The Alternative Minimum Tax for Individuals: Outline

27

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1986 e Alternative Minimum Tax for Individuals: Outline Richard E. Fogg Copyright c 1986 by the authors. is article is brought to you by the William & Mary Law School Scholarship Repository. hps://scholarship.law.wm.edu/tax Repository Citation Fogg, Richard E., "e Alternative Minimum Tax for Individuals: Outline" (1986). William & Mary Annual Tax Conference. 570. hps://scholarship.law.wm.edu/tax/570

Transcript of The Alternative Minimum Tax for Individuals: Outline

College of William & Mary Law SchoolWilliam & Mary Law School Scholarship Repository

William & Mary Annual Tax Conference Conferences, Events, and Lectures

1986

The Alternative Minimum Tax for Individuals:OutlineRichard E. Fogg

Copyright c 1986 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository.https://scholarship.law.wm.edu/tax

Repository CitationFogg, Richard E., "The Alternative Minimum Tax for Individuals: Outline" (1986). William & Mary Annual Tax Conference. 570.https://scholarship.law.wm.edu/tax/570

THE ALTERNATIVE MINIMUM TAX FOR INDIVIDUALS

OUTLINE

By

Richard E. Fogg*Price WaterhouseRichmond, Virginia

I. In Search of a "Fair" Minimum Tax

A. Tax Reform Act of 1969. Tax Reform Act of 1969introduced the concept cof a minimum tax. Aminimum tax was imposed on 10% of the taxpayer'stax preference items reduced by a $30,000 exemp-tion. The tax applied to the extent that itexceeded the taypayer's federal income taxreduced by credits. In 1976, Congress signifi-cantly tightened the minimum tax rules. Theminimum tax rate increased to 15% and the exemp-tion was reduced to the greater of $10,000 orone-half of the regular tax liability. The listof tax preferences was expanded and the carryoverof excess regular taxes was repealed.

B. Revenue Act of 1978. The Alternative Minimum Taxfor taxpayers other than corporations was intro-duced in the Revenue Act of 1978, Sec. 421(a),and applies to tax years beginning after December31, 1978. The Senate Finance Committee notedthat the "Add-On Minimum Tax" does not well serveeither the goal of tax equity or the goal ofencouraging capital formation and economic growthby means of tax incentives. Becanuse the tax doesnot fully depend on the amount of regular taxespaid by the taxpayer, the present minimum tax canresult in a substantial tax increase for indivi-duals already paying regular taxes and highrates. S.REP. No. 95-1265, 95th Cong., 2nd Sess.201 (1978), 1978-3 C.B. 315, 499.

C. Economic Recovery Act of 1981 (ERTA). In 1981,the Alternative Minimum Tax was revised by theEconomic Recovery Tax Act of 1981. These changeswere generally limited to conforming the Alter-native Minimum Tax to technical and tax rateprovisions of the act.

* The author wishes to express appreciation to Robert L. Mandel,

Tax Senior, Price Waterhouse, Richmond, for his assistance ineveloping this oAtline.

D. Tax Equity and Fiscal Responsibiity Act of 1982(TEFRA). In 1982, the Tax Equity and FiscalResponsibility Act of 1982 (TEFRA), eliminatedthe Add-On Minimum Tax and significantly alteredthe Alternative Minimum Tax.

a. Congressional intent. Congress amended thepresent minimum tax provisions applying tothe individuals with one overriding objec-tive - that no taxpayer with substantialeconomic income should be able to avoid alltax liability by using exclusions, deduc-tions and credits. They explained that theability of high income individuals to paylittle or no tax undermines respect for theentire tax system and, thus, for the in-centive provisions themselves. Therefore,Congress provided an Alternative MinimumTax which was intended to ensure that, whenan individual's ability to pay taxes ismeasured by a broad based concept of in-come, a measure which can be reduced byonly a few of the incentive provisions, taxliability is at least a minimum percentageof that broad measure (See, generally, theGeneral Explanation of the Revenue Provi-sions of the Tax Equity- and Fiscal Respon-sibility Act of 1982 prepared by the staffof the Joint Committee on Taxation, be-ginning at page 16).

b. Summary of TEFRA changes. For years be-ginning in 1983 several new tax preferenceswere added, the treatment of itemizeddeductions was restructured, a flat 20%rate was established, and the minimum taxexemption was increased to $30,000 for un-married persons and $40,000 for marriedcouples.

E. Tax Reform Act of 1984. Additional technical andclarifying amendments to Sec. 55 and 57 were madein the Tax Reform Act of 1984.

F. Tax Reform Act of 1986. This act recognizes thatthe provisions of TEFRA are not broad enough toensure that individuals with substantial economicincome are not able to avoid significant tax lia-bility by using exclusions, deductions, andcredits. Although these incentives are providedto promote social objectives and other goals,Congress feels that the perceived unfairness inthe tax systems due to these incentives continueto outweigh their inherent values.

-3-

The new alternative minimum tax provisions in-clude more preferences, a broader interpretationof existing preferences, and the concept ofadjustments for deferral preferences. Theseadjustments, unlike exclusion preferences, maybenefit the taxpayer. They recognize the factthat certain items defer taxable income ratherthan exclude it and they allow the taxpayer tocarry deferral credits against regular taxliability in future years through minimum taxcredits. (See, generally, the Reasons for Changeof the Report of the Committee on Finance UnitedStates Senate to accompany H.R. 3838, beginningat page 518.)

TI. Current Law

A. There are Three Sections in the Internal RevenueCode that Pertain to the AMT for Individuals.

1 . Sec. 55 - imposes an alternative minimumtax on taxpayers other than corporatons;

2. Sec. 57 - defines the items of taxpreference;

3. Sec. 58 - provides rules for the applica-tion of the AMT.

B. Review of Sec. 55

1. Tax Imposed.

For individual taxpayers, *a tax of 20% isimposed on the excess, if any, of theAlternative Minimum Taxable Income (AMTI)over the exemption amount. This tax ispayable. to the extent it exceeds theregular tax for the taxable year. Sec.55(a)(1) and (2).

2. AMTI is Defined in Sec. 55(b).

a. Adjusted gross income ("AGI"), with-out regard to the net operating loss("NOL") deduction allowed by Sec.172;

b. Reduced under Sec. 55(b)(1) by:

(1) The alternative tax NOL deduc-tion;

-4-

(2) The alternative tax itemizedeductions; and,

(3) Alcohol fuel credits includedin gross income (Sec. 87) andthrowback trust distributions(Sec. 667).

c. Increased under Sec. 55(b)(2) by theitems of tax preference.

3. The Alternative Tax NOL is Defined in Sec.55(d).

In general, it is the same NOL as deter-mined under Sec. 172, except tax preferencedeductions are not allowed, and only thealternative tax itemized deductions areallowed. This will have the effect ofmaking AGI a larger amount where such itemsexist.

4. The Alternative Minimum Tax Itemized

Deductions.

They are defined in Sec. 55(e) to include:

(1) Casualty losses under Sec. 165(c)(3)and wagering losses under Sec.165(d);

(2) Charitable contributons;

(3) Medical deductions;

(4) "Qualified interest" as defined inSec. 55(e)(3); and,

(5) The deduction for estate taxes.

5. Exemption Amounts.

The exemption amounts provided in Sec.

55(f) are:

(1) $40,000 for a joint return or sur-viving spouse;

(2) $30,000 for a single taxpayer; or

(3) $20,000 for married filing separateor an estate or trust.

-5-

6. Summary of AMT.

The alternative minimum tax can be calcu-lated as follows:

Adjusted gross income (before NOL)less

The NOL deduction (if any)less

The alternative tax itemized deductionsless

The alcohol fuel credits and throwbackdistributions (if any)

plus

All tax preference itemsequals

Alternative minimum taxable income (AMTI)less

The exemption amountequals

AMT base

AMT base multiplied by 20%, less the regu-lar tax, is the alternative minimum tax.

7. The Regular Tax for Purposes of Sec. 55.

It is defined by Sec. 55(f) (2) as thetaxpayer's regular tax, excluding the taxesfor disposed general business property,annuities, pension plan lump-sum distribu-tions, early dispositions from IRA's, and"trust accumulation distributions.

a. The regular tax, as described above,

is then reduced by all tax creditsexcept the refundable credits ofwithheld income tax (Sec. 31), theearned income credit (Sec. 32), taxwithheld at source on nonresidentaliens and foreign corporations (Sec.33), credits for use of gasoline andfuels for farming and nontaxablepurposes (Sec. 34), and overpavmentsof tax (Sec. 35).

-6-

8. Payment of Difference Required.

If the taxpayer's gross AMT exceeds hisregular tax, he must pay this difference!Thus, other credits are not available tooffset this liability. Therefore, Sec.55(c)(3) is intended to provide thesecredits can be carried over to the extentthey are not used to offset the AMTliability. These credits are the resi-dential energy credit (Sec. 23), the creditfor interest on certain home mortgages(Sec. 25), the research credit (Sec. 30),the alcohol fuels credit (Sec. 40), theESOP credit (Sec. 41), the investment taxcredit (Sec. 46) and the targeted jobscredit (Sec. 51).

9. The Foreign Tax Credit May Reduce AMTLiability.

Therefore, Sec. 55(c)(2) provides rulesthat allow it only to offset such tax tothe extent of the foreign tax on foreignsource AMTI.

C. A Review of Sec. 57

1. Sec. 57 Defines the Items of Tax Prefer-ence.

There are twelve which are set forth below.

a. The dividends received exclusion.

b. For each item of depreciable realproperty (Sec. 1250 property), theexcess of accelerated depreciationover "as-if" straight line depre-ciation.

c. For each item of personal property(Sec. 1245 property) subject to alease, the excess of accelerateddepreciation over "as-if" straightline depreciation.

d. For each certified pollution controlfacility, the excess of the 60-monthamortization over the "as-if"straight line depreciation.

-7-

e. For each mine or other hard mineraldeposit, the excess of the develop-ment expenses and mining explorationexpenditures allowed under Sec. 616and 617 over a straight line amorti-zation expense over a 10-year life.

f. For circulation, the excess of cir-culation expenses over a 3-yearstraight line amortization of suchexpenses.

g. For research and experimental expen-ditures, the excess of research andexperimental expenses over a 10-yearstraight line amortization of suchexpenses.

h. For depletion, the excess of statu-tory depletion over the adjustedbasis of the property at the end ofthe taxable year (determined withoutregard to current year depletion).

i. For capital gains, the 60% netcapital gain deduction.

j. For incentive stock options (ISO's),the excess of the fair market valueof the stock over the exercise priceat the time of exercise.

k. In general, the amount by which theexcess productive well intangibledrilling costs (IDC) exceed thetaxpayer's net income from oil andgas properties is a tax preferenceitem. The excess IDC is the excessof such IDC over a straight lineamortization of such IDC over 10years or amortization on a units-of-production basis.

1. With respect to ACRS property subjectto a lease, the excess of ACRS depre-ciation over defined straight linedepreciation.

D. Election to Amortize Provision of Sec. 58

1. General.

Sec. 58(i)(1) generally provides the in-dividual taxpayer an election to ratablyamortize over 10 years (3 years for circu-lation expenditures) expenditures which areotherwise currently deductible. The elec-tion can be made with respect to anyqualified expenditure and is made to avoidthe inclusion of these expenditures as taxpreference items.

2. Qualified Expenditures as Provided by Sec.58(i) (2).

(1) Circulation expenditures under Sec.173;

(2) Research and experimental expendi-

tures under Sec. 174;

(3) IDC under Sec. 263(c);

(4) Mining development expenses underSec. 616(a); or

(5) Mining exploration expenses underSec. 617.

3. Special Election for IDC.

Allowed under Sec. 58(i)(4) to treat "non-limited IDC" as a 5-year ACRS propertyeligible for ITC.

(1) Non-limited IDC is IDC not allocableto a "limited business interest" asdefined in Sec. 55(e)(8)(C).

(2) Election is made at partner (or Scorporation stockholder) level.Therefore, IDC must be separatelystated on Schedule K-i.

E. A Closer Look at the Itemized Deduction forQualified Interest

1. Definition.

Sec. 55(e)(3) defines qualified interest asthe sum of:

a. Qualified housing interest; and,

b. Other interest to the extent it doesnot exceed the qualified net invest-ment income of the taxpayer.

2. Qualified Housing Interest.

Under Sec. 55(e)(4), qualified housinginterest includes interest on indebtednessfor:

(1) The taxpayer's principal residence;and,

(2) A "second home" (a vacation home) of

the taxpayer.

3. Qualified Net Investment Income.

Under Sec. 55(e)(5), qualified net invest-ment income is the excess of qualifiedinvestment income under Sec. 55(e)(5)(B)over qualified investment expenses underSec. 55(e)(5)(C).

(I) Investment income is defined underSec. 163(d)(3)(B) , which is interest,dividends, rents and royalties, netshort term capital gains, and depre-ciation recapture;

(2) Capital gain net income; and

(3) The divid-end exclusion.

4. Qualified Investment Expenses.

Under Sec. 55(e)(5) (C), qualified invest-ment expenses means deductions directlyconnected with the production of qualifiedinvestment income to the extent:

(1) Such deductions are allowable in com-puting AGI; and

(2) Such deductions are not tax prefer-ence items.

-10-

5. Income or Loss from Limited BusinessInterests.

These are taken into account in computingqualified net investment income.

(1) Limited business interest means aninterest as a limited partner in apartnership or a shareholder in an Scorporation if the taxpayer does notactively participate in management.

III. New Law: Tax Reform Act of 1986

A. There are six Sections in the Internal RevenueCode that Pertain to the AMT for Individuals:

1. Sec. 55 - imposes an alternative minimumtax.

2. Sec. 56 - provides adjustments in computingalternative minimum taxable income.

3. Sec. 57 - defines the items of taxpreference.

4. Sec. 58 - provides additional adjustmentsfor certain losses in computing alternativeminimum taxable income.

5. Sec. 59 - defines other items applicable tothe alternative minimum tax and providesseveral special rules.

6. Sec. 53 - introduces a credit for minimum

tax liability in prior years.

B. Review of Sec. 55

1. Tax imposed

For individual taxpayers, there is an addi-tional tax of the excess, if any, of thetentative minimum tax (TMT) over the regu-lar tax. Sec. 55(a).

2. TMT is defined in Sec. 55(b)(1)

The TMT is 21 percent of the excess of thealternative minimum taxable income tax(AMTI) over the exemption amount, reducedby the AMT foreign tax credit (FTC).

-11-

3. AMTI is defined in 55(b)(2)

It includes the adjustments in Sec. 56 and58 and the tax preference items in Sec. 57.

4. Exemption Amounts

The exemption amounts provided in Sec.55(d) are:

a. S40,000 for a joint return or a

surviving spouse;

b. $30,000 for a single taxpayer; or

c. $20,000 for a married taxpayer filinga separate return or an estate ortrust.

These exemption amounts are reduced by 25percent of the amount by which the AMTI ofthe taxpayer exceeds (1) $150,000, (2)$112,500, (3) $75.000, respectively.

5. Summary of Minimum Tax

Taxable Incomeplus/minus

All Adjustmentsplus

All Tax Preference Itemsequals

AMTIless

The Exemption amountthis quantity multiplied by

21 Percent Rateless

AMT Foreign Tax Creditequals

TMTCompare TMT with the Regular Tax. If TMTis higher, it must be paid. If Regular Taxis higher, it may be reduced by the MinimumTax Credit (MTC) to the amount of the TMT;then, it must be paid!

-12-

6. The Regular Tax for Purposes of Sec..55

Regular tax liability (Sec. 26(b)), reducedby the allowable foreign tax credit (Sec.27(a)).

a. It does not include any tax imposedon lump sum distributions to a bene-ficiary of a trust under 402(e).

b. It does not include any increase intax on certain dispositions of Sec.38 properly under Sec. 47.

C. Review of Sec. 56

1. Sec. 56 Defines the Adjustments in Com-puting AMTI.

There are nine which are set forth below:

a. Depreciation - Regular taxable incomemust be increased or decreased by the"net" difference between ACRS depre-ciation and alternative method depre-ciation. This provision applies toproperty placed in service after1986..

b. Mining exploration and costs - Theexcess of expensing over 10-yearamortization is an adjustment.

c. Certain long-term contracts - Methodsof accounting for long-term contractsthat permit deferral of income duringthe contract period (e.g., completedcontract method), are treated as anadjustment by requiring use of thepercentage of completion method forminimum tax purposes in post-March 1,1986 long-term contracts.

d. NOLs - The regular tax NOL is re-placed by an AMT NOL, which is aseparate calculation of the currentyear AMT NOL plus the AMT NOL carry-over, if any. AMT NOLs are allowedto offset up to 90 percent of AMTI.Amounts disallowed by reason of thislimitation may be carried over toother taxable years.

-13-

e- Pollution control facilities - Theexcess of 60-month amortization oncertified pollution control facili-ties over alternative depreciation isan adjustment.

f. Installment method of accounting -Use of the installment method ofaccounting is treated as an adjust-ment by not permitting use of theinstallment method for minimum taxpurposes on sales after March 1,1986. This applies to all trans-actions subject to proportionatedisallowance of the installmentmethod (i.e., dealer sales and salesof a trade or business or rental pro-perty where the purchase price ex-ceeds $150,000).

g. Itemized deductions - Most regulartax itemized deductions are allowedfor AMT purposes. The followingitemized deductions are not allowed:

i. state and local taxes

ii. real estate taxes

iii. medical expenses not greaterthan 10 percent of AGI

iv. miscellaneous deductions great-er than 2 percent of AGI (e.g.,tax preparation fees and pro-fessional dues)

v. interest expense other thanhome mortgage interest andinvestment interest to the ex-tent of net investment income.

o Upon a refinancing of aloan that gives rise toqualified housing inter-est, interest paid on thenew loan is treated asqualified housing inter-est to the extent that itqualified under the priorloan and the amount ofthe loan was not in-creased. The definitionof net investment income

-14-

is conformed to the defi-nition for regular taxpurposes, although deter-mined with regard tominimum tax items ofincome and deduction.There is also a carryoverof investment interestdeduction that is dis-allowed.

o the phase-in rule forinvestment interest forregular tax purposes isdisregarded for AMTpurposes.

vi. standard deduction

h. Circulation - The excess of expensingover 3-year amortization.

i. Research - Experimental expenditures- the excess of expensing over 10-year amortization.

D. Review of Sec. 57

1. Sec. 57 Defines the Items of Tax Pre-ference.

There are six which are set forth below:

a. Percentage Depletion

The excess of percentage depletionover the adjusted basis of the deple-table property.

b. Intangible Drilling Costs

The excess of expensing over 10 yearamortization or cost depletion to theextent in excess of 65 percent of oiland gas income.

c. Incentive Stock Options (ISOs)

The excess of the FMV over the exer-cise price of the stock. The stockacquires a basis of its exerciseprice for regular tax purposes, butits FMV for minimum tax purposes.

-15-

d. Tax-exempt interest

Interest on private activity bondsissued on or after August 8, 1986.Certain refundings of pre-1986 bonds,however, are not treated as apreference.

e. Appreciated property charitablededuction

The amount of untaxed appreciationallowed as a regular tax deduction isa preference. This preference doesnot apply to carryovers of the deduc-tion from charitable contributionsmade prior to August 16, 1986.

f. Accelerated depreciation

For property placed in service before1987, the excess of accelerated overstraight-line depreciation on realproperty and leased personal propertyis a preference.

E. Review of Sec.. 58

1. Sec. 58 Denies Passive Losses.

There is a four-year phase-in periodbeginning in 1987 during which a limitedamount of passive losses may be used tooffset earned income and portfolio incomefor regular tax purposes, but not forminimum tax purposes.

a. Passive farm losses

Net losses from farming activities inwhich the taxpayer does not materi-ally participate are treated as aminimum tax preference.

b. Passive trade or business activitylosses

Net losses from trade or businessactivities in which the taxpayer doesnot materially participate aretreated as a minimum tax preference.These passive losses follow theregular tax rules.

-16-

i. The regular tax rules permit upto $25,000 of losses and creditfrom rental real estate activi-ties in which the taxpayeractively participates to offsetnon-passive income of thetaxpayer, with a phase-outratably between $100,000 and$150,000 of AGI. These lossesand credits should not bepreference items.

c. Passive losses may be carried forwardand treated as a deduction againstAMTI passive gains in succeedingyears.

F. Review of Sec. 59

1. Sec. 59 Provides Definitions and SpecialRules.

a. AMT Foreign Tax Credit

AMT foreign tax credits are allowedto offset a maximum of 90 percent ofTMT liability. Ahy excess may becarried back or forward into otheryears.

b. Election to Amortize Provision

This provision generally allows theindividual taxpayer an election toratably amortize over 10 years expen-ditures which are otherwise currentlydeductible, to avoid the inclusion ofthese expenditures as tax preferenceitems.

G. Review of Sec. 53

1. Sec. 53 Provides a Minimum Tax Credit (MTC)for Deferral Preferences.

a. The MTC allows the amount of minimumtax liability relating to deferralpreferences to be carried forward asa credit against regular tax liabil-ity in future years.

-17-

2. Exclusion Preferences.

Only four items fall outside of thedeferral preference category: (1) percent-age-depletion preference; (2) appreciated-property charitable-contribution prefer-ence; (3) itemized-deductions; and, (4)tax-exempu preferences.

3. Application and Limitation

MTC is applied against the regular taxliability. It may reduce the regular taxliability to an amount equal to the TMT forthat year.

IV. Tax Planning Under The New Law

A. Introduction

Under current law, where planning for the alter-native minimum tax (AMT) is a concern, theclient's tax affairs are arranged to equalize theAMT and regular tax. This is accomplished byproper timing of transactions that generate taxpreference income, e.g., an excercise of an ISO,electing alternative tax methods' such as thestraight-line method of depreciation, or defer-ring non-AMT deductions such as state incometaxes. Planning within this framework assumessufficient flexibility to avoid the AMT. Thespread between the AMT rate and the 50 percentmarginal rate is used to the client's advantagein certain situations. That is, the 30 percentrate spread (assuming a 50 percent rate in thesubsequent year) is viewed as a permanent taxsavings. Thus, accelerating ordinary incomeand/or deferring deductions will result in perma-nent tax savings, discounted by the negative cashflow associated with the one year acceleration oftax. This planning concept will remain importantin 1986 and 1987. However, with the tax bracketsnarrowing and the introduction of the minimum taxcredit (MTC) concept, the permanent tax savingsassociated with the equalization objective willeffectively disappear after 1987.

-18-

B. Three Scenarios

Any 1986 AMT strategy should not be implementedwithout considering both tax and non-tax factors.Below are 3 scenarios and related planning ideas:

1. Regular Tax in 1986 and AMT Position in1987

a. Accelerate deductions in 1986, par-ticularly those which are not allowedfor AMT purposes (e.g., prepayingtaxes or miscellaneous deductions).

b. Defer ordinary income to 1987 (e.g.,deferred compensation arrangements).

c. Accelerate realization of long-termcapital gains, taking advantage ofthe expiring capital gain deduction.

i. On the surface, this could beviewed as primarily a nontaxdecision because the marginalrate is almost the same in bothyears (20 percent in 1986 and21 percent in 1987). However,the disadvantages of waitinguntil 1987 to incur the gain isthat you would increase regulartax at a 28 percent rate whichreduces the spread betweententative minimum tax (TMT) andregular tax, thus reducing the1987 MTC. In effect, thismeans that the gain will ulti-mately result in a 28 percenttax cost when the reduced MTCis used to offset regular taxin a subsequent year. Thus,there is a 7 percent spreadbetween the ultimate 28 percenttax cost, if sold in 1987, andthe sale of 20 percent in 1986,versus the negative cash flowassociated with realizing thecapital gain in 1986.

d. Accelerate the exercise of ISOs, aslong as the bargain element does notput the client into an AMT positionin 1986.

-19-

e. Defer realization of short-termcapital gains and accelerate reali-zation of short-term capital losseswhich can be offset against existingshort-term capital gains or S3,000 ofordinary income.

2. AMT Position in 1986 and Regular Tax in1987

a. Defer until 1987 the payment of itemswhich can be claimed as deductionsunder the new law. Payment in 1986will yield a smaller tax benefit ifdeductible for AMT purposes (e.g.,charitable contributions) or willwaste prospective deductions if notdeductible for AMT purposes (e.g.,state taxes).

b. Accelerate ordinary income into 1986to the extent AMT is equalized withregular tax.

c. Accelerate realization of long-termor short-term capital gains, and thusbe taxed at the lower AMT rate in1986. The 7 percent rate advantagehas to be weighted against the re-duced cash flow in making thedecision.

d. Defer realization of a short-term orlong-term capital loss, if it can beused against either capital gains or$3,000 of ordinary income in 1987.

e. Defer the contemplated exercise of anincentive stock option (ISO) until1987. The deferral would avoid the20 percent AMT on the bargin elementin 1986.

f. If the client has already exercisedan ISO in 1986, consider having himmake a disqualifying disposition ofthe stock in 1986. The dispositionremoves the bargain element from the"tax preference taint" in 1986, andsince AMT is operative, the entiregain on the sale will be taxed at the20 percent rate. This planningmaneuver eliminates the double taxa-tion of the bargain element, that is,

-20-

once as a tax preference in deter-mining AMT in 1986, and then in 1987as part of the presumed gain on thesale, taxed at the 28 percent rate.

i. Under this scenario, an exer-cise in 1986 without a disqual-ifying disposition guarantees adouble tax on the bargainelement, assuming appreciationof the stock.

ii. A disqualifying disposition,however, cannot be made withoutconsidering nontax factors,such as the SEC's "Insider Rule16(b)" and the impact the dis-position would have on manage-ment and other stockholders.

3. AMT Position in Both Years

a. With the AMT rate being 20 percent in1986 and 21 percent in 1987, theacceleration or deferral of income ordeductions has little direct taximpact if the transactions do not putthe client back into a regular taxposition, except with respect to the1987 MTC. Any transaction thateither reduces the 1987 regular taxor increases the 1987 TMT will in-crease the 1987 MTC. Thus, althoughyou may pay more AMT in 1987, some,if not all, of that payment willeventually be refunded via the MTCoffset against regular tax.

i. For example, an exercise of anISO will produce 20 percent AMTin 1986 and 21 percent AMT in1987. However, exercising in1987 will not only defer pay-ment of AMT for 1 year on thetax preference, it also willincrease TMT, which in thiscase will increase the MTC bythe same amount. Thus, al-though AMT will be paid in 1987on the bargain element, an MTCwill be available to offsetregular tax in future years.The same cannot be said of theAMT paid on the bargain elementof the exercised ISO in 1986.

-21-

V. APPENDIX

-22-

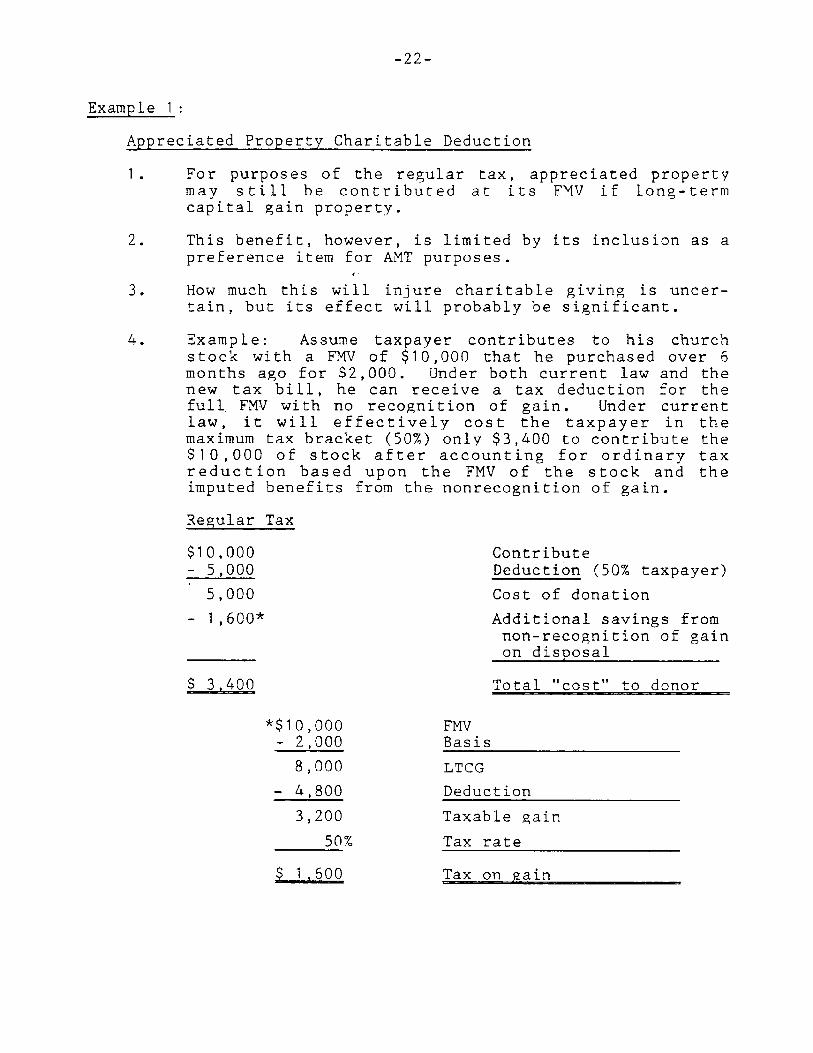

Example I:

Appreciated Property Charitable Deduction

1. For purposes of the regular tax, appreciated propertymay still be contributed at its FMV if long-termcapital gain property.

2. This benefit, however, is limited by its inclusion as apreference item for AMT purposes.

3. How much this will injure charitable giving is uncer-tain, but its effect will probably be significant.

4. Example: Assume taxpayer contributes to his churchstock with a FMV of $10,000 that he purchased over 6months ago for 82,000. Under both current law and thenew tax bill, he can receive a tax deduction for thefull FMV with no recognition of gain. Under currentlaw, it will effectively cost the taxpayer in themaximum tax bracket (50%) only $3,400 to contribute the$10,000 of stock after accounting for ordinary taxreduction based upon the FMV of the stock and theimputed benefits from the nonrecognition of gain.

Regular Tax

$10,000 Contribute- 5,000 Deduction (50% taxpayer)

5,000 Cost of donation

- 1,600* Additional savings fromnon-recognition of gainon disposal

$ 3,400 Total "cost" to donor

*$I0,000 FMV

- 2,000 Basis

8,000 LTCG

- 4,800 Deduction

3,200 Taxable gain

50% Tax rate

$ 1,600 Tax on gain

-23-

There is currently no tax preference for the gift, but,under the new tax bill, both the regular tax and theAMT must be considered:

Regular tax

$10,000- 2,800

7,200

- 2,240*

ContributionDeduction (28% taxpayer)

Cost of donation

Additional savings fromnon-recognition of gainon disposal

Total "cost" to donor

*$10 .000- 2,000

8,000

.28

S2,240

FMVBasis

LTCG (no specialdeduction)

Tax rate

Tax on gain

Thus, it will cost this taxpayer of appreciated stockat least 46% more under the new tax law than under thecurrent system to contribute the same property ($3,400vs. $4,960) and he will incur a tax preference item of$8,000.

-24-

Example 2:

Disqualifying Disposition of ISO

1. Both the current law and the Tax Reform Act of 1986include the bargain element of an exercised ISO as atax preference item for AMT purposes.

2. However, the new tax law treats the bargain elementsubject to the preference as a deferral item. Thebasis of the stock acquired through the exercise of anISO after 1986 is the FMV at the time the ISO is exer-cised.

3. For example, if the taxpayer pays an exercise price ofS8 to purchase stock having a FMV of $16, then thepreference in the year of exercise is equal to $8 andthe stock has a basis of $8 for regular tax purposesand $16 for minimum tax purposes. If, in a subsequentyear, the taxpayer sells the stock for $20, the gainrecognized is $12 for regular tax purposes and $4 forminimum tax purposes.

4. A taxpayer in a regular tax position in 1986 shouldaccelerate the exercise of ISOs, as long as the bargainelement does not put him in a AMT position.

5. If the taxpayer is already in an AMT position, heshould consider making a disqualifying disposition ofthe stock in 1986.

a. A disqualifying disposition will remove thebargain element from the "tax preference taint"in 1986.

b. If the taxpayer is still in an AMT position fromhis other preference items, then the entire gainwill be taxed at the flat AMT rate of 20 percent.

o in the above example, if the stock is soldfor $20, the taxpayer will incur a taxliability of $2.40, i.e. (20-8) x 20% -

$2.40.

c. This may remove him from the AMT position, and hewill be taxed on the gain.

i. If the disqualifying disposition in 1986occurs within 6 months after the exercise ofthe ISO, then the full gain will be taxed atthe regular tax rate.

o in the above example, if the stock issold for $20 and the taxpayer is in a 50percent tax bracket he will incur a taxliability of $6, i.e. (20-8) x 50% = $6

-25-

ii. If the disqualifying disposition in 1986occurs 6 months or more after the exerciseof the ISO, then the bargain element fromthe "tax preference taint" will be taxed asordinary income, but the additional appre-ciation will be taxed as long-term gain,subject to the capital gains deduction.

o thus, the taxpayer will incur a tax lia-bility of $4.80

[($16-8) + .4 ($20-16)] x 50% = $4.80

6. If the taxpayer waits until 1987 to dispose of thestock, he will.be subject to the Tax Reform Act of1986.

a. If he was in an AMT position in 1986, he will besubject to a double tax since he will be taxed onthe bargain element as a tax preference in 1986and again at the time of disposal of the stock in1987.

7. Assuming the taxpayer is in a regular tax position in1987, and he has held the stock for less than 6 monthsafter the exercise of the ISO, then he must pay tax onthe bargain element in 1986 and the gain in 1987. Thefull gain will be taxed at the transitional regularrate of 38.5%. Thus, the total tax to the taxpayer is$6.22.

o 1986: ($16-8) x .2 = $1.601987: ($20-8) x .385 = 4.62

$6.22

a. If the taxpayer has held the stock for more thansix months but within one year after the exerciseof the ISO, then the portion of his gain thatwould, under the current law in 1986, be subjectto the capital gains deduction will now be sub-ject to a tax rate of 28%. Thus, the total taxto the taxpayer is $5.80.

0 1986: $1.601987: ($16-8) x .385 = 3.08

($20-10) x .28 1.12

$5.80

-26-

b. If the taxpayer has held the stock for more thanone year, then the full gain in 1987 will besubject to a rate of 28%. He will incur a taxliability of $4.96.

o 1986: $1.601987: ($20-8) x .28 3.36

$4.96

c. The same result as subsection (b), above, willoccur for a disposition after 1987.

8. Assuming the taxpayer is in an AMT tax position in 1987(or a later year), the exercise of the ISO will produce20% AMT in 1986 and 21% AMT in 1987 (or a later year)when the taxpayer disposes of the stock.

o 1986: $1.601987: ($20-8) x .21 = 2.52

$4.12