The BHF Southern African Conference 22-25 July’07 Sun City Health Sector Reform in South Africa ~...

40

The BHF Southern African Conference 22-25 July’07 Sun City S q u arin g th e C ircle S q u arin g th e C ircle Health Sector Reform in South Africa ~ focus on the ‘Supply Side’ issues Dr Brian Ruff MB.BCh.; FCP (SA)

-

Upload

beverly-benson -

Category

Documents

-

view

214 -

download

0

Transcript of The BHF Southern African Conference 22-25 July’07 Sun City Health Sector Reform in South Africa ~...

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Health Sector Reform in South Africa

~ focus on the ‘Supply Side’ issuesDr Brian Ruff MB.BCh.; FCP (SA)

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Agenda

• Introduction to health sector reform• Supply side issues• Possible responses ~ reform experiences

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Agenda

• Introduction to health sector reform• Supply side issues• Possible responses ~ reform experiences

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Intro: Health Sector value

3 critical measures:• Access:• Equity:• Efficiency:

For society, there are always trade offs between these.Economics 101: Demand: control varies from being in individual consumers hands or may

be concentrated in organisation or state hands

Supply: of services is either private / independent or by the state

This paper explores these variables in regard to the SA private health sector.

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle Definitions:• Access: ability of a sick person to gain entrée to the system to

establish a diagnosis & plan therapy. Also the ability to move between differing levels of the system i.e. primary care to specialist / highly specialised care. Funding is critical.

• Equity: provision of the same care based purely on their medical problem – unaffected by income or influence.

Success is achieved when the demand side is controlled by structures / processes ensure effective demand. I.e.:

• Unnecessary care is denied (3rd party funding issue) • Necessary care is provided (both supplier induced demand,

and denial of care is avoided) Evaluation at an individual level is required.

Intro: Health Sector value

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Efficiency: two definitions concern us:• financial efficiency i.e. relative cost / price

• quality

They may be combined as ‘value’.

On the Supply side, there are:• ‘trade offs’ between cost and quality• but in healthcare, over time, good quality is more cost

effective than bad quality, since unresolved problems recur and incur new costs

Intro: Health Sector value

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

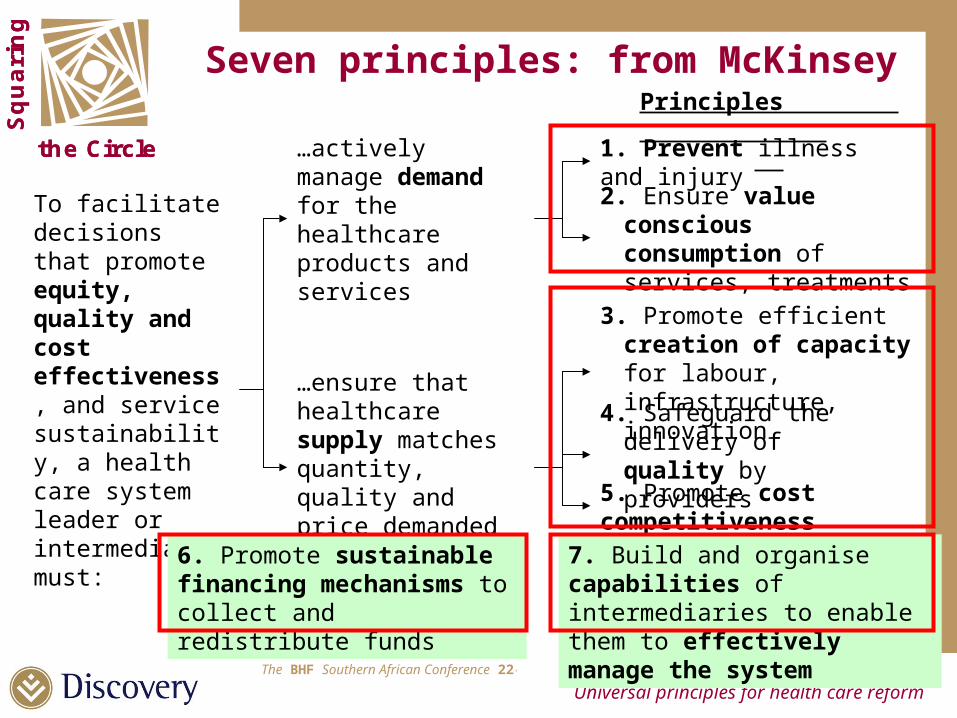

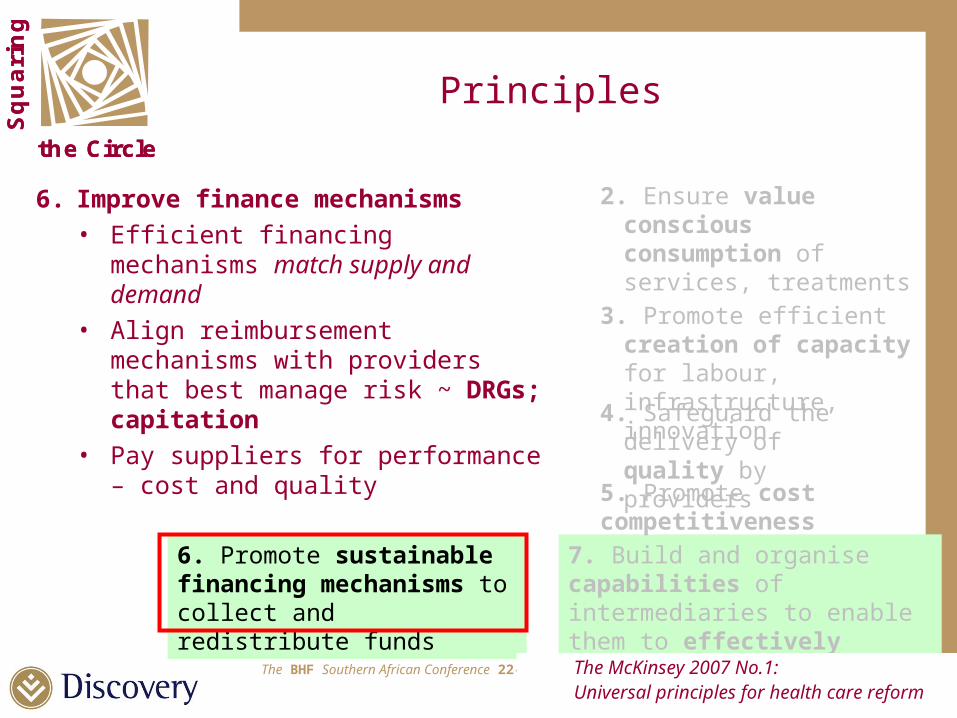

Seven principles: from McKinsey

The McKinsey 2007 No.1: Universal principles for health care reform

To facilitate decisions that promote equity, quality and cost effectiveness, and service sustainability, a health care system leader or intermediary must:

…actively manage demand for the healthcare products and services

…ensure that healthcare supply matches quantity, quality and price demanded by the market

Principles

6. Promote sustainable financing mechanisms to collect and redistribute funds

7. Build and organise capabilities of intermediaries to enable them to effectively manage the system

1. Prevent illness and injury

2. Ensure value conscious consumption of services, treatments

3. Promote efficient creation of capacity for labour, infrastructure, innovation

4. Safeguard the delivery of quality by providers

5. Promote cost competitiveness

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Principles

Demand:

1. Prevent illness and injury:• Promote wellness and safety

2. Value conscious consumption:• Information / flexibility: support rational

choice ~ current transparency re price and quality not sufficient

• Overcome 3rd party funding problem by increase consumer accountability

7. Build and organise capabilities of intermediaries to enable them to effectively manage the system

2. Ensure value conscious consumption of services, treatments

3. Promote efficient creation of capacity for labour, infrastructure, innovation

4. Safeguard the delivery of quality by providers

5. Promote cost competitiveness

6. Promote sustainable financing mechanisms to collect and redistribute funds

The McKinsey 2007 No.1: Universal principles for health care reform

1. Prevent illness and injury

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Principles:

Supply:

3. Analyze capacity ~ under / over?• Physical capacity and capital• Skills & labour supply• Technology

4. Quality of suppliers:• Clinical practice standards• Available information re organisational

performance• Risk based monitoring & audits, including

supplier self reporting5. Cost competitiveness:

• Enhance productivity (but not by excess capacity & over servicing)

• Purchase effectively

7. Build and organise capabilities of intermediaries to enable them to effectively manage the system

2. Ensure value conscious consumption of services, treatments

3. Promote efficient creation of capacity for labour, infrastructure, innovation

4. Safeguard the delivery of quality by providers

5. Promote cost competitiveness

The McKinsey 2007 No.1: Universal principles for health care reform

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Principles

6. Improve finance mechanisms• Efficient financing mechanisms match

supply and demand• Align reimbursement mechanisms with

providers that best manage risk ~ DRGs; capitation

• Pay suppliers for performance – cost and quality

7. Build and organise capabilities of intermediaries to enable them to effectively manage the system

2. Ensure value conscious consumption of services, treatments

3. Promote efficient creation of capacity for labour, infrastructure, innovation

4. Safeguard the delivery of quality by providers

5. Promote cost competitiveness

6. Promote sustainable financing mechanisms to collect and redistribute funds

The McKinsey 2007 No.1: Universal principles for health care reform

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Principles

7. Implementation:

• Build awareness – align consumer

and supplier interests; or• Provide financial incentives –

assumes non alignment; or• Impose mandates - if awareness

and incentives fail

7. Build and organise capabilities of intermediaries to enable them to effectively manage the system

2. Ensure value conscious consumption of services, treatments

3. Promote efficient creation of capacity for labour, infrastructure, innovation

4. Safeguard the delivery of quality by providers

5. Promote cost competitiveness

6. Promote sustainable financing mechanisms to collect and redistribute funds

consumerism

incentives

regulation

consumerism

incentives

regulation

More nuanced view….

The McKinsey 2007 No.1: Universal principles for health care reform

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Agenda

• Introduction to health sector reform• Supply side issues• Possible responses ~ reform experiences

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

GDP PPP $5 000 - $10 000

0

1

1

2

2

3

3

4

4

5

5

Méx

ico

Colom

bia

Alger

ia

Mal

aysi

a

Venez

uela

Turkey

Brazil

South A

frica

Uruguay

Poland

Russia

0

1

2

3

4

5

6

7

8

9

10GPs per 1000 people

Specialists per 1,000 people

Beds used per 1000 people

SA supply / 1000 population:

GP: 0.34

Specialists: 0.15

Beds used: 2.8

Discovery research: Monitor database

Low versus peers

CountryMedical

GraduatesSouth Africa 2.86Mexico 3.77Columbia 5.50Turkey 7.14Poland 8.50Russia 11.06

2.86

- also ‘pipeline’

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Medical Education

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

The supply of Medical Professionals in SA Nurses:

• “Production of new nurses has failed to keep up with the increase in population, let alone with the shortages created by the emigration exodus and the need for new nurses as a result of the HIV pandemic.”

Medical Education:

Medical schools enrolments unchanged: 1996 – 2003; except Limpopo ++

Demographics of 2003 enrolment: • Black 41%; White 34%; Indian 18%; Coloured 7%• 54.6% female ~ worldwide phenomenon and issue re Specialisation: Prof Carol Black; President of Royal College of Physicians: noted that female graduates

tended to specialise in areas such as geriatrics and palliative care and avoid cardiology and gastro because of their long hours.

Others identified that women are deterred from hospital practice by its “inflexible training and practice”

UCT case study 2003: undergrad = 63%; MMed = 37%; favoured Paediatrics; Anaesthetics; Psychiatry; O&G; Public Health.

Doctors in a Divided Society

(HSRC): Breier & Wildschut

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Structural issues

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

0

1

2

3

4

5

6

7

US

Singap

ore

Canad

a

Sweden

Irela

nd

Spain

Austra

lia UKIta

ly

Nether

lands

France

0

1

2

3

4

5

6

7GPs per 1000 people

Specialists per 1,000 people

Beds used per 1000 people

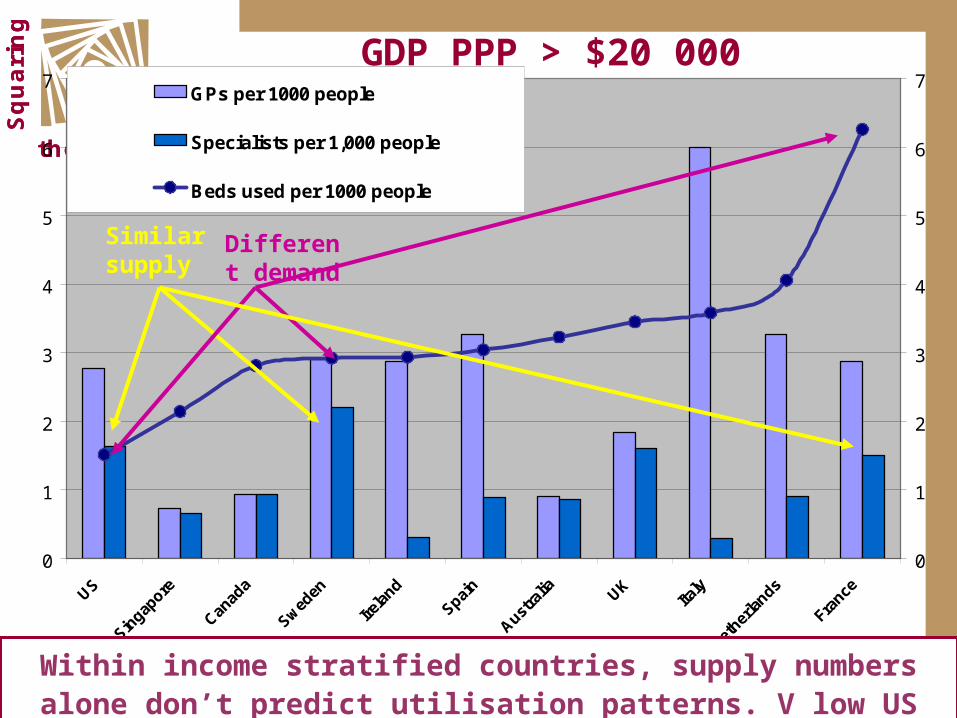

GDP PPP > $20 000

Similar supply

Different demand

Discovery research: Monitor database

Within income stratified countries, supply numbers alone don’t predict utilisation patterns. V low US beds after 25 years of DRGs

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

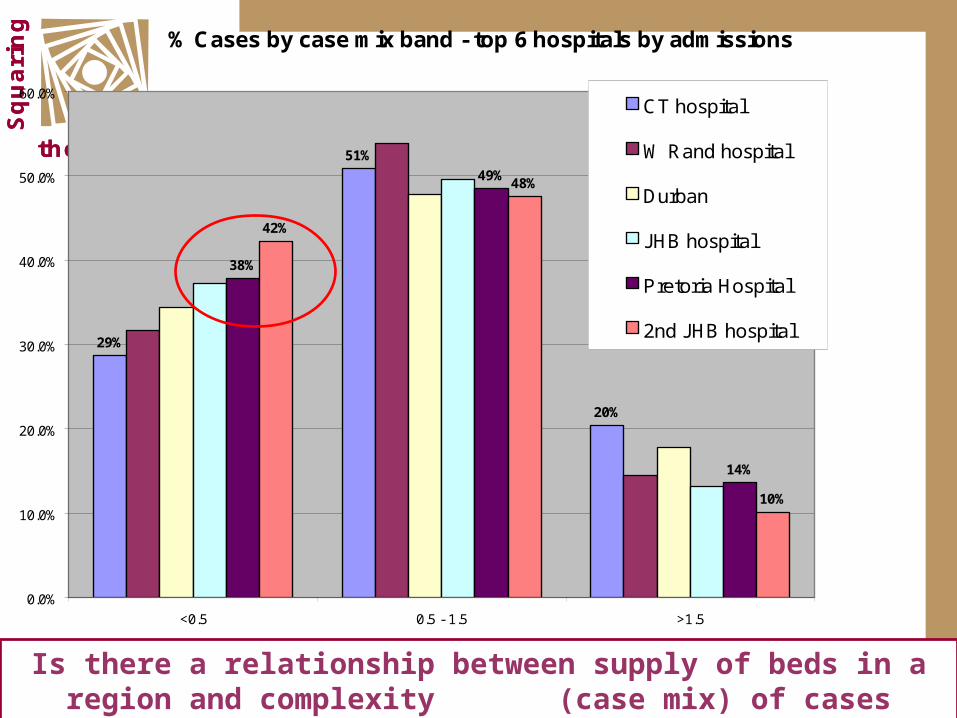

% Cases by case mix band - top 6 hospitals by admissions

29%

51%

20%

38%

49%

14%

42%

48%

10%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

<0.5 0.5 - 1.5 >1.5

CT hospital

W Rand hospital

Durban

JHB hospital

Pretoria Hospital

2nd JHB hospital

Discovery Health

Is there a relationship between supply of beds in a region and complexity (case mix) of cases admitted?

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Pretoria hospital – top 20% of admissions by volume

GroupingCasemix

IndexNo of

EventsHospital

Cost

vs. national average

06371 - OTHER GASTROENTERITIS & ABDOMINAL PAIN W/O CC 0.30 596 R4,062 1.2114601 - CESAREAN DELIVERY W/O CC 1.25 481 R14,241 1.0503081 - TONSIL & ADENOID PROCEDURES W/O CC 0.37 314 R4,211 1.0104361 - SIMPLE PNEUMONIA & WHOOPING COUGH W/O CC 0.66 276 R8,943 1.2406381 - OTHER DIGESTIVE SYSTEM DIAGNOSIS W/O CC 0.29 247 R3,578 1.14

Discovery Health

Top 5 admission types – unusually low complexity; and significantly more costly than expected

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

SADFM study 2004

• 24 acute public hospitals; alpha and beta functional scores applied to 5,243 inpatients

• Results:– 34% required acute care– 43% sub acute care– 9% rehab services– 5% palliative care– 10% home care

Dr H Loubsher

SADFMStructural issue: absence of facility alternatives

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

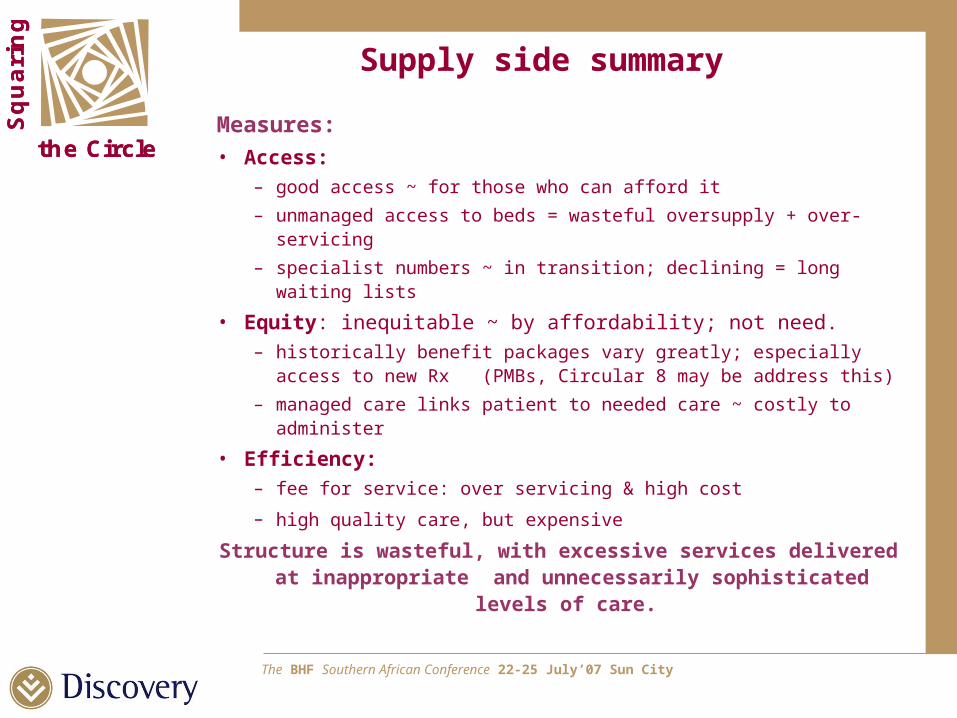

Supply side summary

• Hospital beds:– selective oversupply e.g. Pretoria, JHB = supplier induced demand– dearth of day hospitals; step down facilities (structural issues)

• Professionals supply norms low in SA overall:– Underinvestment & inadequately managed demographic transition is leading to an

undersupply of doctors and specialists– Worrying number of older specialists, not enough younger specialists in practice ~ also

effects mentoring – private sector now has growing waiting lists

• Inefficiently structured referral system:– care delivered at inappropriately costly levels (especially hospitals)– health professional practice highly individualistic; rarely in teams e.g.

– senior specialist supervising GPs; clinical nurses with a doctor– ‘fee for service’ remuneration incentive to perform high priced services

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the CircleMeasures:• Access:

– good access ~ for those who can afford it – unmanaged access to beds = wasteful oversupply + over-servicing– specialist numbers ~ in transition; declining = long waiting lists

• Equity: inequitable ~ by affordability; not need. – historically benefit packages vary greatly; especially access to new

Rx (PMBs, Circular 8 may be address this) – managed care links patient to needed care ~ costly to administer

• Efficiency:– fee for service: over servicing & high cost

– high quality care, but expensive

Structure is wasteful, with excessive services delivered at inappropriate and unnecessarily sophisticated levels of care.

Supply side summary

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Agenda

• Introduction to health sector reform• Supply side issues• Possible responses ~ reform experiences

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

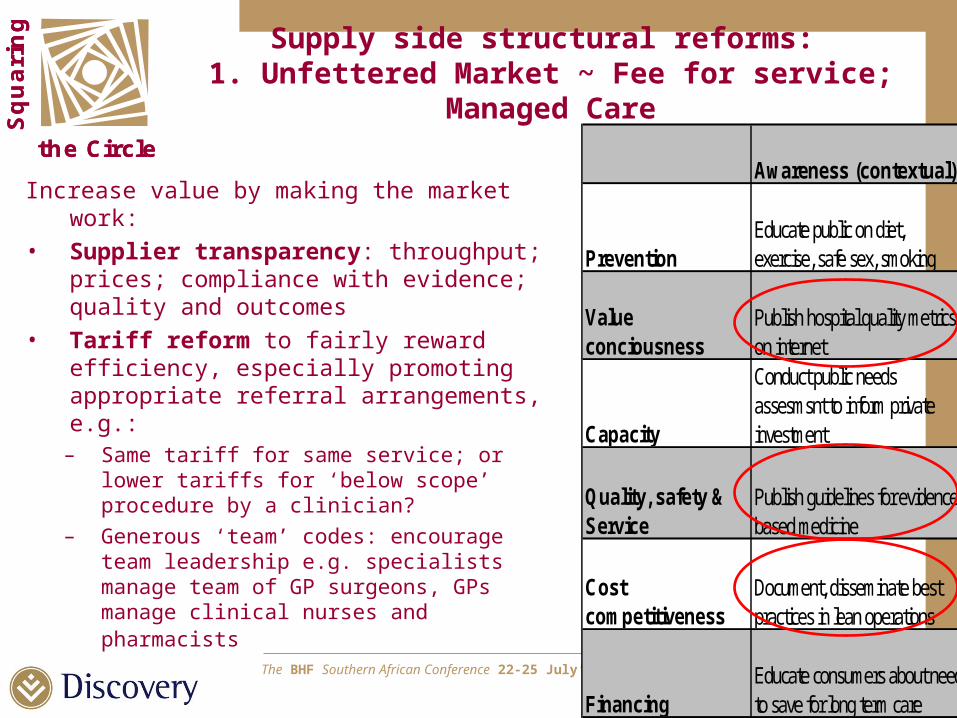

the CircleAwareness (contextual) Incentives (indirect) Mandates (direct)

Prevention

Educate public on diet, exercise, safe sex, smoking

Contribute to health saving accounts (HSAs) to reward lifestyle changes

Require accination for children before they start kindergarten

Value conciousness

Publish hospital quality metrics on internet

Design benefit packes to encourage use of specific providers

Exclude coverage for high cost providers or procedures

Capacity

Conduct public needs assesmsnt to inform private investment

Forgive loans for physicians practicing in underserved areas

Require regulatory approval based on demonstration of need

Quality, safety & Service

Publish guidelines for evidence based medicine

Pay bonuses to providers for implimenting evidence based medicine

License / credintial providers based on minimum standards

Cost competitiveness

Document, disseminate best practices in lean operations

Negotiate preferred vendor agreements with low cost providers

Impose standard pricing for all doctors, set at low level to drive cost reductions

Financing

Educate consumers about need to save for long term care

Offer tax subsidies for purchase of emloyer-sponsored coverage

Mandate insurance coverage for all not covered by public entitlement program

Implimentation approaches to shaping deand and supply

‘Unfettered’ Market Contract for Value Regulation

The McKinsey 2007 No.1: Universal principles for health care

reformMcKinsey: Implementation choices:

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the CircleAwareness (contextual) Incentives (indirect) Mandates (direct)

Prevention

Educate public on diet, exercise, safe sex, smoking

Contribute to health saving accounts (HSAs) to reward lifestyle changes

Require accination for children before they start kindergarten

Value conciousness

Publish hospital quality metrics on internet

Design benefit packes to encourage use of specific providers

Exclude coverage for high cost providers or procedures

Capacity

Conduct public needs assesmsnt to inform private investment

Forgive loans for physicians practicing in underserved areas

Require regulatory approval based on demonstration of need

Quality, safety & Service

Publish guidelines for evidence based medicine

Pay bonuses to providers for implimenting evidence based medicine

License / credintial providers based on minimum standards

Cost competitiveness

Document, disseminate best practices in lean operations

Negotiate preferred vendor agreements with low cost providers

Impose standard pricing for all doctors, set at low level to drive cost reductions

Financing

Educate consumers about need to save for long term care

Offer tax subsidies for purchase of emloyer-sponsored coverage

Mandate insurance coverage for all not covered by public entitlement program

Implimentation approaches to shaping deand and supply

‘Unfettered’ Market Contract for Value Regulation

The McKinsey 2007 No.1: Universal principles for health care

reformMcKinsey: Implementation choices:

consumerism incentives

regulation

More nuanced view….

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Increase value by making the market work:• Supplier transparency: throughput; prices;

compliance with evidence; quality and outcomes

• Tariff reform to fairly reward efficiency, especially promoting appropriate referral arrangements, e.g.:

– Same tariff for same service; or lower tariffs for ‘below scope’ procedure by a clinician?

– Generous ‘team’ codes: encourage team leadership e.g. specialists manage team of GP surgeons, GPs manage clinical nurses and pharmacists

Supply side structural reforms: 1. Unfettered Market ~ Fee for service; Managed Care

Awareness (contextual)

Prevention

Educate public on diet, exercise, safe sex, smoking

Value conciousness

Publish hospital quality metrics on internet

Capacity

Conduct public needs assesmsnt to inform private investment

Quality, safety & Service

Publish guidelines for evidence based medicine

Cost competitiveness

Document, disseminate best practices in lean operations

Financing

Educate consumers about need to save for long term care

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Interactions between member and Scheme administrator: Fee for Service vs. Contract for Value

Interaction FFS NetworkDoctor visits claim: 3.5 0

Related calls: 1 0Pharmacy Claims: 13 2 non network drugs

Related Calls: 0.5 0.5Podiatry; optician claim etc 7 0

Related calls 1 0Path; Rad claims etc 5 0Related calls 1 0

Hospital Claims: 1.5 0.7 lower admit rate

Related calls 3 2other administration 2 4 loaded for network

rules calls etc

Total interactions 38.5 9.2

difference 418%

Contract

annualised; expert opinion“Arms length” Managed Care is costly to administer

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

• Rigid regulation may result in unintended consequences?

– Further distort referral chain – undermine quality or drive inappropriate care

– Indication ‘creep’ re billing

• Helpful regulation in areas of ‘positive externalities’ which market won’t / can’t address:

– Mandatory cover for employed– Preventing monopoly behaviour

• By creating framework, may be enabling of market and contracting:

– Mandate transparent; minimum level reporting on results of contracts

Supply side structural reforms: 3. Regulation

Mandates (direct)

Prevention

Require accination for children before they start kindergarten

Value conciousness

Exclude coverage for high cost providers or procedures

Capacity

Require regulatory approval based on demonstration of need

Quality, safety & Service

License / credintial providers based on minimum standards

Cost competitiveness

Impose standard pricing for all doctors, set at low level to drive cost reductions

Financing

Mandate insurance coverage for all not covered by public entitlement program

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Aim: to promote selective contracting to bring value to the system:

• Selectively increase beds in strategic areas:

– Day and Step down facilities– Licenses– Sell some Public hospital stock?

• Clinician supply ~ HPC(SA): – create transitory increase in specialist

supply, promote entry for foreign specialists– permit hospitals to selectively employ

doctors in strategic areas to improve efficiency – ICU; ER; night cover etc

• Pay for performance – quality and cost

Supply side structural reforms: 2. Purchaser / Provider contract for value:

Incentives (indirect)

Prevention

Contribute to health saving accounts (HSAs) to reward lifestyle changes

Value conciousness

Design benefit packes to encourage use of specific providers

Capacity

Forgive loans for physicians practicing in underserved areas

Quality, safety & Service

Pay bonuses to providers for implimenting evidence based medicine

Cost competitiveness

Negotiate preferred vendor agreements with low cost providers

Financing

Offer tax subsidies for purchase of emloyer-sponsored coverage

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Purchaser / Provider ‘contract for value’:Competent authorities purchase services from independent providers on a capitated basis for a contracted period.

Model represents the consensus of international reform efforts.

Demand side reform: • based on a limited number of large efficient purchaser funds, whose available

funds are population risk adjusted i.e. link overall need to funding.• purchaser role is to:

– purchase services from suppliers on a capitated / budget basis– provider funding linked to predicted need of population segment to be served– constant measurement & robust management of contracted independent

providers of care to meet budget and quality aims– supplier failure = contract termination; replacement of managers / providers

• purchasers must be:– sufficiently large to deploy predictive data tools; and manage contracts– sufficient in number to compete ~ on value (price and quality) for members– mandatory environment but choice of fund; with transparent tools e.g. HQA

• Making risk profit – attract brightest minds

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Contracting includes:

• Evidence based medicine: – identify which procedures (drugs, surgical interventions, processes of care) produce best

results relative to cost– reward those procedures with providers.

• Appropriate level of skill: – Service rewarded at appropriate expertise level i.e. move patients down skill gradient:

Specialist to GP to nurse, as necessary.

• Process redesign / reconfiguration: – reward integrated service delivery (team approach)– incentivise a new model of primary (first contact) care with bigger practices, more

specialists, more equipment– encourage the transfer of ‘inpatient’ functions to primary care– separation of emergency and elective / chronic care (different specialisation mix

requirements)

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Purchaser provider contract for value:

Measures:• Access: good; may use selective co-payments • Equity:

– Provider links services to individual need; supported by adequate funds– Incentives: deliver appropriate type & volume & quality of services within framework

• Efficiency: purchaser / supplier separation is most successful in producing efficiency:

– Purchaser tools link funds to efficiency + quality, as their major managerial concern (i.e. not running services)

– Provider / supply side is internally incentivised to primarily respond to the customers (market competition) equity, efficiency and quality needs.

– Managers know that their available funding is population risk adjusted i.e. under spending implies denial of care; and over spending implies wastage.

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

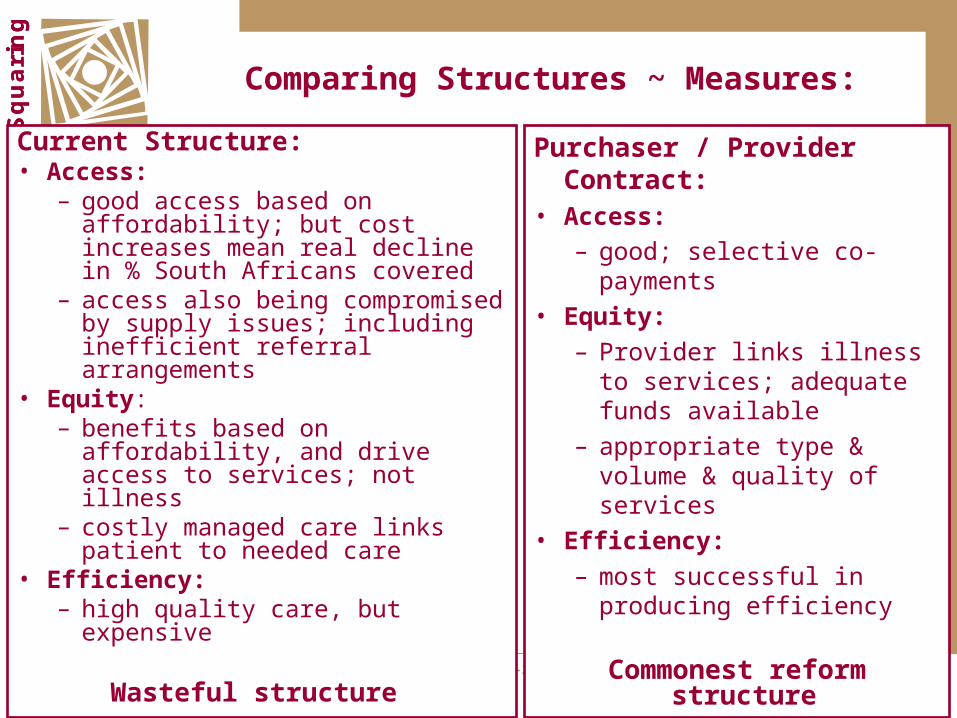

Comparing Structures ~ Measures:

Purchaser / Provider Contract:• Access:

– good; selective co-payments

• Equity: – Provider links illness to

services; adequate funds available

– appropriate type & volume & quality of services

• Efficiency: – most successful in producing

efficiency

Commonest reform structure

Current Structure:• Access:

– good access based on affordability; but cost increases mean real decline in % South Africans covered

– access also being compromised by supply issues; including inefficient referral arrangements

• Equity: – benefits based on affordability, and

drive access to services; not illness– costly managed care links patient to

needed care • Efficiency:

– high quality care, but expensive

Wasteful structure

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

US experience: Doctors coordinating care

Medicare pilot:• By coordinating care and keeping their patients out of hospital, doctors can help

reduce overall health care spending, Medicare officials said yesterday in announcing the results of an experiment that allowed doctors to share in cost savings.

New York Times 2007

Comparison UK NHS with California Kaiser Permanente:• Similar per capita cost but Kaiser far better comprehensive and convenient primary care; and access

to specialists and hospitalisation. Age adjusted hospital admissions 1/3 lower than NHS • Kaiser / 1000 supply: OH specialists double; no GPs in single practice, most in large group practices• Kaiser performance underpinned by good integration; efficient hospital use; benefits of

competition, investment in IT. BMJ January 2002

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

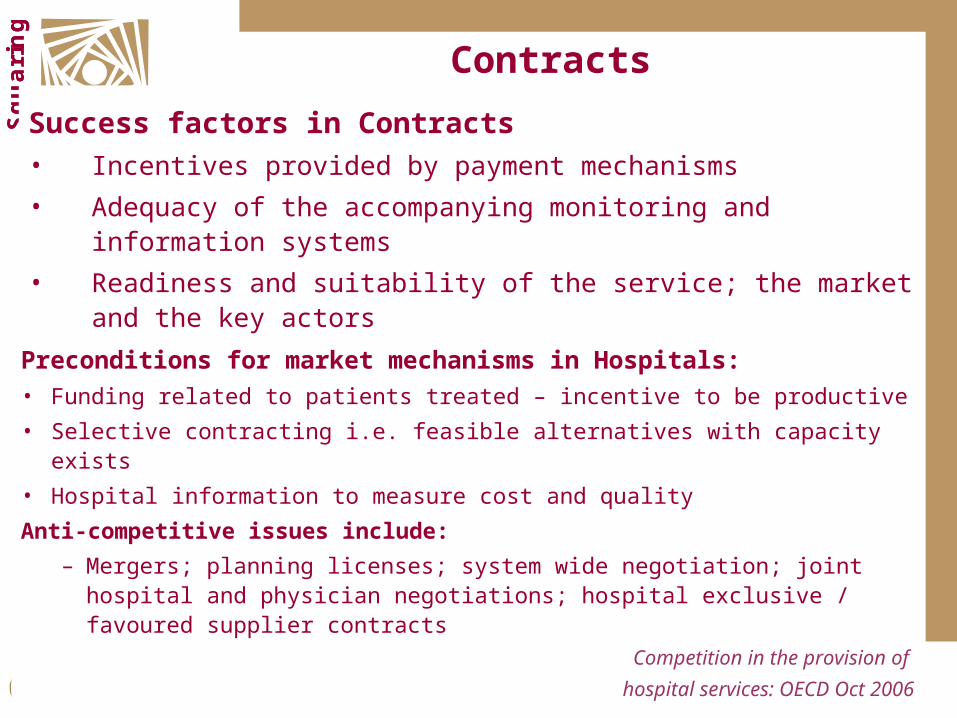

Contracts

Success factors in Contracts• Incentives provided by payment mechanisms• Adequacy of the accompanying monitoring and information systems• Readiness and suitability of the service; the market and the key actors

Public Purchaser-Private provider Contracting for Health Services: Inter-American Development Bank

Preconditions for market mechanisms in Hospitals:• Funding related to patients treated – incentive to be productive• Selective contracting i.e. feasible alternatives with capacity exists• Hospital information to measure cost and quality

Anti-competitive issues include:

– Mergers; planning licenses; system wide negotiation; joint hospital and physician negotiations; hospital exclusive / favoured supplier contracts

Competition in the provision of

hospital services: OECD Oct 2006

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Risk adjusted purchasing:

• DRG implementation by country:– USA 1983– Sweden 1985– Finland 1987– Portugal 1989– Canada 1990– UK 1992– Australia; Ireland 1993– Italy; Belgium 1995– France 1997– Denmark; Norway 1999– Singapore early 2000’s– Netherlands; Germany; Japan 2003

• Others countries with pilots or investigations: – China; Russia; Brazil etc

Analysing Changes in Health Financing Arrangements in High Income countries: Busse et al 2007 World bank HNP:

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

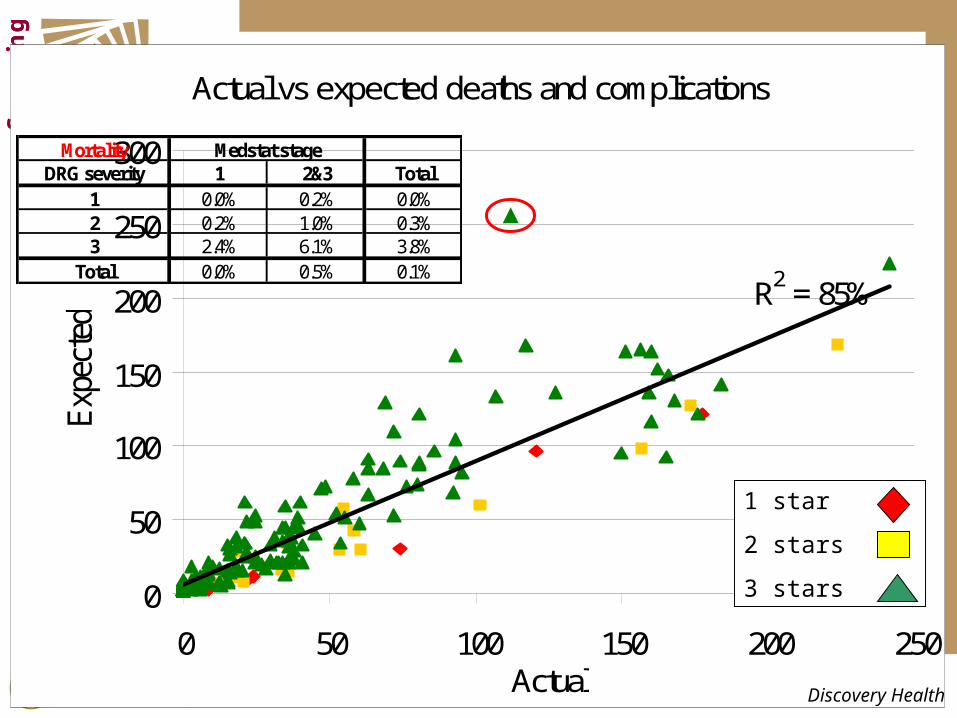

Predicting outcomes Actual vs expected deaths and complications

R2 = 85%

0

50

100

150

200

250

300

0 50 100 150 200 250Actual

Exp

ecte

d

1 star

2 stars

3 stars

Discovery Health

MortalityDRG severity 1 2&3 Total

1 0.0% 0.2% 0.0%2 0.2% 1.0% 0.3%3 2.4% 6.1% 3.8%

Total 0.0% 0.5% 0.1%

Medstat stage

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

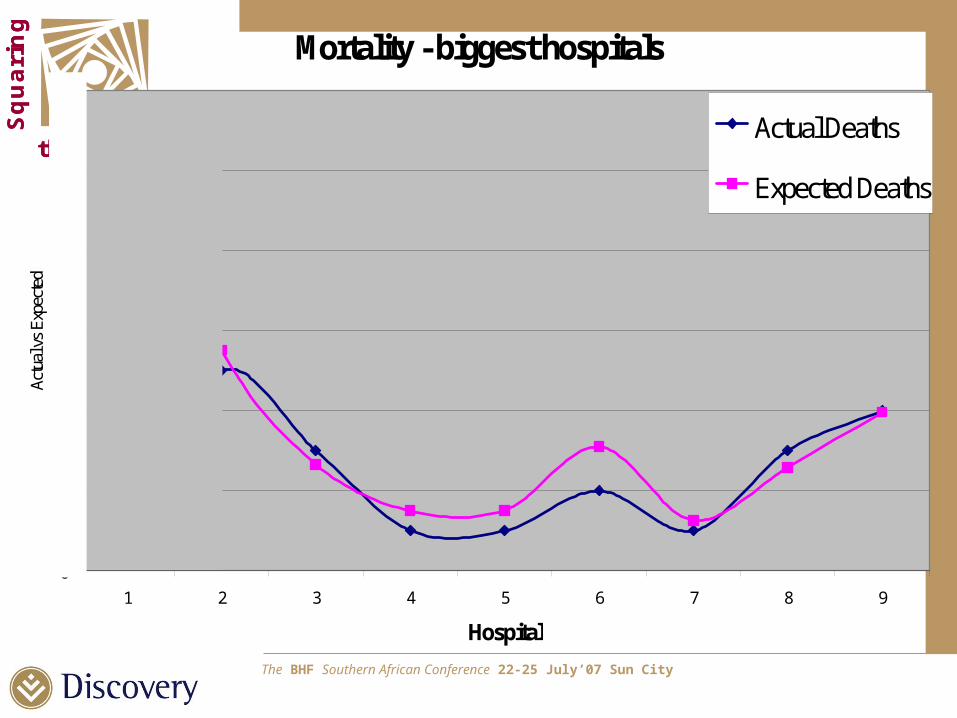

Mortality - biggest hospitals

0

2

4

6

8

10

12

1 2 3 4 5 6 7 8 9

Hospital

Actu

al v

s Ex

pect

ed

Actual Deaths

Expected Deaths

?

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Summary: health sector reform in SA

• Align supply with need – supply is both capacity and how the system is structured

• NB of separating procurement from supply

• NB to manage and incentivise providers to balance quality and costs

• Need tools to monitor and manage the balance

The BHF Southern African Conference 22-25 July’07 Sun City

Sq

uari

ng

the Circle

Sq

uari

ng

the Circle

Thank you

![Ruff Newsletter Jan2011[1]](https://static.fdocuments.in/doc/165x107/577d2f731a28ab4e1eb1bee2/ruff-newsletter-jan20111.jpg)