The Chamber of Tax Consultants · PDF fileN.R. Company Germany India Company I.P. I.P....

85

The Chamber of Tax Consultants 13 th January, 2017 Naresh Ajwani Rashmin Sanghvi & Associates Chartered Accountants TDS on Non-resident payments - Capital Gains

-

Upload

trinhduong -

Category

Documents

-

view

214 -

download

2

Transcript of The Chamber of Tax Consultants · PDF fileN.R. Company Germany India Company I.P. I.P....

The Chamber of Tax Consultants

13th January, 2017

Naresh AjwaniRashmin Sanghvi & Associates

Chartered Accountants

TDS on Non-resident payments -Capital Gains

Topics covered

• A. TDS on Capital Gain

• B. Capital Gain under DTA

• C. India-Mauritius DTA Protocol

India-Singapore DTA Protocol

• D. Indirect Transfer

Slide No.: 1

A. TDS on Capital Gain

Slide No.: 2

Capital Gains

• Capital Gain taxation for residents and non-residents is same under the ITA – except for :

- Rate of tax for some transactions.

- FX fluctuation provision.

- FII / FPI income.

- Indirect transfer.

- Merger / demerger etc.

• DTA can have bearing on taxation.

Slide No.: 3

TDS on Capital gain

• Payer is required to deduct tax at source u/s. 195on payment of purchase price.

• TDS is on “sum chargeable to tax” – i.e. Capitalgain and not on sale price.

[Transmission Corp. 239 ITR 587 (SC).

GE India Technology Cen. Pvt. Ltd. – (193 Taxman234) 2010 SC.]

Slide No.: 4

Sums chargeable – Buying a flat

• Indian resident wants to purchase a flat from anNRI. Should he deduct tax at source from the fullsale consideration, or from the capital gain only?

• Syed Aslam Hashmi – 26 taxmann.com 6 (Bang.ITAT 2012)

R. Prakash – 38 taxmann.com 123 (Bang ITAT)2013

TDS should be on sale proceeds.

• Decisions have not considered SC decisions in GETechnologies and Transmission Corporation incorrect perspective. Slide No.: 5

Sum chargeable to tax

• Circulars clarifying CBDT understanding:

- CBDT circular no. 02/2014 dated 26.2.2014states that interest u/s. 201 will be on portionrepresenting income (not the whole amount).

- CBDT circular no. 03/2015 dated 12.2.2015states that disallowance u/s. 40(a)(i) will be onsums chargeable to tax (not the whole amount).

Slide No.: 6

ITA provisions for non-residents

• FX fluctuation provision for shares and debenturespurchased in foreign currency – S. 48, 1st proviso.

• Rate of tax on Long Term Capital Gain on unlistedsecurities or shares of closely held company - 10%without considering FX fluctuation and inflationadjustment – S. 112(1)(c)(iii).

• Long Term Capital Gain of NRI – tax rate of 10% -Chapter XII-A. (FX fluctuation relief available.)

• Special provisions for FPI, ADR/GDR , etc. – Ss.115AB, 115AC, 115AD.

Slide No.: 7

B. Capital Gain under DTA

Slide No.: 8

9

• “Capital Gains” has not been defined in the DTA.Meaning will be derived from the country’sdomestic law. [Article 3 (2)].

ITA – “Capital Gains” not defined. Meaning ishowever well understood.

• DTA uses the term “Alienation”. DTA refers tovarious types of “assets”. ITA defines “Transfer”and “Capital Asset”.

• Rights of taxing capital gains are on similar lines asthe income from the assets.

DTA

10

DTA

• The article applies to gains earned by resident ofone country, from sale of property situated inanother country.

• For gains on some assets, Country of Residence(COR) is given sole right to tax. For gains onsome other assets, Country of Source (COS) alsohas the right to tax.

11

• DTA does not consider the following:

- Difference between Capital Gains & BusinessIncome.

- Difference between Long Term & Short CapitalGain.

- Difference between Capital Gains & speculationgains.

• Domestic law applies for the manner of taxation.

DTA

12

Source Rules - DTA

• There are no source rules prescribed specifically forcapital gains.

Situs of asset may not be the source.

Domestic rules will apply normally.

13

Transfer/Alienation - DTA

• Alienation includes several kinds of transactions:

- Exchange of property.

- Partial alienation.

- Expropriation.

- Gift.

- Passing of property on death.

• Annuities – may be considered as capital gains ornormal income.

14

Appreciation of Asset - DTA

• Some countries levy tax on emigration (Thedifference between market value on the date ofemigration & cost is considered as gains).

DTA permits treatment of appreciation as capitalgains.

• Practical difficulties:

Emigration in Year 1; & actual sale after severalyears.

Will COR give credit for tax in COS?

What should be the cost of asset – actual cost orvalue as on emigration date?

15

Some ITA provisions

• S.45(1A) – Amount received from an insurer onaccount of damage to the capital asset due to flood,etc. – This may not be covered under a DTA.

• S.50C – sale consideration for immovable propertywill be considered atleast equal to the stamp dutyvalue.

• S.50D – If consideration cannot be determined, thenfair market value will be the consideration.

• Personal effects.

16

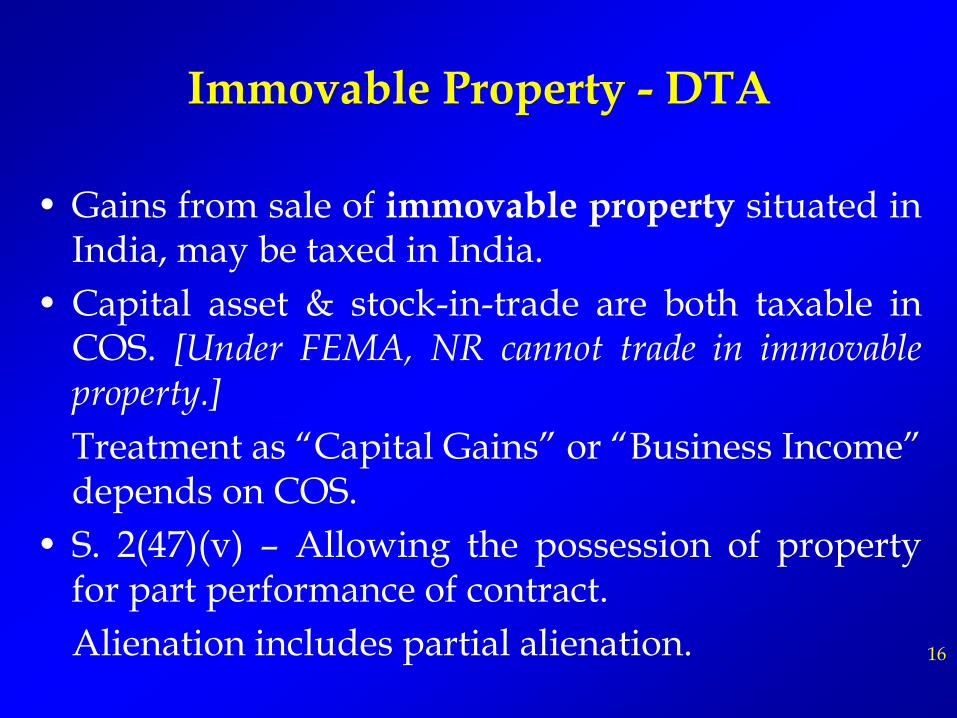

Immovable Property - DTA

• Gains from sale of immovable property situated inIndia, may be taxed in India.

• Capital asset & stock-in-trade are both taxable inCOS. [Under FEMA, NR cannot trade in immovableproperty.]

Treatment as “Capital Gains” or “Business Income”depends on COS.

• S. 2(47)(v) – Allowing the possession of propertyfor part performance of contract.

Alienation includes partial alienation.

17

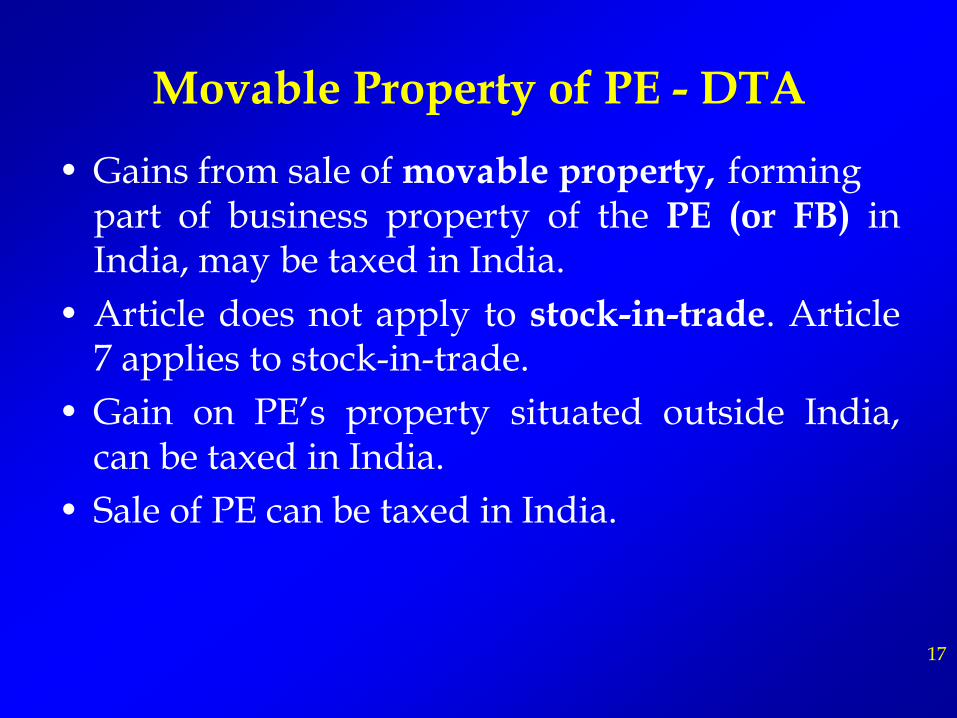

• Gains from sale of movable property, formingpart of business property of the PE (or FB) inIndia, may be taxed in India.

• Article does not apply to stock-in-trade. Article7 applies to stock-in-trade.

• Gain on PE’s property situated outside India,can be taxed in India.

• Sale of PE can be taxed in India.

Movable Property of PE - DTA

18

Movable Property of PE - DTA

• If PE is for exempt activities [Article 5(4)], thegain of sale of such PE’s property is not taxablein India.

• If property does not form a part of PE, thenother clauses will apply – normally residuaryarticle i.e. in some DTAs, only COR can tax thegain.

19

India

• Immovable property in third country is not taxablein COS.

Immovable Property of PE - DTA

Ownership officein Singapore

GermanResident

PE

20

• Gains from sale of:

- ship or aircraft which is operated inInternational traffic,

- boats engaged in inland waterways transport,and

- movable property pertaining to operation ofsuch ships, aircrafts or boats,

are taxable only where the place of effectivemanagement is situated.

Ships and Aircrafts - DTA

21

Ships & Aircrafts - DTA

• As this is a special clause, it takes precedence overarticle 13(2).

• Movable property pertaining to operation of ships& aircrafts can be taxed ONLY in the COR.

Immovable property pertaining to ships &aircrafts will be taxed under article 13(1) – i.e. COS.

22

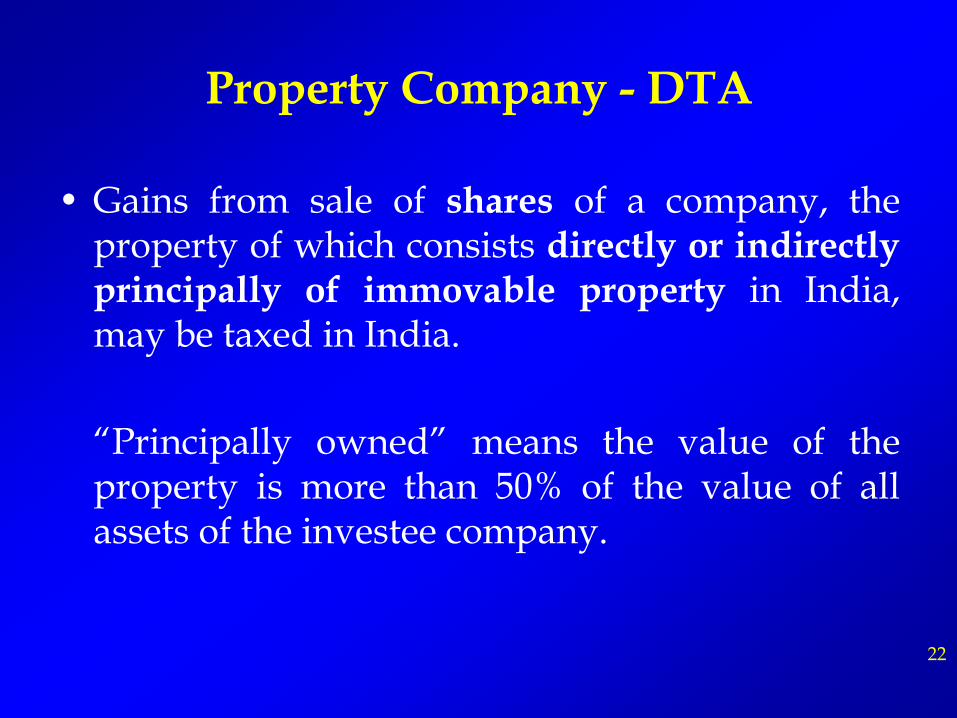

• Gains from sale of shares of a company, theproperty of which consists directly or indirectlyprincipally of immovable property in India,may be taxed in India.

“Principally owned” means the value of theproperty is more than 50% of the value of allassets of the investee company.

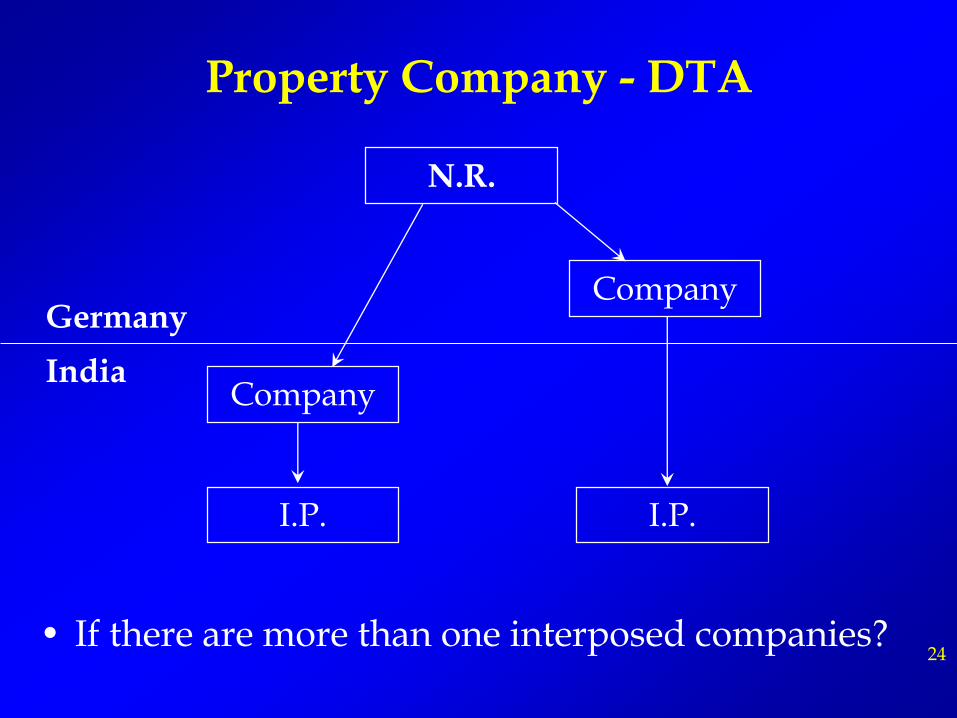

Property Company - DTA

23

Property Company - DTA

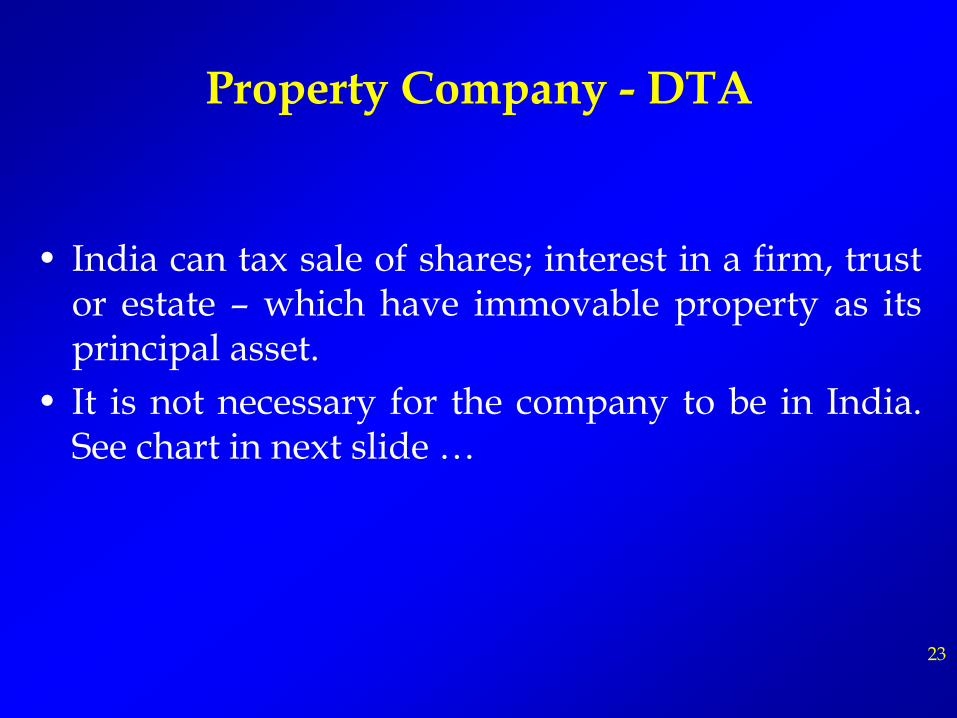

• India can tax sale of shares; interest in a firm, trustor estate – which have immovable property as itsprincipal asset.

• It is not necessary for the company to be in India.See chart in next slide …

24

Property Company - DTA

N.R.

CompanyGermany

IndiaCompany

I.P.I.P.

• If there are more than one interposed companies?

25

Property Company - DTA

• When should the value of immovable property beconsidered?

- Date of sale of shares.

- Date of purchase of property.

- Date of last audited balance sheet.

• If due to losses, the value of property is more than50%, will it be considered as Property Company?

• Are debts to be considered – is it net value or grossvalue?

26

Substantial shareholding - DTA

• UN Model 2011:

If the person held,

directly or indirectly at any time during the 12month period preceding the alienation,

a specified percentage of the investee company inIndia,

gains on sale of shares [other than thosementioned in article 13(4)],

may be taxed in India.

27

Substantial shareholding - DTA

• UN model 2001 and many DTAs:

A person holds 20% of the investee company. TheDTA prescribes shareholding of 10%. Will thearticle apply if the person sells shares:

- equal to 15% of the company’s shares?

- equal to 5% of the company’s shares?

- equal to 15% of the shares in Year 1, & 5% of theshares in Year 2?

- equal to 15% of the shares in Year 1, & 5% of theshares in Year 10?

28

• Gains of property other than those mentionedabove, is taxable only in COR.

• Gain on sale of following assets cannot be taxedin India:

- Shares of Indian companies.

- Units, Bonds, etc..

- Bullion.

- Work of Art.

- Sale of technical know-how.

- Sale of brands.

Other assets - DTA

C. India-Mauritius DTA Protocol

India-Singapore DTA Protocol

Slide No.: 29

Mauritius DTA protocol

• Protocol signed on 16th May 2016 introducing /amending following articles of DTA of 1982:

- Service PE (90 days in any 12 month period).

- Tax on interest reduced to 7.5% from fulltaxation.

Tax exemption to interest earned by banksgrandfathered for debt claims existing as on31.3.2017.

- FTS article introduced – tax upto 10%.

30

Mauritius DTA protocol

- Capital gain on shares acquired on or after1.4.2017 taxable in India.

50% tax relief for gains between 1.4.2017 and31.3.2019.

Tax exemption on shares grandfathered forshares acquired upto 31.3.2017.

- LOB clause introduced for Capital gain onshares.

- Other income – if source is in COS, COS can tax.

31

Mauritius DTA – Capital Gain and LOB

• Capital Gain on shares now taxable in India.

Only shares are covered. Other assets such asdebentures, LLP stake continue to be taxable inMu. only.

• Reliefs – Shares purchased upto 31.3.2017 – gaintaxable only in Mu. (Grandfathering).

• Gains earned between 1.4.2017 and 31.3.2019 –taxable @ 50% of normal tax.

LOB clause – for 50% relief only. (2 year life)

32

Mauritius DTA – Capital Gain and LOB

• If CCDs are acquired upto 31.3.2017, and these areconverted into shares on or after 1.4.2017 – will thegains on shares be taxable in India?

• If CCPS are acquired before 1.4.2017, and these areconverted into shares on or after 1.4.2017 – will thegains on shares be taxable in India?

33

Mauritius DTA – Capital Gain and LOB

• LOB - 50% relief not available under any of the 2tests:

i) Affairs are arranged with the primary purpose of taking advantage of the relief.

ii) Shell company – if expenditure is less than Mu.Rupees 15 lakhs or INR 27 lakhs in 12 monthsimmediately before the gain.

• Is it sufficient if Mu. Company incurs theminimum expenditure?

34

Mauritius DTA and GAAR

• LOB clause is only for shares. It has a life of 2 years. Then there is no LOB clause in the DTA.

• GAAR can apply from FY 2017-18.

Due to GAAR, the use of DTA is very limited.

35

Mauritius DTA - Implications

• Long Term Capital gain on listed shares – noimpact as it is exempt under ITA.

• Short Term Capital gain on listed shares – taxablein India.

• LTCG on unlisted shares – taxable in India.

• Gain on Securities (other than shares) – Not taxablein India.

• Interest on debt – tax only 7.5%.

36

Mauritius DTA – CBDT Panel

Issues under consideration:

• Merger - Shares in amalgamating companyacquired before 1.4.2017. Shares acquired inamalgamated company on or after 1.4.2017.

• Same issue for demerger.

• Bonus shares acquired after 1.4.2017.

• Partly paid shares acquired before 1.4.2017. Balancecall money paid on or after 1.4.2017.

• Conversion of ADR / GDR into shares.37

Singapore DTA Protocol

• 3rd Protocol signed on 30th December 2016introducing / amending following articles of DTAof 1994:

- Corresponding adjustment for Transfer Pricing.

- Capital gain on shares acquired on or after1.4.2017 taxable in India.

50% tax relief for gains between 1.4.2017 and31.3.2019.

Tax exemption on shares grandfathered forshares acquired upto 31.3.2017. Slide No.: 38

Singapore DTA Protocol

- LOB continued for Capital gain on shares.

- Domestic anti-abuse provisions can be applied– new article introduced.

-----------------

- Capital gain tax is in line with India-Mu. DTA.

- Differences with India-Mu. DTA … Next slide.

Slide No.: 39

Singapore Mauritius Differences

• A Company will be considered as Shell companyif expenditure incurred by the company is:

- less than INR 50 lakhs / S$ 2 lakhs per 12 monthsin each of the 24 month period before the date ofsale, if the shares have been acquired before31.3.2017 (grandfathered shares).

- less than INR 50 lakhs / S$ 2 lakhs in the 12months before the date of sale, if the gains arisebetween 1.4.2017 and 31.3.2019 (50% of normaltax).

Slide No.: 40

Singapore Mauritius Differences

• For Mauritius, expenditure requirement is half.

• For shares acquired before 1.4.2017, there is noexpenditure test.

• Further domestic anti-abuse provisions can beapplied as per Singapore DTA (Art. 28A).

• Does it mean domestic anti-abuse provisionscannot be applied in case of Mu. DTA?

Slide No.: 41

D. Indirect Transfer

Slide No.: 42

Indirect Transfer - ITA• Section 9(1)(i), Explanation 5:

Asset or Capital asset,

being share or interest,

in a company or entity,

registered or incorporated outside India,

shall be deemed to be situated in India,

if the share or interest derives directly or indirectly,its value substantially from assets located inIndia. Slide No.: 43

To Check

• Extent of shareholding or voting rights or interest inthe entity which holds assets directly in India.

• Existence of management rights or control ininvestee entity; and entity which holds assets directlyin India.

• Value of assets in India of the investee company.

• Value of assets outside India of the investeecompany.

Slide No.: 44

To Check

Not relevant:

• How many shares are sold by the transferor.

• Value of assets outside India of Indian entity.

(Examination stops at Indian company.)

Slide No.: 45

To Check

Slide No.: 46

FCO 1

Transferor

FCO 2

ICO

Assets

No. of shares sold – Not relevant

Existence of management rights.Value of assets in & outsideIndia.

Assets

Outside India

India

Outside India

Assets

Extent of shareholding directly orindirectly (=>5%).Existence of management rights.

Value of assets – Not relevant. i.e. to be included in the value of ICO

Any number of intermediateentities

Value to be excluded

Shareholding & Management

• Provisions apply if:

- Transferor along with AEs holds ≥ 5% of votingrights, or shares or interest directly or indirectly inentity which holds assets directly in India; OR

- Transferor holds management rights inInvestee entity; OR

- Transferor holds management rights in entitywhich holds assets directly in India.

[Above may be held at anytime during the preceding12 months.]

[S. 9(1)(i), Explanation 7]Slide No.: 47

Indirect Transfer - ITA

• Sale of shares of foreign entities resident in Indiacovered by these provisions.

(Shares are situated abroad. Hence prima faciesource is abroad. Because of residence, gains aretaxable in India.)

• Sale by foreign company resident in India:

Payment to Indian residents – No TDS.

However payment to foreign entity resident inIndia – TDS u/s. 195.

Slide No.: 48

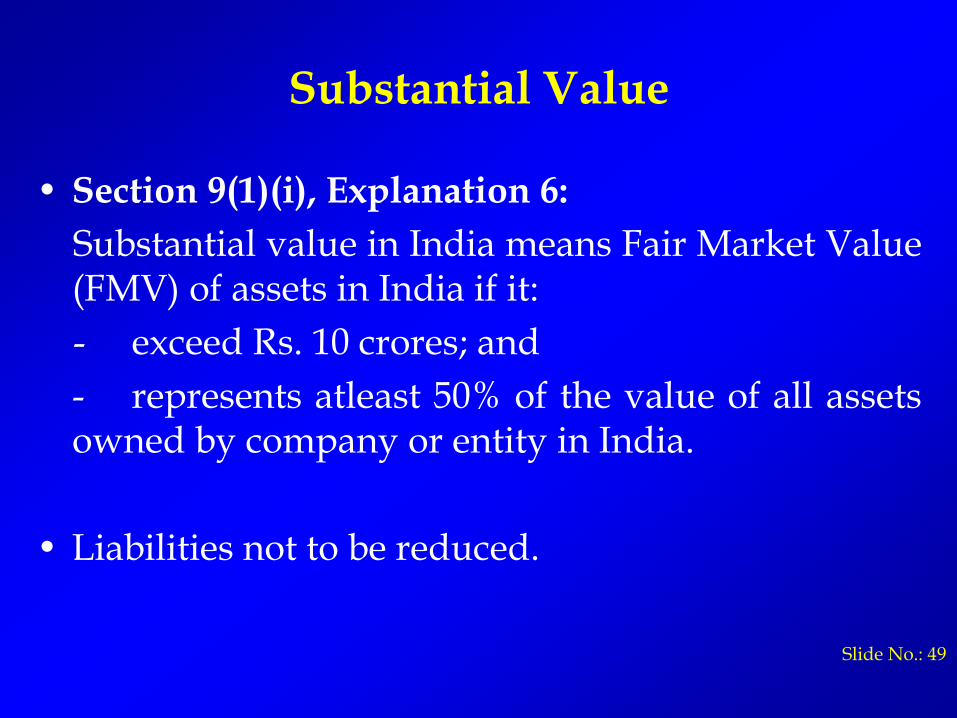

Substantial Value

• Section 9(1)(i), Explanation 6:

Substantial value in India means Fair Market Value(FMV) of assets in India if it:

- exceed Rs. 10 crores; and

- represents atleast 50% of the value of all assetsowned by company or entity in India.

• Liabilities not to be reduced.

Slide No.: 49

Substantial Value

• Value as on specified date – i.e.

- last date of accounting period preceding thedate of transfer; OR

- date of transfer if the book value of the investeeentity on the date of transfer exceeds 15% of thebook value as on the accounting period date.

Rule 11UB for valuation of assets.

[Specified date is only to determine the FMV ofassets in India. Capital gain computation is as peractual transaction values.] Slide No.: 50

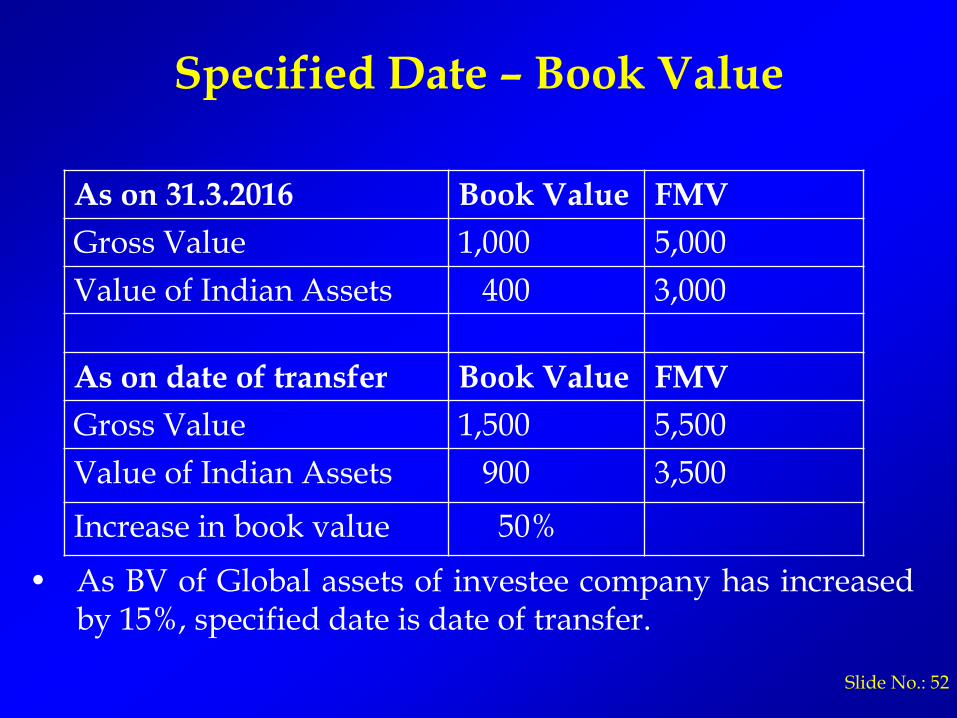

Specified Date – Book Value

• If Book value has increased by more than 15%,FMV has to be considered as on date of transfer.

• Book Value is only to consider on what dateshould the substantial value be considered.

• BV is not relevant for determination of income.

• BV is not relevant for determining whethersubstantial value is in India.

• If Book Value falls, or increases by less than 15%, itis not relevant. FMV on year end to be considered.

Slide No.: 51

Specified Date – Book Value

Slide No.: 52

As on 31.3.2016 Book Value FMV

Gross Value 1,000 5,000

Value of Indian Assets 400 3,000

As on date of transfer Book Value FMV

Gross Value 1,500 5,500

Value of Indian Assets 900 3,500

Increase in book value 50%

• As BV of Global assets of investee company has increasedby 15%, specified date is date of transfer.

Specified Date – Book Value

Slide No.: 53

As on 31.3.2016 Book Value FMV

Gross Value 1,000 1,500

Value of Indian Assets 1,000 1,000 (60%)

By 30.6.2016 foreign investor invests 1,000 in foreign co.

As on 30.6.2016 Book Value FMV

Gross Value 2,000 2,500

Value of Indian Assets 1,000 1,000 (40%)

Increase in Book Value 100%

If shares are transferred on 30.6.2016, is it taxable? No.

On date of transfer, FMV of Indian assets < 50%.

Specified Date – Book Value

If share are transferred on 30.6.2016, is it taxable? Yes.

On date of transfer, FMV of Indian assets ≥ 50%.Slide No.: 54

As on 31.3.2016 Book Value FMV

Global Value 1,000 1,500

Value of Indian Assets 1,000 500 (33.3%)

As on 30.6.2016 Book Value FMV

Global Value 2,000 2,500

Value of Indian Assets 2,000 1,500 (60%)

Increase in B.V. 100%

By 30.6.2016 foreign investor invests 1,000 in foreign co.Foreign company invests 1,000 in Indian company.

Assets outside India

• Value of assets located outside India of foreigninvestee company has to be excluded.

[Assets held outside India by the Indian entitywhose shares are transferred indirectly are to beincluded.]

Rule 11UC for income attributable to assets inIndia.

Slide No.: 55

Slide No.: 56Slide No.: 56

FCO n

FCO 1

Indian Company / Assets

Assets Outside India

India

Outside India

Foreign Assets -Exclude

Outside India

Foreign Assets -Include

Assets outside India –which entity?

Slide No.: 57

FCO 1

FCO 2

220

120 100

40 60

FCO 3

60

Outside

India

India

FCO 1 – Substantial value outside India.

FCO 2 – Substantial value in India.

FCO 3 – Substantial value in India.

Assets

Assets

Assets

Summary

• Summary with reference to the foreign investeecompany / entity whose shares are sold:

- Value from Indian assets held directly orindirectly exceeds Rs. 10 cr. and is at least of 50% ofthe total value of assets.

- Holding should be 5% or more, or there shouldbe management rights.

- Value of assets outside India are to be excluded.

Slide No.: 58

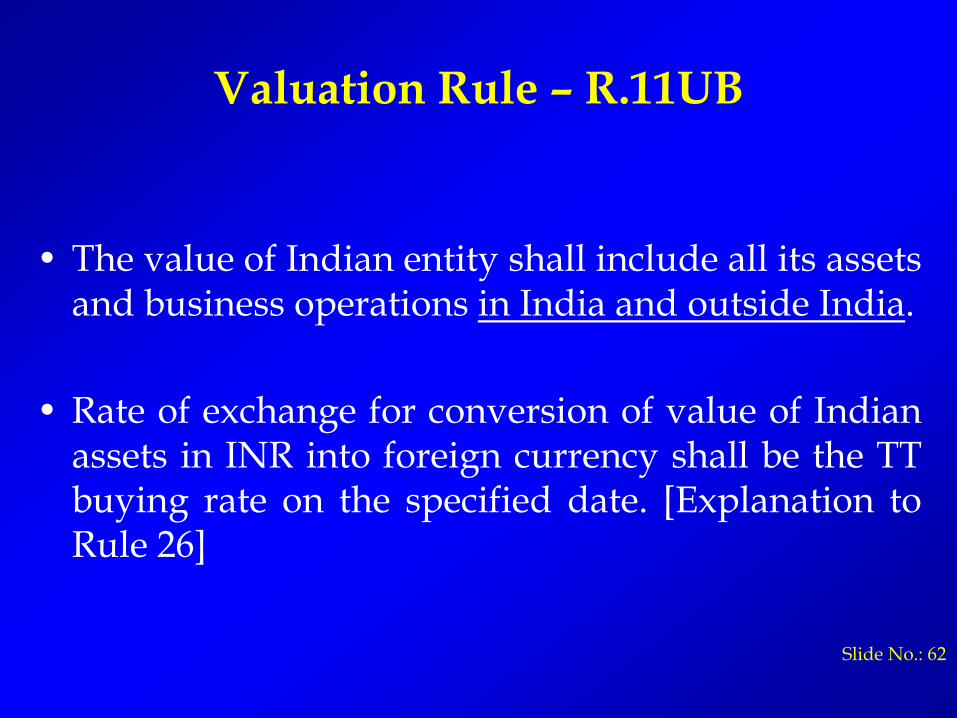

Valuation Rule – R.11UB

• Listed shares of Indian co. – Observable shareprice.

If it includes management rights – FMV = (marketcapitalisation + BV of liabilities) / total shares.

• Unlisted shares of Indian Co. – FMV as perinternationally accepted methodology + liabilitiesif considered for the valuation.

Slide No.: 59

Valuation Rule – R.11UB

• Interest in partnership firm or AOP – FMV as perinternationally accepted methodology + liabilitiesif considered for such valuation.

Value to be allocated to partner / member asunder:

(i) Upto Capital – in ratio of capital contribution.

(ii) Residual value - in ratio agreed for distributionon dissolution of the entity.

[If there is no agreement for distribution ondissolution, allocation will be as per profit sharingratio.]

Slide No.: 60

Valuation Rule – R.11UB

• Other assets – open market value + liabilities ifconsidered for valuation.

• Assets of foreign company or entity.

- In case of transfer between unconnected persons -FMV = value based on full value of consideration+ BV of liabilities.

- In case of connected persons,

For listed company - FMV = observable shareprice + BV of liabilities.

For unlisted company - FMV of assets + liabilitiesif considered.

[Connected person defined in S.102]Slide No.: 61

Valuation Rule – R.11UB

• The value of Indian entity shall include all its assetsand business operations in India and outside India.

• Rate of exchange for conversion of value of Indianassets in INR into foreign currency shall be the TTbuying rate on the specified date. [Explanation toRule 26]

Slide No.: 62

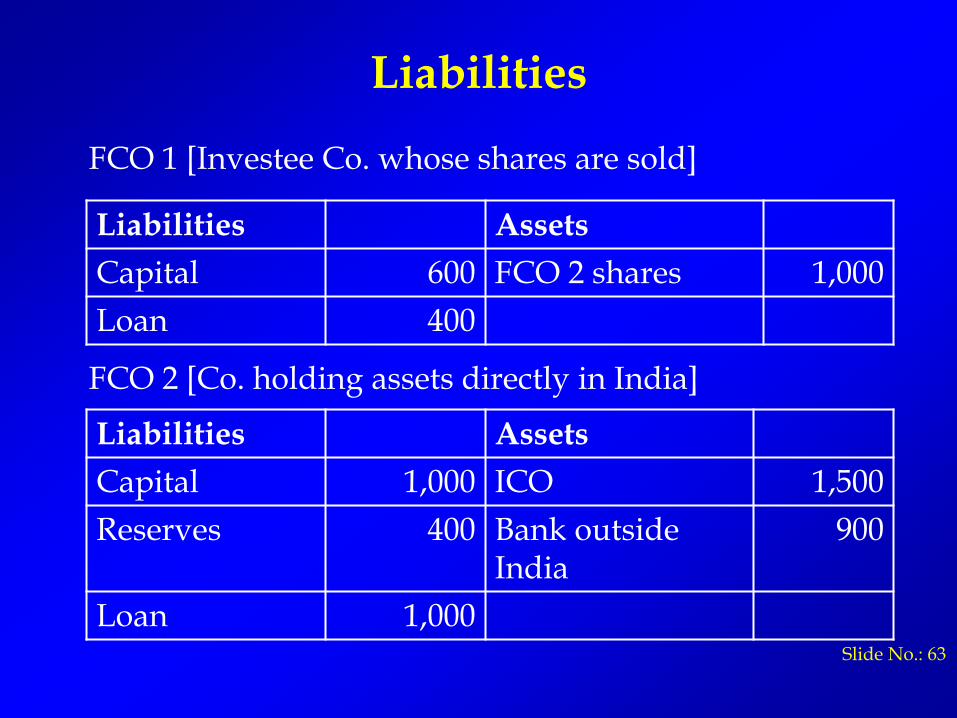

Liabilities

Slide No.: 63

FCO 1 [Investee Co. whose shares are sold]

FCO 2 [Co. holding assets directly in India]

Liabilities Assets

Capital 600 FCO 2 shares 1,000

Loan 400

Liabilities Assets

Capital 1,000 ICO 1,500

Reserves 400 Bank outside India

900

Loan 1,000

Liabilities

Slide No.: 64

Liabilities Assets

Capital 1,500 Factory 2,500

Loan 1,000

ICO

Liabilities Assets

Capital in India …. In India 2,500

Capital outside India 1,000

Loan in India 1,000 Outside India 900

Loan outside India 1,400

Consolidated

Substantial value is in India.

Liabilities

Slide No.: 65

FCO 1

FCO 2 ICO

Investor

Assets 5,000

Liabilities (--)

Net Worth 5,000

Assets 10,000

Liabilities (8000)

Net Worth 2,000

Next slide…

Liabilities

• Value of FCO1:

Slide No.: 66

i) Value of ICO = 2,000+8,000 10,000 66.7%

ii) Value of FCO2 5,000 33.3%

Total Global Value 15,000 100.0%

Liabilities

• Gross assets in India > 50% - Hence substantialvalue in India.

• Net worth – not relevant.

• Only in case of listed shares where there are nomanagement rights, liabilities are not to beconsidered.

Slide No.: 67

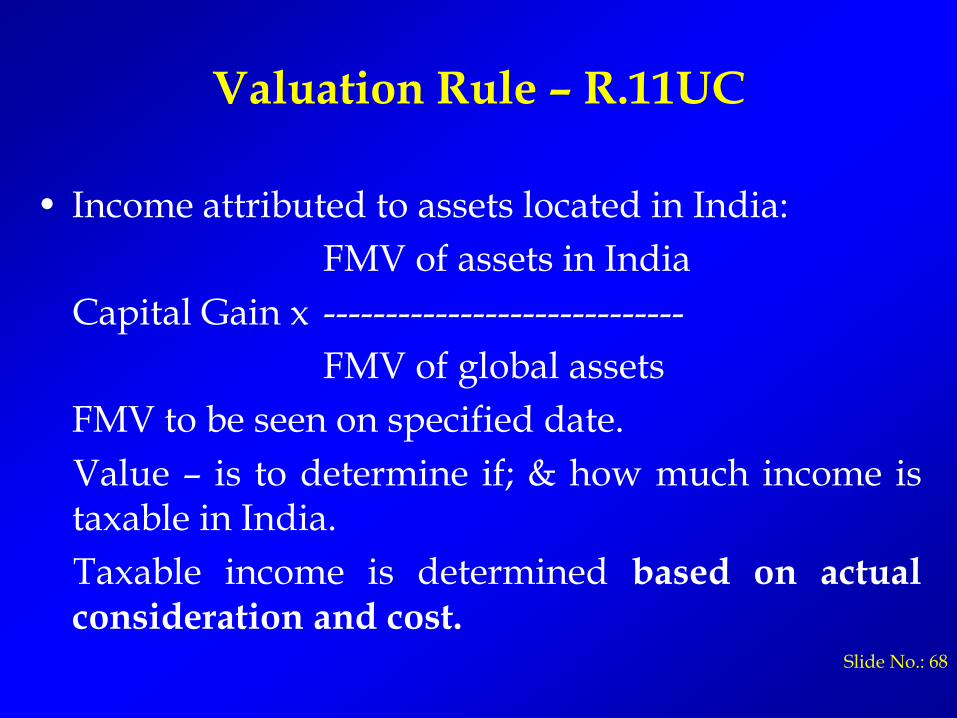

Valuation Rule – R.11UC

• Income attributed to assets located in India:

FMV of assets in India

Capital Gain x -----------------------------

FMV of global assets

FMV to be seen on specified date.

Value – is to determine if; & how much income istaxable in India.

Taxable income is determined based on actualconsideration and cost.

Slide No.: 68

Valuation Rule – R.11UB

• If the FMV has been determined on the basis of aninterim balance sheet on the specified date, theFMV has to be modified after finalisation of thebalance sheet.

• Valuation can be undertaken by Indian accountant.Foreign entity can be valued by accountant in thatcountry.

Conditions are specified for accountants.

• FX fluctuation not available as shares are not ofIndian company. Inflation adjustment available.

Slide No.: 69

Tax rate

• Section 112(1)(c)(iii) – 10% on Long Term Gain -without inflation adjustment and FX fluctuationreliefs.

• Short Term Gain - 40% (foreign company) / 30%(non-foreign company) - without inflationadjustment and FX fluctuation reliefs.

Slide No.: 70

Compliance

• Transferor is required to file a report in Form 3CTfrom an accountant with the tax return. (R.11UC(2)).

• Indian company whose shares are transferredindirectly, has to file Form 49D within 90 daysfrom the end of the year in which transfer takesplace.

In case transfer has the effect of transfer ofmanagement rights, Form has to be filed within 90days from the transaction.

Slide No.: 71

DTA – Indirect Transfer

• S.9(1)(i) Explanation 5 – deems situs of foreigncompany shares to be in India.

Foreign company shares are not treated as Indiancompany shares/ Indian assets.

• DTA – Capital gains on any other assets are taxableonly in COR.

If this article applies, Capital Gains is not taxable inIndia.

• GAAR applicable.

Slide No.: 72

Other provisions & Indirect Transfer Provision

• Indirect Transfer provisions apply to Transfer ofshares or interest in foreign entity – includingmerger / demerger / liquidation.

• Not applicable for dividend – [Circular 4 dated26.3.2015].

• Not applicable to acquisition at discount.[S.56(2)(vii) & (viia)].

Slide No.: 73

Other provisions & Indirect Transfer Provision

• Not applicable to investment in shares[S.56(2)(viib)]

• Options or derivatives are not shares or interest inan entity. Hence should not be covered by Indirecttransfer provisions.

-----------

• Transfer Pricing applicable.

• GAAR applicable.Slide No.: 74

Merger & Demerger – Indirect Transfer

• Exemption available for amalgamating &demerged company [S. 47(viab)& S. 47(vicc)].

[In line with direct amalgamation / demerger ofIndian co. [S. 47(vi)& S. 47(vib)]

• No exemption for shareholder of amalgamated &demerged company.

[Exemption available for domestic amalgamation /demerger - S. 47(vii)& S. 47(vid)]

• Exemption available for transfer to holding co. orsubsidiary co. [S. 47(iv) & S. 47(v)] Slide No.: 75

Merger

Slide No.: 76

Exemption available for FCO 1 [S. 47(viab)]

No exemption for Investor.

Investor

FCO 1

ICO

FCO 1Outside India

India

Shares onMerger

Extinguished on merger

Merger

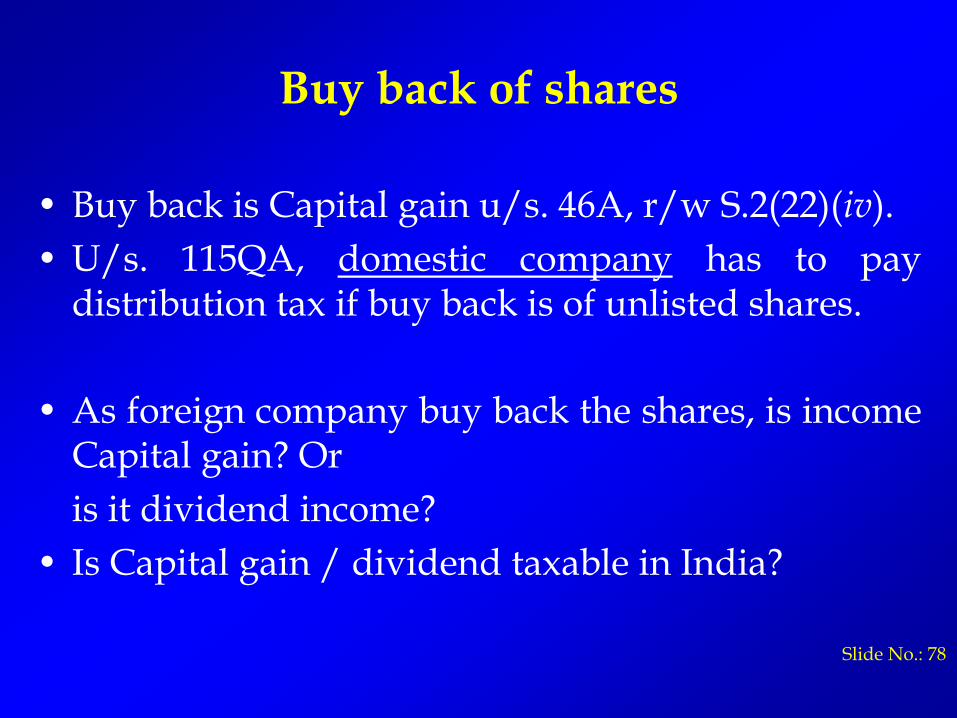

Buy back of shares

Slide No.: 77

Investor

FCO 1

ICO

Outside India

India

Payment of consideration

Buy Back of shares

Buy back of shares

• Buy back is Capital gain u/s. 46A, r/w S.2(22)(iv).

• U/s. 115QA, domestic company has to paydistribution tax if buy back is of unlisted shares.

• As foreign company buy back the shares, is incomeCapital gain? Or

is it dividend income?

• Is Capital gain / dividend taxable in India?

Slide No.: 78

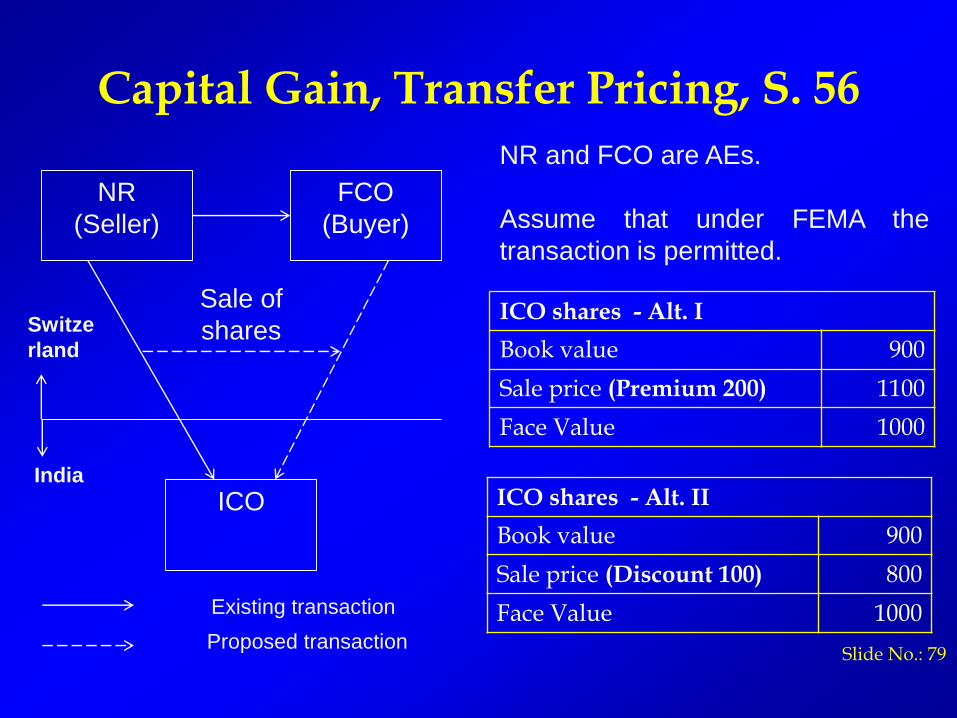

Capital Gain, Transfer Pricing, S. 56

ICO shares - Alt. I

Book value 900

Sale price (Premium 200) 1100

Face Value 1000

NR

(Seller)

FCO

(Buyer)

ICO

Sale of

shares

Proposed transaction

Existing transaction

ICO shares - Alt. II

Book value 900

Sale price (Discount 100) 800

Face Value 1000

NR and FCO are AEs.

Assume that under FEMA the

transaction is permitted.

India

Switze

rland

Slide No.: 79

Capital Gain, Transfer Pricing, S.56

• Transfer Pricing:

- Share investment is a capital transaction. It doesnot give rise to income – unless specificallyprovided. (Vodafone India Services – 50taxmann.com 300 – BOM HC – AY 2009-10).

- TP provisions cannot apply if there is no income.

- Shell India Markets – 51 taxmann.com 519 (BOMHC) also is in line with Vodafone case.(Observation – If Form 3CEB was not filed asrequired, consequences may follow.)

Slide No.: 80

Capital Gain, Transfer Pricing, S.56

- S.56(2) clause (vii) has been inserted from1.10.2009; clause (viia) has been inserted from1.6.2010.

Acquiring asset at discount is taxable.

- However still do TP provisions apply? If yes, willwe have to compute the ALP, or only incomeunder section 56(2)?

- Reporting of “International Transaction” isrequired u/s. 92E – Form 3CEB.

- “International Transaction” is defined to includecapital financing …. (Expln. (c) to S. 92B).

Slide No.:81

Capital Gain, Transfer Pricing, S.56

• Alt. I – FCO (Buyer):

- No specific tax implication.

- Should the transaction be reported althoughthere is no tax implication?

- Any implication of buying shares at a highvalue?

• Alt. I – NR (Seller):

- Normal capital gain.

- File TP report.

Slide No.: 82

Capital Gain, Transfer Pricing, S.56

• Alt. II – FCO (Buyer):

- Difference between Book Value and Sale price(100) - is taxable u/s. 56(2)(viia).

- Should ALP be computed and reported?

• Alt. II – NR (Seller):

- Apply TP, compute ALP and pay tax.

- This leads to double tax to the extent of 100. Isthis all right?

Slide No.: 83

![[I.P._Natanson]_Theory_of_Functions_of_a_Real_Vari( ).pdf](https://static.fdocuments.in/doc/165x107/55cf91c7550346f57b909643/ipnatansontheoryoffunctionsofarealvaribookzzorgpdf.jpg)