The Chinese Conundrum - Platts · B 236 8.40 Colour order (left to right, top to bottom) R 59 G 110...

20

Rabobank Food & Agribusiness Research and Advisory September 2016 The Chinese Conundrum Self Sufficiency or Imports?

-

Upload

truongxuyen -

Category

Documents

-

view

215 -

download

0

Transcript of The Chinese Conundrum - Platts · B 236 8.40 Colour order (left to right, top to bottom) R 59 G 110...

12.40

6.40

6.80

5.80

0.80

1.20

7.80

8.80

9.00

0.20

0.20

12.40 7.90

7.50

Guides for gutter

Text colours

R 27 G 66 B 152

R 0 G 0 B 0

R 127 G 127 B 127

Background shading

R 242 G 242 B 242

R 225 G 235 B 244

R 227 G 244 B 236

8.40

Colour order (left to right, top to bottom)

R 59 G 110 B 143

R 251 G 193 B 119

R 115 G 198 B 161

R 103 G 153 B 200

R 186 G 163 B 171

R 191 G 191 B 191

R 127 G 127 B 127

R 201 G 48 B 146

R 27 G 66 B 152

R 84 G 7 B 91

R 248 G 152 B 29

R 241 G 237 B 238

R 254 G 234 B 210

R 211 G 227 B 237 Rabobank

Food & Agribusiness Research and Advisory September 2016

The Chinese Conundrum

Self Sufficiency or Imports?

2

Our approach to client relationships

Driven by sector knowledge & supported by product capabilities

Sectors covered:

Dairy

Ingredients & Sugar

Grains & Oilseeds

Value-added Processing

Beverages

Animal Protein

Farm Inputs

Broader sub sector coverage

Sub sector specialists involved in both origination and execution for financing and advisory products

Sub sector coverage bankers cover an entire region (Europe, Americas or Asia)

M&A bankers specialised into 11 sub sectors of the food, drinks and agri spectrum

Access to deeper research

Rabobank has its own unique group of dedicated and highly specialised Food and Agri Research analysts (FAR)

FAR comprises 80 analysts in 13 countries around the globe

Fundamental research covering the entire food and drinks chain

Output in the form of tailored presentations for internal and external clients, World Maps, Industry Notes, F&A Reviews, Commodity Notes and Regional Banking Reports

3

Leading global financial institution for Sugar sector

9/10 9 of the Top 10 Global Sugar companies are Rabobank clients

70 clients around the globe 70 $2.8 billion

in commitments to the global sugar industry

4

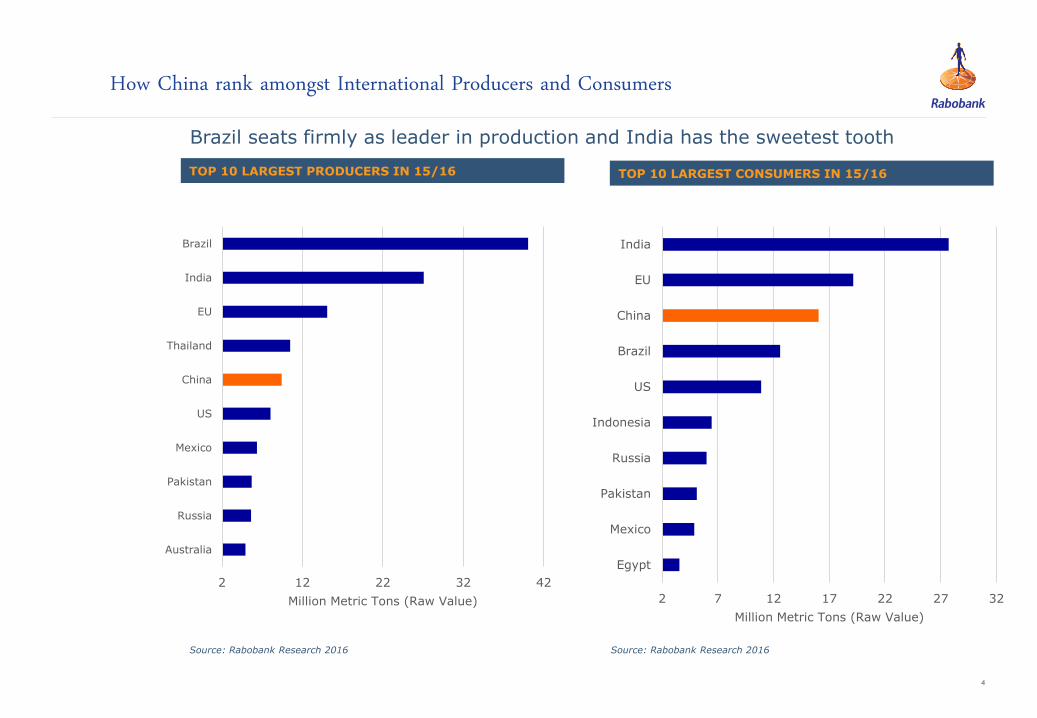

Brazil seats firmly as leader in production and India has the sweetest tooth

Source: Rabobank Research 2016

TOP 10 LARGEST PRODUCERS IN 15/16 TOP 10 LARGEST CONSUMERS IN 15/16

How China rank amongst International Producers and Consumers

Source: Rabobank Research 2016

2 12 22 32 42

Australia

Russia

Pakistan

Mexico

US

China

Thailand

EU

India

Brazil

Million Metric Tons (Raw Value) 2 7 12 17 22 27 32

Egypt

Mexico

Pakistan

Russia

Indonesia

US

Brazil

China

EU

India

Million Metric Tons (Raw Value)

5

China per-capita-consumption vs the region

Source: Chinese National Bureau of Statitiscs, Rabobank

Reseach World Bank/IMF/China Bureau of Statistics

Prospects of consumption sweetens

0

10

20

30

40

50

60

70

Kg-P

er-

Capita

2014/15 2015/16 (f) World Ave Asia Ave

5

10

15

20

25

30

35

1.26

1.28

1.3

1.32

1.34

1.36

1.38

1.4

1.42

Thousands

Billions

Total Population (LHS)

Disposable Income per capita (RMB) (RHS)

6

China’s sugar consumption still to grow by 2% in the next few years

Source: China Sugar Association, Rabobank Estimates 2016

5

7

9

11

13

15

17

19

21

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16(f)

2016/17(f)

2020/21(f)

Million m

t (r

aw

valu

e)

7

China’s sugar balance sheet – a deficit structure

Source: China Sugar Association, Rabobank estimates

0

1

1

2

2

3

3

4

4

5

5

2

4

6

8

10

12

14

16

18

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17(F)

Raw

Valu

e M

illion M

T

Raw

Valu

e M

illion M

T

Production Consumption Imports (RHS)

8

Henan Gansu

Heilongjiang

Jilin

Liaoning

Hebei

Shandong

Fujian

Jiangxi

Hubei

Hunan

Guangdong Guangxi

Shanxi

Hainan

Inner Mongolia

Shaanxi

Ningxia Qinghai

Guizhou

Yunnan

Tibet

Xinjiang

Jiangsu

Tianjin

Beijing

Taiwan

Anhui

Zhejiang

Shanghai

Sichuan Chongqing

Production 10000-50000

Production>50000

Production 1000-10000

Production 500-1000

Production <500

Unit: Thousand Metric Tonnes of cane

China’s Main Cane Growing Area

Source: China Statistics Yearbook 2014

9

Henan Gansu

Heilongjiang

Jilin

Liaoning

Hebei

Shandong

Fujian

Jiangxi

Hubei

Hunan

Guangdong Guangxi

Shanxi

Inner Mongolia

Shaanxi

Ningxia Qinghai

Guizhou

Yunnan

Tibet

Xinjiang

Jiangsu

Tianjin

Taiwan

Anhui

Zhejiang

Shanghai

Sichuan Chongqing

Hainan

1500<Production

Production>5000

500<Production

50<Production

10 <Production

Unit: Thousand Metric Tons beet

China’s Main Beet Growing Areas

Source: China Statistics Yearbook

10

• Growth in planted acreage erratic, farmers switched to competing crops especially eucalyptus, which grows faster

and generate more income.

• Planted area plummeted after 2014/15 season, when the Chinese Government removed the state reserves

purchase program in 2013/14, removing one of the largest domestic offtaker.

• Agricultural investments growth slowed down in the recent years while rural farm-hands declined as urbanization

rate increases.

Issues that the Chinese sugar industry is facing…

Source: China National Bureau of Statistics, China Sugar Association

0.0

10.0

20.0

30.0

40.0

50.0

60.0

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Agricultural Machinery Chemical Fertilizer Usage

Urban Population % (RHS)

Growth % declining

-20%

-15%

-10%

-5%

0%

5%

10%

800

1,000

1,200

1,400

1,600

1,800

2,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Thousands h

ecta

res

Cane Planted Area Beet Planted Area

% Growth (RHS)

11

• Plenty of room for improvement in terms of yields. Modernization of farming technology, educating farmers on

better farming techniques and further research and development will no doubt help farmers achieve better yield.

Comparison of Sugar Crop Yields

Source: LMC, F.o.Licht, Chinese National Bureau of Statistics

Average Cane Yield Comparison (Tonnes/Ha) Average Beet Yield Comparison (Tonnes/Ha)

0

10

20

30

40

50

60

70

USA China Ukraine Russia

0

10

20

30

40

50

60

70

80

90

12

Chinese Domestic Prices vs Imported Prices

Source: Bloomberg, GMSN

100

300

500

700

900

1100

1300

#11 USD/MT Physical Spot (Ex-Guangxi) USD/MT

Removal of State Reserves Sugar Purchase program

13

Brazil is now the top exporter of sugar to China

Source: China Customs

Top Import Origins for China in 1999/2000 Top Import Origins for China in 2014/15

China Sugar Imports, where do they come from now?

Source: China Customs

Thailand Cuba Australia Brazil

Guatemala Costa Rica Others

Brazil Thailand Cuba Guatamela

Australia S.Korea Others

LIAONING

JILIN

HEILONGJIANG

SHANDONG XIAXI

GANSU

GUANGDONG GUANGXI

HUNAN JIANGXI

ANWEI

HENAN

HUBEI

SHANXI

HEBEI

GUIZHOU

SICHUAN

CHIFENG 800 / day

50,000-80,000

FUXIN 800 / day 50,000- 60,000

JINZHOU 700 / day 200,000 / yr

YINGKOU 1000 / day 250,000-300,000 / yr

YINGKOU 2,000 / day 500,000 / yr

DALIAN 5,000 / day 300,000 / yr

LELING 1,600 / day 500,000 / yr

RIZHAO 1,500 / day 2,400,000 / yr

HUAI’AN 500-600 / day 150,000 / yr

ZHANGZHOU 600 / day 100,000-150,000 / yr

ZHANGZHOU 1,200 / day 300,000 /yr

DONGGUAN 2,000-2,200 / day 120,000 / yr

ZHANJIANG 2,000 / day 200,000-300,000 / yr

FANGCHENGGANG

1,000 / day 200,000 / yr

CHONGZUO 1,000 / day

190,000 / yr

TANGSHAN 1,500 / day

500,000 / yr

CITY (Refineries) Production (MT) per day Production (MT) per year

Legend

Refineries in China

BEIJING

TIANJIN

Port of calls

concentrated in NE

China (~14,000/mt/day)

15

How does China handle its imports?

Import Quotas

Out-of-Quota

imports have

higher tariffs

Crop Tender for

State reserves

Increase cane

purchase price

Consolidate the

sugar industry

• China allocates 1.945 million tonnes (tel quell) of in quota licenses to its importers. These

imports are subjected to 15% tariff. China also imports 400,000 annually from Cuba, as per

WTO agreement.

• For importers not being issued with the quota licenses, they can still import but will be subjected at 50%

tax tariff, which in general erodes most the margins compared to in quota imports.

• At current high prices, out of quota imports makes no sense as domestic prices are not high enough to

offset the tariff of 50%. Higher duty tariffs might be used to discourage imports

• Previously, this effectively brought down domestic prices, which made out of quota imports unprofitable.

This is also to discourage smuggling, which is detrimental to the entire Chinese sugar industry.

• Cane purchase price for Guangxi region increased from RMB 400/ton to RMB440/ton, so as to encourage

farmers to plant more cane.

• The Chinese Government recently asked 28 sugar companies in the biggest producing region, Guangxi, to

merge into 6 major groups. This is to strengthen the sector and ensure farmers get paid. The plan is to

complete the consolidation by 2020

16

Going forward, China will still have to import

Source: Rabobank Estimates CSA

China Balance Sheet (RV) 13/14 14/15 15/16 (e) 16/17 (f)

Opening Stocks 4,651 6,980 7,102 4,317

Production 14,476 11,474 9,200 10,050

Consumption 16,150 16,000 16,050 16,600

Import 4,054 4,700 4,100 4,200

Export 51 52 35 40

Closing Stocks 6,980 7,102 4,317 1,927

(2,000)

(1,500)

(1,000)

(500)

0

500

1,000

1,500

2,000

2,500

3,000

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

0

250

500

750

1,000

US/M

T

S/D (RHS) China Sugar Price (LHS)

17

What’s Next? Chinese Companies has been acquiring overseas assets

Source: Various State Media reports

18

2016/17 Asia production estimates El Nino is having a severe impact on production…

• Major countries experience a drop in

their sugar production, from the last peak

in 2012/13

• Number 2 sugar producer India is

expected to see a fall in production for

16/17 season due to droughts, thus

swinging into a net importer status

• Constrained production in Thailand will

not be able to help reduce the deficit gap

• Suppressed domestic Chinese prices is

not encouraging more sugar production

• Lack of innovation and farm inputs

combined with bad weather have caused

Vietnam to see a severe decline in

production

• Indonesia drive of self sufficiency is

laudable, but is still a net importer in the

near and mid term.

Source: LMC, Rabobank, 2016

1

3

9

1

0

CHINA

2.

4 2.

3 2.

2

PHILIPPINES

1

1 1

0

1

0

THAILAND

3 2 2

INDONESIA

1

. 1

.

1

.

VIETNAM

2

9

2

7

2

3

INDIA

12/13

15/16

16/17 (f)

*in Million Metric Tonnes

19

0

5

10

15

20

25

30

-15

-10

-5

0

5

10

15

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16e 16/17f

Usc/

lb

Millio

n T

on

nes

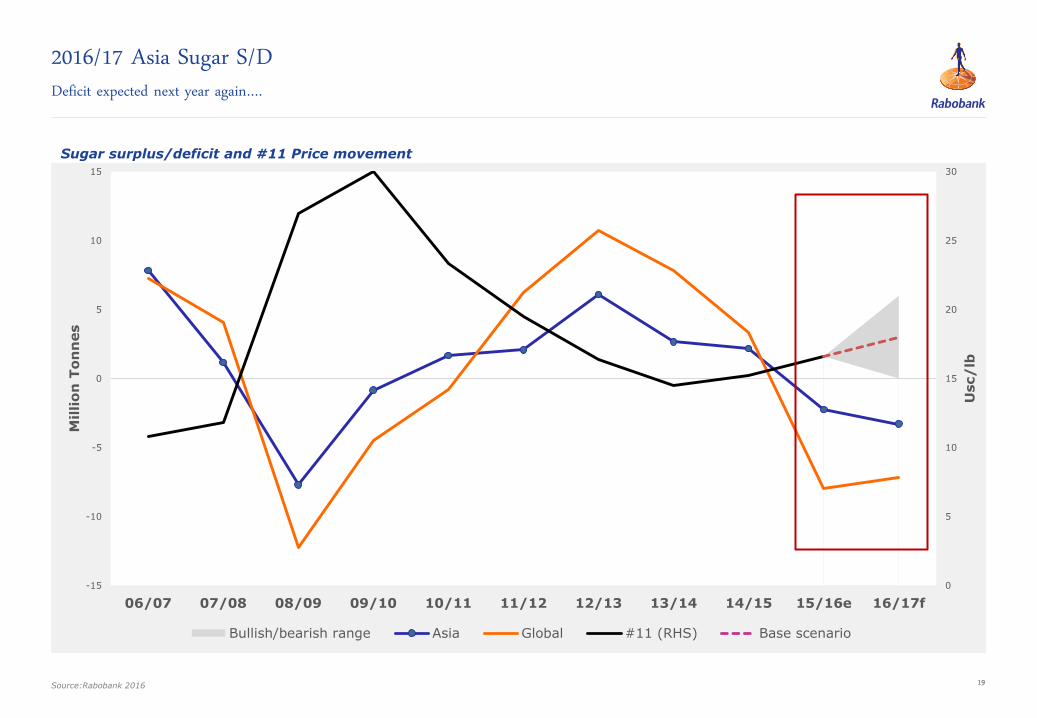

Bullish/bearish range Asia Global #11 (RHS) Base scenario

2016/17 Asia Sugar S/D Deficit expected next year again….

Source:Rabobank 2016

Sugar surplus/deficit and #11 Price movement

20

Thank You!

The information contained in this presentation is based on sources which Rabobank considers reliable and which are regularly updated. However, Rabobank

assumes no liability or guarantee for the accuracy, completeness and current validity of the information. Opinions or recommendations reflect the views of the

relevant author and do not necessarily represent the opinion of Rabobank or its associated companies. They may be amended at any time without prior notice.

The information should not be understood as an offer or recommendation for any and/or certain investment products. This applies even in the event of

individual issuers or securities being mentioned. Such information cannot serve as a substitute for objective advice based on the individual situation of the

investor. The information contained in this presentation must not be amended, reproduced or communicated to third parties in any way without the prior

express permission of Rabobank.

Rabobank Singapore

38 Beach Road, #31-11

South Beach Tower

Singapore 189767

Telephone: (65) 6536 3363

Rabobank International Kelvin Chow Senior Commodities Analyst Food & Agribusiness Research & Advisory

Telephone +65 6230 6748 E-mail [email protected]