THE ARC OF MOREHOUSE - app1.lla.la.gov · PDF file2,697 2,697 2,697 4,691 64,733 69,424...

28

C ~- 1 . -'<'. ' ~ THE ARC OF MOREHOUSE Financial Statements For the Years Ended June 30, 2005 and 2004 Under provisions of state law, this report is a public document. Acopy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the officepf the parish clerk of court. Release Date

Transcript of THE ARC OF MOREHOUSE - app1.lla.la.gov · PDF file2,697 2,697 2,697 4,691 64,733 69,424...

C ~- 1 .

-'<'. '~

THE ARC OF MOREHOUSE

Financial StatementsFor the Years Ended June 30, 2005 and 2004

Under provisions of state law, this report is a publicdocument. Acopy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the officepf the parish clerk of court.

Release Date

THE ARC OF MOREHOUSE

JUNE 30,2005 and 2004

TABLE OF CONTENTS

Page

Independent Auditors' Report 1

Statements of Financial Position 3

Statements of Activities 5

Statements of Functional Expenses 7

Statements of Cash Flows 9

Notes to Financial Statements 10

SUPPLEMENTAL SCHEDULES

Combining Schedules of Financial Position 17

Combining Schedules of Activities 19

REPORT REQUIRED BY GOVERNMENT AUDITING STANDARDS

Independent Auditors' Report on Compliance and Internal Control over FinancialReporting Based on an Audit of Financial Statements Performed inAccordance With Government Auditing Standards 22

Status of Prior Year Findings 24

Luff GV L Fred Monroe'CPAFrancis I. Huffman, CPAL. Fred Monroe, CPAEsther Atteberry, CPA

JohnL. Luffey, MBA, CPA (1963-2002)

& Monroe(A Professional Accounting Corporation)

C E R T I F I E D PUBLIC A C C O U N T A N T S

INDEPENDENT AUDITORS' REPORT

Board of DirectorsThe ARC of MorehouseBastrop, Louisiana

We have audited the accompanying statements of financial position of The ARC ofMorehouse (a nonprofit organization - the Association) as of June 30,2005 and 2004, andthe accompanying statements of activities, functional expenses and cash flows for theyears then ended. These financial statements are the responsibility of the Association'smanagement. Our responsibility is to express an opinion on these financial statementsbased on our audit.

We conducted our audit in accordance with auditing standards generally accepted in theUnited States of America; the standards for financial audits contained in GovernmentAuditing Standards, issued by the Comptroller General of the United States and theLouisiana Governmental Audit Guide published by the Society of Louisiana Certified PublicAccountants and the Louisiana Legislative Auditor. Those standards require that we planand perform the audit to obtain reasonable assurance about whether the financialstatements are free of material misstatement. An audit includes examining, on a testbasis, evidence supporting the amounts and disclosures in the financial statements. Anaudit also includes assessing the accounting principles used and significant estimatesmade by management, as well as evaluating the overall financial statement presentation.We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all materialrespects, the financial position of the Association as of June 30, 2005 and 2004, and thechanges of its net assets and its cash flows for the years then ended in conformity withaccounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report datedSeptember 30,2005 on our consideration of the Association's internal control over financialreporting and our tests of its compliance with certain provisions of laws, regulations,contracts and grants. That report is an integral part of an audit performed in accordancewith Government Auditing Standards and should be read in conjunction with this report inconsidering the results of our audit.

(318) 387-2672 • FAX (318) 322-8866 • www.lhm-cpas.com1100 N 18th ST. PO Box 4745 • Monroe LA 71211-4745

MEMBERS OF THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS

Board of DirectorsThe ARC of Morehouse

Our audit was made for the purpose of forming an opinion on the financial statementstaken as a whole. The accompanying financial information listed as SupplementalSchedules in the accompanying Table of Contents is presented for purposes of additionalanalysis and is not a required part of the financial statements of the Association. Suchinformation has been subjected to the auditing procedures applied in the audit of thefinancial statements and, in our opinion, is fairly presented in all material respects inrelation to the financial statements taken as a whole.

(A Professional Accounting Corporation)

September 30, 2005

THE ARC OF MOREHOUSESTATEMENTS OF FINANCIAL POSITION

ASSETS

Cash and cash equivalentsInvestmentsAccounts receivablePrepaid assetsFixed assetsAccumulated depreciation

TOTAL ASSETS

June 30, 2005

Unrestricted

235,540 $81,072

172,20826,413

1,033,134(525,805)

1,022,562 $

TemporarilyRestricted

- $-

2,521-

33,344(33,344)

2,521 $

Total

235,54081,072

174,72926,413

1,066,478(559,149)

1,025,083

LIABILITIES AND NET ASSETS

LiabilitiesAccounts payableAccrued liabilities

Total Liabilities

Net AssetsUnrestrictedTemporarily restricted

Total net assets

11,431 $82,51293,943

928,619

928,619

TOTAL LIABILITIES AND NET ASSETS $ 1,022,562 $

- $

2,5212,521

11,43182,51293,943

928,6192,521

931,140

2,521 $ 1,025,083

The accompanying notes are an integral part of this financial statement.

June 30,2004Temporarily

Unrestricted Restricted Total

172,213 $80,158211,29613,866

1,008,828(502,640)

983,721 $

- $-

2,697-

33,344(33,344)

2,697 $

172,21380,158213,99313,866

1,042,172 .(535,984)

986,418

4,691 $64,73369,424

914,297-

914,297

983,721 $

---

_

2,6972,697

2,697

4,69164,73369,424

914,2972,697

916,994

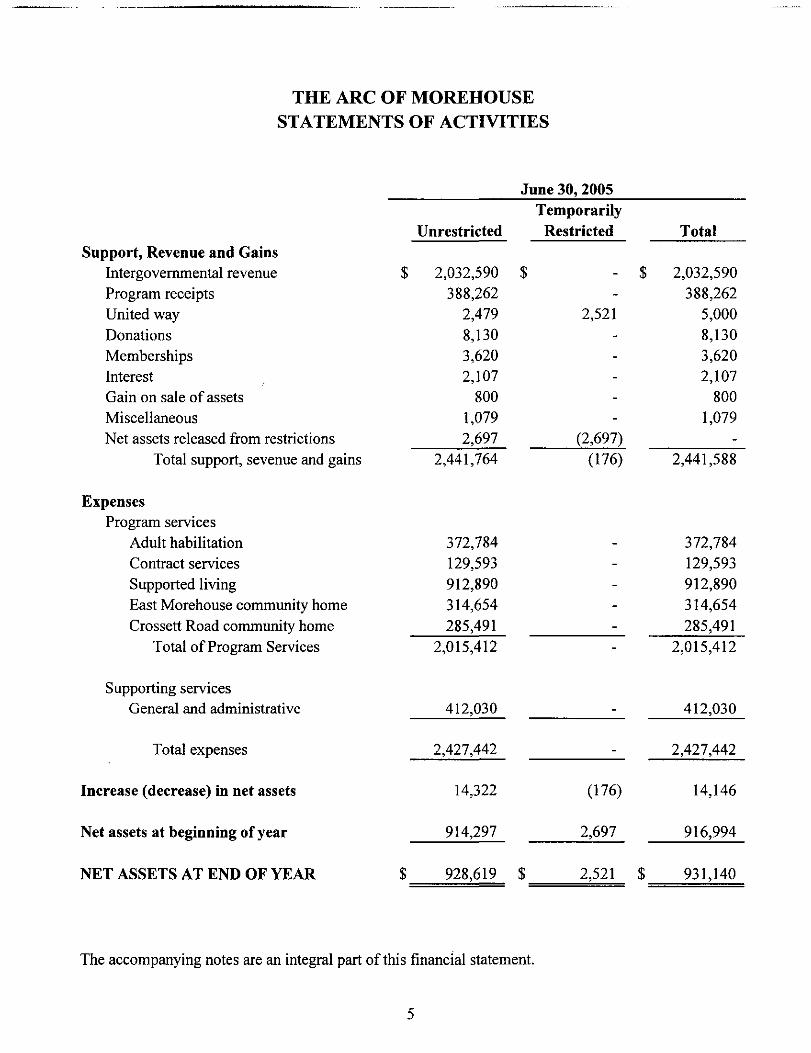

THE ARC OF MOREHOUSESTATEMENTS OF ACTIVITIES

June 30, 2005

Support, Revenue and GainsIntergovernmental revenueProgram receiptsUnited wayDonationsMembershipsInterestGain on sale of assetsMiscellaneousNet assets released from restrictions

Total support, sevenue and gains

ExpensesProgram services

Adult habilitationContract servicesSupported livingEast Morehouse community homeCrossett Road community home

Total of Program Services

Supporting servicesGeneral and administrative

Total expenses

Increase (decrease) in net assets

Net assets at beginning of year

NET ASSETS AT END OF YEAR

TemporarilyUnrestricted Restricted

$ 2,032,590 $ - $388,262

2,479 2,5218,1303,6202,107

8001,0792,697 (2,697)

2,441,764 (176)

372,784129,593912,890314,654285,491

2,015,412

412,030

2,427,442

14,322 (176)

914,297 2,697

$ 928,619 $ 2,521 $

Total

2,032,590388,262

5,0008,1303,6202,107

8001,079

-2,441,588

372,784129,593912,890314,654285,491

2,015,412

412,030

2,427,442

14,146

916,994

931,140

The accompanying notes are an integral part of this financial statement.

June 30,2004Temporarily

Unrestricted Restricted

1,932,660 $ - $361,457

9,673 2,697191

3,8502,576

1,43510,553 (10,553)

2,322,395 (7,856)

371,201134,120845,931276,592285,461

1,913,305

321,534

2,234,839

87,556 (7,856)

826,741 10,553

914,297 $ 2,697 $

Total

1,932,660361,457

12,370191

3,8502,576

1,435-

2,314,539

371,201134,120845,931276,592285,461

1,913,305

321,534

2,234,839

79,700

837,294

916,994

ieiE» gtd -E« M2 tZ O w

d c/2

1ORE

HOUS

E:T

IONA

L EX

PED

ED

JU

NE

30,

2'

Prog

ram

* sE zS S w0 fa PSu fa «:Ptf O td3 £ > -UJ Z Wffi w ffiH g H

td PSbi o< faHw

0H

*4*•* _.

| ISE u<u

."s"c uW Ml•a 3

"« « 2J* A ^SOS Id £.o

•oa>^ fio .-,C. >g-J

tfl

tion

Con

trac

tim

Se

rvic

es

S C:s M« PH

— «•s e•*t_>— «

2 „ i:** ff .24* rt B™

U £•o

o cs— 1 ft*n --

o -<tvo_ rs

«

t- O

\O (N

^ OS~* OSOS OTf1 ^o rN— •

m (N(N mr^ <*TO T

W

•* OO O

m" m"

oo mas oo

in" — Tr- TrN

V), ,

T t i n - — - ( N I ~ - W - ) O r < i O O O r - - ' * ( N - - ' * v O ' O r ^ i ^ -

v o i Q ^ ^ I S S M ^ ^ " ' S S ^ 0 1 ^ ^ ^ " ^

!j

OO f*^ OO CT*i ^5 *O O> F~- ^O 00 ^^ • — < ^T OO ^^ W"l C**l */*>r^ - r * ^ i — ^ T " — I T ^ - O O r * 4 * — • V i ' / ' i ^ O ^ O ^ O ^O O

OC ^ fN \O

O s ^ O ^ - o O ^ . ^ . O - r S O s O ^ v O O s O s O O— \^ ^4 f**| v~i TJ- os OO OO *~* ^^ *-O OO 1^ r^ Os ^O fNO O •— ' m so •— 'SO O ( N r ^ s O ^ i n s o O S ^ O m w i•—i m •— ' OcTr* - ) <N (S •— 'in — (N so" t~J •— ' *OO r-( ^-t os(N

O C S O ' - D — r n O ' O O ' ( S t S t N i n - ^ - O ' *S-- in^^ r*~i Os f~> Os os os ^^ ff°t r^i -— • r^ O^ in oo in in> n m r N m o r n ^ O O o o o o o s o s o o i n ^ f i nO m •— m O Tt in s o ^ f - . — ' T T T T n O s f S

(N —2-

*— ^O OO fS

oo" — " oo"

O -- f~- OO •— • (N (N •— ' Tt- -- m SO (S *O— ' ro — CS

. i o i r> ' t i i ov vc i < = , . . < r M 'K § S * " S- 2

ro OsTf OS

(N —S Sa-(N OO^5 ^3oo o

O —ro •— i

• - oo

w-j OVO • — 'm

~^ inOs mOsooo

OsinOs"r-i

oo oooo so

c^ —

rt inTf OO

Sala

ries

ge b

enef

its

c

Payr

oll t

axes

and

fri

and

rela

ted

expe

nses

in

SIA

1H

Con

sulta

nts

Dat

a pr

oces

sing

co

Due

s an

d su

bscr

ipt! T3

Food

and

cli

ent n

eeIn

sura

nce

Mai

nten

ance

$ ,§g faJ O

1o

V

1o0, P

rofe

ssio

nal

fees

Pub

lic

awar

enes

sS

uppl

ies

Tax

es a

nd l

icen

ses

Tel

epho

ne on'5'5H

co

Tra

nspo

rtat

ion

Tra

vel

and

conv

ent!

=3 E

cp-

«3UCO

ZUPHX!U

-1

Hyzu.J

(/JUJ

o

2

s0 E ctfU fa •<PS o w< H >w z; wB w ffiH S H

VIuu

1£1.61O

£

_,at"SH

^v pn

dk ** SS S o

•™ 2 '"V

£ uu

"a

g v

."2 *"g 'tS 2jj 93 ^3PS ^ t.

O

S

73U „-•w U

s —a .£1^

u 2£ .2'B .£o v

So c'•C S3 2•3 5)-D £

M^.^ QT3 &

V

"•3"5 *h •« ~g s =

fl O— i U")_i so**• oOS (N""*", M

— soON Ooo coCN r-iin rN

V*

(N r-— oo

r*-j (v)vi (N_<

1 v,SO r*"lr~ (Nf«T Q^

ON (N

^O m— o.

—

O f--3- oo

o" o'(N

W

ro v i ^ o i o M O N O t N — O N O o o r M — o o r - m s o^O "*3~ oo ^^ t r ON oo r*"i fN r*1! Vi r*^ r*4 O r*J co ^O v*iI> r f ^ o O ^ v ^ v ^ ^ O •— ' •— * C T \ ^ ' ! r f N l O - - ' O ^ -^ o o ^ D t o r ^ - r r " i T <— fN Tf ^ t-- r- ^?f O O1

D1 M

ON ON VD f - C> VO OO •"" ^~ " T^ OS r - fi CO (N ON r*^^O — ' O ^ O O r - f l t ^ - m f N v i l - ^ ^ t O O - - fN

tS — "" 0^"° ^ " ^ r r i -™ -140

-1

ON - n - r ^ o o o e o N O O O N r n v i o r - i o ^ r s i — <"i

— o S S P ! o v : ; S " " i o S 2 v ^ ? v S t ^ ( N ^ ^so (N— osr - "T" i— < r-T vi •— • <N -- 'Ct ON•--

O N ^ ^ - m ^ ^ - v , • v . ^ o v . v . o o - ^ o o oON C^ i™™1 ^T vo fN C3 CO ^ — ' ^5 C> VI f l OO vo SO i™™1

ON — (N m ** --• -- i n o o o o o m o o N !--•—•

(N

— . • • • r s i O N ' V i « ' « ' m - * 1 1 ' •^- O rO 'O CO (~-J*— * Os ro CN oo ON

CN

fN m r^ o '•"' r*** os *—* os *^ *"^ t c^ v~i o^ c i os oor^ (^i •* — • *N oo r ~ - ^ - r ^ f ^ o o o c o ^-i--

— — — Os" g 2 M' ^ "* "• ' m" "" v°"r^j

. , , ^ , , . , ^ . - 0 - 0 0 .ON r*i O OO rO— <n m O*— (N*

r- rNOO Wl(N VIVI ONr- to

IN"

ON SO*£> ONrM o(N —r-i —f^i

fN mso rMON t—

r oo<— 'ro

oo \o*r r-ON — <

OOON

•q- sovS *o"*„ ^rn

O Or en

— ^Tj-

— O*o ONON^ V~l

m fNr-i

ON 'inoo_^^(Nrs"

V) • >\o c^ft ON£' £~cn ^—^

VI ^"QO ON

<n" r-f i ^rtn s — '

^(N ON-- —t~-^ «-Too -3-OS —

o •r^J".M

^O 0o ooo co

^- - — -

— roT ON>o ONso' ^rM os

(N

ON

CO^T

CN"

V*

SO'J-

oo(N

W

CMON"T.so"t"^(N

<T^ONwJ1

oo

orN" ,

ro

6fl

O(N

r;fn

V*

ff)

V~l

^^fN

J!

c: -cT3 ^

O ^

I?

to enCS P

B n2 •«-^ n>O. u

ff'S S

U M US -Q -a

u

"Soo 5.S —•

c.2

"o

Q-UQ

•su

"raSiK

X(tn

BUD.

U

13.0

cU.

u3

!s•o•aca"3au00

t—oB

_O

13u

13&

^^t/iZft.X

-J2OHU2

te,-J

HOH

THE ARC OF MOREHOUSESTATEMENTS OF CASH FLOWS

Cash Flows From Operating ActivitiesIncrease in net assetsAdjustments to reconcile decrease in net assets to net cash

provided by operating activities:DepreciationGain on sale of assetsChanges in assets and liabilities:

Accounts receivablePrepaids and other current assetsAccounts payableAccrued liabilities

Net cash provided by operating activities

Cash Flows From Investing ActivitiesMaturity of investmentsPurchse of investmentsProceeds from sale of assetsAdditions to property and equipment

Net cash used by investing activities

Cash Flow From Financing ActivitiesPayment on long-term debt

Net cash used in financing activities

Net Increase in Cash and Cash Equivalents

Beginning Cash and Cash Equivalents

ENDING CASH AND CASH EQUIVALENTS

Non-Cash Investing ActivitiesPurchase of property and equipment

June 30,2005 2004

$ 14,146 $ 79,700

64,199 59,552(800)

39,264(12,547)

6,74017,779

128,781

63,327

172,213

(47,128)(2,122)(7,631)10,79893,169

28,350(914)800

(65,340) (36,537)(65,454) (8,187)

(24,868)(24,868)

60,114

112,099

$ 235,540 $ 172,213

$ (24,868)

Supplemental Cash Flow InformationInterest Paid

The accompanying notes are an integral part of this financial statement.

9

$ $ 599

THE ARC OF MOREHOUSENOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED JUNE 30,2005 AND 2004

Note 1 - Description of Organization

The ARC of Morehouse (the Association) is a nonprofit voluntary health and welfareassociation chartered in 1958 to promote the general welfare of mentally retarded personsresiding in Morehouse Parish.

Note 2 - Summary of Significant Accounting Policies

A. Financial Statement Presentation

In accordance with Statement of Financial Accounting Standards (SFAS) No. 117,"Financial Statements of Not-For-Profit Associations," the Association is required toreport information regarding its financial position and activities according to threeclasses of net assets (unrestricted net assets, temporarily restricted net assets, andpermanently restricted net assets) based upon the existence or absence of donor-imposed restrictions. The Association has not received any contributions with donor-imposed restrictions that would result in permanently restricted net assets.

The Association has also adopted SFAS No. 116, Accounting for ContributionsReceived and Contributions Made. In accordance with SFAS No. 16, contributionsreceived are recorded as unrestricted, temporarily restricted, or permanently restrictedsupport depending on the existence or nature of any donor restrictions. At June 30,2005 and 2004, the Association had receivables of $2,521 and 2,697, respectively,representing United Way contributions awarded during fiscal years ending June 30,2005 and 2004 that will be received during the subsequent fiscal year. Under SFASNo 116, such contributions are required to be reported as temporarily restrictedsupport and are then reclassified to unrestricted net assets upon expiration of therelated time restrictions.

Donations are considered to be available for unrestricted use unless specificallyrestricted by the donor. Restricted contributions received during the year whoserestrictions are met in the same reporting period are treated as unrestrictedcontributions.

B. Basis of Accounting

The financial statements have been prepared on the accrual basis of accounting,whereby revenues are recognized when earned and expenses are recognized when therelated liabilities are incurred.

10

THE ARC OF MOREHOUSENOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED JUNE 30, 2005 AND 2004

C. Cash and Cash Equivalents

The Association considers all highly liquid investments with a maturity of threemonths or less when purchased to be cash equivalents.

D. Fixed Assets

Fixed assets are recorded at actual or historical cost. Donated assets are recorded atfair market value on the date of donation. Maintenance and repairs of property andequipment are charged to operations and major improvements are capitalized. TheAssociation has a policy to capitalize fixed assets costing more than $500. Uponretirement, sale or other disposition of property and equipment, the cost andaccumulated depreciation are eliminated from the accounts and the gain or loss isincluded in operations.

Depreciation of buildings and equipment is computed by the straight-line methodover the following estimated service lives:

YearsBuildings and Improvements 15-30Furniture and Equipment 5-10Vehicles 3-5

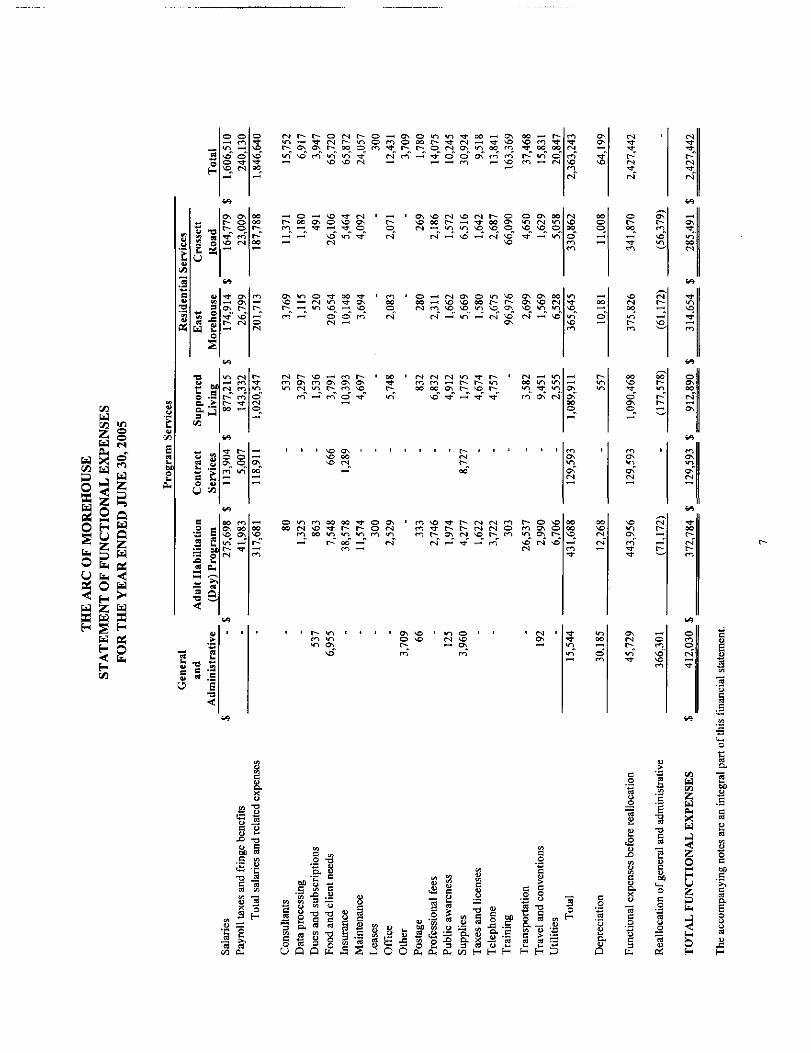

E. Functional Expenses

Expenses that can be identified with a specific program and support service areallocated directly according to their natural expenditure classification. The percentageof Direct Cost of each program to total direct cost is the basis used to allocate otherexpenses that are common to several functions.

F. Programs

The Association's principal programs and primary funding sources are:

Adult Habilitation (Day Program) - The Adult Habilitation funds are used to trainclients in vocational and prevocational activities and supportive services.

Contract Services - Contract Services income is derived from services performed byclients which include janitorial and other contracts.

Supported Living - Supported Living income is received from the LouisianaDepartment of Health and Hospitals. This program, similar to the CommunityHomes, helps the individual clients become more independent by providing supportand training in their residences within the community.

11

THE ARC OF MOREHOUSENOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED JUNE 30,2005 AND 2004

Residential Services - Residential Services income is received from the LouisianaDepartment of Health and Hospitals. Clients pay a pro-rata share of the costs basedon their income. This program provides clients with a home environment within thecommunity and helps them become more independent citizens.

G. Tax-Exempt Status

The Association is exempt from income tax under Section 501(c)(3) of the InternalRevenue Code (Code) and, therefore, has no provision for Federal income taxes.Contributions to the Association are tax deductible within the limitations prescribedby the Code.

H. Estimates

The preparation of financial statements in conformity with generally acceptedaccounting principles requires management to make estimates and assumptions thataffect certain reported amounts and disclosures. Accordingly, actual results coulddiffer from those estimates.

/. Reclassifications

Minor reclassifications have been made to the prior year financial statements to makethem comparable to the current year presentation.

12

THE ARC OF MOREHOUSENOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED JUNE 30, 2005 AND 2004

Note 3 - Fixed Assets

Fixed assets consisted of the following:

June 30, 2005 June 30, 2004Buildings $ 472,697 $ 473,795Equipment 195,821 195,888Vehicles 304,812 302,046Land 16,220 16,220Improvements 54,223 54,223Less: Accumulated depreciation (559,149) (535,984)

Net fixed assets 484,624 506,188

Construction in process 22,705 -

TOTAL FIXED ASSETS $ 507,329 $ 506,188

Included in vehicles above is one vehicle with a cost of $33,344 that was acquired througha Federal grant in previous years. The Association retains title to this vehicle as long as itis kept, maintained and used for the Association's designated purpose. This vehicle is notto be sold or disposed of during its useful life, 5 years or 100,000 miles, without thegrantor's permission. In addition, the vehicle, even though fully depreciated, cannot bereleased from restriction unless the grantor gives its permission. Therefore, the vehicle lessrelated accumulated depreciation, is shown as temporarily restricted.

Depreciation charged to expense in 2005 and 2004 is $64,199 and $59,552, respectively.

Note 4 - Allocation of General and Administrative Expenses

Expenses that can be identified with a specific program and support service are allocateddirectly according to their natural expenditure classification. Other expenses that arecommon to several functions are allocated in proportion to the direct expenses of theprogram to total direct expenses of all the programs. The following is the detail of thegeneral and administrative expenses that have been reclassified from program services onthe Statement of Functional Expenses for the years ended June 30, 2005 and 2004:

13

THE ARC OF MOREHOUSENOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED JUNE 30, 2005 AND 2004

June 30,2005 2004

Data Processing $ 6,792 $ 6,686Dues and Subscriptions 3,165 4,126Food 2,858 1,819Insurance 14,961 11,063Maintenance 11,379 10,544Office Expense 11,096 9,500Payroll Taxes and Fringe Benefits 29,909 25,839Postage 1,705 2,113Professional Fees 17,403 15,81!Public Awareness 10,119 3,754Salaries 234,778 185,150Supplies 3,777 3,984Telephone 7,979 8,088Travel and Conventions 5,117 2,111Utilities 5,263 4,405TOTAL $ 366,301 $ 294,993

Note 5 - Significant Concentrations of Risk

Certain financial instruments potentially subject the Association to concentration of creditrisk. These financial instruments consist primarily of cash and cash equivalents. TheAssociation maintains its cash in various bank deposit accounts, which at times mayexceed federally insured limits. The Association has not experienced any losses in suchaccounts. At June 30,2005, the various bank deposits exceeded the federal insured limitsby approximately $8,800.

The Association receives approximately 83% of total revenue and support from variousstate agencies.

Note 6 - Subsequent Event

Effective July 1,2005, the Association began contributing to the American Funds 503(b)retirement plan at a rate of fifty percent of the employees' contributions. The vesting of theemployer's share of the contributions will be as follows:

14

THE ARC OF MOREHOUSENOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED JUNE 30, 2005 AND 2004

1. Full time employees with two years of service will be vested at 25% of theemployer's contribution.

2. Full time employees with three to four years of service will be vested at 50%of the employer's contribution.

3. Full time employees with over five years of service will be vested at 100% ofthe employer's contribution.

15

SUPPLEMENTAL SCHEDULES

16

-Jp

zoHNHC/J

o0--J

« n§§S z ">td ft oCtf b^ ^^

is*fa W a0 Iw § £5 ? 9

^ KS wX enH o

ZSSou

u -e^ CBB^ ft

e S

r gS - s5-J

Contr

aS

ervi

ce

-2 ES 2S 61•= O^

o oo r-

"S ^3 sO 3

enHidenen<

irt

u

_>

CT

U•o

U

ives

tmen

ts

c ccou

nts

Rec

eiva

ble

<

repa

id A

sset

s

Cu,

ue F

rom

Oth

er F

unds

Q

ixed

Ass

ets

b*

c

13

1D.OQT3s3

u<

OT

AL

AS

SE

TS

H

ET

ASS

ET

S

z

LIA

BIL

ITIE

S A

ND

urre

nt L

iabi

litie

s

U

Acc

ount

s Pa

yabl

eA

ccru

ed L

iabi

litie

sD

ue T

o O

ther

Fun

dsab

ilitie

s

' i

Tota

l Cur

rent

1

et a

sset

s (d

efic

it):

Z

Unr

estri

cted

Tem

pora

rily

rest

ricte

d

'ouQ-i2

Tota

l Net

Ass

e

i•4

OT

AL

LIA

BIL

ITIE

S .

H

NE

T A

SSE

TS

W

QIdffiUen

m oo fi so— in ON 'O<N — > ON OO

oo <Nso •*ON O

sor-f

w

uou

ofd fe

1 PO ft*

p£ M oo y N.

o s z

u-1

o

W

u

W

TJ

!|o- .i

ON

ri

ONrs

SO

SO

-*

(N

r- o r-— o t-m (N VIo" o"

•-§ Ea CQS L.s ^A Z« PH

•S8

SO•*SO

I- SO OSO t— TOO SO OO

CQSo

so inr~r -— " o"

o ON r- oo- — r- — ON

V) S

1 13 g.

ash

and

Cas

h

U

ives

tmen

ts

&

1

ccou

nts

Rec

ei

< repa

id A

sset

s

n,

wT33

ue F

rom

Oth

e

Q

ixed

Ass

ets

IX,

ciat

ion

K8-

ccum

ulat

ed D

<

XH

OT

AL

ASS

E

H

iND

NE

T A

SSE

TS

•

LIA

BIL

ITIE

S ,

rren

t Lia

bilit

ies

aU

u

Acc

ount

s Pa

yab

.2

Acc

rued

Lia

bilit

nds

rent

Lia

bilit

ies

3 1-1

Due

To

Oth

er F

iTo

tal C

u

asse

ts (

defi

cit)

:

u2

Unr

estri

cted

-o.15

Tem

pora

rily

resl

'5(Su

1

Tota

l Ne

IES

AN

D

t—.

TA

L L

IAB

ILI1

OH

NET

ASS

ET

S

o i N O O o r - o o s

S «H §

Ed ?" ®» h ***^ ^ w0 ^ 5

= fa —Ed o 7s a l* g §fe w w0 a BSy u <:a w u<: o >•Ed Z EdK S KH S H

I oO Ebu

Con

trSe

rvic

•s 2S 2,:s us JTH a,5S,IS<

o r- o 'OC4 O O vi

2 3r-i —

sit•a S S

i> ec^ ^

H a.2 «

^4=

P5 3I c So H

in ft >ca *r ^U « U

qj •* O" « S °

3 T3 C 00o cs u o

•§•§ ^55 s S a

,-< U

g.« 8 iHS SU w

D.

•8

~ 8

I Ic ^8 ^

» Ie H

t £

S.

. .S O

a•» a

| Oi; «

.u£.O

S O

•s o" 5,s zI H« <

pC X

" Hv tdz z

oo r-- o —

— f) 00

QUQ5-JUZ "*0§

WCfl

E > §rt H e

S "^! Qb fc

z*HzHH

CQ

Ou

H*> V

2 .a

•2 =

S «

IIs fr

I II 0 e S S

irt B ' 'i a 13s! i--s J"5 -s SIS £»5 8 Si 8£ 3 = a » Ko.IB W U 3a, < u yj

> cL O.

C

e 5-

t 'rt .H

o S H95 01 01U S. D.a o o

5 o £ z

REPORT REQUIRED BY GOVERNMENT AUDITING STANDARDS

21

Francis I. Huffman, CPAL. Fred Monroe, CPAEsther Atteberry CPA

John L. Luffey, MBA, CPA (1963-2002)

& Monroe(A Professional Accounting Corporation)

C E R T I F I E D P U B L I C A C C O U N T A N T S

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE AND INTERNALCONTROL OVER FINANCIAL REPORTING BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCEWITH GOVERNMENT AUDITING STANDARDS

Board of DirectorsThe ARC of MorehouseBastrop, Louisiana

We have audited the financial statements of The ARC of Morehouse (the Association) asof and for the years ended June 30, 2005 and 2004 and have issued our report thereondated September 30,2005. We conducted our audit in accordance with auditing standardsgenerally accepted in the United States of America; the standards applicable to financialaudits contained in Government Auditing Standards, issued by the Comptroller General ofthe United States; and the Louisiana Governmental Audit Guide, issued by the LouisianaSociety of Certified Public Accountants and the Louisiana Legislative Auditor.

Compliance

As part of obtaining reasonable assurance about whether the Association's financialstatements are free of material misstatement, we performed tests of its compliance withcertain provisions of laws, regulations, contracts and grants, noncompliance with whichcould have a direct and material effect on the determination of financial statementamounts. However, providing an opinion on compliance with those provisions was not anobjective of our audit and, accordingly, we do not express such an opinion. The results ofour tests disclosed no instances of noncompliance that are required to be reported underGovernment Auditing Standards.

Internal Control over Financial Reporting

In planning and performing our audit, we considered the Association's internal control overfinancial reporting in order to determine our auditing procedures for the purpose ofexpressing our opinion on the financial statements and not to provide assurance on theinternal control over financial reporting.

Our consideration of the internal control over financial reporting would not necessarilydisclose all matters in the internal control over financial reporting that might be a materialweakness. A material weakness is a condition in which the design or operation of one ormore of the internal control components does not reduce to a relatively low level the riskthat misstatements in amounts that would be material in relation to the financial statements

(318) 387-2672 • FAX (318) 322-8866 • www.lhm-cpas.com1100 N 18th ST • PO Box 4745 • Monroe LA 71211-4745

MEMBERS OF THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS _Page 22

Board of DirectorsThe ARC of Morehouse

being audited may occur and not be detected within a timely period by employees in thenormal course of performing their assigned functions. We noted no matters involving theinternal control over financial reporting that we consider material weaknesses.

However, we noted other matters involving internal control and it operations that we havereported to management of The ARC of Morehouse in a separate letter dated September30, 2005.

This report is intended solely for the information and use of management of theAssociation, its oversight agency, other entities granting funds to the Association and theLegislative Auditor for the state of Louisiana and is not intended to be used and should notbe used by anyone other than these specified parties. Under Louisiana Revised Statute24:513, this report is distributed by the Legislative Auditor as a public document.

(A Professional Accounting Corporation)

September 30, 2005

23

The ARC of MorehouseStatus of Prior Year Findings

June 30, 2005

The following is a summary of the status of findings in the Schedule of Findings and QuestionedCosts issued in connection with the examination of the financial statements of the ARC ofMorehouse as of June 30, 2004.

There were no audit findings for the year ended June 30, 2004.

24

Francis I. Huffman, CPAI I iff OW L. Fred Monroe, CPAi_VJ I I y Esther Atteberry, CPA

John L. Luffey, MBA, CPA (1963-2002)

& Monroe(A Professional Accounting Corporation)

C E R T I F I E D PUBL IC A C C O U N T A N T S

MANAGEMENT LETTER

Board of DirectorsARC of Morehouse10650 Lucy Hudson DriveBastrop, Louisiana 71220

In planning and performing our audit of the financial statements of the ARC ofMorehouse (a nonprofit organization - the Association) for the year ended June 30,2005, we considered its internal control in order to determine our auditing proceduresfor the purpose of expressing our opinion on the financial statements and not to provideassurance on internal control. However, we noted a certain matter involving internalcontrol and its operation that we consider to be a reportable conditions under standardsestablished by the American Institute of Certified Public Accountants. Reportableconditions involve matters coming to our attention relating to significant deficiencies inthe design or operation of internal control that, in our judgment, could adversely affectthe Association's ability to initiate, record, process and report financial data consistentwith the assertions of management in the financial statements.

Payroll-

We noted during our test of the payroll policies that the Association's personnel recordshad some deficiencies. Of the twenty-five payroll items tested, six of the hourly ratespaid to the employees did not agree with the pay rate authorized in the personnelrecords. In checking further, it was determined these six employees' files were not up todate and the pay they received was accurate. Without proper authorization of the wagerate in the personnel file an employee could be paid the wrong hourly wage rate. Wealso noted that six additional personnel files did not contain any W-4's or L-4's. TheAssociation could be deducting Federal and State tax in amounts not authorized by theemployee because the proper deduction information is not maintained In their personnelfile.

We recommend that the Human Resources department of the Association review allemployee files to insure that there is proper authorization for the hourly rate being paidand also, that a current W-4 and L-4 is included to insure that the proper amounts ofwithholding authorized by the employee is being deducted.

(318) 387-2672 • FAX (318) 322-8866 • www.lhm-cpas.com1100 N 18mST.PO Box 4745 • Monroe LA 71211-4745

MEMBERS OF THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS

ARC of MorehouseManagement Letter

Management's Response:

The Arc of Morehouse obtains W-4's and L-4's for all employees as part of the newemployee hiring process. However, the Arc will implement measures to periodicallyaudit personnel files to insure that all salary and wage information is current, accurate,and present in each employee file.

This report is intended solely for the information and use of management of theAssociation, its oversight agency, other entities granting funds to the Association andthe Legislative Auditor for the State of Louisiana and is not intended to be and shouldnot be used by anyone other than these specified parties. Under Louisiana RevisedStatutes 24:513, this report is distributed by the Legislative Auditor as a publicdocument.

(A Professional Accounting Corporation)

September 30, 2005