The Basic Rules of Business Finance. Key Terms & Concepts Accountancy The communication of financial...

16

The Basic Rules of Business Finance

-

Upload

richard-parrish -

Category

Documents

-

view

213 -

download

0

Transcript of The Basic Rules of Business Finance. Key Terms & Concepts Accountancy The communication of financial...

The Basic Rules of Business

Finance

Key Terms & Concepts

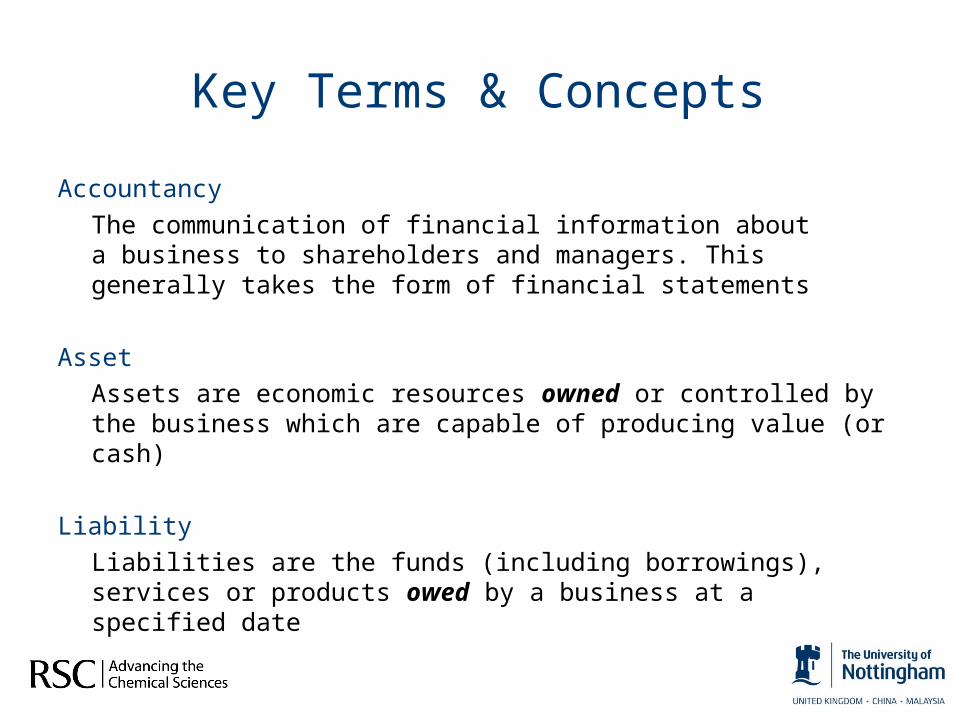

Accountancy

The communication of financial information about a business to shareholders and managers. This generally takes the form of financial statements

Asset

Assets are economic resources owned or controlled by the business which are capable of producing value (or cash)

Liability

Liabilities are the funds (including borrowings), services or products owed by a business at a specified date

Capital & Reserves (or Owner’s Equity)

Funds put into the business by the owners or shareholders and retained on their behalf

Profit/Loss Statement (past financial performance)

Shows the performance of the business over a given time period

The Profit/Loss = Total Income – Total Expenditure

Gross Profit = sales revenue (and other income) – cost of making the product before deducting overheads, payroll, taxation and other costs for the period

Net Profit = gross profit – all costs (e.g. manufacture/sales, operating costs, taxes etc.) i.e. after subtracting all costs, expenses and losses for the period

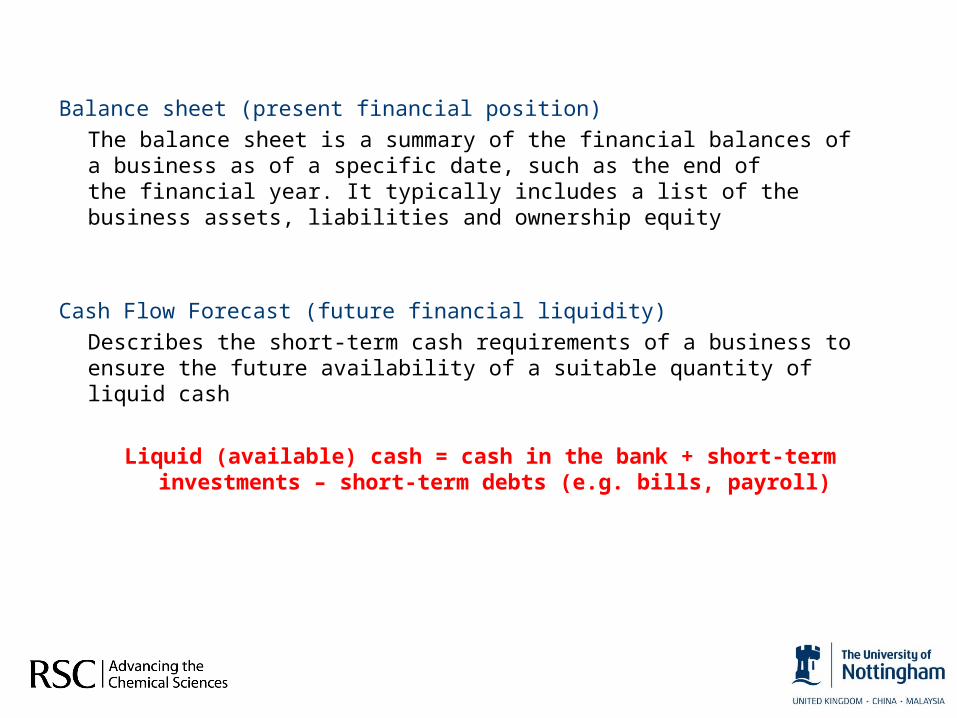

Balance sheet (present financial position)

The balance sheet is a summary of the financial balances of a business as of a specific date, such as the end of the financial year. It typically includes a list of the business assets, liabilities and ownership equity

Cash Flow Forecast (future financial liquidity)

Describes the short-term cash requirements of a business to ensure the future availability of a suitable quantity of liquid cash

Liquid (available) cash = cash in the bank + short-term investments – short-term debts (e.g. bills, payroll)

Cost, Price and Value

Cost

“How much it cost you to produce/manufacture”

Price

“How much you are selling the product for”

Value

“How much the customer is prepared to pay for it”

This shows the profit/loss that has been achieved over a given period of time (i.e. in the past). Profit = Total Income – Total Expenditure

You have your own monthly profit/loss statement – A bank statemente.g. Alan Sugar’s Personal Bank Statement for December

The Profit/Loss StatementA Personal Example

Item Credit (£) Debit (£)

Apprentice income 75,000

Loan repayments 10,000

Electricity and Gas bill 600

T.V. and advertising appearances 50,000

Other bills 1,250

Cleaning Co. household cleaners 350

Credit card bill (food, entertainment, clothes, travel) 15,550

Total Credit/Debit 125,000 27,750

Balance carried forward to January 97,250

Alan Sugar is in profit for December

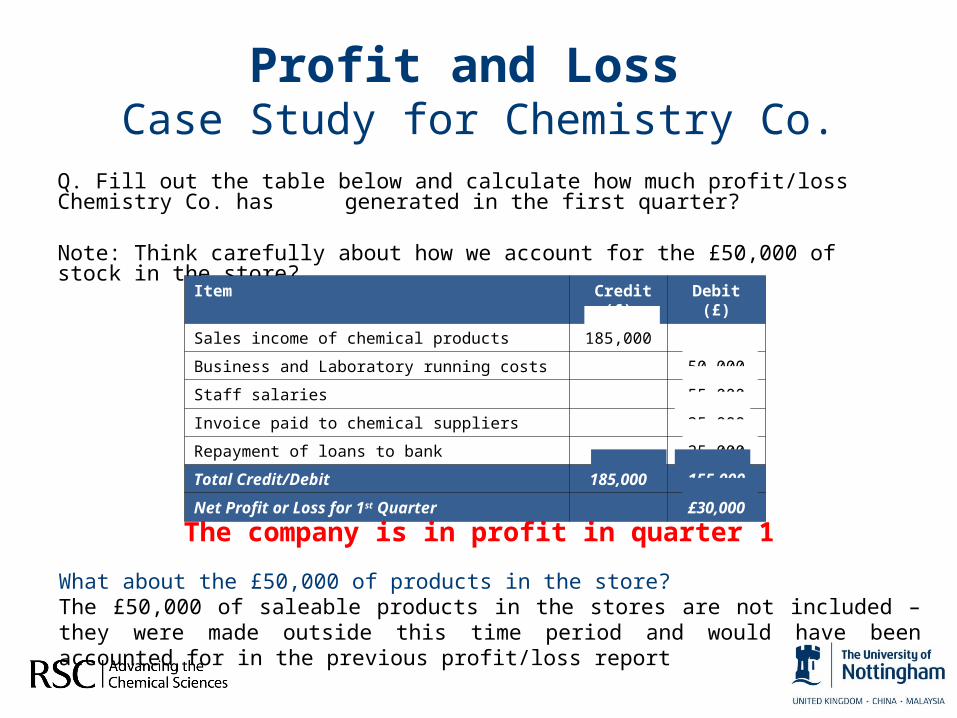

Q. Fill out the table below and calculate how much profit/loss Chemistry Co. has generated in the first quarter?

Note: Think carefully about how we account for the £50,000 of stock in the store?

Profit and Loss Case Study for Chemistry Co.

Item Credit (£) Debit (£)

Sales income of chemical products 185,000

Business and Laboratory running costs 50,000

Staff salaries 55,000

Invoice paid to chemical suppliers 25,000

Repayment of loans to bank 25,000

Total Credit/Debit 185,000 155,000

Net Profit or Loss for 1st Quarter £30,000

What about the £50,000 of products in the store?The £50,000 of saleable products in the stores are not included – they were made outside this time period and would have been accounted for in the previous profit/loss report

The company is in profit in quarter 1

Understand your own present financial circumstances What is likely to be your principal asset? Do you own it outright or is it financed (i.e. a liability)?

The Balance SheetA Personal Example

House value £200,000

Mortgage from the Bank £120,000Your equity (profit) £80,000

£200,000

Your personal balance sheet balances

Asset – Items of value owned or controlled by the business

Liability – Amounts or servises owed by the business

Capital & Reserves – Amounts input by the owners/shareholders

The Balance Sheet

Stock,Fixtures & Fittings

Resourcese.g. Vehicles, I.T. etc.

Cash Reserve

Bank Loans

Using the information below complete the following balance sheet

Q. Label each item as an asset (fixed/variable), liability or as capital & reserve

The Balance Sheet Case Study for Chemistry Co.

Item £ Asset, Liability or Capital & Reserve

Freehold of laboratory 350,000 Asset (fixed)

Equipment used within the business (inc. chemistry, I.T. etc.) 775,000 Asset (fixed)

Business fixtures and fittings 175,000 Asset (fixed)

Amount owed to chemical suppliers/other bills 25,000 Liability

Stocks of chemicals within the laboratory 25,000 Asset (variable)

Stocks of saleable chemical products 50,000 Asset (variable)

Loan from bank (repayable in 5 years) 250,000 Liability

Venture capitalist investment 500,000 Liability

Cash in the bank 125,000 Asset (variable)

Capital invested by the owner 375,000 Capital & Reserve

Accumulated profits (after 5 years trading) 350,000 Capital & Reserve

Q. Using the information in the previous table, complete the following balance sheet

The Balance Sheet As of 31st December

Fixed Assets £ Liabilities £

1. Freehold of laboratory2. Equipment used in business 3. Business fixtures and fittings

350,000775,000175,000

1. Amount owed to suppliers/other bills2. Loan from bank3. Venture capitalist investment

25,000250,000500,000

Variable Assets £ Capital and Reserves £

1. Stocks of chemicals2. Stocks of saleable products3. Cash in the bank

25,00050,000

125,000

1. Capital invested by the owner2. Accumulated profits

375,000350,000

Total Assets 1,500,000 Total Liabilities & Capital 1,500,000

So the balance sheet balances

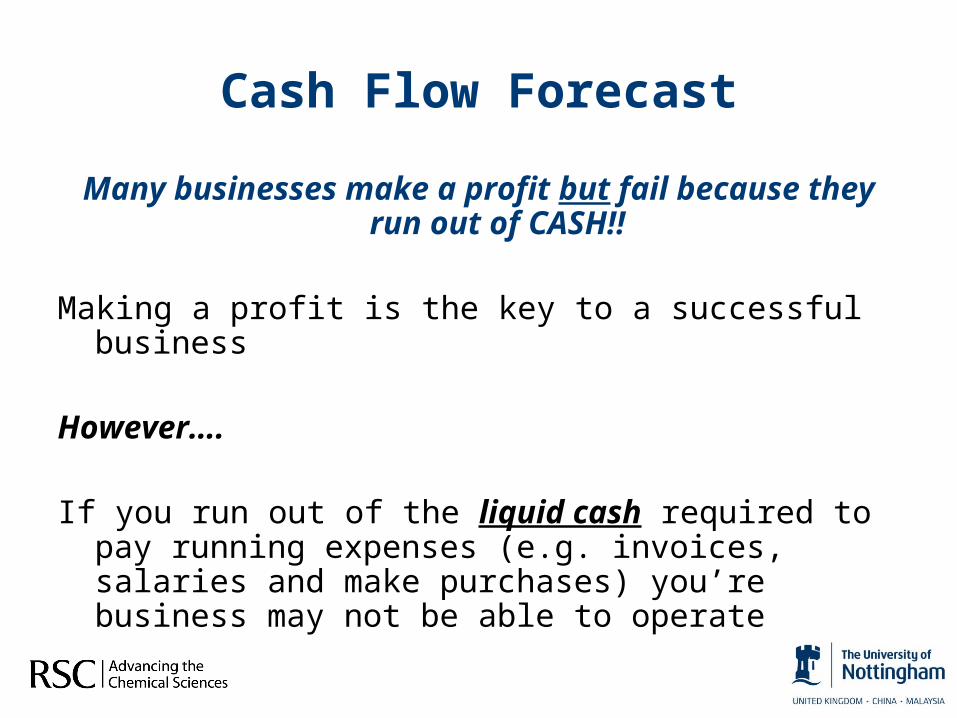

Many businesses make a profit but fail because they run out of CASH!!

Making a profit is the key to a successful business

However….

If you run out of the liquid cash required to pay running expenses (e.g. invoices, salaries and make purchases) you’re business may not be able to operate

Cash Flow Forecast

The Cash Flow Forecast describes the short-term cash requirements of a business to ensure the future availability of a suitable quantity of liquid cash

Liquid (available) cash = cash in the bank + short-term investments – short-term debts (e.g. bills, payroll)

“CASH IS KING”Without liquid cash your business can’t operate

Cash Flow Forecast

Summary

Profit/Loss Statement (past)Lists transactions for a given period (e.g. a year) and shows whether the business is making a profit or loss

The Balance Sheet (present)Shows whether the finances balance on a given date

Cash Flow Forecast (future)Describes the short-term cash requirements of a business

“CASH IS KING”

AuthorsDr. Trevor Farren, Dr. Simon Mosey & Dr. William Drewe

OrganisationSchool of Chemistry, University of Nottingham, U.K.

Supported by: