The Affordable Care Act ACA Reporting & Cadillac Tax October 7, 2015 Presented by: Maggie Lepore,...

24

The Affordable Care Act ACA Reporting & Cadillac Tax October 7, 2015 Presented by: Maggie Lepore, Senior Account Executive Scott Aston, Vice President

-

Upload

shona-hunt -

Category

Documents

-

view

215 -

download

0

Transcript of The Affordable Care Act ACA Reporting & Cadillac Tax October 7, 2015 Presented by: Maggie Lepore,...

The Affordable Care ActACA Reporting & Cadillac Tax

October 7, 2015

Presented by: Maggie Lepore, Senior Account Executive Scott Aston, Vice President

2Burnham Benefits

PART I - ACA Reporting

1) Which districts must comply?

2) What forms are required, from who, and when are they due?

3) What are the penalties for non-compliance with ACA Reporting?

4) 1094-C IRS Employer Transmittal

5) 1095-C Individual Employee Statement

6) Recommended Next Steps

PART II - Cadillac Tax

7) Overview of the Cadillac Tax and its Implications

8) How to calculate your projected Cadillac Tax

9) Recommended Next Steps

AGENDA

I. ACA Reporting

ACA Reporting

Which Districts Must Comply?

Burnham Benefits

• Self-Insured and Fully-Insured

• Districts/Employers identified as Applicable Large Employers or ALEs must comply with the ACA Reporting Requirements.

• An ALE is an employer with over 50 Full Time Equivalent Employees, determined by employment activity from previous calendar year (For 2015 only, an employer may use any consecutive six month period in 2014, instead of all 12 months).

Sample Over/Under 50 Test Result

4

TEST RESULT: OVER 50 (Must Comply)

CLASSIFICATION TOTALS TEST RESULT TOTALS

Full Time (75%+ or 30+ hours) 32 Full Time (75%+ or 30+ hours) 32

Part Time 18 Full Time Equivalents (FTEs out of 54) 24

Variable Hour 36 OVERALL TOTAL 56

TOTAL W-2 EMPLOYEES 86 Over 50 / Under 50 Status OVER 50

Is your district an ALE member?

ACA Reporting

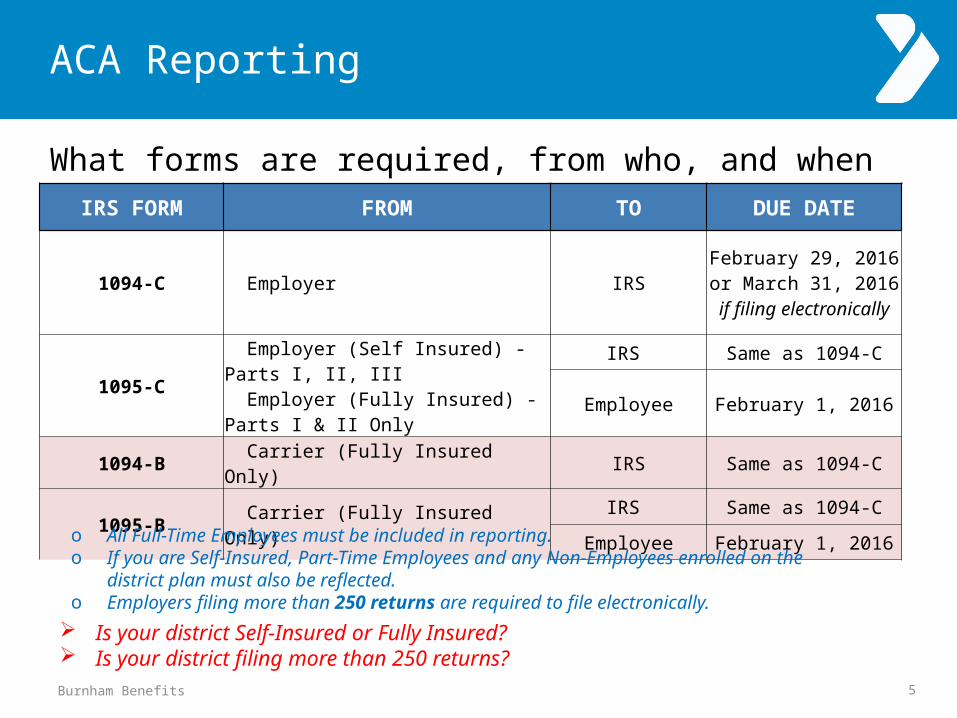

What forms are required, from who, and when are they due?

Burnham Benefits 5

IRS FORM FROM TO DUE DATE

1094-C Employer IRSFebruary 29, 2016

or March 31, 2016 if filing electronically

1095-C Employer (Self Insured) - Parts I, II, III Employer (Fully Insured) - Parts I & II Only

IRS Same as 1094-C

Employee February 1, 2016

1094-B Carrier (Fully Insured Only) IRS Same as 1094-C

1095-B Carrier (Fully Insured Only)IRS Same as 1094-C

Employee February 1, 2016

o All Full-Time Employees must be included in reporting.o If you are Self-Insured, Part-Time Employees and any Non-Employees enrolled on the district plan

must also be reflected.o Employers filing more than 250 returns are required to file electronically. Is your district Self-Insured or Fully Insured? Is your district filing more than 250 returns?

ACA Reporting

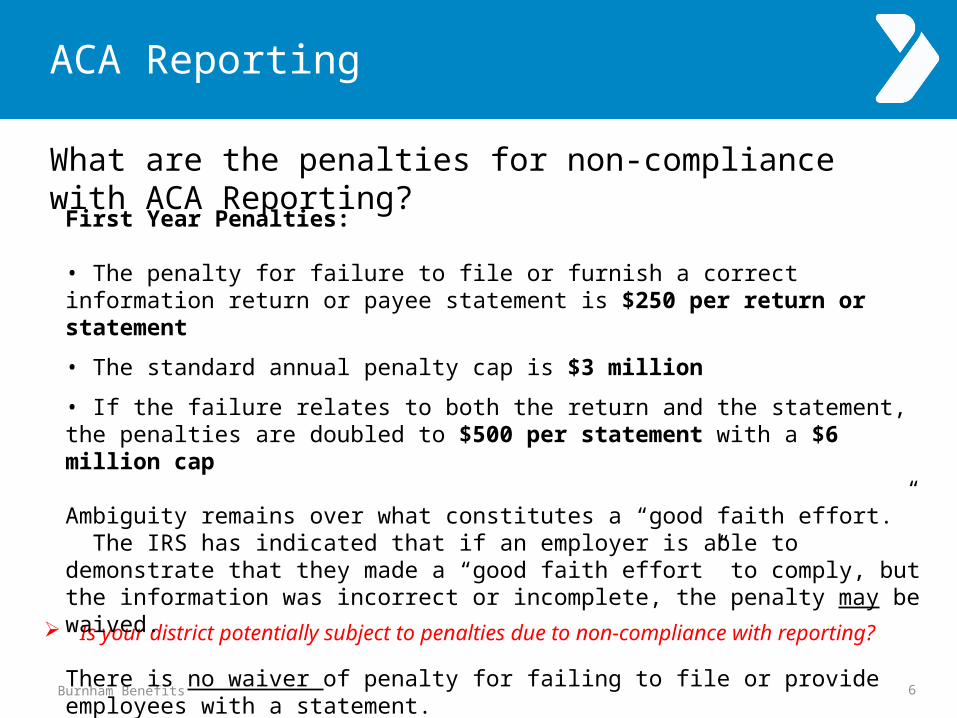

What are the penalties for non-compliance with ACA Reporting?

Burnham Benefits 6

Is your district potentially subject to penalties due to non-compliance with reporting?

First Year Penalties:

• The penalty for failure to file or furnish a correct information return or payee statement is $250 per return or statement

• The standard annual penalty cap is $3 million

• If the failure relates to both the return and the statement, the penalties are doubled to $500 per statement with a $6 million cap

Ambiguity remains over what constitutes a “good faith effort.” The IRS has indicated that if an employer is able to demonstrate that they made a “good faith effort” to comply, but the information was incorrect or incomplete, the penalty may be waived.

There is no waiver of penalty for failing to file or provide employees with a statement.

ACA Reporting

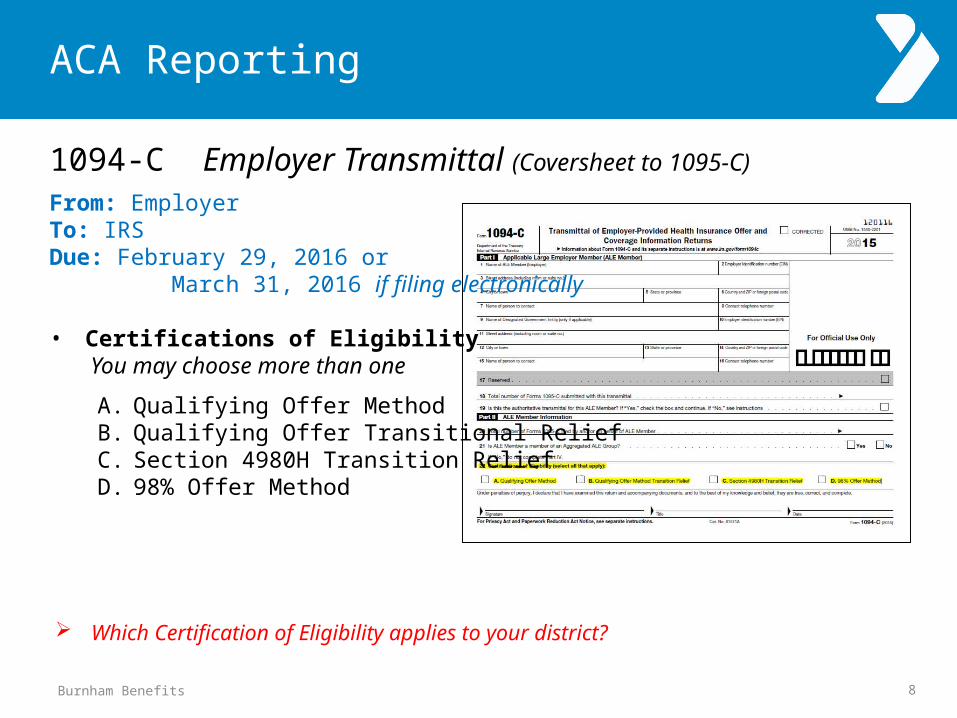

1094-C Employer Transmittal (Coversheet to 1095-C)

Burnham Benefits

From: EmployerTo: IRSDue: February 29, 2016 or March 31, 2016 if filing electronically• Four Parts

• Part I General Employer Information such as Name, Address, EIN• Part II

Certification of Eligibility

• Part III Offer of MEC, Number of FT & PT Employees per month of Calendar Year• Part IV Other ALE Members Listed

7

Who is generating and submitting the 1094-C on behalf of your district?

ACA Reporting

1094-C Employer Transmittal (Coversheet to 1095-C)

Burnham Benefits

From: EmployerTo: IRSDue: February 29, 2016 or March 31, 2016 if filing electronically

• Certifications of Eligibility You may choose more than one

A. Qualifying Offer MethodB. Qualifying Offer Transitional ReliefC. Section 4980H Transition ReliefD. 98% Offer Method

8

Which Certification of Eligibility applies to your district?

ACA Reporting

1094-C Employer Transmittal

Burnham Benefits

Certifications of Eligibility - What do they mean?

A. Qualifying Offer Method 1) Employer offers Minimum Essential Coverage providing a 60% Minimum Actuarial Value to

Full Time employee + spouse + dependent children2) Cost of lowest “single” plan option for employee is less than 9.5% of Federal Poverty Level

2015: $11,770 = $93.18 (12thly) or $111.82 (10thly)

B. Qualifying Offer Transitional Relief1) Same rules apply as “A” above, except made Qualifying Offer in year 2015 to at least 95%

of Full Time employees + spouse + dependent children

9

Which Certification of Eligibility applies to your district?

ACA Reporting

1094-C Employer Transmittal

Burnham Benefits

Certifications of Eligibility - What do they mean?

C. Section 4980H Transition ReliefIf one of the following applies:

1) Employer has less than 100 FTE employees2) Plan has a non-calendar year plan (aka fiscal plan)3) Offered coverage to at least 70% of FT EE’s (not 95% required in 2016)4) Did not offer coverage to dependent children

D. 98% Offer Method1) Employer certifies it has offered coverage to at least 98% of Full Time employees and

dependent(s) children2) Plan meets affordability to 98% of Full Time EE’s (FPL, W2, Rate of Pay)3) All months of the calendar year

10

Which Certification of Eligibility applies to your district?

ACA Reporting

1095-C Individual Employee Statement

Burnham Benefits

From: EmployerTo: Employee Due: February 1, 2016

AND

From: EmployerTo: IRSDue: February 29, 2016 or March 31, 2016 if filing electronically

11

Has your district determined how these statements will be generated and submitted?

ACA Reporting

1095-C Individual Employee Statement – Data Needed

Burnham Benefits 12

What existing systems at your district house this data? Which pieces of data are available and which aren’t?

ITEM # DESCRIPTION

PART I

1 Employee Name2 Social Security number3 Street Address4 City or Town5 State or Province6 Zip7 Name of Employer8 EIN9 Employer Street Address

10 Employer Contact Phone11 Employer City12 Employer State13 Employer Zip

PART II14 Offer of Coverage?15 Employee Share for Lowest Cost Plan (12thly)16 Applicable Section 4980H Safe Harbor used by District

PART III

17 Name of Covered Individuals, SSN, DOB, Months Covered18 Name of Covered Individuals, SSN, DOB, Months Covered19 Name of Covered Individuals, SSN, DOB, Months Covered20 Name of Covered Individuals, SSN, DOB, Months Covered21 Name of Covered Individuals, SSN, DOB, Months Covered22 Name of Covered Individuals, SSN, DOB, Months Covered

Part III provided by carrier and may be left blank on statement, if Fully-Insured.

ACA Reporting

1095-C Individual Employee Statement

Burnham Benefits

• Part II

• Line 14 – Offer of Coverage • Line 15 – Employee Share of Lowest Cost• Line 16 – Applicable Affordability

Safe Harbor

13

Does your district know which codes will apply to each bargaining unit for Lines 14-16?

ACA Reporting

1095-C Individual Employee Statement

Burnham Benefits

• Part II• Line 14 – Offer of Coverage

• 1A - Qualifying Offer made: MEC providing MV with employee contribution for self-only coverage equal to or less than 9.5% mainland single federal poverty line and at least MEC offered to spouse and dependent(s). Two-Tier Bronze Plans would not apply since the plan is not offered to spouse (SISC, CVT).

• 1B - MEC providing MV to EE only Not Applicable to most district plans.

• 1C - MEC providing MV offered to employee, MEC offered to dependent(s) but not spouse Two-Tier Bronze Plans would apply if offered.

• 1E - MEC providing MV offered to employee and MEC offered to spouse and dependent(s) Most plans will fall in this category.

• 1H - No offer of coverage to employee This is a code that should be interpreted by the reporting system

14

ACA Reporting

1095-C Individual Employee Statement

Burnham Benefits

• Part II• Line 15 – Employee Share of Lowest Cost

15

Will the employee share of the lowest cost plan be compliant with affordability?

• Line 16 – Applicable Affordability Safe Harbor

• 2F - Section 4980H affordability Form W-2 safe harbor used

• 2G - Section 4980H affordability federal poverty line safe harbor used 2015: $11,770 = $93.18 (12thly) or $111.82 (10thly)

• 2H - Section 4980H affordability rate of pay safe harbor used

Does your district know which affordability safe harbor will apply to each bargaining unit for Line 16?

ACA Reporting

Recommended Next Steps

Burnham Benefits

Is there a system in place at the district that will generate and appropriately submit the 1094 and 1095 forms?

o IF YES: What information is available/inputted and what is missing? For missing data, who will input? What steps are being made to ensure that inputs/codes are correct, compliant, and

on time?

o IF NOT: What information is available/inputted and what is missing? Work with your Consultants to:

Gain knowledge of your current compliance status Shop the market for available vendors that will suit your districts needs Gain support/guidance during implementation and launch of selected system

16

Act fast! Many vendors such as ADP, Equifax, and HealthE(fx) are no longer taking new clients for the 2015 reporting year.

II. Cadillac Tax

Cadillac Tax

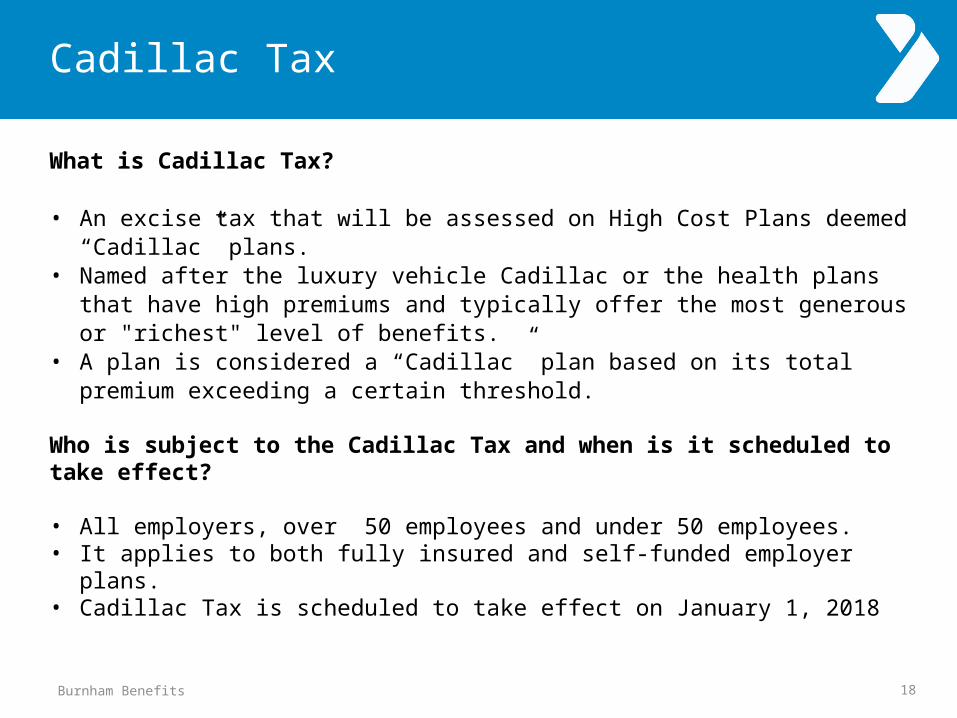

Burnham Benefits

What is Cadillac Tax? • An excise tax that will be assessed on High Cost Plans deemed “Cadillac” plans.• Named after the luxury vehicle Cadillac or the health plans that have high premiums and

typically offer the most generous or "richest" level of benefits.• A plan is considered a “Cadillac” plan based on its total premium exceeding a certain

threshold.

Who is subject to the Cadillac Tax and when is it scheduled to take effect?

• All employers, over 50 employees and under 50 employees.• It applies to both fully insured and self-funded employer plans.• Cadillac Tax is scheduled to take effect on January 1, 2018

18

Cadillac Tax

Burnham Benefits

Why is Cadillac Tax a part of the Affordable Care Act?

(1) Generate Tax Revenue• Increased tax revenue from employers paying the Cadillac tax• Income tax revenue increase as employers move monies from subsidizing health coverage

to increasing salaries, resulting in higher payroll taxes and income taxes.

Congressional Budget Office projects Cadillac Tax will raise $80 billion between 2018 and 2023, $5 billion in 2018 alone.

(2) Reduce the Existence of Cadillac Plans• Assumption that many employers will not offer Cadillac plans in order to avoid tax• Fewer Cadillac plans in the market, helps with over-utilization factors that drive healthcare

costs• Research behind ACA shows that benefit-rich plans insulate members from the high cost of

care, via low copays and deductible, and in-turn results in the overuse of care ultimately driving up medical costs for everyone else.

19

Do all units at your district know what Cadillac Tax is and understand its implications?

Cadillac Tax

Burnham Benefits

History

• Stabilization Act of 1942, authorized and directed the President to freeze prices, wages and salaries in order to aid in the prevention of inflation during WWII.

• New laws at the time allowed employers to offer health benefits tax free in lieu of wages.• Incentivized employers to make health insurance a part of the compensation package they

offer employees.• Employers began offering generous or comprehensive health benefits to compete for

better employees.

Employer-sponsored health insurance being excluded from individuals' taxable income = the federal government currently provides Americans with more than $250 billion each year in tax subsidies.

Cadillac tax is projected to change this balance slightly.

20

Cadillac Tax

Burnham Benefits

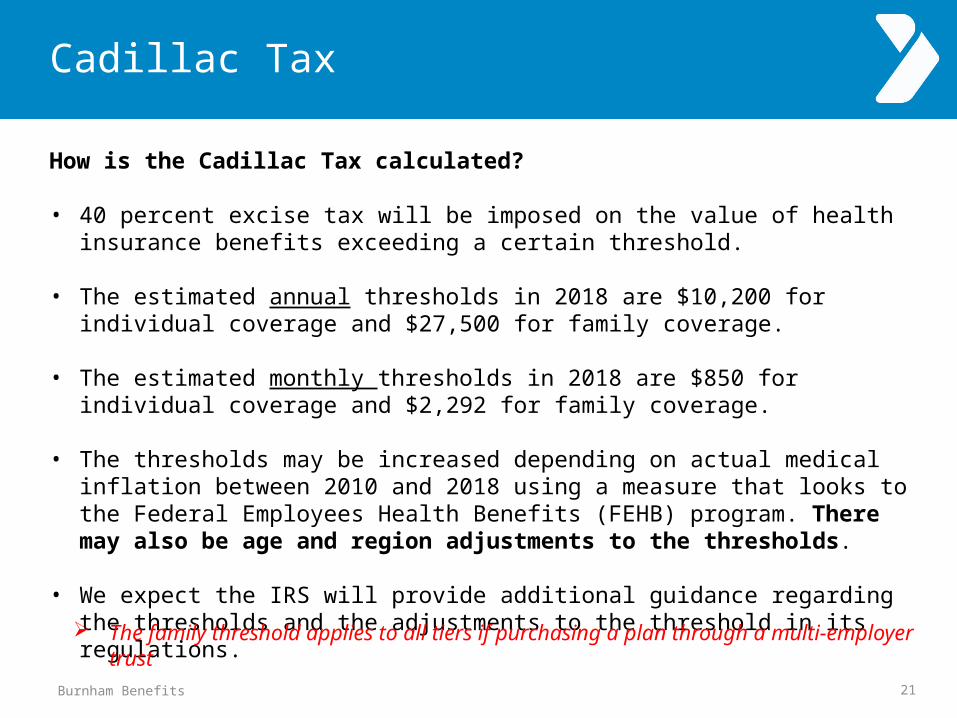

How is the Cadillac Tax calculated?

• 40 percent excise tax will be imposed on the value of health insurance benefits exceeding a certain threshold.

• The estimated annual thresholds in 2018 are $10,200 for individual coverage and $27,500 for family coverage.

• The estimated monthly thresholds in 2018 are $850 for individual coverage and $2,292 for family coverage.

• The thresholds may be increased depending on actual medical inflation between 2010 and 2018 using a measure that looks to the Federal Employees Health Benefits (FEHB) program. There may also be age and region adjustments to the thresholds.

• We expect the IRS will provide additional guidance regarding the thresholds and the adjustments to the threshold in its regulations.

21

The family threshold applies to all tiers if purchasing a plan through a multi-employer trust

Cadillac Tax

Burnham Benefits 22

Has your district calculated a Cadillac Tax projection based on current plans?

Sample School District2013 Cadillac Tax Projection - PLAN 1 (Anthem HMO)

October 1, 2015

2015 2016 2017 2018

Actual EE Annual Premium $17,432.80 $19,088.92 $20,902.37 $22,888.09Excise Tax Threshold EE Only $7,768.87 $8,506.91 $9,315.07 $10,200.00

Difference from Actual ($9,663.93) ($10,582.01) ($11,587.30) ($12,688.09)Pass (YES/NO) NO NO NO NO

Actual EE+SP Annual Premium $17,432.80 $19,088.92 $20,902.37 $22,888.09Excise Tax Threshold EE+SP $20,945.48 $22,935.30 $25,114.16 $27,500.00

Difference from Actual $3,512.68 $3,846.38 $4,211.79 $4,611.91Pass (YES/NO) YES YES YES YES

Actual EE+CH(REN) Annual Premium $17,432.80 $19,088.92 $20,902.37 $22,888.09Excise Tax Threshold EE+CH(REN) $20,945.48 $22,935.30 $25,114.16 $27,500.00

Difference from Actual $3,512.68 $3,846.38 $4,211.79 $4,611.91Pass (YES/NO) YES YES YES YES

Actual Family Annual Premium $17,432.80 $19,088.92 $20,902.37 $22,888.09Excise Tax Threshold Family $20,945.48 $22,935.30 $25,114.16 $27,500.00

Difference from Actual $3,512.68 $3,846.38 $4,211.79 $4,611.91Pass (YES/NO) YES YES YES YES

EE's40% of

Difference Tax182 ($5,075.24) ($923,693.11)

Anthem HMO

Real world example of existing Burnham client.

Calculation by plan design, premium, and current enrollment.

Recommended Next Steps

Burnham Benefits

How should you best handle Cadillac Tax?

o Work with your Consultants to: Calculate your current Cadillac Tax projection Educate all units at the district on the implications of Cadillac Tax Gain an understanding of strategy on how to avoid tax as it stands today

Tiered Rating Explore plans in a Trust Reduce the level of benefits offered Eliminate the plan offerings that leave you subject to the tax

23

This piece of ACA is scheduled to be implemented January 1, 2018. There are 2 remaining renewals before Cadillac Tax takes effect.

Cadillac Tax

Burnham Benefit Insurance Services

Burnham Benefits

Thank you!Maggie Lepore

Senior Account Executive(805) 771-9830 Office(714) 614-2895 Cell

Scott AstonVice President

(949) 252-4597 Office(310) 709-6153 Cell

24

![[OINP2014] Luca Lepore, Cisco "Il programma Cisco networking academy"](https://static.fdocuments.in/doc/165x107/548ba8f0b47959d30c8b6202/oinp2014-luca-lepore-cisco-il-programma-cisco-networking-academy.jpg)