The 2007–2008 financial crisis and the availability of ... · PDF filethe world. Gover...

13

The 2007–2008 financi Abstract The widespread consolida declining availability of funds to between bank consolidation and financial crisis of 2007–2008. Us state of California, the empirical had a negative impact on the leve crisis. The findings do not supply small business credit in the pre-c Keywords: financial crisis, bank commercial banks Journal of Finance a The 2007–2008 ial crisis and the availability of sm credit Burak Dolar Western Washington University Fang Yang University of Detroit Mercy ation in the banking industry has raised concern o small businesses. In this paper, we investigate t the availability of small business lending in the sing a dataset comprising banking institutions op results indicate that higher consolidation in ban el of small business lending in the period after th y any evidence indicating the impact of market c crisis era. consolidation, small business lending, banking m and Accountancy financial crisis, 1 mall business ns about the the relationship aftermath of the perating in the nking markets has he financial consolidation on markets,

-

Upload

truongtuong -

Category

Documents

-

view

214 -

download

0

Transcript of The 2007–2008 financial crisis and the availability of ... · PDF filethe world. Gover...

The 2007–2008 financial

Abstract

The widespread consolidation in the banking industry has raised concerns about declining availability of funds to small businesses. between bank consolidation and the financial crisis of 2007–2008. Using state of California, the empirical results indicate had a negative impact on the level of crisis. The findings do not supply any evidence indicating the impact of market consolidation on small business credit in the pre-crisis era.

Keywords: financial crisis, bank commercial banks

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

inancial crisis and the availability of small

credit

Burak Dolar Western Washington University

Fang Yang

University of Detroit Mercy

idespread consolidation in the banking industry has raised concerns about

declining availability of funds to small businesses. In this paper, we investigate the and the availability of small business lending in the aftermath of the

Using a dataset comprising banking institutions operating , the empirical results indicate that higher consolidation in banking markets has

the level of small business lending in the period after the financial crisis. The findings do not supply any evidence indicating the impact of market consolidation on

crisis era.

bank consolidation, small business lending, banking markets,

Journal of Finance and Accountancy

2008 financial crisis, 1

mall business

idespread consolidation in the banking industry has raised concerns about the , we investigate the relationship

in the aftermath of the institutions operating in the

in banking markets has in the period after the financial

crisis. The findings do not supply any evidence indicating the impact of market consolidation on

, banking markets,

1. INTRODUCTION

The financial crisis of 2007Depression of the 1930s. While the real economy, leading to the failure of prolonged unemployment, and significant the world. Governments around the world monetary and fiscal policies but economic growth has not been strong.

Access to external funds becomes increasingly difficult for economic downturns. The availability of bank credit to small businesses decreased considerably during the financial crisis of 2007loans under $1 million) provided by banking institutions declined by 8.3% from 2008 toSmall business financing continued to decline from 2009 to 2010 even after the economy started to grow. Small business loans comprised 15.3% in 2010. Similarly, the ratio of small business 68.9% between 2005 and 2010 which indicates the diminishing importance of small business lending for depository lenders (Haynes and Williams 2011

In the United States, small businesses play a According to the US Small Business Administrationabout 6 million employer firms and product (GDP). They employ slightly more than half accounted for 64% of the net new jobsurvive and grow depends on their small businesses using bank credit, liquidity, and the share of bank credit to total assetsthat fast-growing small businesses are different types of loans from commercial banks and finance companiesfirms.

In this paper, we use dataof California to test whether the availability of consolidation in the period after the financial crisis of 2007The changing structure of the banking industry in the last two decades raised questions about the competitive effects of consolidation becomes particularly critical during a credit crunch when accessible for small firms and when the economic recovery dependspeech, the Federal Reserve (Fed) businesses for the nation’s economyonce small firms begin to prosper” (Di Leo and Zibel 2011).

The empirical results of the present study to declines in small business lending in banking markets in the aftermath of the financialThese findings suggest that the recent small businesses in terms of decreased availability of bank creditconsolidated markets. Given the importance of small businesses for the nation’s economy, the

1 Small businesses are defined as firms with less than 500 employees but almost 90% of all small businesses have less than 20 employees (US Census Bureau).

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

he financial crisis of 2007–2008 is deemed by many the worst crisis since the Great While the crisis began in the financial sector, it quickly spread to the the failure of a large number of financial and non-financial

prolonged unemployment, and significant declines in consumer confidence and spendingnments around the world responded to the crisis by pursuing expansionary

but economic growth has not been strong. Access to external funds becomes increasingly difficult for most small businesses during

The availability of bank credit to small businesses decreased considerably financial crisis of 2007–2008. The amount of small business lending (

loans under $1 million) provided by banking institutions declined by 8.3% from 2008 toSmall business financing continued to decline from 2009 to 2010 even after the economy started

Small business loans comprised 16.8% of total assets of banks in 2005 but it declined to 15.3% in 2010. Similarly, the ratio of small business loans to total loans declined from 81.7% to 68.9% between 2005 and 2010 which indicates the diminishing importance of small business lending for depository lenders (Haynes and Williams 2011a).

small businesses play a vital role in the nation’s economy.According to the US Small Business Administration (n.d.), small businesses make up 99.

and generate more than half of the non-farm gross domestic slightly more than half of all private sector employees

net new job-creation from 1998 through 2008. Small firms’ ability to on their access to credit. In a recent study, Cole (2010)

small businesses using bank credit, there is a positive relationship between profitability and , and the share of bank credit to total assets. Likewise, Haynes and Brown growing small businesses are significantly more likely to use external credit

different types of loans from commercial banks and finance companies, than small, non

data comprising commercial banks and thrifts operating in the state availability of small business loans changes with

in the period after the financial crisis of 2007–2008. Why is this issue important? The changing structure of the banking industry in the last two decades raised questions about the competitive effects of consolidation on the availability of credit to small businesses. The issue becomes particularly critical during a credit crunch when bank credit tends to become less accessible for small firms and when the economic recovery depends on their viability. In a 2001

(Fed) Chairman Ben Bernanke highlighted the importance of small businesses for the nation’s economy by pointing out that “a full recovery will only be achieved once small firms begin to prosper” (Di Leo and Zibel 2011).

the present study indicate that increased market consolidationsmall business lending in banking markets in the aftermath of the financial

recent credit squeeze is likely to have imposed challengein terms of decreased availability of bank credit, particularly in more

Given the importance of small businesses for the nation’s economy, the

mall businesses are defined as firms with less than 500 employees but almost 90% of all small businesses have less than 20 employees (US Census Bureau).

Journal of Finance and Accountancy

2008 financial crisis, 2

worst crisis since the Great in the financial sector, it quickly spread to the

financial businesses, confidence and spending across

expansionary

small businesses during The availability of bank credit to small businesses decreased considerably

mall business lending (i.e., business loans under $1 million) provided by banking institutions declined by 8.3% from 2008 to 2010. Small business financing continued to decline from 2009 to 2010 even after the economy started

but it declined to loans to total loans declined from 81.7% to

68.9% between 2005 and 2010 which indicates the diminishing importance of small business

e nation’s economy.1 make up 99.7% of

farm gross domestic of all private sector employees and

Small firms’ ability to Cole (2010) finds that, for

profitability and Haynes and Brown (2009) show

external credit, including than small, non-growth

operating in the state with bank

Why is this issue important? The changing structure of the banking industry in the last two decades raised questions about the

the availability of credit to small businesses. The issue bank credit tends to become less

on their viability. In a 2001 Chairman Ben Bernanke highlighted the importance of small

by pointing out that “a full recovery will only be achieved

consolidation led small business lending in banking markets in the aftermath of the financial crisis.

challenges on , particularly in more

Given the importance of small businesses for the nation’s economy, the

mall businesses are defined as firms with less than 500 employees but almost 90% of all small businesses have

effects of the decline in the competitive position of these firms go beyond the local communities they operate in.

2. PRIOR EVIDENCE ON BANK CONSOLIDATION

As a result of the merger and acquisition activity of number of institutions decreased sharply and a handful of institutions emerged to dominate the US banking industry. Many observers competition and increased market power of existing financial institutions affecting the viability of small banks them for credit. According to Avery and Samolyk (2000), to be affected by consolidation than some other banking servicesnature.2 Local lenders are also better equipped to involving firms with specific credit needs and risks.

Small and large firms differ significantly in the way they obtain credit. the value of relationship lending to small businesses find that small borrowers benefit from forming long-term relationships with their banks in a number of ways. Berger and Udell (1995) show that small firms with longer banking relationcollateral requirements. According to Petersen and Rajan (1994), establishing longrelationships with and concentrating borrowing from a few lenders increase the availability of financing and reduce its cost for small businesses. Their findings also suggest that building a close relationship with a lender has a more significant effect on the availability rather than the price of credit.3 In this regard, the declining number of banks (many of which are small institutions) due to the consolidation of the industry may based small business lending.

Berger et al. (1999) review a large number of research literature (over 250 references) to design a framework for analyzing the caservices industry consolidation. According to Berger et al., a number of studies show that large banks have a disproportionately smaller portfolio of small business loans than small banks. Also, most research findings indicate that consolidations of large banks tend to decrease small business lending while consolidations of small institutions are likely to increase small business lending. Keeton’s (1996) findings from the Fed’s Tenth District states pthat banks lend less to local farms and businesses after being acquired by distant banking organizations or becoming junior partners in new organizations. (1998) suggest that consolidation businesses; however, they argue that large mergers and acquisitions do not have a significant impact on small business lending. According to Peek and Rosengren (1998), the size of the merging banks is not sufficient to determine the small business loan portfolio of the consolidated institution. They argue that the acquiring institution’s prean important determinant of its small business lending policy aft

In their market-level analysis, consolidation on small business lending depends on the suggest that small business loan growth was lower in rural markets affected by mergers and

2 According to Kwast et al. (1997), 84.9% and 10.9% of small businesses use financial services provid(operating within 30 miles) commercial banks and thrifts, respectively. 3 Also see Cole (1998) and Scott (2004).

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

effects of the decline in the competitive position of these firms go beyond the local communities

BANK CONSOLIDATION

As a result of the merger and acquisition activity of the 1980s and 1990s, the total decreased sharply and a handful of institutions emerged to dominate the

Many observers argue that bank consolidation may have reduced market power of existing financial institutions hence,

the viability of small banks as well as small businesses and communities According to Avery and Samolyk (2000), small business lending is more likely

to be affected by consolidation than some other banking services because it is mostly better equipped to underwrite and monitor small busi

involving firms with specific credit needs and risks. Small and large firms differ significantly in the way they obtain credit. Studies looking at

the value of relationship lending to small businesses find that small borrowers benefit from term relationships with their banks in a number of ways. Berger and Udell (1995)

show that small firms with longer banking relationships enjoy lower loan interest rates and collateral requirements. According to Petersen and Rajan (1994), establishing longrelationships with and concentrating borrowing from a few lenders increase the availability of

or small businesses. Their findings also suggest that building a close relationship with a lender has a more significant effect on the availability rather than the

the declining number of banks (many of which are small stitutions) due to the consolidation of the industry may have a negative effect on relationship

Berger et al. (1999) review a large number of research literature (over 250 references) to design a framework for analyzing the causes, consequences, and future implications of financial services industry consolidation. According to Berger et al., a number of studies show that large banks have a disproportionately smaller portfolio of small business loans than small banks. Also,

research findings indicate that consolidations of large banks tend to decrease small business lending while consolidations of small institutions are likely to increase small business lending. Keeton’s (1996) findings from the Fed’s Tenth District states provide partial support for the view that banks lend less to local farms and businesses after being acquired by distant banking organizations or becoming junior partners in new organizations. Findings of Strahan and Weston (1998) suggest that consolidation among small banks increases the availability of credit to small businesses; however, they argue that large mergers and acquisitions do not have a significant impact on small business lending. According to Peek and Rosengren (1998), the size of the

banks is not sufficient to determine the small business loan portfolio of the consolidated institution. They argue that the acquiring institution’s pre-merger small business lending focus is an important determinant of its small business lending policy after the merger.

level analysis, Avery and Samolyk (2000) show that the effect of bank consolidation on small business lending depends on the nature of the market. Their findings

that small business loan growth was lower in rural markets affected by mergers and

According to Kwast et al. (1997), 84.9% and 10.9% of small businesses use financial services provid(operating within 30 miles) commercial banks and thrifts, respectively.

Also see Cole (1998) and Scott (2004).

Journal of Finance and Accountancy

2008 financial crisis, 3

effects of the decline in the competitive position of these firms go beyond the local communities

1980s and 1990s, the total decreased sharply and a handful of institutions emerged to dominate the

reduced hence, adversely

and communities which rely on small business lending is more likely

because it is mostly local in underwrite and monitor small business loans

Studies looking at the value of relationship lending to small businesses find that small borrowers benefit from

term relationships with their banks in a number of ways. Berger and Udell (1995) ships enjoy lower loan interest rates and

collateral requirements. According to Petersen and Rajan (1994), establishing long-term relationships with and concentrating borrowing from a few lenders increase the availability of

or small businesses. Their findings also suggest that building a close relationship with a lender has a more significant effect on the availability rather than the

the declining number of banks (many of which are small a negative effect on relationship-

Berger et al. (1999) review a large number of research literature (over 250 references) to uses, consequences, and future implications of financial

services industry consolidation. According to Berger et al., a number of studies show that large banks have a disproportionately smaller portfolio of small business loans than small banks. Also,

research findings indicate that consolidations of large banks tend to decrease small business lending while consolidations of small institutions are likely to increase small business lending.

rovide partial support for the view that banks lend less to local farms and businesses after being acquired by distant banking

Findings of Strahan and Weston among small banks increases the availability of credit to small

businesses; however, they argue that large mergers and acquisitions do not have a significant impact on small business lending. According to Peek and Rosengren (1998), the size of the

banks is not sufficient to determine the small business loan portfolio of the consolidated merger small business lending focus is

Avery and Samolyk (2000) show that the effect of bank Their findings

that small business loan growth was lower in rural markets affected by mergers and

According to Kwast et al. (1997), 84.9% and 10.9% of small businesses use financial services provided by local

acquisitions than rural markets which did not experience consolidation during the midOne exception was mergers among smaller banks which resulted in small business credit in local banking markets. business lending in urban markets. However, concentrated urban markets experiencing withinmarket consolidation had lower small business lending growththat bank consolidation may have anticompetitive effects.(2003) find that small business loan growth was significantly lower in urban markets where within-market merger activity increasduring the late 1990s. Their results also indicate that bank consolidation is likely to have a negative impact on small business borrowers and credit markets may be valid.

Some analyses have demonstrated that the net effects of consolidation on the availability of small business lending depends on external factors. Using data on over 6,000 US bank mergers and acquisitions from the late 1970s to the early 1990s, Berger et al. (1998) find that consolidation substantially reduces small business lendingby the dynamic effects. In response to decreasing supply of small busmergers and acquisitions, other banking institutions in the same market, and in some cases consolidating institutions themselves, increase their small business lending which mostly offsets the initial reduction. Berger et al. (2the banking industry during the period from 1980 to 1998. Their findings suggest that mergers and acquisitions significantly increase the probability of entry into the markets where the consolidation activity is taking place. They argue that a decline in small business lending in a local banking market owing to consolidation may be partially offset by de novo entry. However, as we investigate in this paper, these external factors may not be strongdeclining availability of small business loans when

3. SMALL BUSINESS CREDIT DURING A CREDIT CRUNCH

A credit crunch is defined as a general decline in the availability of credit as financiainstitutions tighten their lending standards and raise the cost of borrowing.and Scharfstein (2010), a credit crunch has important implications because declining supply of credit puts an upward pressure on interest rate spreads causing further declines in lending than one might see in a typical recession. also play a role in the decline of bank with decreasing demand for loans by borrowersactivity. Even though a decrease in lending may generally one of the factors tends to be (1991) show that during the (relatively mild) (or the “capital crunch” which is a supplybank credit, whereas reduced demand for credit lending slowdown.

The Federal Reserve Board’s Senior Loan Officer Opinion Surveys on Bank Lending Practices from 2008 and 2009 suggest that a number of sdeclining business lending, both for large and small firms.

4 The quarterly surveys are completed by approximately 80 large domestic banks and the US branches of foreign banks.

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

acquisitions than rural markets which did not experience consolidation during the midOne exception was mergers among smaller banks which resulted in increased availa

credit in local banking markets. Bank consolidation had limited impact on small business lending in urban markets. However, concentrated urban markets experiencing withinmarket consolidation had lower small business lending growth, a result consistent with the view that bank consolidation may have anticompetitive effects. Similarly, Samolyk and Richardson

small business loan growth was significantly lower in urban markets where market merger activity increased the local market share of the surviving institutions

eir results also indicate that bank consolidation is likely to have a negative impact on small business borrowers and that antitrust concerns about small business

Some analyses have demonstrated that the net effects of consolidation on the availability of small business lending depends on external factors. Using data on over 6,000 US bank

nd acquisitions from the late 1970s to the early 1990s, Berger et al. (1998) find that consolidation substantially reduces small business lending; however, this decline is largely offset by the dynamic effects. In response to decreasing supply of small business loans associated with mergers and acquisitions, other banking institutions in the same market, and in some cases consolidating institutions themselves, increase their small business lending which mostly offsets the initial reduction. Berger et al. (2004) look at the effects of consolidation on market entry in the banking industry during the period from 1980 to 1998. Their findings suggest that mergers and acquisitions significantly increase the probability of entry into the markets where the

tion activity is taking place. They argue that a decline in small business lending in a local banking market owing to consolidation may be partially offset by de novo entry. However, as we investigate in this paper, these external factors may not be strong enough to reverse declining availability of small business loans when there is a general decline in credit supply.

3. SMALL BUSINESS CREDIT DURING A CREDIT CRUNCH

A credit crunch is defined as a general decline in the availability of credit as financiainstitutions tighten their lending standards and raise the cost of borrowing. According to Ivashina

a credit crunch has important implications because declining supply of credit puts an upward pressure on interest rate spreads causing further declines in lending than one might see in a typical recession. Other than supply-side factors, demand-side

of bank credit. Contraction in business lending may be associated with decreasing demand for loans by borrowers following a general slowdown in economic

decrease in lending may be caused by a combination of the two factors, tends to be more significant. For example, Bernanke and Lown

(1991) show that during the (relatively mild) recession of the early 1990s, declining bank capital (or the “capital crunch” which is a supply-side factor) had a small effect on the availability of bank credit, whereas reduced demand for credit by borrowers played a more important role in the

he Federal Reserve Board’s Senior Loan Officer Opinion Surveys on Bank Lending Practices from 2008 and 2009 suggest that a number of supply-side factors contributed todeclining business lending, both for large and small firms.4 According to the surveys, t

The quarterly surveys are completed by approximately 80 large domestic banks and the US branches of foreign

Journal of Finance and Accountancy

2008 financial crisis, 4

acquisitions than rural markets which did not experience consolidation during the mid-1990s. increased availability of

Bank consolidation had limited impact on small business lending in urban markets. However, concentrated urban markets experiencing within-

, a result consistent with the view Samolyk and Richardson

small business loan growth was significantly lower in urban markets where ed the local market share of the surviving institutions

eir results also indicate that bank consolidation is likely to have a antitrust concerns about small business

Some analyses have demonstrated that the net effects of consolidation on the availability of small business lending depends on external factors. Using data on over 6,000 US bank

nd acquisitions from the late 1970s to the early 1990s, Berger et al. (1998) find that this decline is largely offset iness loans associated with

mergers and acquisitions, other banking institutions in the same market, and in some cases consolidating institutions themselves, increase their small business lending which mostly offsets

004) look at the effects of consolidation on market entry in the banking industry during the period from 1980 to 1998. Their findings suggest that mergers and acquisitions significantly increase the probability of entry into the markets where the

tion activity is taking place. They argue that a decline in small business lending in a local banking market owing to consolidation may be partially offset by de novo entry. However,

enough to reverse there is a general decline in credit supply.

A credit crunch is defined as a general decline in the availability of credit as financial According to Ivashina

a credit crunch has important implications because declining supply of credit puts an upward pressure on interest rate spreads causing further declines in lending than

side effects may in business lending may be associated

general slowdown in economic ombination of the two factors,

. For example, Bernanke and Lown of the early 1990s, declining bank capital

side factor) had a small effect on the availability of played a more important role in the

he Federal Reserve Board’s Senior Loan Officer Opinion Surveys on Bank Lending contributed to

According to the surveys, the

The quarterly surveys are completed by approximately 80 large domestic banks and the US branches of foreign

majority of banks tightened their lending standards and increased the margin between the interest charged on loans and the cost of funds in the postreported that increased losses, and diminished capitatheir lending capacities which, as a result, contributed to the tightening of credit standards. Tsurveys also show that banks decreased the size of loans, shortened the maturity of lending, and imposed higher collateral requirements throughout the period.

A number of research reports published by the US Small Business Administrationthe changes in small business lending during the recent financial crisis.dramatic declines in the volume as well as portfolio share of small business loans (to total assets and to total business loans) even after the economy stopped contracting in 2009. The total value of small business loans (which consisindustrial loans) by banks declined by 2.3% from 2008 to 2009 and by 6.2% from 2009 to 2010. The number of small business loans also declined in the post2009 and 3.9% from 2009 to 2010. Small businesses have also been less successful in competing with other borrowers (including large businesses) for credit. Between 2003 and 2008, the average proportion of total assets allocated to small business loans was 16.5%. The rato 15.9% and 15.3% in 2009 and 2010, respectively. Similarly, the average ratio of small business loans to total loans was 76.6% in the period from 2003 to 2008. In 2009 and 2010, it dropped to 69.9% and 68.9%, respectively.

One of the primary causes of the crisis is the collapse of the housing market in the United States after years of steadily increasing prices. Fueled by low interest rates and risky lending practices, the US housing market experienced a longBetween 1997 and 2006, the Standard and Poor’s/Casemeasures for the US residential housing market, increased by 124% (“CSI: Credit Crunch” 2007). However, after the peaked in midFrom the 2006 peaks through May 2012, the prices dropped approximately 35%. Udell (2009) argues that loans secured by business owners using their personal residences as collateral, may be particularly difficult to obtain because of major problems in the lending by commercial finance co1992 credit crunch; however, theyas many large financial companiesinstitutions since 1992. Moreovercrunch themselves as they rely on thestrain during the crisis) and bank

There have been anecdotal newspaper reports of in the aftermath of the financial crisis of 2007bank lending, small business credit Congressional Oversight Panel report, by 9% while their overall lending portfolios Similarly, small business loan portfolios and overall respectively at the smallest banks for

5 Haynes and Williams (2011a); Haynes and Williams (2011b); Haynes and Williams (2010); US Small Business Administration (2010); US Small Business Administration (2009).

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

majority of banks tightened their lending standards and increased the margin between the interest charged on loans and the cost of funds in the post-crisis period. A significant share of institutions reported that increased losses, and diminished capital and liquidity positions negatively impacted their lending capacities which, as a result, contributed to the tightening of credit standards. T

ecreased the size of loans, shortened the maturity of lending, and er collateral requirements throughout the period.

A number of research reports published by the US Small Business Administrationthe changes in small business lending during the recent financial crisis.5 The findings suggest dramatic declines in the volume as well as portfolio share of small business loans (to total assets and to total business loans) even after the economy stopped contracting in 2009. The total value of small business loans (which consists of commercial real estate loans, and commercial and industrial loans) by banks declined by 2.3% from 2008 to 2009 and by 6.2% from 2009 to 2010. The number of small business loans also declined in the post-crisis period: 14.8% from 2008 to

from 2009 to 2010. Small businesses have also been less successful in competing with other borrowers (including large businesses) for credit. Between 2003 and 2008, the average proportion of total assets allocated to small business loans was 16.5%. The rato 15.9% and 15.3% in 2009 and 2010, respectively. Similarly, the average ratio of small business loans to total loans was 76.6% in the period from 2003 to 2008. In 2009 and 2010, it dropped to 69.9% and 68.9%, respectively.

causes of the crisis is the collapse of the housing market in the United States after years of steadily increasing prices. Fueled by low interest rates and risky lending practices, the US housing market experienced a long-lasting boom which lasted until 2Between 1997 and 2006, the Standard and Poor’s/Case-Shiller Home Price Indices, the leading measures for the US residential housing market, increased by 124% (“CSI: Credit Crunch”

However, after the peaked in mid-2006, U.S house sales prices began their steep decline. From the 2006 peaks through May 2012, the prices dropped approximately 35%.

oans secured by real-estate, a major source of financing for small business owners using their personal residences as collateral, may be particularly difficult to

problems in the real estate market. Udell also notes that finance companies helped offset the decline in bank credit during the

they may not have played the same role in the recent ompanies have disappeared or they have been acquired by banking

Moreover, some finance companies may have experiencecrunch themselves as they rely on the commercial paper market (which experienced significant

and banking institutions for financing. ve been anecdotal newspaper reports of declining bank credit to

in the aftermath of the financial crisis of 2007–2008. Even though there was a general decline in credit decreased disproportionately more. According to a

Congressional Oversight Panel report, large banks decreased their small business loan portfolios while their overall lending portfolios fell by 4.1% in 2009 from the previous year.

portfolios and overall loan portfolios dropped by 2.7% and 0.2%, respectively at the smallest banks for the same period (Maltby 2010).

Williams (2011a); Haynes and Williams (2011b); Haynes and Williams (2010); US Small Business Administration (2010); US Small Business Administration (2009).

Journal of Finance and Accountancy

2008 financial crisis, 5

majority of banks tightened their lending standards and increased the margin between the interest crisis period. A significant share of institutions

l and liquidity positions negatively impacted their lending capacities which, as a result, contributed to the tightening of credit standards. The

ecreased the size of loans, shortened the maturity of lending, and

A number of research reports published by the US Small Business Administration look at The findings suggest

dramatic declines in the volume as well as portfolio share of small business loans (to total assets and to total business loans) even after the economy stopped contracting in 2009. The total value

ts of commercial real estate loans, and commercial and industrial loans) by banks declined by 2.3% from 2008 to 2009 and by 6.2% from 2009 to 2010.

crisis period: 14.8% from 2008 to from 2009 to 2010. Small businesses have also been less successful in competing

with other borrowers (including large businesses) for credit. Between 2003 and 2008, the average proportion of total assets allocated to small business loans was 16.5%. The ratio declined to 15.9% and 15.3% in 2009 and 2010, respectively. Similarly, the average ratio of small business loans to total loans was 76.6% in the period from 2003 to 2008. In 2009 and 2010, it

causes of the crisis is the collapse of the housing market in the United States after years of steadily increasing prices. Fueled by low interest rates and risky lending

lasting boom which lasted until 2006. Shiller Home Price Indices, the leading

measures for the US residential housing market, increased by 124% (“CSI: Credit Crunch” egan their steep decline.

From the 2006 peaks through May 2012, the prices dropped approximately 35%. In this respect, major source of financing for small

business owners using their personal residences as collateral, may be particularly difficult to that increased

mpanies helped offset the decline in bank credit during the recent credit squeeze

been acquired by banking experienced a credit

(which experienced significant

declining bank credit to small businesses general decline in

decreased disproportionately more. According to a large banks decreased their small business loan portfolios

by 4.1% in 2009 from the previous year. dropped by 2.7% and 0.2%,

Williams (2011a); Haynes and Williams (2011b); Haynes and Williams (2010); US Small Business

4. EMPIRICAL MODEL AND RESULTS

4.1. Description of the dataset

We utilize the database of the Federal Deposit Insurance Corporation (FDIC), which reports demographic and financial information on thrifts. Our sample consists of 322 observations gathered from 46California from 2004 to 2010, inclusivelyAreas (MSAs) and rural markets as nonsmall businesses and banking institutions in the US economy. Cstate in the nation, with a population of over 37 million as of 201population). The state has the eighth largest economy in the world $1,936 billion in 201) producing 13of bank offices in the US totaling 7,176 as of 201

4.2. Description of variables and a priori expectations

Table 1 (Appendix) describes

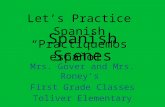

loans to include commercial real estate under $1 million (as well as theirsmall business loan volume by following the approach used by Avery and Samolyk (2004). Small business lending volume of a bank bank’s deposit market share of the business lending volume of a market institution operating in the market. In order to test for possible effects of market compare the periods before (i.e., 2004 through 2007) and after (i.e., 2008 through 2010) the financial crisis. Figure 1 (Appendix) by loan type from 2004 through 2010. Overall, the figurelending peaked in 2007. Also, there is a slight increase in average small business2008 to 2009, followed by a significant decline from 2009 to 2010. Descriptive statistics for all variables in Table 2 (Appendix). The data are annual (as of June 30) and all dollar amounts are converted to constant 2010 dollars using the Consumer Price Index (CPI) deflator.THREE (which denotes the threelevel of small business lending and market would expect that higher market loans on the assumption that low levels of competition leads to higher rates on loans as well as lower availability of loans, ceteris paribus

particularly vulnerable since consolidation are the major providers of credit to small businesses.

6 The information about California is based on sources gathered fromEconomic Analysis, and the FDIC. 7 The findings of Haynes and Williams (2011a) also suggest a significant decline in most CRE and CI loan categories from 2009 to 2010.

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

4. EMPIRICAL MODEL AND RESULTS

Description of the dataset

database of the Federal Deposit Insurance Corporation (FDIC), which reports demographic and financial information on all FDIC-insured US commercial banks and

consists of 322 observations gathered from 46 banking markets in the state of , inclusively. Urban markets are defined as Metropolitan Statistical

Areas (MSAs) and rural markets as non-MSA counties. The dataset is a representative sample of small businesses and banking institutions in the US economy. California is the most populous

, with a population of over 37 million as of 2011 (11.9% of the total US has the eighth largest economy in the world (with a gross producing 13.3% of the US GDP. California also had the highest number

totaling 7,176 as of 2011.6

Description of variables and a priori expectations

describes the variables used in this study. We define small business loans to include commercial real estate loans (CRE), and commercial and industrial

ir sum). We calculate the annual estimates of each institution’s small business loan volume by following the approach used by Avery and Samolyk (2004). Small business lending volume of a bank in a given market is estimated by multiplying the

the market by its total small business lending. The market is then calculated by summing up the loan estimate

institution operating in the market. possible effects of market consolidation on small business lending

compare the periods before (i.e., 2004 through 2007) and after (i.e., 2008 through 2010) the (Appendix) graphs average small business lending in banking markets rough 2010. Overall, the figure shows that average small business

Also, there is a slight increase in average small businessfollowed by a significant decline from 2009 to 2010.7

Descriptive statistics for all variables for periods 2004–2007 and 2008–2010The data are annual (as of June 30) and all dollar amounts are converted

to constant 2010 dollars using the Consumer Price Index (CPI) deflator. We employ (which denotes the three-firm concentration ratio) to study the relationship between the

level of small business lending and market consolidation in banking markets in California.would expect that higher market consolidation in a market has a negative impact on business loans on the assumption that low levels of competition leads to higher rates on loans as well as

ceteris paribus. Small businesses lending would be expected to be particularly vulnerable since consolidation leads to the disappearance of many small banks which

major providers of credit to small businesses.

about California is based on sources gathered from the US Census Bureau, the US

The findings of Haynes and Williams (2011a) also suggest a significant decline in most CRE and CI loan

Journal of Finance and Accountancy

2008 financial crisis, 6

database of the Federal Deposit Insurance Corporation (FDIC), which US commercial banks and

markets in the state of Urban markets are defined as Metropolitan Statistical

The dataset is a representative sample of alifornia is the most populous

(11.9% of the total US ross state product of

had the highest number

We define small business (CRE), and commercial and industrial loans (CI)

each institution’s small business loan volume by following the approach used by Avery and Samolyk (2004).

multiplying the The total small

estimates of each

on small business lending, we compare the periods before (i.e., 2004 through 2007) and after (i.e., 2008 through 2010) the

banking markets hat average small business

Also, there is a slight increase in average small business lending from

2010 are provided The data are annual (as of June 30) and all dollar amounts are converted

We employ the variable study the relationship between the

in banking markets in California. One impact on business

loans on the assumption that low levels of competition leads to higher rates on loans as well as . Small businesses lending would be expected to be leads to the disappearance of many small banks which

the US Census Bureau, the US Bureau of

The findings of Haynes and Williams (2011a) also suggest a significant decline in most CRE and CI loan

The coefficient on the interaction termvariable which equals 0 for observations from the years 20042008 through 2010) indicates the change in ththe financial crisis. In this respect, our main focus is the sign of the coefficients onPOSTxTHREE which enables us to test whethean impact on the availability of small business lending example, a negative and significantin market consolidation leads to aceteris paribus. Based on anecdotal evidence indicating the relative banks (compared to large institutions) in the latest crisis, wcredit crunch on small business lending dominated by larger institutions. OFFICE serves as a proxy for market size. The coefficient on expected to be greater than zero, assuming that the level of small business lending is higher in larger markets (measured in terms of control for the effect that average institution size given banking market may have on the level of small business lending.control for the presence of institutions affiliated wstudies, including Berger et al. (1999)less likely to provide services to DeYoung et al. (1999) suggest that on small business lending. We follow the findingsign on the coefficients of DEPOINS

OFFRATIO is the market average of the in a given market to its total number of offices.of presence of institutions in a given market. performance of banking institutions in a market by entering explanatory variables. Finally, the variable UNEMP is employed to control for the effects that macroeconomic conditions may have on small business credit. Holding other factors constant, the level of small business lending is more likely to decline (due to both demand and supply factors) during times of slow economic activity and high unemployment.

4.3. Model specifications and regression

We use a fixed effects model to explain variations in the level of small business lending in banking markets in California in the prethe independent variables, THREESince the relationship is specified as linear in the natural logarithms of these independent variables, their estimated coefficients can be interpreted as elasticities.

The regression model has the following general form: Ln(Y) = b0 + b1POST + b + b5LnDEPOINS + + b10UNEMP + α +

8 Note that interacting THREE with POST is equivalent to estimating two separayears before the financial crisis and one for the years afterwards (Wooldridge 2000, pp. 412

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

icient on the interaction term POSTxTHREE (where POST is the time dummy variable which equals 0 for observations from the years 2004–2007 and 1 for observations from

the change in the small business lending volume in the period after crisis. In this respect, our main focus is the sign of the coefficients on

enables us to test whether or not the level of market consolidationthe availability of small business lending in the aftermath of the crisis.

example, a negative and significant coefficient on POSTxTHREE would suggest that an increase leads to a decline in small business lending in the post-crisis

Based on anecdotal evidence indicating the relative financial strength of small nstitutions) in the latest crisis, we hypothesize that the effect of the

on small business lending was more significant in consolidated banking markets

proxy for market size. The coefficient on OFFICE would be expected to be greater than zero, assuming that the level of small business lending is higher in larger markets (measured in terms of offices held), ceteris paribus. We enter DEPOINS

average institution size (measured by deposits per institution) in a given banking market may have on the level of small business lending. HOLD is

institutions affiliated with a multibank holding companyr et al. (1999) and Strahan and Weston (1998) argue that large bank

less likely to provide services to small businesses. Also, the findings of Keeton (1995) and suggest that multibank holding company affiliation has a negative impact

We follow the findings of previous research and expect a negative DEPOINS and HOLD, ceteris paribus.

OFFRATIO is the market average of the ratio of an institution’s number of bank offices in a given market to its total number of offices. This variable is included to control for the

of institutions in a given market. We control for the financial condition and banking institutions in a market by entering ROA and CAPRATIO as

he variable UNEMP is employed to control for the effects that macroeconomic conditions may have on small business credit. Holding other factors constant,

level of small business lending is more likely to decline (due to both demand and supply factors) during times of slow economic activity and high unemployment.

regression results

We use a fixed effects model to explain variations in the level of small business lending in anking markets in California in the pre- and post-crisis era. The dependent variables as well as

THREE, OFFICE, and DEPOINS are entered in natural logarithms. Since the relationship is specified as linear in the natural logarithms of these independent

their estimated coefficients can be interpreted as elasticities. The regression model has the following general form:

b2Ln(THREE) + b3(POST x Ln(THREE)) + b4LnOFFICE LnDEPOINS + b6HOLD + b7OFFRATIO + b8ROA + b9CAPRATIO UNEMP + α + ε

with POST is equivalent to estimating two separate regression equations, one for the years before the financial crisis and one for the years afterwards (Wooldridge 2000, pp. 412–413).

Journal of Finance and Accountancy

2008 financial crisis, 7

POST is the time dummy and 1 for observations from

in the period after crisis. In this respect, our main focus is the sign of the coefficients on

consolidation has had aftermath of the crisis.8 For

suggest that an increase crisis period,

strength of small the effect of the banking markets

would be expected to be greater than zero, assuming that the level of small business lending is higher in

DEPOINS to (measured by deposits per institution) in a

is employed to ith a multibank holding company. A number of

Strahan and Weston (1998) argue that large banks are Keeton (1995) and

multibank holding company affiliation has a negative impact of previous research and expect a negative

ratio of an institution’s number of bank offices This variable is included to control for the level

We control for the financial condition and CAPRATIO as

he variable UNEMP is employed to control for the effects that macroeconomic conditions may have on small business credit. Holding other factors constant,

level of small business lending is more likely to decline (due to both demand and supply

We use a fixed effects model to explain variations in the level of small business lending in crisis era. The dependent variables as well as

in natural logarithms. Since the relationship is specified as linear in the natural logarithms of these independent

LnOFFICE CAPRATIO

te regression equations, one for the 413).

where α is the market fixed effect which contains all factors that do not vary over time and the idiosyncratic error term. The estimated fixed effects model generates the (Appendix) where we regress threeactivity on market consolidation significant at the 1% level. They explain level of small business lending in

The coefficients on THREEstatistically significant. In this respect, our results do not supply any indicating the impact of market consolidationcrisis. The coefficients on POSTxTHREEfinding indicates that, holding other factors constant, market on the level of small business lending in banking markets in the aftermath of the financial crisis.For example, in column 1 of Table total small business lending with respect to the (the result is not statistically significantsignificant coefficient on POSTxlending with respect to the three-period, ceteris paribus, with each 10% increase in the additional decrease in total small business lendingof market consolidation on small business lending became more crisis.

In all models estimated, the coefficients on significant at the 1% level. The findings suggest that the level of small business lending increases with market size, ceteris paribus

result which is not consistent with our relationship between average institution size The coefficients on HOLD are negative and statistically significant at conventional levelsof the models suggesting that increased company has a negative impact on ROA are negative and statistically significant in all modelsof small business loans declines at more coefficients on CAPRATIO are negative Finally, the coefficients on UNEMP are negative and statistically siestimated indicating that small business lending unemployment and economic downturn,

5. CONCLUDING REMARKS

The financial crisis of 2007had a serious impact on the US real economy. declining availability of bank credit during of external financing.

9 The results are similar in the regression models where CRE and CI are entered as the dependent variables

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

fixed effect which contains all factors that do not vary over time and

The estimated fixed effects model generates the regression results reported in three dependent variables measuring small business lending

consolidation and control variables. All estimated models are statistically significant at the 1% level. They explain 51.65%, 45.75% and 48.23% of the variation in the level of small business lending in California’s banking markets, respectively.

THREE are negative in all estimated models howeverIn this respect, our results do not supply any conclusive evidence

consolidation on small business lending before the financial he coefficients on POSTxTHREE are negative and significant in all the models.

that, holding other factors constant, market consolidation had a negative impact the level of small business lending in banking markets in the aftermath of the financial crisis.

n column 1 of Table 3, the coefficient on THREE indicates that the elasticity of total small business lending with respect to the three-firm ratio was -0.14 in the pre

significant). On the other hand, the negative and statistically coefficient on POSTxTHREE implies that the elasticity of total small business

-firm ratio is higher in the post-crisis period versus the pre, with each 10% increase in the three-firm ratio resulting in a

decrease in total small business lending.9 These results indicate that the neon small business lending became more pronounced after the financial

, the coefficients on OFFICE are positive and statistically level. The findings suggest that the level of small business lending increases

ceteris paribus. The coefficients on DEPOINS are positive and which is not consistent with our a priori expectation. The findings indicate

average institution size and the level of small business lendinghe coefficients on HOLD are negative and statistically significant at conventional levels

increased presence of banks operating under a multibank holding impact on small business lending, ceteris paribus. The coefficients on

ROA are negative and statistically significant in all models. This result implies that the declines at more profitable banking institutions, ceteris paribus

are negative and only marginally significant in one of the models. inally, the coefficients on UNEMP are negative and statistically significant in all models

indicating that small business lending of all types decline during times of high downturn, ceteris paribus.

5. CONCLUDING REMARKS

2007–2008 did not only affect the financial services industry but it real economy. Small businesses are particularly vulnerable to

declining availability of bank credit during economic downturns since they have

The results are similar in the regression models where CRE and CI are entered as the dependent variables

Journal of Finance and Accountancy

2008 financial crisis, 8

fixed effect which contains all factors that do not vary over time and ε is

results reported in Table 3 measuring small business lending

All estimated models are statistically of the variation in the

however, they are not evidence

on small business lending before the financial are negative and significant in all the models. This

had a negative impact the level of small business lending in banking markets in the aftermath of the financial crisis.

the elasticity of in the pre-crisis-era and statistically

implies that the elasticity of total small business versus the pre-crisis

resulting in a 1.57% the negative effect

after the financial

are positive and statistically level. The findings suggest that the level of small business lending increases

positive and significant, a indicate that the

level of small business lending is positive. he coefficients on HOLD are negative and statistically significant at conventional levels in two

resence of banks operating under a multibank holding . The coefficients on

that the volume ceteris paribus. The

marginally significant in one of the models. gnificant in all models

decline during times of high

did not only affect the financial services industry but it are particularly vulnerable to since they have limited sources

The results are similar in the regression models where CRE and CI are entered as the dependent variables.

Both demand and supply factors are likely to have played a role in declining bank credit in the period after the recent financial crisisparticular significance since the crisis had a severe impact on the system (determining the more dominant factor is beyond the scope of this paper). we develop and estimate an econometric model to test whether or not had a negative impact on small business lending banking markets in the aftermath of the financial crisis. We use market-level datainclusively. Our paper is one of the few analyses consolidation and small business credit at the market level. literature that studies the effect of bank consolidation on small business lenmarkets. It also adds to the literature on the availability of small business low bank credit supply. Our study has important policy implications. indicating that small businesses located in experienced challenges in accessing bank credit 2008. The empirical results suggest that tconsolidated banking markets in the posteffect of consolidation and market concentration on small business credit seem to be validespecially when there is a general decline in the supply of bank credit. REFERENCES

Avery, Robert B., and Samolyk, Katherine A. 2004. “Bank Consolidation and Small Business

Lending: The Role of Community Banks.” 291–325.

Avery, Robert B., and Samolyk, Katherine A. 2000. “Bank ConsoBanking Services: The Case of Small Commercial Loans.” Corporation Working Paper Series

Berger, Allen N., Bonime, Seth D., Goldberg, Lawrence G., and White, Lawrence J. 2004. “The Dynamics of Market Entry: The Effects of Mergers and Acquisitions on Entry in the Banking Industry.” Journal of Business

Berger, Allen N., Demsetz, Rebecca S., and Strahan, Philip E. 1999. “The Consolidation of the Financial Services IndustrJournal of Banking and Finance

Berger, Allen N., Saunders, Anthony, Scalise, Joseph M., and Udell, Gregory F. 1998. “The Effects of Bank Mergers and Acquisitions on Small Business LenFinancial Economics 50: 187

Berger, Allen N., and Udell, Gregory F. 1995. “Relationship Lending and Lines of Credit in Small Firm Finance.” Journal of Business

Bernanke, Ben S., and Lown, Cara S. 1991. “The Credit CruncEconomic Activity 2: 205

Cole, Rebel. 2010. “Bank Credit, Trade Credit or No Credit: Evidence from the Surveys of Small Business Finances.” US Small Business Administration Office of Advocacy, Banking and

Financial Economic Research

Cole, Rebel. 1998. “The Importance of Relationships to the Availability of Credit.” Banking and Finance 22: 959

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

supply factors are likely to have played a role in declining bank credit financial crisis; however, the latter factor may have been of

particular significance since the crisis had a severe impact on the workings of the (determining the more dominant factor is beyond the scope of this paper).

nometric model to test whether or not market consolidationsmall business lending banking markets in the aftermath of the

level data comprising commercial banks and thrifts from 2004 to 2010Our paper is one of the few analyses looking at the association between

and small business credit at the market level. This study contributes to the the effect of bank consolidation on small business lending in local banking

markets. It also adds to the literature on the availability of small business loans during times of Our study has important policy implications. We find evidence

located in consolidated banking markets are likely to have challenges in accessing bank credit in the aftermath of the financial crisis of

The empirical results suggest that the level of small business lending was lower in more in the post-crisis period. In this respect, concerns over the

market concentration on small business credit seem to be validthere is a general decline in the supply of bank credit.

Avery, Robert B., and Samolyk, Katherine A. 2004. “Bank Consolidation and Small Business Lending: The Role of Community Banks.” Journal of Financial Services Research

Avery, Robert B., and Samolyk, Katherine A. 2000. “Bank Consolidation and the Provision of Banking Services: The Case of Small Commercial Loans.” Federal Deposit Insurance

Corporation Working Paper Series 00-01.

Berger, Allen N., Bonime, Seth D., Goldberg, Lawrence G., and White, Lawrence J. 2004. “The Dynamics of Market Entry: The Effects of Mergers and Acquisitions on Entry in the

Journal of Business 77: 797–834. Berger, Allen N., Demsetz, Rebecca S., and Strahan, Philip E. 1999. “The Consolidation of the

Financial Services Industry: Causes, Consequences, and Implications for the Future.” Journal of Banking and Finance 23: 135–194.

Berger, Allen N., Saunders, Anthony, Scalise, Joseph M., and Udell, Gregory F. 1998. “The Effects of Bank Mergers and Acquisitions on Small Business Lending.” Journal of

50: 187–229. Berger, Allen N., and Udell, Gregory F. 1995. “Relationship Lending and Lines of Credit in

Journal of Business 68: 351–381. Bernanke, Ben S., and Lown, Cara S. 1991. “The Credit Crunch.” Brookings Papers on

2: 205–247. Bank Credit, Trade Credit or No Credit: Evidence from the Surveys of Small

Small Business Administration Office of Advocacy, Banking and

Financial Economic Research (June). Cole, Rebel. 1998. “The Importance of Relationships to the Availability of Credit.”

22: 959–977.

Journal of Finance and Accountancy

2008 financial crisis, 9

supply factors are likely to have played a role in declining bank credit the latter factor may have been of

workings of the US banking (determining the more dominant factor is beyond the scope of this paper). In this study,

consolidation has small business lending banking markets in the aftermath of the

comprising commercial banks and thrifts from 2004 to 2010, looking at the association between

contributes to the ding in local banking

during times of e find evidence

are likely to have in the aftermath of the financial crisis of 2007–

level of small business lending was lower in more concerns over the adverse

market concentration on small business credit seem to be valid,

Avery, Robert B., and Samolyk, Katherine A. 2004. “Bank Consolidation and Small Business Journal of Financial Services Research 25:

lidation and the Provision of Federal Deposit Insurance

Berger, Allen N., Bonime, Seth D., Goldberg, Lawrence G., and White, Lawrence J. 2004. “The Dynamics of Market Entry: The Effects of Mergers and Acquisitions on Entry in the

Berger, Allen N., Demsetz, Rebecca S., and Strahan, Philip E. 1999. “The Consolidation of the y: Causes, Consequences, and Implications for the Future.”

Berger, Allen N., Saunders, Anthony, Scalise, Joseph M., and Udell, Gregory F. 1998. “The Journal of

Berger, Allen N., and Udell, Gregory F. 1995. “Relationship Lending and Lines of Credit in

Brookings Papers on

Bank Credit, Trade Credit or No Credit: Evidence from the Surveys of Small Small Business Administration Office of Advocacy, Banking and

Cole, Rebel. 1998. “The Importance of Relationships to the Availability of Credit.” Journal of

“CSI: Credit Crunch.” 2007. Economist

DeYoung, R., Goldberg, L. G., and Banks: Credit Availability to Small Business in an Era of Banking Consolidation.” Journal of Banking and Finance

Di Leo, Luca, and Zibel, Alan. 2011. “Bernanke: US Economy Looks Better, for Small Firms.” Wall Street Journal

Haynes, George W., and Williams, Victoria. 2011. “Lending by Depository Lenders to Small Businesses, 2003 to 2010.” Banking and Financial Economic Research

Haynes, George W., and Williams, Victoria. 2011. “Small Business Lending in the United States, 2009–2010.” US Small Business Administration Office of Advocacy Banking Study

2010 (February). (b) Haynes, George W., and Williams, Victoria. 2010. “Small Business and Micro Business Lending

for Data Years 2008–2009” Banking Study 2009 (January).

Haynes, George W., and Brown, James R. 2009. “How Strong Is Finance and Small Firm Growth? Evidence from the Survey of Small Business Finances.” US Small Business Administration Office of Advocacy, Banking and Financial

Economic Research (July).Ivashina, Victoria, and Scharfstein, Davi

2008.” Journal of Financial Economics

Keeton, William R. 1996. “Do Bank Mergers Reduce Lending to Businesses and Farmers? New Evidence from Tenth District States.” Review Q III: 63–75.

Keeton, W. R. 1995. “Multi-Office Bank Lending to Small Businesses: Some New Evidence.” Federal Reserve Bank of Kansas City, Economic Review

Kwast, M., Starr-McClure, M., and Wolken, J. 1997. “Mark Antitrust in Banking.” Antitrust Bulletin

Maltby, Emily. “The Credit Crunch That Won’t Go Away: Forget the Improving Economy, Entrepreneurs Still Find It Hard to Get Loans; Here’sWe May Get Out of It.” Wall Street Journal

Peek, J., and Rosengren, E. S. 1998. “Bank Consolidation and Small Business Lending: It’s Not Just Size That Matters.” Journal of Banking and Finance

Peterson, Mitchell A., and Rajan, Raghuram G. 1994. “The Benefits of Lending Relationships: Evidence from Small Business Data.”

Samolyk, Katherine A., and Richardson, Christopher, A. 2003. “Bank Consolidation and Small Business Lending Within Local Markets.” Working Paper Series 03

Scott, Jonathan A. 2004. “Small Businesses and the Value of Community Financial Institutions.” Journal of Financial Services Research

Strahan, Philip E., and Weston, James P. 1998. “Small Business Lending and the Changing Structure of the Banking Industry.”

Udell, Gregory F. 2009. “How Will a Credit Crunch Affect Small Business Finance?” Reserve Bank of San Francisco, Economic Letter

US Census Bureau. “Statistics of U.S. Businesses.” Available from <http://www.census.gov/econ/susb/>.

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

Economist (20 October): 385. DeYoung, R., Goldberg, L. G., and White, L. J. 1999. “Youth, Adolescence and Maturity of

Banks: Credit Availability to Small Business in an Era of Banking Consolidation.” Journal of Banking and Finance 23: 463–492.

Di Leo, Luca, and Zibel, Alan. 2011. “Bernanke: US Economy Looks Better, but More Needed Wall Street Journal (13 January).

Haynes, George W., and Williams, Victoria. 2011. “Lending by Depository Lenders to Small Businesses, 2003 to 2010.” US Small Business Administration Office of Advocacy,

Banking and Financial Economic Research (March). (a) Haynes, George W., and Williams, Victoria. 2011. “Small Business Lending in the United

Small Business Administration Office of Advocacy Banking Study

George W., and Williams, Victoria. 2010. “Small Business and Micro Business Lending 2009” US Small Business Administration Office of Advocacy

(January). Haynes, George W., and Brown, James R. 2009. “How Strong Is the Link Between Internal

Finance and Small Firm Growth? Evidence from the Survey of Small Business Small Business Administration Office of Advocacy, Banking and Financial

(July). Ivashina, Victoria, and Scharfstein, David. 2010. “Bank Lending During the Financial Crisis of

Journal of Financial Economics 97: 319–338. Keeton, William R. 1996. “Do Bank Mergers Reduce Lending to Businesses and Farmers? New

Evidence from Tenth District States.” Federal Reserve Bank of Kansas City, Economic

Office Bank Lending to Small Businesses: Some New Evidence.” Federal Reserve Bank of Kansas City, Economic Review Q II, 46–57.

McClure, M., and Wolken, J. 1997. “Market Definition and the Analysis of Antitrust Bulletin 42: 973–995.

Maltby, Emily. “The Credit Crunch That Won’t Go Away: Forget the Improving Economy, Entrepreneurs Still Find It Hard to Get Loans; Here’s Why We’re in This Mess and How

Wall Street Journal. 21 June 2010. Peek, J., and Rosengren, E. S. 1998. “Bank Consolidation and Small Business Lending: It’s Not

Journal of Banking and Finance 22:799–819. eterson, Mitchell A., and Rajan, Raghuram G. 1994. “The Benefits of Lending Relationships:

Evidence from Small Business Data.” Journal of Finance 49: 3–37. Samolyk, Katherine A., and Richardson, Christopher, A. 2003. “Bank Consolidation and Small

s Lending Within Local Markets.” Federal Deposit Insurance Corporation

03-02.

Scott, Jonathan A. 2004. “Small Businesses and the Value of Community Financial Institutions.” Journal of Financial Services Research 25: 207–230.

n, Philip E., and Weston, James P. 1998. “Small Business Lending and the Changing Structure of the Banking Industry.” Journal of Banking and Finance 22: 821

Udell, Gregory F. 2009. “How Will a Credit Crunch Affect Small Business Finance?” serve Bank of San Francisco, Economic Letter 2009–09.

“Statistics of U.S. Businesses.” Available from <http://www.census.gov/econ/susb/>.

Journal of Finance and Accountancy

2008 financial crisis, 10

White, L. J. 1999. “Youth, Adolescence and Maturity of Banks: Credit Availability to Small Business in an Era of Banking Consolidation.”

but More Needed

Haynes, George W., and Williams, Victoria. 2011. “Lending by Depository Lenders to Small Small Business Administration Office of Advocacy,

Haynes, George W., and Williams, Victoria. 2011. “Small Business Lending in the United Small Business Administration Office of Advocacy Banking Study

George W., and Williams, Victoria. 2010. “Small Business and Micro Business Lending Small Business Administration Office of Advocacy

the Link Between Internal Finance and Small Firm Growth? Evidence from the Survey of Small Business

Small Business Administration Office of Advocacy, Banking and Financial

d. 2010. “Bank Lending During the Financial Crisis of

Keeton, William R. 1996. “Do Bank Mergers Reduce Lending to Businesses and Farmers? New Kansas City, Economic

Office Bank Lending to Small Businesses: Some New Evidence.”

et Definition and the Analysis of

Maltby, Emily. “The Credit Crunch That Won’t Go Away: Forget the Improving Economy, Why We’re in This Mess and How

Peek, J., and Rosengren, E. S. 1998. “Bank Consolidation and Small Business Lending: It’s Not

eterson, Mitchell A., and Rajan, Raghuram G. 1994. “The Benefits of Lending Relationships:

Samolyk, Katherine A., and Richardson, Christopher, A. 2003. “Bank Consolidation and Small Federal Deposit Insurance Corporation

Scott, Jonathan A. 2004. “Small Businesses and the Value of Community Financial Institutions.”

n, Philip E., and Weston, James P. 1998. “Small Business Lending and the Changing 22: 821–845.

Udell, Gregory F. 2009. “How Will a Credit Crunch Affect Small Business Finance?” Federal

US Small Business AdministrationPresident.” Available from <http://www.sba.gov/sites/default/files/sb_econ2010.pdf>.

US Small Business AdministrationPresident.” Available from <http://www.sba.gov/sites/default/files/Small_Business_Ec

US Small Business Administration<http://www.sba.gov/advocacy/7495>.

Wooldridge, Jeffrey, M. 2000. Introductory Econometrics: A Modern Approach

South-Western College Publishing.

APPENDIX

Figure 1. Average small business lending in banking

300,000

600,000

900,000

1,200,000

1,500,000

2004 2005

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

US Small Business Administration. 2010. “The Small Business Economy 2010: A Report to the ident.” Available from <http://www.sba.gov/sites/default/files/sb_econ2010.pdf>.

US Small Business Administration. 2009. “The Small Business Economy 2009: A Report to the President.” Available from

http://www.sba.gov/sites/default/files/Small_Business_Economy_2009.pdf>US Small Business Administration. “Research and Statistics.” Available from

<http://www.sba.gov/advocacy/7495>. Introductory Econometrics: A Modern Approach. Mason, OH:

Western College Publishing.

Figure 1. Average small business lending in banking markets by loan type

2006 2007 2008 2009 2010

Total SBL

CRE

CI

Journal of Finance and Accountancy

2008 financial crisis, 11

. 2010. “The Small Business Economy 2010: A Report to the ident.” Available from <http://www.sba.gov/sites/default/files/sb_econ2010.pdf>.

. 2009. “The Small Business Economy 2009: A Report to the

onomy_2009.pdf>.

. Mason, OH:

markets by loan type

Total SBL

CRE

CI

Table 1. Description of variablesVariable name Description

TSBL Sum of commercial real estate loansunder $1 million

CRE Commercial real estate loans CI Commercial and industrial loans POST Equals 0 for observations from the years 200

observations from THREE Three-firm concentration ratio measuring the deposit market share

of the three largest institutionsOFFICE Number of bank offices in a marketDEPOINS Deposits per institution in a market

in a market / number of instiHOLD Market share of institutions operating under a multibank holding

company (%)OFFRATIO Market average of (number of offices

total offices) ROA Market average of return on assets (%)CAPRATIO Market average of core capital ratio (%)UNEMP Unemployment rate

Table 2. Descriptive statistics

TSBL CRE CI POST THREE OFFICE DEPOINS HOLD OFFRATIO ROA CAPRATIO UNEMP n

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

ariables Description

commercial real estate loans, and commercial and industrial loans under $1 million (in 1000s)

ommercial real estate loans under $1 million (in 1000s) ommercial and industrial loans under $1 million (in 1000s)

for observations from the years 2004–2007 and 1 for observations from 2008 through 2010

firm concentration ratio measuring the deposit market share of the three largest institutions (%) Number of bank offices in a market Deposits per institution in a market (in 1000s) (amount of deposits in a market / number of institutions in a market) Market share of institutions operating under a multibank holding company (%) Market average of (number of offices of a bank in a market / the bank’s total offices) (%) Market average of return on assets (%) Market average of core capital ratio (%)

nemployment rate in a market (%)

Table 2. Descriptive statistics

2004–2007 2008–2010 Mean Std. Dev. Mean Std. Dev.

1,187,834 3,421,957 1,238,771 3,622,725 679,304 1,941,609 687,733 2,013,898 508,530 1,485,247 551,038 1,612,577

0 0 1 0 63.68 18.67 63.68 17.97

147.07 368.54 158.62 399.70 325,296 470,305 308,605 458,238

45.66 17.48 54.70 19.61 16.31 13.93 16.79 14.08 1.22 0.35 -0.06 0.85 9.34 2.11 9.24 1.41 7.17 2.49 12.08 4.08 184 138

Journal of Finance and Accountancy

2008 financial crisis, 12

commercial and industrial loans

and 1 for

firm concentration ratio measuring the deposit market share

(amount of deposits

Market share of institutions operating under a multibank holding

the bank’s

Table 3. Effects of market consolidation TSBL

Coefficient

Intercept 3.818*** POST 0.648*** THREE -0.140 POSTxTHREE -0.157*** OFFICE 1.312*** DEPOINS 0.394*** HOLD -0.002** OFFRATIO 0.005** ROA -0.040*** CAPRATIO -0.010* UNEMP -0.160*** F-statistic 28.42 p-value <0.01*** R2 (with-in) 0.5165 n 322 # of groups 46

***, **, and * denote 1%, 5%, and 10% significance, respectively.

Journal of Finance and Accountancy

The 2007–2008 financial crisis,

consolidation on small business lending

TSBL CRE Std. Error Coefficient Std. Error Coefficient

0.850 4.415*** 0.981 1.301 0.240 0.572** 0.277 0.831***0.167 -0.165 0.193 -0.0830.057 -0.143** 0.066 -0.194***0.137 1.297*** 0.158 1.367***0.080 0.317*** 0.092 0.487***0.001 -0.003*** 0.001 -0.0010.002 0.007** 0.003 0.001 0.014 -0.044*** 0.016 -0.030**0.006 -0.010 0.007 -0.0090.047 -0.161*** 0.054 -0.166***

22.44 24.78 <0.01*** <0.01*** 0.4575 0.4823 322 322 46 46

5%, and 10% significance, respectively.

Journal of Finance and Accountancy

2008 financial crisis, 13

CI Coefficient Std. Error

0.909 0.831*** 0.257

0.083 0.179 0.194*** 0.061 1.367*** 0.146 0.487*** 0.085

0.001 0.001 0.003

0.030** 0.014 0.009 0.006

0.166*** 0.050

<0.01*** 0.4823