The Art of Economic Forecasting & the US ...

45

The Art of Economic Forecasting & the US Economic Forecasting & the US Economic Outlook Jeffrey C. Cleveland Senior Economist Payden & Rygel Investment Counsel Michael J. Budzik, CPA, CTP Directory of Treasury Directory of Treasury Zebra Technologies Corporation

Transcript of The Art of Economic Forecasting & the US ...

The Art of Economic Forecasting & the US EconomicForecasting & the US Economic

OutlookJeffrey C. Clevelandy

Senior EconomistPayden & Rygel Investment Counsel

Michael J. Budzik, CPA, CTPDirectory of TreasuryDirectory of Treasury

Zebra Technologies Corporation

The Art of Economic ForecastingThe Art of Economic Forecasting

The Problem: The Plight of the Fortune TellersI

II Types of Forecasting

Our Model: The NarrativeIII

The Output: GDP, Employment, Inflation, Interest Rates

IV

2

I The Problem: TheI The Problem: The Plight of the Fortune Tellers

3

The Problem: How do we make decisions about the future in a world of uncertainty?

Where is the economy headed?

What is the path of interest rates?

Wh t thWhat are the inflation/deflation

risks?

4The Cardsharps, Cavaggio (1594)

The Meteorologist or the Economist: Which is More Accurate?

Meteorology Economics

Physical science- Measurable

Rain

Social science- Challenging

Human Beings

Snow

Wind

Human Choice

Data Availability

Laboratory Experiments History, But Few Labs

“Most fundamentally, and perhaps most challenging for researchers, the crisis should motivate economists to think further b t th i d li f h b h i ” B B k ti i i th k f th fi i l i i

5

about their modeling of human behavior.” – Ben Bernanke commenting on economics in the wake of the financial crisis

II Types of ForecastsII Types of Forecasts

6

Types of ForecastsForecast Type Example

“Theory-free” forecasts

Leading Indicators

“Human behavior is simply too complex and nuanced to be fully represented

th ti ll t l tMathematical “models” of the economy

The Fed Model mathematically, at least with the maths known to modern man. Maths can help us to gain insight into

i b t itMarket-based models

The Yield Curve

“Th M t l M d l” C bi

economic processes, but it is not the only way to gain such insight, nor even the most productive.” -- DeLisleW ll G f th“The Mental Model” Combines

narrative + economic

indicators + market-based

Worrell, Governor of the Central Bank of Barbados

7indicators

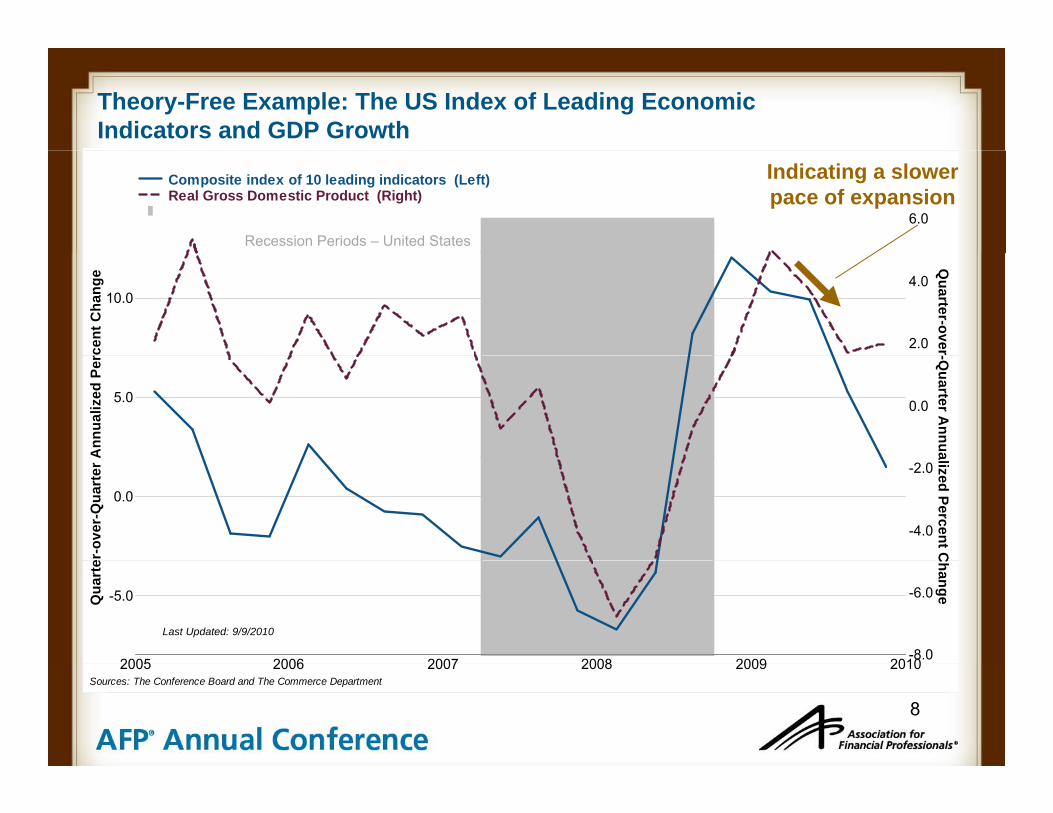

Theory-Free Example: The US Index of Leading Economic Indicators and GDP Growth

6.0

Composite index of 10 leading indicators (Left)Real Gross Domestic Product (Right)

Recession Periods – United States

Indicating a slowerpace of expansion

10.0

rcen

t Cha

nge

2.0

4.0

Quarter-over

5.0

Ann

ualiz

ed P

er

0.0

-Quarter A

nnua

0.0

er-o

ver-

Qua

rter

A

-4.0

-2.0

alized Percent C

2005 2006 2007 2008 2009 2010

-5.0Qua

rte

-8.0

-6.0

Change

Last Updated: 9/9/2010

8

2005 2006 2007 2008 2009 2010Sources: The Conference Board and The Commerce Department

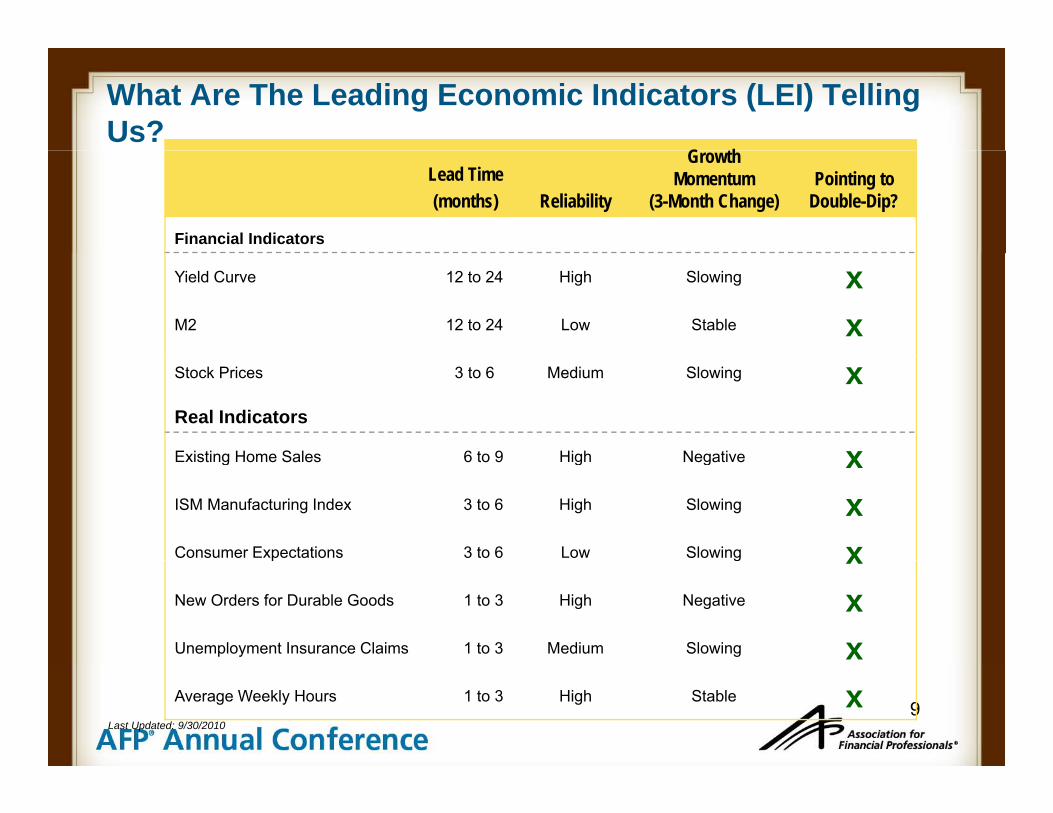

What Are The Leading Economic Indicators (LEI) Telling Us?

G th Lead Time(months) Reliability

Growth Momentum

(3-Month Change)Pointing to

Double-Dip?

Financial Indicators

Yield Curve 12 to 24 High Slowing xM2 12 to 24 Low Stable xStock Prices 3 to 6 Medium Slowing xReal Indicators

Existing Home Sales 6 to 9 High Negative xExisting Home Sales 6 to 9 High Negative xISM Manufacturing Index 3 to 6 High Slowing xConsumer Expectations 3 to 6 Low Slowing xp g xNew Orders for Durable Goods 1 to 3 High Negative xUnemployment Insurance Claims 1 to 3 Medium Slowing x

9Average Weekly Hours 1 to 3 High Stable x

Last Updated: 9/30/2010

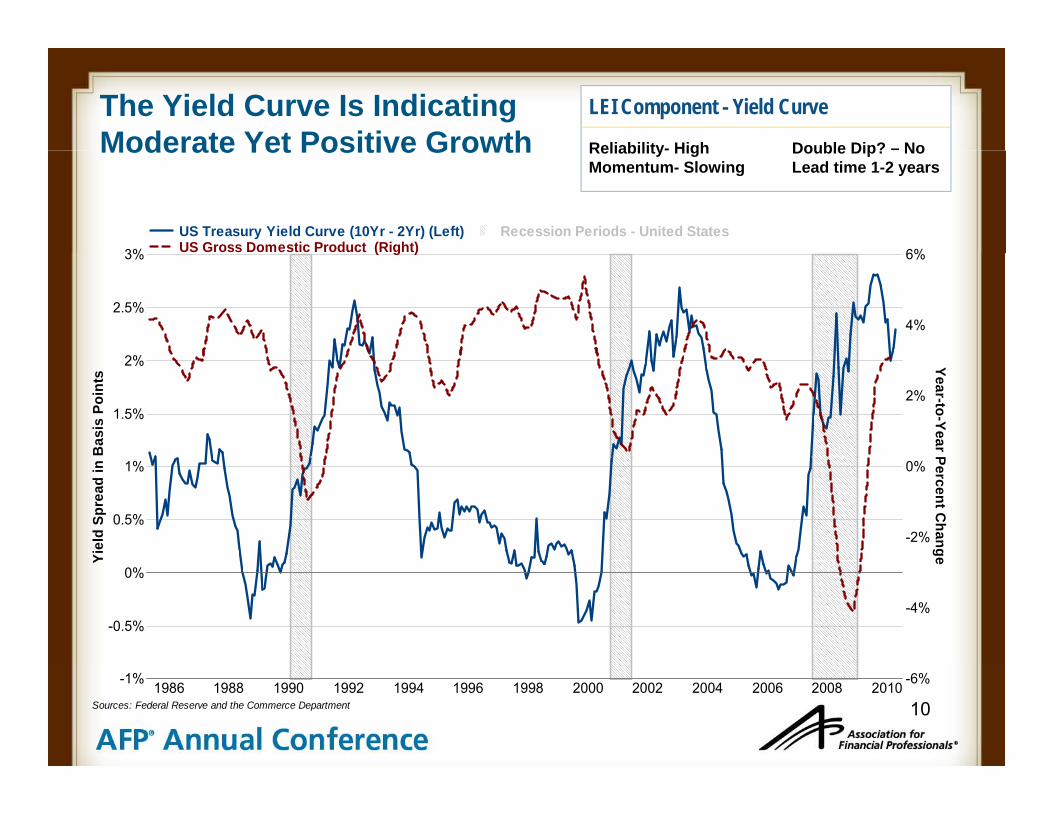

The Yield Curve Is Indicating Moderate Yet Positive Growth

LEI Component - Yield Curve

Reliability- High Double Dip? – NoModerate Yet Positive Growth

3% 6%US Treasury Yield Curve (10Yr - 2Yr) (Left)US Gross Domestic Product (Right)

Recession Periods - United States

Reliability- High Double Dip? NoMomentum- Slowing Lead time 1-2 years

2%

2.5%

3%

4%

6%( g )

1.5%

2%

Bas

is P

oint

s

2%

Year-to-Year P

0.5%

1%

Yiel

d Sp

read

in

-2%

0%

Percent Change

-0.5%

0%

Y

-4%

e

101986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010-1% -6%

Sources: Federal Reserve and the Commerce Department

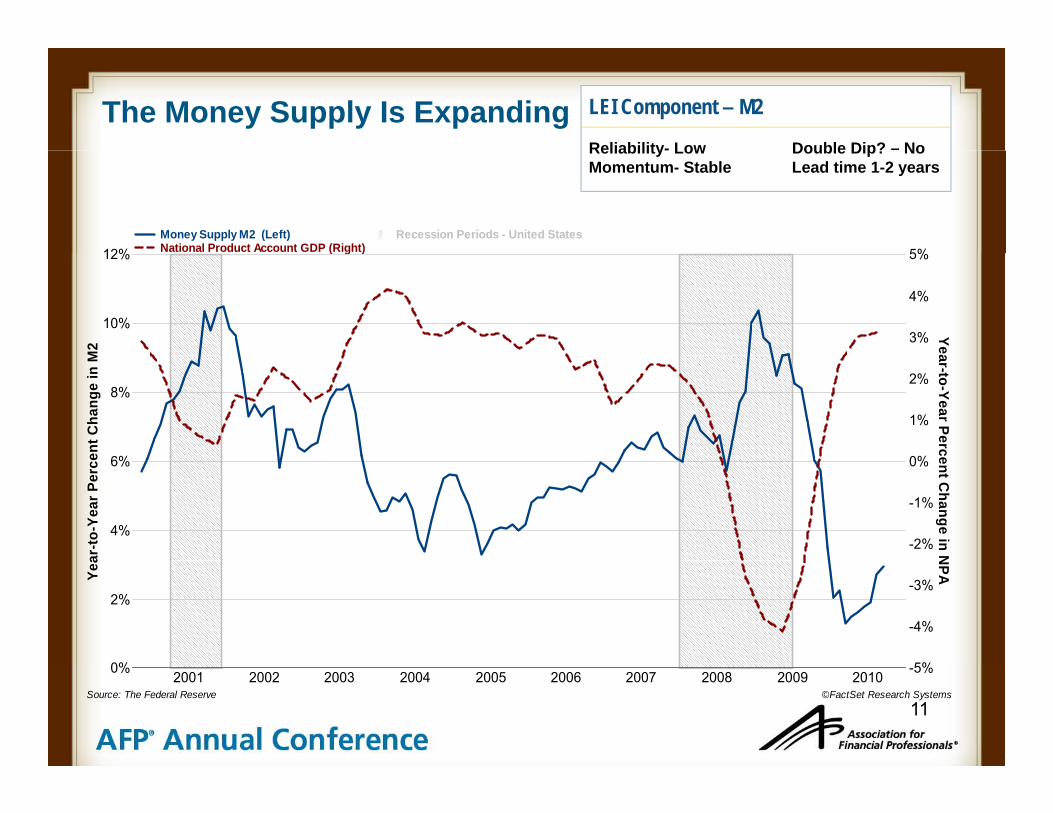

The Money Supply Is Expanding LEI Component – M2

Reliability- Low Double Dip? – No

12% 5%Money Supply M2 (Left)National Product Account GDP (Right)

Recession Periods - United States

Reliability- Low Double Dip? NoMomentum- Stable Lead time 1-2 years

10%

12%

M2 3%

4%

5%

Yea

( g )

6%

8%

ent C

hang

e in

M

0%

1%

2%

ar-to-Year Perce

4%

6%

ar-to

-Yea

r Per

ce

-2%

-1%

0% ent Change in N

0%

2%

Yea

5%

-4%

-3%

NPA

11

2001 2002 2003 2004 2005 2006 2007 2008 2009 20100% -5%

©FactSet Research SystemsSource: The Federal Reserve

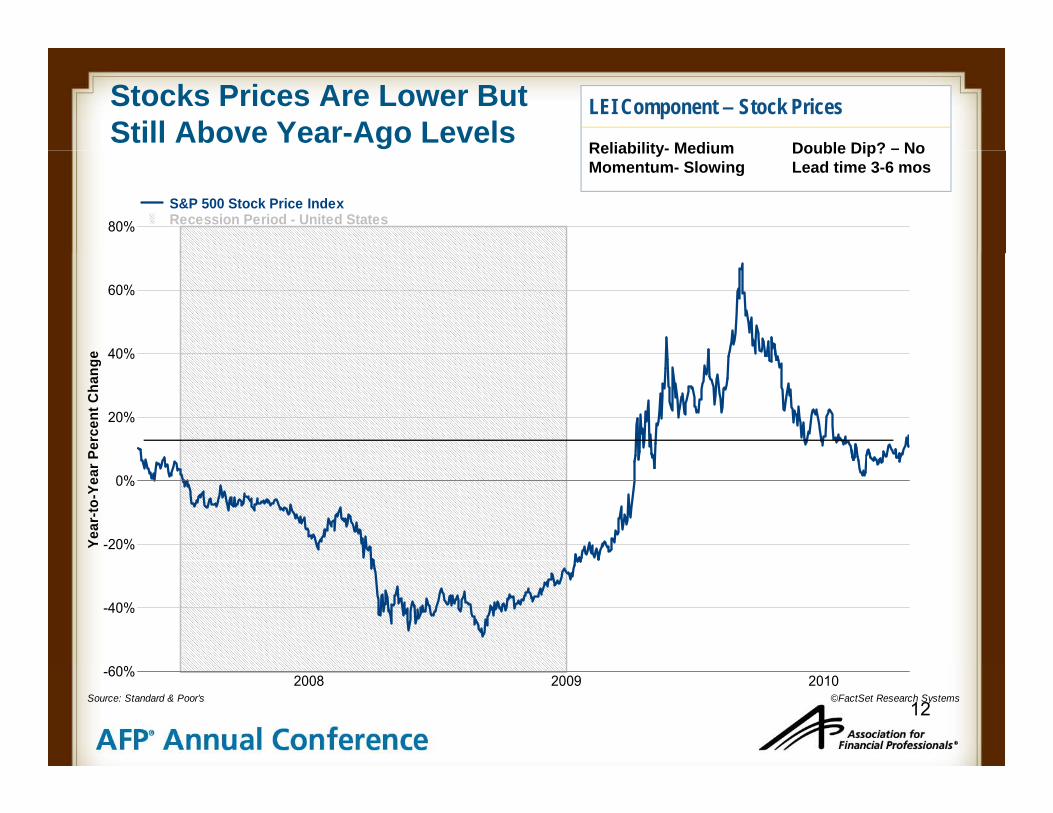

Stocks Prices Are Lower But Still Above Year-Ago Levels

LEI Component – Stock Prices

Reliability- Medium Double Dip? – No

80%S&P 500 Stock Price Index Recession Period - United States

Reliability- Medium Double Dip? NoMomentum- Slowing Lead time 3-6 mos

40%

60%

e

20%

40%

Perc

ent C

hang

e

-20%

0%

Year

-to-Y

ear P

-40%

122008 2009 2010-60%

©FactSet Research SystemsSource: Standard & Poor's

Post Tax-Credit, Home Sales Suffer

LEI Component – Home Sales

Reliability- High Double Dip? –

30% 5%US Existing-Home Sales (Left)US Real Gross Domestic Product (Right)

Recession Periods - United States

Reliability- High Double Dip? MaybeMomentum- Negative Lead time 6-9 mos

20%

30%

es

3%

4%

5%( g )

Impact of theFederal Home

buyer Tax Credit

10%

ge in

Hom

e Sa

le

1%

2%

Year-to-Year C

-10%

0%

r-to

-Yea

r Cha

ng

-2%

-1%

0%

Change in G

DP

-20%

Yea

-4%

-3%

132001 2002 2003 2004 2005 2006 2007 2008 2009 2010

-30% -5%

Sources: National Association of Realtors and Commerce Department

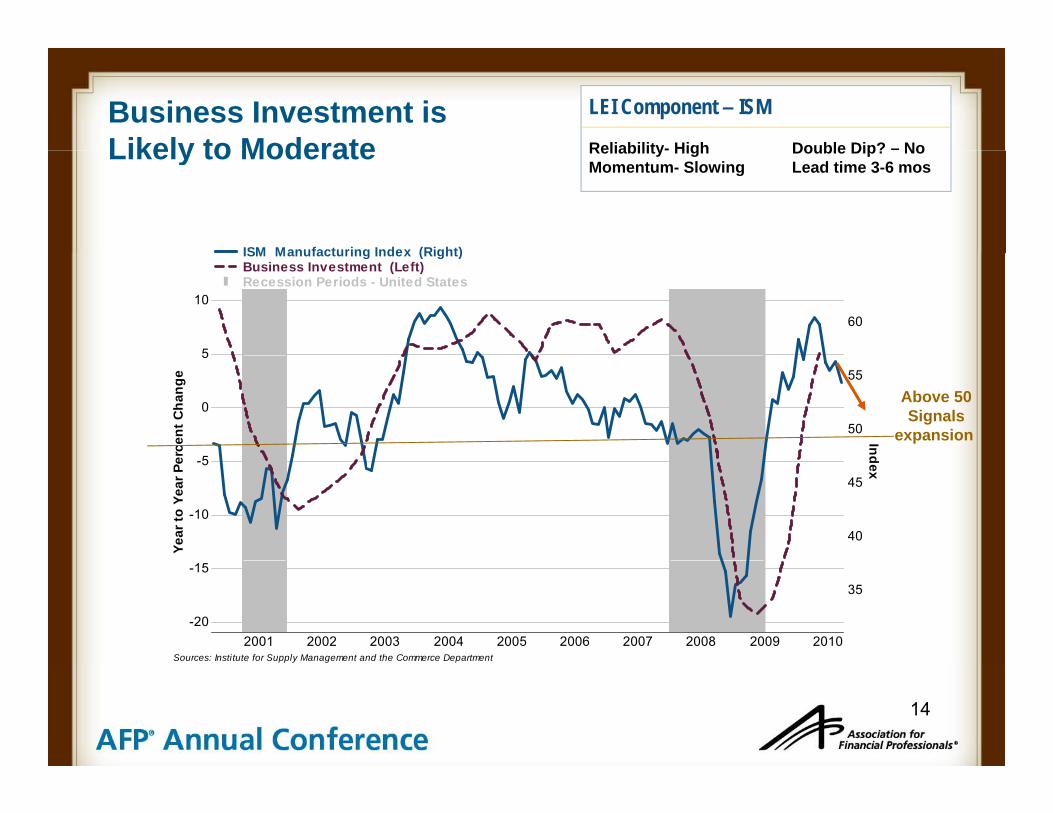

Business Investment is Likely to Moderate

LEI Component – ISM

Reliability- High Double Dip? – NoLikely to Moderate

ISM Manufacturing Index (Right)

Reliability- High Double Dip? NoMomentum- Slowing Lead time 3-6 mos

5

1060

ISM Manufacturing Index (Right)Business Investment (Left)Recession Periods - United States

5

0

5

erce

nt C

hang

e

50

55

Ind

Above 50Signals

expansion

-10

-5

Year

to Y

ear P

e

40

45

dex

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-20

-1535

Sources: Institute for Supply Management and the Commerce Department

14

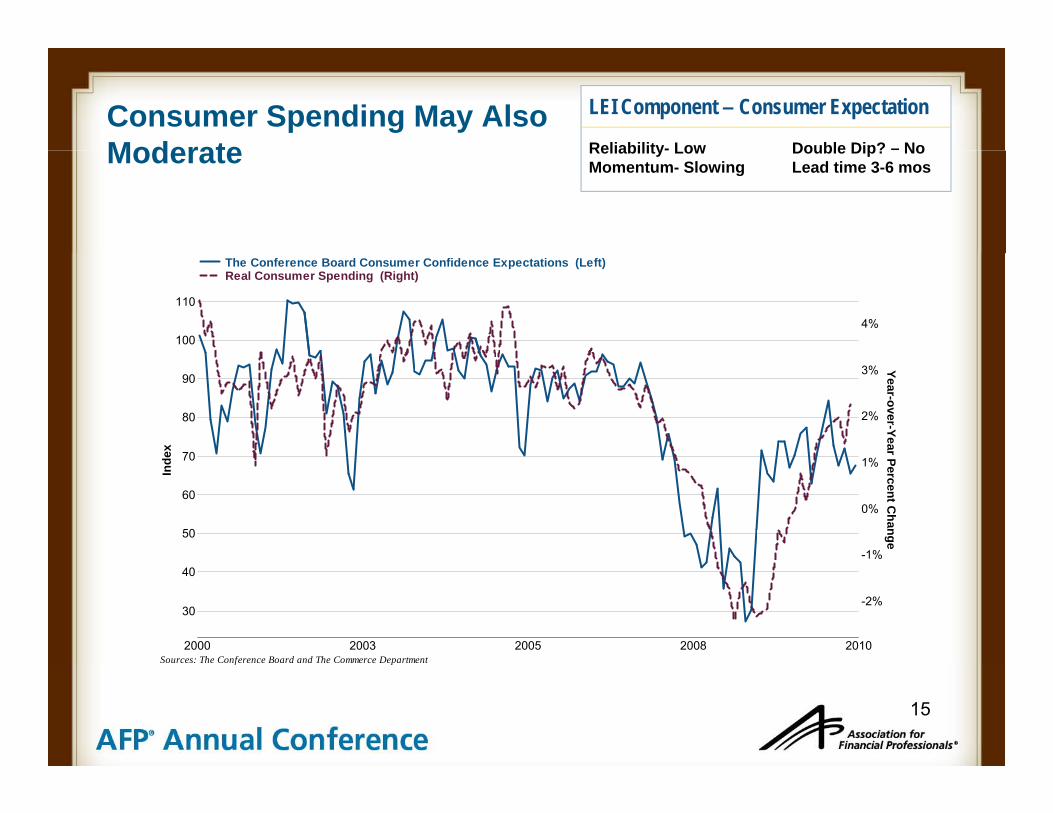

Consumer Spending May AlsoModerate

LEI Component – Consumer Expectation

Reliability- Low Double Dip? – NoModerate Reliability- Low Double Dip? NoMomentum- Slowing Lead time 3-6 mos

100

110

4%

The Conference Board Consumer Confidence Expectations (Left)Real Consumer Spending (Right)

70

80

90

ex

1%

2%

3% Year-over-Year

50

60

70

Ind

-1%

0%

1%

Percent Change

2000 2003 2005 2008 2010

30

40

-2%

Sources: The Conference Board and The Commerce Department

15

f p

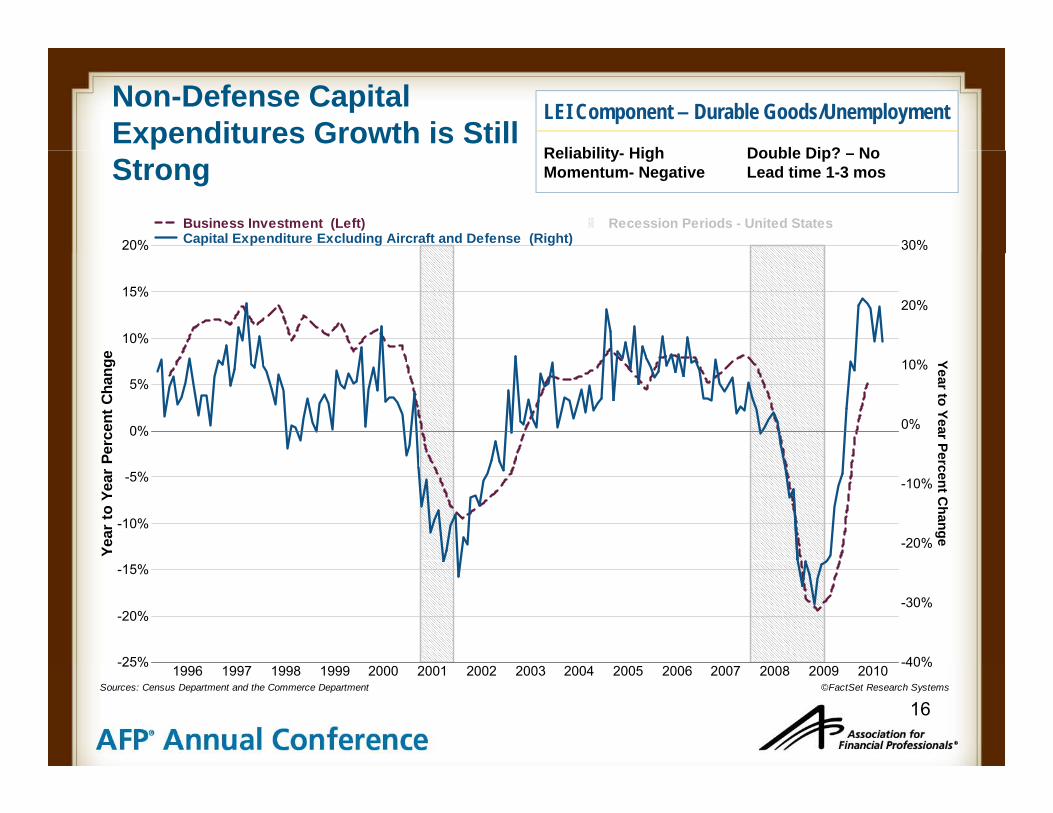

Non-Defense Capital Expenditures Growth is Still

LEI Component – Durable Goods/Unemployment

Reliability High Double Dip? No

20% 30%Business Investment (Left)Capital Expenditure Excluding Aircraft and Defense (Right)

Recession Periods - United States

StrongReliability- High Double Dip? – NoMomentum- Negative Lead time 1-3 mos

10%

15%

e

20%

0%

5%

Perc

ent C

hang

e

0%

10%

Year to Year Pe

-10%

-5%

Year

to Y

ear

P

-20%

-10%

ercent Change

-25%

-20%

-15%

-40%

-30%

16

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-25% -40%

©FactSet Research SystemsSources: Census Department and the Commerce Department

Average Workweek and Jobless Claims Stabilizing

LEI Component

Reliability- High Double Dip? – No

39 650

Initial Claims for Unemployment Insurance (Right)Average Workweek (Left)

Recession Periods - United States

Claims Stabilizing Reliability- High Double Dip? NoMomentum- Stable Lead time 1-3 mos

39

39.5

Hou

rs)

550

600

650

W

g ( )

40

40 5ng W

orkw

eek

(H

450

500

550

Weekly U

nemp

40.5

41

e M

anuf

actu

rin

350

400

450

ployment C

laim

41.5

42

Ave

rage

250

300

350

ms

17

2000 2001 2002 2004 2005 2006 2007 2008 2009 201042 250

Example: Mathematical Models of the Economy

Th EAbstracting Further…

The Economy

Standard Regression Model:

Y = α + β1x1 + β2x2 + β3x3 + εβ1 1 β2 2 β3 3

ExampleIS (Investment-Savings) Equation of a National Economyof a National Economy

Y = C(Y-T(Y)) + I(i) + G + NX(Y)

18

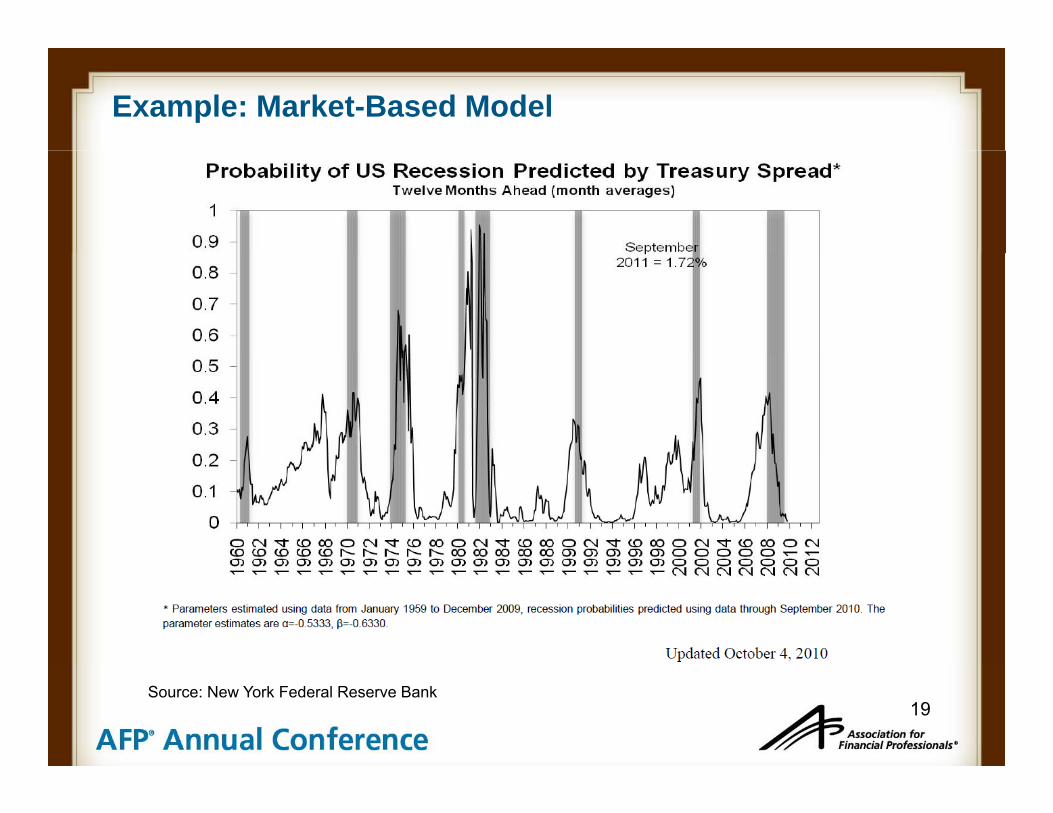

Example: Market-Based Model

19Source: New York Federal Reserve Bank

III Our Model: TheIII Our Model: The Narrative

20

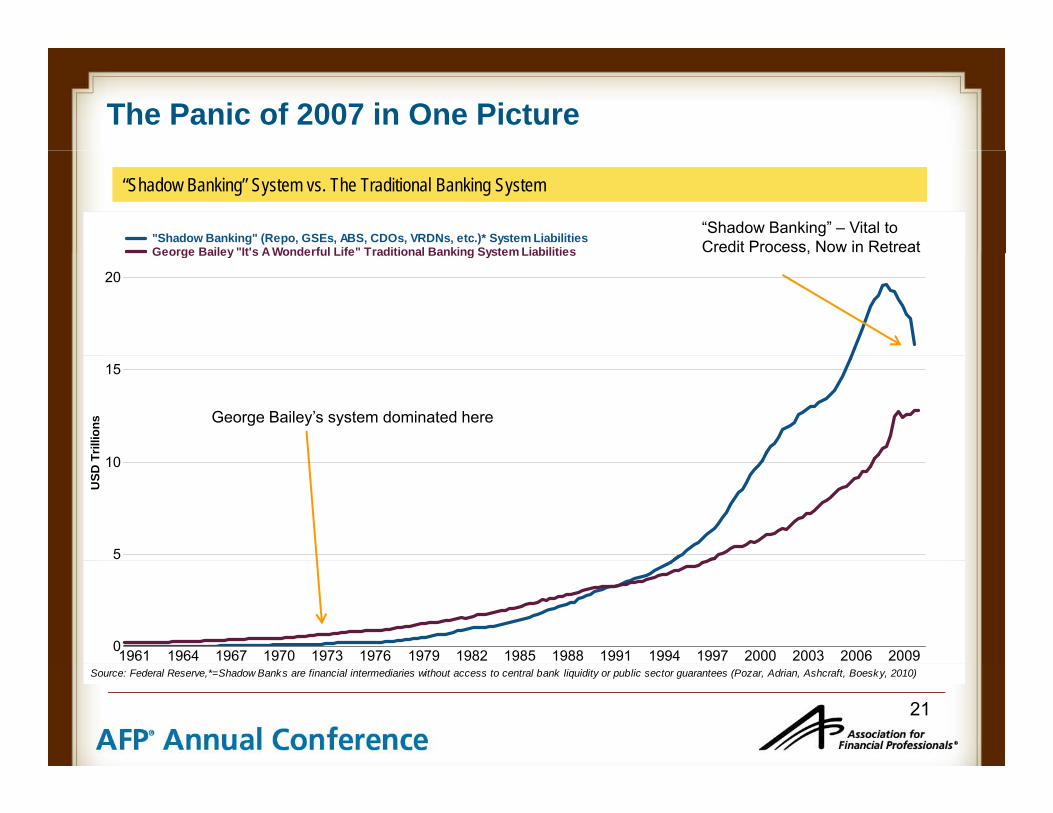

The Panic of 2007 in One Picture

"Shadow Banking" (Repo, GSEs, ABS, CDOs, VRDNs, etc.)* System LiabilitiesGeorge Bailey "It's A Wonderful Life" Traditional Banking System Liabilities

“Shadow Banking” System vs. The Traditional Banking System

“Shadow Banking” – Vital to Credit Process, Now in Retreat

20

George Bailey It s A Wonderful Life Traditional Banking System Liabilities ,

10

15

Trill

ions George Bailey’s system dominated here

5

10

USD

T

1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 20090

21

Source: Federal Reserve,*=Shadow Banks are financial intermediaries without access to central bank liquidity or public sector guarantees (Pozar, Adrian, Ashcraft, Boesky, 2010)

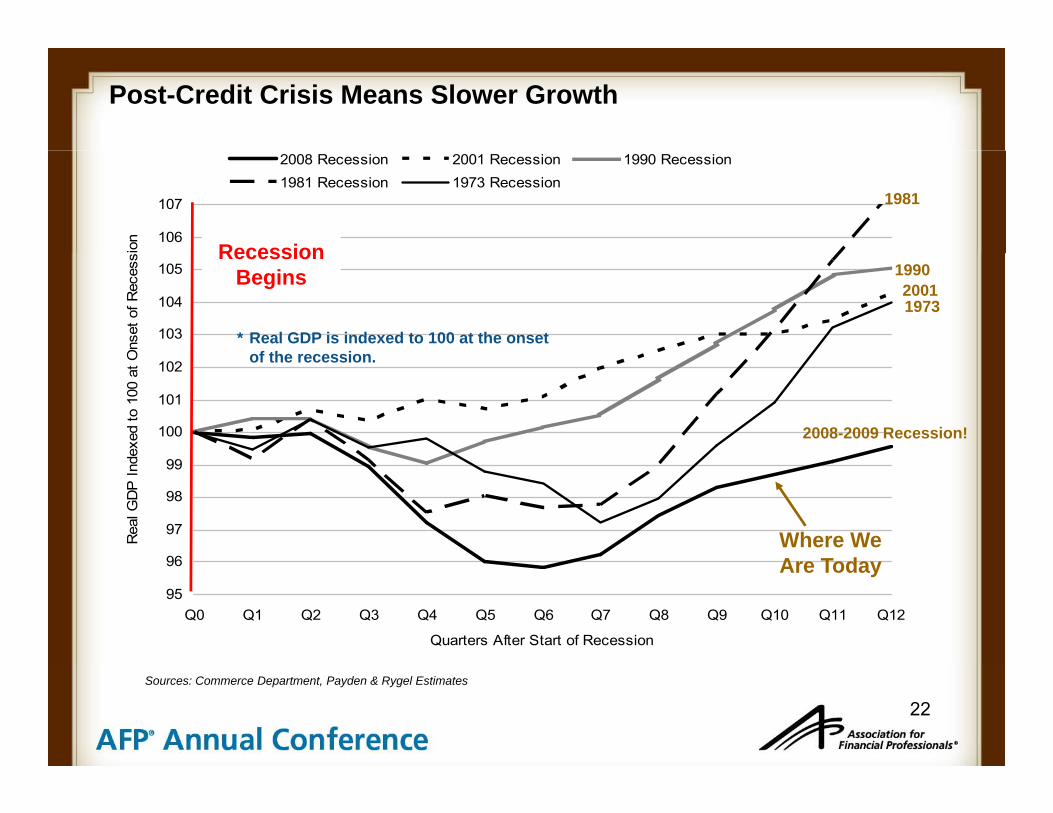

Post-Credit Crisis Means Slower Growth

106

107

ion

2008 Recession 2001 Recession 1990 Recession1981 Recession 1973 Recession

Recession

1981

103

104

105

Ons

et o

f Rec

ess Recession

Begins

* Real GDP is indexed to 100 at the onset of the recession

1973

19902001

100

101

102

dexe

d to

100

at O

2008-2009 Recession!

of the recession.

96

97

98

99

Rea

l GD

P In

d

Where We A T d

95

96

Q0 Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 Q9 Q10 Q11 Q12

Quarters After Start of Recession

Are Today

22Sources: Commerce Department, Payden & Rygel Estimates

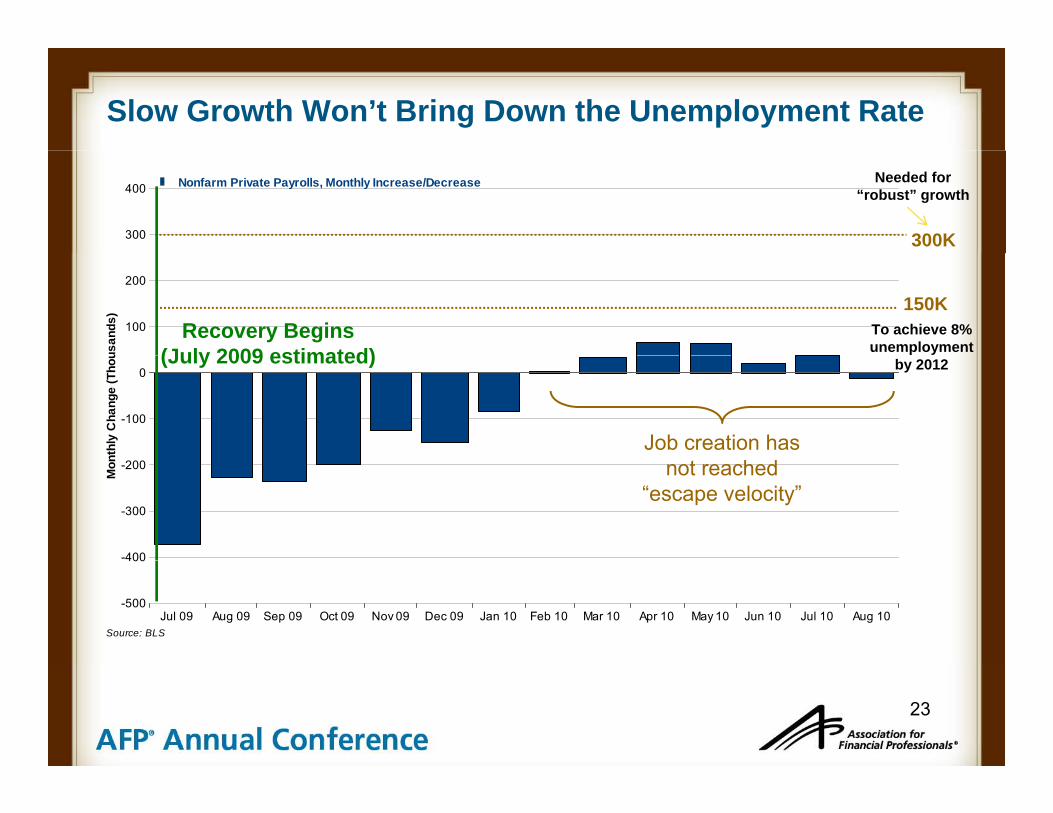

Slow Growth Won’t Bring Down the Unemployment Rate

300

400 Nonfarm Private Payrolls, Monthly Increase/Decrease

300K

Needed for “robust” growth

100

200

usan

ds) 150K

Recovery Begins (July 2009 estimated)

To achieve 8% unemployment

-100

0

nthl

y C

hang

e (T

hou (July 2009 estimated)

Job creation has

by 2012

-400

-300

-200

Mon not reached

“escape velocity”

Jul 09 Aug 09 Sep 09 Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10 Jun 10 Jul 10 Aug 10-500

400

Source: BLS

23

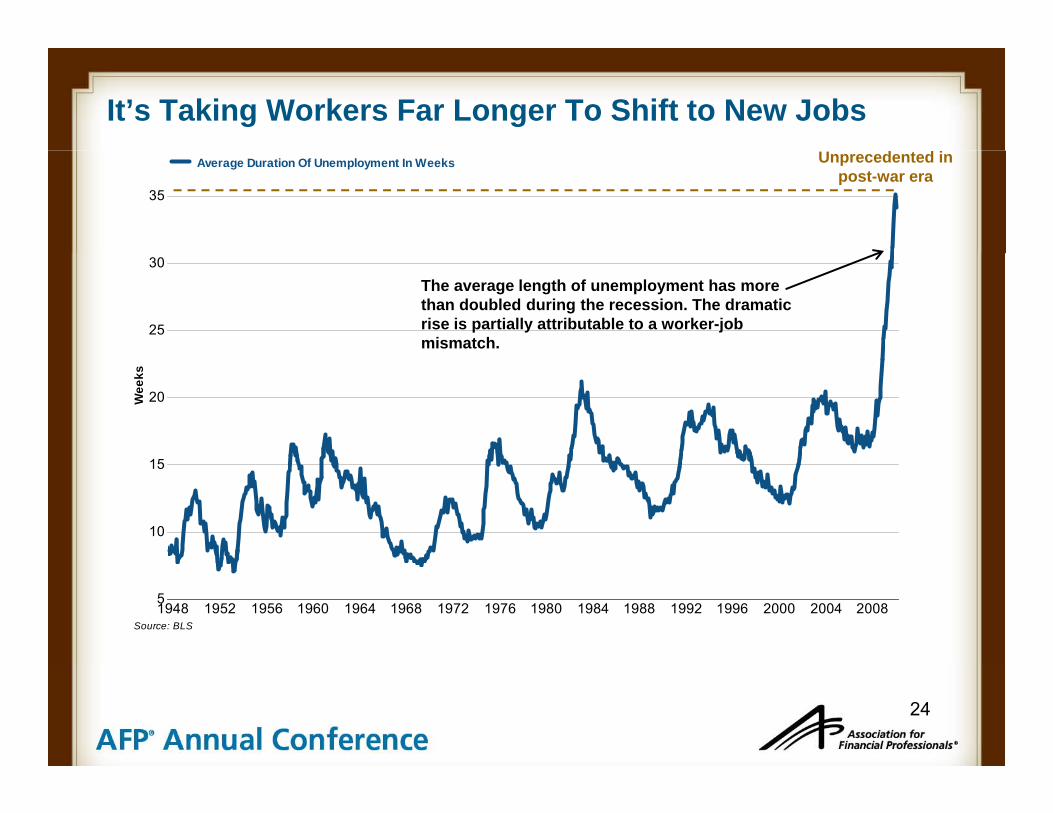

It’s Taking Workers Far Longer To Shift to New Jobs

35

Average Duration Of Unemployment In Weeks Unprecedented in post-war era

25

30

The average length of unemployment has more than doubled during the recession. The dramatic rise is partially attributable to a worker-job mismatch.

20Wee

ks

10

15

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 20085

Source: BLS

24

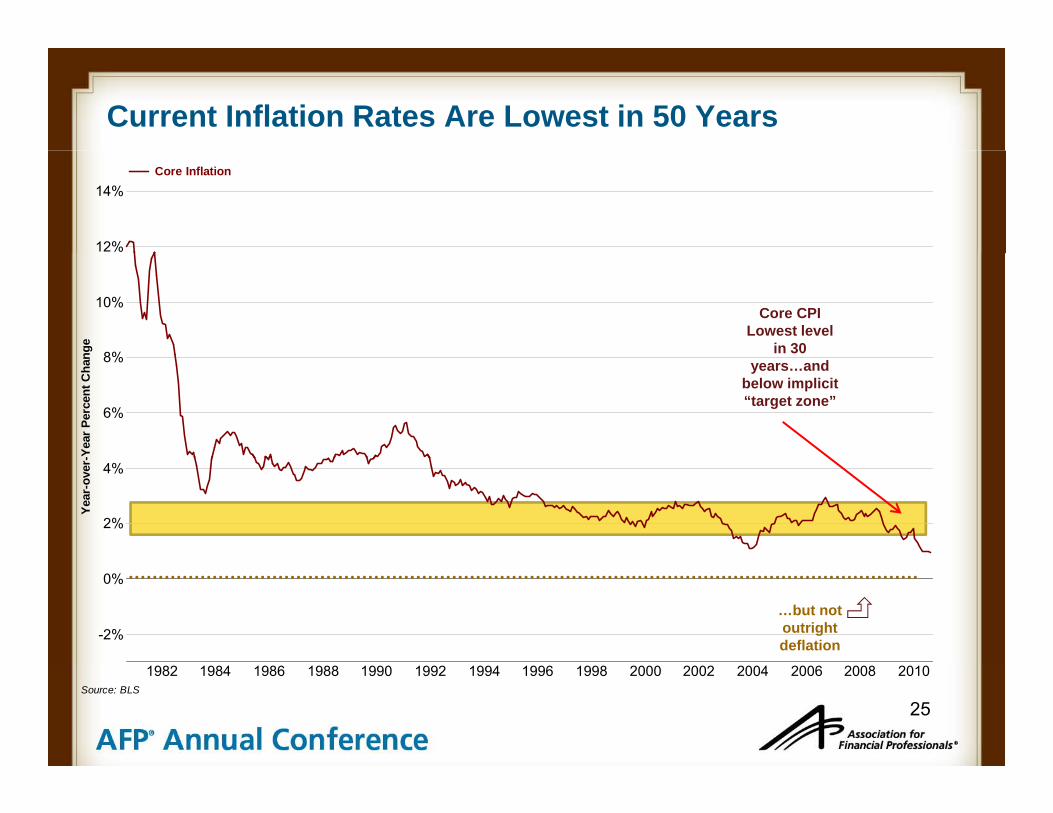

Current Inflation Rates Are Lowest in 50 Years

12%

14%Core Inflation

8%

10%

nge

Core CPI Lowest level

in 30

6%

8%

-Yea

r Per

cent

Cha

n

years…and below implicit “target zone”

2%

4%

Year

-ove

r-

-2%

0%

…but not outright deflation

25

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010Source: BLS

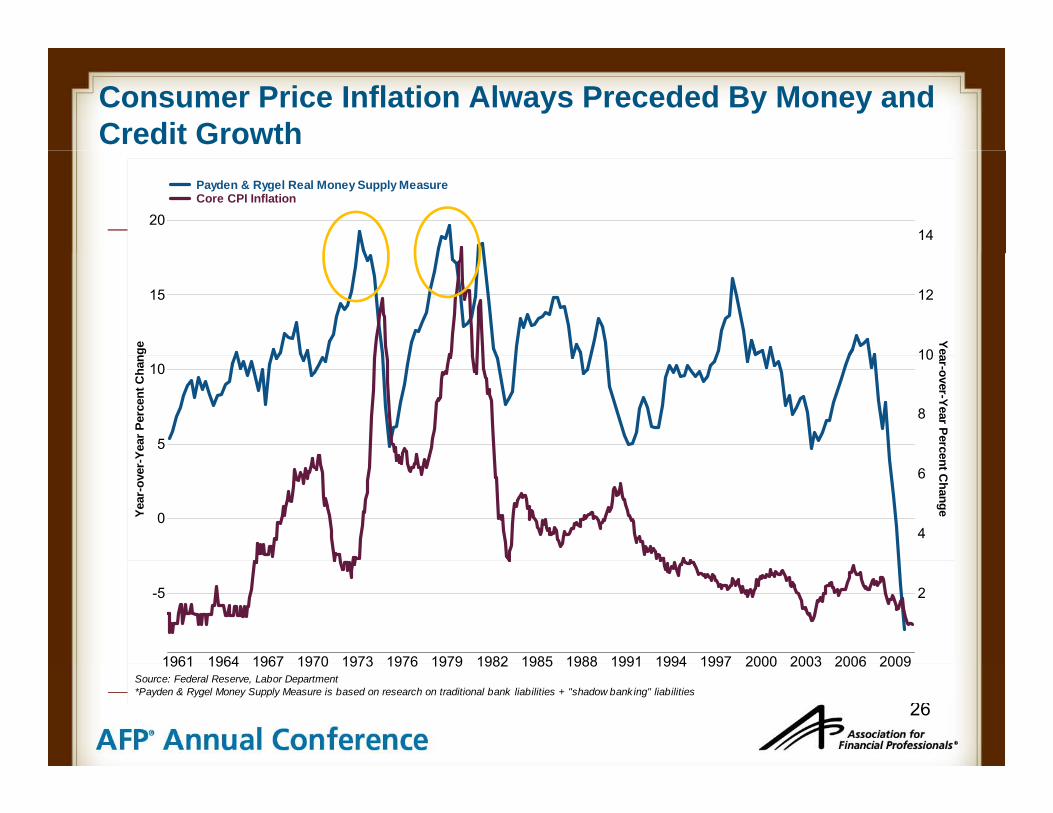

Consumer Price Inflation Always Preceded By Money and Credit Growth

2014

Payden & Rygel Real Money Supply MeasureCore CPI Inflation

15

nge

10

12

Yea

5

10

Year

Per

cent

Cha

n

8

10 ar-over-Year Perce

0Year

-ove

r-Y

4

6

ent Change

1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

-5 2

26

1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009Source: Federal Reserve, Labor Department*Payden & Rygel Money Supply Measure is based on research on traditional bank liabilities + "shadow bank ing" liabilities

Understanding Monetary Policy Goals in One PictureThe Fed wants to increase aggregate demand (spending);

if people think prices are set to rise they will increase their spending

27

Monetary Policy Scorecard Makes “Quantitative Easing 2” Likely

The Federal Reserve's mandate is "to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates" (1977 Federal Reserve Act). Today this is referred to as the "dual mandate" since long-term interest rates can only remain moderate in a stable macroeconomic environment. In the wake of unprecedented monetary policy actions, how has the Fed fared?

Macroeconomic Category IndicatorPolicy Goal

Current Reading

Year Ago

ReadingMeeting Goal?

Employment Unemployment Rate 5‐7% 9.6% 9.7%No

Core CPI NoInflation

Core CPI (year‐over‐year) 1.5% ‐ 2% 0.95% 1.6%

No

Payroll GrowthNon‐Farm Payrolls (monthly change)

150,000‐300 000 -39 000 -197 000

NoPayroll Growth (monthly change) 300,000 39,000 197,000

28

More Likely Before

Further Ammunition: What Options Are Available?

I Long-Term Treasury Purchases (“Quantitative Easing” or “QE2”)II

More Likely Before Year-End

( Q g Q )

Communication StrategyII

III

Reduce Interest Paid on Reserves

Raise Inflation Target

IVLess Likely

Raise Inflation Target

Source: Ben Bernanke, “The Economic Outlook and Monetary Policy,” Jackson Hole, Wyoming, August 27, 2010.

29

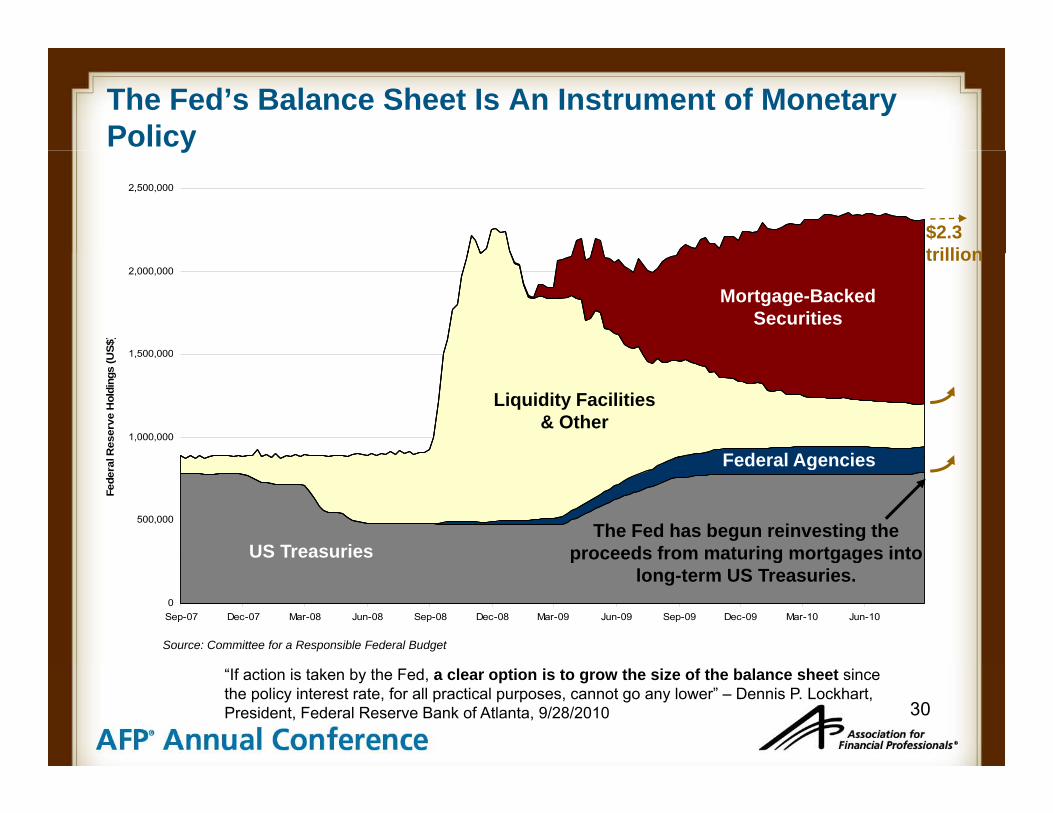

The Fed’s Balance Sheet Is An Instrument of Monetary Policyy

2,500,000

$2.3 trillion

1 500 000

2,000,000

US$

)

trillion

Mortgage-Backed Securities

1,000,000

1,500,000

Res

erve

Hol

ding

s (U

Liquidity Facilities & Other

Federal Agencies

500,000

Fede

ral

The Fed has begun reinvesting the proceeds from maturing mortgages into US Treasuries

Federal Agencies

0Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

p g g glong-term US Treasuries.

Source: Committee for a Responsible Federal Budget

30

“If action is taken by the Fed, a clear option is to grow the size of the balance sheet since the policy interest rate, for all practical purposes, cannot go any lower” – Dennis P. Lockhart, President, Federal Reserve Bank of Atlanta, 9/28/2010

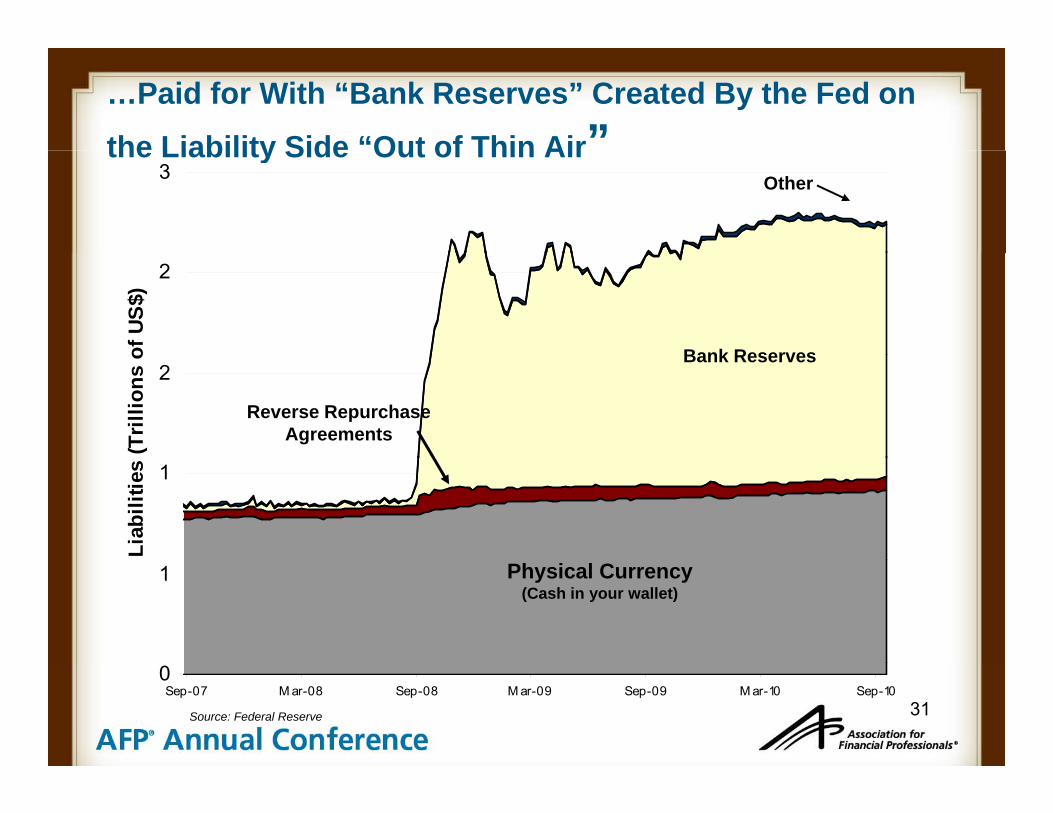

…Paid for With “Bank Reserves” Created By the Fed on

the Liability Side “Out of Thin Air”3

the Liability Side Out of Thin AirOther

2

of U

S$)

Bank Reserves2

(Tril

lions

o

Reverse Repurchase Agreements

Bank Reserves

1

Liab

ilitie

s

1 Physical Currency(Cash in your wallet)

31

0Sep-07 M ar-08 Sep-08 M ar-09 Sep-09 M ar-10 Sep-10

Source: Federal Reserve

Would Further “QE” Have an Impact?Would Further “QE” Have an Impact?

On Capital Markets? Yes

On the Real Economy? YesEconomy?

Probably Not

32

The Limits of QE: Banks Accumulate Excess Reserves, Not New LoansNot New Loans

1 7Commercial & Industrial Bank Loans (Right)"Printed Money" = Excess Reserves Held at Federal Reserve (Left)

In textbooks, reserves work through the “money multiplier” to increase aggregate lending and demand.

1

1.2

1.6

1.65

1.7

0.6

0.8

D T

rillio

ns

1.45

1.5

1.55

USD

Trilli

The banks are hoarding money…

0.4

0.6

USD

1.3

1.35

1.4

ions…and not making new loans.

2009 20100

0.2

1.2

1.25

Source: Federal Reserve

33

Source: Federal Reserve

Commercial Banks Appear to Be Hoarding Cashpp g

1,400 1,400,000

Assets Of Commercial Banks, Cash Assets, Bil. (Left)Excess Reserves Of Depository Institutions (Right)

1,200

1,000,000

1,200,000

800

1,000

D B

illion

s 800,000

US

D M

illi

600

US

D

400,000

600,000

ions

200

400

0

200,000

34

1/08 4/08 7/08 10/08 1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10200 0

Non-Financial Corporations Also Appear to Be Hoarding Cash

1.8

2 Nonfarm nonfinancial corporate business - Total Liquid Assets

1.4

1.6

1

1.2

US

D T

rillio

ns

0 4

0.6

0.8

0

0.2

0.4

35

'46 '48 '50 '52 '54 '56 '58 '60 '62 '64 '66 '68 '70 '72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '080

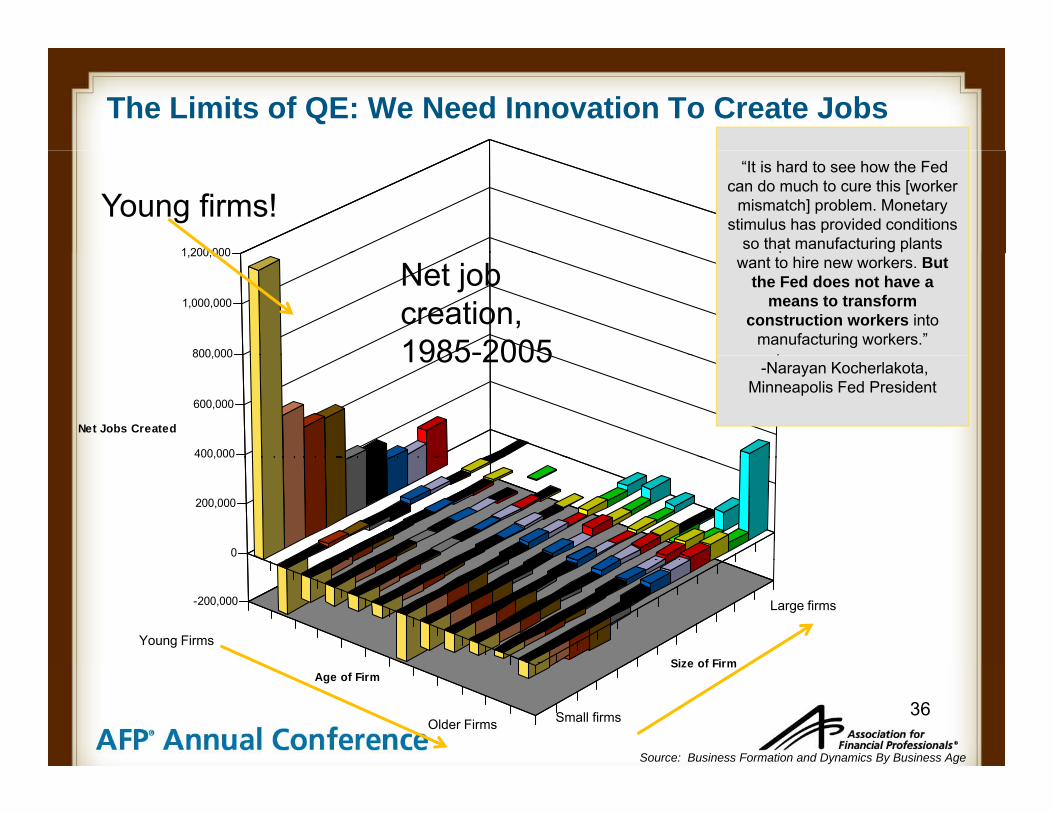

The Limits of QE: We Need Innovation To Create Jobs

1 200 000

“It is hard to see how the Fed can do much to cure this [worker

mismatch] problem. Monetary stimulus has provided conditions

so that manufacturing plants

Young firms!

800 000

1,000,000

1,200,000want to hire new workers. But

the Fed does not have a means to transform

construction workers into manufacturing workers.”

Net job creation, 1985-2005

400,000

600,000

800,000

Net Jobs Created

-Narayan Kocherlakota, Minneapolis Fed President

1985 2005

0

200,000

,

-200,000

Size of Firm

Young Firms

Large firms

36

Age of FirmSize of Firm

Source: Business Formation and Dynamics By Business Age

Older Firms Small firms

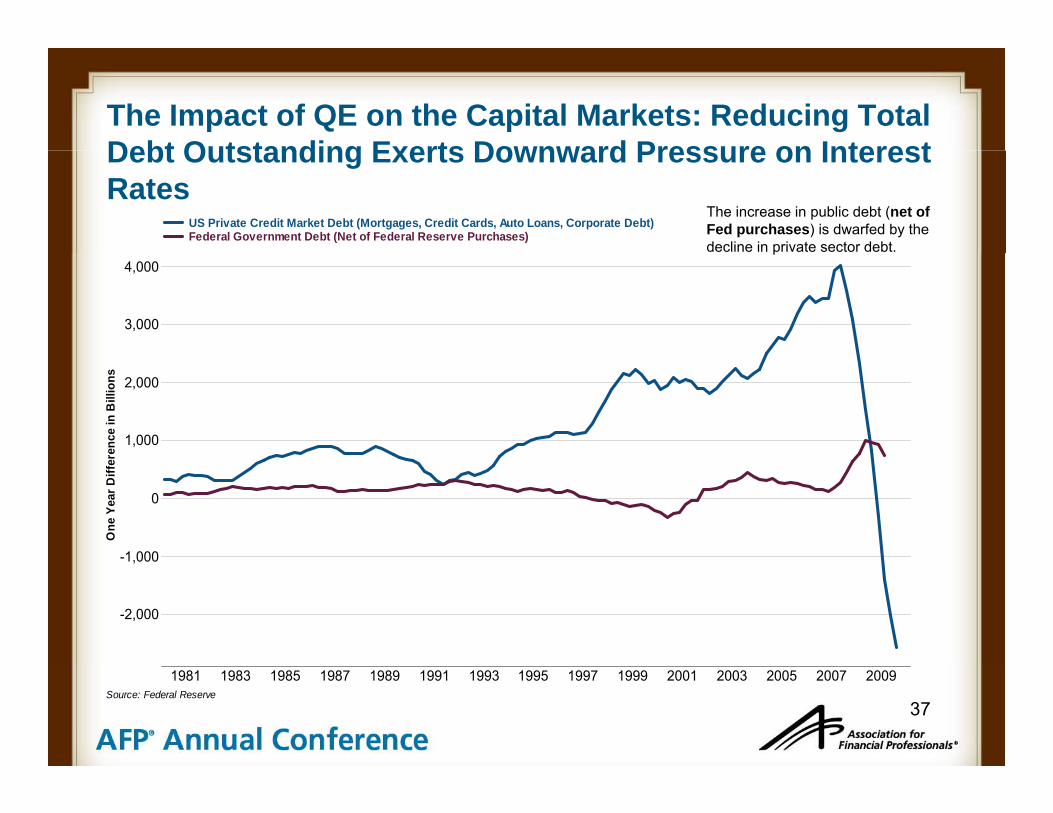

The Impact of QE on the Capital Markets: Reducing Total Debt Outstanding Exerts Downward Pressure on InterestDebt Outstanding Exerts Downward Pressure on Interest Rates

US Private Credit Market Debt (Mortgages, Credit Cards, Auto Loans, Corporate Debt)Federal Government Debt (Net of Federal Reserve Purchases)

The increase in public debt (net of Fed purchases) is dwarfed by the decline in private sector debt.

3,000

4,000p

1,000

2,000

renc

e in

Bill

ions

-1,000

0

One

Yea

r Diff

er

-2,000

1,000

37

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009Source: Federal Reserve

Meanwhile, Investor Demand for Bonds Has Surged

208200220

Year-to-Date Flows By Fund Type, USD Billions

100120140160180

s

“Thus, our purchases of Treasury, agency debt, and agency MBS likely both reduced the yields on those securities and also pushed investors into holding other assets with similar characteristics, such as credit risk and duration. For example, some investors who sold MBS to the Fed may have replaced them in their portfolios with longer-term, high-quality corporate bonds, depressing the yields on those assets as well ” Ben Bernanke August 27 2010

30 2814

200

20406080

USD

Bill

ions

In

yields on those assets as well. - Ben Bernanke, August 27, 2010

-59-80-60-40-20

Taxable Bond Municipal Bond Foreign Equity Hybrid Domestic Equity

Out

S ICIThe Portfolio Balance Effect

38

Source: ICI

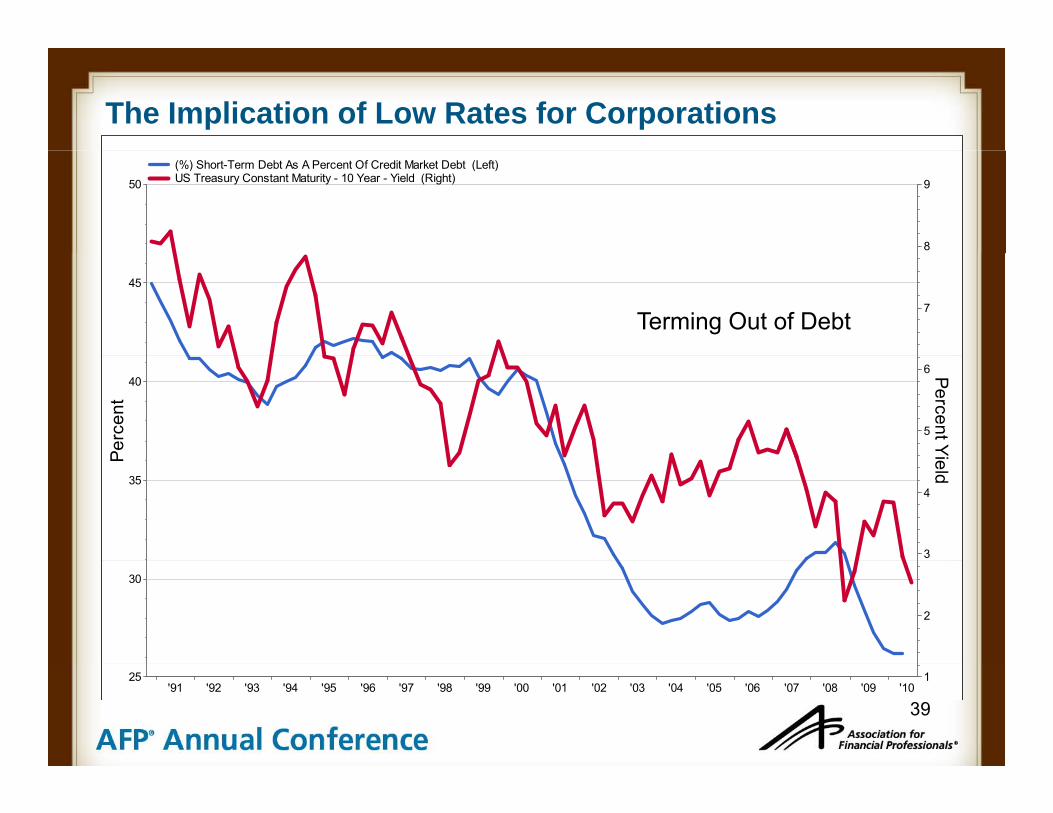

The Implication of Low Rates for Corporations

50

8

9

(%) Short-Term Debt As A Percent Of Credit Market Debt (Left)US Treasury Constant Maturity - 10 Year - Yield (Right)

45

7Terming Out of Debt

40

Perc

ent

5

6 Percent Yi

35

P

3

4

ield

30

2

39'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

25 1

The Contributions to Growth By Major Sector

3.5%Q3 2010 Real GDP Growth = 2.0%

1.5%

2.5%

on to

Rea

l GD

P

Sustainable Drivers of Growth

Temporary Drivers of Growth

0.9%1.4%

1.8%

0.7%0.5%

Poi

nt C

ontri

butio

-0.8%

-2.0%

1 5%

-0.5%

Per

cent

age

P

-2.5%

-1.5%

Consumer Private Inventories Business Government Housing Net Exports

40

Spending Investment Spendingg

Investmentp

Source: The Commerce Department

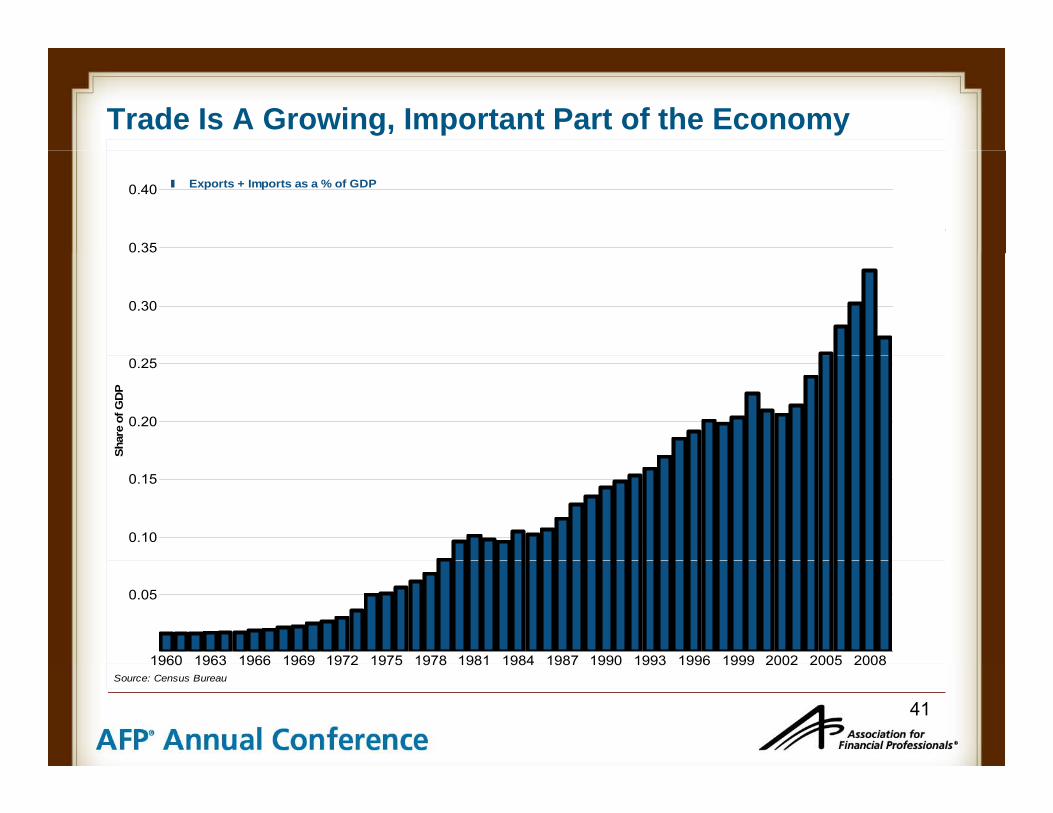

Trade Is A Growing, Important Part of the Economy

0.35

0.40 Exports + Imports as a % of GDP

0.30

0.20

0.25

Shar

e of

GD

P

0.10

0.15

1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

0.05

41

1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008Source: Census Bureau

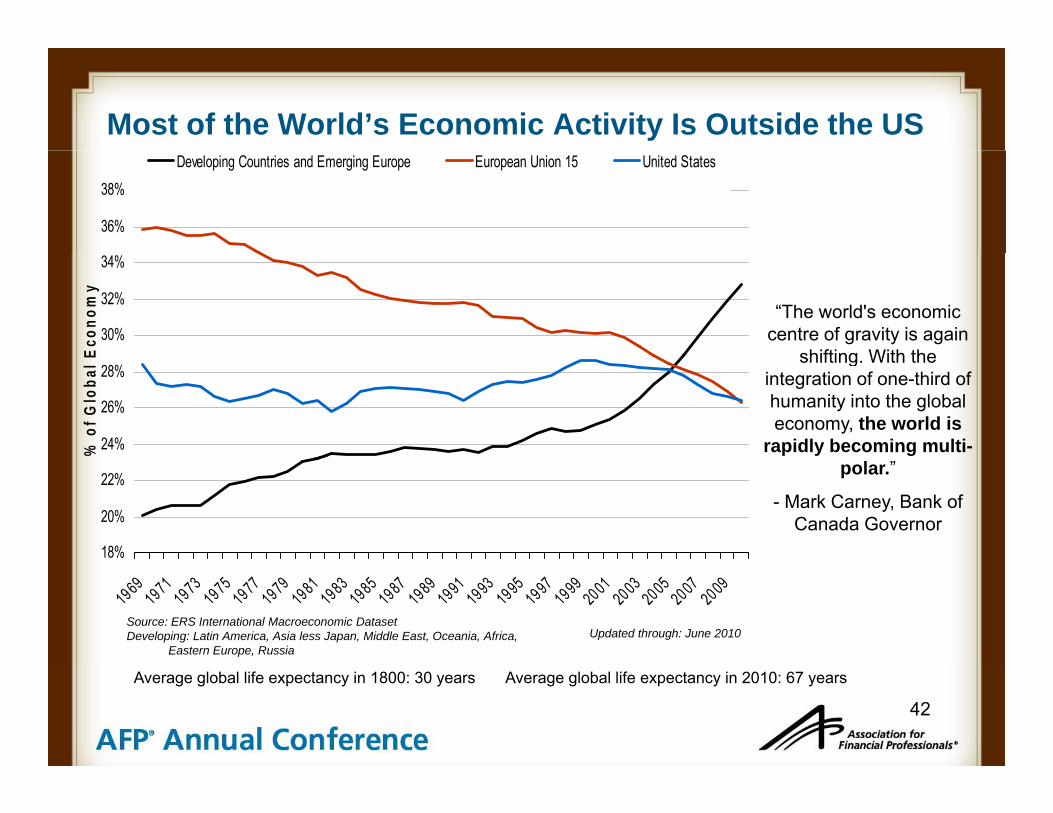

Most of the World’s Economic Activity Is Outside the US

36%

38%Developing Countries and Emerging Europe European Union 15 United States

30%

32%

34%

Econ

omy

“The world's economic centre of gravity is again

shifting With the

24%

26%

28%

% o

f Glo

bal E shifting. With the

integration of one-third of humanity into the global economy, the world is

rapidly becoming multi-

18%

20%

22% polar.”

- Mark Carney, Bank of Canada Governor

Source: ERS International Macroeconomic DatasetDeveloping: Latin America, Asia less Japan, Middle East, Oceania, Africa,

Eastern Europe, Russia

196919711973197519771979198119831985198719891991199319951997199920012003200520072009

Updated through: June 2010

42

Average global life expectancy in 1800: 30 years Average global life expectancy in 2010: 67 years

IV The Output: GDP,V The Output: GDP,

Employment, Inflation, Interest RatesRates

43

The Output: GDP, Employment, Inflation, Interest Rates“I can calculate the motions of heavenly bodies, but not the madness of people.” – Sir Isaac Newton

Actual Forecast

2010 2011Q1 Q2 Q3 Q4 Q1 Q2Q1 Q2 Q3 Q4 Q1 Q2

Real GDP(quarter-to-quarter annualized percent change)

3.7 1.6 1.5 2.0 2.5 2.7

Unemployment Rate(percent)

9.7 9.7 9.6 9.5 9.5 9.5

Headline CPI Inflation(year-over-year percent change)

2.4 1.8 1.8 1.8 1.6 1.4

Core CPI Inflation(year-over-year percent change)

1.3 1.0 0.9 0.8 1.0 1.2

Federal Funds Rate(percent)

<0.25 <0.25 <0.25 <0.25 <0.25 <0.25

2-Year Treasury(percent)

1.05 0.60 0.42 0.30 0.25 0.25

10-Year Treasury 3.71 3.49 2.80 2.50 2.50 2.50

44

*Data represent quarterly averages

The Risks to the Forecast

“I can calculate the motions of heavenly bodies, but not the madness of people.” – Sir Isaac Newton

State & Local Government Fiscal/Debt

D fl iDeflation

Fiscal/Regulatory Uncertainty

Housing Market Supply Overhang

International Currency War

45