The Changing Market for Doctors - What You Should Know in 10 Minutes Mansfield Advisors PPt

21

This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organisation without prior written approval from Candesic. Mansfield Advisors The Changing Market for Doctors – What You Should Know in 10 mins! Dr Victor Chua 27 February 2013

Transcript of The Changing Market for Doctors - What You Should Know in 10 Minutes Mansfield Advisors PPt

This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organisation without prior written approval from Candesic.

Mansfield

Advisors

The Changing Market for Doctors –What You Should Know in 10 mins!

Dr Victor Chua

27 February 2013

SUMMARY

• Why you should pay attention: Career planning matters!• Making lateral transitions in medicine is more difficult than in other professions• Case study: cardiothoracic surgery

• Economics are not on your side• Medical school admissions have doubled• The number of consultants has also almost doubled• …during a period of big increases in NHS spending• But the years of expansion are over, and NHS spending is likely to be flat for many years

• A shift in the nature of medicine• Greater workload in managing long term conditions such as diabetes, heart disease, pulmonary disease• The surgical specialities over-recruited in the past, leading to fewer NTN’s going forward• While the demand for most types of surgery has increased due to an ageing and longer-living population, some

types of surgery have been replaced by newer surgical techniques or medical therapy• Varicose veins• Benign prostatic hyperplasia by transurethal resection (TURP)• Gallstones

• General practice as a career• Drivers for growth in general practice• Demand for general practice• General practitioners as small businessmen• Partnership model in general practice

• Careers for doctors outside medicine

Making lateral transitions in medicine is more difficult than in other professions

Source: Candesic Analysis

MEDICINE AND LAW CAREER PATHS

Medical School 6 years

F1/F22

years

Speciality Training3 – 8 years

Fellowships, MD, PhD

1 – 3 yearsConsultant

Law School3 years

Associate / Senior Associate6 – 8 Years

Partner Senior Partner

Medicine

City Law (Solicitor)

LPC 1 year

Training Contract 2 years

• Seniority generally retained if changing speciality

• Due to specific knowledge, need to restart in order to change speciality

• Compared to other professions, lateral changes are are more challenging in medicine:

• A higher level of specific knowledge is required in order to move specialities, meaning seniority is not retained during transition

• The need to do unpaid fellowships in competitive specialities limits accessibility for doctors without family wealth

• Choosing a growing area is therefore more important for medical career progression than in other professions

3

In the mid 2000’s, percutaneous coronary interventions (PCI) by interventional cardiologists started to replace the need for coronary artery bypass grafts (CABG), resulting in a fall in the demand for cardiothoracic surgeons in the mid 2000’s

PCI: Percutaneous coronary intervention, done by invasive cardiologists or radiologists in an angiography suite through a small incisionCABG: Coronary artery bypass graft, done by a cardiothoracic surgeon in a laminar flow theatre, “Open heart surgery”

Source: Hospital Episode Statistics: K40.1- K49.9; K75.1 - K76.1; PTCA.org “History of angioplasty”; Candesic interviews

TREATMENT FOR CORONARY ARTERY DISEASE, ENGLAND, VOL UMES

• In the mid 2000’s, many cardiac surgeons finishing their registrar training were unable to find consulting posts at the end of their long training.

• The first angioplasty was done by Gruntszig in 1977. PCI (with stenting) started to replace CABG in the USA in the mid to late 1990s. The trend became pronounced in the UK about seven years later. As a profession, cardiothoracic surgeons were uninterested in training to perform PCI, opening up the field to interventional cardiologists

• The surplus of cardiothoracic surgeons was entirely foreseeable. But no action was taken to avert it

PCI has increased whilst CABG has decreased‘000s

“In all honesty, we (the cardiac surgeons) missed the boat when Andreas Gruntzig came to this country and the surgeons paid little heed to his catheter work.”Atiq Rehman, M.D., FACS

Performed by interventional cardiologists

Performed by cardiothoracic surgeons

The fall in the demand for CABG’s can be seen in the number of cardiac surgeons employed in the NHS in the mid 2000’s

Source: Centre for Workforce Intelligence, 2011

CARDIOTHORACIC SURGEONS BY GRADE

• In 2003-2005, the number of speciality trainees grew by over 20%, as fully trained surgeons were unable to secure a consultant post. Some hung on and eventually secured a post; others retrained in other specialities

• By 2011, the number of consultants leaving the profession due to retirement started to match the supply of qualifying trainees. The Centre for Workforce Intelligence projects a declining number of cardiothoracic surgeons due to retirement

• These numbers include both predominantly cardiac and predominantly thoracic surgeons, plus paediatric and transplant surgeons

SUMMARY

• Why you should pay attention: Career planning matters!• Making lateral transitions in medicine is more difficult than in other professions• Case study: cardiothoracic surgery

• Economics are not on your side• Medical school admissions have doubled• The number of consultants has also almost doubled• …during a period of big increases in NHS spending• But the years of expansion are over, and NHS spending is likely to be flat for many years

• A shift in the nature of medicine• Greater workload in managing long term conditions such as diabetes, heart disease, pulmonary disease• The surgical specialities over-recruited in the past, leading to fewer NTN’s going forward• While the demand for most types of surgery has increased due to an ageing and longer-living population, some

types of surgery have been replaced by newer surgical techniques or medical therapy• Varicose veins• Benign prostatic hyperplasia by transurethal resection (TURP)• Gallstones

• General practice as a career• Drivers for growth in general practice• Demand for general practice• General practitioners as small businessmen• Partnership model in general practice

• Careers for doctors outside medicine

Medical school admissions have doubled since 1990, despite the population remaining constant. Much of the increase is female

Source: Webster & Spavin: ‘Who are the doctors of tomorrow and what will they do?’; ONS – 1971 to 2010 population estimates

MEDICAL SCHOOL ADMISSIONSUK Medical School Intake, Population of England (m) 1971-2004

6

• Since the mid 90s, there has been an huge growth in the UK medical school intake, which is only now levelling off at around 8,000 admissions per year

• The demographic of the intake has also shifted; females now account for around 60% medical school admissions, compared to below 50% in 1990, and just 25% in 1960

• The rate of increase in medical admissions has far outstripped the rate of population growth, and will therefore increase the number of doctors per-capita

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

50m

40m

30m

20m

10m

0

Population of England (m)

Female admissions to medical schoolMale admissions to medical school

The number of consultants has gone up by 60% in ten years

Source: NHS IC – NHS Staff 2001 – 2011 Overview

GROWTH IN THE MEDICAL WORKFORCENumber of staff (Full Time Equivalents)

7

92,910

102,344

114,470121,264

132,683134,713

Consultants

GP Providers (Partners)

GP Registrars,Retainers and Others

Doctors in Training

Other medicalworkers

• Since 2001, the medical workforce has grown at a rate of 3.8% year on year

• The rise in number of consultants has outstripped the rate of growth of the workforce, showing 4.8% year on year increases. This is due to:

• Increases in the number of training positions, as a part of planned NHS expansion

• Consultants working into later age

CAGR3.8%

8

But the years of NHS expansion are over, and NHS spending is likely to be flat for many years

Source: ‘Comprehensive Spending Review 2010’ HM Treasury; Candesic analysis

SPENDING REVIEW 2010 – HEALTH FORECAST EXPENDITURE£bn

CAGR

2.7%

• The 2010 Spending Review set out HM Treasury plans on health spending for this Parliament

• In the last two years, the Coalition government has stuck to the plan. There has been an increase in spending in cash terms of about 2-3% pa. This is obviously far below the 6-10% annual growth NHS England had become accustomed to up to 2010.

• Once the impact of social care funding within the NHS settlement is taken out, though, the growth is smaller

• For practical purposes, we are assuming a flat NHS budget for the next five years

109.8106.9

104.0

101.5

98.7

Social care funding within the NHS settlement

SUMMARY

• Why you should pay attention: Career planning matters!• Making lateral transitions in medicine is more difficult than in other professions• Case study: cardiothoracic surgery

• Economics are not on your side• Medical school admissions have doubled• The number of consultants has also almost doubled• …during a period of big increases in NHS spending• But the years of expansion are over, and NHS spending is likely to be flat for many years

• A shift in the nature of medicine• Greater workload in managing long term conditions such as diabetes, heart disease, pulmonary disease• The surgical specialities over-recruited in the past, leading to fewer NTN’s going forward• While the demand for most types of surgery has increased due to an ageing and longer-living population, some

types of surgery have been replaced by newer surgical techniques or medical therapy• Varicose veins• Benign prostatic hyperplasia by transurethal resection (TURP)• Gallstones

• General practice as a career• Drivers for growth in general practice• Demand for general practice• General practitioners as small businessmen• Partnership model in general practice

• Careers for doctors outside medicine

Surgical specialities over-recruited in the past, leading to fewer NTN’s going forward. The CfWI, which has analysed the workforce, did not specifically look at the impact of technological change. Hence the demand shift away from surgery towardsmedicine and general practice is likely to be more marked

Source: Centre for Workforce Intelligence – Shape of the Medical Workforce: Informing Speciality Training Numbers (2011)

EMERGING AND DECLINING SPECIALITIES

10

General Practice

Dermatology

Cardiothoracic surgery

Anaesthetics

Neurosurgery

Gastroenterology

Respiratory Medicine

Obstetrics and GynaecologyTrauma and Orthopaedic Surgery

General Surgery

Paediatric Surgery

Otolaryngology

Renal Medicine

* National Training Numbers

• Increase required to support shift from secondary to primary care

• Incorrect expectation GPs with special interests would take work from dermatologists.

• Strong growth in medium term expected to exceed demand. Numbers linked to surgical demand

• Current neurosurgical workforce is young and does not need imminent replacement

• Current growth of consultant positions (6.9%) not expected to continue. Preventing oversupply risk

• Supply expected to meet demand by 2018, though conflicting data mitigate robust analysis

• Reduction recommended to correct impending ‘bulge’ on qualified consultants in 2014

• Oversupply predicted in near future, as rate of growth has outstripped population growth

• Oversupply predicted. Areas (e.g. breast) growing, others (e.g. vascular) only maintaining intake

• While there is a current shortage of consultant paediatric surgeons, there are currently too many in training

• No information available

• Oversupply already exists: many newly qualified consultants are waiting over 2 years for positions

• After glut of trainees seeking consultant jobs in mid 2000’s, retirements match qualifying trainees

2,800

42

370

17

95

124

200

146

158

13

45

57

12

NTNs*(2011)

3,250

48

354

16

89

114

160

116

123

10

33

32

12

NTNs*(2014)

-43.9%

Over the past decade, the treatment of varicose veins by general surgeons has given way to injection scleropathy and endovenous transluminal procedures

Source: Hospital Episode Statistics – Main Procedures and Interventions (3 Character) 2000/01 – 2010/11

TREATMENT FOR VARICOSE VEINSNumber of finished consultant episodes, 2000 - 2010

11

Total number of treatments

Conventional Surgery

Injection Scleropathy

Transluminal Procedures

• Varicose veins are a common medical problem, and a frequent cause for referral and treatment within the NHS. They are one of the most commonly performed operations by general surgeons in the UK

• Several treatment options exist, with a range of minimally invasive techniques increasingly available

• Over the past decade, there has been a sharp decline in traditional surgical techniques in favour of injection scleropathy and endovenoustransluminal procedures

• Proponents of minimally invasive procedures cite advantages including reduced post-operative complications, faster recovery, and improved quality of life

• Injection scleropathy can be performed by a nurse, and therefore reduces the requirement for general surgeons

In the 1990s, transurethral resection of the prostate was the gold standard of treatment for prostatic hyperplasia. Medical treatment, however, has greatly diminished the demand for TURPs

Source: Long et al, Impact of pharmacotherapy on the incidence of TURP for BPH, Irish Medical Journal (2012)

TREATMENT OF BENIGN PROSTATIC HYPERPLASIA, IRELAND, 1995-2008

12

• In this retrospective study over a 14 year period, national figures for transurethalresections of the prostate (TURPs) were obtained from public funding bodies. (The figures do not include privately funded procedures).

• There is a strong, significant correlation between the 50% drop in TURPs between 1995 and 2005 and the increased use of medical therapies for benign prostatic hypertrophy (BPH)

• As TURPs are for a trainee a “gateway” to more difficult endoscopic procedures such as bladder resections, the reduction in training opportunities causes concern to the authors

It is plausible that medical advances will reduce the requirement for cholecystectomies, one of the most commonly performed operations be general surgeons. Preventative and litholytic drugs could radically alter the treatment pathway for gallstones.

Source: World Journal of Gastrointestinal Pharmacology and Therapeutics: Therapy of gallstone disease: What it was, what it is, what it will be

TREATMENT PATHWAYS FOR GALLSTONES

13

Symptomatic patient with gallstones

Consider medical and

surgical options

ComplicatedNon complicated

LaproscopicCholecystectomy

Expectant management Oral Litholysis Novel

treatments

Elective

• Cholecystectomies are one of the most commonly performed operations in the UK, with almost 64,000 performed in 2010/11 in England. They are considered the gold standard treatment of symptomatic gallstones.

• Gall-stones composed predominantly of cholesterol which are calcium free may be ‘dissolved’ by litholysis with UDCA* or TUDCA**. However, only a minority of patients (<10%) are amenable to oral dissolution therapy

• Novel treatments for gallstones include statins, and agonists and antagonists of nuclear receptors involved in biliary lipid secretion. It is possible that further development in medical therapy will further reduce the need for cholecystectomies

* Ursodeoxycholic acid** Tauroursodeoxycholic acid

SUMMARY

• Why you should pay attention: Career planning matters!• Making lateral transitions in medicine is more difficult than in other professions• Case study: cardiothoracic surgery

• Economics are not on your side• Medical school admissions have doubled• The number of consultants has also almost doubled• …during a period of big increases in NHS spending• But the years of expansion are over, and NHS spending is likely to be flat for many years

• A shift in the nature of medicine• Greater workload in managing long term conditions such as diabetes, heart disease, pulmonary disease• The surgical specialities over-recruited in the past, leading to fewer NTN’s going forward• While the demand for most types of surgery has increased due to an ageing and longer-living population, some

types of surgery have been replaced by newer surgical techniques or medical therapy• Varicose veins• Benign prostatic hyperplasia by transurethal resection (TURP)• Gallstones

• General practice as a career• Drivers for growth in general practice• Demand for general practice• General practitioners as small businessmen• Partnership model in general practice

• Careers for doctors outside medicine

A number of demographic, political and sociological factors are driving the growth of general practice

Source: CfWI – General Practice Summary Sheet; ONS population projections (2010 estiamtes) - England

DRIVERS FOR GROWTH IN GENERAL PRACTICE

15

Agenda to move care into community

Increased commissioning role

Age of General Practice trainees

Ageing Population

Driver Comments

• The UK hosts an increasingly elderly population

• By 2020, the number of individuals over 80 will have increased by 25%, and will have doubled by 2035

• Over 80s have by far the highest number of consultations per patient per year. The increasing age of the population will drive demand for general practice services

• Government policy stipulates that care should be provided in a community rather than a hospital setting

• The 2010 government white paper ‘Equity and excellence –Liberating the NHS’ outlined plans for for commissioning of services to be carried out by GPs

• Individuals applying to train for general practice tend to be older than those applying for other medical or surgical specialities

• The Royal College of General Practitioners believes that most problems can be managed in primary care, with acute referral as needed

• Community care is comprehensive, manages cost, and frees up acute providers for serious and specialist work

• An increase in the amount of time spent by GPs commissioning services will reduce time spent with patients

• In order to maintain services, there will have to be an increase in the number of GPs

• GPs have often commenced or completed training in another speciality before training as a GP

• As a result, the working life of a GP will be shorter than for other specialities, necessitating a higher number of training places to maintain numbers

General practitioners hold privileged position as independent operators within a highly regulated market which prevents entryby others. They currently are able to generate profits and keep surpluses, whilst having an NHS pension.

Source: Laing & Buisson Healthcare Market Review (2011-12)

SIMILARITIES BETWEEN GENERAL PRACTICE AND PRIVATE E NTERPRISE

16

Similarities to private sector

GPs are regarded as independent contractors . They compete for contracts, hire members of staff within their practice, and draw their salary from income provided by PCT contracts

GPs have a public sector pension entitlement. This is a significant barrier to entry to ‘non-NHS’ practices

The health and social care bill suggests that in future, contracts will be open to any willing provider of care

General medical services and personal medical services contracts are only open to GPs, as part of the ‘NHS-family’

It is illegal for GPs to sell the goodwill of their practice when they retire

Similarities to pubic sector

Contractual Elements

Market Elements GPs not allowed to exceed practice boundaries,

preventing growth of entrepreneurial GPsPatients will have “the right choose to register with any GP practice with an open list,” suggesting a relaxation of current rules

Market strictly regulated by PCTs, which have discretionary powers to pay or withold important revenue streams

It is possible that NHS commissioning boards will open the market more, reducing barriers to entry for private GPs

Changes suggested by Health and Social Care Act

• General Practitioners receive an NHS pension but are not salaried NHS employees. They are independently contracted by PCTs, and manage their own practice, essentially operating as private enterprises

• GPs businesses are protected as the market is highly regulated, deterring entry from ‘non-NHS family’ operators. The Health and Social Care Act will likely open the market more to private sector practitioners, though the extent that this will occur is still unclear

The number of non-Partner GPs have doubled in the last six years, as existing GP Partners have been reluctant to appoint new Partners

Source: NHS IC – NHS Staff 2001 – 2011 Overview

GROWTH IN THE MEDICAL WORKFORCENumber of staff (Full Time Equivalents)

17

92,910

102,344

114,470121,264

132,683134,713

Consultants

GP Providers (Partners)

GP Registrars,Retainers and Others

Doctors in Training

Other medicalworkers

• Since the 2005 GMS contract which allowed GP Partnerships to keep and distribute their year end surpluses, there has been a big rise in the number of non-Partner GPs

• On partner retirement, existing partners have been employing salaried GPs rather than sharing the fruits of Partnership with new GPs

• We believe that over time, GP Partnerships will come to resemble other professional services partnerships, with a “pyramid” structure

CAGR3.8%

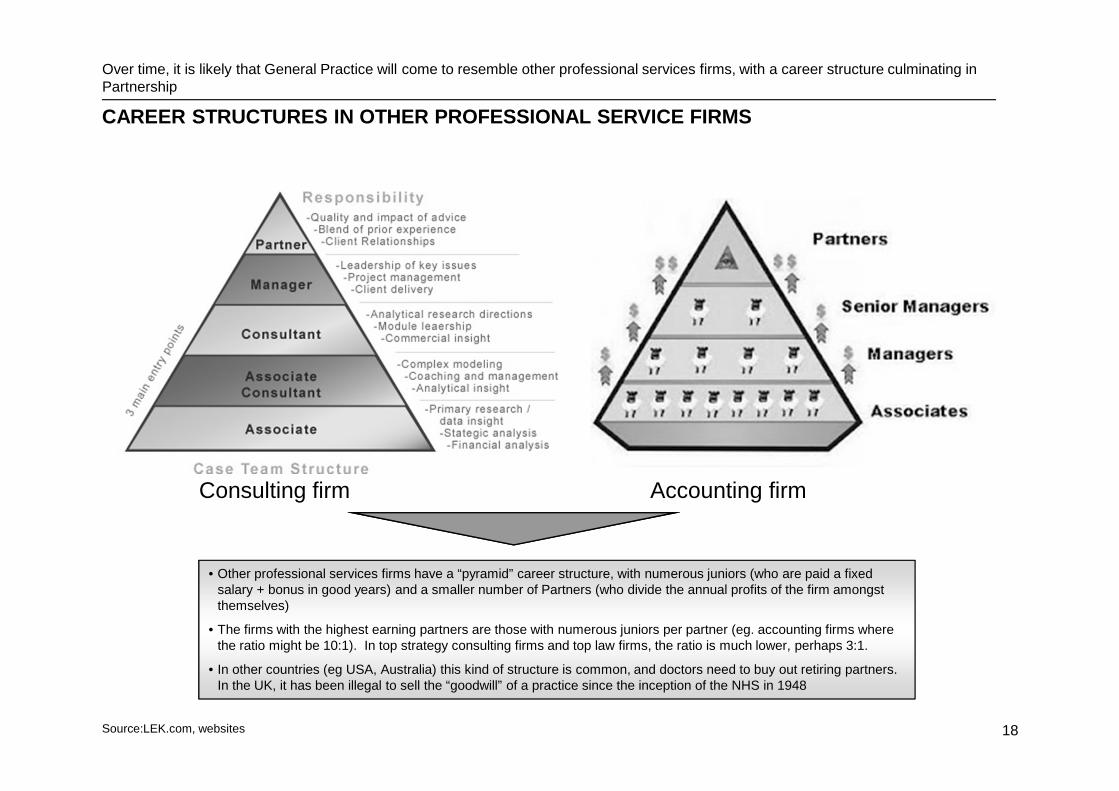

Over time, it is likely that General Practice will come to resemble other professional services firms, with a career structure culminating in Partnership

Source:LEK.com, websites

CAREER STRUCTURES IN OTHER PROFESSIONAL SERVICE FIR MS

18

Consulting firm Accounting firm

• Other professional services firms have a “pyramid” career structure, with numerous juniors (who are paid a fixed salary + bonus in good years) and a smaller number of Partners (who divide the annual profits of the firm amongst themselves)

• The firms with the highest earning partners are those with numerous juniors per partner (eg. accounting firms where the ratio might be 10:1). In top strategy consulting firms and top law firms, the ratio is much lower, perhaps 3:1.

• In other countries (eg USA, Australia) this kind of structure is common, and doctors need to buy out retiring partners. In the UK, it has been illegal to sell the “goodwill” of a practice since the inception of the NHS in 1948

SUMMARY

• Why you should pay attention: Career planning matters!• Making lateral transitions in medicine is more difficult than in other professions• Case study: cardiothoracic surgery

• Economics are not on your side• Medical school admissions have doubled• The number of consultants has also almost doubled• …during a period of big increases in NHS spending• But the years of expansion are over, and NHS spending is likely to be flat for many years

• A shift in the nature of medicine• Greater workload in managing long term conditions such as diabetes, heart disease, pulmonary disease• The surgical specialities over-recruited in the past, leading to fewer NTN’s going forward• While the demand for most types of surgery has increased due to an ageing and longer-living population, some

types of surgery have been replaced by newer surgical techniques or medical therapy• Varicose veins• Benign prostatic hyperplasia by transurethal resection (TURP)• Gallstones

• General practice as a career• Drivers for growth in general practice• Demand for general practice• General practitioners as small businessmen• Partnership model in general practice

• Careers for doctors outside medicine – not really the focus of this talk, come and see me later !

CONTACT

20

Dr Victor Chua MB BChirPartner

Mansfield Advisors LLPSt John's Building79 Marsham StreetLondon SW1P 4SB

UKMobile: +44 7768 003 821

See Twitter for occasional articles on UK healthcare:

https://twitter.com/VictorChuaUK

Dr Chua is willing to be contacted for careers advice / mentorship