The Affordable Care Act - Consumers Unionconsumersunion.org/.../2012/03/The-Affordable-Care.pdfThe...

6

{ The Affordable Care Act What you and your family need to know

Transcript of The Affordable Care Act - Consumers Unionconsumersunion.org/.../2012/03/The-Affordable-Care.pdfThe...

2

{The Affordable Care Act What you and your family need to know

{To download additional copies visit ConsumerReportsHealth.org/freeguides

For a Spanish-language version visit ConsumerReportsenEspanol.org/salud

For other inquiries send an e-mail to [email protected]

PHO

TOG

RA

PHS

BY:

GA

RY

PAR

KER

CO

VER

& P

.2; W

HIT

NEY

CU

RTI

S C

OV

ER &

P.3

; KA

CIE

JEA

N C

OV

ER &

P.4

; CO

UR

TESY

OF

ED M

OR

RIS

P.7

; RO

BER

T G

RA

NT

P.8

In 2010, Congress passed a sweeping health-care reform law known as the Patient Protection and Affordable Care Act (ACA for short), which brought with it many new benefits for consumers. However, many Americans remain confused about this law and are unclear about how it will affect them and their families.

That’s where Consumers Union, the policy and advocacy arm of Consumer Reports, comes in. Since its founding 75 years ago, the organization has been focused on providing consumers with easy-to-understand comparative information so that they can make the best decisions in the marketplace. We know firsthand that the health-care marketplace is one that consumers have had difficulty navigating because of its complexity.

To help consumers figure out how to take advantage of key consumer protections in the ACA, we have put together a series of guides—this being the third about the new health-care law. The protections are aimed at stopping some of the most egregious insurance company practices and making sure Americans have access to quality, more affordable health care.

As always, we appreciate your feedback in our ongoing efforts to provide consumers with the information they need to make the choices they want.

Jim Guest PRESIDENT & CEO Consumer Reports

2

2

“We no longer have to lose sleep worrying about heading for bankruptcy when we hit the lifetime cap on our health insurance policy.”

—Bill, of Santa Clara, Calif., who was until recently quickly approaching a lifetime limit on his policy for treatment of his daughter’s spinal muscular atrophy.

{

▪ Some plans received temporary waivers delaying this requirement until January 1, 2014, and some plans in place before March 23, 2010, may be exempt. Check with your insurer or employer.

▪ Because serious illnesses such as cancer can be financially devastat- ing even with insurance, caps on the total amount of health benefits you can get in one year are being phased out. In 2012, at least $1.25 million in health benefits must be covered; in 2013, $2 million; and in 2014 no limits will be allowed.

Closing Insurance Loopholes Insurance is regulated differently in each of the 50 states, so your rights and protections depend on where you live. New rules now give patients protections that apply to all plans throughout the country, with a few exceptions.

Phasing out yearly limits on benefits

No more lifetime limits▪ Health insurers can no longer place a lifetime limit on certain “essen- tial” benefits, like hospitalization.

▪ Each state determines the full list of essential benefits with guidance from federal officials. See what must be included in every state at: ConsumersUnion.org/health/ essential_benefits.html.

Protection from insurance cancellations▪ Health insurers can no longer arbitrarily cancel your policy if you get sick or if you made an honest mistake on your application.

▪ Insurers can still cancel your policy for fraud or intentional misrep- resentation, such as concealing a recent cancer diagnosis.

New appeal rights▪ If you disagree with a benefit deci- sion by your insurer, you now have a standard, reliable way to dispute it, including guaranteed access to an outside, independent appeal panel if the insurer’s internal process is not satisfactory. If it is an urgent-care issue, decisions must be made within 72 hours.

▪ Not all plans have to follow these new rules. If your insurance plan is “self-insured” or was in place before March 23, 2010, this change may not apply. Check with your insurer or employer.

“Allowing us to keep him on our insurance until 26 came at the perfect time.”

—Lori, of St. Louis, Mo., who can now keep her son who suffers from celiac disease covered while he finishes college.

{3

▪ Starting January 1, 2014, insurers will no longer be able to deny coverage or raise premiums based on your health history. At the same time, people who do not already have insurance but can afford it will be responsible for getting coverage, so their health costs won’t be shifted onto those who do have insurance.

▪ Insurers can no longer deny chil- dren and teens under 19 coverage due to their health status. But until 2014, insurers may still charge higher premiums for sick children and states may limit when they can enroll.

Securing Your Family’s Health Coverage At least 50 million non-elderly Americans have some type of pre-existing health condition, which puts them at risk of losing their job-based coverage if they become unemployed or start their own business. Americans will now have more security under provisions that prohibit insurance denials based on health history.

The end of denials for pre-existing conditions

“The new law gives us peace of mind that we’ll always be able to find health coverage for our daughter.”

—Nydia, of Brentwood, Calif., who has a daughter born with a heart defect.{

Bridging the gap for the sick & uninsured▪ Until 2014, people with pre- existing conditions who have been uninsured for at least six months can get insurance through the Pre-existing Condition Insurance Plan (PCIP).

▪ Premiums vary by age (but not by health status) and are tied to

average rates for healthy individu- als in your state. Premiums have gone down in some states. If you considered a PCIP earlier but couldn’t afford it, check back to see whether coverage is more affordable now.

▪ Find the program in your state at: PCIP.gov.

Help paying for insurance & out-of-pocket costs▪ In 2014, lower- and middle-income families will get help buying pri- vate insurance through tax credits.

▪ For example, a family of four making around $50,000 will get an up-front tax credit to pay for all but $3,385 per year for comprehensive insurance. Lower-income families

will get more, higher earners will get less.

▪ Also, a family of four, for example, earning up to $58,562 annually will get help paying for out-of-pocket costs like co-pays for doctor visits and annual deductibles.

Keeping coverage for older children▪ Young adults up to age 26 can now remain on a parent’s health insur- ance plan regardless of whether they are living at home, married, or a student.

▪ Some young adults who can get coverage through their work may not qualify until 2014. Check with your insurer or employer.

4

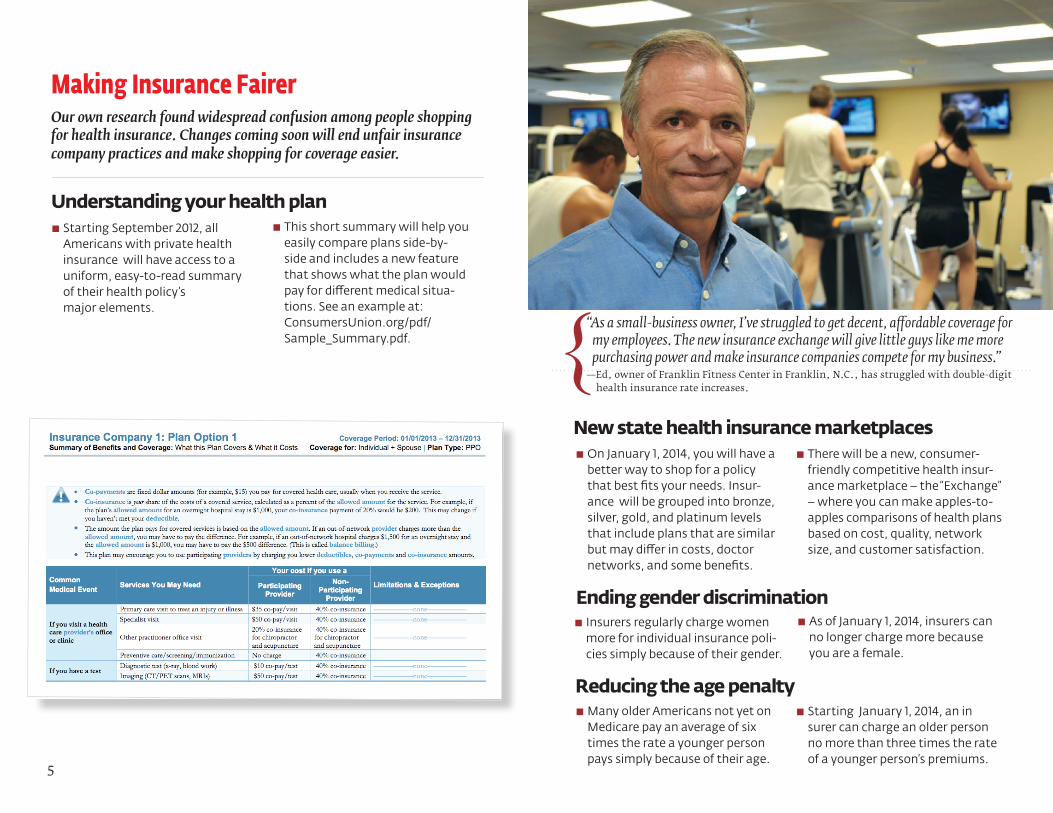

▪ This short summary will help you easily compare plans side-by- side and includes a new feature that shows what the plan would pay for different medical situa- tions. See an example at: ConsumersUnion.org/pdf/ Sample_Summary.pdf.

▪ Starting September 2012, all Americans with private health insurance will have access to a uniform, easy-to-read summary of their health policy’s major elements.

Making Insurance Fairer Our own research found widespread confusion among people shopping for health insurance. Changes coming soon will end unfair insurance company practices and make shopping for coverage easier.

Understanding your health plan

New state health insurance marketplaces▪ On January 1, 2014, you will have a better way to shop for a policy that best fits your needs. Insur- ance will be grouped into bronze, silver, gold, and platinum levels that include plans that are similar but may differ in costs, doctor networks, and some benefits.

▪ There will be a new, consumer- friendly competitive health insur- ance marketplace – the “Exchange” – where you can make apples-to- apples comparisons of health plans based on cost, quality, network size, and customer satisfaction.

Ending gender discrimination▪ Insurers regularly charge women more for individual insurance poli- cies simply because of their gender.

▪ As of January 1, 2014, insurers can no longer charge more because you are a female.

Reducing the age penalty▪ Many older Americans not yet on Medicare pay an average of six times the rate a younger person pays simply because of their age.

▪ Starting January 1, 2014, an in surer can charge an older person no more than three times the rate of a younger person’s premiums.

“As a small-business owner, I’ve struggled to get decent, affordable coverage for my employees. The new insurance exchange will give little guys like me more purchasing power and make insurance companies compete for my business.”

—Ed, owner of Franklin Fitness Center in Franklin, N.C., has struggled with double-digit health insurance rate increases.

{

5

“I lost my insurance in December 2009 when it reached almost $20,000 a year, but I’m now able to get coverage again for a quarter of the price.”

—Gary, of Greens Farms, Conn., who’s now covered by the new Pre-existing Condition Insurance Plan, no longer has to worry about getting continued treatment for his chronic illness.

{

states have chosen to go further, actually rejecting unreasonable increases. ▪ The public now has access to these proposed rate hikes, helping hold insurance companies accountable. View information about insurers in your state at: companyprofiles.healthcare.gov.

▪ Since September 1, 2011, insurers seeking to raise premium rates 10% or more are subject to new scrutiny.

▪ States must now review these proposed rate hikes to determine whether they are unreasonable based on health-care costs and other factors. If a state is unable to make this determination, the federal government will. Some

First Steps in Controlling Rising Costs A critical component of the new health-care law is slowing rising health insurance costs, while giving people real value for their health-care dollars. New requirements are holding insurers accountable for how they spend customers’ premiums, ultimately helping lower rates.

Rate hikes getting a closer look

administrative costs, it will have to give you a rebate or lower premi- ums. Remember, rebates are based on the average for all of a com- pany’s policyholders in one state.

▪ While some insurers have met the standards, those who have failed to do so might owe consumers up to $1.4 billion overall in rebates. Small insurers, new insurers just starting up, and a few states with very high administrative costs may get to temporarily meet a lower standard.

▪ In addition to paying for medical care, insurers spend your premi- ums on administrative costs like advertising, sales commissions, lobbying, and paperwork.

▪ Insurers now can’t spend more than 20% of premiums on their administrative costs for people who purchase policies on their own and small businesses. If you’re covered by a large employer, no more than 15% of premiums can be spent on non-medical care. If your insurer spends too much on

Premiums for medical care, not overhead & excessive profits

▪ Families with insurance can now get certain preventive care without paying deductibles, co-pays, or co-insurance.

▪ Included among a long list of covered services are annual flu shots, routine vaccinations, and preventive cancer screenings. See the full list of covered services at: ConsumersUnion.org/health/ preventive_services.html.

▪ In some plans, to avoid these out- of-pocket costs, you must visit an in-network doctor. And if ad- ditional treatments are performed, such as removing polyps during a colonoscopy, you may incur costs for those procedures. Check with your doctor and insurer first to be sure. ▪ Not all plans have to follow these new rules. If your insurance plan was in place before March 23, 2010, this change may not apply. Check with your insurer or employer.

Investing in prevention

6