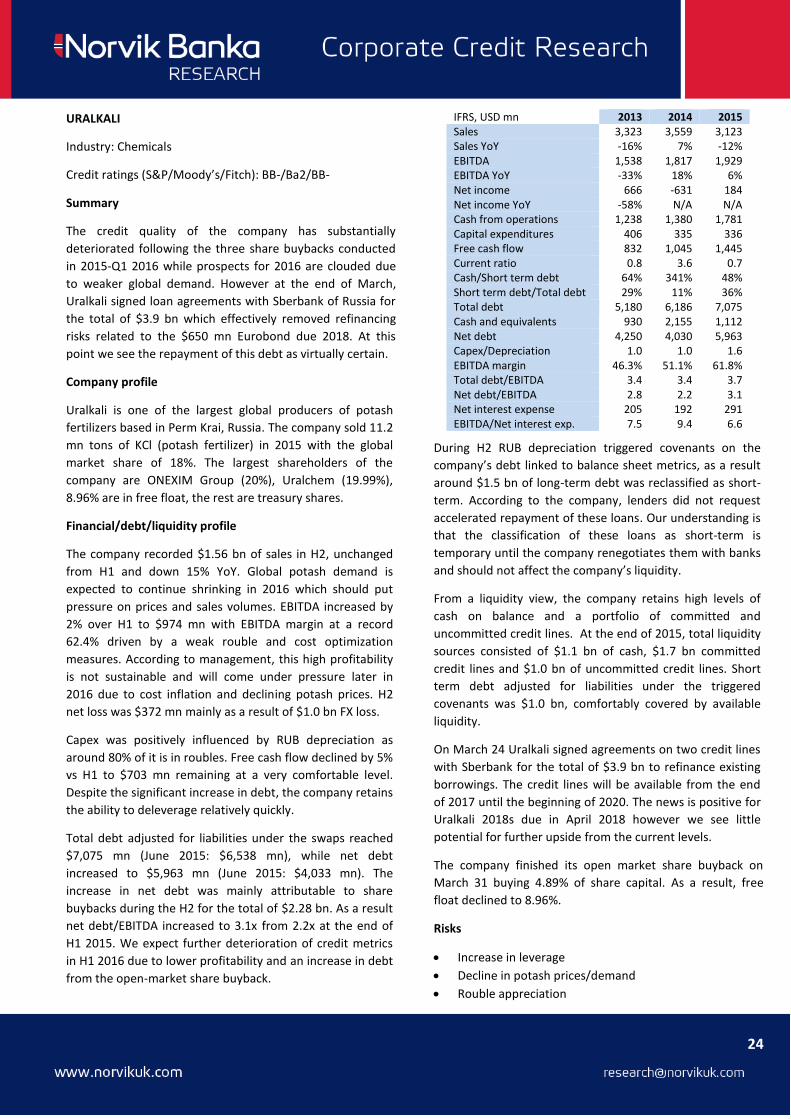

URALKALI

Industry: Chemicals

Credit ratings (S&P/Moody’s/Fitch): BB-/Ba2/BB-

Summary

The credit quality of the company has substantially

deteriorated following the three share buybacks conducted

in 2015-Q1 2016 while prospects for 2016 are clouded due

to weaker global demand. However at the end of March,

Uralkali signed loan agreements with Sberbank of Russia for

the total of $3.9 bn which effectively removed refinancing

risks related to the $650 mn Eurobond due 2018. At this

point we see the repayment of this debt as virtually certain.

Company profile

Uralkali is one of the largest global producers of potash

fertilizers based in Perm Krai, Russia. The company sold 11.2

mn tons of KCl (potash fertilizer) in 2015 with the global

market share of 18%. The largest shareholders of the

company are ONEXIM Group (20%), Uralchem (19.99%),

8.96% are in free float, the rest are treasury shares.

Financial/debt/liquidity profile

The company recorded $1.56 bn of sales in H2, unchanged

from H1 and down 15% YoY. Global potash demand is

expected to continue shrinking in 2016 which should put

pressure on prices and sales volumes. EBITDA increased by

2% over H1 to $974 mn with EBITDA margin at a record

62.4% driven by a weak rouble and cost optimization

measures. According to management, this high profitability

is not sustainable and will come under pressure later in

2016 due to cost inflation and declining potash prices. H2

net loss was $372 mn mainly as a result of $1.0 bn FX loss.

Capex was positively influenced by RUB depreciation as

around 80% of it is in roubles. Free cash flow declined by 5%

vs H1 to $703 mn remaining at a very comfortable level.

Despite the significant increase in debt, the company retains

the ability to deleverage relatively quickly.

Total debt adjusted for liabilities under the swaps reached

$7,075 mn (June 2015: $6,538 mn), while net debt

increased to $5,963 mn (June 2015: $4,033 mn). The

increase in net debt was mainly attributable to share

buybacks during the H2 for the total of $2.28 bn. As a result

net debt/EBITDA increased to 3.1x from 2.2x at the end of

H1 2015. We expect further deterioration of credit metrics

in H1 2016 due to lower profitability and an increase in debt

from the open-market share buyback.

During H2 RUB depreciation triggered covenants on the

company’s debt linked to balance sheet metrics, as a result

around $1.5 bn of long-term debt was reclassified as short-

term. According to the company, lenders did not request

accelerated repayment of these loans. Our understanding is

that the classification of these loans as short-term is

temporary until the company renegotiates them with banks

and should not affect the company’s liquidity.

From a liquidity view, the company retains high levels of

cash on balance and a portfolio of committed and

uncommitted credit lines. At the end of 2015, total liquidity

sources consisted of $1.1 bn of cash, $1.7 bn committed

credit lines and $1.0 bn of uncommitted credit lines. Short

term debt adjusted for liabilities under the triggered

covenants was $1.0 bn, comfortably covered by available

liquidity.

On March 24 Uralkali signed agreements on two credit lines

with Sberbank for the total of $3.9 bn to refinance existing

borrowings. The credit lines will be available from the end

of 2017 until the beginning of 2020. The news is positive for

Uralkali 2018s due in April 2018 however we see little

potential for further upside from the current levels.

The company finished its open market share buyback on

March 31 buying 4.89% of share capital. As a result, free

float declined to 8.96%.

Risks

Increase in leverage

Decline in potash prices/demand

Rouble appreciation

IFRS, USD mn 2013 2014 2015 Sales 3,323 3,559 3,123 Sales YoY -16% 7% -12% EBITDA 1,538 1,817 1,929 EBITDA YoY -33% 18% 6% Net income 666 -631 184 Net income YoY -58% N/A N/A Cash from operations 1,238 1,380 1,781 Capital expenditures 406 335 336 Free cash flow 832 1,045 1,445 Current ratio 0.8 3.6 0.7 Cash/Short term debt 64% 341% 48% Short term debt/Total debt 29% 11% 36% Total debt 5,180 6,186 7,075 Cash and equivalents 930 2,155 1,112 Net debt 4,250 4,030 5,963 Capex/Depreciation 1.0 1.0 1.6 EBITDA margin 46.3% 51.1% 61.8% Total debt/EBITDA 3.4 3.4 3.7 Net debt/EBITDA 2.8 2.2 3.1 Net interest expense 205 192 291 EBITDA/Net interest exp. 7.5 9.4 6.6

25

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015

Production of KCl fertilizer, mn t

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2016 2017 2018 2019 2020+

Liquidity and debt maturity schedule as of end-2015

Uncommitted credit lines

Committed credit lines

Cash

Debt payments

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2011 2012 2013 2014 2015

Cash flow from operations and capex, USD mn

Cash from operations

Capital expenditures

406

2,008

628

81

Geography of sales in 2015, USD mn

Russia

Latin America, China,India, South East Asia

USA, Europe

Other countries

0%

10%

20%

30%

40%

50%

60%

70%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2011 2012 2013 2014 2015

Sales and EBITDA margin, USD mn

Sales EBITDA margin

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014 2015

Leverage metrics

Total debt/EBITDA

Net debt/EBITDA

0

50

100

150

200

250

300

350

400

2012 2013 2014 2015

Cash cost of potash and selling price, USD/mt

Cash costs

Average export potash price, FCA

0

2

4

6

8

10

12

2011 2012 2013 2014 2015

Geography of potash sales, mn t

Domestic

External

26

IFRS, RUB bn 2013 2014 2015 Sales 104.6 123.1 189.7 Sales YoY -1% 18% 54% EBITDA 24.0 37.1 83.3 EBITDA YoY -32% 54% 124% Net income 8.6 -13.4 36.4 Net income YoY -65% -256% -372% Cash from operations 17.9 27.5 63.3 Capital expenditures 17.6 20.4 42.4 Free cash flow 0.3 7.1 20.8 Current ratio 1.5 1.4 1.7 Cash/Short term debt 68% 100% 101% Short-term debt/Total debt 25% 25% 22% Total debt 54.9 124.0 134.6 Cash 8.9 30.7 29.3 Net debt 46.0 93.3 105.3 Capex/Depreciation 2.3 2.6 4.7 EBITDA margin 23% 30% 44% Total debt/EBITDA 2.3 3.3 1.6 Net debt/EBITDA 1.9 2.5 1.3 Net interest expense 1.9 2.7 5.5 EBITDA/Net interest exp. 12.6 13.8 15.3

PHOSAGRO

Industry: Chemicals

Credit ratings (S&P/Moody’s/Fitch): BBB-/Ba1/BB+

Summary

We see Phosagro as the strongest credit in Russia’s

chemicals credit space due to its low leverage, strong

positive free cash flow and a demonstrated commitment to

deleveraging. We see minimal risks to the current credit

position of the company, which are mainly related to the

weakening global demand for fertilizers.

Company profile

Phosagro is the leading vertically integrated producer of

phosphate-based and other mineral fertilizers in Russia. Key

production facilities are located in Vologda, Murmansk,

Saratov and Leningrad regions of Russia. Phosagro produced

5.4 mn t of phosphate-based fertilizers in 2015 with revenue

at $3.1 bn. Company’s ore reserves allow it to keep

production for 70+ years at the current rate. The company is

controlled by Andrey Guryev and his family.

Financial and debt profile

Rouble depreciation resulted in an exceptionally strong year

for the company. Revenue increased by 54% YoY in 2015 to

RUB 190bn, on higher sales volumes and a weaker ruble.

EBITDA surged 124% with EBITDA margin at record 44%

(2014: 30%). Net income for the full year was RUB 36.4 bn

although H2 net income at RUB 8.8 bn was strongly affected

by an FX loss. The company continued to reduce cash cost

of DAP (diammonium phosphate) production in 2016: it was

$133/mt in February 2016 vs $177/mt in 2015, which should

provide support to profitability in H1 2016 despite the

recent decline in DAP prices. At the same time the company

maintains a wide margin of safety in terms of costs as DAP

price in March was at $360/mt. Overall we expect financial

results in 2016 to be weaker compared to 2015 as cost

inflation kicks in while DAP prices in January-February

declined to lows last seen in 2013.

Cash flow from operations declined to RUB 30.2 bn in H2

after RUB 32.7 bn in H1 amid a seasonal increase in working

capital. At the same time capex surged 81% on H1 to RUB

27.4bn and were driven by such projects as construction of

Main Shaft 2 at the Kirovsky underground mine,

construction of a new 760 Kt per annum ammonia plant,

construction of a new 500 Kt per annum urea plant. Free

cash flow improved to RUB 20.8bn for the full year (2014:

RUB 7.1 bn). The main source of free cash flow utilization

was payment of dividends: Phosagro paid RUB 18.1bn to

shareholders versus RUB 5.7bn in 2014.

The company improved its leverage during 2015 after