Manuel João de Albuquerque Rocha Pereira Bóia [email protected]

Upload

aubrey-alexanderCategory

view

220download

3

The application of CIS to Portugal:The application of CIS to Portugal:

Survey Implementation and Survey Implementation and Results Analysis - Innovation vs. ProductivityResults Analysis - Innovation vs. Productivity

Manuel João Bóia Manuel João Bóia

[email protected]@dem.ist.utl.pt

Pedro Faria Pedro Faria

[email protected]@dem.ist.utl.pt

Science and Technology Policy ProgramScience and Technology Policy Program

MSc Engineering Policy and Management of TechnologyMSc Engineering Policy and Management of Technology

5th November 20045th November 2004

OutlineOutline

Part 1 – Innovation IndicatorsPart 1 – Innovation Indicators

1.1. Innovation IndicatorsInnovation Indicators

2.2. The Community Innovation SurveyThe Community Innovation Survey

3.3. Students PresentationStudents Presentation

4.4. Results (CIS 3),Results (CIS 3),

Innovative Enterprises by Sector and CIS Trajectories in the Innovative Enterprises by Sector and CIS Trajectories in the European ContextEuropean Context

Input vs. Output of Innovation in EuropeInput vs. Output of Innovation in Europe

Some Innovation CharacteristicsSome Innovation Characteristics

Other Strategic and Organizational Important ChangesOther Strategic and Organizational Important Changes

Innovation SourcesInnovation Sources

Innovation BarriersInnovation Barriers

5.5. Lessons Learned and ConclusionsLessons Learned and Conclusions

OutlineOutline

Part 2 - Innovation and Productivity: Part 2 - Innovation and Productivity: What can we learn from the CIS 3 Results for What can we learn from the CIS 3 Results for Portugal?Portugal?

1.1. Innovation and Productivity TheoryInnovation and Productivity Theory

2.2. A model for the analysis of innovation and productivity in the short A model for the analysis of innovation and productivity in the short runrun

3.3. Results with CIS 3 dataResults with CIS 3 data

4.4. Lessons Learned and ConclusionsLessons Learned and Conclusions

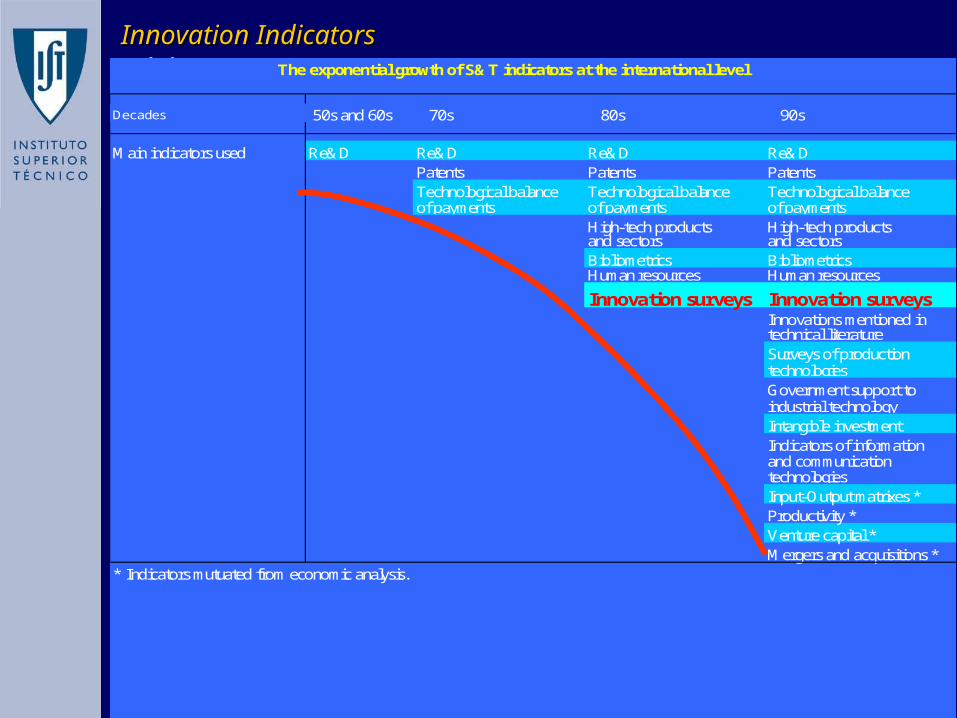

Innovation IndicatorsInnovation Indicators1.11.1 The exponential growth of S&T indicators at the international level

Decades 50s and 60s 70s 80s 90s

Main indicators used Re&D Re&D Re&D Re&DPatents Patents PatentsTechnological balance Technological balance Technological balanceof payments of payments of payments

High-tech products High-tech productsand sectors and sectorsBibliometrics BibliometricsHuman resources Human resources

Innovation surveys Innovation surveysInnovations mentioned intechnical literatureSurveys of productiontechnologiesGovernment support toindustrial technologyIntangible investmentIndicators of informationand communication technologiesInput-Output matrixes *Productivity *Venture capital *Mergers and acquisitions *

* Indicators mutuated from economic analysis.

CIS 3CIS 32.12.1

PortugalPortugal

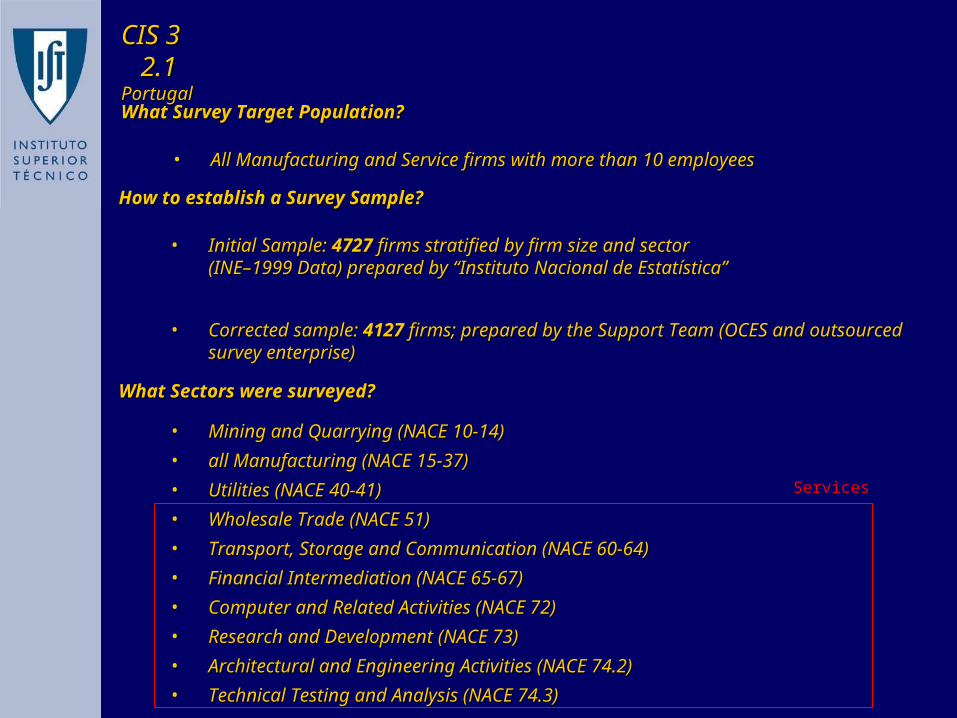

How to establish a Survey Sample?How to establish a Survey Sample?

• Initial Sample: Initial Sample: 47274727 firms stratified by firm size and sector firms stratified by firm size and sector (INE–1999 Data) prepared by “Instituto Nacional de Estatística”(INE–1999 Data) prepared by “Instituto Nacional de Estatística”

• Corrected sample: Corrected sample: 41274127 firms; prepared by the Support Team (OCES and firms; prepared by the Support Team (OCES and outsourced survey enterprise)outsourced survey enterprise)

What Sectors were surveyed?What Sectors were surveyed?

• Mining and Quarrying (NACE 10-14)Mining and Quarrying (NACE 10-14)

• all Manufacturing (NACE 15-37)all Manufacturing (NACE 15-37)

• Utilities (NACE 40-41)Utilities (NACE 40-41)

• Wholesale Trade (NACE 51) Wholesale Trade (NACE 51)

• Transport, Storage and Communication (NACE 60-64)Transport, Storage and Communication (NACE 60-64)

• Financial Intermediation (NACE 65-67)Financial Intermediation (NACE 65-67)

• Computer and Related Activities (NACE 72)Computer and Related Activities (NACE 72)

• Research and Development (NACE 73)Research and Development (NACE 73)

• Architectural and Engineering Activities (NACE 74.2)Architectural and Engineering Activities (NACE 74.2)

• Technical Testing and Analysis (NACE 74.3)Technical Testing and Analysis (NACE 74.3)

What Survey Target Population?What Survey Target Population?

• All Manufacturing and Service firms with more than 10 employeesAll Manufacturing and Service firms with more than 10 employees

Services

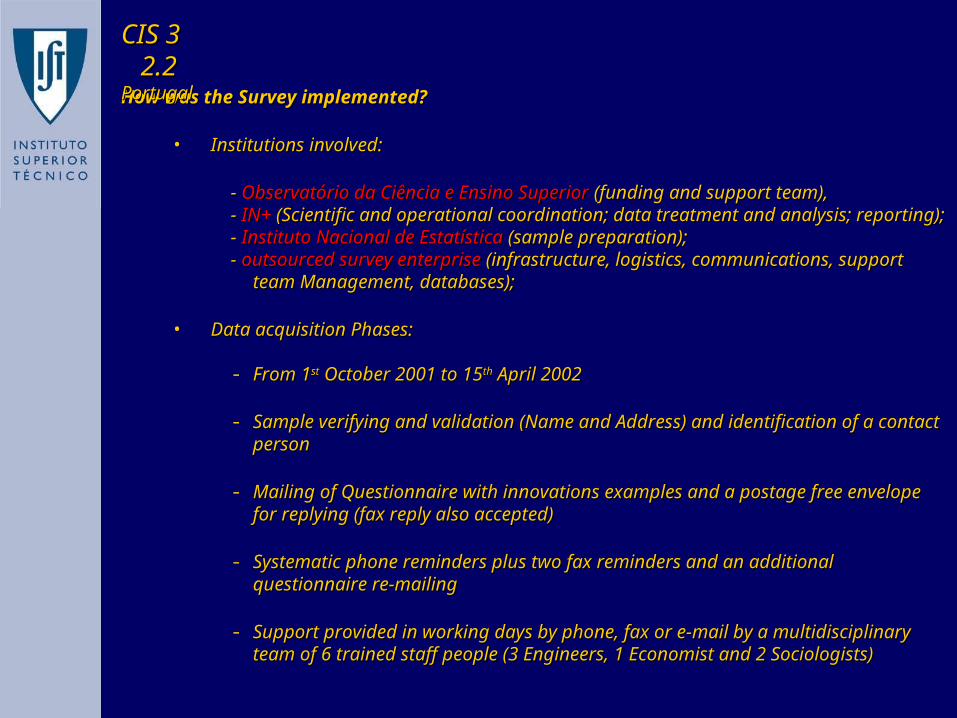

How was the Survey implemented?How was the Survey implemented?

• Institutions involved: Institutions involved:

- - Observatório da Ciência e Ensino SuperiorObservatório da Ciência e Ensino Superior (funding and support team), (funding and support team),- - IN+IN+ (Scientific and operational coordination; data treatment and analysis; (Scientific and operational coordination; data treatment and analysis;

reporting); reporting); - - Instituto Nacional de EstatísticaInstituto Nacional de Estatística (sample preparation); (sample preparation); - - outsourced survey enterpriseoutsourced survey enterprise (infrastructure, logistics, communications, (infrastructure, logistics, communications,

support team Management, databases); support team Management, databases);

• Data acquisition Phases:Data acquisition Phases:

- From 1From 1stst October 2001 to 15 October 2001 to 15thth April 2002 April 2002

- Sample verifying and validation (Name and Address) and identification of Sample verifying and validation (Name and Address) and identification of a contact persona contact person

- Mailing of Questionnaire with innovations examples and a postage free Mailing of Questionnaire with innovations examples and a postage free envelope for replying (fax reply also accepted) envelope for replying (fax reply also accepted)

- Systematic phone reminders plus two fax reminders and an additional Systematic phone reminders plus two fax reminders and an additional questionnaire re-mailingquestionnaire re-mailing

- Support provided in working days by phone, fax or e-mail by a Support provided in working days by phone, fax or e-mail by a multidisciplinary team of 6 trained staff people (3 Engineers, 1 Economist multidisciplinary team of 6 trained staff people (3 Engineers, 1 Economist and 2 Sociologists)and 2 Sociologists)

CIS 3CIS 32.22.2

PortugalPortugal

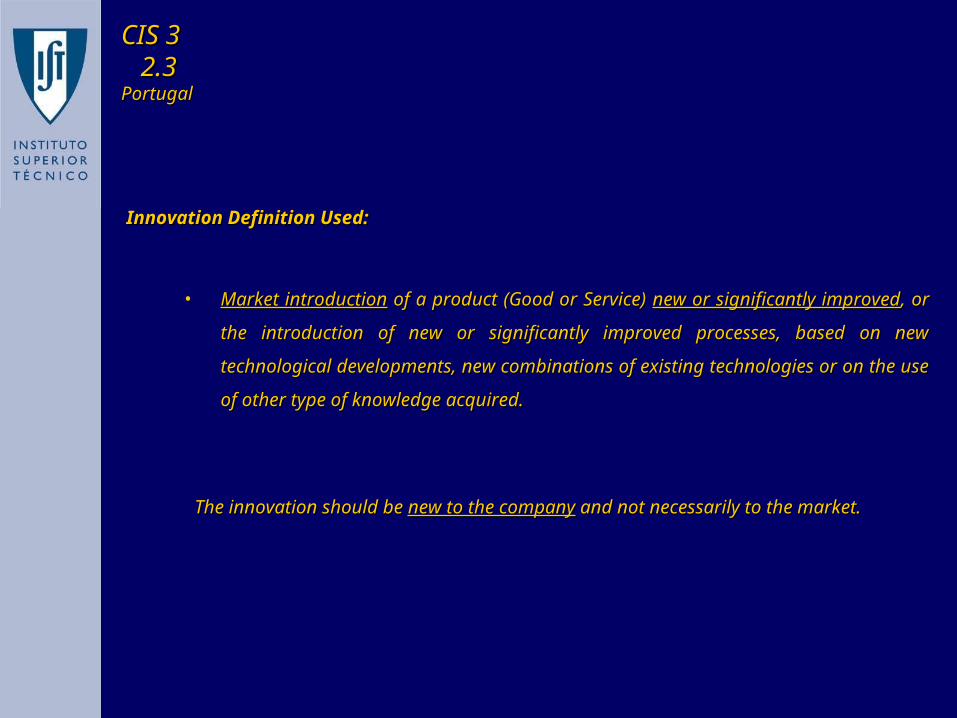

Innovation Definition Used:Innovation Definition Used:

• Market introductionMarket introduction of a product (Good or Service) of a product (Good or Service) new or significantly new or significantly

improvedimproved, or the introduction of new or significantly improved processes, , or the introduction of new or significantly improved processes,

based on new technological developments, new combinations of existing based on new technological developments, new combinations of existing

technologies or on the use of other type of knowledge acquired.technologies or on the use of other type of knowledge acquired.

The innovation should be The innovation should be new to the companynew to the company and not necessarily to the market. and not necessarily to the market.

CIS 3CIS 32.32.3

PortugalPortugal

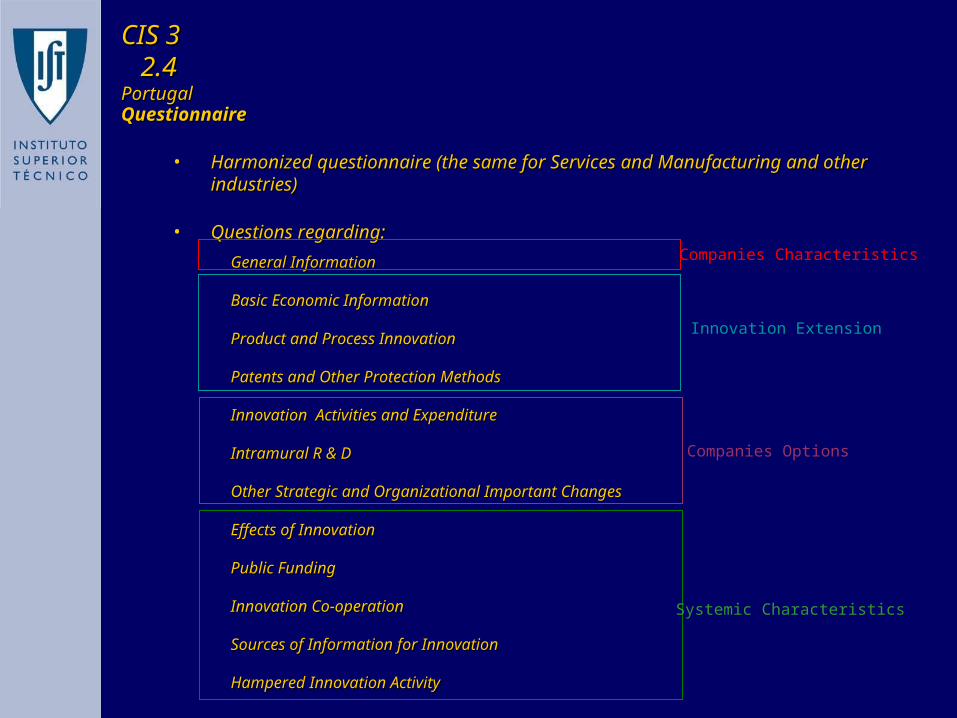

QuestionnaireQuestionnaire

• Harmonized questionnaire (the same for Services and Manufacturing and Harmonized questionnaire (the same for Services and Manufacturing and other industries)other industries)

• Questions regarding:Questions regarding:

General InformationGeneral Information

Basic Economic InformationBasic Economic Information

Product and Process InnovationProduct and Process Innovation

Patents and Other Protection MethodsPatents and Other Protection Methods

Innovation Activities and ExpenditureInnovation Activities and Expenditure

Intramural R & DIntramural R & D

Other Strategic and Organizational Important ChangesOther Strategic and Organizational Important Changes

Effects of InnovationEffects of Innovation

Public FundingPublic Funding

Innovation Co-operationInnovation Co-operation

Sources of Information for InnovationSources of Information for Innovation

Hampered Innovation ActivityHampered Innovation Activity

Companies Characteristics

Innovation Extension

Companies Options

Systemic Characteristics

CIS 3CIS 32.42.4

PortugalPortugal

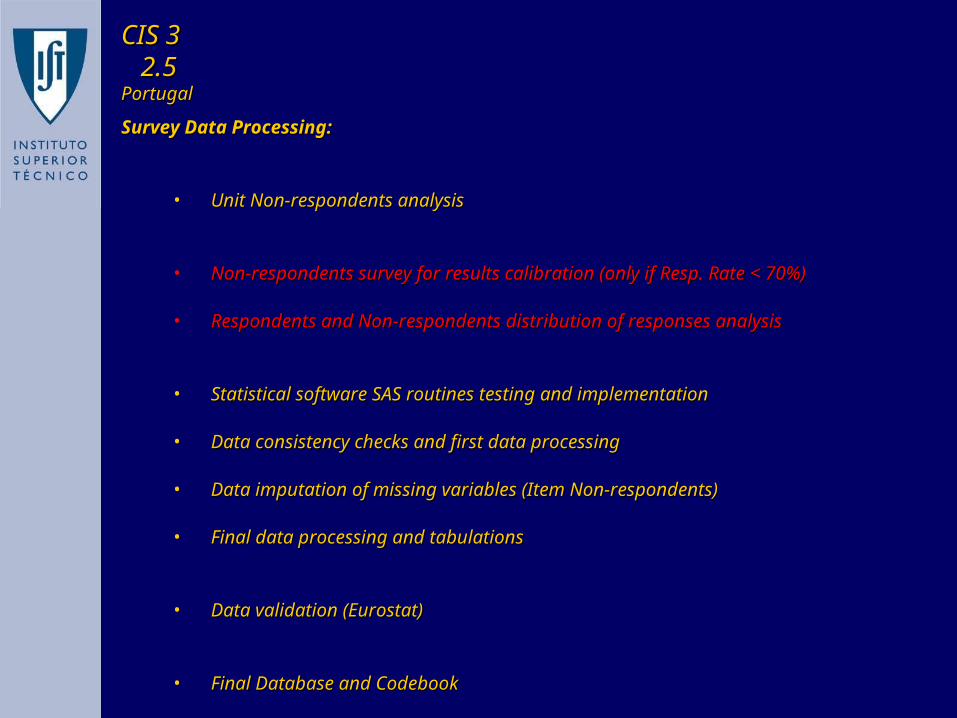

Survey Data Processing:Survey Data Processing:

• Unit Non-respondents analysis Unit Non-respondents analysis

• Non-respondents survey for results calibration (only if Resp. Rate < 70%)Non-respondents survey for results calibration (only if Resp. Rate < 70%)

• Respondents and Non-respondents distribution of responses analysisRespondents and Non-respondents distribution of responses analysis

• Statistical software SAS routines testing and implementationStatistical software SAS routines testing and implementation

• Data consistency checks and first data processingData consistency checks and first data processing

• Data imputation of missing variables (Item Non-respondents)Data imputation of missing variables (Item Non-respondents)

• Final data processing and tabulationsFinal data processing and tabulations

• Data validation (Eurostat)Data validation (Eurostat)

• Final Database and CodebookFinal Database and Codebook

CIS 3CIS 32.52.5

PortugalPortugal

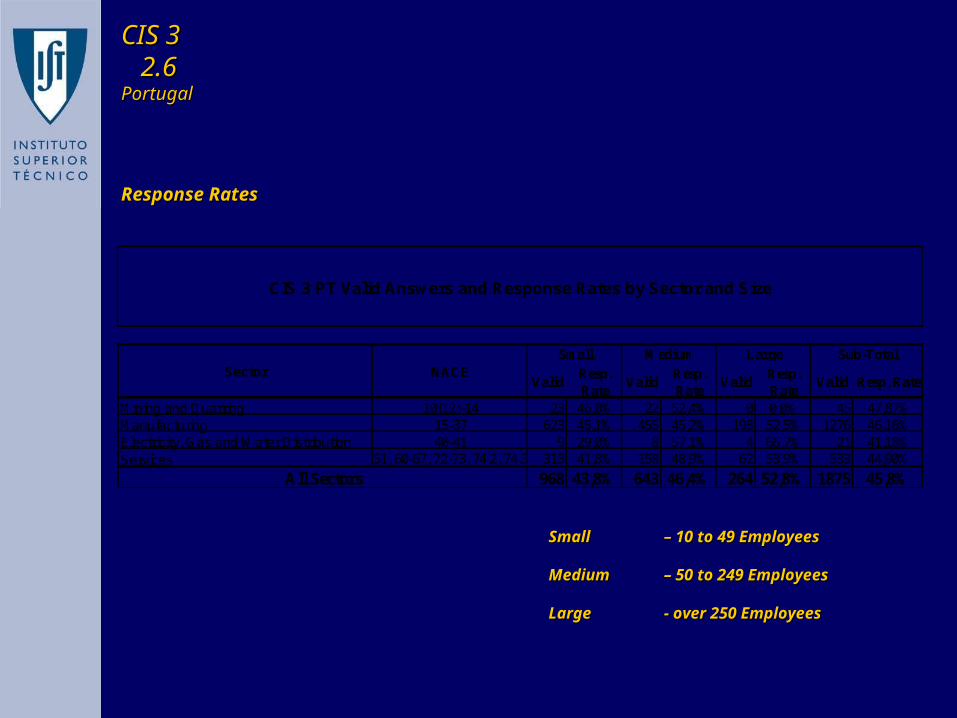

Response RatesResponse Rates

ValidResp. Rate

ValidResp. Rate

ValidResp. Rate

Valid Resp. Rate

Mining and Quarring 10(12)-14 23 46,0% 22 52,4% 0 0,0% 45 47,87%Manufacturing 15-37 623 45,1% 455 45,2% 198 52,5% 1276 46,16%Electricity, Gas and Water Distribution 40-41 9 29,0% 8 57,1% 4 66,7% 21 41,18%Services 51, 60-67, 72-73, 74.2, 74.3 313 41,8% 158 48,9% 62 53,9% 533 44,90%

968 43,8% 643 46,4% 264 52,8% 1875 45,8%

Sector

All Sectors

CIS 3 PT Valid Answers and Response Rates by Sector and Size

Small Medium Large NACE

Sub-Total

Small Small – 10 to 49 Employees– 10 to 49 Employees

Medium Medium – 50 to 249 Employees– 50 to 249 Employees

Large Large - over 250 Employees- over 250 Employees

CIS 3CIS 32.62.6

PortugalPortugal

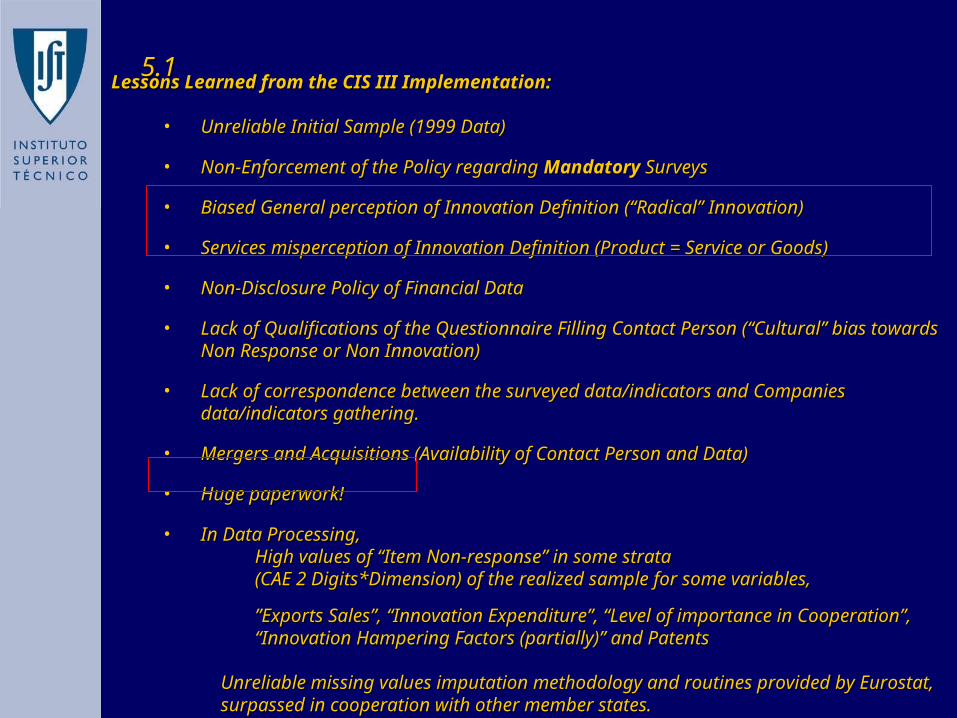

Lessons Learned from the CIS III Implementation:Lessons Learned from the CIS III Implementation:

• Unreliable Initial Sample (1999 Data)Unreliable Initial Sample (1999 Data)

• Non-Enforcement of the Policy regarding Non-Enforcement of the Policy regarding MandatoryMandatory Surveys Surveys

• Biased General perception of Innovation Definition (“Radical” Innovation)Biased General perception of Innovation Definition (“Radical” Innovation)

• Services misperception of Innovation Definition (Product = Service or Goods)Services misperception of Innovation Definition (Product = Service or Goods)

• Non-Disclosure Policy of Financial DataNon-Disclosure Policy of Financial Data

• Lack of Qualifications of the Questionnaire Filling Contact Person (“Cultural” Lack of Qualifications of the Questionnaire Filling Contact Person (“Cultural” bias towards Non Response or Non Innovation)bias towards Non Response or Non Innovation)

• Lack of correspondence between the surveyed data/indicators and Companies Lack of correspondence between the surveyed data/indicators and Companies data/indicators gathering.data/indicators gathering.

• Mergers and Acquisitions (Availability of Contact Person and Data)Mergers and Acquisitions (Availability of Contact Person and Data)

• Huge paperwork!Huge paperwork!

• In Data Processing,In Data Processing,High values of “Item Non-response” in some strata High values of “Item Non-response” in some strata (CAE 2 Digits*Dimension) of the realized sample for some variables,(CAE 2 Digits*Dimension) of the realized sample for some variables,

”Exports Sales”, “Innovation Expenditure”, “Level of importance in ”Exports Sales”, “Innovation Expenditure”, “Level of importance in Cooperation”, “Innovation Hampering Factors (partially)” and PatentsCooperation”, “Innovation Hampering Factors (partially)” and Patents

Unreliable missing values imputation methodology and routines provided by Unreliable missing values imputation methodology and routines provided by Eurostat, surpassed in cooperation with other member states.Eurostat, surpassed in cooperation with other member states.

5.15.1

Students PresentationsStudents Presentations

IrelandAustria

Germany

The Netherlands

UK

Sweden

Norway

France

Luxemburg

Belgium

0%

20%

40%

60%

80%

20% 40% 60% 80%

Proportion of Manufacturing Innovating Enterprises

Pro

po

rtio

n o

f

Ser

vic

e In

no

vati

ng

E

nte

rpri

se

s

Portugal Italy

Finland

Greece

DenmarkSpain

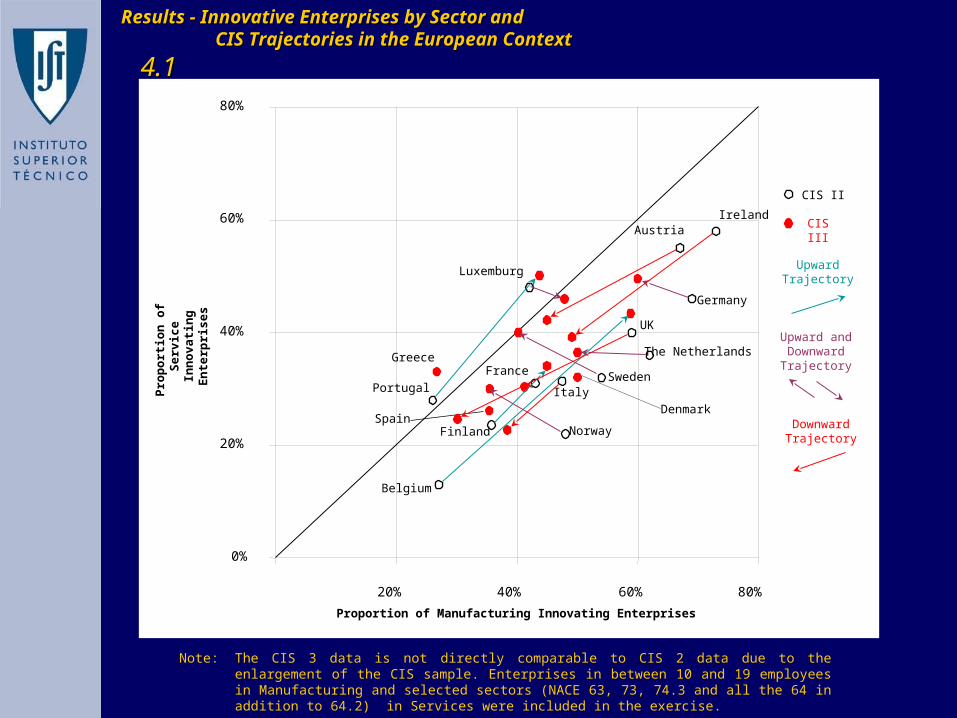

Results - Innovative Enterprises by Sector and Results - Innovative Enterprises by Sector and CIS Trajectories in the European ContextCIS Trajectories in the European Context

Note: The CIS 3 data is not directly comparable to CIS 2 data due to the enlargement of the CIS sample. Enterprises in between 10 and 19 employees in Manufacturing and selected sectors (NACE 63, 73, 74.3 and all the 64 in addition to 64.2) in Services were included in the exercise.

CIS III

CIS II

Upward Trajectory

Upward and Downward Trajectory

Downward Trajectory

4.14.1

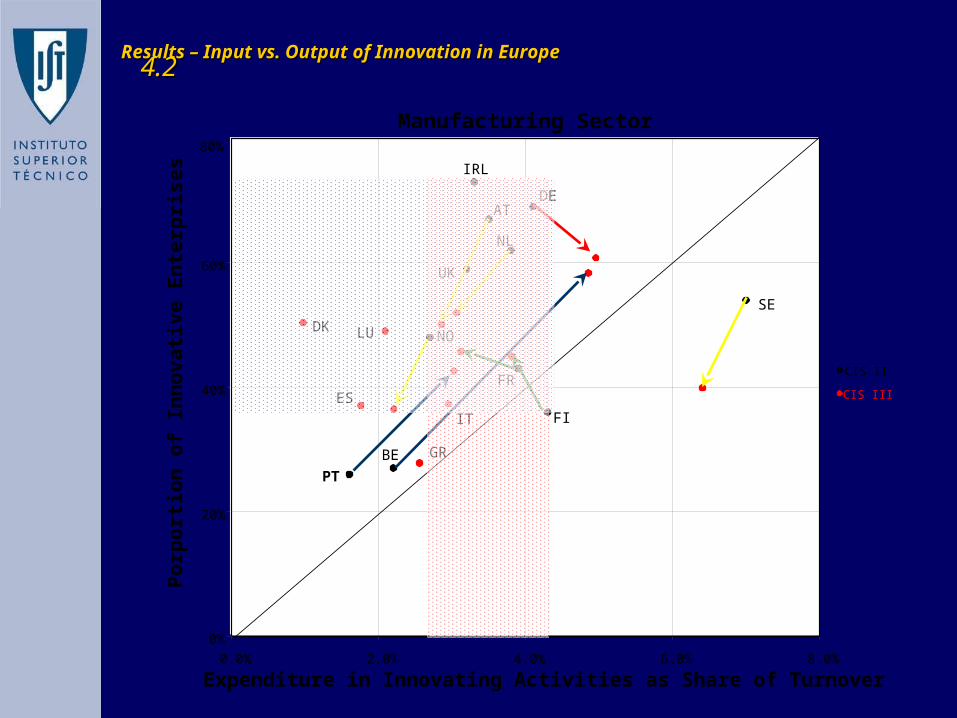

Results – Input vs. Output of Innovation in EuropeResults – Input vs. Output of Innovation in Europe4.24.2

IRL

DEAT

NL

UK

SE

NO

FR

FI

BE

PT

0%

20%

40%

60%

80%

0.0% 2.0% 4.0% 6.0% 8.0%

Expenditure in Innovating Activities as Share of Turnover

Po

rpo

rtio

n o

f In

no

va

tiv

e E

nte

rpri

se

s

Manufacturing Sector

CIS III

CIS II

GR

ES

IT

LUDK

Results – Some Innovation CharacteristicsResults – Some Innovation Characteristics4.34.3

Innovation is Firm Size dependent Innovation is Firm Size dependent (larger firms innovate more)(larger firms innovate more)

Innovation has sector specificitiesInnovation has sector specificities

The integration of the firm in a network The integration of the firm in a network (e.g., integration into a group) (e.g., integration into a group) increases the probability to innovateincreases the probability to innovate

The level of competition in a market influences a firm’s The level of competition in a market influences a firm’s probability to innovate probability to innovate (Highly competitive markets provide more innovative (Highly competitive markets provide more innovative firms)firms)

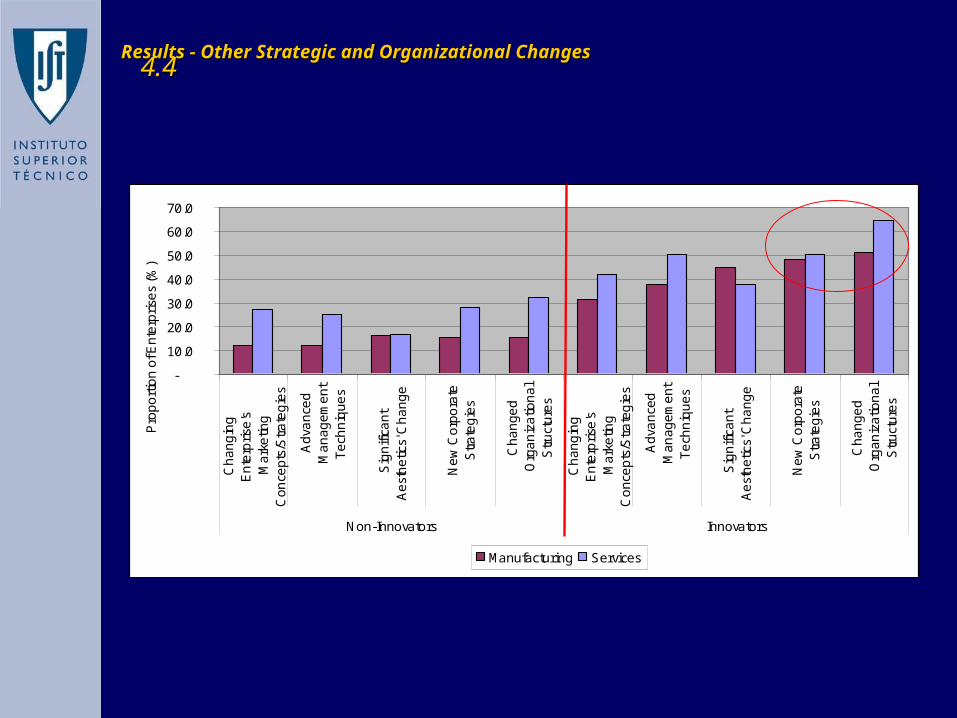

Results - Other Strategic and Organizational ChangesResults - Other Strategic and Organizational Changes

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Ch

an

gin

gE

nte

rpri

se's

Ma

rke

ting

Co

nce

pts

/Str

ate

gie

s

Ad

van

ced

Ma

na

ge

me

nt

Te

chn

iqu

es

Sig

nifi

can

tA

est

he

tics'

Ch

an

ge

Ne

w C

orp

ora

teS

tra

teg

ies

Ch

an

ge

dO

rga

niz

atio

na

lS

tru

ctu

res

Ch

an

gin

gE

nte

rpri

se's

Ma

rke

ting

Co

nce

pts

/Str

ate

gie

s

Ad

van

ced

Ma

na

ge

me

nt

Te

chn

iqu

es

Sig

nifi

can

tA

est

he

tics'

Ch

an

ge

Ne

w C

orp

ora

teS

tra

teg

ies

Ch

an

ge

dO

rga

niz

atio

na

lS

tru

ctu

res

Non-Innovators Innovators

Pro

po

rtio

n o

f En

terp

rise

s (%

)

Manufacturing Services

4.44.4

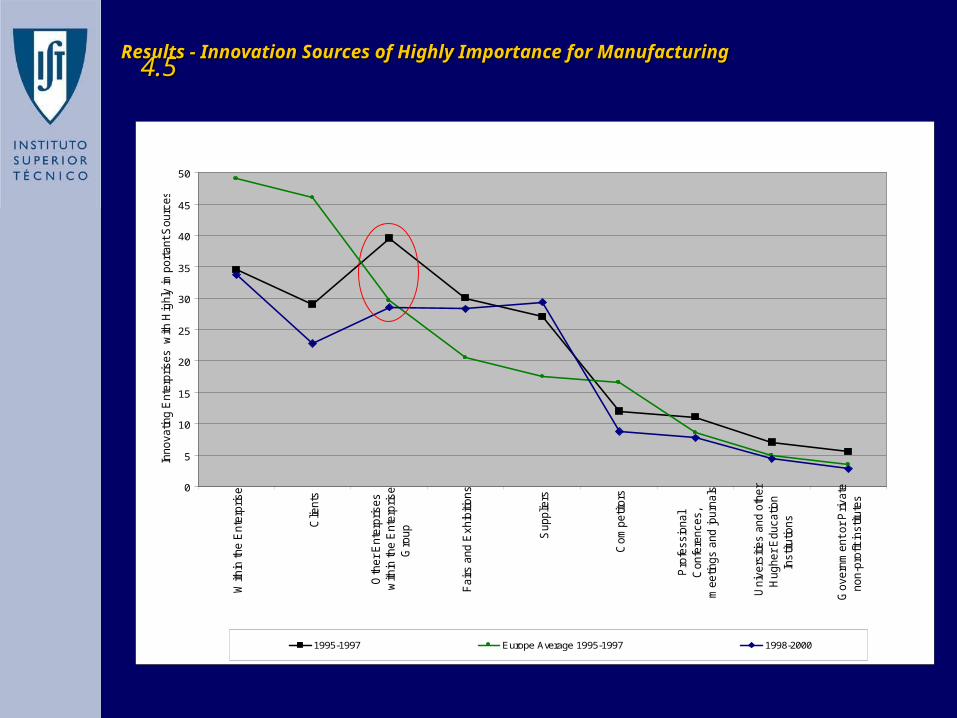

0

5

10

15

20

25

30

35

40

45

50

With

in the E

nte

rprise

Clie

nts

Oth

er

Ente

rprises

with

in the E

nte

rprise

Gro

up

Fairs a

nd E

xhib

itions

Supplie

rs

Com

petit

ors

Pro

fessio

nal

Confe

rences,

meetin

gs a

nd jo

urn

als

Univ

ers

ities a

nd o

ther

Hugher

Educatio

nIn

stit

utio

ns

Govern

ment or

Private

non-p

rofit

instit

ute

s

Innovatin

g E

nte

rprises w

ith H

ighly

import

ant S

ourc

es (

%)

1995-1997 Europe Average 1995-1997 1998-2000

Results - Innovation Sources of Highly Importance for ManufacturingResults - Innovation Sources of Highly Importance for Manufacturing4.54.5

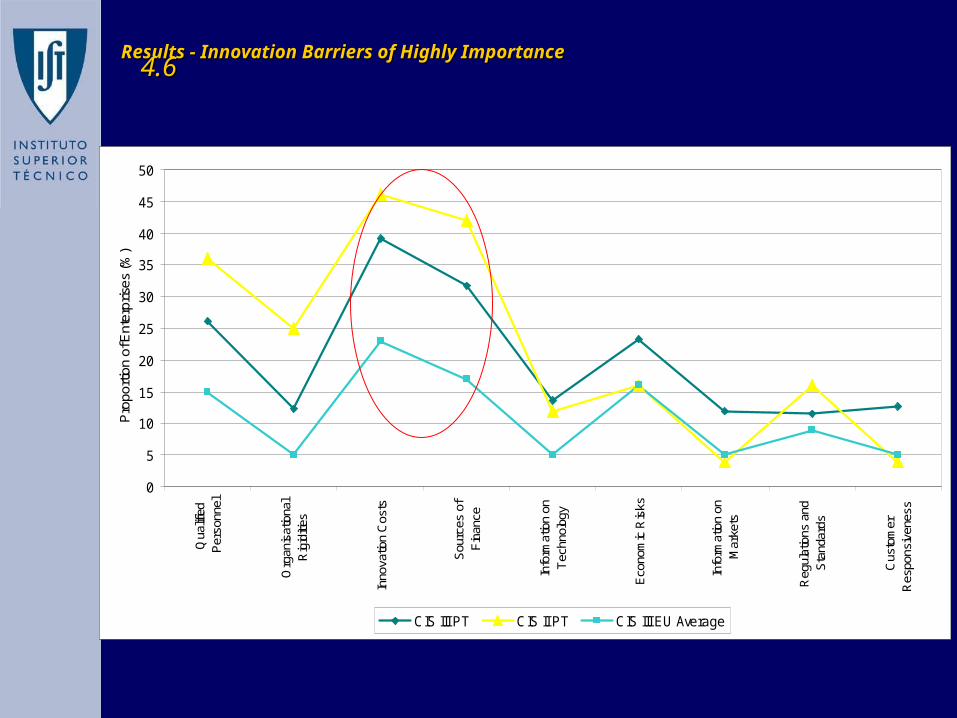

Results - Innovation Barriers of Highly ImportanceResults - Innovation Barriers of Highly Importance

0

5

10

15

20

25

30

35

40

45

50

Qua

lifie

dP

erso

nnel

Org

anis

atio

nal

Rig

iditi

es

Inno

vatio

n C

osts

Sou

rces

of

Fin

ance

Info

rmat

ion

onT

echn

olog

y

Eco

nom

ic R

isks

Info

rmat

ion

onM

arke

ts

Reg

ulat

ions

and

Sta

ndar

ds

Cus

tom

erR

espo

nsiv

enes

s

Pro

porti

on o

f Ent

erpr

ises

(%)

CIS III PT CIS II PT CIS III EU Average

4.64.6

Lessons Learned and Conclusions:Lessons Learned and Conclusions:

1.1. The CIS is a The CIS is a good evolving instrument for benchmarkinggood evolving instrument for benchmarking and follow up of and follow up of

the best practices, although incomplete in what concerns the systemic the best practices, although incomplete in what concerns the systemic

characteristics of innovation.characteristics of innovation.

2.2. A A significant increase in the innovation extension andsignificant increase in the innovation extension and in the firms in the firms

innovation expenditureinnovation expenditure was achieved for Portugal in CIS III compared to was achieved for Portugal in CIS III compared to

CIS II.CIS II.

3.3. In the innovation process, In the innovation process, both sources and barriers to innovation profiles both sources and barriers to innovation profiles

remain consistent with the CIS II dataremain consistent with the CIS II data, where the most relevant are , where the most relevant are

respectively “Within the Enterprise” and financial constraints. respectively “Within the Enterprise” and financial constraints.

4.4. Innovation expenditure has reached a milestone above which innovation Innovation expenditure has reached a milestone above which innovation

effectiveness appears to be more correlated with factors of systemic effectiveness appears to be more correlated with factors of systemic

nature.nature.

5.5. Technological innovation appearsTechnological innovation appears to be strongly to be strongly correlatedcorrelated with with

Organizational Innovation and ChangeOrganizational Innovation and Change..

5.25.2

OutlineOutline

Part 2 - Innovation and Productivity: Part 2 - Innovation and Productivity: What can we learn from the CIS 3 Results for What can we learn from the CIS 3 Results for Portugal?Portugal?

1.1. Innovation and Productivity TheoryInnovation and Productivity Theory

2.2. A model for the analysis of innovation and productivity in the short A model for the analysis of innovation and productivity in the short runrun

3.3. Results with CIS 3 dataResults with CIS 3 data

4.4. Lessons Learned and ConclusionsLessons Learned and Conclusions

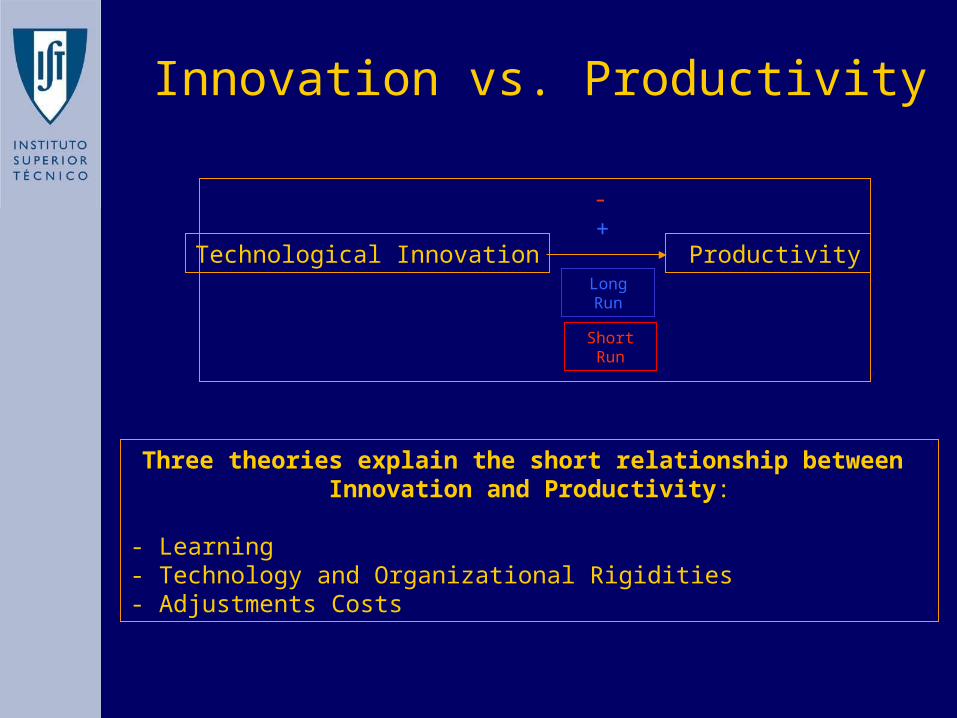

Three theories explain the short relationship between Innovation and Productivity:

- Learning- Technology and Organizational Rigidities- Adjustments Costs

Technological Innovation ProductivityLong Run

+

Short Run

-

Innovation vs. Productivity

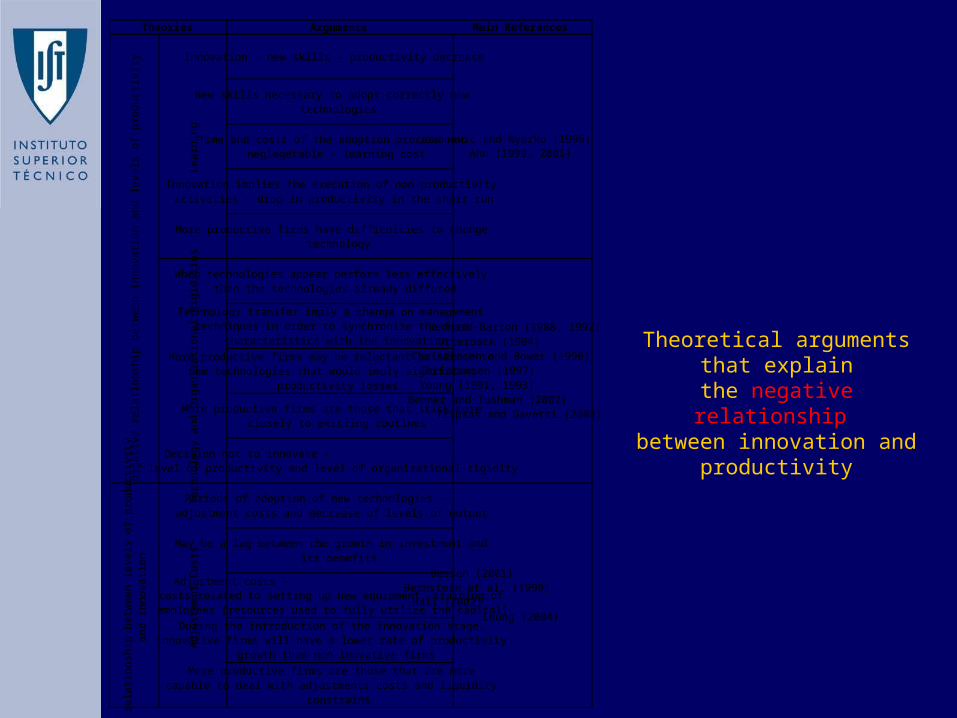

Theoretical arguments that explain

the negative relationship between innovation and

productivity

Arguments Main References

Innovation - new skills - productivity decrease

New skills necessary to adopt correctly new technologies

Time and costs of the adoption process not neglegetable - learning cost

Innovation implies the execution of non-productivity activities - drop in productivity in the short run

More productive firms have difficulties to change technology

When technologies appear perform less effectively than the technologies already diffused

Technology transfer imply a change on management techniques in order to synchronize the firm

characteristics with the innovationMore productive firms may be reluctant to switch to

new technologies that would imply significant productivity losses

More productive firms are those that stick more closely to existing routines

Decision not to innovate - level of productivity and level of organizational rigidity

Periods of adoption of new technologies - adjustment costs and decrease of levels of output

May be a lag between the growth in investment and its benefits

Adjustment costs - costs related to setting up new equipment, training of employees (resources used to fully utilize the capital)

During the introduction of the innovation stage, innovative firms will have a lower rate of productivity

growth than non-inovative firmsMore productive firms are those that are more

capable to deal with adjustments costs and liquidity constrainspo

sitive

rela

tions

hip

betw

een

leve

ls of

pro

duct

ivity

an

d in

nova

tion

Adju

stm

ent C

osts

Bessen (2001) Bernstein et al. (1999)

Hall (2002) Leung (2004)

Jovanovic and Nyarko (1996) Ahn (1999, 2001)

Lear

ning

Theories

nega

tive

rela

tions

hip

betw

een

inno

vatio

n an

d le

vels

of p

rodu

ctivi

ty

Tech

nolo

gy a

nd O

rgan

izatio

nal R

igid

ities

Leonard-Barton (1988, 1992) Utterback (1994)

Christensen and Bower (1996) Christensen (1997) Young (1991, 1993)

Benner and Tushman (2002) Tripsas and Gavetti (2002)

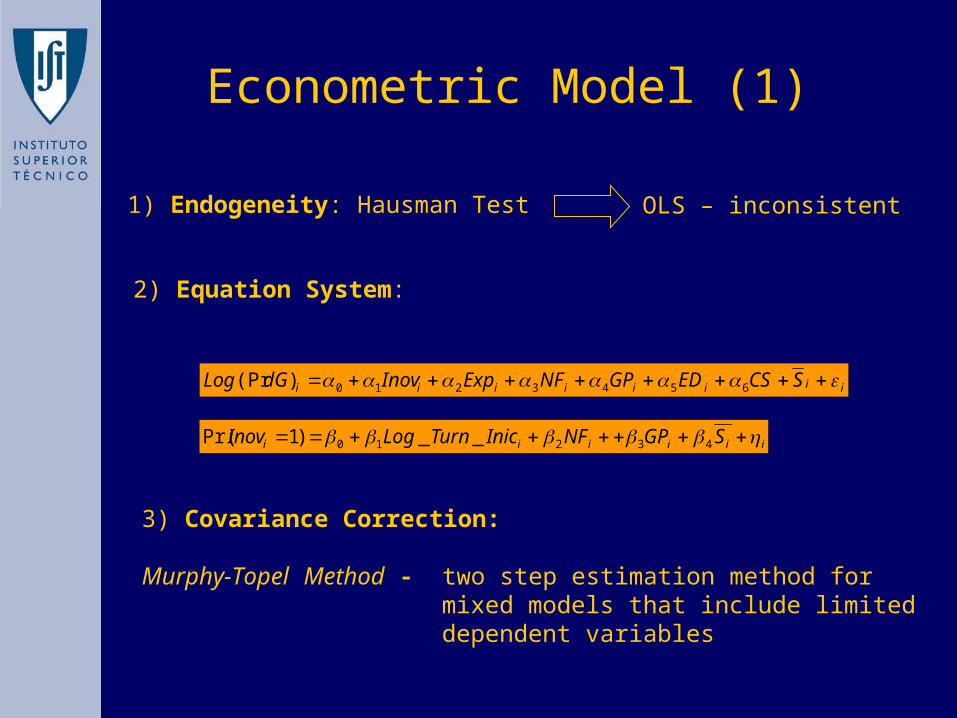

Econometric Model (1)

1) Endogeneity: Hausman Test OLS – inconsistent

2) Equation System:

3) Covariance Correction: Murphy-Topel Method - two step estimation method for mixed

models that include limited dependent variables

iiiiiiii SCSEDGPNFExpInovdGLog 6543210)(Pr

iiiiii SGPNFInicTurnLogInov 43210 __)1Pr(

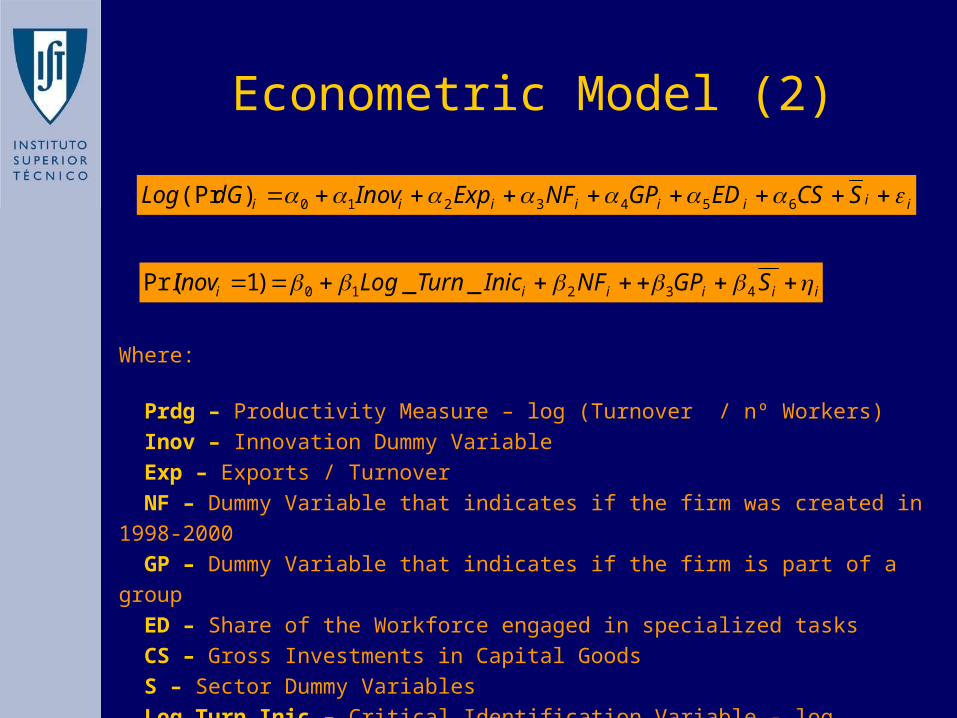

Econometric Model (2)

iiiiiiii SCSEDGPNFExpInovdGLog 6543210)(Pr

iiiiii SGPNFInicTurnLogInov 43210 __)1Pr(

Where:

Prdg – Productivity Measure – log (Turnover / nº Workers) Inov – Innovation Dummy Variable Exp – Exports / Turnover NF – Dummy Variable that indicates if the firm was created in 1998-2000 GP – Dummy Variable that indicates if the firm is part of a group ED – Share of the Workforce engaged in specialized tasks CS – Gross Investments in Capital Goods S – Sector Dummy Variables Log_Turn_Inic – Critical Identification Variable - log (Turnover 1998)

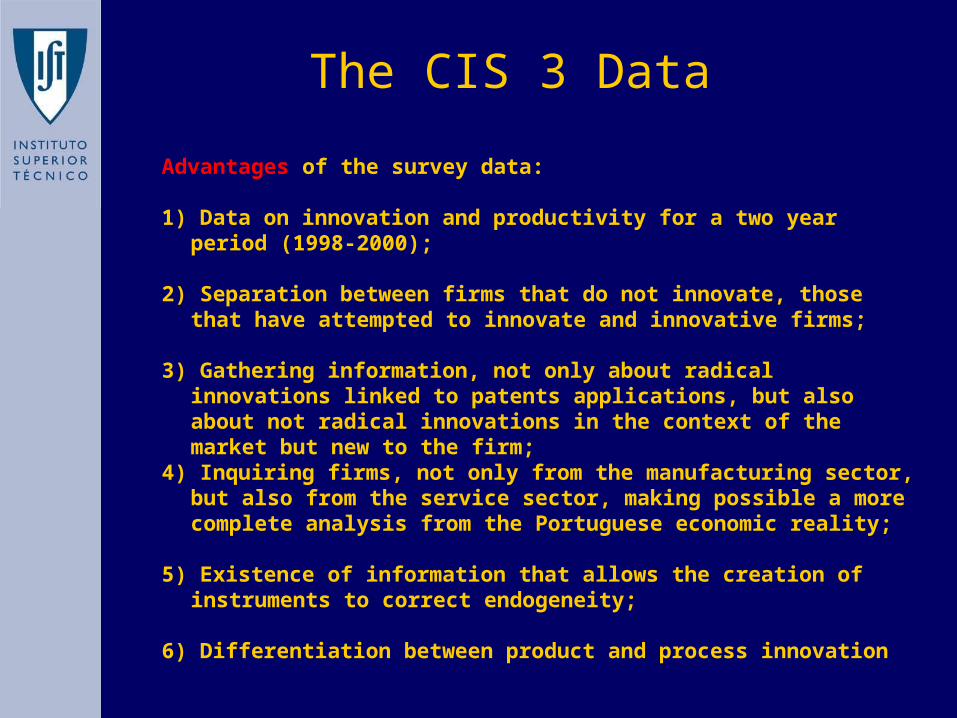

Advantages of the survey data:

1) Data on innovation and productivity for a two year period (1998-2000);

2) Separation between firms that do not innovate, those that have attempted to innovate and innovative firms;

3) Gathering information, not only about radical innovations linked to patents applications, but also about not radical innovations in the context of the market but new to the firm;

4) Inquiring firms, not only from the manufacturing sector, but also from the service sector, making possible a more complete analysis from the Portuguese economic reality;

5) Existence of information that allows the creation of instruments to correct endogeneity;

6) Differentiation between product and process innovation

The CIS 3 Data

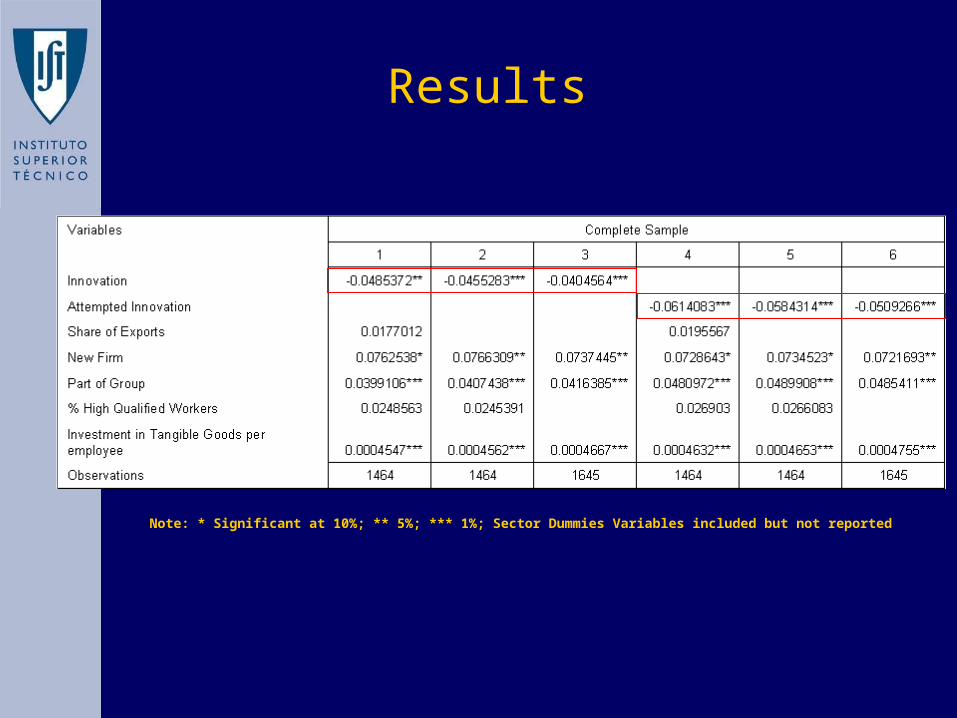

Note: * Significant at 10%; ** 5%; *** 1%; Sector Dummies Variables included but not reported

Results

• In the universe of Portuguese firms enquired by the CIS III, innovative firms have a lower degree of productivity growth when compared with non-innovative firms

• The more productive firms are more innovative – result coherent with the Adjustment Costs theory

• The inclusion of the variable Gross Investment in Capital Goods gives robustness to the model

Conclusions

Additional SlidesAdditional Slides

1995-1997 1998-2000 (1) 1998-2000 (2) 1995-1997 1998-2000 (1) 1998-2000 (2) 1995-1997 1998-2000 (1) 1998-2000 (2)

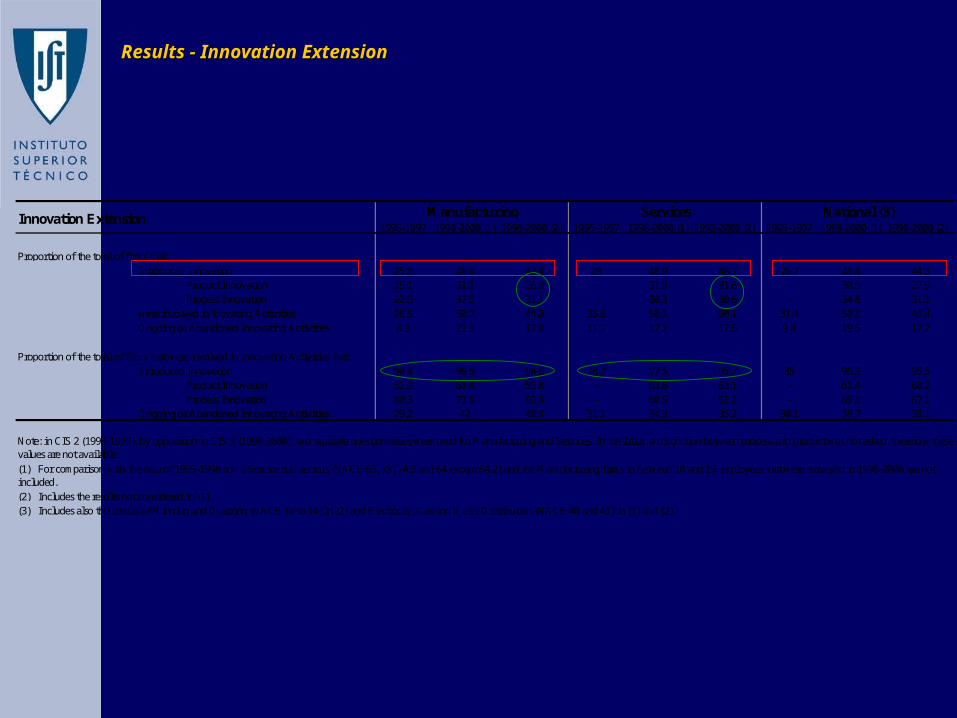

Introduced Innovation 25.8 48.4 42.4 28 48.9 48.7 26.7 48.4 44.3 Product Innovation 15.1 31.1 26.8 - 31.9 31.6 - 30.9 27.9

Process Innovation 22.9 37.5 31.1 - 30.3 30.6 - 34.8 31.1were involved in Inovating Activities 28.5 50.7 44.8 35.6 50.1 50.1 31.4 50.3 46.4

Ongoing or Abandoned Innovating Activities 8.3 21.3 17.8 11.1 17.2 17.6 9.4 19.5 17.7

Introduced Innovation 90.4 95.5 94.6 78.7 97.5 95.7 85 96.3 95.5 Product Innovation 52.9 61.4 59.8 - 63.6 63.1 - 61.4 60.2

Process Innovation 80.3 73.9 69.4 - 60.5 61.2 - 69.1 67.1Ongoing or Abandoned Innovating Activities 29.2 42 40.4 31.1 34.3 35.2 30.1 38.7 38.1

Manufacturing Services

(3) Includes also the results of Minning and Quarring (NACE 10 to 14) in (2) and Electricity, Gas and Water Distribution (NACE 40 and 41) in (1) and (2).

Note: in CIS 2 (1995-1997), by opposition to CIS 3 (1998-2000), two separate questionnaires were used for Manufacturing and Services. In the latter, a distinction between process and product was not asked, therefore these values are not available.

Proportion of the total of firms that were involved in Innovating Activities that:

Proportion of the total of firms that:

National (3)

(1) For comparison with the data of 1995-1998 some Service sub-sectors (NACE 63, 73, 74.3 and 64 except 64.2) and the Manufacturing firms in between 10 and 19 employees that were surveyed in 1998-2000 are not included.

Innovation Extension

(2) Includes the results not considered in (1).

Results - Innovation ExtensionResults - Innovation Extension

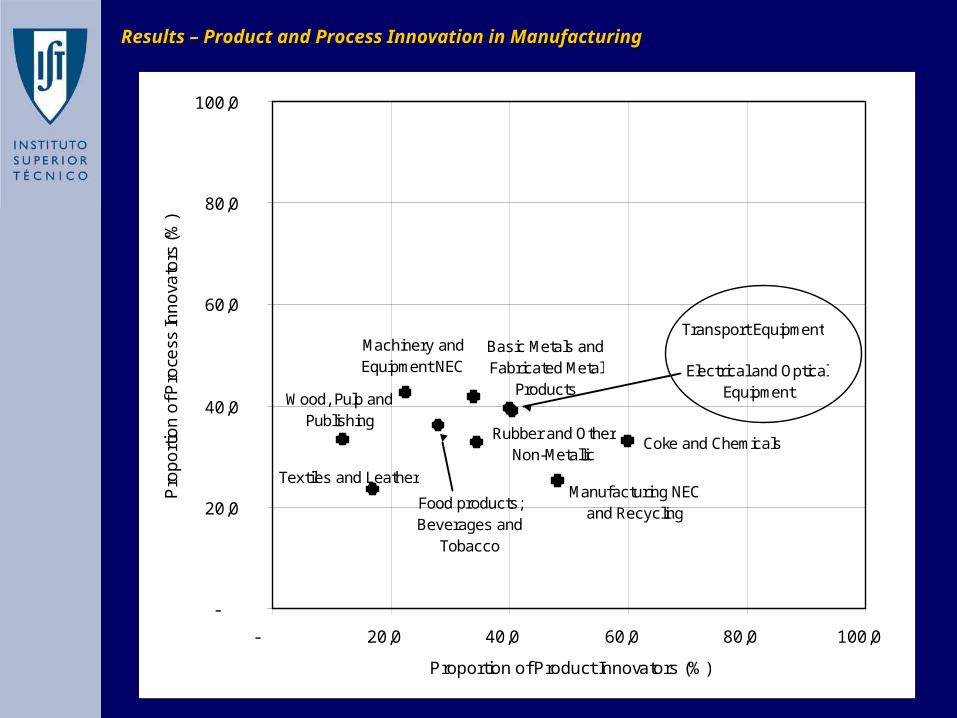

Results – Product and Process Innovation in ManufacturingResults – Product and Process Innovation in Manufacturing

Coke and ChemicalsRubber and Other

Non-Metallic

Food products; Beverages and

Tobacco

Textiles and Leather

Wood, Pulp and Publishing

Basic Metals and Fabricated Metal

Products

Machinery and Equipment NEC Electrical and Optical

Equipment

Transport Equipment

Manufacturing NEC and Recycling

-

20,0

40,0

60,0

80,0

100,0

- 20,0 40,0 60,0 80,0 100,0

Proportion of Product Innovators (%)

Pro

po

rtio

n o

f Pro

cess

Inn

ova

tors

(%

)

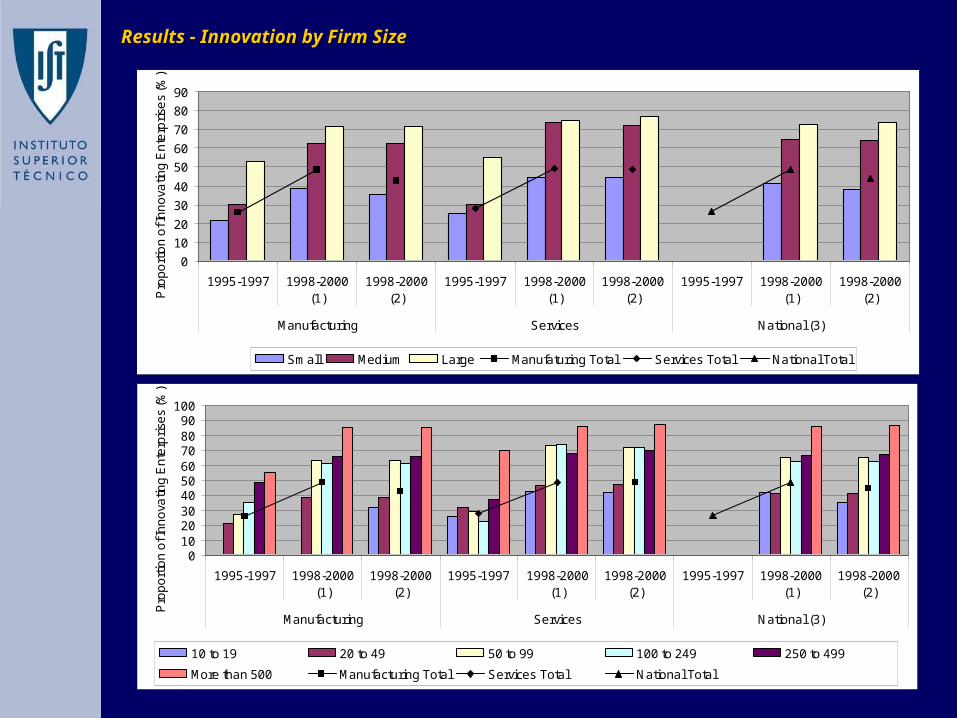

Results - Innovation by Firm SizeResults - Innovation by Firm Size

0

10

20

30

40

50

60

70

80

90

1995-1997 1998-2000(1)

1998-2000(2)

1995-1997 1998-2000(1)

1998-2000(2)

1995-1997 1998-2000(1)

1998-2000(2)

Manufacturing Services National (3)

Pro

po

rtio

n o

f In

no

vatin

g E

nte

rpri

ses

(%)

Small Medium Large Manufaturing Total Services Total National Total

0102030405060708090

100

1995-1997 1998-2000(1)

1998-2000(2)

1995-1997 1998-2000(1)

1998-2000(2)

1995-1997 1998-2000(1)

1998-2000(2)

Manufacturing Services National (3)

Pro

po

rtio

n o

f In

no

vatin

g E

nte

rpri

ses

(%)

10 to 19 20 to 49 50 to 99 100 to 249 250 to 499

More than 500 Manufacturing Total Services Total National Total

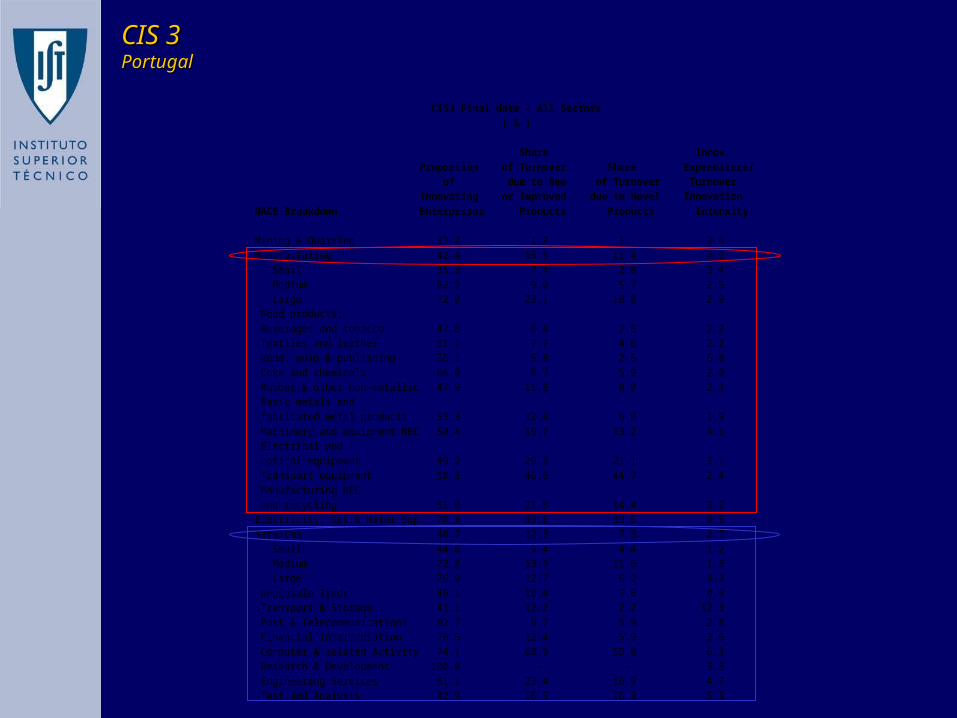

CIS3 Final data - All Sectors ( % ) Share Innov. Proportion of Turnover Share Expenditure/ of due to New of Turnover Turnover Innovating or Improved due to Novel Innovation NACE Breakdown Enterprises Products Products Intensity Mining & Quarring 37.2 1.2 1.1 2.6 Manufacturing 42.4 15.5 11.4 2.9 Small 35.3 7.4 2.8 3.4 Medium 62.2 9.0 5.7 2.5 Large 72.0 23.1 18.8 2.9 Food products; Beverages and tobacco 47.8 6.4 2.6 2.2 Textiles and leather 31.1 7.7 4.6 2.2 Wood, pulp & publishing 36.1 5.8 2.6 6.0 Coke and chemicals 66.0 8.7 5.9 2.0 Rubber & other non-metallic 47.9 11.8 8.0 2.3 Basic metals and fabricated metal products 53.3 12.4 6.0 1.9 Machinery and equipment NEC 50.4 19.7 13.2 4.5 Electrical and optical equipment 49.2 29.3 21.1 3.1 Transport equipment 50.3 46.6 44.7 2.4 Manufacturing NEC and recycling 51.0 21.8 14.4 3.2 Electricity, Gas & Water Sup. 70.3 39.6 39.5 0.5 Services 48.7 12.3 7.3 2.7 Small 44.0 9.4 4.4 1.2 Medium 72.2 13.9 11.6 1.3 Large 76.9 12.7 6.2 4.0 Wholesale Trade 46.1 10.4 7.6 0.9 Transport & Storage 41.1 12.2 2.2 12.3 Post & Telecommunications 92.7 9.7 5.9 2.8 Financial Intermediation 70.5 12.4 5.9 2.6 Computer & related Activity 74.1 60.9 59.0 6.3 Research & Development 100.0 - - 3.8 Engineering Services 61.1 23.4 16.9 4.7 Test and Analysis 42.9 16.5 16.3 5.3

CIS 3CIS 3PortugalPortugal

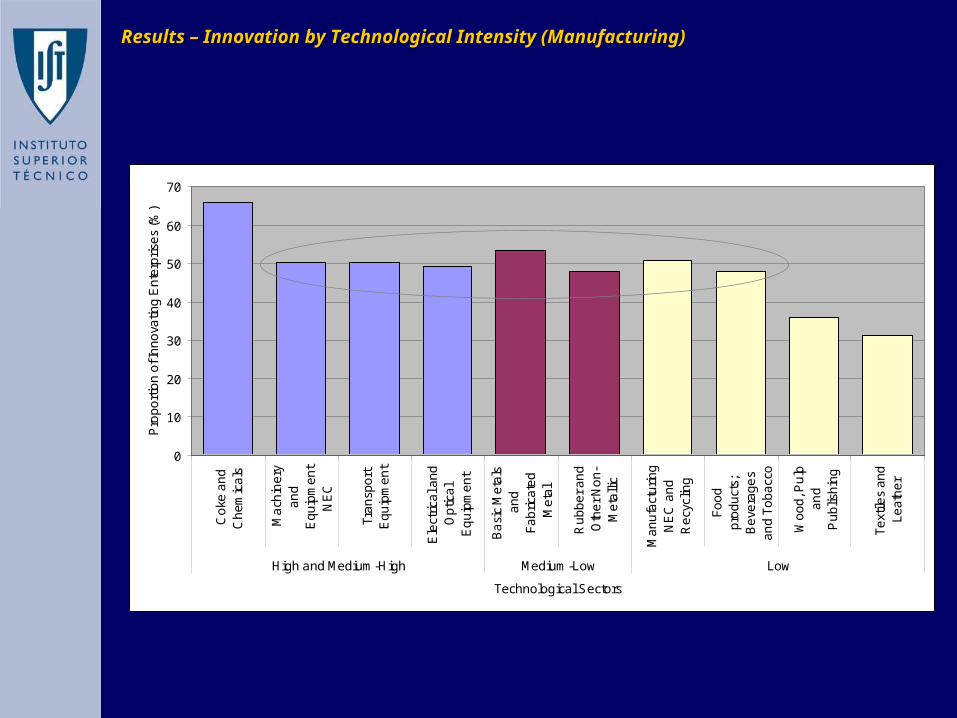

Results – Innovation by Technological Intensity (Manufacturing)Results – Innovation by Technological Intensity (Manufacturing)

0

10

20

30

40

50

60

70

Co

ke a

nd

Ch

em

ica

ls

Ma

chin

ery

an

dE

qu

ipm

en

tN

EC

Tra

nsp

ort

Eq

uip

me

nt

Ele

ctri

cal a

nd

Op

tica

lE

qu

ipm

en

t

Ba

sic

Me

tals

an

dF

ab

rica

ted

Me

tal

Ru

bb

er

an

dO

the

r N

on

-M

eta

llic

Ma

nu

fact

uri

ng

NE

C a

nd

Re

cycl

ing

Fo

od

pro

du

cts;

Be

vera

ge

sa

nd

To

ba

cco

Wo

od

, Pu

lpa

nd

Pu

blis

hin

g

Te

xtile

s a

nd

Le

ath

er

High and Medium-High Medium-Low Low

Technological Sectors

Pro

po

rtio

n o

f In

no

vatin

g E

nte

rpri

ses

(%)

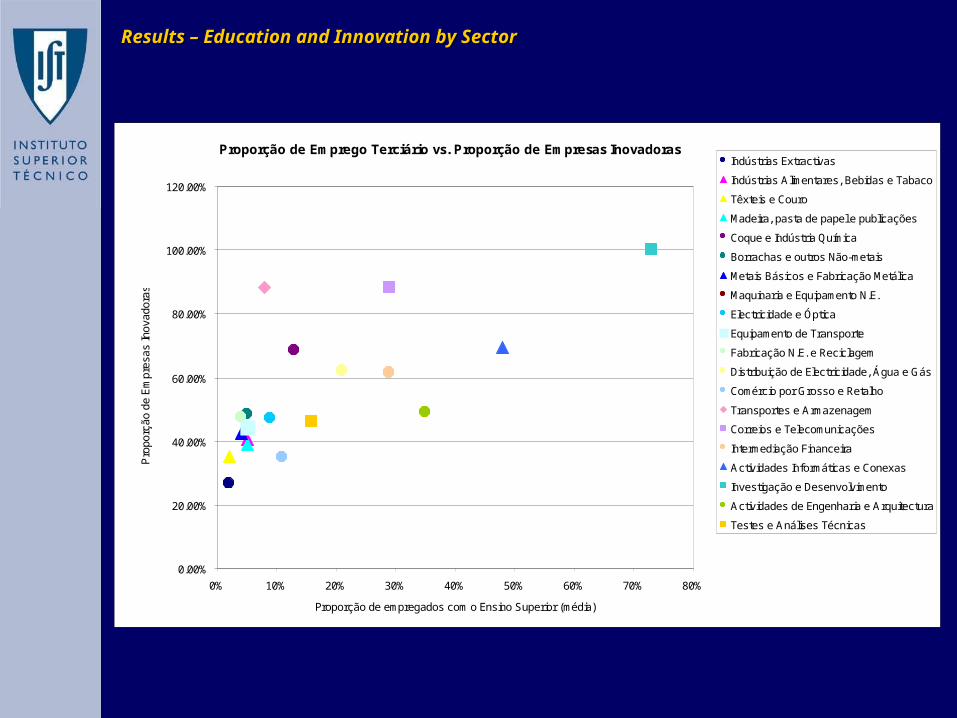

Results – Education and Innovation by SectorResults – Education and Innovation by Sector

Proporção de Emprego Terciário vs. Proporção de Empresas Inovadoras

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Proporção de empregados com o Ensino Superior (média)

Pro

porç

ão d

e E

mpr

esas

Inov

ador

as

Indústrias Extractivas

Indústrias Alimentares, Bebidas e Tabaco

Têxteis e Couro

Madeira, pasta de papel e publicações

Coque e Indústria Química

Borrachas e outros Não-metais

Metais Básicos e Fabricação Metálica

Maquinaria e Equipamento N.E.

Electricidade e Óptica

Equipamento de Transporte

Fabricação N.E. e Reciclagem

Distribuição de Electricidade, Água e Gás

Comércio por Grosso e Retalho

Transportes e Armazenagem

Correios e Telecomunicações

Intermediação Financeira

Actividades Informáticas e Conexas

Investigação e Desenvolvimento

Actividades de Engenharia e Arquitectura

Testes e Análises Técnicas

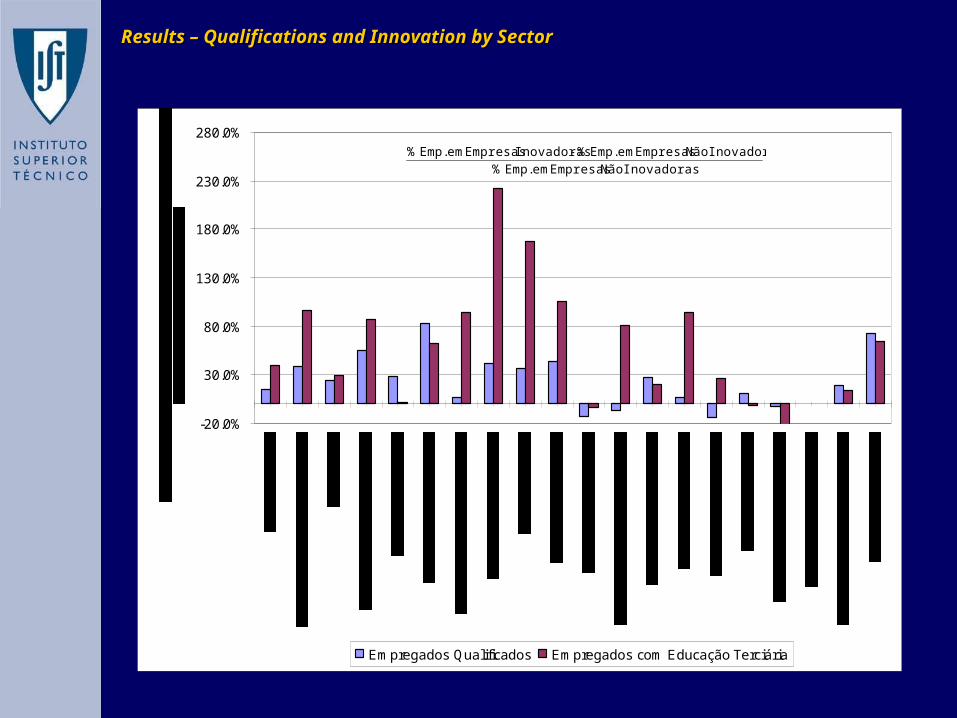

Results – Qualifications and Innovation by SectorResults – Qualifications and Innovation by Sector

-20.0%

30.0%

80.0%

130.0%

180.0%

230.0%

280.0%

Empregados Qualificados Empregados com Educação Terciária

Inovadoras Não Empresas em Emp. %

Inovadoras Não Empresas em Emp. % Inovadoras Empresas em Emp. % -

0

5

10

15

20

25

30

35

40

45

50

With

in th

eE

nter

pris

e

Clie

nts

Oth

erE

nter

pris

esw

ithin

the

Ent

erpr

ise

Gro

up

Sup

plie

rs

Com

petit

ors

Fai

rs a

ndE

xhib

ition

s

Pro

fess

iona

lC

onfe

renc

es,

mee

tings

and

jour

nals

Uni

vers

ities

and

othe

r Hug

her

Edu

catio

nIn

stitu

tions

Gov

ernm

ent o

rP

rivat

e no

n-pr

ofit

inst

itute

s

Inno

vatin

g E

nter

pris

es w

ith H

ighl

y im

porta

nt S

ourc

es (%

)

1995-1997 Europe Average 1995-1997 1998-2000

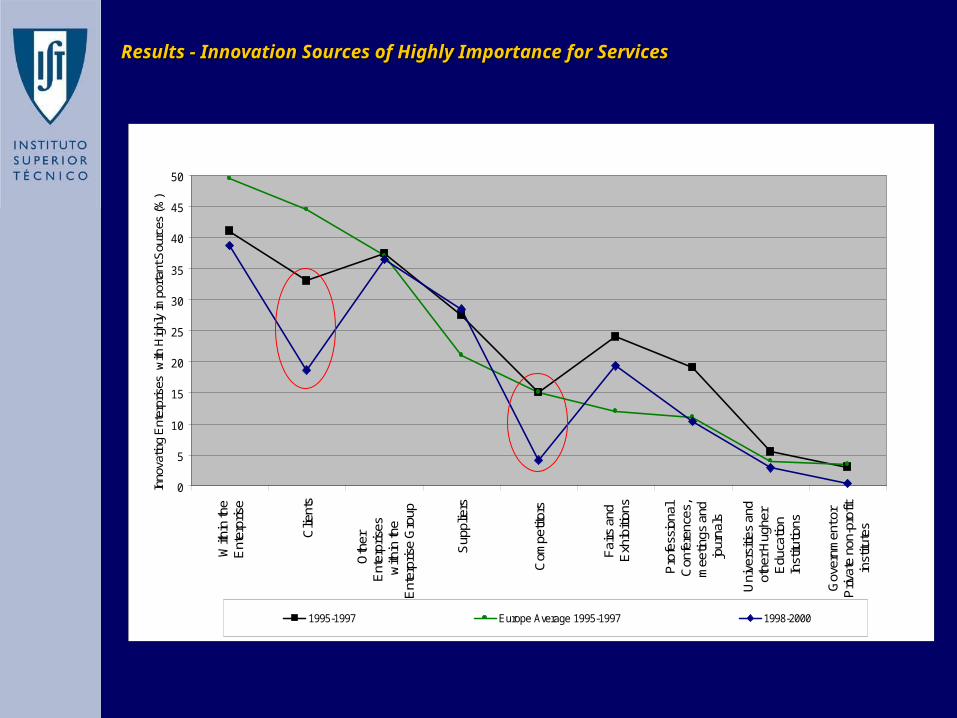

Results - Innovation Sources of Highly Importance for ServicesResults - Innovation Sources of Highly Importance for Services

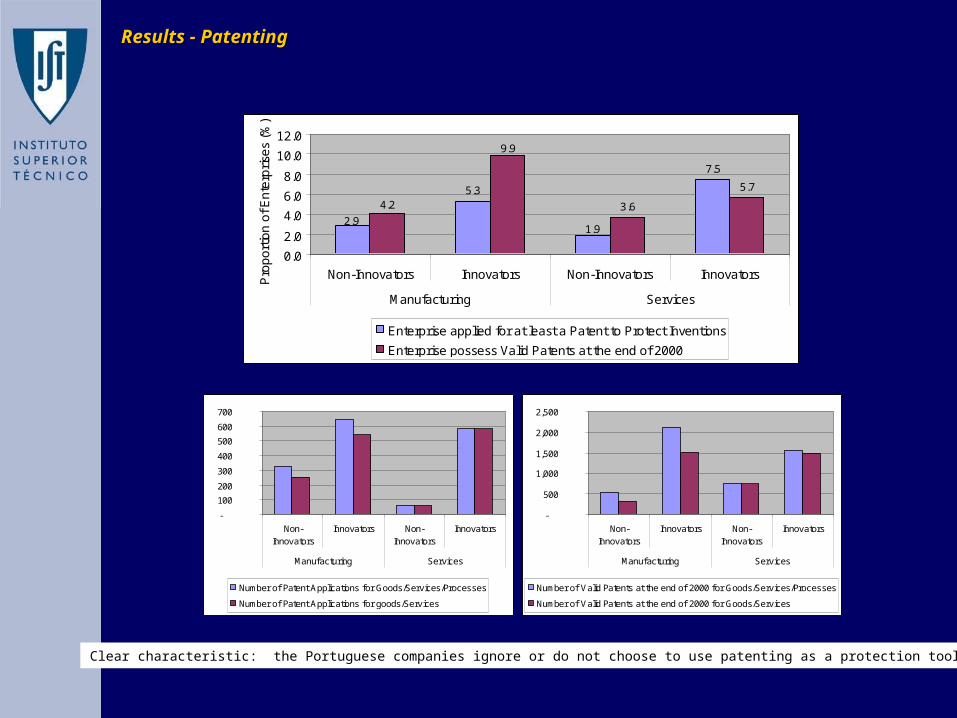

5.3

7.5

3.6

5.7

1.92.9

9.9

4.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Non-Innovators Innovators Non-Innovators Innovators

Manufacturing Services

Pro

po

rtio

n o

f E

nte

rpri

ses

(%)

Enterprise applied for at least a Patent to Protect Inventions

Enterprise possess Valid Patents at the end of 2000

-

100

200

300

400

500

600

700

Non-Innovators

Innovators Non-Innovators

Innovators

Manufacturing Services

Number of Patent Applications for Goods/Services/Processes

Number of Patent Applications for goods/Services

-

500

1,000

1,500

2,000

2,500

Non-Innovators

Innovators Non-Innovators

Innovators

Manufacturing Services

Number of Valid Patents at the end of 2000 for Goods/Services/Processes

Number of Valid Patents at the end of 2000 for Goods/Services

Clear characteristic: the Portuguese companies ignore or do not choose to use patenting as a protection tool

Results - PatentingResults - Patenting

-

5.0

10.0

15.0

20.0

25.0

Non-Innovators

Innovators Non-Innovators

Innovators NonInnovators

Innovators

Manufacturing Services National

Pro

po

rtio

n o

f En

terp

rise

s P

rote

ctin

g

Inn

ova

tion

s (%

)

Registration of Design Patterns Trademarks

Copyright Secrecy

Complexity of Design lead-time advantage over competitors

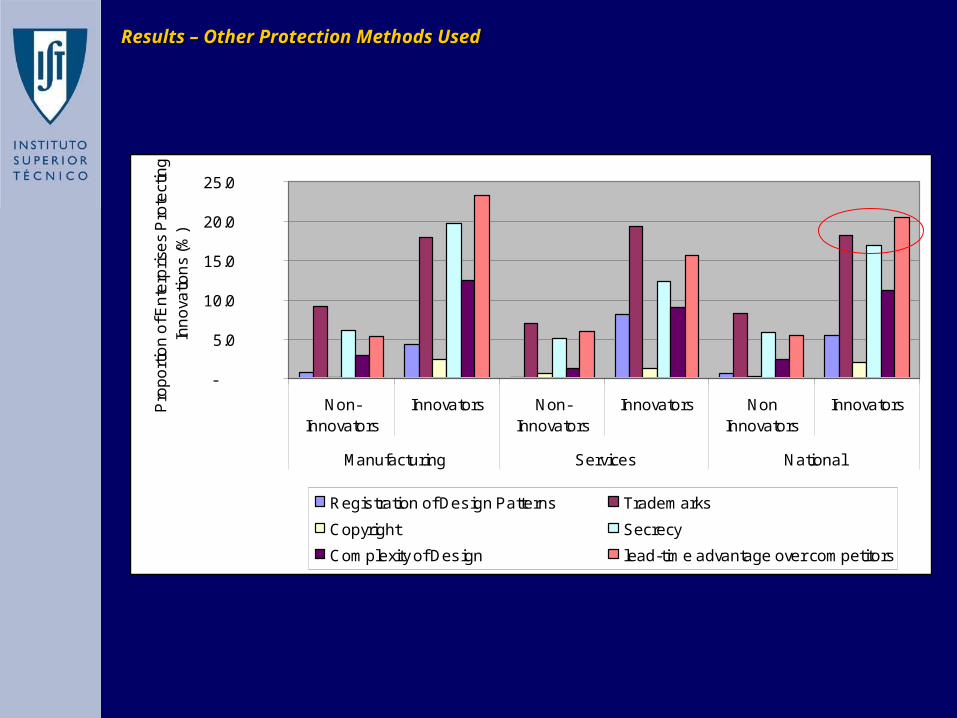

Results – Other Protection Methods UsedResults – Other Protection Methods Used