The Case for a Consumed Income Tax Structure · The Case for a Consumed Income Tax Structure Robert...

29

The Case for a Consumed Income Tax Structure Robert Leeson [email protected] September 4 2010-9 To be presented at the Department of Economics, Bowdoin College, September 16, 2010 Abstract This paper extends the case for a Consumed Income Tax Structure (CITS). The first five components of the case are traditional: it encourages growth, offers flexibility and simplification and introduces some much-needed rationality into the tax system. But the CITS also relates to a deeper definition of income (as final satisfaction, not the receipt of money in return for services rendered); it provides the tax system with a much-needed ethical foundation; it liberates the labor supply/leisure choice from all tax-based distortions, returning the surplus to those to whom it belongs (the worker and the employer); and it helps dissolve societal conflicts by providing a consensus-foundation for the mixed economy. When CITS is embedded in a progressive system, it collects increasing units of marginal taxation from diminishing units of marginal utility (the Paradox of Flat Progressivity). Taxation ceases to be a compulsory levy on socially worthwhile activities and becomes entirely a voluntary donation. CITS thus collects taxes through an invisible hand; it also assists the invisible hand of what Adam Smith called the “impartial spectator” to provide both privately and socially optimal levels of savings. It reduces the incentive to evade and facilitates an increase in future consumption through increased savings (the Non-Paradox of Thrift). Under CITS, Veblen’s snobs would help balance the budget. The Introductory Case i Agreement will never be reached about the optimal size and reach of government: at the margin, value judgments will always dominate. The young Milton Friedman’s (1948, 248-9) solution was to match taxation (T) with a consensus-derived level of government expenditures on goods and services (G*) which should be determined “entirely on the basis of the community’s desire, need and willingness to pay for public services … A decision to undertake additional public expenditure should be accompanied by a revenue measure increasing taxes” (G = G* = T). ii Friedman’s (1948, 248) scheme would eliminate discretionary fiscal policy: “No attempt should be made to vary expenditures, either directly or inversely, in response to cyclical fluctuation in business activity”. This paper examines the T side of the fiscal equation and argues that the

Transcript of The Case for a Consumed Income Tax Structure · The Case for a Consumed Income Tax Structure Robert...

The Case for a Consumed Income Tax Structure

Robert Leeson

September 4 2010-9

To be presented at the Department of Economics, Bowdoin College, September 16, 2010

Abstract

This paper extends the case for a Consumed Income Tax Structure (CITS). The first five components of the case are traditional: it encourages growth, offers flexibility and simplification and introduces some much-needed rationality into the tax system. But the CITS also relates to a deeper definition of income (as final satisfaction, not the receipt of money in return for services rendered); it provides the tax system with a much-needed ethical foundation; it liberates the labor supply/leisure choice from all tax-based distortions, returning the surplus to those to whom it belongs (the worker and the employer); and it helps dissolve societal conflicts by providing a consensus-foundation for the mixed economy.

When CITS is embedded in a progressive system, it collects increasing units of marginal taxation from diminishing units of marginal utility (the Paradox of Flat Progressivity). Taxation ceases to be a compulsory levy on socially worthwhile activities and becomes entirely a voluntary donation.

CITS thus collects taxes through an invisible hand; it also assists the invisible hand of what Adam Smith called the “impartial spectator” to provide both privately and socially optimal levels of savings. It reduces the incentive to evade and facilitates an increase in future consumption through increased savings (the Non-Paradox of Thrift). Under CITS, Veblen’s snobs would help balance the budget.

The Introductory Casei

Agreement will never be reached about the optimal size and reach of government: at the margin, value judgments will always dominate. The young Milton Friedman’s (1948, 248-9) solution was to match taxation (T) with a consensus-derived level of government expenditures on goods and services (G*) which should be determined “entirely on the basis of the community’s desire, need and willingness to pay for public services … A decision to undertake additional public expenditure should be accompanied by a revenue measure increasing taxes” (G = G* = T).ii

Friedman’s (1948, 248) scheme would eliminate discretionary fiscal policy: “No attempt should be made to vary expenditures, either directly or inversely, in response to cyclical fluctuation in business activity”. This paper examines the T side of the fiscal equation and argues that the

optimal budget-balancing tax structure already exists: the Consumed Income Tax Structure (CITS).

There is agreement about the non-sustainability of long-term government deficits; but the so-called Paradox of Thrift muddies the waters about shorter horizons. Under CITS, the Paradox of Thrift becomes a fallacy: annual budget balance can be targeted without adverse consequences.

With the Keynesians fiscal multiplier, governments can supposedly target both a balanced budget plus “benevolent” consumption (low income people with high marginal propensities to spend). But with the deficit multiplier, the government becomes a malevolent consumer of savings. A government that repeatedly borrows (from household savings in the loanable funds market) to finance temporary tax cuts which are then primarily saved (and returned to the loanable funds market) is recycling funds while expanding the budget deficit.iii

The boost to Aggregate Demand from any increase in consumption from each round of transitory income will be crowded-out by the investment-curtailing rise in interest rates. Each rise in interest rates increases both the debt-service burden and the default risk.

A policy rule which mandated a government to respond in this way every time output fell below the “natural” rate would generate ever rising budget deficits. The sum of a geometric series is finite as long as the terms approach zero; but in this deficit multiplier, consumption not savings is the leakage, and the deficit tends to infinity. The universe may be infinite in all directions, but the gullibility of savers is not. This deficit multiplier culminates in the Junk (not to be confused with James) Bond

Governments fail when budgets remain stubbornly unbalanced. The market failure of chronically low household savings exacerbates the situation. Insufficient household savings may partly be caused by the promise or expectation of future government support; it may also partly be caused by a subjective time horizon shift.

In some countries, the forces of current consumption appear to overwhelm the forces of savings and threaten to overrun the government’s budget. The subjective interest rate undervalues the utility to be derived from future consumption relative to the utility derived from consumption today. Under CITS, policy makers can remove this distortion by altering the objective market interest rate, Pc/Ps, the price of consumption today (Pc) relative to the price of consumption in the future (financed by savings, Ps). A rate of household savings can be targeted that will eliminate the intergenerational distortions caused by these unfunded liabilities.iv

The Policy Optimizing Trinity (POT) alleviates the unfunded liabilities problem (1) by removing the distortions caused by taxes on income (2) and the distortions that lead to sub-optimal levels of household savings (3).

Several piecemeal CITS components already exist. Point-of-sale taxes (Value Added, Goods and Services etc) are CITS-type arrangements (with regressive, or at least non-progressive, features) and tax-privileged savings accounts already exist. But such quasi-consumed taxes become embedded in prices: hidden and thus easier and more tempting to raise than visible taxes.

Pre-tax Individual Savings Accounts (ISA) could be voluntary - as in the U.S.A (Unlimited Savings Account) proposed by Sam Nunn (R-Georgia) and Pete Domenici (D-New Mexico) - or compulsory, as in Singapore, Australia and elsewhere. Payday default ISA deposits – or withheld savings – could replace the withholding income tax (prior to the end-of-year adjustment). Sales taxes could be retained or abolished. Saves could access their funds at any time (minus withholding tax) or with restriction. The withholding tax could diminish at 5% per year thus removing all tax on income after 20 years. CITS allows for all these permutations – plus a relatively painless method of targeting an annual balanced budget.

Singapore has perhaps gone the furthest with respect to implementing the structure of the consumed income tax (although debates remain about the system that has been chosen to operate this structure). The income tax can easily be abolished and replaced by CITS through the introduction of ISA: in Singapore, taxes are collected on income minus deposits into accounts at the Central Provident Fund (34.5% of private sector wages, for workers aged below 50).

Most economists regard CITS as ordinally superior to the Pure Income Tax Structure (PITS). Taxes on income unambiguously distort the labor-leisure choice and there are solid reasons for concluding that taxes on consumption increase saving and wealth and are therefore are welfare improving.

Specifically, CITS has at least fifteen desirable characteristics. The first five are traditional: it encourages growth, offers flexibility and simplification and introduces some much-needed rationality into the tax system (1-5). This paper strengthens the case by adding or building upon ten further desirable characteristics.

CITS relates to a deeper definition of income: as final satisfaction, not the receipt of money in return for services rendered (6). CITS provides the tax system with a much-needed ethical foundation: it taxes what people take out of the economic system not what they put in (7).

The abolition of income tax liberates the labor supply/leisure choice from all tax-based distortions. Taxing income leads to welfare losses. CITS returns the surplus to those to whom it belongs: the worker and the employer (8). CITS can help dissolve societal conflicts by providing a consensus-foundation for the mixed economy (9).

When CITS is embedded in a progressive system, it collects increasing units of marginal taxation from diminishing units of marginal utility. It also provides a survey-based method of estimating utility foregone: the optimal Cardinal Utility Tax Structure (CUTS). CUTS flattens progressivity and can produce a flat progressive tax (10).

Taxation ceases to be a compulsory levy on (generally) socially worthwhile activities (such as work) and becomes entirely a voluntary donation (a consequence of the choice to consume above a certain level). CITS thus collects taxes through an invisible hand (11). It assists the invisible hand of what Adam Smith called the “impartial spectator” to provide both privately and socially optimal levels of savings (12). It reduces the incentive to evade (13). It facilitates an increase in future consumption through increased savings: the Non-Paradox of Thrift (14). Under CITS, Veblen’s snobs would help balance the budget (15).

The retreat of arbitrary taxation and the advance of democracy are linked. Taxation can expand the coercive power of the State but it also links government and the governed in a legitimizing embrace. The presence and pressures of taxation tends to increase both the transparency of government and the contestability of politics. The ever-present threat of tax revolt is a permanent reminder that taxpayer Voice can lead to political Exit for those who abuse taxpayer funds.

The State can expropriate bodily property rights through incarceration, the military draft and capital punishment. Such bodily property rights would be eliminated by the elimination of food and shelter. But we have surrendered to the State the property rights over the process by which food and shelter are provided: the income tax is a form of income punishment.v

Since taxation is inevitable - for all except Robinson Crusoe, anarchist communities and oil sheikdoms – optimizing principles should be applied. What follows below is a “least ugly” contest. PITS – the sub-optimal Pure Income Tax Structure – is pitied against CITS – the optimal Consumed Income Tax Structure.

A tax structure becomes a system when rates are attached. CUTS – the optimal Cardinal Utility Tax Structure – is a progressive CITS with a paradoxical feature: the possibility of flat progressivity. PITS undermines the optimization process from the outset; CITS corrects this distortion.

Let the battle begin and may the optimal structure win.

Prelude: Behavioral Economics and Homo Economicus

CITS appeals to both neoclassical economists and their behavioral critics.vi Homo Economicus, the work horse of neoclassical orthodoxy, began life in bondage, “under the governance of two sovereign masters, pain and pleasure … fastened to their thrones … the principle of utility recognises this subjection and assumes it for the foundation of that system” (Bentham 1907 [1823], chapter 1, para 43).

This optimizing agent maximizes lifetime utility, first, by making an optimal choice between the hours of labor supplied and “leisure”. Homo Economicus is also sufficiently far-sighted to

finance a smooth lifetime consumption flow by making an optimal choice between current and deferred consumption (savings).

If the choice turns out to be non-optimal – eating, not planting, the seed corn - Homo Economicus may be forced to revise and extend future labor supply decisions (food-feedback). Alternatively, this once mighty engine of economic analysis becomes a liability, an unfunded ward of the state, financing retirement consumption through an intergenerational begging bowl (on-the-parish-fallback).

Having optimally decided how much income to currently consume, Homo Economicus - in the final step of this optimization trinity - makes a utility maximizing choice between various goods and services (thus deriving demand curves).vii

Consumer sovereignty provides one justification for free market capitalism. If Homo Economicus is victimized by persuasive marketing, this particular justification vanishes: we live, instead, in a Galbraithian world of producer sovereignty and impulsive response functions. If the same “Me, Now, credit card” forces are sufficiently seductive so as to elevate current consumption over deferred consumption, a bald Homo Sampson, having taken an intergenerational haircut, will end his days eyeless in Gaza.

An allegedly dieting Homer Simpson asked for “a sign” to indicate whether or not there would be divine displeasure if he consumed a forbidden donut. In some countries, household savings decisions appear to be made more by Homo Simpson Myopicus than by Homo Economicus.viii

When Homo Simpson Myopicus fails to see his inter-temporal budget constraint, he becomes an unfunded liability for Homo Macroeconomicus.ix Behavioral economists are currently trying to construct Homo Behavicus (behavicus is Latin for “behave yourself and save properly”).x For example, agents with time inconsistent preferences can be embedded in a game-theoretic framework played by successive incarnations of a single decision-maker (Bernheim, Ray and Yeltekin 1999).xi

Laurie Simon Bagwell and B. Douglas Bernheim (1996, 368) concluded that “an excise tax on conspicuous goods amounts to a non-distortionary tax on pure profits”. CITS is distortion-correcting and would be a major contribution to the pursuit of improved savings outcomes.xii

The Traditional Case

Encouraging growth

1. CITS encourages saving and thus capital formation which can generate economic growth and higher wages (Blueprints for Basic Tax Reform 1977, 10). Thus CITS “gives the maximum opportunity for business enterprise and development” (Structure and Reform of Direct Taxation 1978, 502). A National Bureau of Economic Research study estimated that a shift to a

consumption tax could increase long run output by 11% (Altig, Auerback, Kotlikoff, Smetters and Walliser 1997; Auerback 2005).

Marginal rates: flexibility

2. It allows for flexibility: marginal rates of taxation could remain more or less as they are or could be increased at the upper end (as a “luxury” tax or tax on “luxurious” living). Raising taxes on income to try and balance the budget can be electorally hazardous and may also reduce tax revenue (via Laffer curve effects). In contrast, raising taxes on “luxury” may increase both savings and tax revenue.

Simplification and rationalization

3. The existing hybrid system treats some categories of savings in a favourable fashion while others are subject to double taxation in a “totally arbitrary manner” (Structure and Reform of Direct Taxation 1978, 70; Mill 1884, 179; Fisher 1939; Kaldor 1955, 80).

4. It is administratively feasible, hardly more complicated than the current system.

5. Excluding savings from the tax base further simplifies matters by eliminating many issues such as depreciation and inflation adjustments (Blueprints for Basic Tax Reform 1977, 9).

The Extended Case

Consumption: the optimal candidate for taxation

6. CITS relates to a deeper definition of income: as final satisfaction, not the receipt of money in return for services rendered. Maximizing lifetime utility is the fundamental behavioral postulate of neoclassical economics: since consumption generates utility it should also generate the tax revenue to pay for activities that markets do not adequately deliver.

7. All three basic forms of economic activity (production, accumulation and consumption), are transformational. With production and savings, the transformational flow runs from the private to the social sphere. With consumption, the flow runs in the opposite direction: socially produced goods and services are transformed into private utility.

For an individual worker, value-adding production transforms private resources (time) into socially available output. The private decision to save turns deferred consumption into potential future consumption. It also generates at least two social benefits. First, it transfers surplus resources to deficit resource units and is, therefore, available to be transformed into socially productive capital). Second, it reduces the future tax liabilities associated with unfunded retirement income streams.

Pigovian taxes and subsidies are designed to encourage social-value-adding and discourage social-value-subtracting activities. While most, if not all, of the benefits of consumption are

captured by the individual consumer, social costs can be generated too. At the microeconomic level, “sin” taxes on alcohol, tobacco, gambling, petrol, certain types of food etc. can discourage both social costs and self-harm. At the macroeconomic level, CITS can fund all the social activities that governments have been designed to provide. Of the three basic economic activities, consumption is the least worthy of preferential tax treatment. Therefore, on Pigovian grounds, production and savings are worthy of subsidy - or rather should be exempt from the discouragement caused by taxation.

Consumption has some social benefits – most of the benefits are privately captured. Production and accumulation are more generally socially productive and should not, therefore, be discouraged through taxation.xiii In contrast, the third (consumption) uses up resources and is therefore a preferred candidate for taxation.xiv

CITS thus provides the tax system with a much-needed ethical foundation. As James Meade (1978, xvi) put it, taxes should fall on “what people took out of the economic system in higher levels of consumption rather than on what they put into the system through their savings and enterprise”.xv

8. The abolition of income tax liberates the labor supply/leisure choice from all tax-based distortions. Economists traditionally derive an individual’s labor supply curve through a choice theoretical framework: the optimal division of a 24 hour day between labor and leisure. Utility is being maximized along a labor supply curve: leisure produces utility and labor supply produces income (plus “psychic” utility) to fund current and future consumption.

The income tax generates a market labor supply curve which is removed from this utility maximizing curve. It distorts the labor supply decision by driving a wedge between the wage received by the supplier and the wage paid by the employer (the same effect as an upward shift of the supply curve). This causes a reduction in the quantity of labor demanded.

Entire macroeconomic schools are based on this optimization decision. In the basic neoclassical macroeconomic model, dysfunctions occur when the economy operates off the labor supply curve (when the real wage is above equilibrium). The economy is displaced from the “natural” rate of unemployment and output when labor suppliers are confused by unexpected inflation (monetarism) or unanticipated monetary growth (the new classical school).

But PITS thwarts the individual optimizing decision right from the outset. The income derived from the labor supply decision feeds into another optimizing decision relating to the demand curve (or functions) for goods and services. But these supposedly “optimized” demand curves are derived as a constrained optimization exercise: constrained by the sub-optimality of PITS.

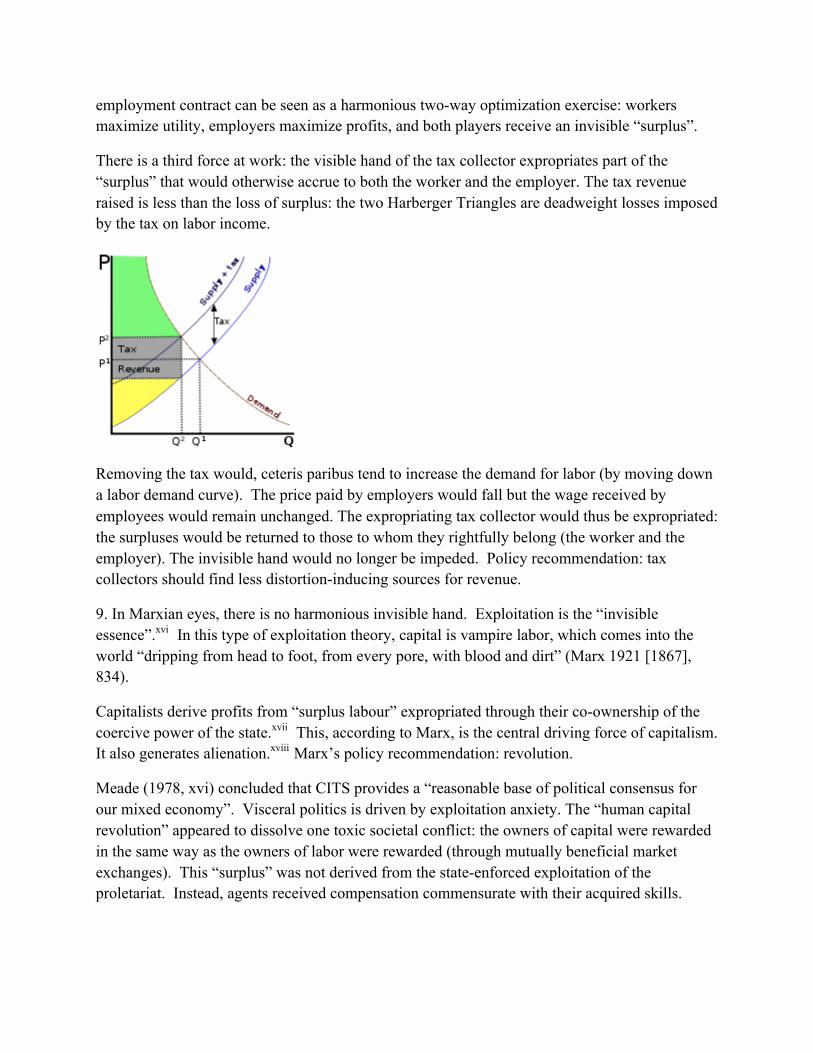

With downward sloping demand curve of labor and upward sloping supply curve of labor, the free market price allows some workers to be paid more than they were prepared to work for and some employers to receive labor at a lower price than they would been prepared to pay. The

employment contract can be seen as a harmonious two-way optimization exercise: workers maximize utility, employers maximize profits, and both players receive an invisible “surplus”.

There is a third force at work: the visible hand of the tax collector expropriates part of the “surplus” that would otherwise accrue to both the worker and the employer. The tax revenue raised is less than the loss of surplus: the two Harberger Triangles are deadweight losses imposed by the tax on labor income.

Removing the tax would, ceteris paribus tend to increase the demand for labor (by moving down a labor demand curve). The price paid by employers would fall but the wage received by employees would remain unchanged. The expropriating tax collector would thus be expropriated: the surpluses would be returned to those to whom they rightfully belong (the worker and the employer). The invisible hand would no longer be impeded. Policy recommendation: tax collectors should find less distortion-inducing sources for revenue.

9. In Marxian eyes, there is no harmonious invisible hand. Exploitation is the “invisible essence”.xvi In this type of exploitation theory, capital is vampire labor, which comes into the world “dripping from head to foot, from every pore, with blood and dirt” (Marx 1921 [1867], 834).

Capitalists derive profits from “surplus labour” expropriated through their co-ownership of the coercive power of the state.xvii This, according to Marx, is the central driving force of capitalism. It also generates alienation.xviii Marx’s policy recommendation: revolution.

Meade (1978, xvi) concluded that CITS provides a “reasonable base of political consensus for our mixed economy”. Visceral politics is driven by exploitation anxiety. The “human capital revolution” appeared to dissolve one toxic societal conflict: the owners of capital were rewarded in the same way as the owners of labor were rewarded (through mutually beneficial market exchanges). This “surplus” was not derived from the state-enforced exploitation of the proletariat. Instead, agents received compensation commensurate with their acquired skills.

As the human capital revolution undermined “working class” parties and perceptions about “wage slavery”, so CITS could undermine the suspicion that drives many self-employed people to see taxation as theft. The Tax Foundation calculated that in 2010, Tax Freedom Day fell on April 9th - the 99th day of the year.xix CITS leaves all Free to Choose their tax bill: spending $20,000 per annum may avoid taxation entirely, but every dollar earned over, say, $500,000, must either be consumed at a later date (saved) or taxed at the highest marginal rate.

10. CITS collects increasing units of marginal taxation from diminishing units of marginal utility.

Because CITS is socially optimal, economists have long had an ordinal preference for it over PITS. It is also privately optimal for economists - it offers the research-enhancing prospect of measuring “utils” (or at least their close proxies).

Cardinal notions of utility pre-date Adam Smith: Francis Hutcheson (2004 [1726], section 3, 37, VIII) developed a quantity theory of happiness.xx Welfare evaluations derived from cardinal perceptions can lead to extreme policy conclusions. Triage is commonly practiced on the battlefield.xxi But few would argue for the redistributive cardinal superiority of ending the life of one healthy person (by extracting five organs) so that five (organ-lacking) people may live (although such decisions are effectively made by those who allocate health care expenditures).

At the other extreme, welfare evaluations derived from non-cardinal perceptions can lead to inactivity. If Robert Mugabe were to extend his dictatorship and appropriate the entire wealth of the world, it would be Pareto inefficient to remove a single dollar from him: Pareto paralysis.

The ordinalist revolutionaries (such as Lionel Robbins and John Hicks) disallowed the societal aggregation of utility because interpersonal comparisons were impossible. With ordinal utility, differences in “utils” are meaningless: we know nothing about the related strength of preferences.

It would, however, be possible to estimate the cardinal strength of dissatisfaction with current tax systems by asking taxpayers each year to attach a number (1-10) to the intensity of their dissatisfaction. Any changes over time would provide an unambiguous cardinal measure of the strength of aversion.

A progressive consumed income tax provides a numerical method of estimating utility foregone: the optimal Cardinal Utility Tax Structure (CUTS).

An individual’s income (Y) has three components: taxation (T), consumption (C) and savings (S):

(1) Y = T + C + S

Under PITS, labor income and personal income taxation (Ty) are simultaneously determined. The causality runs from income to taxation. Agents choose between labor supply and leisure: the decision to supply (paid) labor causes the tax liability. Tax is avoided by not working.

The relevant PITS behavioral equation is:

(2) (Y – Ty) = C + S.

In many countries household savings appears to be a residual, insufficiently related to future consumption needs. But savings are derived from another residual: disposable post-tax income (Y-Ty). Only then can the choice between consumption and savings be made. PITS thus eliminates the possibility of deriving any private utility from the tax withheld.

With CUTS, the choice between consumption and personal consumption taxation (Tc) is simultaneously determined:

(3) (C + Tc) = Y – S.

The causality runs from consumption to taxation. Tax is incurred in the choice between consumption and savings: the decision to consume is associated with the decision to pay tax. Tax is avoided by saving.

Smith (1981 [1776], book 5, chapter 2) favored a progressive tax system.xxii However, the optimal CUTS structure is consistent with either a flat or a progressive tax system.xxiii One advantage of a progressive system is that it minimizes the utility forgone per dollar of tax raised by attaching increasing marginal tax to diminishing marginal utility. This can lead to flat(ish) tax-induced losses in utility and in one case a progressive-flat tax.

Diminishing marginal utility suggests that the utility derived from the first $1 of consumption (A units of utility) is less than the utility derived from the $500,001st dollar of consumption (E units of utility). With a progressive CUTS, each intervening dollar decreases in utility as marginal consumption tax rates increase. As a hypothetical example, consider a five tier CUTS system.

In the lowest bracket ($0-20,000) the tax rate is 0%. The dollars in this bracket are privately the most valuable, but socially (as measured by tax collected) the least valuable (the marginal rate, the tax revenue raised and the tax-induced utility forgone are all zero).

In the second bracket ($20,000-100,000) the tax rate is 20%. The “prudent tax avoider” is free to earn whatever they can and to minimize tax by increasing their wealth (by saving to finance future consumption). Information about the goods and services purchased by this cohort could be obtained through survey evidence.

The 20,001st dollar generates B units of utility (A > B), but is socially more valuable. It generates $0.20 in tax revenue (a private loss to the consumer). The tax-induced loss of utility is therefore B/5.

In the third bracket ($100,000-200,000) the tax rate is 40%. The 100,001st dollar generates C units of utility (A > B > C) but is socially more valuable ($0.40 tax revenue). The tax-induced loss of utility is 2C/5.

In the fourth bracket ($200,000-500,000) the tax rate is 60%. The 200,001st dollar generates D units of utility (A > B > C > D) but is socially more valuable (tax revenue: $0.60). The tax-induced loss of utility is 3D/5.

In the final bracket (over $500,000) the tax rate is 80%. The “luxurious rich” high-end-cohort contribute most in terms of tax revenue. As with the “prudent tax avoider” bracket, information about the goods and services purchased by this cohort could be obtained through survey evidence.

The 500,001st dollar generates E units of utility (A > B > C > D > E) but is socially more valuable ($0.80 tax revenue). The tax-induced loss of utility is 4E/5.

Without diminishing marginal utility, each dollar would generate Z units of utility (Z = A = B = C = D = E). The tax-induced loss of utility for a dollar in each category would increase in exact proportion to the marginal tax rate: 0, Z/5, 2Z/5, 3Z/5 and 4Z/5. With the progressive tax rates described above, the tax on the 500,001st dollar would cause a utility loss four times greater than the tax on the 20,001st dollar: (4Z/5) = 4 x (Z/5).

But with diminishing marginal utility, E < B, and therefore (4E/5) < 4 x (B/5) - the blow is softened. The tax on the 500,001st dollar causes a loss of utility less than four times greater than the tax on the 20,001st dollar.

Evidence about the strength of preferences can be elicited through survey evidence allowing greater numerical accuracy to be attached to the loss of utility associated with each tax dollar.

By comparing the consumption patterns of the “luxurious rich” with the consumption bundles of “the prudent tax avoiders” three types of consumed items would be identified: sticky, disjoint and overlapping.

The sticky set would contain items (such as salt) that are bought in exactly the same volume for approximately the same price (zero income elasticity of demand).

The disjoint set would contain items that are typically exclusive to one cohort. Inferior goods would be exclusively in the lower cohort (negative income elasticity of demand). Luxury goods (elasticity of demand, much greater than one) are purchased to signal exclusive status, income or wealth (designer clothes, yachts, large dwellings, domestic servants etc).xxiv These would be found exclusively in the “luxurious rich” cohort.

The overlapping set would consist of items that fall in more than one cohort but are consumed in different quantities (seats at the opera, tickets to the baseball, holiday expenses etc). Items in the

necessity subset (for example, food and public utilities) are income inelastic. The number of items in the (income elastic) superior subset may not increase much as income increases, but expenditure per item may (for example, wine, holidays etc).

Residential housing is a unique item. In the national income accounts it is typically treated in the “investment”, not the “consumer expenditure” category. It is also typically financed through long-term debt. But for illustrative purposes it provides a perfect comparison.

Survey information could reveal a cardinal ranking of the intensity of preferences (on a scale of 1-10). A “prudent tax avoider” may live in a five bedroom dwelling; the “luxurious rich” would probably occupy more than five rooms. How much utility do the additional rooms provide in absolute terms (or alternatively, per dollar of cost)?

If the “prudent tax avoider” derived “8” reported utils from the last (and maybe only) spare bedroom, and if the “luxurious rich” derived an average of “4” reported utils from their last (maybe nth spare bedroom), this would provide information about diminishing cardinal utility. If the “luxurious rich” reported only “2” utils from their last spare bedroom, ceteris paribus, this may indicate a four-fold diminution in utility.

Real estate is (more or less objectively) valued by “valuation surveyors;" carefully designed contingent evaluation surveys could also elicit information about subjective evaluations. If the “prudent tax avoider” was prepared to pay $10,000 (plus tax) for an additional spare bedroom and the “luxurious rich” was prepared to pay $6,666.66 (plus tax) for an identical (but nth) spare bedroom, they would both face a $12,000 cost. Alternatively, if the “prudent tax avoider” was prepared to pay 1% of income (plus tax) and the “luxurious rich” was prepared to pay 0.66% of income (plus tax) the same equivalence would hold. For those who are suspicious of contingent evaluations, ex post data could be used: the proportion of income that was actually spent on adding a spare bedroom by the two cohorts.

In an extreme case where, on average, the 500,001st dollar yielded one quarter of the utility than the 20,001st dollar, a powerful implication would follow. The loss of utility inflicted on the “luxurious rich” by the $0.80 tax per consumed dollar is exactly identical to the loss of utility inflicted on the “prudent tax avoider” by the $0.20 tax per consumed dollar (the Paradox of Flat Progressivity). Even in less extreme cases, CUTS would cut the tax-induced loss of utility by a factor that is proxy-measurable.

The invisible hand of consumption taxation

11. Taxation ceases to be a compulsory levy on (generally) socially worthwhile activities (such as work) and becomes entirely a voluntary donation (a consequence of the choice to consume above a certain level).xxv

Classical and neoclassical economics were both constructed, in part, to restrain the coercive power of the State. In this tradition, market forces are generally perceived to be a superior social organizer than government coercion. Hence Milton Friedman (1999) described Adam Smith's “invisible hand” as offering “the possibility of cooperation without coercion”.

Smith provides two illustrations by which economic actors are “led by an invisible hand to promote an end which was no part of his intention”: the invisible hand of production and the invisible hand of consumption. The most famous reference is to the invisible hand of production.xxvi But Smith’s (1982 [1759] IV, i, 265) first published reference relates to the “invisible hand” of consumption. The rich are constrained in their ability to consume great quantities of “the necessaries of life” and are “led by an invisible hand” to provide employment and therefore to share “produce” with the poor and “thus without intending it, without knowing it, advance the interest of the society”.xxvii

CITS fits perfectly in this tradition: it is a method of removing the coercive element from tax collection. Smith (1982 [1759], IV.I.10) also described the “luxury and caprice” and “natural selfishness and rapacity” of the “proud and unfeeling” luxurious rich.xxviii Through the invisible hand of consumption they unwittingly pursue social goals. By pursuing private (consumption-derived) utility, they simultaneously – through an invisible hand of consumption taxation – assist the pursuit of a balanced budget.

The invisible hand of the “impartial spectator”

12. In The Theory of Moral Sentiments, Smith (1982 [1759], I, i, v, 26) highlights a private, internal struggle where “passions” (short-term gratification, long-term costs) may defeat the internal “impartial spectator” (the source of “self-denial, of self-government, of that command of the passions which subjects all the movements of our nature to what our own dignity and honour, and the propriety of our own conduct, require”).

There are themes in Smith’s writings that resonate with behavioral economists (Ashraf, Camerer and Loewenstein 2005). Sub-optimal levels of private saving, for example, can be attributed to the victory of the “passions” over the “impartial spectator”. CITS can therefore cooperate with the “impartial spectator” by providing an incentive structure to encourage savings. Thus there is “the possibility of cooperation without coercion” in situations where the invisible hand fails.

Reducing the incentive to evade

13. The voluntary nature of taxation reduces the incentive to evade. Moreover, whilst all tax systems are open to attempts at evasion, CITS provides an additional disincentive.

Current definitions of taxable income can be carried-over into CITS. Pre-tax savings vehicles account (PTSA) additions are deducted from income to derive consumed income. PTSA funds that are withdrawn are assumed to be consumed and therefore added to taxable income.

What would happen if non-PTSA assets were used to finance consumption (thus allowing a greater proportion of income to be saved)? These non-PTSA asset proceeds can be easily tracked and measured by the tax authorities and therefore would not present undue administrative difficulties or excessive exposure to evasion.xxix

But what if unregistered offshore assets were liquidated and consumed? Under-reporting non-PTSA income would, of course, be a crime; electronic transfer of unregistered funds may be traceable; and carrying cash across borders is also potentially detectable. But even if such evasion were successful, the evader would still pay a price: unregistered offshore assets would gradually be eliminated.

Increasing consumption through increased savings: the non-paradox of thrift

14. Increasing savings should increase future consumption/savings opportunities. Life cycle consumption functions assume that households consider the present value of lifetime income (not just the current flow of income). Thus a stream of income received over time {y0, y1, …, yT} must be discounted to derive the present value (pvy).

(4)

1.

The consumption/savings decision is based on the (subjective) trade-off between the utility gained from consumption today c0 and the expected utility associated with deferred consumption, c1+… + cT. Whilst a dollar of current consumption generates more utility than a (purchasing power preserved) dollar of future consumption, CITS operates in the reverse direction and thus nudges current consumption towards the deferred consumption (savings) category.

In a simplified world of stable purchasing power (no inflation) and no interest (nominal or real) paid on savings, the purchasing power of dollar would be constant, regardless of when it is applied to consumption. In the absence of a tax on consumption, c0 would be compared to cT by (subjectively) discounting cT.

But CITS alters this calculation. Suppose that for “the luxurious rich”, current consumption attracted a marginal tax of 80% and that this tax diminished per year of deferral (at say 5% per year of deferral or, in this example, 4 percentage points). Therefore a utility-maximizing agent would adjust the valuation of c0, c1+… + cT by adding the tax.

Thus the choice for “the luxurious rich” lies between a dollar of current consumption (costing $1.80) and a purchasing-power-preserved dollar of consumption (costing $1) in 20 years time

(with intermediate calculations for the intervening years). This provides an incentive for current consumption to fall and savings (and therefore future consumption) to rise.

Consumption (C) is influenced by both (the national income accounts definition of) income (Y) and financial wealth (W):

(5) C = b1Y + b2W

An increase in savings will increase future consumption possibilities when funds are subsequently withdrawn from PTSA for consumption purposes (and added to income). The rise in savings will also tend to increase financial wealth. Although CITS could be expected to reduce the marginal propensity to consume out of income (b1), the corresponding increase in financial wealth (W) would tend to offset the reduction somewhat.

The Paradox of Thrift asserts that an attempt to increase savings may be counterproductive: the corresponding fall in consumption may lower aggregate demand and income and thus lower aggregate savings. But CITS undermines whatever validity this paradox may have possessed. The Paradox of Thrift is no longer a paradox, but is instead part of Keynesian received opinion.xxx It should be replaced by the Non-Paradox of Thrift.

The tax-induced rise in savings (and the tax-induced fall in consumer expenditure) should lead to a two-fold increase in investment (via quantity and price effects). The quantity effect reflects the increased flow of savings-into-investment; the price effect reflects the increase in investment caused by the associated reduction in interest rates.

CITS reduces expenditure on consumer items (some imported) whilst facilitating an increase in capital per worker, productivity, real wages and income - and thus future consumption and savings opportunities.

The budget-balancing invisible hands of Veblen’s snobs

15. Twisting marginal taxes on consumed income to balance the budget produces some powerful results. The goods and services consumed by each tax cohort can be treated as a bundle with estimate-able price elasticities of demand.

If the demand for “luxurious rich” expenditures was price elastic, raising the marginal rate would, ceteris paribus, reduce aggregate expenditure and tax revenue on this tier bundle. This would increase the savings and thus – paradoxically - the wealth of the “luxurious rich”. A government which undertook this tax hike would be indulging in a “taste” for discrimination: a taste that will be paid for by the “prudent tax avoider” in the form of higher taxes.

If on the other hand, such “luxurious rich” expenditures were price inelastic, aggregate expenditure and tax revenue would, ceteris paribus, rise. But the “luxurious rich” would still be on their demand curves (they would still be engaging in utility maximizing behavior).

Bagwell and Bernheim (1996, 350) noted that “members of high classes voluntarily incur costs to differentiate themselves from members of the lower class (invidious comparison), knowing that these costs must be large enough to discourage imitation (pecuniary emulation)”. If commodities in the “luxurious rich” bundle were Veblen goods (where quality is perceived to be a function of price), the tax-driven rise in price would tend to increase demand and thus tax revenue.xxxi In this Veblen world there tends to be an obsession with nth hand financial instruments; but wearing 2nd hand clothes would lead to Exit. Veblen’s snobs - those who visibly display their status through the conspicuous consumption of manicured nails, diamond ringed fingers and designer wrist watches - would be led by an invisible hand to assist in the process of balancing the budget.

Concluding Case

Dysfunctional tariff policy exacerbated the Great Depression and thus contributed to the Second World War. Since then politicians have gradually surrendered the revenue and patronage of tariff walls. The dysfunctional monetary policy of the 1960s and 1970s created the Great Inflation and the pain of the subsequent Great Disinflation. Economists began to insist on politically uncontaminated monetary policy (through inflation targets and more independent for central banks). In the 1990s, politicians surrendered most if not all of their remaining power to abuse monetary policy for re-election purposes.

One economist, later Governor of the Bank of Italy (1945) and President of the Italian Republic (1948), advocated the same approach towards fiscal policy: “a system of taxation, coordinated by a single principle, immune from all the contaminations that can result from the contingencies of the moment, from class or particular interests or from that factor of such great importance in this field, the ‘fantasy’ of the lawmaker stimulated by the urgent needs of the treasury” (Einaudi 2006 [1928-9], 190). A government which phased in CITS would generate short term anxiety from those fearful of change, but long term economic and electoral benefits.

Macroeconomic outcomes are a function of macroeconomic structures. Fiscal, monetary and trade policy have, at times, been a Devil’s Triangle for macroeconomic outcomes. In the last two thirds of a century, politicians have twice embraced the public interest (bringing down tariffs walls and decontaminating monetary policy). In the next third of a century, can they also be persuaded to take the fiscal high ground?

Bibliography

Altig, D. Auerback, A. Kotlikoff, L. Smetters, K. and Walliser, J. 1997. Simulating U.S. Tax Reform. NBER Working Paper Series vol w6248.

Arrow, K. 1997. Invaluable Commodities. Journal of Economic Literature June XXXV: 757-765.

Ashraf, N., Camerer, C.F. and Loewenstein, G. 2005. Adam Smith, Behavioral Economist. Journal of Economic Perspectives 19.3 Summer: 131–145. Auerback, A. 2005. A Consumption Tax. Wall Street Journal August 25. Bagwell, L. S. and Bernheim, B. D. 1996. Veblen Effects in a Theory of Conspicuous Consumption. AER 86.3, June: 349-373.

Bernartzi, S. and Thaler, R. H. 2004. Save More Tomorrow: Using Behavioral Economics in Increase Employee Savings. Journal of Political Economy 112 (1): S164-S187.

Benartzi, S. and Richard H. Thaler, R. T. 2007. Heuristics and Biases in Retirement Savings Behavior Journal of Economic Perspectives Volume 21, Number 3 Summer: 81–104

Bentham, J. 1907 [1823]. An Introduction to the Principles of Morals and Legislation. Oxford: Clarendon Press. Bernoulli, D. 1954. Exposition of a New Measurement of Risk. Econometrica 22 (1): 22–36.

Bernheim, D., Ray, D. and Yeltekin, S. 1999. Self-control, saving and the low asset trap. Unpublished working paper. Einaudi, L. 2006. Luigi Einaudi Selected Economic Essays. New York: Palgrave Macmillan. Edited by Einaudi, L. Faucci, R. and Marchohionatti, R.

Hall, R. and Rabuska, A. 2007. The Flat Tax. Stanford, CA: Hoover Press.

Fisher, I. 1906. The Nature of Capital and Income. London: Macmillan.

Fisher, I. 1937. Income in Theory and Income Taxation in Practice. Econometrica January, 5. 1: 1-55.

Fisher, I. 1939. The Double Taxation of Savings. American Economic Review March 29.1: 16-33.

Fisher, I. and Fisher H. 1942. Constructive Income Tax: A Proposal for Reform. New York. Harper and Brothers.

Frank, R. 2000. Luxury Fever: Why Money Fails to Satisfy in an Era of Success. New York: The Free Press.

Friedman, M. 1943. The Spending Tax as a War Time Fiscal Measure. American Economic Review March 33.1: 50-62

Friedman, M. 1948. A Monetary and Fiscal Framework for Economic Stability. American Economic Review XXXVII, 3, June: 245-264.

Friedman, M. 1999. Introduction. I, Pencil: My Family Tree as told to Leonard E. Read. http://www.econlib.org/library/Essays/rdPncl0.html

Hobbes, T. 1651. Leviathan. http://oregonstate.edu/instruct/phl302/texts/hobbes/leviathan-a.html

Hutcheson, F. 2004 [1726]. An Inquiry into the Original of Our Ideas of Beauty and Virtue in Two Treatises. ed. Wolfgang Leidhold. Indianapolis: Liberty Fund. Chapter

Accessed from http://oll.libertyfund.org/title/858/65996/1608170 on 2010-07-30.

Institute of Fiscal Studies. 1978. The Structure and Reform of Direct Taxation. London: Institute of Fiscal Studies. George Allen and Unwin.

Kaldor, N. 1955. An Expenditure Tax. London: George Allen and Unwin.

Hayek, F.A. 1991. The Fatal Conceit: the Errors of Socialism Volume 3. Chicago: University of Chicago Press.

Lasch, C. 1979. The Culture of Narcissism: American Life in an Age of Diminishing Expectations. New York: W.W. Norton. Marx, K. 1921 [1867]. Capital: a critique of political economy, Volume 1. The Process of Capitalist Production. Chicago: Charles H. Kerr. Meade, J. 1978. Preface. In Institute of Fiscal Studies. 1978. The Structure and Reform of Direct Taxation. London: Institute of Fiscal Studies. George Allen and Unwin.

Mill, J. S. 1884. Principles of Political Economy with some of their Applications to Social Philosophy. London: Parker, Son and Bourne.

Robinson, J. R. 1962. Review of H.G. Johnson's Money, Trade and Economic Growth. Economic Journal September, LXXII, 287: 690-2.

Simons, H. 1938. Personal Income Taxation the Definition of Income as a Problem of Fiscal Policy. Chicago: University of Chicago Press.

Skinner, J. 2007. Are You Sure You’re Saving Enough for Retirement? Journal of Economic Perspectives. Volume 21, Number 3 Summer: 59–80

Smith, A. 1981 [1776]. Glasgow edition of the Works and Correspondence Volume 2a An Inquiry Into The Nature and Causes of the Wealth of Nations. Indianapolis: Liberty Fund.

Smith, A. 1982 [1759]. Glasgow edition of the Works and Correspondence Volume 1 Theory of Moral Sentiments. Indianapolis: Liberty Fund.

Tawney, R. H. 1920. The Acquisitive Society. London: Fabian Society.

Thaler, R. 2007. Mortgages Made Simple. New York Times 5 July.

http://www.nytimes.com/2009/07/05/business/economy/05view.html

U.S. Treasury. 1977. Blueprints for Basic Tax Reform.

http://www.ustreas.gov/offices/tax-policy/library/blueprints/

Veblen, T. 1899. Theory of the Leisure Class: An Economic Study in the Evolution of Institutions. New York: Macmillan.

Whybrow, P. 2005. American Mania: When More Is Not Enough. New York: WW Norton.

Notes

i This paper has been improved by comments provided by Allan Meltzer, David Laidler and seminar participants at the Kansas City Federal Reserve, the Reserve Bank of Australia, the University of Western Australia, Chico State University, the University of Missouri Kansas City and the 2009 Finance, Economics, Marketing and Accounting Centre conference. ii Friedman (1948, 248, 250) proposed three additional discretion-restraining rules (two fiscal, one monetary). First, “No attempt should be made to vary expenditures, either directly or inversely, in response to cyclical fluctuation in business activity” and second “Government would not issue interest-bearing securities to the public; the Federal Reserve System would not operate in the open market”. Eliminating bond-financed expenditure leads to Friedman’s (1948, 251) deficit-surplus-counter-cyclical monetary rule: “Deficits or surpluses in the government budget would be reflected dollar for dollar in changes in the quantity of money”. Five years previously, Friedman (1943) supported the ‘Spending Tax as a War Time Fiscal Measure’ concluding that it was “administratively feasible”; the 1948 system invoked the income tax. By the early 1950s, Friedman replaced the deficit-surplus-counter-cyclical monetary rule with the constant growth (k%) rule.

iii Governments can also malevolently consume household savings and use these funds to bolster the capital adequacy of banks (a Basle Fawlty Accord) and lend (at low interest) to reckless banks who then buy interest-bearing government bonds (a reverse Ponzi scheme).

iv CITS can be seen as a tax-based war on future poverty and future government deficits.

v Since China exports their savings they could also export their incentive structure: capital punishment for financial criminals. A knee-jerk reaction at the other extreme seeks to initiate a lawyer-based recovery (by imposing further static regulations on the dynamic lawyer-hiring-

regulation-avoiding industry). The intergenerational Okun externality tax is a compromise measure (the loss of output caused by a financial crisis is recovered by tracing the fingerprint trail and putting a lien on the future earnings of all ‘Financial Mayflower’ descendants).

vi According to a 1940s University of Chicago graduate student skit, Rational Economic Man, when asked “How much would you charge to kill your grandmother”, replied “Do I have the right to dispose of the remains?” (Arrow 1997, 760, n3). vii This paper does not discuss lifetime utility maximization through political markets. viii See also Thaler (2007). http://www.nytimes.com/2009/07/05/business/economy/05view.html ix One sect of Homo Macroeconomicus - the ISLMPC fundamentalists - add a version of the Phillips Curve to the IS/LM model. Nominal national income (Y) divided by the money supply (M) equals, by definition, the velocity of money (V); and Y, by definition, equals real income (y) multiplied by the price level (P). M and P are closely connected (most economists believe that changes in M cause changes in P). This leads to a non-existent world in which it is possible to, first, cut in half and then double P whilst holding M constant. Since Y = MV = Py, there are only two ways of achieving this gravity-defying feat. First, by holding Y constant and forcing real income (y) to double or to be cut in half. Or second, to compensate for the doubling of P, V must be doubled (by subsidizing every transaction?) and then be cut in half (by taxing every transaction?) when P is cut in half. Either way, the Aggregate Demand curve comes into the world dripping from head to foot with nonsense.

x Joan Robinson (1962) famously described the Keynesian Neoclassical Synthesis as a “bastard Keynesian” species; Homo Economicus has been “working like a bastard” for his Neoclassical landlords. However, behavioral economists believe there is another, more legitimate, child of Adam Smith (Ashraf, Camerer and Loewenstein 2005).

xi With apologies to B. Douglas Bernheim, Debraj Ray and Sevin Yeltekin (1999), such agents can be seen as being stuck in what might impolitely be called a “fat tail, fat ass, low asset trap”. xii For example, the Save More Tomorrow (SMarT) program involved the offer of a retirement savings plan in which employees commit in advance to save a portion of future salary increases. 78 percent of those offered the plan joined; 80% of those enrolled stuck with the program through the fourth pay raise; in 40 months, the average saving rates for program participants increased from 3.5 percent to 13.6 percent (Bernartzi and Thaler 2004; see also ).

xiii Mill argued before a Parliamentary Committee that “what I would lay down as a perfectly unexceptional and just principle of income tax, if it were capable of being practically realized, would be to exempt all savings” (cited by Fisher and Fisher 1942, 218). Mill (1884, 179) also argued that “the proper mode of assessing an income tax would be to tax only the part of income devoted to expenditure, exempting that which is saved. For when saved and invested (and all

savings, speaking generally, are invested) it thenceforth pays income tax on the interest or profit which it brings, notwithstanding that it has already been taxed on the principal. Unless, therefore, savings are exempted from income tax, the contributors are taxed twice on what they save, and only once on what they spend”. Fisher (1906; 1939) also elaborated on this double taxation argument.

xiv Consumption is “a stopping place among the sequence of economic relations. Consumption is a destruction, a using-up and end” (Simons 1938, 89). xv As Thomas Hobbes (1651, 226) noted, “what reason is there, that he which laboureth much, and sparing the fruits of his labour, consumeth little, should be more charged, than he that living idly, getting little, and spendeth all he gets …”. xvi “Surplus-value and the rate of surplus-value are ... the invisible essence to be investigated, whereas the rate of profit and hence the form of surplus-value as profit are visible surface phenomena" (Marx 1921 [1867], 834).

xvii That is, the workers’ unpaid labor and output. xviii Through the associated antagonistic roles for employers and employees - people who would otherwise live in harmony. xix http://www.taxfoundation.org/taxfreedomday/

xx “Virtue is as the Quantity of the Happiness, or natural Good; or that the Virtue is in a compound Ratio of the Quantity of Good, and Number of Enjoyers. In the same manner, the moral Evil, or Vice, is as the Degree of Misery, and Number of Sufferers; so that, that Action is best, which procures the greatest Happiness for the greatest Numbers; and that, worst, which, in like manner, occasions Misery” [emphases in text] (Hutcheson (2004 [1726], section 3, 37, VIII). Daniel Bernoulli (1738 [1954]) also argued that the “utility resulting from any small increase in wealth will be inversely proportionate to the quantity of goods previously possessed [emphases in text].”

xxi Referring to the “question of sacrificing a few lives in order to serve a larger number elsewhere”, Friedrich Hayek concluded in The Fatal Conceit: the Errors of Socialism (1988) that “even if we do not like to face the fact, we constantly have to make such decisions … When the army surgeon after a battle engages in ‘triage’ – when he lets one die who might be saved, because in the time he would have to devote to saving him he could save three other lives – he is acting on a calculus of lives”.

xxii “The luxuries and vanities of life occasion the principal expense of the rich, and a magnificent house embellishes and sets off to the best advantage all the other luxuries and vanities which they possess. A tax upon house-rents, therefore, would in general fall heaviest upon the rich; and

in this sort of inequality there would not, perhaps, be anything very unreasonable. It is not very unreasonable that the rich should contribute to the public expense, not only in proportion to their revenue, but something more than in that proportion” (Smith 1981 [1776], book 5, chapter 2).

xxiii For the Flat Tax argument see Hall and Rabuska 2007. xxiv If the efficient market hypothesis is correct, financial services ‘servants’ would fall into this luxury category also.

xxv Tax rebels (such as Henry David Thoreau and Mahatma Gandhi) could thus legally avoid paying taxes to fund activities (such as wars) of which they disapproved.

xxvi “It is not from the benevolence of the butcher, the brewer or the baker, that we expect our dinner, but from their regard to their own self interest. We address ourselves, not to their humanity but to their self-love, and never talk to them of our own necessities but of their advantages” (Smith 1981 [1776] I.ii.2). xxvii “They consume little more than the poor, and in spite of their natural selfishness and rapacity, though they mean only their own conveniency, though the sole end which they propose from the labours of all the thousands whom they employ, be the gratification of their own vain and insatiable desires, they divide with the poor the produce of all their improvements. They are led by an invisible hand to make nearly the same distribution of the necessaries of life, which would have been made, had the earth been divided into equal portions among all its inhabitants, and thus without intending it, without knowing it, advance the interest of the society, and afford means to the multiplication of the species” (Smith 1982 [1759]).

xxviii Landlords in pre-industrial Britain. xxix Existing tax systems capture capital gains and interest payments. For example, in many countries capital gains on certain assets, when realized, are added to taxable income (sometimes discounted if the asset has been held for more than a specified period). Interest paid on bank accounts is usually taxable and the (non-declared) run-down of balances to finance consumption could also be tracked.

xxx A paradox is a statement that is seemingly contradictory, opposed to common sense, or a tenet contrary to received opinion. xxxi There has been a long tradition of both scorn (e.g. Veblen 1899) and concern (e.g. Tawney 1920; Frank 2000) about top-end consumption patterns (see also Whybrow 2005; Lasch 1979). Raising CITS upper end marginal rates tackles the issue directly. Either consumption would fall (presumably benefiting the afflicted or “mania” individuals), or tax revenue would rise (a Veblen-induced trickle-down tax benefit for lower expenditure cohorts).

Appendix 1

The Retreat of Arbitrary Taxation and the Advance of Democracy

The advance of democratic institutions is a parallel history of the retreat of arbitrary taxation. Five episodes will illustrate the theme of the non-elected (Monarchs, Lords and tax farmers) being obliged to curtain or surrender their power to indulge in arbitrary taxation.

First, the 1215 Magna Carta forced an English King to accept constraints on (amongst other things) his arbitrary power to tax. King John I required resources for military campaigns to recapture the “lost” French territories (Normandy in particular). His “subjects” resented the taxes imposed (including a tax on income and a tax in lieu of military service). Although primarily of symbolic value, it was, nevertheless, a formal statement of principle: a government (in this case a monarchy) was bound by the rule of law.

Second, Charles I’s attempt to levy “ship money” without the authority of parliament was refused - on principle - by John Hampden, a wealthy landowner. Although Hampden lost his legal case, and ship money continued to be levied, the opposition to non-parliamentary taxation intensified, and contributed to the English Civil War (which resulted in the decapitation of the King).

Third, the American Declaration of Independence was, in large part, a revolt against taxation without representation. Article I of the resulting U.S. Constitution vested all legislative power in Congress: all revenue-raising bills must originate in the elected chamber (the House of Representatives).i

Fourth, on the eve of French revolution, the term “taillable” (taxpayer) was, for a nobleman, an insult: only the lower orders paid tax (taille); the upper orders were routinely granted tax exemptions. The revolution led to the decapitation not only of a King (Louis XVI) but also of twenty eight Tax Farmers (Ferme générale). The privatization of tax collection dates back at least as far as Roman times: agents paid the state a specified sum in advance in return for the liberty to extract resources from “subjects”. Such an abuse-prone tax system was clearly suboptimal for “subjects”: in this case it proved sub-optimal for collectors also.

The fifth episode relates to the final surrender of fiscal power by the (unelected) British House of Lords to the (elected) House of Commons. Simultaneously, two fiscal traditions were threatened: first, the tradition of not interfering with House of Commons finance bills; second, the Free Trade consensus which had dominated British politics since the 1846 repeal of the Corn Laws. The second assault was part of the jingoistic atmosphere that led to World War One.

Having lost one empire (the 13 American colonies), the British built a second. At the beginning of the twentieth century moves were made to establish a single British Empire trading block

(“Imperial Preference”) protected by high tariff walls to counteract the growing power of the U.S and Germany. The tariff revenue raised was designed to fund an expanding welfare state.

Joseph Chamberlin was the dominant political force behind Imperial Preference – backed by the Tariff Reform League (founded in 1903).ii In 1917, elements of the Tariff Reform League formed the National Party, which was based on both xenophobia (closing German banks and businesses, the internment of enemy aliens and counter air-raids against German towns) and patriotism: "if you wish for a patriotic race, you must aim at a contented people, reared under healthy conditions...and with full scope for advancement". This “tax-the-foreigner” fiscal policy had a post war fiscal sequel in a promise to “squeeze the German lemon until the pips squeak!”iii Such fiscal sentiments – which launched Keynes’ (1919) polemical career - led to hyperinflation, the near-destruction of the German middle class, the rise of the Nazis and World War Two.

Before World War One, Joseph Chamberlin promised that “Tariff Reform Means Work for All”. Free Trade, he argued, threatened British industry: "sugar is gone; silk has gone; iron is threatened; wool is threatened; cotton will go! How long are you going to stand it? At the present moment these industries…are like sheep in a field.”

In contrast, the Liberal party leader, Henry Campbell-Bannerman, declared that the fight for Free Trade was a fight “against those powers, privileges, injustices, and monopolies which are unalterably opposed to the triumph of democratic principles”. Taxes were “the plaything of the tariff reformer”.

Imperial Preference split the Conservatives and the Liberals won the 1906 election in a landslide. In 1908 Asquith succeeded Cambell Bannerman as PM. Asquith’s government passed "New Liberal" legislation, setting up unemployment insurance and old age pensions. To pay for the new welfare expenditure (plus the mounting costs of the pre-war arms race), in 1909, Chancellor David Lloyd George produced an intentionally provocative "People's Budget". In language that President Lyndon Johnson used half a century later, Lloyd George declared that “This is a war Budget. It is for raising money to wage implacable warfare against poverty and squalidness”. Death duties were increased as were taxes on luxuries, alcohol and tobacco and upper level income. A land tax was also proposed.

Having been defeated at the polls, the Conservatives used their majority in the House of Lords to veto the budget. Amid a constitutional crisis, the Liberal government proposed to reduce the power of the Lords at the subsequent general election (January 1910). Following a second general election (December 1910), the Lords passed the 1911 Parliament Act which codified the supremacy of the House of Commons by limiting the legislation-blocking powers of the Lords and imposing a maximum legislative delay of one month for tax or “money bills” as they were known. In compensation, the Lords were able to squash the proposed land tax.

So as American bankers (1908-13) were constructing a monetary system which would consolidate their power (through the Federal Reserve System), British Lords finally surrendered their fiscal power (1909-11).

Appendix 2

Current Hybrid Tax Systems

Like the financial system, existing tax systems have not generally been “designed” in accordance with socially optimal principles. Tax breaks, for example, to facilitate social stability through the construction of a “property owning democracy” can distort entrepreneurial incentives, exacerbate bubbles and thus undermine economic stability. Likewise, the notorious 1930 Smoot-Hawley Tariff Act began as an attempt to provide protection and thus assistance to the struggling U.S. farm sector but was rapidly expanded to include other special interest groups.

This beggar-thy-neighbor policy provoked foreign retaliatory measures. It became widely recognized that this misplaced search for social and economic stability for farmers contributed to the dislocation of the inter-war period.iv

The U.S. government was initially highly dependent on revenue from tariffs. After the Second World War, tariffs reduced in significance both as a source of government revenue and as a social engineering vehicle.v Thus “the income earner” replaced “the foreigner” as a source of government funding.

Income taxes were often first introduced as emergency war time measures (1798 in the U.K., 1861 in the U.S.); the Sixteenth Amendment (1913) to the U.S. constitution provided a legal justification. But according to two Stanford economists there was “profound discontent” with the tax acts that followed (Canning and Nelson 1934, 28, 31).vi

Economists typically oppose tariffs. Likewise, many economists oppose the income tax (where income is not defined to exclude savings) and have instead proposed variants of the CIT: including Thomas Hobbes (1651, 226), John Stuart Mill (1884), Irving Fisher (1906; 1937; 1939; Fisher and Fisher 1942), Luigi Einaudi (2006 [1928-9], chapters 14, 15 and 16), Milton Friedman (1943), Nicholas Kaldor (1955) and James Meade (1978).

CITS has served as “a high-voltage shock treatment to established thinking” (Musgrove 1957, 205). It is also an unimpeachable framework which has gained an apparently permanent but, so far, only partial grip on the policy apparatus.

A Yale tax economist, Thomas S. Adams, commended the concept to Ogden Livingstone Mills (1921, 331), President of the New York State Tax Association (Fisher 1937, 42). Four months after taking his seat in the U.S. House of Representatives, Mills introduced a “Spendings Tax” bill (H.R. 7867; July 20th 1921). Mills declared that “existing tax evils cannot be cured without a major operation. The country expects one. It will not be satisfied with timid tinkering” (New

York Times July 22 1921). Fisher (1937, 42) described Mills’ bill as an almost perfect embodiment of his own proposal: coming “nearer to a true income-tax bill proposal than any other bill hitherto introduced” (see also Fisher and Fisher 1942; Fisher 1939, 16-17; Friedman 1943, 61, n12).vii In September 1942, the U.S. Treasury proposed to finance the war with CITS (Kaldor 1955, 13). This ‘Spending Tax as a War Time Fiscal Measure’ was supported by Milton Friedman (1943) who concluded that it was “administratively feasible” (see also Poole 1943).

World War Two ended the Great Depression; the Vietnam War initiated the Great Inflation. The Vietnam War period and its aftermath was a low point for both fiscal and monetary policy outcomes (both of which became highly politicized and thus sub-optimal). With respect to monetary policy, Fed Chair Arthur Burns was in danger of joining Richard Nixon’s “enemies list”. According to the White House transcripts, Nixon, was concerned that Burns was not stoking up the economy sufficiently to assist his 1972 re-election chances. Amid references to Burns’ religion (he is “talking to the Jewish press”), Nixon threatened that “war is going to be declared if he doesn't come round some” (cited by Abrams 2006).

Burns responded to these pressures in conversations with Nixon captured on the White House tapes: “I am a dedicated man to serve the health and strength of our national economy and I have done everything in my power, as I see it, to help you as president, your reputation and standing in American life and history. I’ve never seen a conflict between the two, but I want you to know this … the moment a conflict arises, I’m going to be right here. I’ll tell you about it, and we’ll talk about it and try to decide where to go next” (March 1971). The pressure continued, forcing Burns to protest: “No one has tried harder to help you” (June 1971). In December 1971, Nixon continued to hector Burns about money supply growth: “get it up!” (cited by Meltzer 2009, 635, 793, 796).

In January 1972, Nixon supplemented these conversations with a letter to the Fed Chair referring to Burns’ “absolute assurance that the money supply will move adequately to fuel an expanding economy in 1972 … What could happen out of all of this is that a major attack on the independence of the Fed will eventually develop” (cited by Meltzer 2009, 800).

As monetary policy became increasingly politically contaminated, so too did fiscal policy. The reconstruction of fiscal-deficit-ridden Britain in the 1970s would, it was hoped, be facilitated by “taxing the rich until the pips squeak”. Although Labour Chancellor Denis Healey did not actually use that evocative phrase he did promise to “squeeze property speculators until the pips squeak” whilst warning “that there are going to be howls of anguish from those rich enough to pay over 75% on their last slice of earnings". In the mid-1970s, the highest marginal rate of British income tax was lifted to 98% (83% without the investment income surcharge).

Fiscal dysfunction revived interest in CITS: another revolt of economics against politics. CITS continued to receive largely favourable attention: from the 1972 Swedish Government Commission on Taxation (Lodin 1978), the U.S. Treasury’s 1977 Blueprints for Basic Tax

Reform, the Institute of Fiscal Studies’ 1978 Structure and Reform of Direct Taxation (chaired by James Meade)viii plus a 1978 Brookings Institution conference (Pechman 1980). The U.S. Treasury’s report began from the same starting point as earlier analyses: “There has been increasingly widespread dissatisfaction in the United States with the Federal tax system” (Blueprints for Basic Tax Reform 1977, 1).ix

The “tax payer’s revolt” that fuelled the Thatcher-Reagan revolutions also led to a switch in the tax emphasis away from income towards consumption. Rising inflation, in the absence of indexation, increased the tax burden (bracket creep) and created further discontent. In 1979, the Thatcher government lifted the VAT to 15% while making substantial cuts in marginal income tax rates (the highest marginal rate was 40% by 1988). In the U.S., only in four years of the two decades between 1944-63 was the top marginal federal income tax rate below 91%. The 1981 Economic Recovery Tax Act was the largest income tax cut in US history: the top federal income tax bracket fell to to 50% (1982-86) and to 28% for 1988.

But in the U.S. the policy pendulum swung to-and-fro with respect to consumption taxes. First, tax-privileged Individual Retirement Accounts (IRAs) were established (shifting the tax emphasis towards consumption and away from income); but in 1986 significant new restrictions were placed on their use. In 1993, more purpose-specific saving vehicles were offered (Medical Savings Accounts, the Roth IRA, an Education IRA and the Section 529 Qualified Tuition Program).

Thus, several piecemeal CITS components already exist. VAT, the GST and sales taxes are CITS-type arrangements – with regressive, or at least non-progressive, features,x - and numerous tax-privileged savings accounts are now widely available. Singapore has perhaps gone the furthest with the Central Provident Fund (CPF) whereby 34.5% of private sector wages (for workers aged below 50) are channeled into compulsory savings accounts. Attempts at reform have continued elsewhere: in the U.S., for example, in the 1990s, Senators Sam Nunn (R- New Mexico) and Pete Domenici (D- Georgia) proposed the Unlimited Savings Account (USA) Tax bill (Seidman 1997).

Yet the conclusions drawn by an earlier generation retain their validity: these piecemeal components do “not reflect any consistent philosophy about the objectives of the system” (Blueprints for Basic Tax Reform 1977, 1); instead we have “an unsystematic mixture of elements” (Structure and Reform of Direct Taxation 1978, 499).

i Initially, Senators were not elected: "The Senate of the United States shall be composed of two senators from each state, chosen by the legislature thereof, for six years; and each senator shall have one vote" (Article I, Section 3, U.S. Constitution). The Seventeenth Amendment to the

U.S. Constitution established direct election of Senators by popular vote (adopted on April 8, 1913). ii The Tariff Reform League was founded by Sir Cyril Arthur Pearson (the founder of the Daily Express), Harry Brittain (who worked on the staff of two of Pearson's papers, The Standard and Evening Standard) and Henry Page Croft.

iii This promise (or threat) was made by Eric Geddes, a British cabinet minister.

iv In spring 1930, a petition drafted by Claire Wilcox and Paul Douglas of Swarthmore College was circulated (largely at Irving Fisher’s expense) to members of the American Economic Association (AEA). Of the 2,500 or so AEA members, 1,028 signed the petition, including most of the leading American economists. Wilcox delivered a copy of the text and signatures to President Hoover, Senator Reed Smoot (R, Utah, Chair Senate Finance) and Representative Willis Hawley (R, Oregon, Chair House Ways and Means) and it was also published in the New York Times. Senator Pat Harrison had the statement and the list of signers read into the Congressional Record of May 5 1930 (Fetter 1942; Douglas 1972, 71). The 1930 Tariff Act passed the Senate by a vote of 44 to 42 (June 13, 1930) and the House the following day by a vote of 245 to 177 (largely on party lines). Hoover signed Smoot-Hawley bill into law on June 17, 1930.

v Nomenclature reflected this intellectual revolution. In the 1970s, the U.S. Tariff Commission (established 1916) became the International Trade Commission. Between 1974 and 1998, the Australian Tariff Board morphed into the Productivity Commission (via the Industries Assistance Commission and the Industry Commission).