THE ART OF THE ADJUSTMENT PROCESS

62

THE ART OF THE ADJUSTMENT PROCESS George Librizzi George Raymond Brown

-

Upload

cathleen-hall -

Category

Documents

-

view

31 -

download

2

description

THE ART OF THE ADJUSTMENT PROCESS. George Librizzi George Raymond Brown. GOALS. A review of the classical development and application of adjustments in the appraisal process. - PowerPoint PPT Presentation

Transcript of THE ART OF THE ADJUSTMENT PROCESS

THE ART OF THE ADJUSTMENT

PROCESS

George Librizzi

George Raymond Brown

A review of the classicaldevelopment and application of adjustments in the appraisal process

GOALS

This seminar is intended to raise issues and be thought provoking rather than a definitive guide to specific adjustment methodology

What are the

Judges saying?

A strong message has been sent to the

appraisal community by the courts

It is in your best interest to be aware of the

court’s opinions on a particular property type BEFORE appearing before them!https://www.judiciary.state.nj.us/taxcourt/taxcrtopinion.htm

…or your valuation could get booted out!

What is the root

of the issue

?

Incompetence?

Lack of supporting evidence?

Or just poor preparation?

SCOPE OF

WORK

WHAT DID WE PREPAREOUR WORK

PERSONAL HISTORY

EXPERIENCE

OBSERVATIONS

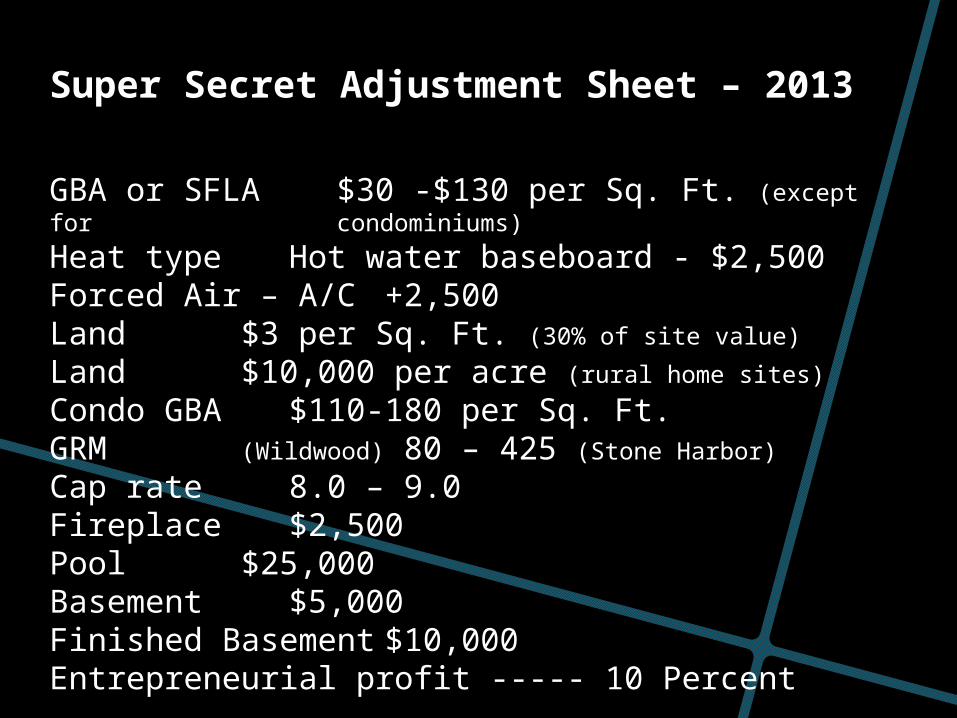

Super Secret

Adjustment Guide

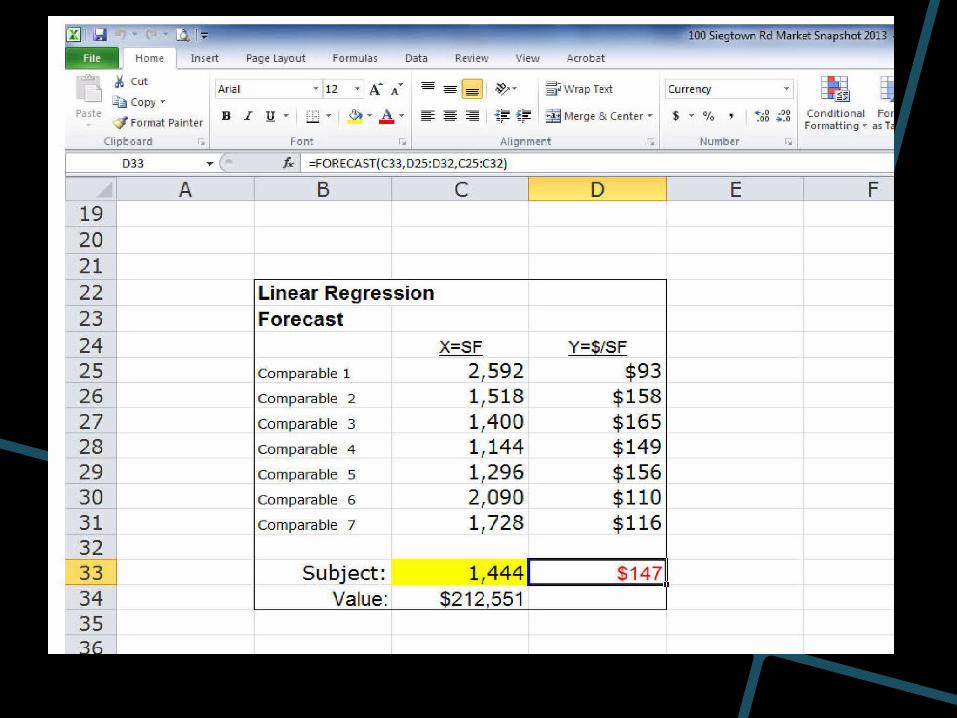

Super Secret Adjustment Sheet – 2013

GBA or SFLA $30 -$130 per Sq. Ft. (except for condominiums)

Heat type Hot water baseboard - $2,500Forced Air – A/C +2,500Land $3 per Sq. Ft. (30% of site value)

Land $10,000 per acre (rural home sites)

Condo GBA $110-180 per Sq. Ft.GRM (Wildwood) 80 – 425 (Stone Harbor)

Cap rate 8.0 – 9.0Fireplace $2,500Pool $25,000Basement $5,000Finished Basement $10,000Entrepreneurial profit ----- 10 Percent

OVER-COMING THEPRESUMPTION OF CORRECTNESSPantasote Co. v. City of

PassaicThe presumption must be rebutted by cogent evidence that must be, ..definite, positive, and certain in quality and quantityPresumption remains in effect even if the district used a flawed valuation method

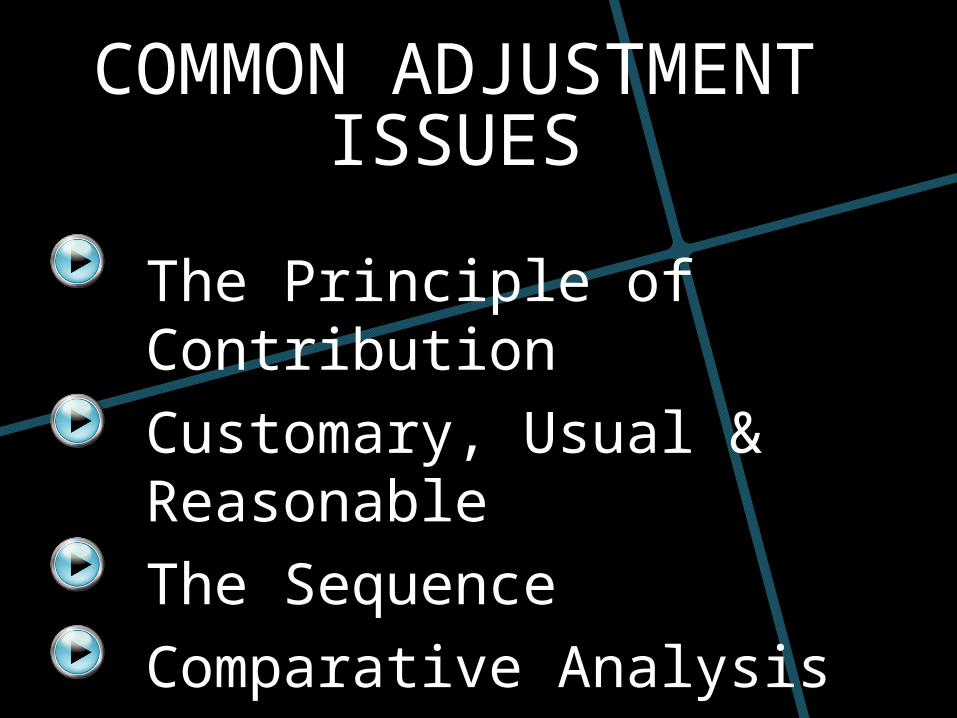

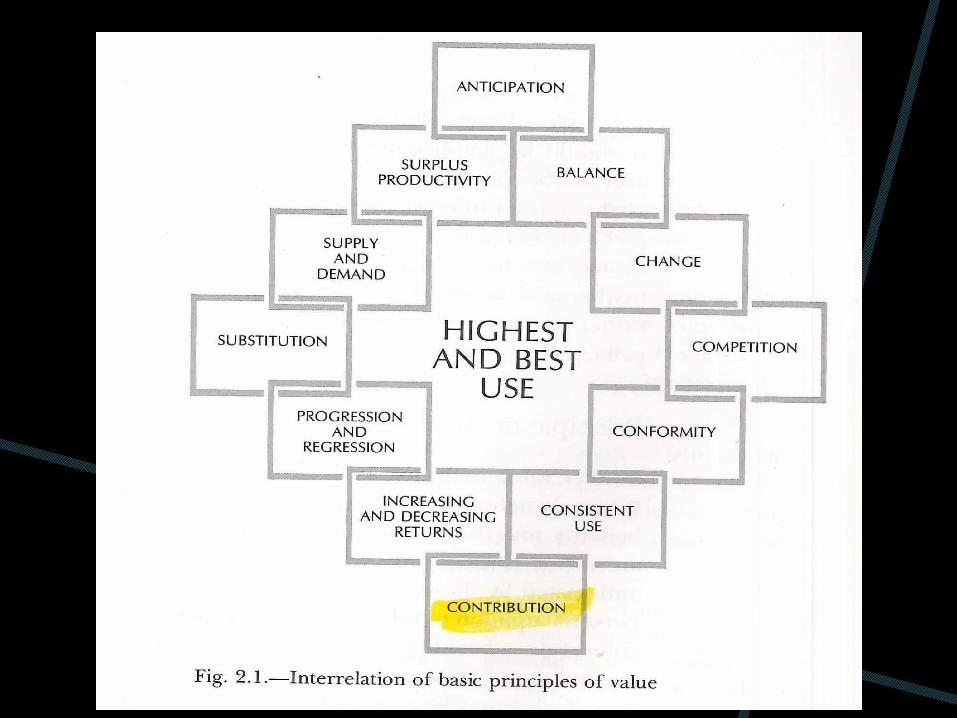

COMMON ADJUSTMENTISSUES

The Principle of ContributionCustomary, Usual & ReasonableThe SequenceComparative Analysis

QUALITATIVE

QUANTITATIVE

Justify the reasonablenessExtensive discussion of reasoning Location = quantitative It is expected the expert will explain the why’s and wherefores

Should be applied first

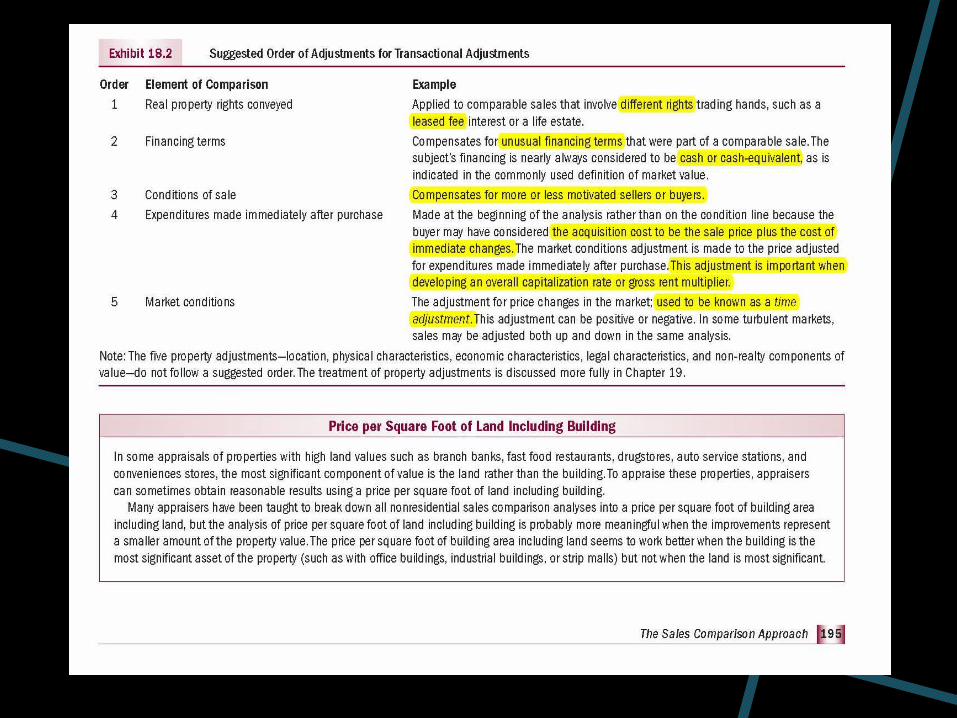

MAJOR SALES COMPARISON TECHNIQUES

RISKY BUSINESS

WHEN YOU RELY ON ONE APPROACH

“Take nothing on its looks; take everything on evidence. There’s no better rule”~Charles Dickens~

VS

LONG BRANCH CITY (APPELLATE ~ FEB 2014)

HOROVITS

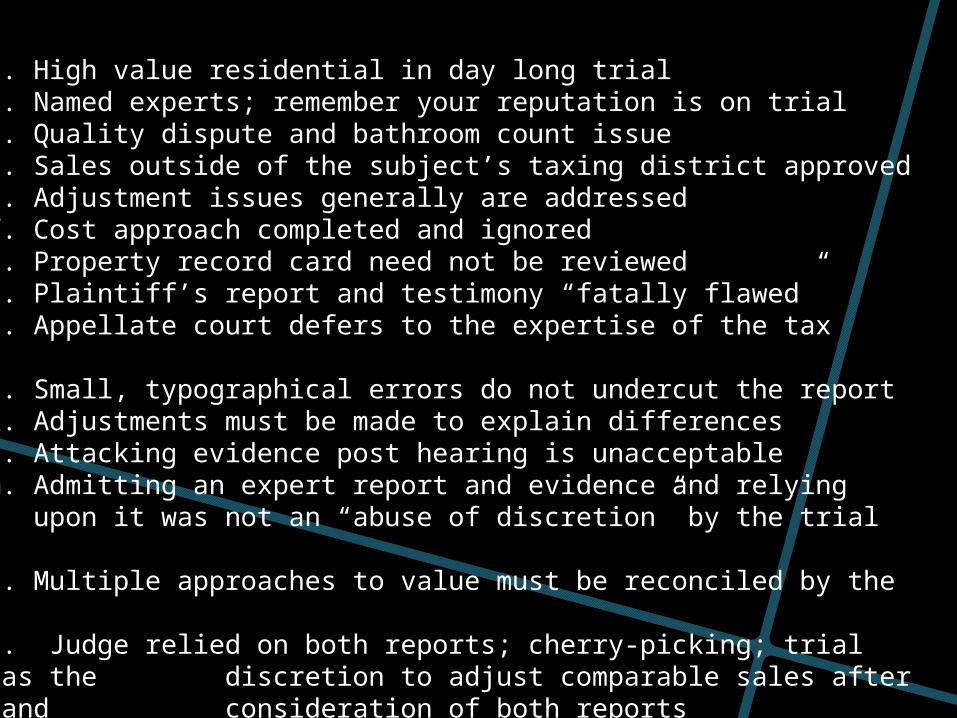

a. High value residential in day long trialb. Named experts; remember your reputation is on trialc. Quality dispute and bathroom count issued. Sales outside of the subject’s taxing district approvede. Adjustment issues generally are addressedf. Cost approach completed and ignoredg. Property record card need not be reviewedh. Plaintiff’s report and testimony “fatally flawed”I. Appellate court defers to the expertise of the tax courtj. Small, typographical errors do not undercut the reportk. Adjustments must be made to explain differencesl. Attacking evidence post hearing is unacceptablem. Admitting an expert report and evidence and relying upon it was not an “abuse of discretion” by the trial judgen. Multiple approaches to value must be reconciled by the courto. Judge relied on both reports; cherry-picking; trial judge has the

discretion to adjust comparable sales after review and consideration of both reports

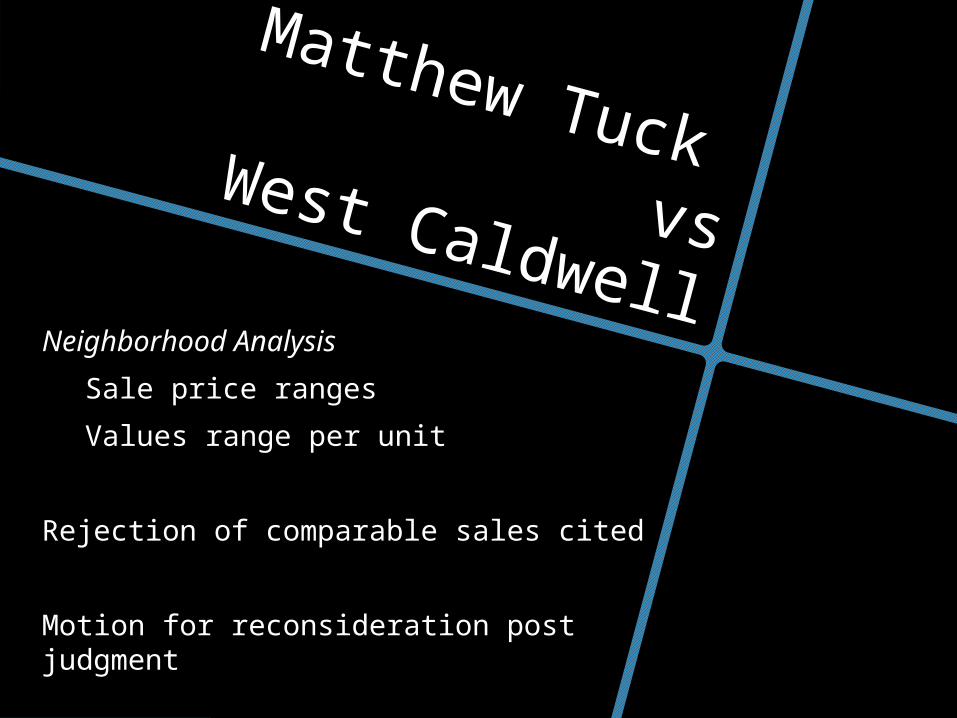

Matthew Tuck vs

West CaldwellNeighborhood Analysis

Sale price ranges

Values range per unit

Rejection of comparable sales cited

Motion for reconsideration post judgment

Elrabievs

Boro ofFranklin Lakes

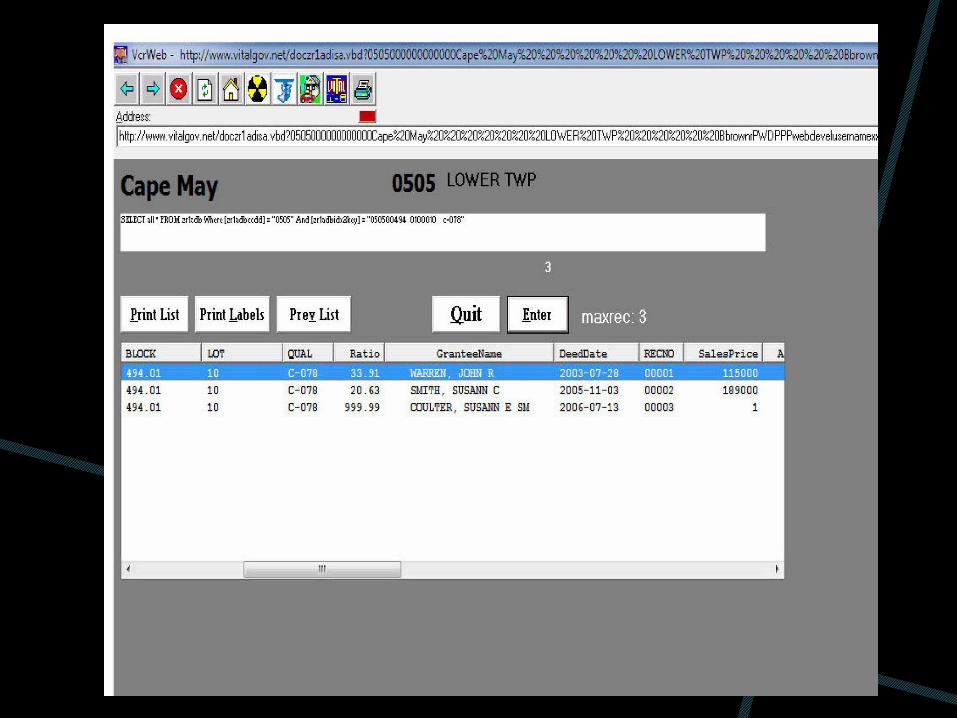

MeasurementsSuggest a mistake, any mistake

Interior inspections

Assessment records presumed correct

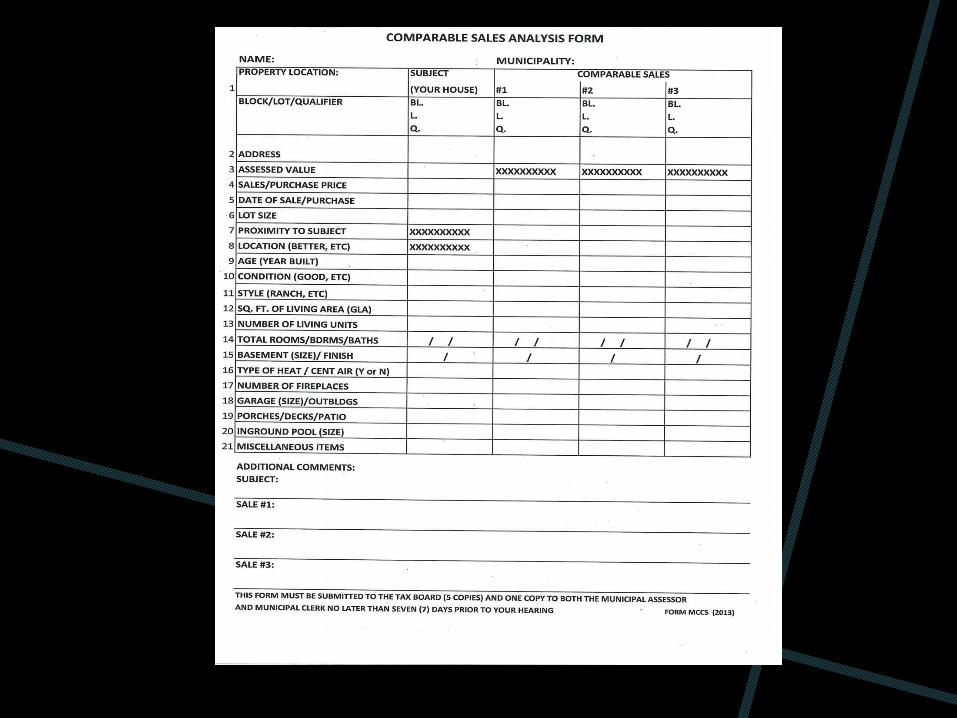

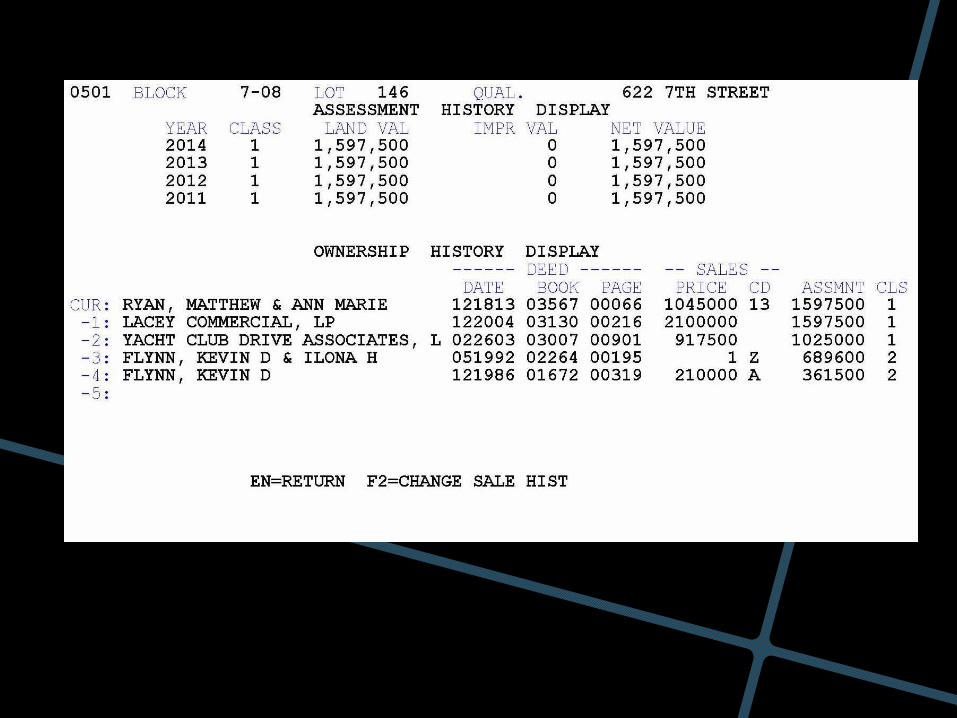

Common types of adjustments

Proper comparable sale selection

Comparable sales grid of plaintiffs’ appraiser

Unit of comparison $/Sq. Ft. of gross living area

Using a size related unit of comparison eliminates the need for size adjustments

More from Elrabie….

Condition v. Quality

Admitting reports (and testimony) into the record

Presumptions of correctness is describe in detail

Burden of proof remains with the plaintiff throughout the trial

The sales comparison approach is the best method of appraising a residence

What spills out of your mouth likely is not retractable; less is more

Chapter 123 is inapplicable in the year of a revaluation

Counter-claims (20 days), should not be made to achieve a tactical advantage

In dealing with the public, government must turn square corners!

Without a claim or counterclaim, the court is unable to increase an assessment in a revaluation year where Chapter 123 is inapplicable

Greenblatt

Englewood

vs

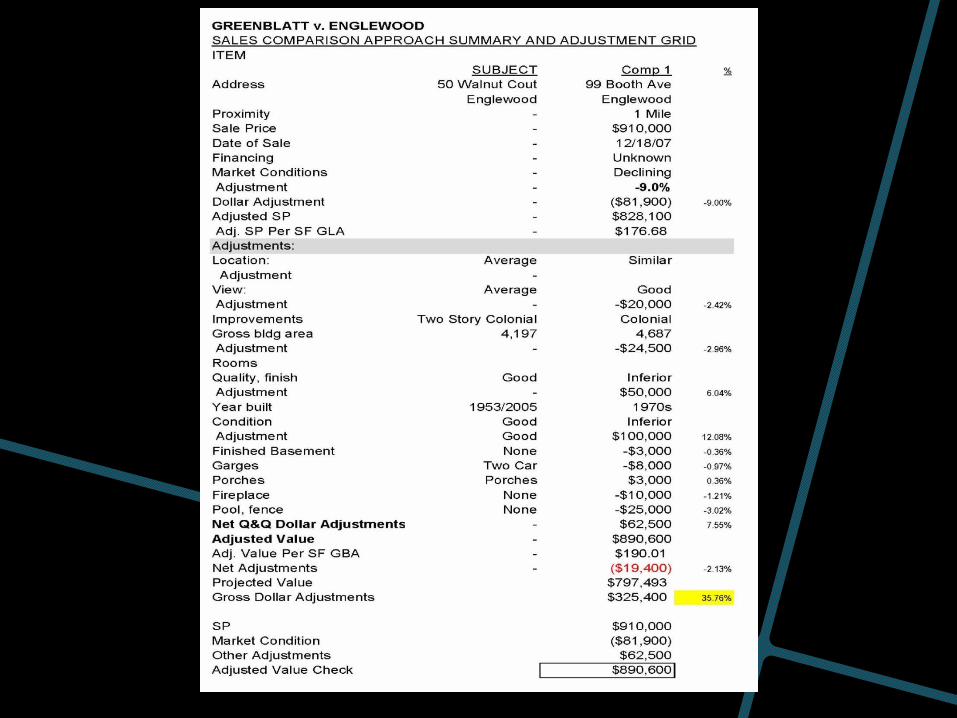

Discrepancy in building area; heated space

Estate sales as market evidence

Burden to prove that a sale is not bona fide falls on the challenger using creditable evidence

Failure to explain adjustments

Facts and data are necessary to support an expert’s opinion

Adjustments must have a foundation in market data; possibly supported by a cost manual

No support for the cost approach, not even a definition for the word ‘area’

Both appraisals tossed due to lack of support for adjustments

a. Using sales in another competitive district

b. Selective rejection of unsupported adjustments

c. Judgment based upon a fair preponderance of evidence provided by both parties

d. Cost approach is appropriate for valuing new or relatively new construction since cost and market are more closely related when properties are new; also applicable to special purpose buildings

e. The tax court is regarded as an expert; they may pick and choose what they rely upon from the expert’s testimony, reports, and the record

f. The court may not apply its own adjustments without support

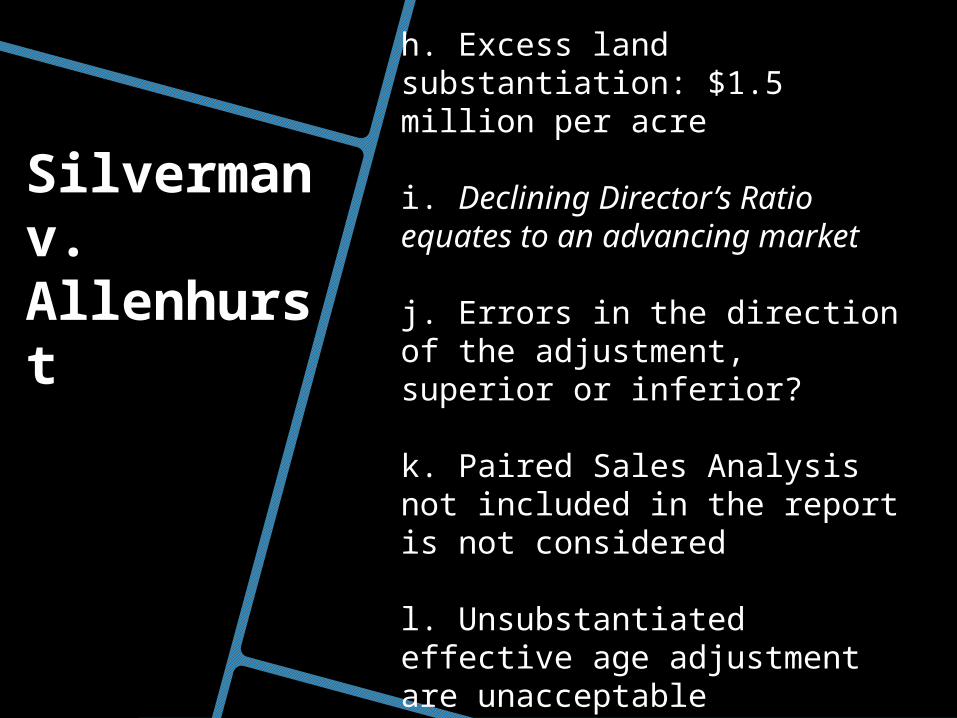

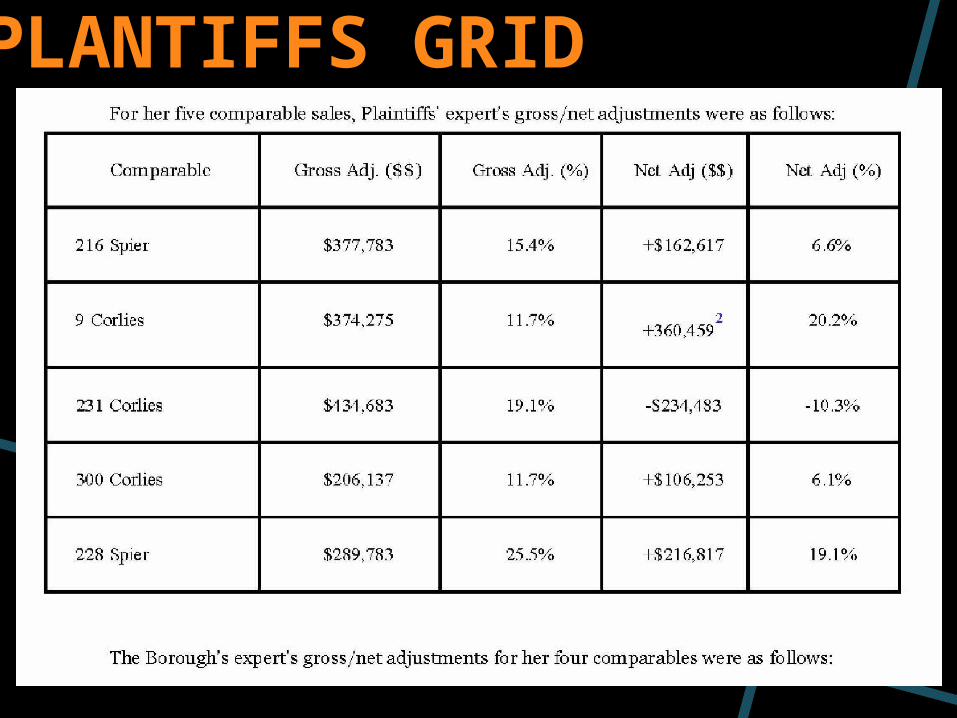

Silverman v. Allenhurst

g. Very often “adjustments made to comparable sales are subjective in nature.”

h. Excess land substantiation: $1.5 million per acre

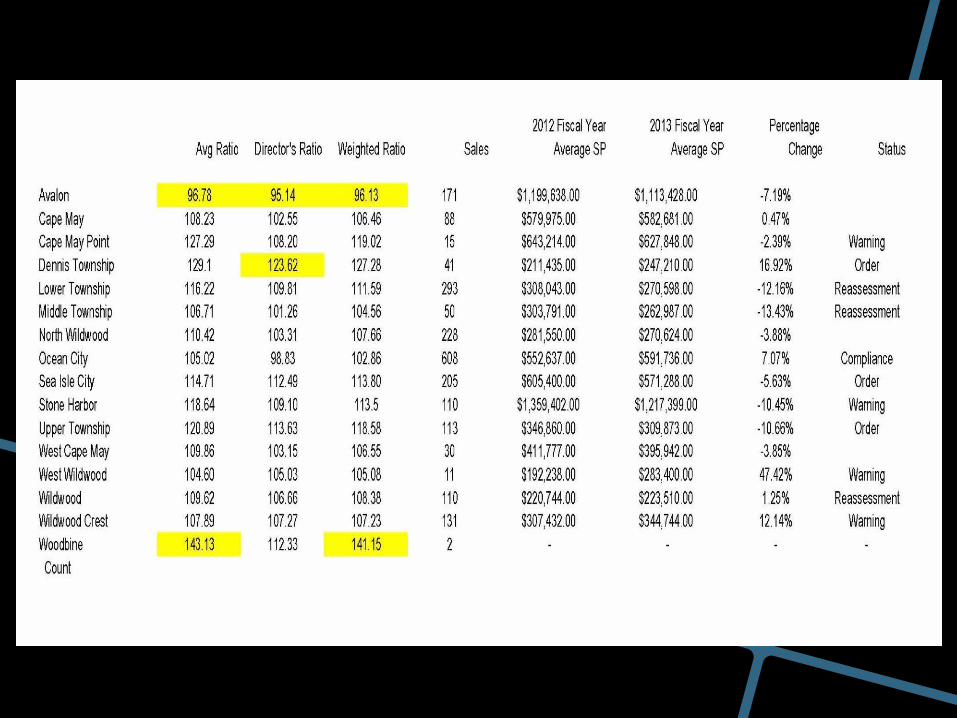

i. Declining Director’s Ratio equates to an advancing market

j. Errors in the direction of the adjustment, superior or inferior?

k. Paired Sales Analysis not included in the report is not considered

l. Unsubstantiated effective age adjustment are unacceptable

Silverman v. Allenhurst

DEFENDANTS GRID

PLANTIFFS GRID

JUDGE’S GRID

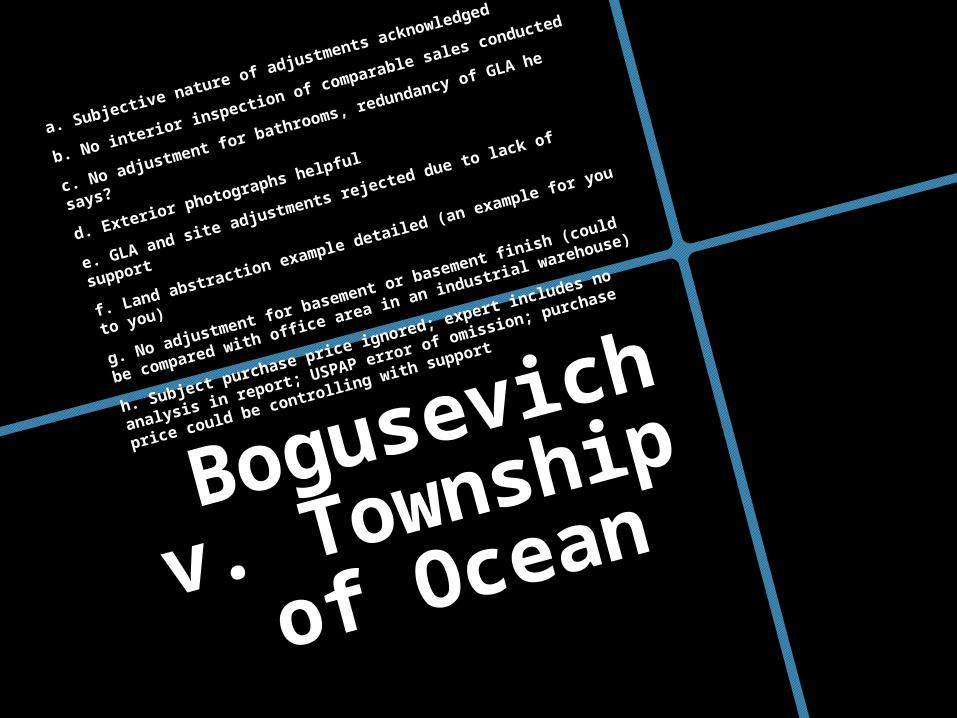

Bogusevich

v. Township

of Ocean

a. Subjective nature of adjustments acknowledged

b. No interior inspection of comparable sales conducted

c. No adjustment for bathrooms, redundancy of GLA he

says?

d. Exterior photographs helpful

e. GLA and site adjustments rejected due to lack of support

f. Land abstraction example detailed (an example for you to

you)

g. No adjustment for basement or basement finish (could be

compared with office area in an industrial warehouse)

h. Subject purchase price ignored; expert includes no

analysis in report; USPAP error of omission; purchase price

could be controlling with support

Common

Adjustment Issues

Adjustment Issues begin

with Comparable Sales

Selection

Com

para

ble

Sale

s Sele

ctio

n

Selected Sales must have the same highest and best use. The sales must be as similar as possible to the subject, reflecting the actions of typical buyers. You must assume the posture of the typical buyer. The goal is to find sales that require little adjustment. Common adjustments should be linked to the buyer’s perspective.

Common Adjustment Issues

A Comparable Sale Should be a Realistic Alternative Investment for Buyers in the Subject’s Market

Com

mon A

dju

stment

Solu

tions

Key Terms Relating to the

Adjustment Process

Paired

Sales

Matched

Pairs

Analysis

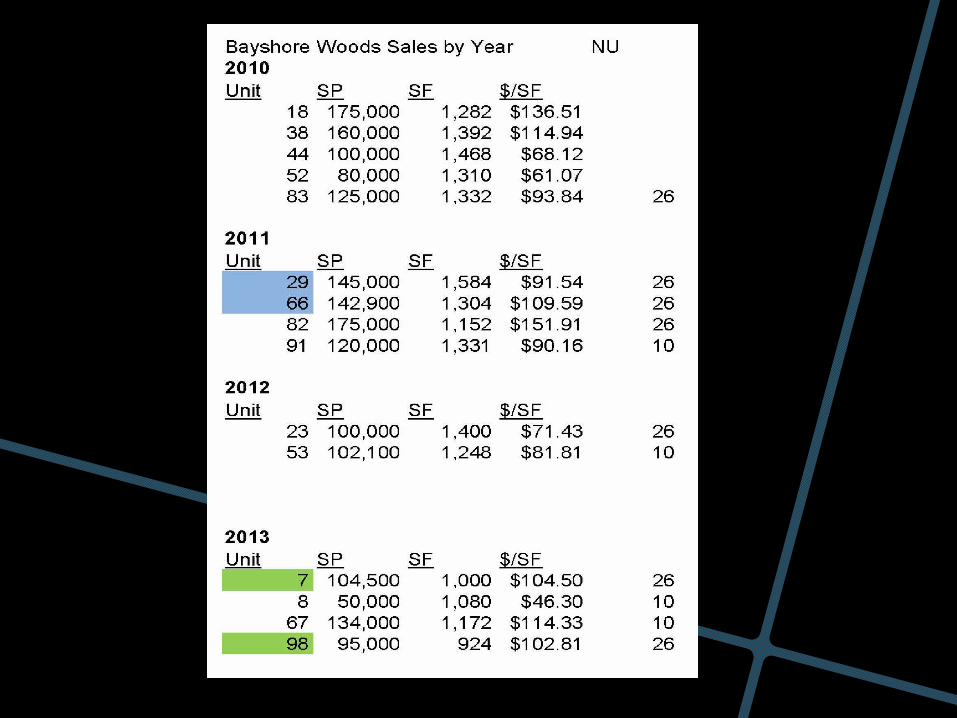

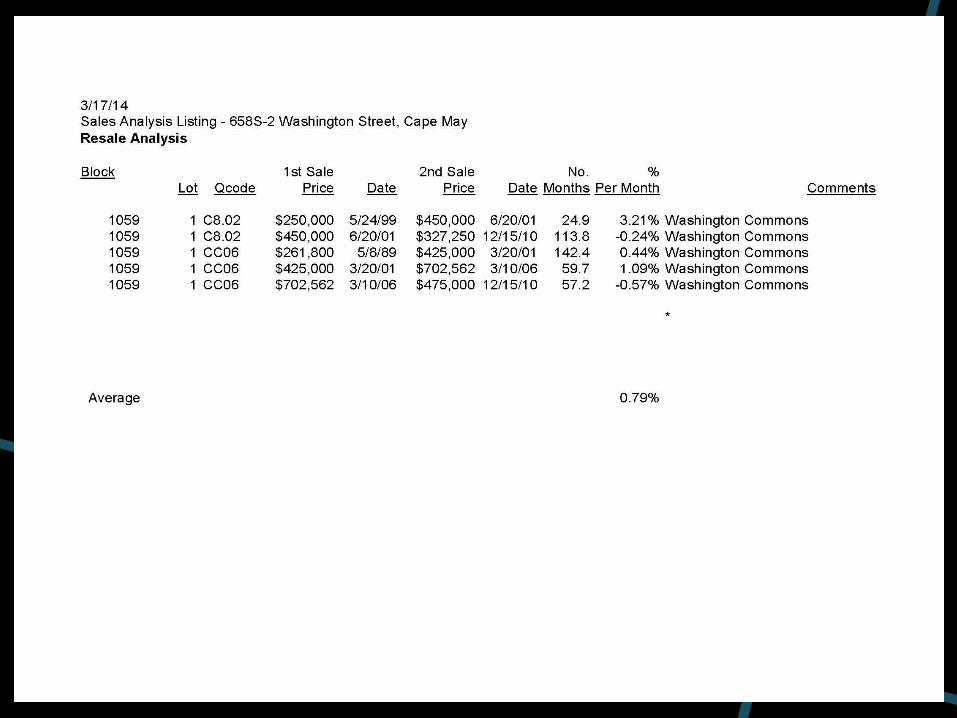

An Adjustment Derived from a Single Pair of Sales is Not necessarily Indicative

Just As a Single Sale Does Not Reflect Market Value

COMMON

ADJUSTMENTS

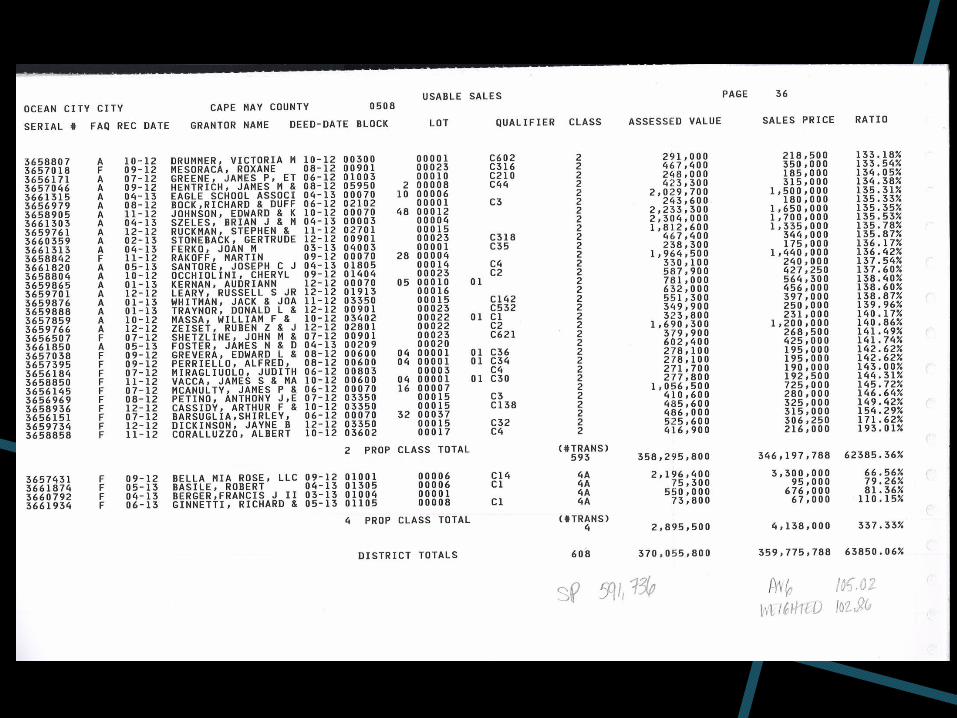

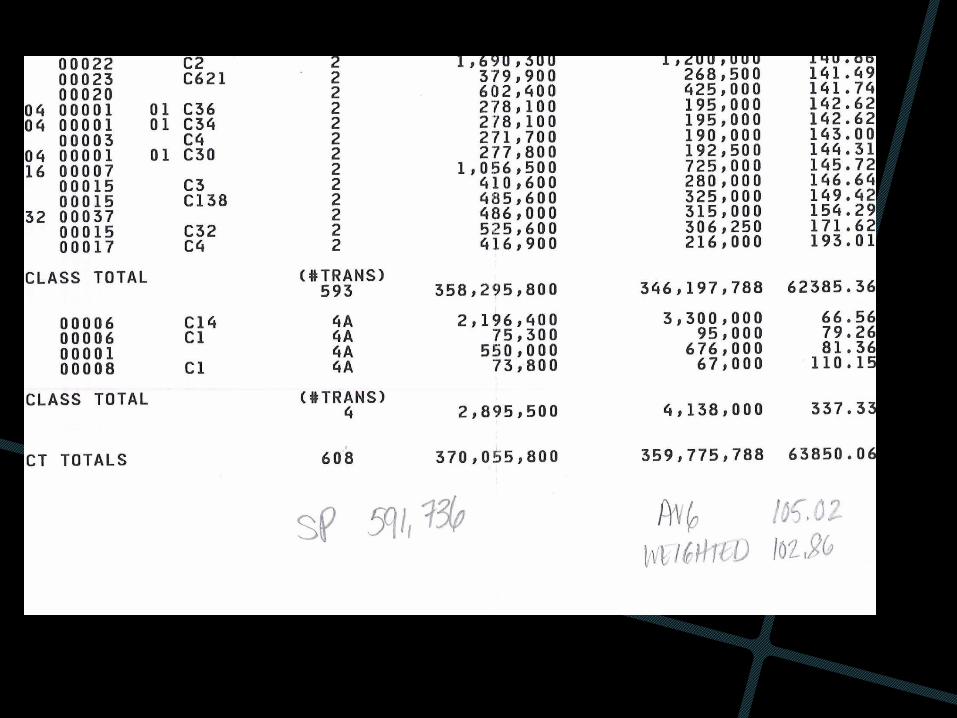

Adjustment Tools

based upon Market

Conditions

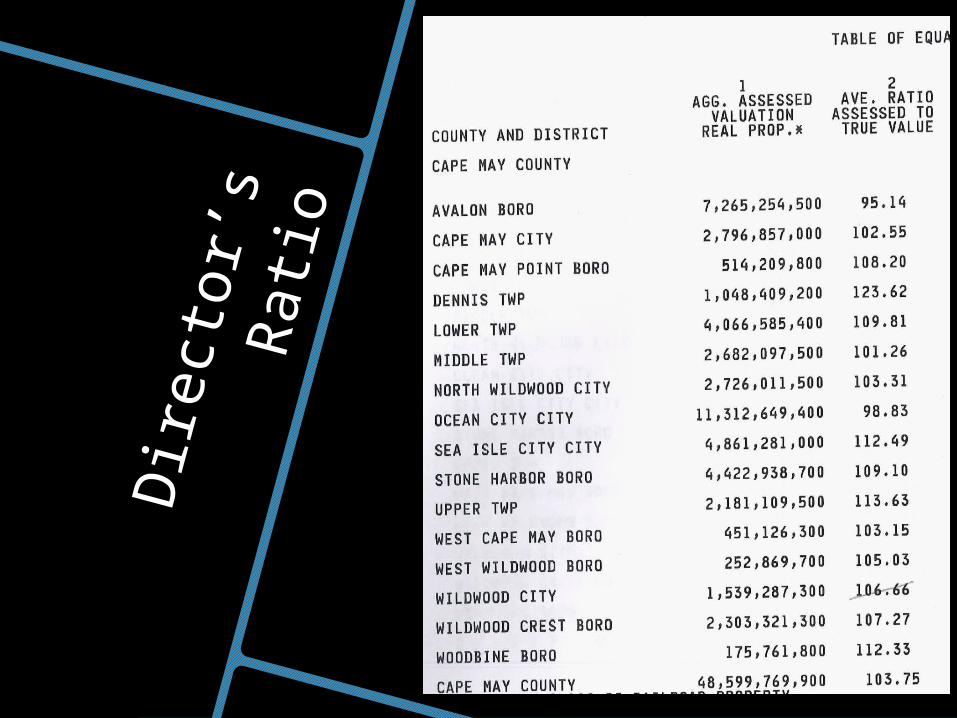

Dir

ect

or’

s R

ati

o

LOCATIONLOCATION

LOCATION

Underlying Land Values and their Analysis

Substantiate Location Adjustments and Much

More!

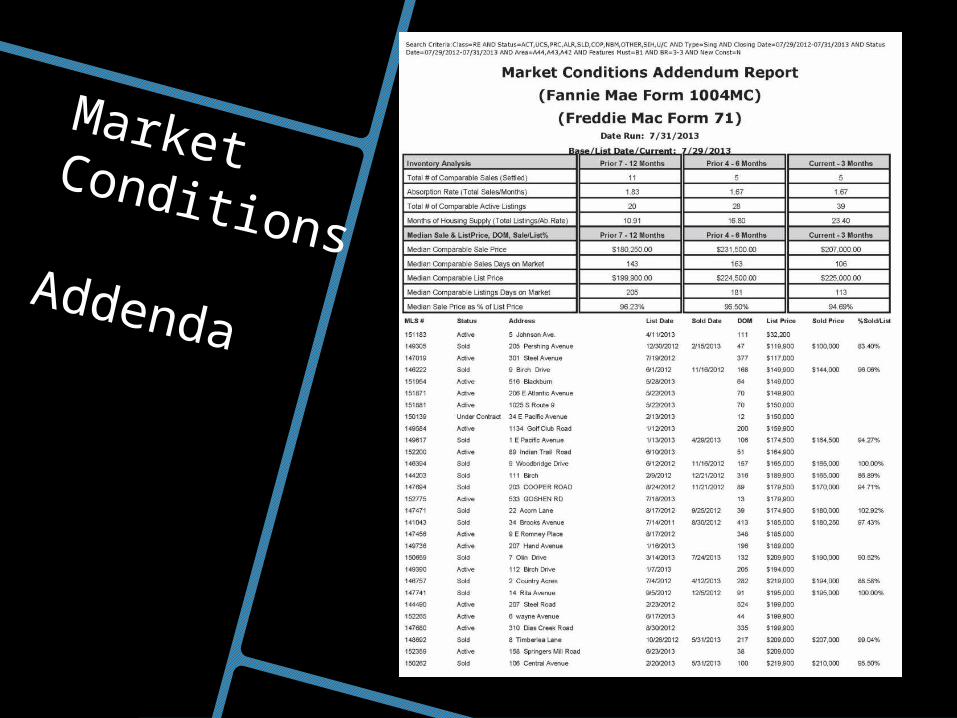

Market Conditions Addenda

GROSS BUILDING

AREA

ADJUSTMENTS

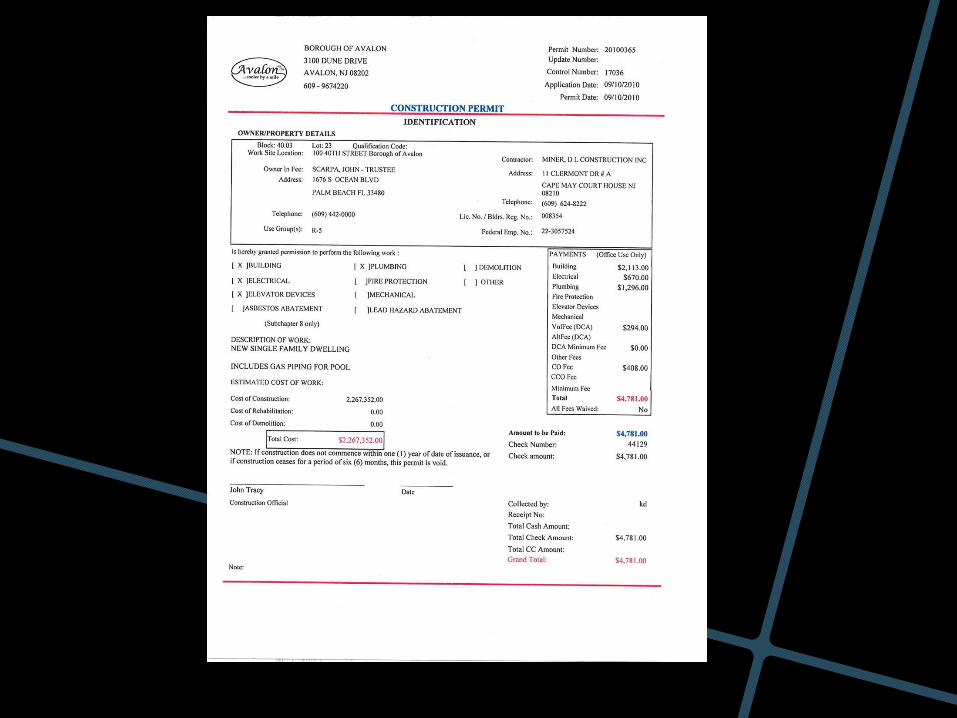

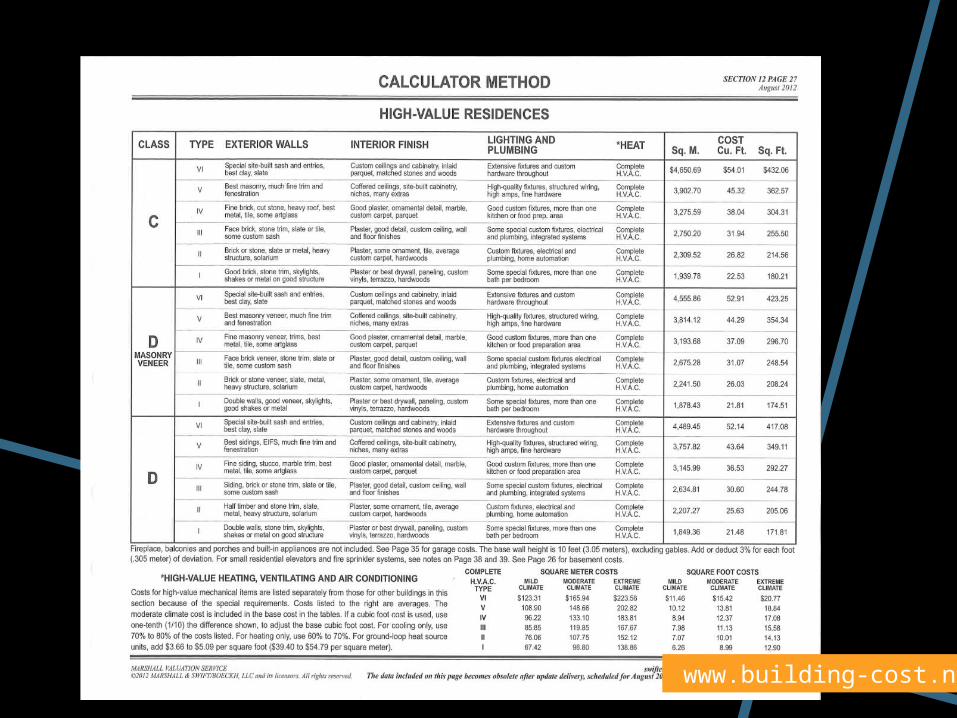

CONTRACTOR’S COST

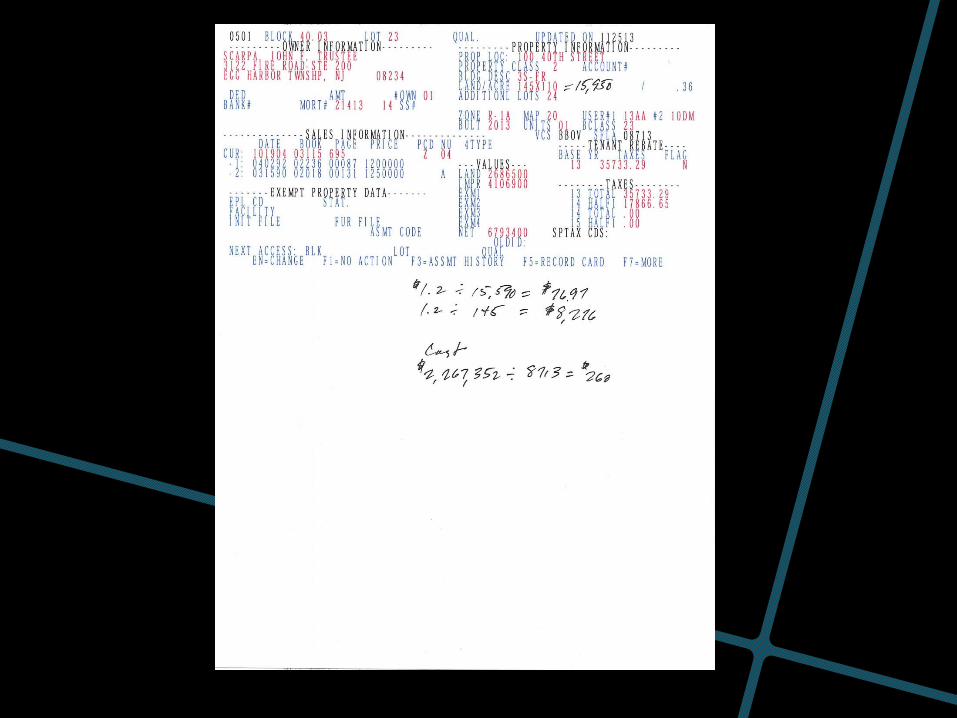

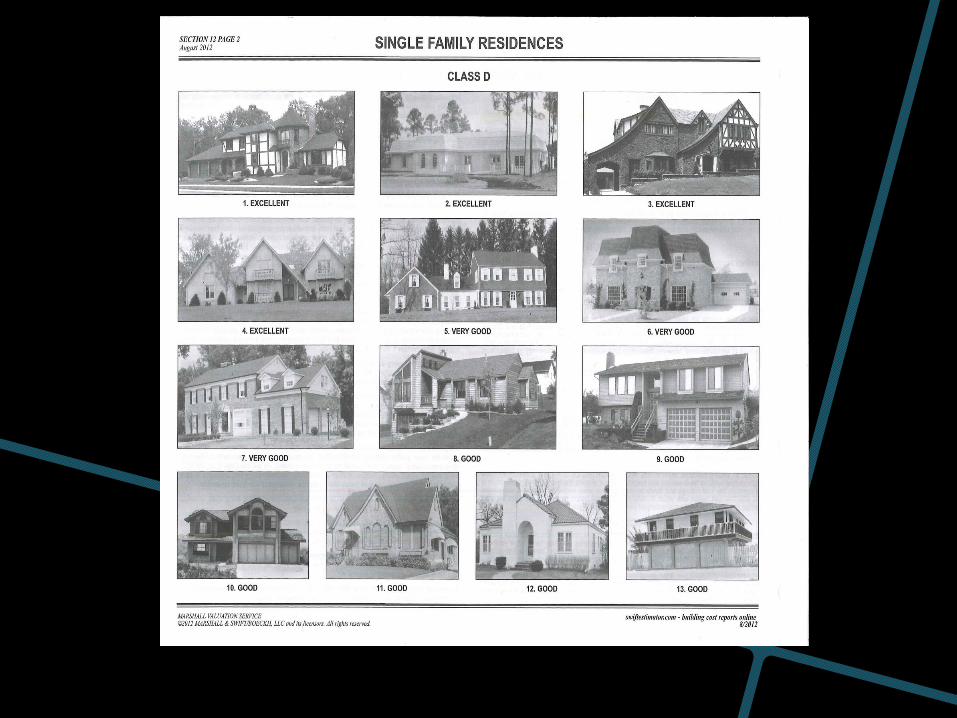

Assessor’s

Property Card?

QUALITY

CONDITIO

N

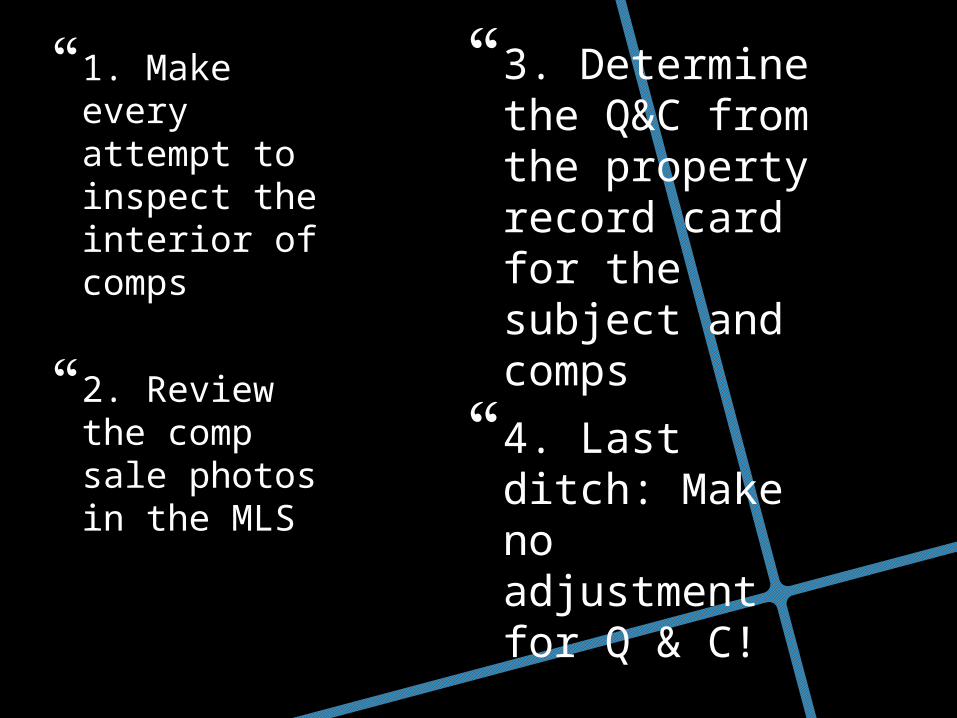

1. Make every attempt to inspect the interior of comps

2. Review the comp sale photos in the MLS

3. Determine the Q&C from the property record card for the subject and comps

4. Last ditch: Make no adjustment for Q & C!

www.building-cost.net