The Changing Nature of Public Expenditure Work (1) · The Changing Nature of Public Expenditure...

21

The Changing Nature of Public Expenditure Work (1) Public Expenditure Analysis and Management Course, May 23, 2002 Anand Rajaram, PRMPS

Transcript of The Changing Nature of Public Expenditure Work (1) · The Changing Nature of Public Expenditure...

The Changing Nature of Public Expenditure Work (1)

Public Expenditure Analysis and Management Course, May 23, 2002

Anand Rajaram, PRMPS

Story Line• Last 2.5 days – various components of PE

work outlined• Our job is to bring it back together

• How do the components add up in reality?• What is the typical framework for such analysis?• How are new challenges being incorporated?• How can such work contribute to better

development impact?

• And to dovetail into next session on PRSP and specific Bank instruments

Logic of the two presentations

• My presentation will provide an overview on the field and some case illustrations of PERs from an economist’s perspective

• Yasuhiko’s presentation will present an institutional/political economy perspective to public expenditure issues

My Outline• Outline of evolutionary changes in PE

scope and content and process• A sample classification of recent PE work• Challenge of collaboration across PREM,

HD, FM• Fiduciary assessment• Poverty impact of public spending

• Illustrations from recent PER cases• Some guidelines/issues for better PE work

Early stages of PE evolutionFocus: Level and composition of Public Exp

Standard conclusions: High wage bill, inadequate O&M, high interest burden, too many projects

PE Analysis Fiscal Sustainability

AllocativeEfficiency

IncidenceAnalysis

Civil Service ReformRelated items

1995-2000 Focus on PEMFocus: Budget formulation, treasury systems, integrated financial

management systemsRecommendations: MTEF, IFMS, Treasury single accounts

PE Analysis

PE Management

Fiscal Sustainability

AllocativeEfficiency

IncidenceAnalysis

BudgetFormulation

Budget Execution

Civil Service ReformRelated items

PolicyPlans

New Elements Added: Fiscal Risk, Tracking Surveys

PE Analysis

PE Management

Fiscal Sustainability

AllocativeEfficiency

IncidenceAnalysis

BudgetFormulation

Budget Execution

Fiscal risk

PolicyProcess

(PRSP?)

Trackingsurveys

Civil Service ReformRelated items

PRSPs – Further Expansion of Expectations“PE for Poverty Reduction”

PE Analysis

PE Management

Fiscal Sustainability

AllocativeEfficiency

IncidenceAnalysis

Poverty Reduction

??Budget

FormulationBudget

Execution

Procurement

Fiscal risk

“Pro-poor PE”

Reporting & oversight

PovertyReduction

PolicyProcess

Trackingsurveys

ServiceDel.survey

Civil Service Reform DecentralizationRelated items

Coming Soon to a PER near you:Costing MDGs, Gender, Participatory Budgeting

Might we Break the Camel’s Back?

PE Analysis

PE Management

Fiscal Sustainability

AllocativeEfficiency

IncidenceAnalysis

Poverty Reduction

??Budget

FormulationBudget

Execution

Procurement

Fiscal risk

“Pro-poor PE”

Reporting & oversight

PolicyProcess

(PRSP?)

Trackingsurveys

ServiceDel.survey

Civil Service Reform DecentralizationRelated items

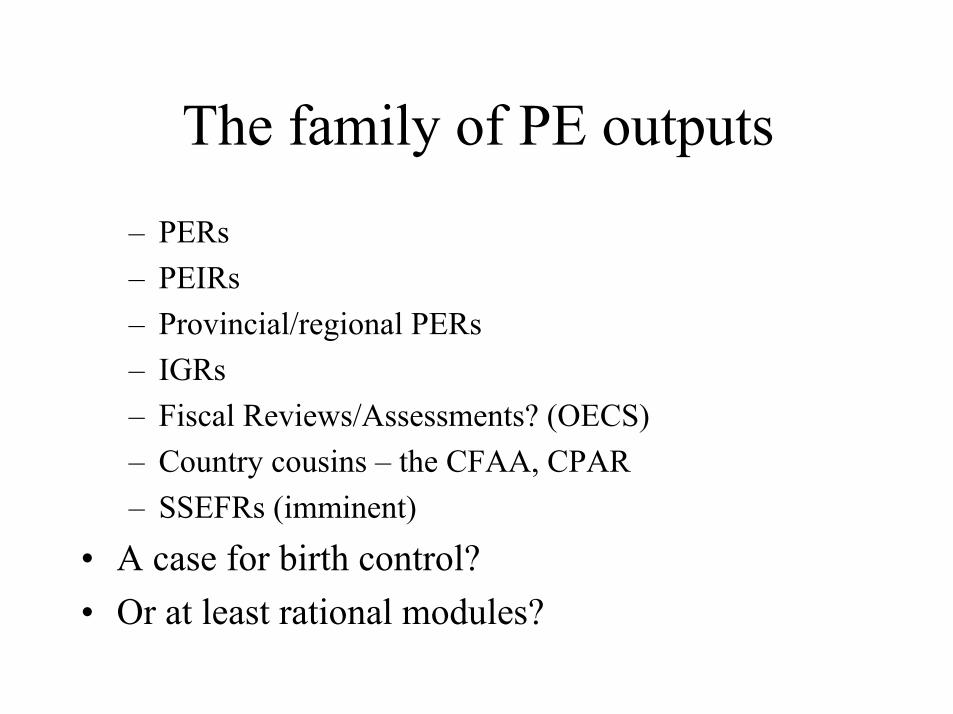

The family of PE outputs

– PERs– PEIRs– Provincial/regional PERs – IGRs– Fiscal Reviews/Assessments? (OECS)– Country cousins – the CFAA, CPAR– SSEFRs (imminent)

• A case for birth control? • Or at least rational modules?

VOLUME OF PE AND FINANCIAL ACCOUNTABILITY WORK, FY97-01

501247444057TOTAL313744SAR407533MNA10460917LAC1221111115ECA616352EAP1541428816AFR

PELEND.

IGRPERCPFACFAACPARRegion

The PE menu: Too Many Cooks/Recipes?

Public Expenditure Institutional Reviews (PEIR)

Expenditure Analysis Budget Formulation Budget Execution

Fiscal ROSC

Public Expenditure Tracking Surveys PETS

Country Procurement Assm’t Reviews (CPAR)

HIPC Expenditure Tracking Assessments

Social Sector Exp.& financel reviews (SSEFRs)

Governance Surveys (e.g., IGRs, Anti-Corruption, Public Officials, Household .)

Country Financial Accountability Assessments (CFAA)

Monitoring &Reporting

PEFA

How have PERs adapted to expectations?A typology of recent PERs

• PIR as a supplement to Customized BM report: Russia• The PEM: Mozambique (2001)• PE Reform support to MTEF: Albania (2001)• Bank supplement to Govt PER: Malawi, Tanzania, Zambia• PEIRs: Turkey, Macedonia, Croatia, Bosnia• Annual PERs with regional supplement – Ethiopia (2001) • PE Process annual report: Uganda• PERs w/Intergovt.Fiscal – Czech,Thailand, Kazakh,Bosnia• Provincial PERs – Punjab (Pakistan), Maharashtra (India)

Indonesia (ongoing), China

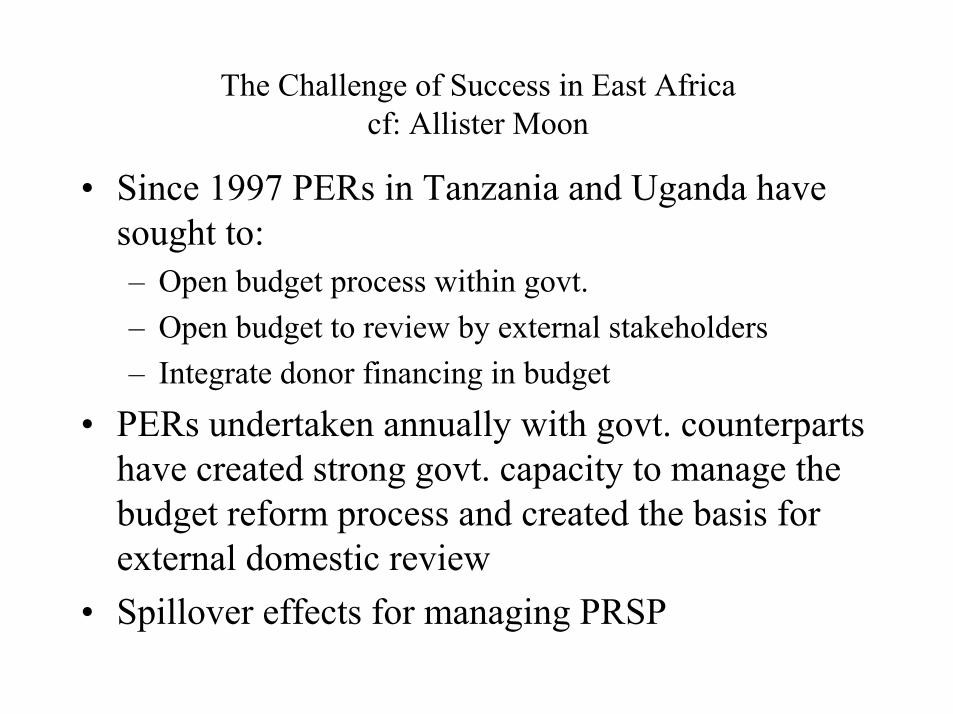

The Challenge of Success in East Africacf: Allister Moon

• Since 1997 PERs in Tanzania and Uganda have sought to:– Open budget process within govt.– Open budget to review by external stakeholders– Integrate donor financing in budget

• PERs undertaken annually with govt. counterparts have created strong govt. capacity to manage the budget reform process and created the basis for external domestic review

• Spillover effects for managing PRSP

East Africa success continued

• Strong and continuous support for this process from staff in resident missions and domestic consultants was key factor

• PER support in two phases in annual budget cycle:– Tech support to budget strategy formulation by

executive– To play a coordinating role in enabling external

review of budget by legislature and NGOs

East Africa continued

• Context and budget achievements:– Fiscal stability maintained– Improved input (commitment) control– Focus on outputs emerging– Citizen feedback on budget

• Challenges:– Too many processes: PRSP and budget process– Earmarking for PAF: “pro-poor”– Managing expectations– Role of legislature– “Death by participation”

Does success mean that the PER as a Bank report will wither away?

• PER is important as an annual process of helping government strengthen its system.

• In Uganda, the PER report is an annual record of key features of development of the budget process.

• Under old QAG rules, this would suffer in the evaluation process.

Turkey: Solving the Common Property Resource Management Problem

• Coalition politics, high turnover• Traditional budgeting but fragmented

institutions and non-comprehensive budget• Implicit and explicit contingent liabilities• PEIR as “process” to address collective

action problems – Bank as honest broker• Process was key to successful agreement on

reform strategy

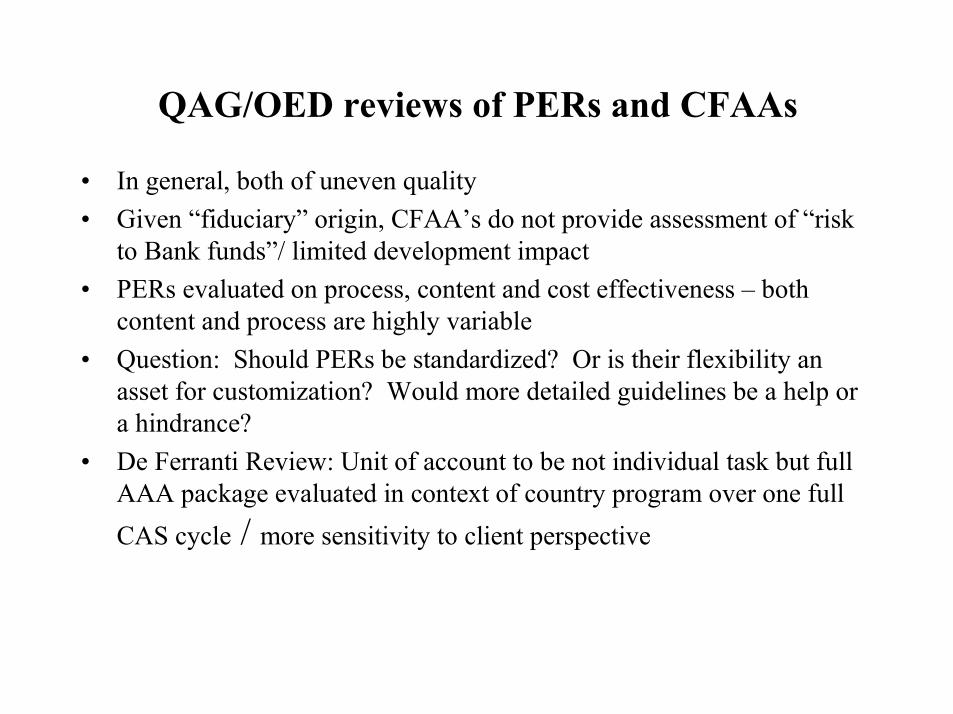

QAG/OED reviews of PERs and CFAAs

• In general, both of uneven quality• Given “fiduciary” origin, CFAA’s do not provide assessment of “risk

to Bank funds”/ limited development impact• PERs evaluated on process, content and cost effectiveness – both

content and process are highly variable• Question: Should PERs be standardized? Or is their flexibility an

asset for customization? Would more detailed guidelines be a help or a hindrance?

• De Ferranti Review: Unit of account to be not individual task but full AAA package evaluated in context of country program over one full CAS cycle / more sensitivity to client perspective

Problems needing attention:

• Most PE work not based on multi-year PE strategy in CAS – hampers systematic progress – de Ferranti report recommend.would help

• Unit of PE analysis must be general govt.-• To provide full coverage of govt activities• To highlight intergovt fiscal issues• To pave way for provincial/local govt PERs• To enable focus on service delivery issues

• Inadequate coordination of different diagnostic instruments – PER, CFAA, CPAR and Fiscal ROSC – the whole is less than the sum

• of parts • After diagnostic work, design of PE reform requires appropriate

sequencing – area of weakness• Tendency to recommend “package” technical fixes – MTEF, IFMS,

independent procurement boards etc. reflects this weakness • Any PEM reform initiated requires close attention and technical

support to govt.– not always within skill set of staff

Improving PE impact on poverty

• Incidence analysis is not systematically undertaken – it is key link to outcomes for the poor

• Tracking surveys should be used more widely• Use of crude proxies for pro-poor PE is widespread but not

analytically justified• Social sectors have initiated work and can deepen this

analysis on incidence and longer run impact• Other sectors (water, infrastructure) need to develop this

budgetary focus