The Basic Building Blocks of the Individual Disability Policy.

23

The Basic Building Blocks of the Individual Disability Policy

-

Upload

augustine-cunningham -

Category

Documents

-

view

215 -

download

1

Transcript of The Basic Building Blocks of the Individual Disability Policy.

The Basic Building Blocks of the Individual Disability

Policy

• Definition of disability– Own occ or any occ

• Insuring Clause• Partial vs Residual• Definition of earnings• Benefit offsets (income offsets)• Benefit duration• Elimination period• Exclusions and limitations• Optional benefits• Issue Options• Claims

Policy Provisions

• Own occupation typically 2,3,5 years or own occ to age 65– Unable to perform all the material duties of own

occupation on a full-time basis for selected # of years

• Any occupation begins after own occupation period ends– Unable to perform the duties of own or any other

occupation for which person is fitted by training, education, experience, age and physical and mental capacity

Definition of Disability (Own/Any Occupation)

Insuring Clause• Non-cancelable (non-can)

– Insurer guarantees that the policy cannot be cancelled for the duration of the coverage, other then for nonpayment of premium

– Insurer promises that the rates will not change– Insurer promises that the other policy provisions cannot be changed

• Guaranteed Renewable– Policy cannot be canceled– Other provisions of the contract cannot be changed– Rates can be adjusted for the entire class of insureds with DOI

approval

• Cancelable – rare, due to the lack of guarantees needed by customers

Partial

• Partial – Typically, loss of income is not a factor. Instead, the policy provides a benefit equal to 50% of the total disability benefit. Usually, partial must follow total disability and the benefit period is of a limited duration (usually 3 to 12 months)

Residual

• Residual – Encourages return to work, at least part-time, following disability. Residual disability results in the inability of the insured to perform some of his/her duties and has a loss of income. The benefit payable is calculated by comparing pre and post-disability income. This percent is then multiplied times the total disability benefit, resulting in the residual disability benefit

Calculation of Incomes Variations

• Cash Method of Accounting – it is the actual cash received during the period of disability that is counted, even if the income was earned through the performance of services rendered prior to the disability

• Accrual – the cash received during disability, but earned prior to the disability is excluded from the the determination of post-disability income

Loss of Earnings Contracts

• Relatively new product• Works similar to Own Occupation with

Residual Benefit policies with one exception . . . The insured’s post-disability earnings from any occupation reduce the benefit payable under the policy

• Considerably less expensive then ‘own occ’ contracts

Financial Underwriting Issues

• Insurable Earned Income – limited to salary, wages, bonuses, net earnings from a business enterprise, and certain executive benefits– W-2 - Employees– Schedule C –self-employed

• Replacement Ratio – the ratio of coverage provided to to earned income– Discretionary income– Issue and Participation Tables

• Unearned Income and Net Worth

• Insurable income is earned income; income generated from an individual’s efforts in his/her profession.

• Income test. Will the income stop if the individual becomes disabled? If it does, it is insurable.

Defining Insurable Income

• Basic Monthly Earnings– With or without commissions and/or bonuses– 12 or 24 month average

• W-2 Earnings

• S-Corporation Earnings

• Partnership Earnings

• Teacher’s Earnings

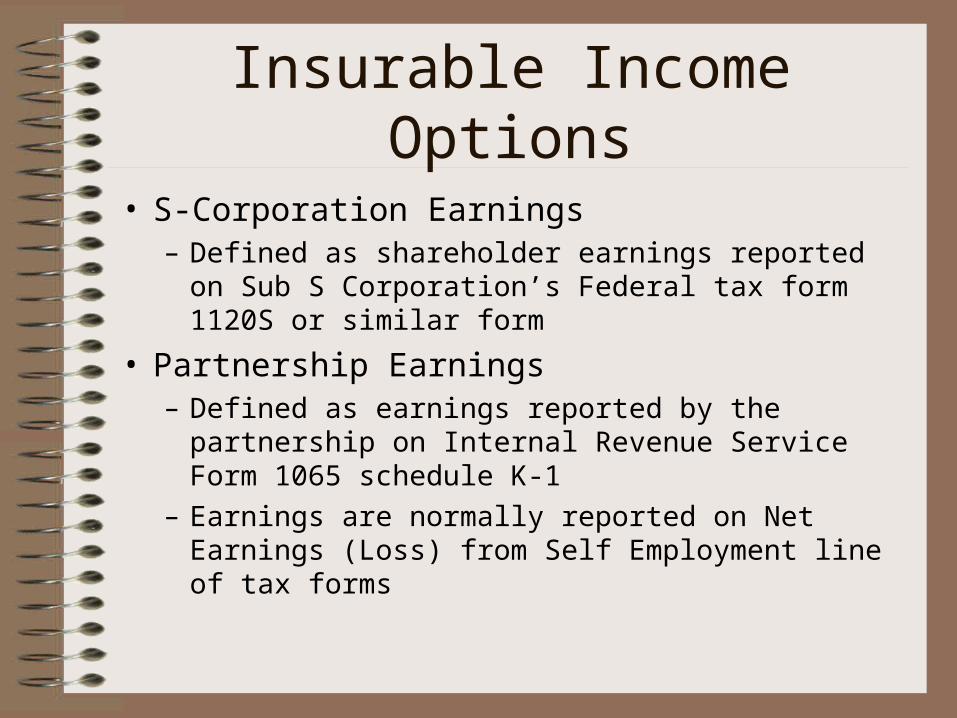

Insurable Income Options

• S-Corporation Earnings– Defined as shareholder earnings reported on Sub S

Corporation’s Federal tax form 1120S or similar form

• Partnership Earnings– Defined as earnings reported by the partnership on

Internal Revenue Service Form 1065 schedule K-1

– Earnings are normally reported on Net Earnings (Loss) from Self Employment line of tax forms

Insurable Income Options

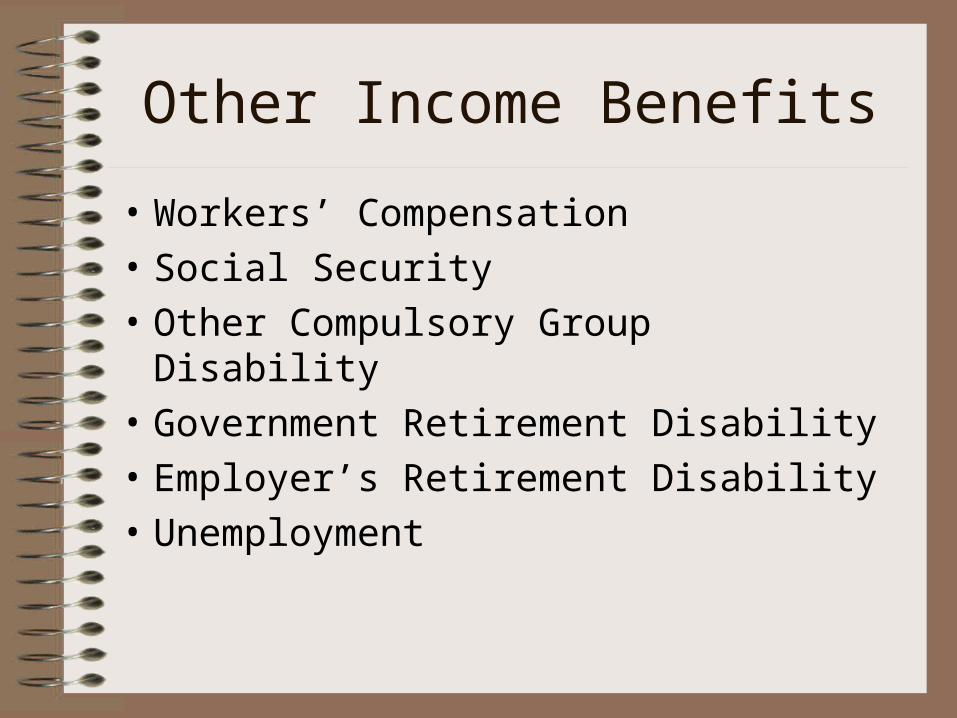

• Workers’ Compensation

• Social Security

• Other Compulsory Group Disability

• Government Retirement Disability

• Employer’s Retirement Disability

• Unemployment

Other Income Benefits

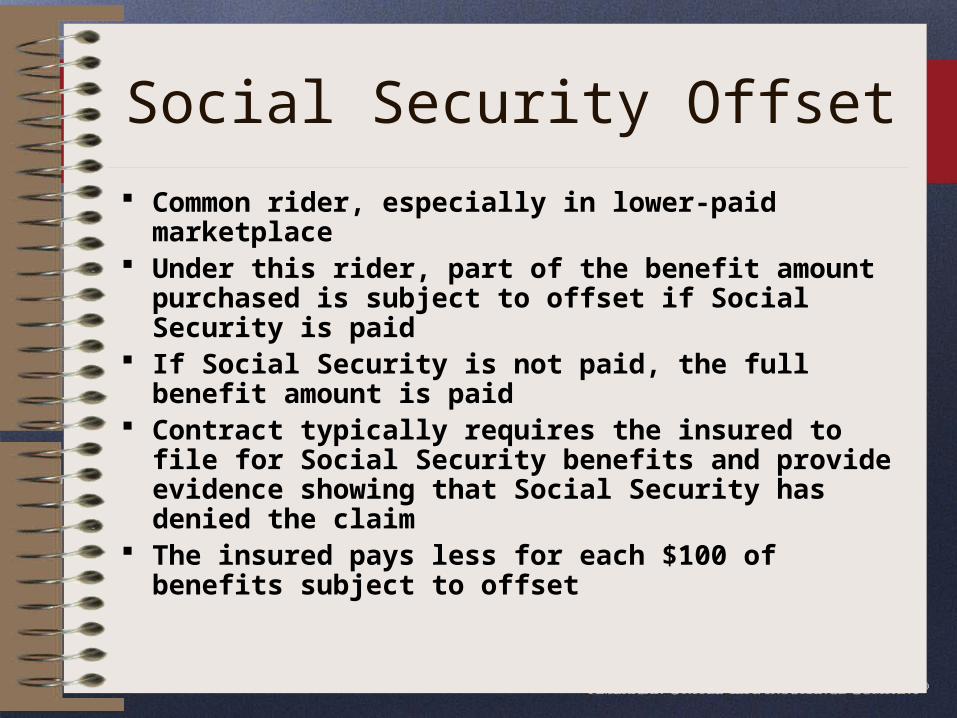

Common rider, especially in lower-paid marketplace Under this rider, part of the benefit amount

purchased is subject to offset if Social Security is paid If Social Security is not paid, the full benefit amount is

paid Contract typically requires the insured to file for

Social Security benefits and provide evidence showing that Social Security has denied the claim

The insured pays less for each $100 of benefits subject to offset

Social Security Offset

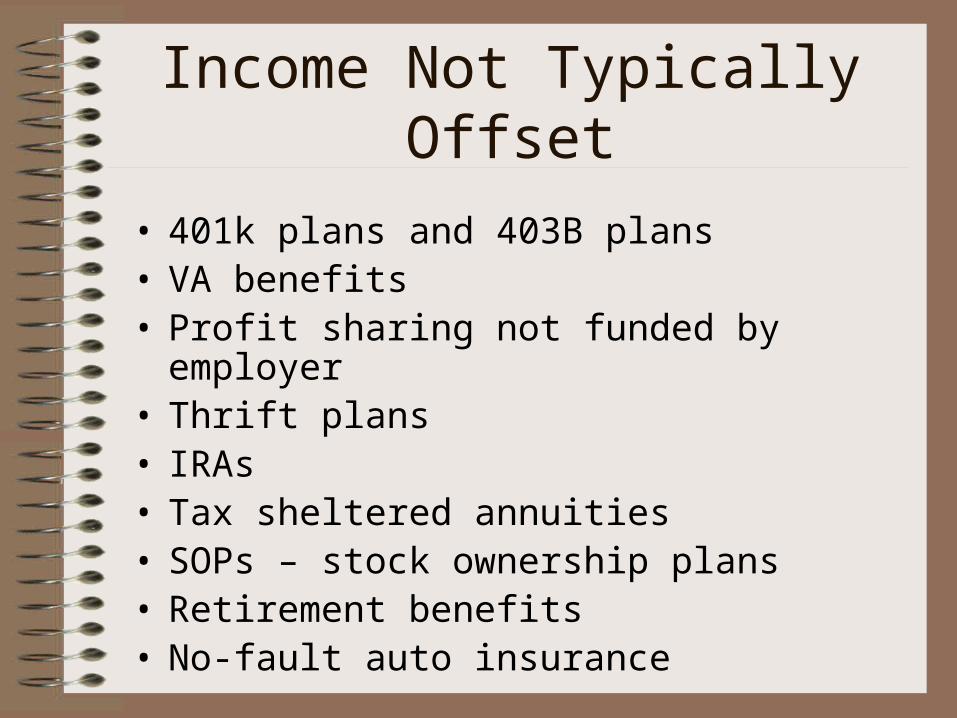

• 401k plans and 403B plans• VA benefits• Profit sharing not funded by employer• Thrift plans• IRAs• Tax sheltered annuities• SOPs – stock ownership plans• Retirement benefits• No-fault auto insurance

Income Not Typically Offset

Benefit Durations

• Most common are plans payable for 2,3, 5 or to age 65

• The most common is 65/65 (accident/sickness or illness)

• Lifetime is available, however, more limited and often restricted to disability form an accident (not sickness)

• Many contracts will limit benefit duration if disability does not occur prior to a specific age, ie., age 55

Elimination Period

• Also called the ‘waiting or qualification’ period

• 30, 60, 90, and 180 day or normal– Remember to coordinate the short and long-

term group plans

• Longer E.P.s are less costly

Optional Benefits

• Automatic Benefit Increase Option (AIB)– Annual increase in benefits

– Non-medical or financial underwriting

– Accept or decline option

– Limited number of years

• Cost of Living Adjustment (COLA)– Usually a flat percent or matches CPI-U

– Usually increases until capped (usually 2 x)

– Simple or Compounded

Optional Benefits (cont.)

• Guaranteed Purchase Option (GPO)– Option, at additional premium, which allows purchase

of additional amounts of coverage at specific intervals or ages

– While no medical underwriting is necessary, the insured must meet financial underwriting guidelines

– New premium charged is based on higher benefit amount

– Increases typically only allowed prior to disability

Optional Benefits (cont.)

• Return of Premium – Concept is that the insured pays premium for a period of time and

does not become disabled or receives benefits that are less than the aggregate premiums paid, the return of premium options refunds the insured a portion or all the premium paid – less benefits received

• Rational is that a skeptical buyer might purchase if they cannot lose the monies paid

• Two options– Cash value and premium refund

• Both options significantly increase the cost to the buyer

Issue Options

• Issued as applied for – standard issue• Exclusion Rider – policy issued as applied for

except for that specific medical issue or activities• Rated Premium – the coverage is issued, however,

there is an ‘additional’ rating– Can be done in conjunction with extending the E.P. or

shortening the benefit period

• Change occupational class to one less favorable• Reduce the benefit applied for• Decline the risk

Claims

• Filing the claim– Usually two parts to the form; Part 1 is completed by

the insured and Part 2 is completed by the attending physician

• Evaluation of the Claim– Contestability period– APS– Financial review

• Denial or payment• Application vs Claims Fraud

Questions?