The ABI’s Response to: Life Insurance Companies: A New ... · ensure that the shareholder profit...

55

1 The ABI’s Response to: Life Insurance Companies: A New Corporate Tax Regime 1 Introduction 1.1 Approach to our response This document contains a section for each chapter of the above Consultation Document. The key points are extracted and summarised at the beginning of each section. Please note that the numbering system is similar to but does not correspond precisely with the numbering system in the Consultation Document. A number of points and themes are particularly important and pervasive and these are summarised in this opening section to our response. But running through our response is a force towards, where there is a choice, aligning the life tax regime with the regime applicable to companies more generally in the UK, and aligning towards the accounts. We would like to record our continued appreciation of the positive engagement by the HM Treasury (HMT) and HM Revenue and Customs (HMRC) teams and we look forward to working together in the same vein in the coming months. 1.2 Summary of key issues and themes (i) Transition. The potential size of the transitional adjustments on the move from the regulatory to the accounts basis makes this a key issue for companies, and we very much welcome the proposal to spread “residual adjustments” over 10 years. However companies are also very conscious of the anticipated accounting changes, and do consider that if such changes do take effect in 2013 and/or in early subsequent periods the resulting transitional adjustments should be spread over the remainder of the period to 2022 (when the 10 year spread on the tax transition will cease). Should the accounting changes take effect only in later accounting periods, the industry would wish to discuss more targeted transitional measures. (ii) Apportionments. It is a very significant change to move from a formula based approach to a business-based approach, and it is even more significant (in a positive way) that industry and HMRC are aligned in recognising this as the way forward. Against the backdrop of such a change, we believe that it is important that there is a flexible and enabling process for companies to agree the commercial allocation basis with their Customer Relationship Manager (CRM) as the new regime commences. We also believe that it is consistent with the business-based approach that the regime should respect how with-profit funds operate, and in particular the allocation of the Fund for Future Appropriations (FFA) or Unallocated Divisible Surplus (UDS) should (where the with-profit fund works in a conventional manner)

Transcript of The ABI’s Response to: Life Insurance Companies: A New ... · ensure that the shareholder profit...

1

The ABI’s Response to: Life Insurance Companies: A New Corporate

Tax Regime

1 Introduction

1.1 Approach to our response

This document contains a section for each chapter of the above Consultation

Document. The key points are extracted and summarised at the beginning of each

section. Please note that the numbering system is similar to but does not

correspond precisely with the numbering system in the Consultation Document.

A number of points and themes are particularly important and pervasive and these

are summarised in this opening section to our response. But running through our

response is a force towards, where there is a choice, aligning the life tax regime with

the regime applicable to companies more generally in the UK, and aligning towards

the accounts.

We would like to record our continued appreciation of the positive engagement by

the HM Treasury (HMT) and HM Revenue and Customs (HMRC) teams and we look

forward to working together in the same vein in the coming months.

1.2 Summary of key issues and themes

(i) Transition. The potential size of the transitional adjustments on the move

from the regulatory to the accounts basis makes this a key issue for

companies, and we very much welcome the proposal to spread “residual

adjustments” over 10 years. However companies are also very conscious of

the anticipated accounting changes, and do consider that if such changes do

take effect in 2013 and/or in early subsequent periods the resulting

transitional adjustments should be spread over the remainder of the period to

2022 (when the 10 year spread on the tax transition will cease). Should the

accounting changes take effect only in later accounting periods, the industry

would wish to discuss more targeted transitional measures.

(ii) Apportionments. It is a very significant change to move from a formula

based approach to a business-based approach, and it is even more

significant (in a positive way) that industry and HMRC are aligned in

recognising this as the way forward. Against the backdrop of such a change,

we believe that it is important that there is a flexible and enabling process for

companies to agree the commercial allocation basis with their Customer

Relationship Manager (CRM) as the new regime commences. We also

believe that it is consistent with the business-based approach that the regime

should respect how with-profit funds operate, and in particular the allocation

of the Fund for Future Appropriations (FFA) or Unallocated Divisible Surplus

(UDS) should (where the with-profit fund works in a conventional manner)

2

ensure that the shareholder profit from conventional with-profit business is

split in proportion to the split of declared bonuses.

(iii) Policyholder tax deduction. Industry and HMRC are aligned on the

deductibility of I minus E policyholder tax in determining basic life assurance

and general annuity business (BLAGAB) trade profit based on the tax paid

on the policyholder share of I minus E profit. However, it is critical in the

industry‟s view that BLAGAB deferred tax provided at the 20% rate is

allowable in the computations, permitting the actual split of shareholder and

policyholder tax to be determined in an actual annual computation on real tax

principles. This is the most compelling way of reconciling the move to

accounts-based taxation and the determination of policyholder tax on a

computational basis (as opposed to an economic basis).

(iv) The use of brought forward losses. The industry believes that historic

Gross Roll-Up Business (GRB), Pension Business (PB) and Permanent

Health Insurance (PHI) losses should be set against profits of the new

category (all existing GRB and PB, all existing PHI and new Protection,

collectively called GRB - PHI) without restriction. This is the most compelling

from a simplicity perspective and places life assurance on a par with other

financial sector industries where all similarly associated activities are taxed

as one trade. We believe that the value for the Exchequer in maintaining

existing streaming or introducing new streaming rules now would not be

significant. In relation to brought forward life assurance trade losses, we

believe that most companies will be able to determine the BLAGAB element

on a factual basis, and it is consistent with the new regime to require this

determination as a starting point.

(v) I minus E volatility. The critical point at the heart of the industry‟s concern

is the fact that the gilt and bond market can spike at 31 December and

reverse on 1 January but the two cannot offset, and this can cause

permanent increases in tax payable. We simply ask for an effective 1-year

carry-back (unlike the current limited carry-back) to eliminate such short-term

timing differences. This is consistent with the position of other companies in

the UK and ought not to cost the Exchequer as against any modelled basis,

on the basis that such short-term volatility is unlikely to be priced into any

models, as it is not priced into those of insurers.

(vi) Transfers of business. Companies undertaking transfers of long-term

insurance business need lead time and certainty. We agree that it is

sensible to adopt different approaches to connected and unconnected party

transfers, and to legislate for the treatment of the Value of In-Force Business

(VIF) on transfer where there is uncertainty today. We would advise that we

monitor emerging accounting rules and retain flexibility as such rules

become clear.

3

Chapter 2 Trade Profits

2.1 Starting Point

Key points:

As is true for companies in other industry sectors, there could be differences

between companies applying UK Generally Accepted Accounting Practice (“GAAP”)

and those applying International Financial Reporting Standards (“IFRS”), since the

measure of profits will be different between those two bases.

Under IAS12, all corporate tax (including current and deferred tax items calculated at

the policyholder rate) should be treated as income tax and it should be included in

the income tax line.

Under UK GAAP, some items may be dealt with as a component of the technical

provisions rather than deferred tax, for example, that on unrealised BLAGAB

investment gains. For such items, it would still be appropriate to follow the accounts

treatment.

UK branches of overseas life assurers should not be subject to rules that require

them to produce accounting figures, solely for the purposes of their UK tax

computations

UK branches should compute their taxable profits, for both general and life

assurance, in either GAAP used by the entity or under IFRS, if adopted at either

entity or group level.

2.1.1 Are any practical difficulties anticipated in identifying the trade profits

starting point? If so, how could they be addressed?

2.1.1.1 Both UK GAAP and IFRS financial statements will disclose a profit for the

year before tax.

2.1.1.2 In the case of UK GAAP this figure will appear in the non-technical account

and will be net of the excess of the tax charge in the long-term business technical

account over that in the non-technical account relating to the transfer from the long-

term business technical account. Because one, or both, of these figures may be

negative, care will be needed in adjusting the profit before tax in the non-technical

account to provide a profit before all corporation tax deductions.

2.1.1.3 A further aspect not yet addressed, is the potential application of the tax regime for property income at part 4 of the Corporation Tax Act (“CTA”) 2009 to the real estate investments of companies writing long-term business. Such investments are often significant in their own right as well as forming a material segment of the

4

investment activities of the companies concerned. Historically, the regime for property income has only been applied in full to assets outside the long-term fund. For assets of the long-term fund it is used to determine profit for I minus E, which should not be affected by the change to the new regime, but not life assurance trade profits.

2.1.2 Could the approach set out above give rise to material inconsistencies

between companies?

2.1.2.1 There could be differences between companies applying UK GAAP and

those applying IFRS, since the measure of profits will be different between those

two bases. The same is true for companies in other industry sectors – namely that

UK GAAP and IFRS profits measures may be different.

2.1.3 What is the nature and extent of income, gains, expenses and losses

included in statements in the accounts other than the income statement or

profit and loss account?

2.1.3.1 For IFRS these are:

Available for sale gains and losses less recycling on realisation less “shadow

adjustments” under IFRS 4 paragraph 30.

Gains and losses on a hedge of a net investment.

Gains and losses on cash flow hedges less reclassification to profit or loss.

Exchange differences on translation of foreign operations.

Actuarial gains and losses on defined benefit pension schemes.

Restatements arising from changes in accounting policy or corrections of

fundamental errors.

Interest on hybrid debt treated as dividends for accounting purposes.

Income tax effect of all the above.

2.1.3.2 For UK GAAP these are:

Unrealised surplus on revaluation of investment properties.

Currency translation difference on foreign currency net investments.

Currency translation difference on related borrowings [this and prior item are

equivalent to the IFRS net investment hedge].

Actuarial gains and losses on defined benefit pension schemes.

5

Restatements arising from changes in accounting policy or corrections of

fundamental errors.

Interest on hybrid debt treated as dividends for accounting purposes.

Tax effects of all the above.

2.1.4 What is the nature and extent of any tax elements not included in the tax

lines in the accounts?

2.1.4.1 Under IAS12, all corporate tax (including current and deferred tax items

calculated at the policyholder rate) should be treated as income tax and it should be

included in the income tax line. (Other taxes that do not meet the income tax

definition under IAS 12 will be classified as expenses and not within the income tax

line. Examples of these would be stamp duty or irrecoverable VAT. This is, of

course, the same for insurers as for all other companies.)

2.1.4.2 Under UK GAAP, some items may be dealt with as a component of the

technical provisions rather than deferred tax, for example, that on unrealised

BLAGAB investment gains. Paragraphs 188, 189, 197 and 209 of the ABI SORP,

permit such treatments. For such items, it would still be appropriate to follow the

accounts treatment. Thus there would be no adjustment in respect of such items,

neither would there be any separate deduction for them as policyholder deferred tax.

2.1.5 Are there any specific considerations in relation to UK branches of

overseas companies if, for example, these companies do not prepare

accounts under either UK GAAP or IFRS?

2.1.5.1 There are some specific points to consider in the case of UK branches of

overseas insurers.

Current Taxation Basis for UK Branches of Life Assurance companies

2.1.5.2 UK branches that currently prepare FSA returns will need to determine the

appropriate basis for preparing their tax computations, once those FSA returns

cease to exist. Under current law, applicable to non-life assurers, this will require

them to prepare their tax computations using UK GAAP, unless the entity of which

they form part, prepares its financial statements using IFRS, in which case these

profits can form the basis of their UK tax computation.

2.1.5.3 Certain UK branches of life assurers are not obliged to file a UK FSA Return.

These insurers form part of entities that are regulated elsewhere in the European

Union. Several of these life assurers are part of composite UK branch enterprises,

who currently perform a separate computation of their general insurance business.

2.1.5.4 If the parent entity of which the branch forms part prepares IFRS Financial

Statements, the branch will prepare life assurance, PHI and general insurance tax

computations using IFRS.

6

2.1.5.5 If however the parent entity does not prepare IFRS Financial Statements, the

insurers need: to prepare UK GAAP figures to compute their PHI and general

insurance results. These are reported for tax purposes only, resulting in

administrative inconvenience. Typically these figures are not audited, albeit most

tax departments will perform reconciliations to ensure that those figures are

accurate. 2.1.5.6 Local GAAP figures, if drawn up under the Insurance Accounts

Directive, will be used to compute life assurance trade profits. Two of the major

branches are pure reinsurers who do not produce I-E computations

2.1.5.7 Certain jurisdictions do not permit local insurance companies to produce

financial statements using IFRS, and are not expected to permit the use of IFRS in

future periods, including 2013. Examples are Germany and Luxembourg, which are

the home states for a number of UK insurance branches and a major UK branch

reinsurer respectively.

Impact of the introduction of Solvency II

2.1.5.8 If the overseas life assurance company (“OLIC”) rules were abolished as of

31 December 2012, but with other relevant legislation remaining in situ, so that UK

branches of life assurers were taxed in the same manner as other non-insurance UK

branches, UK branches of insurers would have to compute both their life assurance

and general insurance profits using UK GAAP or IFRS

2.1.5.9 Certain overseas groups with UK branches either currently adopted IFRS for

group reporting purposes or intend to adopt IFRS by 2013. However, current

indications are that Luxembourg and Germany will still require their resident insurers

to prepare their own entity financial statements using local GAAP, and will not permit

the alternative option of using IFRS.

2.1.5.10 Hence, if the OLIC rules were abolished, so that UK branches of life

assurers were taxed in the same manner as other UK branches, including general

insurance branches, such UK branches would have to compute their entire profits

using UK GAAP, even though the same operations would have computed their

accounting results under IFRS, albeit for group purposes. The figures produced for

UK GAAP would serve no purpose other than to compute UK taxable profits for

accounting periods up to the date when UK GAAP ceases to exist. Such figures

would remain unaudited and their compilation would require considerable extra

manpower.

2.1.5.11 It would therefore be preferable to allow either:

the adoption of IFRS by such UK branches for computing taxable profits for

2013, so UK branches can use the figures they report for consolidation

purposes (prior obviously to consolidation journals). Any introduction of IFRS

should fall to be taxed in accordance with the normal principles of taxing the

transition to IFRS; or

7

to allow UK branches to continue to use local GAAP to compute taxable

profits of life assurance business, and potentially extending this to general

insurance business too.

8

2.2 Loan Relationships and derivative contracts

Key points:

The basic principle of the loan relationships rules is that the debits and credits

brought into account for tax purposes follow those in the company accounts. Given

that under the new rules the calculation of a life company‟s BLAGAB trading profit

and its aggregate non-BLAGAB result will also be based on the accounts prima facie

there should not be a fundamental difference between the tax position of a

company‟s interest income and expenses under the loan relationships rules

compared to the rules governing the calculation of life company trading profits in the

current section 83 of the Finance Act (“FA”).

The loan relationship rules should be used for the purposes of calculating life

assurance trading profits in respect of non-profit funds. This would help to bring the

life assurance industry in line with other businesses in the financial services sector.

While the use of the loan relationships provisions should be the general rule,

applying them to the calculation of trade profits for with-profit funds could create

unnecessary complexity. Accordingly, for such funds, any investment returns from

loan relationships should be taxed on a quasi-section 83 basis – i.e. the measure of

trading receipts/(expenses) be based on the unadjusted accounting figures.

Given the same accounts-based principles apply to the taxation of derivatives as to

loan relationships, there is in theory no reason why the standard derivative contract

taxation regime should not generally apply to contracts held within non-profit funds.

However some departures from the rules will be required in relation to contracts that

might otherwise be within the scope of section 641 CTA 2009.

Whether or not the loan relationship and derivatives rules are adopted for life

companies‟ trade profits calculations, the treatment of creditor and debtor balances

should be made symmetrical.

2.2.1 Given that investment returns are integral to a life company’s trading

profit, and given that loan relationship rules are founded on accounting

treatment, might it be feasible to continue to disapply those rules in

computing life company trade profits, and rely purely on the accounting

results to capture the relevant income and gains?

2.2.1.1 The basic principle of the loan relationships rules is that the debits and

credits brought into account for tax purposes follow those in the company accounts.

Given that under the new rules the calculation of a life company‟s BLAGAB trading

profit and its aggregate non-BLAGAB result will also be based on the accounts

(rather than the FSA return as previously, PHI business excepted), prima facie there

should not be a fundamental difference between the tax position of a company‟s

interest income and expenses under the loan relationships rules compared to the

9

rules governing the calculation of life company trading profits in the current section

83 FA 1989. The loan relationship rules would apply to both the BLAGAB and the

aggregate non-BLAGAB trading profit calculations.

2.2.1.2 Under the current tax regime for life companies any debtor (i.e. liability) loan

balances are already subject to the loan relationship rules – resulting in a

discrepancy between the treatment of a company‟s creditor relationships (i.e.

assets), which are taxed under section 83, and its debtor relationships, to which the

loan relationships rules apply.

2.2.1.3 Whether or not the loan relationship rules are adopted for life companies‟

trade profits calculations, the treatment of creditor and debtor balances should be

made symmetrical. This would reduce the possibility of both arbitrage-style planning,

and disadvantages to companies due to asymmetric tax treatment.

2.2.1.4 While it would be feasible to continue with a system analogous to the current

section 83 (i.e. for the taxation of loan relationships simply to follow the accounts) it

would be preferable to adopt the loan relationship rules for calculating life assurance

trading profits (both BLAGAB and aggregate non-BLAGAB) in respect of non-profit

business. This would help to bring the life assurance industry in line with other

businesses in the financial services sector (for example banks) who apply the loan

relationship rules to loan balances held for trading purposes.

2.2.1.5 One impact of adopting the loan relationship rules for loan balances in the

life assurance trading profits calculation would be the effect of the connected party

rules in Chapter 6, Part 5 CTA 2009. Many life companies within groups have loans

to or from connected companies; the impact of applying the loan relationships rules

to life companies would be that future write-offs of these loans would, under normal

circumstances, be non-deductible/non-taxable in the life companies. It may be

possible to grandfather existing intercompany loans so that they remain outside the

scope of the loan relationship rules if these are introduced for life companies.

However this would potentially leave in place the discrepancy between the treatment

of debtor and creditor balances as discussed above. As noted, there should be

consistency of treatment of debtor and creditor balances whether or not the loan

relationship rules are implemented.

2.2.1.6 For life companies which invest in index-linked gilts, adopting the loan

relationships rules would result in a reduction in fair value gains (or an increase in

losses) as a result of applying indexation in accordance with section 399 CTA 2009).

Since 2005 other corporates with holdings of index-linked gilts have been able to

claim indexation relief for the purposes of calculating their trade profits. It would be

unfair if this relief was not extended to life companies. The reasons why index-

linked gilts are held by life companies are similar to the reasons why they are held

as investments by other financial companies – specifically as a hedge against the

potential impact of inflation on both their cost base and the level of future liabilities to

their customers, whether these be holders of, for instance, index-linked ISAs or

holders of index-linked annuities. There is no clear reason why the after-tax cost of

10

hedging for life insurance companies should be higher than the cost for other

financial corporates such, as for instance, banks and general insurers.

2.2.1.7 Although there are benefits from the general extension of the loan

relationship rules to life assurance trade profit calculations, it appears that the

application of the rules to the calculation of the profits of with-profit funds could

cause unnecessary complexity and potential distortions. As outlined at 3.1.7.3, the

trading profit for 90:10 funds should be based on the level of shareholder transfers.

While some fiscal adjustments might be required (such as, for instance, those

relating to disallowable expenditure) for such funds, there is a risk that the full-scale

application of the adjustments required under the loan relationship rules could

produce a trading result that diverged radically (and inappropriately) from the

quantum of shareholder transfers. Consequently, it would be preferable to retain a

quasi-section 83 approach for loan relationship assets held within with-profits funds.

2.2.2 Could such an approach also apply to derivative contracts?

2.2.2.1 Given the same accounts-based principles apply to the taxation of

derivatives as to loan relationships, there is in theory no reason why it should not.

Indeed, for the reasons outlined in 2.2.1.4 above the derivatives rules should be

extended to contracts held within non-profit funds (although not for those held within

with-profit funds.)

2.2.2.2 However, there is a potential issue for life companies where the tax

treatment prescribed by the derivatives rules departs from the accounting treatment

– in particular this is the case for those derivatives which Part 7 of CTA 2009 (and

specifically section 641) requires to be taxed on a chargeable gains basis, even

where the derivatives themselves are held as trading stock.

2.2.2.3 There is a risk with regard to life assurance trading profit calculations

(whether BLAGAB or aggregate non-BLAGAB) that an accounts-based tax

treatment of, for example, an investment might differ from the treatment of a

derivative hedging it. Applying the chargeable gains rules to derivatives could in

some specific circumstances have a distorting effect, in that hedges which would be

effective from a commercial and accounting perspective might not be so where tax

is concerned.

2.2.2.4 If therefore, life assurance trade profits calculations are brought within the

general scope of the derivatives rules, there would need to be a specific

disapplication of section 641 for these purposes. Rather than being taxed under

the chargeable gains rules, any gains or losses on these contracts would be treated

as either trading receipts or expenses. In the interests of simplicity, the

measurement of these receipts or expenses should be based on the unadjusted

accounting figures. For the avoidance of doubt, the disapplication of section 641

should only apply for trade profit calculations – i.e. these contracts should continue

to be taxed under chargeable gains rules within the I minus E.

11

2.3 Intangible Fixed Assets

Key points:

The exclusion of intangible assets relating to life assurance business is appropriate

whilst the trade profits of that business are computed by reference to regulatory

surplus. The new regime is based on accounting profits and intangible assets will be

recognised on acquisition in the balance sheet at fair value and amortised

appropriately. For intangible assets acquired after the start of the new regime, this

amortisation should be deductible in the same way as for similar assets held in

connection with other trades.

If this approach is followed post Solvency II, it will be important that where intangible

assets are held as fixed capital, relief is available for non-trading as well as trading

debits.

The removal of the restriction should apply to separately identifiable intangible

assets held on fixed capital account including brands, customer lists, software of

various kinds and goodwill.

The exclusion from the intangible assets rules should continue to apply to

“intangible” assets which represent the recognition of future trade profits or the

deferral of revenue expenditure as these are in essence adjustments to the timing of

the recognition of profit not assets of enduring benefit to the business. They would

include the value of in-force business and deferred acquisition costs which would

each be addressed on normal trading principles.

2.3.1 Under the new accounts based regime, do you think that the exclusion

from the provisions of Part 8 of CTA 2009 of intangible fixed assets held by an

insurance company for the purposes of its life assurance business should be

removed, and, if so, why?

2.3.1.1 The exclusion of intangible assets relating to life assurance business is

appropriate whilst the trade profits of that business are computed by reference to

regulatory surplus. Such assets are generally inadmissible for the purpose of pillar I

of Solvency I and relief is available in the trade profit computation for any resulting

write down in the value of such assets brought into account through Form 40 line 13.

The new regime is based on accounting profits and intangible assets will be

recognised on acquisition in the balance sheet at fair value and amortised

appropriately. For intangible assets acquired after the start of the new regime, this

amortisation should be deductible in the same way as for similar assets held in

connection with other trades. In this context, it will be important that where

intangible assets are held as fixed capital, relief is available for non-trading as well

as trading debits.

12

2.3.2 What implications, including fiscal impacts, would you expect to arise if

the exclusion were removed? What types of assets would be affected?

2.3.2.1 The removal of the exclusion would substitute relief for accounting

amortisation for the current relief for the admissibility restriction where new regime

intangibles are held by the long-term fund. Relief for accounting amortisation for

such assets would become available where these are currently held by a company

writing long-term business as assets of the shareholder fund.

2.3.2.2 The removal of the restriction should apply to separately identifiable

intangible assets acquired on fixed capital account under the new regime. These

would include brands, customer lists, software of various kinds and goodwill. The

exclusion from the intangible assets rules should continue to apply to “intangible”

assets which represent the recognition of future trade profits or the deferral of

revenue expenditure as these are in essence adjustments to the timing of the

recognition of profit not assets of enduring benefit to the business. They would

include the value of in-force business and deferred acquisition costs which would

each be addressed on normal trading principles.

2.3.3 What transitional issues would arise?

2.3.3.1 The difference between the value of aggregate intangible assets in Form 13

of the FSA return and the balance sheet in the financial statements should be dealt

with in a manner similar to that for deferred acquisition costs (“DAC”). There would

be no credit to the transitional adjustment to trade profits. Relief will implicitly be

given for any accounting amortisation between acquisition and the date of transition

to the new regime. This should not be reversed. Future amortisation of these

assets would be disallowed.

13

2.4 Policyholder Tax

Key points:

The deduction for policyholder tax should comprise current policyholder tax

(defined as corporation tax at the policyholder rate as set out in the submitted

computation for an accounting period) and the movement in the year in deferred

tax recognised at policyholder rate.

A deferred tax deduction is required to match the incidence of tax allowances in

contract liabilities and to mitigate unwanted volatility. Not to give an adjustment

for policyholder deferred tax will result in a fundamentally distorted and

unrealistic figure of taxable shareholder profit in many cases.

The deferred tax items qualifying for a policyholder tax deduction will always be

set up and reversed at policyholder rates, their ultimate marginal impact on

current tax also being at policyholder rate.

Transitional adjustments may be required where companies do not currently

obtain a policyholder deferred tax deduction, and/or where the current tax

deduction is based on an accounts rather than computational amount.

2.4.1 Is it possible to identify an accounts-based method of computing

policyholder tax deductions, which is simple, consistent, transparent and

linked to tax actually paid at the policyholder rate?

2.4.1.1 The policy decision of giving a deduction for policyholder tax in the

Consultation Document is welcome but that cash tax payable at the policyholder

rate is not a sufficient basis of calculating the policyholder tax deduction for the

following reasons:

It does not take into account deferred tax (discussed further below).

It is not consistent with an accounts based approach to determining the tax

charge.

The cash tax paid at the corporate level is not consistent with the incidence

of tax allowed for in policyholder liabilities.

2.4.1.2 In respect of policyholder current tax, the tax adjustment should be for the

corporation tax at the policyholder rate as set out in the submitted computation for

an accounting period.

14

2.4.1.3 There should be a deduction for policyholder deferred tax for the following

reasons:

It is included as an expense in the accounts as tax which relates (dependant

on the definition used) to policyholders and it is right that it is deductible as

an expense of the trade. There is a distinction between “tax expended by a

life company on behalf of its policyholders” and “tax borne by policyholders”.

This is a critical distinction and it could influence the calculation of the

policyholder tax deduction.

It reflects commercial reality. From 2013 the starting point in the BLAGAB

trade profits computation will be the profit before all taxes from the financial

statements. That profit will reflect movements in the actuarial liabilities and

the fund for future appropriations (UK GAAP) or unallocated divisible surplus

(IFRS) (“UDS - FFA”) which in turn will reflect charges in respect of tax made

to unit linked (“UL”) and with-profits (“WP”) funds. The other side of that

adjustment is the tax (both UL and WP) which will be included as part of the

overall income statement tax charge. That tax will include both current and

deferred tax. If a tax deduction were not given for the other side of the

actuarial liability movements, the taxable profit would not reflect the

commercial profit from writing the business as both elements relate directly

to policyholders.

It is recognised that deferred tax can be a large number which may never

turn into cash tax purely because equity markets might reverse or a tax

asset, such as excess expenses of management (“XSE”), is utilised.

However in such cases the deferred tax provision would always reverse, and

reverse at the policyholder rate, (giving a taxable credit) and so will give a

matched result over time.

It is further recognised that in some circumstances a deduction for

policyholder tax could lead to a significant tax credit e.g. from a large market

shock.

2.4.1.4 A straightforward balance sheet approach should be the most appropriate

basis satisfying all of the Government‟s criteria for policyholder tax. Other options

have been examined and dismissed as follows:

The deduction for policyholder tax could be based on the tax disclosed in the

income statement or notes to the financial statements as “policyholder tax”.

This approach is problematic as it is considered opaque because of different

approaches to calculating this amount (if it is disclosed at all) and the lack of

a specific accounting standard governing this disclosure for IFRS purposes.

Alternatively, the deduction for policyholder tax could be based on the actual

charge made against policyholder liabilities (via unit pricing for UL contracts

and asset shares for WP contracts). This charge would cover both current

and deferred tax, reflecting the economic impact of tax on income and

15

expense items arising to policyholders. However, this basis requires data

from underlying actuarial calculations and does not provide a transparent,

accounts-based methodology. There is also a risk of material inconsistency

between companies.

2.4.2 If so, how would it work in practice?

2.4.2.1 The policyholder deferred tax would be defined as the movement between

the opening and closing deferred tax amounts in the balance sheet which have been

calculated at policyholder tax rates.

2.4.2.2 Companies calculate deferred tax at each balance sheet date on

temporary/timing differences relating to BLAGAB I minus E items at the policyholder

rate of tax. At subsequent balance sheet dates, such timing/temporary differences

are reassessed such that the prior year amount reverses at the same rate of tax.

2.4.2.3 A key attraction of this approach is that it is accounts-based and reflects the

actual numbers within the tax charge in the accounts. As the basis of the tax

computation moves towards an accounting measure then it seems entirely

appropriate to use an accounts measure of deferred tax. Furthermore this is a

relatively straightforward way to identify policyholder deferred tax and is widely

available as each company has to undertake this calculation and there is

consistency across companies as to how the calculation is undertaken.

2.4.2.4 Government may be concerned that a deferred tax item, once the related

timing difference reverses, may be taxed at the shareholder corporation tax rate.

This is not the case for a company that has an excess of income and chargeable

gains over BLAGAB trade profits (“is XSI”), or even for one that has XSE temporarily

but will return to being XSI. This is because the marginal impact of such an item will

either be to increase tax in the period it crystallises at 20%, or decrease XSE carried

forward which is deductible ultimately at 20%. The following example illustrates this

effect (see next page).

16

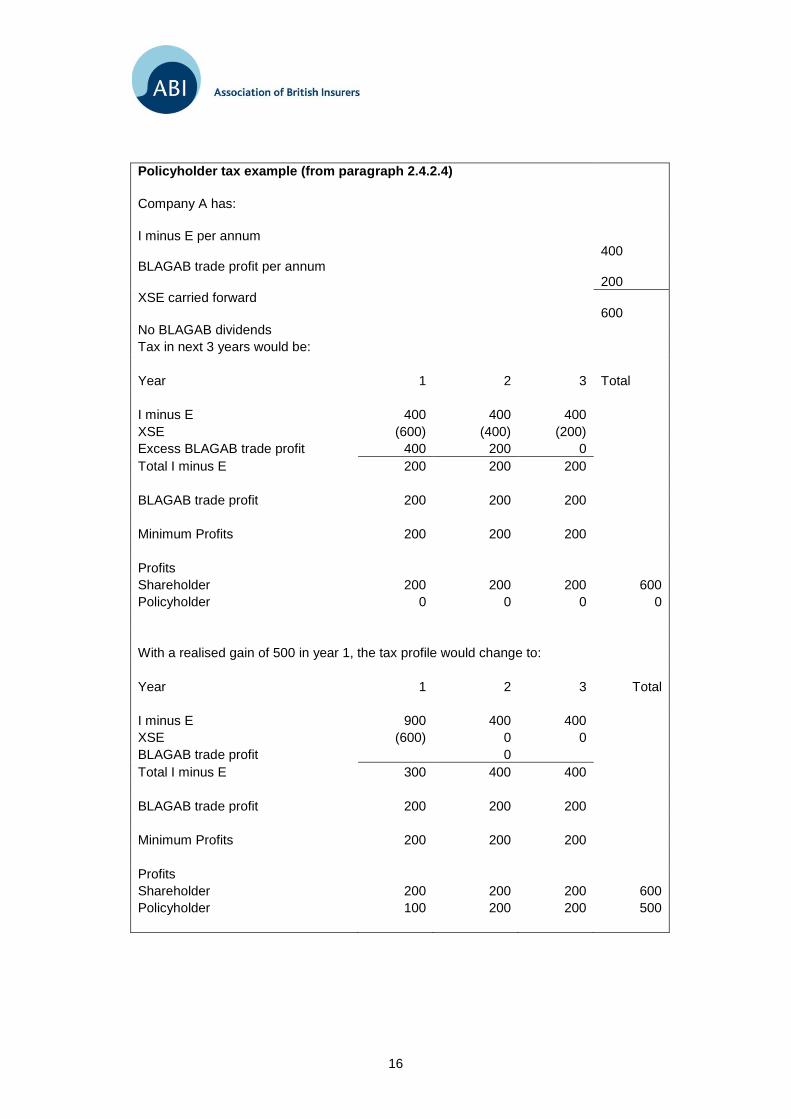

Policyholder tax example (from paragraph 2.4.2.4)

Company A has:

I minus E per annum 400 BLAGAB trade profit per annum 200

XSE carried forward 600

No BLAGAB dividends

Tax in next 3 years would be:

Year 1 2 3 Total

I minus E 400 400 400

XSE (600) (400) (200)

Excess BLAGAB trade profit 400 200 0

Total I minus E 200 200 200

BLAGAB trade profit 200 200 200

Minimum Profits 200 200 200

Profits

Shareholder 200 200 200 600

Policyholder 0 0 0 0

With a realised gain of 500 in year 1, the tax profile would change to:

Year 1 2 3 Total

I minus E 900 400 400

XSE (600) 0 0

BLAGAB trade profit 0

Total I minus E 300 400 400

BLAGAB trade profit 200 200 200

Minimum Profits 200 200 200

Profits

Shareholder 200 200 200 600

Policyholder 100 200 200 500

17

2.4.2.5 The above example apparently shows the additional 500 of gain only

producing an additional 100 policyholder profit in year 1. In fact, the faster unwind of

XSE illustrates that the full 500 marginal increase is taxed at policyholder rate. This

effect applies to any policyholder (i.e. I minus E impacting) deferred tax attribute in

any company that ultimately is XSI. Therefore, the Government‟s concern that

deferred tax items will be taxed at shareholder rate is misplaced.

2.4.2.6 As companies have employed different policyholder tax methodologies prior

to 2013, there would also need to be an appropriate transition mechanism to allow

for variations in deferred tax treatment (including where currently a company does

not get a deduction for policyholder deferred tax).

2.4.2.7 Policyholder deferred tax in respect of unit-linked business is normally

incorporated within mathematical reserves under regulatory reporting, but is a

deferred tax item under IFRS. Certain companies may still retain unit-linked deferred

tax within investment contract liabilities under UK GAAP. For simplicity, no

adjustment to liabilities would be made in these circumstances nor would the

deferred tax form part of the policyholder tax deduction. Implicitly this gives the

same answer as if the adjustments were made.

2.4.3 What are the implications of restricting relief to amounts payable in

respect of a particular year?

2.4.3.1 Including deferred tax within the definition of policyholder tax is essential to

preserve a matched position relative to the allowance for tax in both UL unit prices

and WP asset shares, both of which translate into either policy charges in the

income statement (for investment contracts) or insurance contract liabilities/UDS -

FFA in the balance sheet.

2.4.3.2 Restriction of relief to actual amounts of cash tax in a particular year is likely

to create volatility in the BLAGAB trade profit measure. For example, take a case

where a unit linked book of business of £7bn is invested entirely in collective

investments and the market growth in the year is 15%. In this scenario, ignoring any

discount, the fund deduction from income would be £210m (£7bn x 15% x 20%).

The current tax liability (ignoring expenses and the interaction with the BLAGAB

trade profit) would be £30m (£210m / 7) and the deferred tax charge would be

£180m. If no deduction is taken for deferred tax, shareholder taxable profit of

£180m is higher than the accounting profit .

2.4.3.3 Use of the policyholder tax charge/credit as per the tax computation finally

agreed for a period will mean that there is no deduction required for prior year

adjustments in respect of post 2012 periods, or for prior periods for companies

whose current methodology also follows a computational approach. A transitional

measure will be required to address prior year adjustments made in 2013 or later in

respect of current tax provided in 2012 by companies whose current methodology

does not use a computational approach.

18

Chapter 3 Other Technical Issues

3.1 Allocation of profits, income and gains

Key points:

The ability to determine and allocate accounts profit to specific lines of business will

depend upon the internal systems and procedures of each company rather than the

identity or nature of the lines of business. It should be expected that companies will

be able to identify separately the accounts profit arising from with-profit business,

unit-linked business and non-linked non-profit business.

For with-profits business, it is the trading profit of each with-profit fund and before

fiscal adjustments (e.g. in respect of loan relationships) that is being apportioned.

Any individual company will need to agree with its CRM an allocation methodology to

be used in the tax computation which reflects the manner in which it runs its

business; different companies may thus use different methodologies..

Non profit business written within a with profit fund should be allocated in proportion

to with-profit bonuses, except where a mechanism other than bonus declaration is

used to pass profits to shareholders in which case direct attribution based on the

computation of profits to pass to the shareholder should be used.

For the purpose of tax on chargeable gains, assets which are not directly allocated

to a category of business should be allocated to a different pool from those which

are. Direct attribution will be possible for some lines of business. For other lines of

business, “hybrid” pools may support both basic life assurance and gross roll-up

business. Chargeable gains should be allocated in the same way as other income

and gains. A liabilities based approach might be appropriate for some chargeable

gains.

The I minus E and trade profit allocation methods can be reconciled by the

mechanism described in paragraph 3.1.10 below. Equity and property gains will be

chargeable gains in I minus E but market value movements and realisations for trade

profit purposes. No special measures seem necessary beyond extending the boxes

in section 440(4) of the Income and Corporation Taxes Act (“ICTA”) 1988 where

relevant.

As was discussed at the Open Meeting on 29 June, it is not considered necessary

for there to be an alternative statutory method provided that it is recognised that

different companies will commercially use different methodologies. For some

companies, a method akin to the existing formulaic approach may be suitable. There

is no need for an election.

19

3.1.1 For what lines of business can the accounts profit arising on that

business be directly determined and allocated?

3.1.1.1 The ability to determine and allocate accounts profit to specific lines of

business will depend upon the internal systems and procedures of each company

rather than the identity or nature of the lines of business.

3.1.1.2 In any event, it should be expected that companies will be able to identify

separately the accounts profit arising from with-profit business, unit-linked business

and non-linked non-profit business.

3.1.2 To what extent will current internal accounting and actuarial procedures

enable companies to allocate directly a substantial part of the income and

gains arising on assets held for the purposes of its life insurance business?

What will be the cost of introducing new systems and/or adapting existing

systems?

3.1.2.1 It should be expected that companies will be able to identify separately the

income and gains attributable to policies to which an asset share methodology is

applied as well as to unit-linked policies. Attribution to non-linked non-profit

business will also be possible if the assets are managed in pools specifically

matched to the different types of such business.

3.1.2.2 For clarification for with-profits funds, it is the trading profit of the funds as a

whole and before fiscal adjustments (e.g. in respect of loan relationships) that is

being apportioned.

3.1.2.3. Any individual company will need to agree with its CRM an allocation

methodology to be used in the tax computation which reflects the manner in which it

runs its business; different companies may thus use different methodologies.

3.1.2.4 The cost of separately identifying for tax purposes the income and gains

attributable to lines of business where this is currently not required for those

purposes will vary from company to company.

3.1.3 What bases might be acceptable and/or possible for the allocation of

assets which are not directly allocated to products or lines of business?

3.1.3.1 It is assumed that this question is intended to refer to income and gains

arising from assets rather than to the assets themselves. In so far as it relates to

assets, assets which are not directly allocated to a category of business should be

allocated for the purpose of tax on chargeable gains to a different pool from those

which are.

3.1.3.2 Direct attribution is already used with sub-apportionment for business linked

to more than one category. Other major lines of business, such as with profit

business, are similarly matched to specific pools of assets including real estate and

equities as well as loan relationships. These pools may support both BLAGAB and

20

GRB in a manner analogous to a property linked fund linked to more than one

category. Investment return from these “hybrid” pools could still prima facie be

capable of direct attribution if investment return is attributed directly to policies by

reference to asset shares, but the assets will not themselves be segregated and

there will be no direct matching of specific assets to specific liabilities. A mean

liability approach by reference to the liabilities matched to the hybrid pool might be a

suitable way of addressing the attribution of investment return in these

circumstances. It is understood that individual ABI members are already discussing

with HMRC approaches which may be suitable in their own circumstances.

3.1.4 Will companies always be able to compute the accounts profit of a with-

profit fund?

3.1.4.1 Companies should always be able to compute the accounts profit of a with-

profit fund. This will be the case whether or not the profit is determined by reference

to bonuses declared or because it is derived through the charging of management

or guarantee fees to the with-profit fund.

3.1.5 Is allocation by bonuses always representative of the actual allocation of

assets to the different categories of business?

3.1.5.1 Bonuses in this context are the aggregate of reversionary and terminal

bonuses declared. Allocation by bonus is affected by the mix of policies terminating

in any period. Reversionary bonus policy can also vary from product to product.

There could thus be a persistent bias in using allocation by bonus for the allocation

of income and gains in favour of products where reversionary bonuses are declared.

3.1.5.2 A bonus based apportionment of income and gains for BLAGAB I minus E

will not reflect the underlying allocation of income and gains to the extent that there

is business in the with-profit fund where income and gains pass either to

policyholders or shareholders other than by way of a share in the cost of bonus. For

example, if there were unitised with-profit business where the shareholder profits

were derived in a non-profit fund from charges made to the with-profit fund, the

allocation of income and gains to BLAGAB I minus E would not reflect the

proportions of unitised with-profit business but only the bonus proportions of

conventional with-profit business. Similarly, if there were non-profit annuity business

in a with-profit fund, income and gains would pass to the relevant policyholders by

way of annuities not bonuses. Also where BLAGAB is running off faster than

pension business where pension business is written in the same fund bonuses will

not reflect the underlying allocation of income and gains.

3.1.5.3 Allocation by bonus would thus only fortuitously be representative of the

actual allocation of income and gains in a particular year.

21

3.1.6 What special considerations are there where non-profit business is

written within a with-profit fund?

3.1.6.1 There are two possible circumstances here: in the first, the profits of the non-

profits business are part of the profit pool in which both policyholders and

shareholders share; in the second, the profits of the non-profit business pass to the

shareholder by some legal mechanism agreed with the regulator and the with-profits

actuary. In the first circumstance it will be necessary to allocate income and gains

relating to the non-profit business. This would be done directly if there were a

specific pool of assets for the business or through an agreed method for the with-

profit fund asset pool as a whole. In this circumstance however, the profit from the

non-profit business will only inure to shareholders through the bonus declaration

mechanism and no specific tax adjustment will be required. In the second

circumstance, both the allocation of investment return and profit should be capable

of direct attribution based on the computation of profits to pass to the shareholder.

3.1.7 This document focuses on the allocation of investment income and

gains. Are there other types of income or expenditure which could not be

attributed to categories of business by reference to internal accounting

systems?

3.1.7.1 Direct attribution is already widely established in the allocation of the

components of trade profits from life assurance business. Indeed, it is used for

premiums, benefits, expenses, tax deductions, and movements in liabilities to

policyholders. Looked at in this way, investment return is the exception rather than

the rule.

3.1.7.2 There is however one specific and important item where direct attribution is

unlikely to be possible. Financial statements, whether under IFRS or UK GAAP, do

not permit a "book value" election. They do however currently contain a mechanism

for providing an additional liability for what would otherwise be profits of a with-profit

fund but which have not been allocated between policyholders and shareholders.

This liability is the UDS under IFRS or the FFA under UK GAAP. An allocation

mechanism will be required for the movement in the UDS - FFA. As this is the

movement in a liability, direct attribution would be the normal approach but, given

that the amounts are specifically unallocated, is unlikely to be practicable.

3.1.7.3 However, as discussed at 3.1.10.2, bonuses are the correct and appropriate

way for allocating trade profits of a with-profit fund.

3.1.8 How should chargeable gains be allocated?

3.1.8.1 Chargeable gains should be allocated in the same way as other income and

gains, by direct attribution, allocation by reference to the liabilities matched to a

hybrid pool or mean fund apportionment.

3.1.8.2 One obvious development however would be to include assets matched to

only one category in the relevant linked pools for section 440 ICTA 1988. A

22

transitional provision would be needed if assets changed category as a result at the

date of transition.

3.1.9 Would retaining a liabilities based approach for chargeable gains be

appropriate?

3.1.9.1 Chargeable gains should be allocated in the same way as other income and

gains, by direct attribution, allocation by reference to the liabilities matched to a

hybrid pool or mean fund apportionment. A liabilities based approach is thus

appropriate for some chargeable gains.

3.1.10 If I-E allocation does not follow that used for trade profit purposes are

there any mechanisms that could protect against significant under or over

allocation?

3.1.10.1 The I minus E and trade profit allocation methods can be reconciled by the

mechanism described in the paragraph below. The measure of loan relationship

and derivative gains and losses will be the same. Equity gains will be chargeable

gains in I minus E but market value movements and realisations for trade profit

purposes.

3.1.10.2 It is implicit in allocating trade profit of with-profit funds that the UDS - FFA

should be allocated in such a way as to secure that the shareholder profit from

conventional with-profit business was split in proportion to the split of declared

bonuses for the year. The allocations of investment return to unitised with-profit and

other business within the with-profit fund but where shareholder profits are derived

by way of fees not as a proportion of bonuses would however still reflect the

investment return out of which the fees were borne, and so the profits made, rather

than an allocation by reference to bonuses from another part of the business of the

fund. Direct allocation in respect of non-profit business within a with-profit fund

would also be unaffected. The approach consistent with the current regime would

be to allocate the movement in the UDS - FFA in such a way as to secure that the

shareholder profit from conventional with-profit business was split in proportion to

the split of declared bonuses for the year. This seems an appropriate way to deal

with profits from such business as the shareholder profit is a proportion, frequently

one-ninth, of such bonuses. The allocation of the UDS - FFA would not affect the

direct attribution or apportionment of the income and gains of the with-profit fund as

a whole and would have no impact on I minus E. The allocation basis applied to

income and gains would be consistent between I minus E and trade profit.

3.1.10.3 To summarise the specific issues here, no special measures seem

necessary beyond extending the boxes in section 440(4) ICTA 1988 where relevant.

The use of the bonus allocation is appropriate but only for the movement in UDS -

FFA to give a consistent allocation of the profit from conventional with-profit

business.

23

3.1.11 What would be an appropriate process for reaching agreement with

HMRC and ensuring fairness between companies?

3.1.11.1 The agreement of the details of a factual allocation method should be part

of the self assessment process through discussion between a company and its CRM

in line with the high level principles to be set up in legislation and HMRC guidance

and reflecting the facts and circumstances of each company‟s specific

circumstances.

3.1.12 In what circumstances should any election for factual allocation be

revoked/revocable?

3.1.12.1 As was discussed at the Open Meeting on 29 June, it is not considered

necessary for there to be an alternative statutory method provided that it is

recognised that there are a number of different methodologies which may be

appropriate. For some companies, a method akin to the existing formulaic approach

may be suitable. There is no need for an election.

3.1.13 What would be an appropriate basis for the single apportionment rule?

3.1.13.1 There is no need for such a rule.

24

3.2 Combining GRB and PHI

Key points:

Both PHI and GRB transitional losses, and historic pension business losses, should be

permitted to be used against the new category (“GRB-PHI”) without restriction.

It should not be difficult initially to stream transitional losses against GRB and PHI, but

given the significant level of GRB losses in the industry, it may be that the losses last

much longer than the underlying rationale for streaming GRB-PHI profits using historical

category definitions.

The restriction on the utilisation of pension business losses has not in practice placed any

significant restriction on the use of losses, and it would not cause a significant loss to the

Exchequer for this restriction to be abolished.

Simplification is best achieved by avoiding any need to track historic differences into the

future. It is inefficient to open up what this simplification has meshed together.

3.2.1 Use of losses (including transitional losses)

3.2.1.1 It is appropriate to permit both PHI and GRB transitional losses, and historic

pension business losses, to be used against the new category without restriction. It

is recognised that this is the most generous relief, but it is also consistent with

simplification that companies should not be required to continue to maintain records

in respect of the historic categories for what may be many years.

What levels of unused GRB and PHI losses might exist at 31 December 2012?

3.2.1.2 Some groups are expected to have significant levels of unused GRB losses

at 31 December 2012, as is consistent with taxing on the FSA basis, where new

business strain was written off immediately. It is understood that there are much

less significant levels of unused PHI losses, where the tax basis has followed the

accounts.

Transitional loss streaming

3.2.1.3 It should not be difficult initially to stream transitional losses against GRB

and PHI. But given the significant level of GRB losses in the industry, it may be that

the losses last much longer than any meaningful recollection of the underlying

rationale for streaming GRB-PHI profits using historical category definitions. On an

ongoing basis there would be a systems challenge in identifying the profits arising

from particular historic categories. Neither of these points would seem to be

consistent with the concept of simplification.

25

Other than unrestricted use against new GRB/PHI profits and streaming, what

approaches to transitional loss use might be feasible

3.2.1.4 Allowing use of transitional losses against profits of GRB-PHI should not

cause particular concern for HMRC, as long as it is clear that losses which convert

into full corporation tax rate losses on transition should not be available for

surrender as group relief to other companies in the year of conversion, or by way of

offset in that year against the shareholders share of BLAGAB I minus E.

3.2.1.5 There are other possible methods of restricting loss utilisation. For example,

one might spread the losses over 10 years which is consistent with the rule for

transitional adjustments. This does not give a reasonable result if profits naturally

emerge against which the losses would have been usually offset. The losses do not

arise on transition – they arose historically and should be available against profits

whenever they emerge. A alternative approach therefore would be to offset losses

on transition against profits arising on transition before any net profit is spread. This

could have the effect of matching the losses against the reversal of the items giving

rise to them and would be simpler to administer if all the losses were offset, but, to

the extent that losses were offset in this way, it would be equivalent to spreading

them as they would reduce the amount which would otherwise be spread.

Companies should therefore be able to opt for either a simple carry forward or this

treatment.

3.2.1.6 If there was a wish to stream, HMRC might consider approaching this on the

basis of liabilities. However this brings difficulty. Both protection and PHI business

routinely use negative reserving, which would tend to over-allocate to GRB under

current law. It is not clear what would happen under IFRS Phase II but negative

reserving is expected to be a significant feature on Solvency II.

3.2.1.7 A more prosaic example may assist. It is commonplace to undertake

reinsurance on a “fund only basis” which passes liabilities to a counterparty but

leaves the profit to emerge in the same place as it did before. A mean liability basis

may therefore apportion profits to PHI (say) where the profits are really GRB and

this might deny the utilisation of losses attributable to this business. This would not

be consistent with the direction of the consultative document towards a commercial

and factual basis, not an arithmetic calculation which gives an uncommercial

answer.

3.2.1.8 The factual./commercial direction of the life tax changes together with

simplification objectives point strongly towards a conclusion that there should be no

streaming or other restriction on the use of historic losses in the GRB-PHI category.

Streaming of PB losses up to 2006

3.2.1.9 On amalgamation of the “5 into 1” categories as a result of the last

consultation exercise, streaming was introduced to restrict pension business losses

so that they were restricted and not permitted to be offset against profits of other

GRB categories. This restriction does not appear to have placed any significant

26

restriction on the use of losses, and it would not cause a significant loss to the

Exchequer for this restriction to be abolished.

What levels of streaming exist now, and what might remain at 31 December 2012?

3.2.1.10 Significant levels of streaming do not appear to exist in the industry.

Is there likely to be any difficulty in practice in identifying PB profits within a new

GRB/PHI category?

3.2.1.11 Please see 3.1.2.3 above.

To what extent will PHI business be backed by equities with dividends being

allocated to PHI on a factual basis?

3.2.1.12 PHI is usually backed by fixed interest securities, but fixed interest

securities may include preference shares which are regarded as fixed interest by

investment teams.

3.2.1.13 Where a company has not elected to make allocations on a factual basis,

the identification should be consistent with the basis of allocation generally used in

that situation.

3.2.2 Taxation of dividends

3.2.2.1 See responses above which are relevant.

27

3.3 Shareholder Fund (“SHF”) Assets

Key points:

In addition to the investments held as circulating assets to support its

insurance trade, a life company may hold an investment portfolio which

represents a separate investment business within section 1219 CTA 2009.

Grandfathering of existing SHF and structural assets over transition should

be available at the option of the company.

Transitional measures will be required for long-term fund (“LTF”) assets

which fall to be treated as capital assets.

The segregation of assets between circulating and capital should be agreed

with HMRC using the same process as for the basis of allocation of

investment return (section 3.1.2.3 above).

Capital introduced to a life company by means of a capital contribution

should, as for other traders, be treated as a transaction on capital account.

3.3.1 What practical difficulties are foreseen with the approach outlined in

paragraph 3.26? How might they be addressed?

Introduction

3.3.1.1 At the Open Meeting on 20 June 2011, HMRC suggested that assets of a life

insurance company should be segregated between three categories:

Circulating assets held to support the insurance trade

Fixed assets held for the purposes of the insurance trade

Assets held otherwise than to support the insurance trade (hereafter, capital

assets).

3.3.1.2 Taxable amounts in respect of circulating and fixed assets would be

allocated as between BLAGAB and GRB-PHI and reflected appropriately in the

relevant computations. Taxable amounts in respect of capital assets would be taxed

otherwise than as part of the BLAGAB I minus E profit and the GRB-PHI trading

profit.

3.3.1.3 Practical issues may arise in respect of the classification of assets between

these categories. There may also be transitional issues, in particular where assets

28

of the LTF fall to be dealt with as capital assets. These issues are addressed

separately below.

Categorisation of assets

3.3.1.4 For the majority of life companies, the categorisation of assets of a life

company is currently based upon the regulatory classification. SHF assets will be

treated as capital assets; assets of the LTF will in the main be dealt with as

circulating assets:

The SHF is generally dealt with as if it were a separate investment business

within section 1219 CTA2009.

Section 83XA FA 1989 provides that “structural assets” (broadly, shares in,

debts from and loans to insurance dependants) of a non-profit fund are

treated in the same way as SHF assets.

3.3.1.5 Typically in other businesses, assets which would be regarded as capital

rather than circulating assets would include investments in group companies

including joint ventures, joint operations and associates; own-occupied property; and

goodwill and intangible assets. The identification of such assets held by life

companies is not likely to be problematic.

3.3.1.6 HMRC‟s recognition at the Open Meeting on 20 June 2011 that the capital

asset category will not be limited to such assets is to be welcomed, and that a life

company may carry on a separate investment business within section 1219 CTA

2009 which will continue to be recognised as such in the post 2012 regime. For

example, many life companies currently maintain investment portfolios which are

separately identified and managed as representing “shareholder capital”.

3.3.1.7 Life insurers will need to determine to what extent assets in what is currently

the SHF represent such a separate “investment business” portfolio and to what

extent they are an intrinsic part of the life business and so should be treated as

circulating assets. This is an issue to be determined having regards to the facts of

each case, including the extent to which there is a differentiated and separately

managed portfolio. This may not always be straightforward.

Transitional matters – SHF and s83XA assets

3.3.1.8 The Consultation Document envisages that existing SHF and section 83XA

assets will be grandfathered and will continue to be treated as now. This

grandfathering is intended to apply on an “asset” rather than a “portfolio” basis; thus

on the disposal and reinvestment of current SHF assets, the classification of the

replacement assets will fall to be determined on a factual basis as above.

3.3.1.9 Whilst grandfathering is clearly appropriate in many cases, some companies

have suggested that it would be administratively simpler for them to transition all

29

assets to their new classifications on 1 January 2013. Companies should also

therefore be able to opt out of the proposed grandfathering treatment.

Transitional matters – LTF assets which fall to be classified as capital assets

3.3.1.10 There will be situations in which LTF assets which do not currently fall

within section 83XA would fall to be treated from first principles as capital assets. An

example would be investments held by the LTF in group companies other than

insurance dependents. (Assets held by an internal linked fund should be dealt with

as circulating assets since they are held to back the linked liabilities.) It will be

necessary to determine how such assets shall be dealt with on transition.

3.3.1.11 There are a number of possible options to deal with this transition. Value

differences up to 31 December 2012 in respect of such assets will have been

reflected in trading profits computations either as they arose and/or as part of the

wider transitional measures (refer Chapter 4 below). Accordingly, the simplest

approach is likely to be a transition based upon 31 December 2012 value:

No further adjustments would be required in respect of trading profit

calculations

For BLAGAB I minus E purposes, there would be a deemed disposal and

reacquisition for chargeable gain or loss purposes at that date. The BLAGAB

share of any resulting gain or loss would be held over, as a BLAGAB

chargeable gain, until an actual disposal of the underlying asset.

Capital contributions

3.3.1.12 New capital may be introduced into a life company, as for any trading

company, by means of a capital contribution from the shareholder. A capital

contribution into a life company will currently be injected into the SHF; a transfer

then may or may not be made from the SHF into the LTF.

3.3.1.13 Capital contributions are dealt with as capital items and not as trading

receipts in the case of other traders. To prevent any uncertainty on the point, HMRC

should confirm that the same treatment will continue to apply to life companies.

3.3.2 What processes might be put in place to give companies certainty over

the nature and tax treatment of particular assets?

3.3.2.1 As at 3.1.11.3 above dealing with allocation, the agreement of the

categorisation of assets should be part of the self assessment process, dealt with

through discussion between a company and its CRM and reflecting the facts and

circumstances of each company‟s specific circumstances.

3.3.2.2 In particular, it would not be appropriate to seek to prescribe a list of assets

which will automatically be treated as capital or circulating assets. A prescribed list

may actually create problems in unusual situations (which is where difficulties are

more likely to arise in any case).

30

3.3.3 How should the shareholders’ and policyholders’ shares of BLAGAB

gains be identified?

3.3.3.1 The Consultation Document accepts that there should be a continuation of a

(limited) offset of BLAGAB and capital asset gains and losses. It is appropriate as a

matter of policy that there is such an offset.

3.3.3.2 The transition to Solvency II need not give rise to significant complications

with regard to the operation of section 210A of the Taxation of Chargeable Gains

Act (“TCGA”) 1992. In particular:

Chargeable gains and allowable losses on SHF assets (which are currently

referred to in the legislation as “non-BLAGAB” chargeable gains and

allowable losses) would need to be redefined to reflect the new segregation

and to refer to capital assets (or similar); and

The policyholders‟ and shareholders‟ shares of BLAGAB gains and losses

could be calculated on a basis consistent with the rules as currently drafted

(with clarification that these amounts relate to the BLAGAB apportionment of

gains and losses on circulating assets).

3.3.4 What implications are there for other existing tax rules (for example

sections 171, 171A, 212 TCGA 1992, substantial shareholdings exemption)?

Capital allowances

3.3.4.1 It will be necessary to ensure that the post 2012 regime interacts

appropriately with the capital allowances legislation in order to ensure that capital

allowances are duly reflected in trading profits computations for BLAGAB and GRB-

PHI, and in the BLAGAB I minus E computations.

3.3.4.2 Capital allowances on management assets should be allowed in the

BLAGAB and GRB-PHI trading profits calculations and in the BLAGAB I minus E

computation. Capital allowances which have not previously been given in life trading

profit calculations, because accounting depreciation was effectively tax deductible

as a result of section 83(2), should be given under the new regime.

CGT boxes

3.3.4.3 Currently, the legislation provides for SHF assets to form a separate box

(sections440 A&B ICTA 1988), with transfers between that box and other boxes of

the company being dealt with as market value transactions.

31

3.3.4.4 A separate box treatment should continue for capital assets of the company.

More generally, it is suggested that the section 440 “boxes” are amended so as to

become:

Circulating assets linked (or directly attributable) to GRB-PHI;

Circulating assets linked (or directly attributable) to BLAGAB;

Other circulating assets; and

Capital assets, including SHF and section 83XA assets as at 31 December

2012 which are treated as capital assets.

Legislative references to assets of the LTF

3.3.4.5 There are various places in which the life tax legislation refers explicitly to

assets of the “long-term insurance fund”. Many of these provisions will be re-written

as part of the broader reforms to the regime for taxing life insurance companies.

However, those which remain will need to be amended so as to replace references

to assets of the long-term insurance fund with reference to circulating assets (or

similar).

3.3.4.6 There are also a number of places where other legislative provisions

differentiate as between assets of the LTF and other assets of a life insurer. These

provisions will need to be recast to refer to the expected new segregation as