THE ACADEMY H2C STRATEGIC SURVEY – Q4 2016 · PDF fileCurrently, what do you believe ......

8

1 Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com THE ACADEMY H2C STRATEGIC SURVEY – Q4 2016 Monitoring the Rate of Change at Leading Health Systems Melissa Stahl | Research Manager | The Health Management Academy Key Findings Tracking Changes on Strategic Issues for Leading Health Systems A majority (55%) of health systems expect margins to decrease in 2017, leading most (68%) to prioritize cost reduction and control higher in 2017 than in 2016. When acquiring new physician practices, health system executives rank cultural integration of new physicians (80%) and aligning physicians with system quality and performance goals (60%) as significant challenges. Health system executives report a slowing pace of change to value-based payments year over year, with 40% of executives rating the pace of change as slow or very slow in Q4 2016, compared to 26% in Q4 2015. Strategic Priorities Population Health Continues to be a Top Priority United around population health and financial sustainability as top priorities, the largest health systems are preparing to take on more risk through developing innovative insurance products, partnering with payers, expanding their ambulatory network, improving data analytics capabilities, and launching consumer engagement initiatives. Figure 1. What are your health system’s top three priorities? 2015 2016 In 2015, we were concentrating on expanding our insurance, and we were focused on our bottom line margin to improve operations. We were more tactical then; now we are more strategic.” (COO)

Transcript of THE ACADEMY H2C STRATEGIC SURVEY – Q4 2016 · PDF fileCurrently, what do you believe ......

1Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

THE ACADEMY H2C STRATEGIC SURVEY – Q4 2016

Monitoring the Rate of Change at Leading Health SystemsMelissa Stahl | Research Manager | The Health Management Academy

Key FindingsTracking Changes on Strategic Issues for Leading Health Systems

�A majority (55%) of health systems expect margins to decrease in 2017, leading most (68%) to prioritize cost reduction and control higher in 2017 than in 2016.

�When acquiring new physician practices, health system executives rank cultural integration of new physicians (80%) and aligning physicians with system quality and performance goals (60%) as significant challenges.

�Health system executives report a slowing pace of change to value-based payments year over year, with 40% of executives rating the pace of change as slow or very slow in Q4 2016, compared to 26% in Q4 2015.

Strategic PrioritiesPopulation Health Continues to be a Top Priority United around population health and financial sustainability as top priorities, the largest health systems are preparing to take on more risk through developing innovative insurance products, partnering with payers, expanding their ambulatory network, improving data analytics capabilities, and launching consumer engagement initiatives.

Figure 1. What are your health system’s top three priorities?

2015 2016

In 2015, we were concentrating on expanding our insurance, and we were focused on our bottom line margin to improve operations. We were more tactical then; now we are more strategic.” (COO)

2Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

Consolidation OutlookAcquisitions Slow while Focus on Physician Practices Remains

¹ Operational issues include: cost initiatives, IT conversion, and cybersecurity.² Payment model changes include: changes in Medicare & Medicaid reimbursement

and changes in private insurance payments.³ Growth and Consolidation includes: mergers & acquisitions, partnerships, and

selection and execution.⁴ Population health includes value-based care and insurance partner affiliations.

Clinical issues include quality scores and clinical integration.

Operational Issues¹

Payment Model Changes²

Growth and Consolidation³

Government Regulation/Compliance

Economic Risk from Payer Mix

Other(Population Health, Clinical Issues)⁴

%8

16

36

24

8

8

Figure 2. Currently, what do you believe is your health system’s biggest enterprise risk?

Hospital/Rehab/Long-Term Care Facility

Ambulatory Center

Physician Practice/Medical Group

Figure 3. Did your health system acquire any of the following over Q3 2016?

0%

10%

20%

30%

40%

50%

60%

70%

80%90%

100%

Q1 2016 Q2 2016 Q3 2016Q4 2015Q3 2015

24%

44%

24% 24%

20% 16%

60%

16% 8% 10% 20% 15%

60% 52%

35%

Perc

ent o

f Hea

lth S

yste

ms

Part

icip

atin

g in

an

Acqu

isitio

nFrom improving cost-effectiveness to maintaining functionality and security of Information Technology (IT) systems, operational issues was ranked as the top enterprise risk by 36% of health system executives (Figure 2).

“The top risk is IT…security, functioning of the system, making sure we keep up-to-date. Everything is IT-related. It is very important to our business.” (CFO)

With operational issues being top of mind, 80% of health systems expect to increase their spend on technology during 2016. Executives also expect to allocate more dollars to population health infrastructure and health plan development (32%), as well as physician recruitment and medical group expansion (24%).

Enterprise Risk36% of Executives Rank Operational Issues as Top Concern

Although consolidation in the healthcare industry continues, the pace slowed year over year, with deal volume decreasing 1.4% and deal value decreasing 59.6% in 2016 compared to 2015. (1) Consistent with this trend, responding health systems have slowed their M&A activity, with over half (55%) of health systems not acquiring anything during Q3 2016–up from 44% in Q2 2016.

Those that have participated in an acquisition are still largely focused on purchasing individual group

practice physician offices, with 35% reporting the acquisition of a physician practice or medical group during the third quarter of 2016 (Figure 3).

Health systems expect M&A activity to pick up slightly in the future, with 85% of health systems planning to acquire a hospital (25%), ambulatory center (40%), physician practice/medical group (70%), surgical center, health plan, or mail order pharmacy over Q4 2016–Q1 2017.

3Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

Strategic PartnershipsProvider Interest in Partnerships Increases

Physician AlignmentCultural Integration of Newly Acquired Physicians is a Top ChallengeAll responding health systems expect growth in their number of employed physicians, particularly primary care physicians, during 2016 and 2017 with 40% and 44% of health systems expecting large increases over 2016 and 2017, respectively (Figure 5).

“We are recruiting nurse practitioners and physician assistants that support our retail clinic strategy. We do a lot of recruitment for primary care and specialists that match the key clinical services in each of our markets. It is driven by overall market needs and strategies.” (CSO)

However, as Leading Health Systems continue to acquire new physician practices, many encounter challenges around the cultural integration of newly acquired physicians (80%), as well as aligning physicians with system quality and performance goals (60%) (Figure 6). Health system executives also

As health systems reduce their number of acquisitions, increasingly health systems are focused on developing strategic partnerships around non-core business areas (e.g., pharmacy, telehealth, revenue cycle, IT) or forming joint ventures or joint operating agreements with other

provider organizations. Health system executives expect to continue this trend, with approximately two-thirds (65%) of responding health systems planning to form a strategic partnership in Q4 2016–Q1 2017, up from 50% in Q2–Q3 2016 (Figures 4A, 4B).

Figure 5. If you have an employed medical group, do you expect growth in the number of employed physicians during 2016 and 2017?

0%

20%

40%

60%

80%

100%

20172016

44% 40%

56% 60%

Perc

ent o

f Hea

lth S

yste

ms

Yes, large increaseYes, small increaseNo

Figure 4A. Over the last 6 months (Q2–Q3 2016), did your health system form a strategic partnership? If yes, with whom?

Provider

Both

IndustryYes

No

% %50 50

5

10

35

Figure 4B. Do you plan to form a strategic partnership in the next 6 months (Q4 2016–Q1 2017)? If yes, with whom?

Provider

Both

IndustryYes

No

% %6535

5

3030

Two unlike organizations within the same industry coming together and focusing on a common customer.” (CEO)

rank IT/EMR integration, compensation transition, and practice management integration as significant challenges.

4Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

Quality and CostIncreased Pressure on Margins Puts Higher Priority on Cost ReductionA majority (55%) of health systems expect margins to decrease in 2017, with many citing changing payer models, payer mix degradation, and reduced hospital rates as margin pressures (Figure 7).

“We are expecting tighter margins because reimbursement is increasing at a slower pace than inflation—we are having to look more at our underlying cost structure.” (CMO)

This increased financial pressure has most (68%) health systems prioritizing cost reduction and control higher in 2017 than in 2016 (Figure 8). Those that are not prioritizing cost reduction higher cite successful ongoing cost reduction efforts.

“I wouldn’t say [cost reduction] is higher—would just say it’s harder. The easy stuff has been done.” (CMO)

In order to successfully assimilate newly acquired physician practices, most health systems work to integrate physicians into the EHR (85%), redesign physician compensation packages in line with system practices and benefits (80%), undergo rebranding (e.g., lab coats, signage, IDs, etc.) (75%), and utilize physician onboarding programs (75%). Health systems also work to involve physicians in decision making through physician councils or dyad leadership structures.

% Increase

Decrease

Stay the Same

30

15

55

% Yes

No

No Change

68

21

11

Figure 6. What are the primary challenges your health system has encountered after acquiring a new physician practice?

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Cultural integration of newly acquired physician practice

Aligning physicians with health system quality and performance goals

Balancing health system oversight with physician autonomy

Increased pressure on health system finance

80%

60%

55%

55%

Percent of Health Systems

Figure 7. Do you expect your operating margin to increase, decrease, or stay the same in 2017?

Figure 8. Will/does your 2017 strategic plan refresh prioritize cost reduction/control higher than 2016’s?

We want to make sure we engage a physician from each practice into the leadership structure. When we acquire a group we identify one physician that will represent that group in a series of councils going forward.” (COO)

5Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

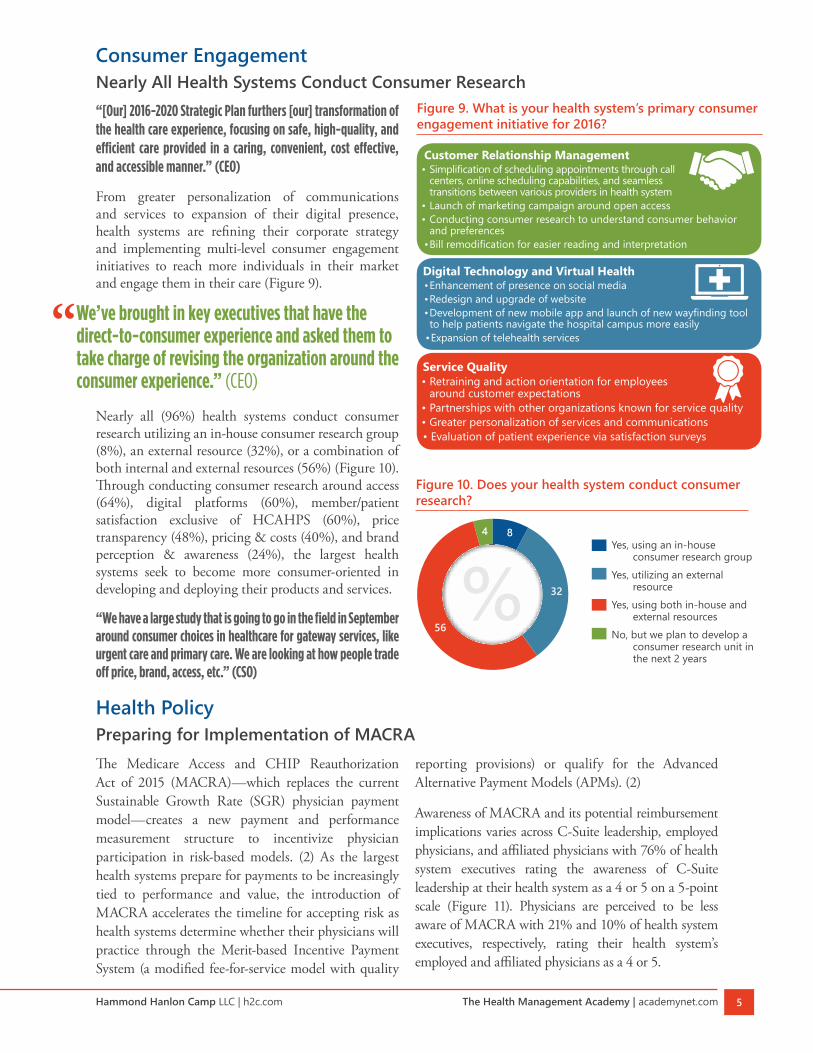

Consumer EngagementNearly All Health Systems Conduct Consumer Research“[Our] 2016-2020 Strategic Plan furthers [our] transformation of the health care experience, focusing on safe, high-quality, and efficient care provided in a caring, convenient, cost effective, and accessible manner.” (CEO)

From greater personalization of communications and services to expansion of their digital presence, health systems are refining their corporate strategy and implementing multi-level consumer engagement initiatives to reach more individuals in their market and engage them in their care (Figure 9).

Nearly all (96%) health systems conduct consumer research utilizing an in-house consumer research group (8%), an external resource (32%), or a combination of both internal and external resources (56%) (Figure 10). Through conducting consumer research around access (64%), digital platforms (60%), member/patient satisfaction exclusive of HCAHPS (60%), price transparency (48%), pricing & costs (40%), and brand perception & awareness (24%), the largest health systems seek to become more consumer-oriented in developing and deploying their products and services.

“We have a large study that is going to go in the field in September around consumer choices in healthcare for gateway services, like urgent care and primary care. We are looking at how people trade off price, brand, access, etc.” (CSO)

Figure 10. Does your health system conduct consumer research?

Yes, using an in-house consumer research group

Yes, utilizing an external resource

Yes, using both in-house and external resources

No, but we plan to develop a consumer research unit in the next 2 years

%4

32

56

8

Figure 9. What is your health system’s primary consumer engagement initiative for 2016?

Customer Relationship Management• Simplification of scheduling appointments through call

centers, online scheduling capabilities, and seamless transitions between various providers in health system

• Launch of marketing campaign around open access• Conducting consumer research to understand consumer behavior

and preferences• Bill remodification for easier reading and interpretation

Digital Technology and Virtual Health• Enhancement of presence on social media• Redesign and upgrade of website• Development of new mobile app and launch of new wayfinding tool to help patients navigate the hospital campus more easily

• Expansion of telehealth services

Service Quality• Retraining and action orientation for employees

around customer expectations• Partnerships with other organizations known for service quality• Greater personalization of services and communications• Evaluation of patient experience via satisfaction surveys

We’ve brought in key executives that have the direct-to-consumer experience and asked them to take charge of revising the organization around the consumer experience.” (CEO)

Health PolicyPreparing for Implementation of MACRAThe Medicare Access and CHIP Reauthorization Act of 2015 (MACRA)—which replaces the current Sustainable Growth Rate (SGR) physician payment model—creates a new payment and performance measurement structure to incentivize physician participation in risk-based models. (2) As the largest health systems prepare for payments to be increasingly tied to performance and value, the introduction of MACRA accelerates the timeline for accepting risk as health systems determine whether their physicians will practice through the Merit-based Incentive Payment System (a modified fee-for-service model with quality

reporting provisions) or qualify for the Advanced Alternative Payment Models (APMs). (2)

Awareness of MACRA and its potential reimbursement implications varies across C-Suite leadership, employed physicians, and affiliated physicians with 76% of health system executives rating the awareness of C-Suite leadership at their health system as a 4 or 5 on a 5-point scale (Figure 11). Physicians are perceived to be less aware of MACRA with 21% and 10% of health system executives, respectively, rating their health system’s employed and affiliated physicians as a 4 or 5.

6Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

Figure 11. On a scale of 1–5, how aware of MACRA and its potential reimbursement implications is your health system’s:

Perc

ent o

f Hea

lth S

yste

ms

0%10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Employed Physicians

Affiliated Physicians

C-Suite Leadership

5 (Highly aware of MACRA and its implications)

4

3

2

1 (Not familiar with MACRA)

8% 17%

63%

13%

76%

27%

72%

45%

18% 5% 5% 10%

8%

38%

42%

13%

8%

21%

29%

1 (Not familiar with MACRA) 4

2 5 (Highly aware of MACRA and its implications) 3

Note: Data collected April, 2016.

Figure 12. What percent of your health system’s employed and affiliated physicians do you expect to practice through the Merit-Based Incentive Payment System (“MIPS”) track versus the Alternative Payment Model (“APM”) track?

Note: Data collected April, 2016.

0%10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AffiliatedEmployed

69% 47%

31% 53%

Perc

ent o

f Phy

sicia

ns

APM

MIPS

A major challenge for health systems is determining whether clinicians will practice in MIPS or qualify for an exclusion and the incentive payments associated with practicing through Advanced APMs.

As seen in Figure 12, executives anticipate that more than one-half (53%) of their employed physicians will participate in Advanced APMs, while 31% of affiliated physicians are expected to practice through Advanced APMs. However,

36% of executives report that they are unsure in which track their employed physicians will participate.

Although most (80%) responding health systems participate in the 340B Drug Pricing Program and predict potential changes in the program will result in a small (62%) or large (15%) decrease on their profit margin, health systems are primarily focused on general cost reduction efforts to help alleviate overall financial pressure.

The Evolving Payment ModelPace of Change Towards Value-Based Payments SlowsFee-for-service continues to be the dominant reimbursement method for the largest health systems with fee-for-service payments comprising 82% of health system revenue and value-based payments at 18% (Figure 13).

Figure 14 illustrates the slowing of the pace of change towards value-based reimbursement year over year, with 40% of executives rating the pace of change as slow or very slow in Q4 2016, compared to 26% in Q4 2015. No health systems reported moving very quickly to value-based payment in Q4 2016, down from 17% in Q4 2015.

Most health systems (72%) cite payer negotiations as a challenge they have encountered in the movement to value-based reimbursement.

“We are continuing to refine our care management structure and approach and enhance the infrastructure that makes it easier to coordinate care. We are still struggling with adversarial payer negotiations and the inability of payers to give us timely data.” (CMO)

Despite these challenges, health systems are continuing to take on risk with 80% planning to expand their participation in bundling (48%), ACOs (28%), partial or full capitation (32%), Medicare Advantage (44%), and/

Value-based payments is a narrow part of our overall reimbursement profile. We are dipping our toe in the water but on a small scale.” (CFO)

7Hammond Hanlon Camp LLC | h2c.com The Health Management Academy | academynet.com

or another risk arrangement over the next six months. Among responding health systems, 56% have a provider-owned health plan with some co-owning it with an

Figure 14. On a scale of 1-5, how would you describe the pace of change towards value-based payments at your health system?

1 (Very Slowly) 3 4

2 5 (Very Quickly)

0%

20%

40%

60%

80%

100%

Q4 2016Q4 2015

20%

20%

45%

15% 0%

4%

22%

48%

9%

17% 1 (Very Slowly)

2

3

4

5 (Very Quickly)

Perc

ent o

f Hea

lth S

yste

ms Figure 15. Does your health system participate in

Medicare Advantage?

Yes, as part of our health planYes, in an arrangement with a

health insurerYes, both as part of our

health plan and in an arrangement with a health insurer

No, and we do not plan to within the next 12 months

%17

54

12

17

Note: Data collected April, 2016.

Figure 13. Currently, what percent of your care delivery is fee-for-service and value-based? What do you expect your care delivery to look like in 12 months?

0%

10%

20%

30%

40%

50%

60%

70%

80%90%

100%

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016Q1 2015Q4 2014

21%

15%

18%

15%

85%

79%

85%

82%

18%

15% 15%

85% 85%

82% 82%

82%

81%

18%

18%

19% 21%

16%

84%

79%

19%

16%

84%

81%

23%

18%

82%

77%

20%

18%

82%

80% Current Fee-for-Services

Anticipated Fee-for-Service in 12 months

Current Value-Based Care

Anticipated Value-Based Care in 12 months

Note: Participating health systems may vary by quarter. Fee-for-service is comprised of self-pay, Medicare DRGs, Medicaid, and commercial payments. Value-based payments include: shared savings ACO, Medicare Advantage, Medicare Shared Savings Program (MSSP), bundled payments, partial or full capitation products, Medical Home contracts, and commercial shared savings.

Perc

ent o

f Pat

ient

Ser

vice

Rev

enue

insurer, such as Anthem or Blue Cross. Three health systems reported that they are considering establishing a provider-owned health plan in the next 3 years. Currently, 83% of reporting health systems participate in Medicare Advantage with most participating in a risk arrangement with a health insurer (Figure 15).

Profile of Participating Health SystemsAverage Net Patient Revenue

$4.9 BILLIONOwn or operate 314 hospitals with 63,892 beds

75%Single-State

Systems

25%Multi-State

Systems

45%Have a Provider-

Owned Health Plan

Representative of the various regions of the U.S.

45%40%

15%

THE HEALTH MANAGEMENT ACADEMY

515 Wythe Street Alexandria, VA 22314

academynet.com

HAMMOND HANLON CAMP LLC

Atlanta | Chicago | San Diego | New York

www.h2c.com

MethodologyIn October 2016, The Academy conducted the ninth round of its quarterly strategic survey among 20 senior health system executives, including: CEOs, COOs, CFOs, CMOs, CNOs, and CSOs. The survey for the interview consisted of: (1) a tracking section that provides insight into trends around primary strategic areas; (2) a special topic area that allows for an in-depth look into a timely, developing issue. Innovation, consumer engagement, ambulatory and real estate strategies, physician alignment, bundling, data analytics, telehealth, and pharmacy strategies were topics of previous surveys.

The Health Management Academy, “The Academy” The Academy is a leading research and analysis company serving the largest 100 health systems that own or operate 1,800 hospitals. The Academy provides services to the C-suite, including research, analytics, health policy, consumer research, fellowship programs, and collaboratives.

Hammond Hanlon Camp LLC, “H2C”Hammond Hanlon Camp LLC (“H2C”) is an independent strategic advisory and investment banking firm committed to providing superior advice as a trusted advisor to healthcare organizations throughout the United States. The company traces its heritage back almost 30 years through its predecessor organizations, including Shattuck Hammond Partners.

References1. Donkar N. US Health Services Deals Insights Year-end 2016. PwC. http://pwchealth.com/cgi-local/hregister.cgi/reg/

pwc-health-services-deals-insights-q4-2016.pdf.

2. Centers for Medicare & Medicaid Services. Quality Payment Program: Delivery System Reform, Medicare Payment Reform, & MACRA. Retrieved from: https://www.cms.gov/Medicare/Quality-Initiatives-Patient-Assessment-Instruments/Value-Based- Programs/MACRA-MIPS-and-APMs/MACRA-MIPS-and-APMs.html. Accessed: 9 Aug 2016.

*Significant contributions to this report were made by Melissa Braganza, MPH.

* Includes all health systems participating in 2016.

Participating Health Systems