Thai Oil Public Company Limited Oil’s Businesses The majority of refined petroleum products are...

83

Thai Oil Public Company Limited Presentation to Investors March 2015

Transcript of Thai Oil Public Company Limited Oil’s Businesses The majority of refined petroleum products are...

Thai Oil Public Company Limited

Presentation to Investors

March 2015

-2-

Disclaimer

The information contained in this presentation is intended

solely for your personal reference. Please do not circulate this

material. If you are not an intended recipient, you must not

read, disclose, copy, retain, distribute or take any action in

reliance upon it.

-3-

VISION A LEADING FULLY INTEGRATED REFINING & PETROCHEMICAL

COMPANY IN ASIA PACIFIC

MISSION

• To be in top quartile on performance and return on investment

• To create a high-performance organization that promotes

teamwork, innovation and trust for sustainability

• To emphasis good Corporate Governance and commit to Corporate

Social Responsibility

VALUES

Corporate Vision, Mission and Values

Professionalism

Ownership & Commitment

Social Responsibility Integrity Teamwork & Collaboration Initiative

Vision Focus

Excellent Striving

-4-

Corporate Governance Policy

Corporate Governance Policy

The board of directors, management

and all staff shall commit to moral

principles, equitable treatment to all

stakeholders and perform their duties for

the company’s interest with dedication,

integrity, and transparency.

Roles and Responsibilities for

Stakeholders

• Truthfully report company’s situation and

future trends to all stakeholders equally

on a timely manner.

• Shall not exploit the confidential

information for the benefit of related

parties or personal gains.

• Shall not disclose any confidential

information to external parties.

CG Channels

Should you discover any

ethical wrongdoing that is

not compliance to CG policies

or any activity that could

harm the Company’s interest,

please inform:

Corporate Management Office Thai Oil Public Company Limited 555/1 Energy Complex Building A

11F, Vibhavadi Rangsit Road,

Chatuchak, Bangkok 10900

[email protected] http://www.thaioilgroup.com

+66-0-2797-2999 ext. 7312-5

+66-0-2797-2973

-5-

Thaioil Group Sustainable Development

Member of DJSI Emerging Markets for 2 consecutive years • Highest Ranked Level in RobecoSAM Gold Class of Global Oil & Gas Companies • No.1 in ENERGY industry around the WORLD (Industry Group Leader) • No.1 in Oil & Gas Producers Worldwide (Industry Leader)

-6-

Presentation Agenda

TOP GROUP BUSINESS OVERVIEW

KEY FINANCIAL HIGHLIGHT

STRATEGIC INVESTMENT PLAN

MARKET OUTLOOK

KEY TAKE AWAY MESSAGES

APPENDIX

Q4 & FY/14 PERFORMANCE ANALYSIS

GLOBAL REFINERY MARGINS / INVENTORY / THAILAND PETROLEUM DEMAND

-7-

TOP Group Business Overview

-8-

Strategic Relationship and Operational Integration with PTT

Thai Oil’s strong shareholder base

49.1%

25.1%

20.3%

5.5%

PTT

Foreign Investors

Local Investors

NVDR

• Benefits from PTT’s dual role as our major shareholder and key business partner

• All transactions take place at arm’s length and in adherence with strong corporate governance principles

Key strategic benefits for Thai Oil

1. Long-term strategic partnership

• Thai Oil is PTT’s principal refiner

• Long-term strategic shareholder and joint investment

2. Business partnership

• Product offtake • Crude procurement

3. Operational synergies

• Freight costs reduction • Knowledge transfer and shared

services • Close management collaboration

and secondment of trained staff

49.1%

As of 27 Feb 2015

-9-

TOP Group Synergy & Strategic Role in PTT Group Value Chain

NATURAL GAS

CRUDE IMPORT

Mixed-Xylene

Solvent

Toluene

Pentane

Hexane

SOLVENTS

TP provides electricity and steam to Thai Oil, TLB and TPX and sells its remaining power to the national grid

Paraxylene

Benzene

Mixed-Xylene

Toluene

AROMATICS

Lube Base Oil

Bitumen

TDAE

Slack Wax

Extract

LUBE BASE

REFINERY LPG

Fuel Oil

Diesel

Gasoline

Jet/Kero

PLATFORMATE

LONG RESIDUE

REFINED PETROLEUM

POWER

Diversifying to a broad

range of downstream

products to enjoy higher

profit margins and

reduce earnings

volatility

Thai Oil’s Businesses

The majority of refined petroleum products are sold domestically to PTT

PTT is our principal domestic customer for our lube base products

Upstream Intermediate Downstream

-10-

Key Milestones: 53 Years, A Long Track Record of Success

2007 • Increased refining capacity to 275 kbd 2008 • The first refinery in Thailand with diesel

production to comply with the sulfur content requirements of Euro IV

• Capacity expansion of Thai Paraxylene with total aromatics capacity of 900,000 tons p.a.

• Invested in Solvents business in Thailand and Vietnam

1993 • We expanded our refining capacity to 190 kbd

1994 – 1997 • Increased total refining capacity to 220 kbd • Initial investment in Thai Paraxylene (“TPX”) and

Thai Lube Base (“TLB”) • IPT became the first IPP to enter into a PPA with

EGAT2 with 700 MW capacity ; separately, Thaioil Power (“TP”) constructed the power generation plant under the SPP with 118 MW capacity

1961 – 1997 Capacity expansion and initial stage of

business diversification

2004 – 2011 Listing, expansion and

diversification

Today A leading integrated refining and

petrochemical group in Asia Pacific

• 275 kbd refinery ( approximately 25% of Thailand’s total refining capacity)

• Nelson index 9.71 • Diversified business through 13

subsidiaries • The 3rd largest listed company by revenue in Thailand

1961 – 1964

2004

1961 • Incorporated

1964 • Commenced

operation with distillation capacity of 35 kbd

• Simple refinery with Nelson complexity Index ~ 41

1970 • Refining capacity

expanded to 65 kbpd

1989 • Increased refining

capacity to 90 kbpd

2004 • IPO and listed on the SET • Acquired remaining shares in

Thai Paraxylene and Thai Lube Base which became our wholly-owned subsidiaries

2007 -2008

2010

2011

1993-1997

1970-1989

2013 • Established LABIX to

produce LAB • Invested in power biz

via GPSC • TOP SPP for 239 MW • Revenue 414,599 MB • Net profit 10,394 MB

2011 • 1st refinery in the Asia-

Pacific region to manufacture diesel and ULG in compliance with the sulfur and BZ aromatics content requirements of the Euro IV

• Acquired 1st VLCC

2010 • Established

Thaioil Ethanol • Production

expansion of TDAE by 50,000 tons per annum

Note 1. Based on our internal estimates using the methodology of the Nelson Complexity Index 2. The Electricity Generating Authority of Thailand (“EGAT”) is the national grid

2013

-11-

Thai Oil Group Business Structure

40% 34% 15% 10% Refinery Aromatics Lube Base Others

• 4 Oil & Chemical Tankers Capacity : 51,250 DWT

• Crude Tankers: 3VLCCs Capacity: 881,500 DWT

• 11 crew & utility boats (120 DWT each)

• 2 Large vessels for crude, feedstock & product storage and transportation services

Capacity: 200,000 DWT • Ship management services

9.2 %

Principal power plant of PTT capacity 1,038 MW of electricity 1,340 tons/hour of steam Total aggregate capacity 1,357 MW

Platformate 1.8 million tons/annum

PTT Group 80.0%

100.0% 100.0% 74.0% 100.0%

Thaioil (TOP) Thai Lube Base

(TLB) Thaioil Power

(TP)

Global Power Synergy Company Limited

Thaioil Energy Services (TES)

Thaioil Marine (TM)

Maesod Clean Energy (MCE)

Capacity : 275,000 barrels/day Small Power Producer

Program 3-on-1 Combined Cycle Electricity 118 MW Steam 168 tons/hour

PTT 26.0%

Proceeds the business on various professional of management services

Sugarcane Based Ethanol Capacity : 230,000 lts/day

PTT 30.1%

Thaioil 11.9%

TP 27.7%

Padaeng 35.0%

Mitr Phol 35.0%

100.0%

Thappline (THAP)

Multi-product Pipeline Capacity:26,000 m.lts/y

20.0%

PTT 40.4%

Others 50.4%

Lube Base Oil Capacity : Base Oil 267,015 tons/annum Bitumen 350,000 tons/annum TDAE 67,520 tons/annum

Thaioil Solvent

Through TOP Solvent (TS)

100.0%

100.0%

Thaioil Ethanol (TET)

Capacity : 141,000 tons/annum

Thai Paraxylene (TPX)

100.0% 80.5%

Solvent distribute in Thailand

Sak Chaisidhi (SAKC)

Top Solvent Vietnam

Solvent distribute in Vietnam

PTT ICT Solutions (PTT ICT)

Sapthip (SAP) Cassava Based Ethanol Capacity : 200,000 lts/day

50.0%

Ubon Bio Ethanol (UBE) 21.3%

Cassava/Molasses Based Plant Capacity : 400,000 lts/day

100%

PTT Energy Solutions (PTTES)

Provides engineering technique consulting services

20.0% PTT 40.0%

PTTGC 20.0% IRPC 20.0%

BCP 21.3% Others 57.4%

PTTGC 30.3%

30.0%

Aromatics Capacity: Paraxylene 527,000 tons/annum Mixed Xylene 52,000 tons/annum Benzene 259,000 tons/annum Total 838,000 tons/annum

LABIX Company Limited (LABIX)

LAB producer and distributor Capacity: 100 KTA COD: 2015

Mitsui 25.0% 75.0% TOP SPP Company

Limited

2 Small Power Producers Total capacity: 239 MW COD 2016

100.0%

Sells Electricity/Steam to Group

Net Profit Contribution

(Avg. from 2006 – 2014)

-12-

Process Linkage: Beauty of Integration

Thai Paraxylene

Thai Lube Base

PROCESS FLOWCHART

JET

ULG91

LPG

ULG95

KEROSENE

CDU-1

45,000

CDU-2

50,000

CDU-3

165,000

MX

AGO

DIESEL

FUEL OIL

BITUMEN

SULPHUR

HVU-1

HVU-2

HVU-3

95,000

FUELGAS

BBU

1,800

ADIP

TCU

19,000

FCCU

10,400

HCU-

1 HCU 2

50,000

SRU-1/2

SRU-3/4

2x210

KMT-1

KMT-2

HMU-1

HDT-1

HDT-2

HDT-3

85,000

HMU-2

140TH2

HDS-2

HDS-3

75,000

MX

40,000

CCR-1

CCR-2

50,000

ISOM

20,000

ADIP

Thai Oil

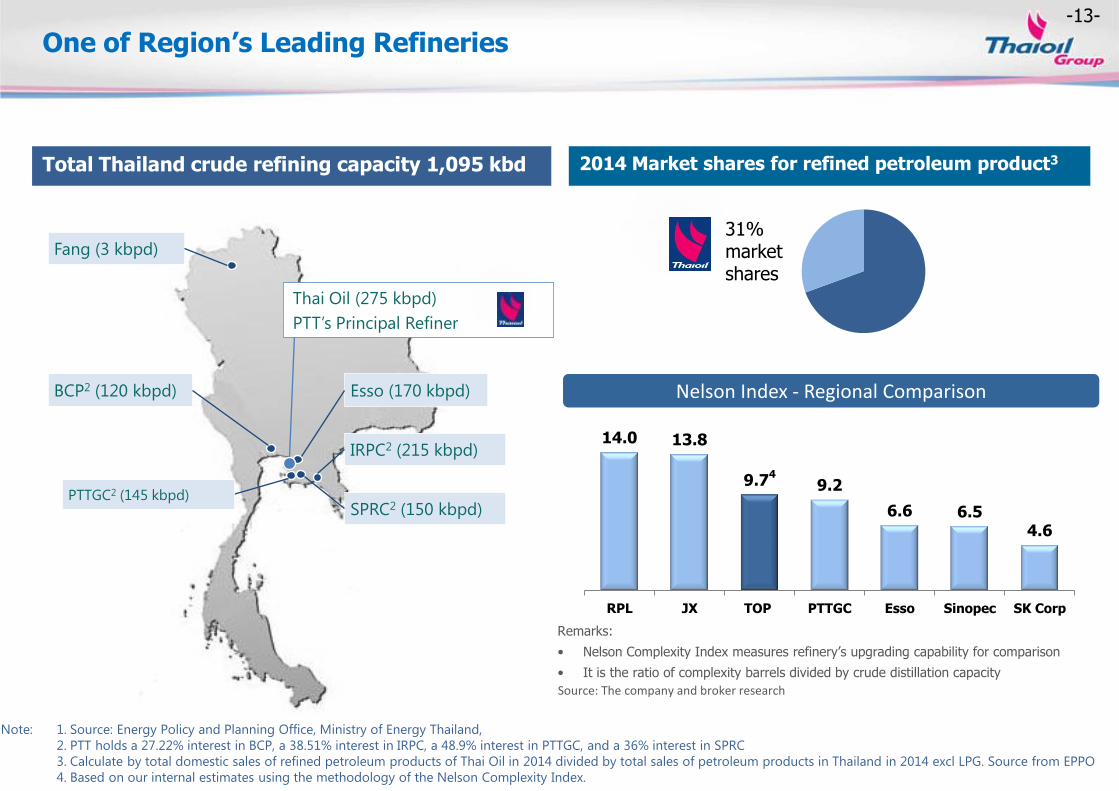

-13-

Total Thailand crude refining capacity 1,095 kbd 2014 Market shares for refined petroleum product3

One of Region’s Leading Refineries

Thai Oil (275 kbpd)

PTT’s Principal Refiner

Esso (170 kbpd)

IRPC2 (215 kbpd)

SPRC2 (150 kbpd)

BCP2 (120 kbpd)

Fang (3 kbpd)

Remarks:

• Nelson Complexity Index measures refinery’s upgrading capability for comparison

• It is the ratio of complexity barrels divided by crude distillation capacity

14.0 13.8

9.74 9.2

6.6 6.5 4.6

RPL JX TOP PTTGC Esso Sinopec SK Corp

Source: The company and broker research

Nelson Index - Regional Comparison

31% market shares

Note: 1. Source: Energy Policy and Planning Office, Ministry of Energy Thailand,

2. PTT holds a 27.22% interest in BCP, a 38.51% interest in IRPC, a 48.9% interest in PTTGC, and a 36% interest in SPRC

3. Calculate by total domestic sales of refined petroleum products of Thai Oil in 2014 divided by total sales of petroleum products in Thailand in 2014 excl LPG. Source from EPPO

4. Based on our internal estimates using the methodology of the Nelson Complexity Index.

PTTGC2 (145 kbpd)

-14-

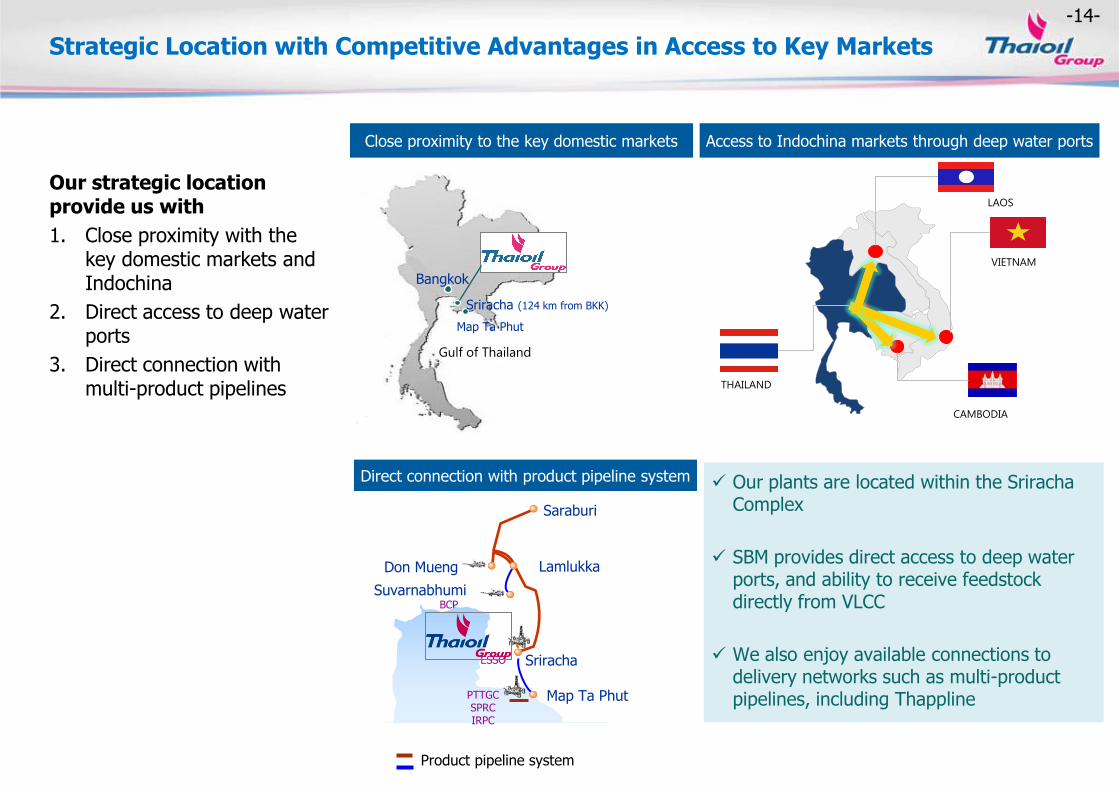

Strategic Location with Competitive Advantages in Access to Key Markets

Our strategic location provide us with

1. Close proximity with the key domestic markets and Indochina

2. Direct access to deep water ports

3. Direct connection with multi-product pipelines

Our plants are located within the Sriracha Complex

SBM provides direct access to deep water ports, and ability to receive feedstock directly from VLCC

We also enjoy available connections to delivery networks such as multi-product pipelines, including Thappline

Ø24”, 134 km

Saraburi

Lamlukka Don Mueng

Suvarnabhumi

ESSO

PTTGC SPRC IRPC

Map Ta Phut

Sriracha

BCP

Product pipeline system

Direct connection with product pipeline system

Access to Indochina markets through deep water ports

Close proximity to the key domestic markets

Bangkok

Map Ta Phut

Gulf of Thailand

Sriracha (124 km from BKK)

THAILAND

LAOS

VIETNAM

CAMBODIA

-15-

Optimized & Flexible Operations…Superior Performance

72%

9%

8%

11%

9%

38%

20%

16%

13%

4%

4%

41%

11%

17%

27%

27% 13% 7%

32%

29% 32%

41% 58% 61%

Oman Dubai Murban

Short Residue Waxy Gas/Distillates

Far East

Local

Middle East

Sources of Crude

FY/14

1

Spread over Dubai (US$/bbl)

-35.6

15.9

16.1

-8.3

14.3

Others

18.3

• Flexibility in crude intake allows diversification of crude types to source cheaper crude

• Flexibility in product outputs by maximizing middle distillates (jet and diesel) by adjusting production mode to capture domestic demand and price premium

• Maximize Platformate production to capture higher margin on aromatics

• Minimize fuel oil output to avoid lower margin products

1.LPG price = 76% CP + 24%*333 $/ton

LPG

PLATFORMATE

GASOLINE

JET

DIESEL

FUEL OIL

Product output

Domestic demand for

petroleum products*

*Source: Energy Policy and Planning Office, Ministry of Energy Thailand

FY/14

% S = 0.79 API = 39.7

% S = 1.54 API = 31.2

% S = 2.13 API = 30.4

Crude Assays based on TOP configuration

Thai Oil is able to diversify its type of crude intake and product outputs to maximize demand and margin

-16-

84% 81% 83%

16% 19% 17%

FY/13 Q4/14 FY/14

Export

Domestic

Strong Domestic Sales despite Flatten Local Demand

Refinery Intake (KBD)

280

TOP’s Domestic & Export Sales Sales breakdown by customers

38%

12% 7%

1%

23%

17% 2%

Domestic Jobbers

Q4/14

Sales

Breakdown

Export 19%

296 269

38%

13% 9%

2%

22%

15% 2%

Domestic Jobbers

FY/14

Sales

Breakdown

Export 17%

686 694 640 689 724 698 667 700 732 706 668 706 698 701

92% 88% 85%

89% 93%

89% 92% 92% 86% 85% 85%

92% 92% 87%

0%

20%

40%

60%

80%

100%

-

200

400

600

800

1,000

1,200

Domestic Demand/Sales Net Export Others Utilization Rate

Domestic Oil Demand / Domestic Refinery Intake Domestic Oil Demand

KBD

Utilization = 98%

including LPG from refinery only

*

*including TOP intake (Excluding TOP = 65%)

0

200

400

600

800

1,000

LPG Mogas Jet/Kero Diesel Fuel Oil Total Demand

2013 2014 KBD

-0.2% +3.8% -1.0%

0.9%

-3.9%

0.6%

-17-

Competitive Performance Benchmarking

Shell Global Solutions International (SGSi) Solomon (Bi-Annually)

2012

2010

Operational Performance Review

Hydrocarbon Management Review

Operational Troubleshooting

Staff Competency Development

Knowledge Management & Research

-18-

Thailand’s largest and

one of the region’s

most advanced and

competitive refineries 1 Strategic relationship

and operational

integration with PTT as

the Group’s principal

refiner

3

Technological

superiority, logistical

advantages & cost

leadership

6

Industry with high

barriers to entry and

strong market

positioning

5 Strategic location with

competitive advantages

in access to key markets

4

Diversified earnings

through integration

with, and significant

contribution from, our

subsidiaries

2

Highly experienced

management team

7 Strong financial profile

8

TOP Group Key Highlights

-19-

Key Financial Highlights

-20-

2014 Key Industry Highlights

Implication

4.5 $/bbl inventory loss (from stock gain 0.8 to stock loss 4.5 $/bbl Y/Y)

Improved market GRM (from 4.3 to 5.7 $/bbl Y/Y)

$48/bbl drop in Dubai crude price pressured by ample supply ,while demand remains soft

Benefits from crude price collapse (i.e. lower refinery fuel & loss / crude premium) supports GRM

Refinery

Aromatic

Base Oil

Pressured Aromatic Margins (GIM contribution from 1.8 to 0.1 $/bbl Y/Y)

PX oversupply from new capacities and slowdown in Chinese polyester / PTA demand pressured margins

Soften Base Oil margins (GIM contribution from 0.9 to 0.7 $/bbl Y/Y)

More competition from Gr II/III, while sharp drop in HSFO supported margins

Refinery + Aromatics + Base Oil

$/BBL 2014 2013

Market GIM 6.2 6.8

Stock Gains / (Loss) -4.3 0.8

Accounting GIM 1.9 7.6

-21-

2014 Key Events/Achievements & TOP Group Net Profit

Key Events / Achievements 2014

Completion of CDU-3 Turnaround 9 days earlier than plan (46 vs 55 day)

Successful COD of key margin improvement products i.e. HVU-2 revamp, CDU-3 Preheat Train

Active commodities hedging resulting in gains of 2,218 MB

Maintain strong credit rating profile by all 3 agencies

Oil & Gas Industry Leader for sustainability, only Thai Company for Gold Class for 2 consecutive yr (announce as of 19 Jan 2015)

Implementing Profit Recovery Plan

2,115 5,773 7,621 6,692

(3,637)

(10,454) (14,439)

2,624

(653)

(1,798)

(2,451)

5,243

NP w/o Stock G/L Stock G/(L) LCM Additional benefits

Top Group Net Profit

Unit : million THB

Q4/14

Excluding tax

(6,479) MB

Q3/14

(2,175) MB

FY/14

(4,026) MB

FY/13

9,316* MB

Including (tax expense) /reversal

12,864 MB

-22-

FY/14 Success on TOP Profit Recovery Program

Hydrocarbon / Supply Chain & Commercial Management save 0.57 US$/bbl

Commodities Hedging (both crack spread & Inventory)

2. Profit Recovery Program

1,102 MB

5,243 Million Baht Success from Margin Improvement / Profit Recovery Program / Risk Management

OPEX & Cost Management , Supply & Marketing Initiatives

1,923 MB 2,218 MB

Less CDU-3 Maintenance time HVU-2 Revamp CDU-3 Preheat Train Alternative feedstock to TLB

More specialty product sale (TLB) Optimize Gasoline Export (upgrade low value component) Negotiate on Insurance Premium

-23-

Integrated Margin & Competitive Cash Cost

6.4

1.1

3.3 4.6

5.3

4.3

8.2

5.7

2.2 3.4

4.1

6.2

4.5 5.1

(3.5)

1.2

2008 2009 2010 2011 2012 2013 Q4/14 2014

6.1 2.6

1.1 2.9 3.1 3.9 4.4

5.9 5.1 4.3 4.1 4.9 7.9

(3.3)

5.4

1.1

1.1

1.1 2.6

2.6 1.5 1.5 2.1

2.1 1.7

1.7 1.8 1.8

(0.3)

(0.3)

0.1

0.1

0.7

0.7 0.7

0.7 1.0

1.0

1.3 1.3

0.9 0.9 0.9

0.9 0.4

0.4

0.7

0.7

7.9

4.3 5.6

7.8 7.6 6.8

8.0 6.2

4.3 6.1 6.3

9.3

6.9 7.6

(3.2)

1.9

2008 2009 2010 2011 2012 2013 Q4/14 2014

TOP TPX TLB

(Unit: US$/bbl)

Marketing GIM Accounting GIM (Marketing GIM + Stock G/L)

Marketing GRM Accounting GRM (Marketing GRM + Stock G/L)

Gross Refining Margin

Gross Integrated Margin

(Unit: US$/bbl)

0.9 0.9 1.0 1.1 1.2 1.4 1.7 1.6 0.4 0.5 0.5 0.4 0.4 0.7 0.7 0.8 1.4 1.4 1.5 1.5 1.6 2.1 2.4 2.4

2008 2009 2010 2011 2012 2013 Q4/14 2014

Operating Cost Interest Expense (Net)

1.1 1.1 1.2 1.4 1.5 1.7 1.9 1.8 0.5 0.5 0.5 0.4 0.4 0.6 0.7 0.7 1.6 1.7 1.8 1.8 1.9 2.3 2.6 2.5

2008 2009 2010 2011 2012 2013 Q4/14 2014

Operating Cost Interest Expense (Net)

Refinery’s Cash Cost

(Unit: US$/bbl)

Group’s Cash Cost

(Unit: US$/bbl)

*Including MTA cost in MTA period since mid Jun-late July 2014 for 46 days (TOP MTA cost in 2014 = 436 MB)

*

*Including MTA cost in MTA period since mid Jun-late July 2014 for 46 days ( TOP group MTA cost in 2014 = 609 MB)

*

*Including MTA cost 0.14 $/bbl

*Including MTA cost 0.20 $/bbl

-24-

Financial Performance

2,157

14,035

10,349

13,753

16,946

3,801 5,767

2008 2009 2010 2011 2012 2013 2014

22,897

12,846 14,585

23,868 22,808

19,713

6,880

19,541

7,949

21,393 17,381

28,760

20,350 22,337

(5,373)

2,651

2008 2009 2010 2011 2012 2013R Q4/14 2014

EBITDA (excl stk G/L) EBITDA (incl stk G/L)

399,125

284,123 318,391

446,241

447,432

414,575

88,545

390,090

2008 2009 2010 2011 2012 2013R Q4/14 2014

11,435

5,652 6,999

9,961

14,777

6,692 5,773

12,864

224

12,062

8,956

14,853 12,320

9,316

(6,479) (4,026)

2008 2009 2010 2011 2012 2013R Q4/14 2014

NP (excl stk G/L before tax) NP (incl stk G/L)

Unit: Million THB

Sales Revenue EBITDA

Unit: Million THB

Net Profit

Unit: Million THB

Free Cash Flow*

R Restated financial statement

Unit: Million THB

* Free Cash Flow (FCF) = Operating cash flow – CAPEX(PP&E)-Net

CAPEX (PP&E)-Net

6,103 12,330 18,666 3,850 3,187 1,300 6,284

Financial

-25-

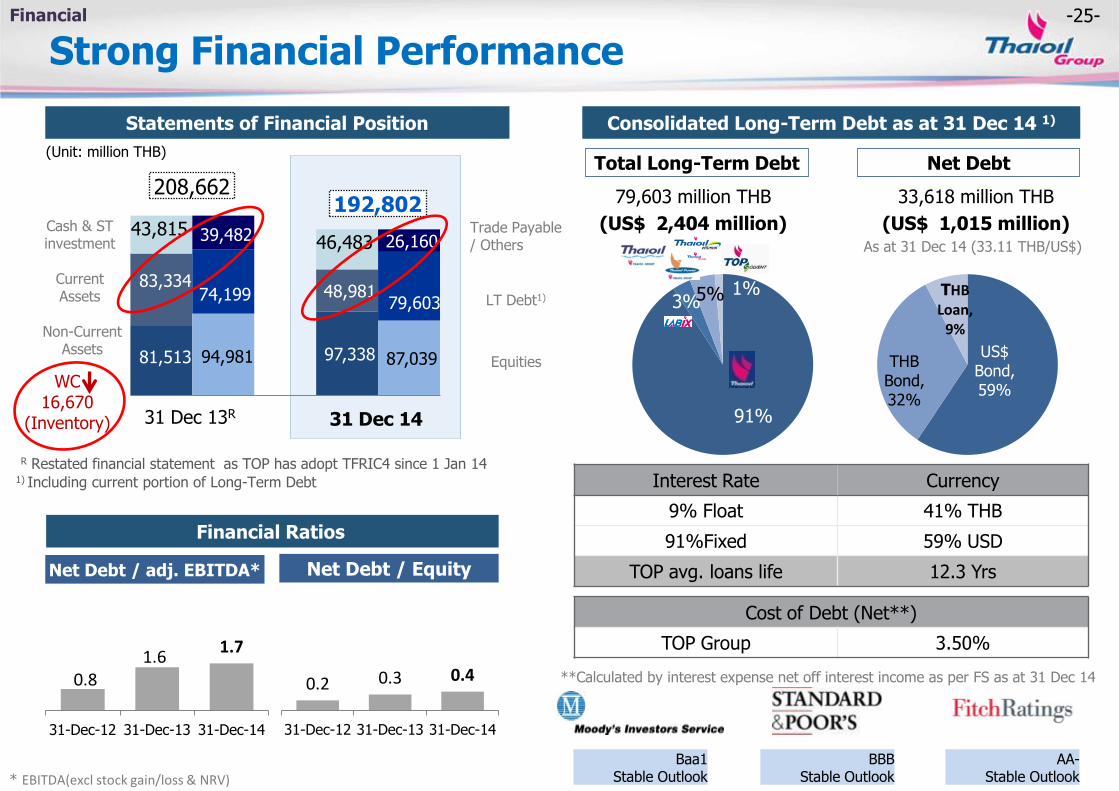

Strong Financial Performance

0.2 0.3 0.4

31-Dec-12 31-Dec-13 31-Dec-14

1) Including current portion of Long-Term Debt

Financial Ratios

Net Debt / adj. EBITDA* Net Debt / Equity

Cost of Debt (Net**)

TOP Group 3.50%

BBB Stable Outlook

Baa1 Stable Outlook

AA- Stable Outlook

Interest Rate Currency

9% Float 41% THB

91%Fixed 59% USD

TOP avg. loans life 12.3 Yrs

Consolidated Long-Term Debt as at 31 Dec 14 1)

79,603 million THB

(US$ 2,404 million)

33,618 million THB

(US$ 1,015 million)

Total Long-Term Debt Net Debt

As at 31 Dec 14 (33.11 THB/US$)

R Restated financial statement as TOP has adopt TFRIC4 since 1 Jan 14

81,513 97,338

83,334 48,981

43,815 46,483

94,981 87,039

74,199 79,603

39,482 26,160

Statements of Financial Position

(Unit: million THB)

Trade Payable / Others

LT Debt1)

Equities

Current Assets

Non-Current Assets

Cash & ST investment

192,802 208,662

31 Dec 13R 31 Dec 14 91%

3% 5% 1%

US$ Bond, 59%

THB Bond, 32%

THB Loan,

9%

**Calculated by interest expense net off interest income as per FS as at 31 Dec 14

Financial

WC 16,670

(Inventory)

0.8 1.6

1.7

31-Dec-12 31-Dec-13 31-Dec-14

* EBITDA(excl stock gain/loss & NRV)

-26-

7.82

9.19

8.13

9.40

0.11

5.91

4.41

7.28

6.04

5.09

-1.97

1.80

3.50 3.50

4.50

2.75 2.55 2.00

3.30 2.70

2.30

1.16

FY/04 FY/05 FY/06 FY/07 FY/08 FY/09 FY/10 FY/11 FY/12 FY/13 FY/14

1.50 1.75 1.75

1.05 0.60

1.30

0.50 0.80 0.56

Dividend Payment

Dividend Policy : Not less than 25% of consolidated net profit after deducting reserves, subject to cash flow and investment plan

25%

40%

45%

48%

Yield* 4.0% 5.6% 5.6% 6.2% 5.2% 7.1% 4.0% 4.7% 4.2% 3.6% 2.3%

n.a.

43%

THB/Share

45% 45%

EPS

Total dividend

Interim dividend

Dividend payout

45%

TOP price

44.7 63.0 62.7 72.7 53.3 35.9 49.9 69.8 65.1 64.6 50.4

45%

* Based on average TOP price in each year

Financial

n.a.

-27-

Strategic Investment Plans

-28-

Broadening Growth, Capturing Step Out ,Pursuing Sustainability

Logistics

AEC countries

Value Chain Enhancement

Adjacent

Quick win

Core Business

Geography

New Business

Operational Excellence Growth (Core & Step Out)

Project Update

-29-

Strategic Investment Plan

Projects COD Total Project

Cost 2014 2015 2016 2017 2018

Refinery upgrading 2014 137 32

Reliability, efficiency and flexibility improvement

- 353 103 58 14 8 31

Environmental and fuel efficiency improvement

- 269* 89 12

CDU-3 preheat train 2014 68 45 15

Benzene Derivatives - LAB 2015 300 141 77 10 16

Power – 2 SPPs 2016 380 140 192 48

Solvent expansion – SAKC 2014 64 13 7

Marine fleets expansion 2014/15 56 15 8

Lorry Expansion 2016 55 28 27

Total 1,682 578 396 98 24 31

CAPEX Plan (Unit US$ million)

Notes: Excluding approximately 40 M$/year for annual maintenance *anticipated to receive BOI for environmental projects

Our CAPEX

investments will

cover improvements

in plants reliability,

efficiency &

flexibility,

environmental & fuel

efficiency

improvement as well

as value chain

enhancement

Thai Oil has

sufficient internal

cash flow to fund

this investment plan

$153m

Remaining capital investment

Project Update

Update as of Feb 2015

-30-

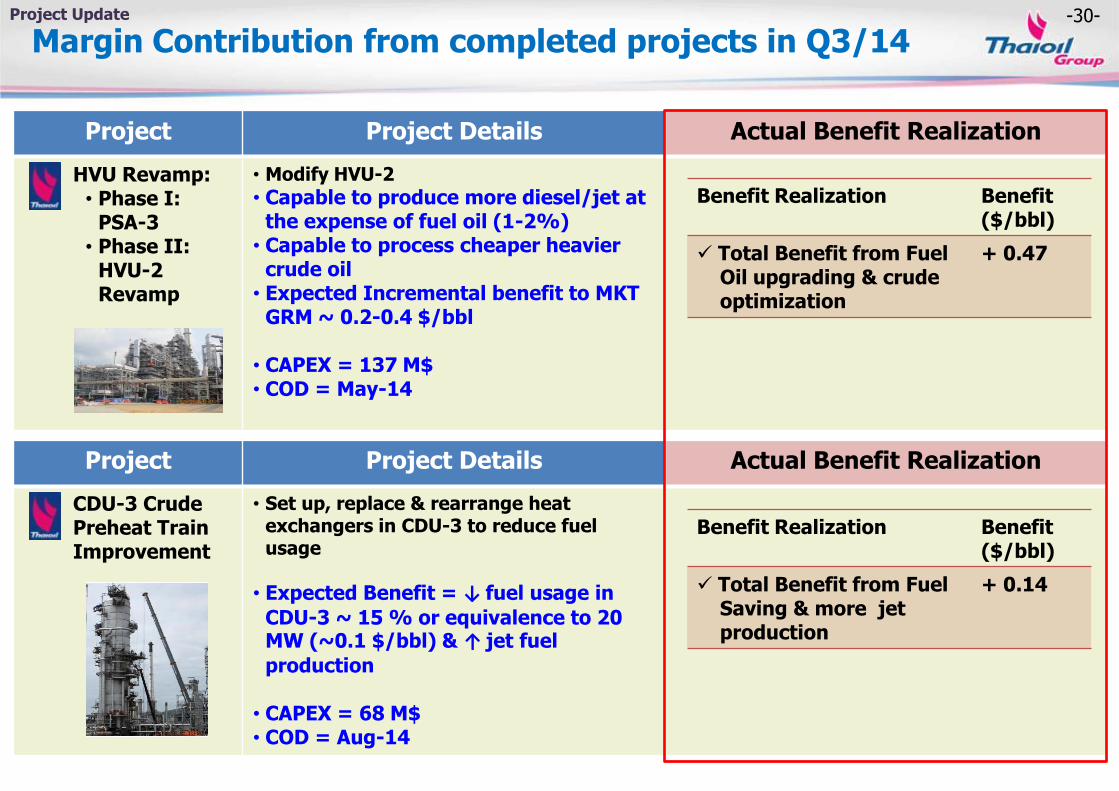

Margin Contribution from completed projects in Q3/14

Project Project Details Actual Benefit Realization

HVU Revamp: • Phase I:

PSA-3 • Phase II:

HVU-2 Revamp

• Modify HVU-2

• Capable to produce more diesel/jet at the expense of fuel oil (1-2%)

• Capable to process cheaper heavier crude oil

• Expected Incremental benefit to MKT GRM ~ 0.2-0.4 $/bbl

• CAPEX = 137 M$ • COD = May-14

Project Project Details Actual Benefit Realization

CDU-3 Crude Preheat Train Improvement

• Set up, replace & rearrange heat exchangers in CDU-3 to reduce fuel usage

• Expected Benefit = ↓ fuel usage in

CDU-3 ~ 15 % or equivalence to 20 MW (~0.1 $/bbl) & ↑ jet fuel

production • CAPEX = 68 M$ • COD = Aug-14

Benefit Realization Benefit ($/bbl)

Total Benefit from Fuel Oil upgrading & crude optimization

+ 0.47

Benefit Realization Benefit ($/bbl)

Total Benefit from Fuel Saving & more jet production

+ 0.14

Project Update

-31-

Key Project Progress Update : LAB Project Update

Project Detail Progress

Linear Alkyl Benzene (LAB)

• TPX JV with Mitsui (75% : 25%) • Upgrade existing Benzene and Kerosene into higher valued product; LAB which is an intermediate feedstock in production of surfactant (detergent)

•Capacity: 100 KTA (First Integrated LAB Plant in SEA)

•Benefit = add to GIM ~ 0.4-0.6 $/bbl •CAPEX = 400 M$ (TPX’s part = 300 M$) •COD = Q4 2015

86%

KTA %

Feedstock

Kerosene (from TOP) 520 94%

Benzene (from TPX) 33 6%

Product/ By-products

LAB 100 19%

By-products (mostly Kerosene

components) (to TOP)

453 81%

LABIX site LABIX : Feedstock / Products

-32-

Key Project Progress Update : 2 SPPs Project Update

Project Detail Progress

TOP SPP (2 blocks of SPP)

• Low risk power business enhance income stability • Support reliability of electricity & steam supply for TOP Group

• Develop 2 new SPP power plants; • Total power capacity 239 MW (~20% used

in TOP complex ~80% sales to national Grid under firmed contract)

• Total steam capacity 498 T/H (100% used in TOP complex)

•CAPEX = 380 M$ •COD = 1H 2016

60%

-33-

New Project Approval in Q3/14 : Lorry Expansion Project New Project

Project Project Detail

Lorry Expansion Project

• Expand lorry loading capacity

• CAPEX : ~ 60 M$ • Benefit : Margin Improvement ~ 0.10 – 0.15 $/bbl (capture future local & Indochina vol) • COD : 2H 2016

Existing Capacity Lorry Expansion Project

Designed Capacity : 10 mml/day (10 gantries)

Planned Additional Capacity : +5 mml/day (+ 5 gantries)

-34-

Progress on Myanmar Project Project Update

Study Project Detail Progress

Refinery Upgrading Project in Myanmar

• On mid-July, 2014, Myanmar Petrochemical Enterprise (MPE) issued Invitation to Tender, specifying the proposal deadline by mid-Oct, 2014

• Planned Two Phase Proposal (TOP in collaboration with PTT Group) 1 - Revamp existing Thanlyin Refinery 2 – Option to Develop new green field refinery

PTT/TOP had submitted proposal on Oct 13, 2014

Thanlyin

Yangon

(Expect result announcement by Q1/15)

Thanlyin Refinery Thanlyin Refinery

Thanlyin Refinery Info

Total Capacity 20 KBD

Year Built 1963

Location 14 km from Yangon

-35-

2015 MARKET OUTLOOK

• Crude Oil

• Petroleum Products

• Aromatics

• Base Oil & Bitumen

-36-

Macroeconomics and Crude Price

-37-

2015 Global GDP Growth by IMF

Sources: (1) ASEAN-5 includes Thailand, Malaysia, Indonesia, Vietnam, Philippines

(2) IMF’S WEO Oct, 2014 (3) IMF ‘S WEO Jan, 2015 (4) BOT Sep, 2014 (5) BOT Dec, 2014

IMF revised down the Global GDP growth to 3.5%

2.8%

-0.6%

5.2%3.9%

3.2% 3.3% 3.3%3.5%

-6%

-3%

0%

3%

6%

9%

12%

2008 2009 2010 2011 2012 2013 2014 2015

Growth (%YoY)

China US EU World

Macroeconomics & Crude Prices

2013

2014 2015

Oct-14(2) Jan-15(3) Oct-14(2) Jan-15(3)

USA 2.2% 2.2% 2.4% 3.1% 3.6%

EU -0.5% 0.8% 0.8% 1.3% 1.2%

China 7.8% 7.4% 7.4% 7.1% 6.8 %

Japan 1.6% 0.9% 0.1% 0.8% 0.6%

India 5.0% 5.6% 5.8% 6.4% 6.3%

ASEAN-5(1) 5.2% 4.7% 4.5% 5.4% 5.2%

Thailand 2.9% 1.5%(4) 0.8%(5) 4.8%(4) 4.0%(5)

World 3.3% 3.3% 3.3% 3.8% 3.5%

-38-

490 0

140

North America

2015 Global Oil Demand Growth

Macroeconomics & Crude Prices

IEA Demand (MBD)

Growth (MBD)

2013 91.8 +1.3

2014 92.4 +0.6

2015 93.3 +0.9

OPEC Demand (MBD)

Growth (MBD)

2013 90.2 +1.2

2014 91.2 +1.0

2015 92.3 +1.1

EIA Demand (MBD)

Growth (MBD)

2013 90.5 +1.3

2014 91.4 +0.9

2015 92.4 +1.0

IEA forecasted 2015’s global oil demand to increase by 0.9 MBD mainly from Asia

Unit: KBD

-90 -260

-70

Europe

350 310 540

Asia 160 200 220

Middle East

50 90 170

Africa

200 150 110

Latin America

130 100

-210

FSU

Source: IEA, Oil Market Report, January 2015

Source: IEA, Oil Market Report January 2015 Source: EIA, Short Term Energy Outlook January 2015 Source: OPEC, Oil Market Report January 2015

The global oil demand will grow

by 0.9 MBD in 2015, amid weak

global demand conditions.

Slump in crude prices have

limited effects to boost demand.

EU’s deflation, strong USD,

revenue impact on oil exporters

and subsidy cuts policies are key

reasons why low oil prices fail to

stimulate demand.

2013

2014 2015

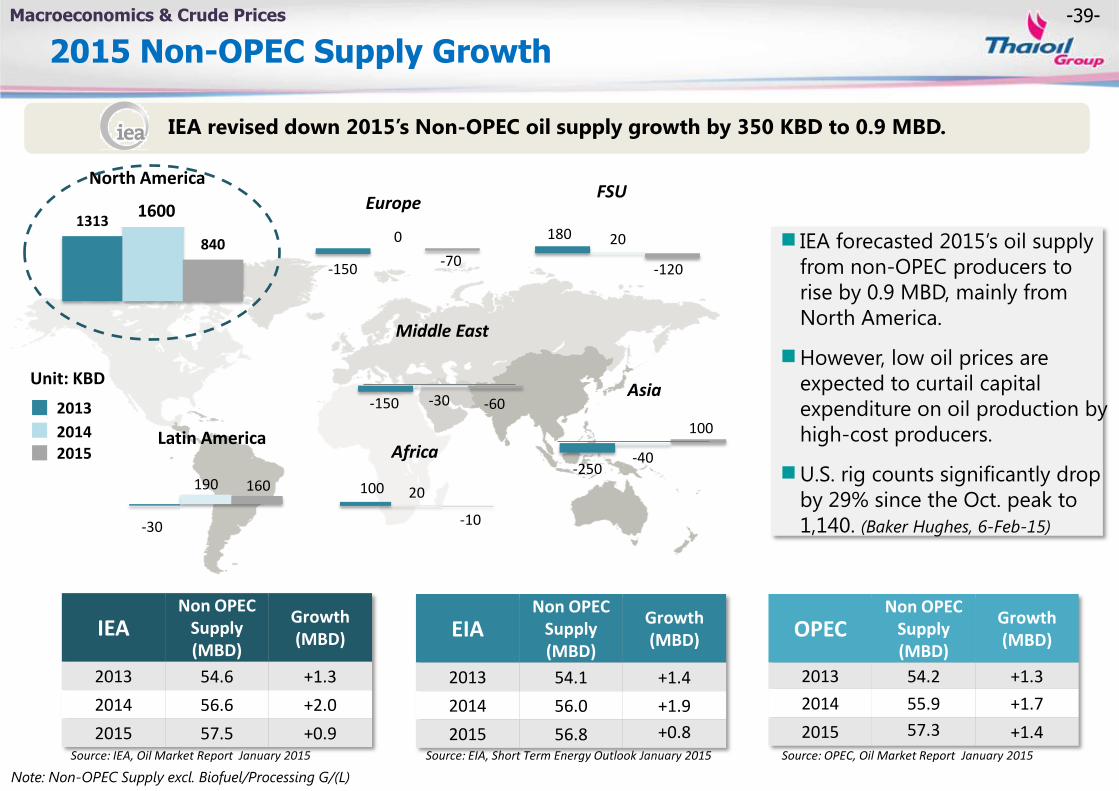

-39-

-150

0

-70

Europe

-250 -40

100

Asia -150 -30 -60

Middle East

100 20

-10

Africa

-30

190 160

Latin America

1313

840

North America

180 20

-120

FSU

2015 Non-OPEC Supply Growth

Macroeconomics & Crude Prices

IEA revised down 2015’s Non-OPEC oil supply growth by 350 KBD to 0.9 MBD.

IEA Non OPEC

Supply (MBD)

Growth (MBD)

2013 54.6 +1.3

2014 56.6 +2.0

2015 57.5 +0.9

OPEC Non OPEC

Supply (MBD)

Growth (MBD)

2013 54.2 +1.3

2014 55.9 +1.7

2015 57.3 +1.4

EIA Non OPEC

Supply (MBD)

Growth (MBD)

2013 54.1 +1.4

2014 56.0 +1.9

2015 56.8 +0.8 Source: IEA, Oil Market Report January 2015 Source: EIA, Short Term Energy Outlook January 2015 Source: OPEC, Oil Market Report January 2015

Unit: KBD

2013

2014 2015

IEA forecasted 2015’s oil supply

from non-OPEC producers to

rise by 0.9 MBD, mainly from

North America.

However, low oil prices are

expected to curtail capital

expenditure on oil production by

high-cost producers.

U.S. rig counts significantly drop

by 29% since the Oct. peak to

1,140. (Baker Hughes, 6-Feb-15)

1600

Note: Non-OPEC Supply excl. Biofuel/Processing G/(L)

-40-

Overview of Crude Prices in Q1/15

Macroeconomics & Crude Prices

40

50

60

70

80

90

100

Oct-14 Nov-14 Dec-14 Jan-15 Feb-15

USD/BBL

Dubai Price Rebound in Late Jan’ 15

$ 54.2

MTD Feb (16 Feb 15)

Fundamental Factors

Aug-11, 1055

Oct-14, 1609

Feb-15, 1056

600

800

1000

1200

1400

1600

Rigs

Total U.S. Oil Rig Counts 2011-2015

Abundant Supply from both Non-OPEC and OPEC producers, amid weak global demand conditions

MBD MBD

Source: IEA Jan’15

Source: Baker Hughes, 2015

Response to the dramatic drop in oil rig counts

Reduced CAPEX on oil production, mainly by non-OPEC producers

Why Do Crude Prices Rebound?: Slowdown in Supply Growth

2015 2014

Surplus

DB $105/BBL

DB $54/BBL

DB $87/BBL

Feb-11 DB $100/BBL

-41-

2015 Crude Outlook

Macroeconomics & Crude Prices

FACTORS TO WATCH

SUPPLY-SIDED FACTORS

Estimates as of Feb’15

Fed’s stance on interest rate hike

ECB’s QE impacts on economy

China’s Strategic Petroleum Reserve Plan

DEMAND-SIDED FACTORS

Declining oil rig counts and reduced CAPEX on oil production

MENA Unrest (i.e. Libya and Iraq)

Iran’s nuclear talks

105 97

104 106 101

74

51 50 53 61

53

20

40

60

80

100

120

2013 2014 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 2015

USD/BBL Dubai Price Movement

Actual (Annually) Actual (Quarterly) Forecast

53$/BBL

-42-

PETROLEUM PRODUCTS

-43-

Overview 2014-20 Refinery Status

Source: FACTs Semi Annual Reports, October 2014, Reuters, Bloomberg, TOP estimate

Note: Adjusted capacity based on start-up period (Effective additional capacity)

525

796

82

958

782

1,004

714

-600

-400

-200

0

200

400

600

800

1000

1200

1400

2014 2015 2016 2017 2018 2019 2020

KBD

AP Additional Demand ME Additional Demand

ME Addition China

Australia Japan

India Vietnam

Other AP Net Addition

Addition (start-up period)

Country Nameplate (KBD)

Company

Q4-14 Saudi Arabia 400 Jubail

Saudi Arabia 400 Yanbu

China 90 Sinopec Yangxi

China 45 Local

Q1-15 UAE 417 Ruwais

India 300 IOC Paradip

Q2-15 China 14 Local

Pakistan 10.5 Attock Rawalpindi

Q3-15 China 30 Sinopec Yangxi

Q4-15 China 60 CNOOC Jiangsu

China 140 CNOOC Zhejiang

New Zealand 8 Marsden Point

Closure

Q4-14 Australia -125 Caltex (Kurnell)

Q2-15 Australia -95 BP Bulwer

Japan -124 Cosmo/Tonen Chiba

Q4-15 Taiwan -205 CPC Kaohsiung

China -75 Local

New barrels from AP/ME are expected to continually flood the petroleum product market

CDU Addition VS Additional Demand – AP & ME

-44-

High Supply Pressures GRM

Refinery

($/bbl) 2013 2014 Q4-14 Q1-15 Q2-15TD* 2015(F)**

ULG95-DB 13.7 14.3 13.4 15.5 16.3

JET-DB 17.5 15.9 17.7 17.0 14.1

GO-DB 17.9 16.1 16.0 16.3 14.7

HSFO-DB (8.0) (8.3) (5.6) (1.9) (3.6)

SG GRM Crack 6.1 5.8 6.2 8.5 7.8

+ High winter demand for heating oil

+ Crude prices slump

+ Improved regional economy

+ Lower price to support demand

Refinery

Remark : *as of 7 Apr 15 , **Compared to 2014

- New barrels from China and ME started to enter the market stream

- Increased refinery run rates, incentivized by healthy refinery margins

- More supply from new AP/ME refineries

- Energy subsidy cuts and consumption tax policies dampen regional oil demand

Overall Market in Q1-15 Factor to Watch for 2015…

-45-

Feb 02: New LPG ex-ref. price formula (CP-$20 /T)

Better benefit when LPG CP price is higher than $416/T

Thailand Oil Demand Outlook Refinery

Year on Year 2013 2014 2015(F)

LPG +2% 0% +3%

MogasA +7% +4% +4%

Jet/Kero +9% -1% +3%

DieselA +2% +1% +1%

Fuel Oil -8% -4% -5%

Total +3.0% +0.6% +2.1%

GDP Growth +2.9% +0.7% +4.0%B

A) Mogas and diesel have included ethanol and biodiesel, respectively

B) Forecasted by BOT ( Monetary Policy Report as of Dec-14 )

Thailand oil demand in 2015 is expected to grow at 2.1% YoY supported by better economic

outlook compared to 2014

Higher local petroleum demand supported by

lower crude oil price

FACTORS TO WATCH “Energy Policy & Economic Stimulus Program”

-46-

AROMATICS

-47-

Has PX Spread Hit the Bottom? Aromatics

-48-

Heavy PX Capacity Addition Causing Supply Surplus

HC

Petr

och

em

Ten

glo

ng

1

Ten

glo

ng

2

Sin

op

ec H

inan

TP

PI

Country Plan KTA Company

China Feb 650 Petrochina Sichuan Petrochemical

SaudiArabia Feb 660 SATORP

China Feb 700 Qingdao Lidong (restart)

China May 800 Dragon Aromatics No.2 (restart)

Korea Jun (delay from May) 1,000 Ulsan Aromatics

China Jul 700 Qingdao Lidong (restart)

Korea Jul (delay from Jun) 1,300 SK Energy

Korea Jul (delay from May) 1,000 Samsung Total 2

India Aug (delay from

May) 920 ONGC Mangalore Petrochemicals

Singapore Sep (delay from Jun) 800 Jurong Aromatics Corp

Algeria Oct 220 Sonatrach

• Heavy new capacity in Feb pressured

PX market in Q1’14

Early plan of PX capacities

• Delay start-up of new capacity in

Jul and Aug helped support PX

market in Q3’14

Delay start-up of new PX plants

Aromatics

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan Sep Oct Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

Feedstock Uncertainty MTA

2013 2014

-49-

2015 PX and PTA Capacity Update Aromatics

-1.0

0.0

1.0

2.0

3.0

4.0

Q1 Q2 Q3 Q4

MTA

Country Plan KTA Company

Korea Q1’15 -200 Lotte Chemical1

Kazakhstan Q2’15 469 JSC KazMunaiGas

China Q3’15 800 Ningbo Zhongjin Petrochemical 1

India Q3’15 2,250 Reliance Industries 4

Thailand Q3’15 120 PTTGC

Total 2015 3,439 MTA

Global Nameplate PX Additional/Closure Capacity

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Q1 Q2 Q3 Q4

Global Nameplate PTA Additional/Closure Capacity

• 5.6 MTA of new PTA capacity will be

added (3.8 MTA as PX equivalent) in 2015

• PX spread remains under pressure due to

heavy supply

• New PTA capacity will help support PX

market -1.0

0.0

1.0

2.0

3.0

4.0

Q1 Q2 Q3 Q4 2015

PX PTA (PX equivalent)

MTA

2015

Source: PCI Xylene&Polyesters as of Nov’14

-50-

PX Demand/Supply Outlook

Source: PCI Xylene & Polyesters as of Nov’14 and TOP estimate

AP/ME PTA Additional New Capacity*

25 27 28 30 31 33 35 37 39 41

29 30 30 33 37

42 45 47 50

53

0

10

20

30

40

50

60

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Demand Capacity

AP/ME PX Capacity* and Demand

3.2

1.6

-0.1

2.6

4.5 4.2

3.7

1.7

2.7

3.6

-2

0

2

4

6

8

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Demand Growth Effective Additional Capacity

AP/ME Effective Additional New Capacity

MTA

MTA

Forecast

2010-2014 Dem: 7.4% Cap: 8.1%

2015 Dem: 5.7% Cap: 11.1%

2016-2019 Dem: 5.8% Cap: 6.4%

Forecast

New PX capacity of 2.9 mil tons/yr will be added in China, S. Korea, Brunei, Vietnam and ME during 2016-2019

New PTA additional capacity support PX demand growth

Remark : * Nameplate capacity

Aromatics

2

4

12

1

11

6

2

0

4 4

1

3

8

0

7

4

1 0

3 3

-2

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

PTA PTA (PX equivalent)

MTA

SUPPLY

DEMAND

Remark : * Nameplate capacity

-51-

Weak Benzene Spread on Soft Demand and Bearish Crude Market

Aromatics

-52-

3.1

1.6

0.4

1.2

2.4

1.8

1.0 0.9

1.6 1.9

0

1

2

3

4

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Demand Growth Effective Capacity Addition

BZ Demand/Supply Outlook

New BZ capacity of 1.4 mil tons/yr will be added in China, S. Korea, Brunei, Vietnam and ME during 2016-2019

Healthy BZ demand, driven by US import

SUPPLY

DEMAND

Remark : * Nameplate capacity

AP/ME BZ Capacity* and Demand

AP/ME Effective Additional New Capacity MTA

23 23 23 24 26 27 28 29 30 32 31 33 33 34 37 39 40 40 42 44

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Demand Capacity

2010-2014 Dem: 5.2% Cap: 5.6%

2015 Dem: 4.3% Cap: 4.9%

2016-2019 Dem: 4.5% Cap: 3.3%

MTA

Forecast Forecast

Aromatics

Source: IHS as of Nov’14 and TOP estimate

0.0

1.0

2.0

3.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

BZ Imports by North America

MT

-53-

Stable PX Spread Due To Production Cut

($/t) 2013 2014 Q4-14 Q1-15 Q2-15TD* 2015(F)**

PX-ULG95 486 279 252 253 238

BZ-ULG95 289 268 207 101 171

Note: PX = Paraxylene, BZ = Benzene

Overall Market in Q1-15

- Weak downstream margin on weak Chinese economy

- Slow US buying interest due to weak BZ price following weak crude price

+ Cut run of PX plants due to soft margin

+ Improved PTA margin on rising polyester demand

PX:

BZ:

Factor to Watch for 2015…

- Bearish downstream demand on weak margin

+ Lower BZ production following reduction of PX run rate

+ PX plants reduce operating rate

+ New PTA capacity (5.6 MTA) will help support PX market

- New PX plants (3.5 MTA) start-up in Q2 and Q3’15

PX:

BZ:

Aromatics

Remark : *as of 7 Apr 15 , **Compared to 2014

-54-

BASE OIL & BITUMEN

-55-

-200

0

200

400

600

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

$/ton

Gr.III vs Gr.I

Gr.II vs Gr.I

200

400

600

800

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

$/ton

500SN-HSFO

150SN-HSFO

Weak Base Oil Prices

478 • Lower 150SN and 500SN

spreads due to Gr.II supply

surplus

374

495 374

2014 YTD-15*

Key Factors

(5) 33

102 417

2014 YTD-15*

• Widening Gr.II and Gr.III over

Gr.I supported Gr.I market

Key Factors

Base Oil & Bitumen

*As of 13 Feb 2015

-56-

200

350

500

650

800

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

$/ton

Bitumen

HSFO

-200

-100

0

100

200

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

$/ton

Bitumen-HSFO

Weak Fuel Oil Support Bitumen Spread

• Positive spread due to

weakening fuel oil price in

Q4-2014

Key Factors

527 337

2014 YTD-15*

561 308

(32) 28

2014 YTD-15*

Base Oil & Bitumen

*As of 13 Feb 2015

-57-

Abundant Supply to Pressure Base Oil Prices

($/t) 2013 2014 Q4-14 Q1-15 Q2-15TD* 2015(F)**

500SN-HSFO 485 495 493 370 406

Bitumen-HSFO (14) (32) 85 24 41

Factor to Watch for 2015…

+ Steady regional demand, especially from Indonesia and Vietnam

- Increasing HSFO price, following crude price, limits bitumen margin

- Continued Gr.II price competition

- Expansion of Exxon Mobil pressures market in Mar (1.2MTA to 1.6 MTA in Singapore)

Overall Market in Q1-15

- Additional capacity (1.28MTA) affected base oil market

+ Widening Gr.II over Gr.I supported Gr.I market

Base Oil & Bitumen

Bitumen:

Base oil:

Bitumen:

Base oil:

+ Firm regional demand especially from AEC infrastructure projects

Remark : *as of 7 Apr 15 , **Compared to 2014

-58-

CONCLUSION

-59-

2015 Market Conclusion

• Expected crude prices recovery in 2H15,

supported by declining non-OPEC production

• Additional supply from new refineries pressure

refinery margins

Refinery

Aromatics

Base Oil & Bitumen

Conclusion

• Stable PX spread due to production cut

• Soft SM downstream margin limited BZ demand

• Stable base oil spread due to widen Gr.II price

• Stable bitumen spread supported by firm regional

demand

-60-

Key Take Away Messages

-61-

Key Take Away Messages

Maximize Refinery Run to capture decent GRM

Flexible & Optimized Run for Aromatics & Base Oil

Maintain Regional 1st Quartile Cost Effectiveness

Prudent Risk Management Strategies

Sustain Strong Financial Discipline

Further Enhance Cost Management Program i.e.

2015 Key Focus

1.) Improve Energy Intensity Index (EII) i.e. 2014 EII @ 82.3point, every 1 EII reduction = energy saving 14.9 MW or 5.5 M$ (@Dubai 53$/bbl)

2.) Procurement Strategy i.e. PTT Group procurement plan to save cost, IT system to enhance process

3.) Negotiate service contract (operation & maintenance) i.e. contractor / service & consultant fees

-62-

Appendix

• Q4 & FY/14 Performance analysis

• World GRM / Inventory

• Thailand petroleum demand by products

-63-

Q4 & FY/2014 PERFORMANCE

ANALYSIS

-64-

Thai Oil Refinery : Superior Performance…

Q4/2014

TOP’s Refinery Utilization vs Industry TOP’s Refinery Crude sources & Product Output

102% 108%

98% 92% 92%

87%

2013 Q4/14 2014

TOP Refinery Overall Industry (Thailand)

TOP’s Domestic Sale vs Industry

84% 76% 81%

72% 83% 76%

16% 24% 19%

28% 17% 24%

FY/13 Q4/14 FY/14

TOP Industry TOP Industry TOP Industry

Domestic Sales Export Sales

Source : *Department of Energy Business, Ministry of Energy

FY/13 Q4/14 FY/14

Thailand Thailand Thailand

73%

9%

8%

11%

9%

37%

20%

17%

13%

4%

4%

41%

11%

17%

27% Far East

Local

Middle East

Sources of Crude

Others LPG

PLATFORMATE

GASOLINE

JET

DIESEL

FUEL OIL

Product output

Domestic demand for

petroleum products*

• Flexibility in crude intake allows diversification of crude types to source cheaper crude

• Flexibility in product outputs by maximizing middle distillates (jet and diesel) by adjusting production mode to capture domestic demand and price premium

• Maximize Platformate production to capture higher margin on aromatics

• Minimize fuel oil output to avoid lower margin products

-65-

2014 2015

$/bbl Q1 Q2 Q3 Q4 Q1 Q2TD

DUBAI (DB) 104.4 106.1 101.5 74.4 51.8 54.6

ULG95 - DB 14.6 16.1 13.2 13.4 15.5 16.3

JET - DB 17.0 14.3 14.5 17.7 17.0 14.1

GO - DB 17.8 16.0 14.4 16.0 16.3 14.7

HSFO - DB (8.5) (10.6) (8.4) (5.6) (1.9) (3.6)

104 105 104 105 106 108 106 102 96

87 76

60

46 55 55 55

40

60

80

100

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

2014 2015

Q4/14:Robust Refining Margins…Offset by Huge Inventory Loss Refining

2014

$/bbl Q1 Q2 Q3 Q4

Marketing GRM 5.1 4.4 4.6 8.2

Stock G/(L) (1.7) 1.4 (5.2) (11.7)

Accounting GRM

3.4 5.8 (0.6) (3.5)

2013 2014

FY13 FY14

105.5 96.6

13.7 14.3

17.5 15.9

17.9 16.1

(8.0) (8.3)

Dubai Crude Price & Key Petroleum Product Spreads Refinery Utilization

2013 Q4/14 2014

102% 108% 98%*

Gross Refinery Margins - GRM

- Excess OPEC & Non OPEC supplies; High US shale oil production, Maintained OPEC production after OPEC meeting

- Sluggish demand; as weak world economy, IEA revised down 2015 global oil demand growth by 0.2 MBD to 0.9 MBD

Dubai

Benefits to Q4/14 TOP GRM

Dubai Price

(US$/bbl)

*CDU-3 MTA mid Jun to end Jul 14

2013 2014

FY13 FY14

4.3 5.7

0.8 (4.5)

5.1 1.2

*

* As of 7 Apr 15

• Margin improvement Projects 0.6 $/bbl

• Crude Premium ~1.2 $/bbl

• F&L 0.8 $/bbl

3.6$/bbl QoQ

Total 2.6$/bbl

-66-

353 273

191 180 191

290

381 415

317 242 248 266 290

251 224 238

340 285

232 241 228 293

333 372

275 270 229

122 120 56 119 171

0

200

400

600

800

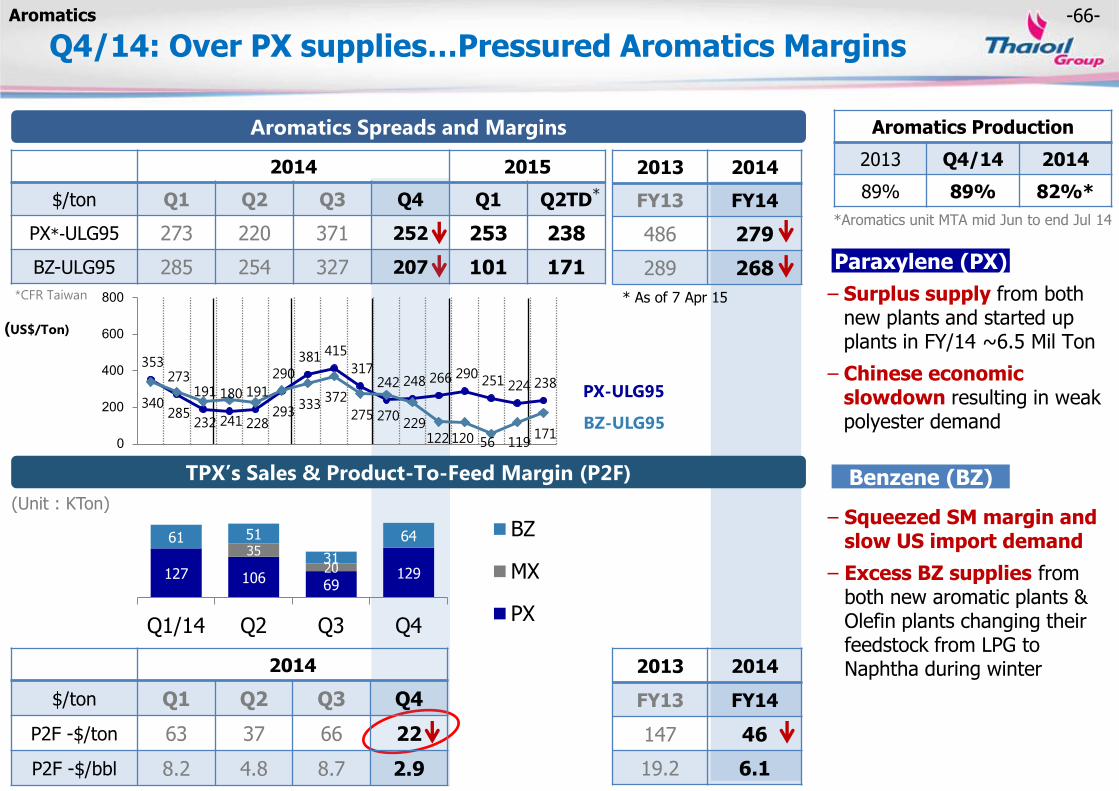

Q4/14: Over PX supplies…Pressured Aromatics Margins

Aromatics

127 106 69

129

35

20

61 51

31

64

Q1/14 Q2 Q3 Q4

BZ

MX

PX

Aromatics Spreads and Margins

TPX’s Sales & Product-To-Feed Margin (P2F)

Aromatics Production

2013 Q4/14 2014

89% 89% 82%*

(Unit : KTon)

(US$/Ton)

PX-ULG95

BZ-ULG95

Paraxylene (PX)

Benzene (BZ)

*CFR Taiwan

*Aromatics unit MTA mid Jun to end Jul 14

2013 2014

FY13 FY14

486 279

289 268

2013 2014

FY13 FY14

147 46

19.2 6.1

*

* As of 7 Apr 15 − Surplus supply from both new plants and started up plants in FY/14 ~6.5 Mil Ton

− Chinese economic slowdown resulting in weak polyester demand

− Squeezed SM margin and slow US import demand

− Excess BZ supplies from both new aromatic plants & Olefin plants changing their feedstock from LPG to Naphtha during winter

2014

$/ton Q1 Q2 Q3 Q4

P2F -$/ton 63 37 66 22

P2F -$/bbl 8.2 4.8 8.7 2.9

2014 2015

$/ton Q1 Q2 Q3 Q4 Q1 Q2TD

PX*-ULG95 273 220 371 252 253 238

BZ-ULG95 285 254 327 207 101 171

-67-

2014 2015

$/ton Q1 Q2 Q3 Q4 Q1 Q2TD

500SN-HSFO 486 501 500 493 370 406

BITUMEN-HSFO (69) (77) (66) 85 24 41

Q4/14: G II/III Price Competition…Soften Lube Margins Lube Base Oil

− Additional GII supply from US & South Korea triggering price war between GI & II

− Weak demand as buyers kept low stock during year end

+ Spread highly supported by soft fuel oil price

+ Resumed regional demand especially from Indonesia & Vietnam to expedite road repairs during year end

+ Spread supported by soft fuel oil price

493 483 486 506 505 492 497 501 507 534 454 490

430 312 366 406

(49) (78) (78) (68) (75) (90) (78) (74) (48) 32 76

145 73

(22) 19 41

-200

0

200

400

600

800

2014

$/ton Q1 Q2 Q3 Q4

P2F -$/ton 135 117 107 90

P2F -$/bbl 20.5 17.8 16.2 13.6

70 60 58 52 33 40 37 32

90 89 87 93

Q1/14 Q2 Q3 Q4

Bitumen

TDAE/Extract/Slack Wax

Base Oil

Base Oil & Bitumen Spreads & Margins

TLB’s Sales & Product-To-Feed Margin (P2F)

Base oil Production

2013 Q4/14 2014

102% 80% 92%*

500SN-HSFO

Bitumen-HSFO

Lube Base Oil

Bitumen

(US$/Ton)

(Unit : KTon)

*Base oil unit T/A in end-Sep 14

2013 2014

FY13 FY14

485 495

(14) (32)

2013 2014

FY13 FY14

144 112

21.9 17.1

*

* As of 7 Apr 15

-68-

18.0 20.1 24.0 25.0 20.5 17.8 16.2 13.6 21.9 17.1

Q1/13 Q2 Q3 Q4 Q1/14 Q2 Q3 Q4 FY/13 FY/14

5.3 2.0

8.6

3.3 3.3 5.6

(0.6) (3.3)

4.9 1.1

2.0

1.4

1.9

2.1 0.4

0.0

0.4

(0.3)

1.8

0.1

0.5

0.8

1.2

1.0

0.8

0.8

0.7 0.4

0.9

0.7

7.7 4.2

11.7

6.4 4.5

6.4

0.5

(3.2)

7.6

1.9

TOP TPX TLB GIM

Q1/13 Q2 Q3 Q4 Q1/14 Q2 Q3 Q4 FY/13 FY/14

Beauty of Integration…Sustainable GIM

(Unit: US$/bbl)

Marketing GIM Accounting GIM

Crude

Product to Feed

Product to Feed

Marketing GRM (excluded stock gain / loss)

(Unit: US$/bbl) (Unit: US$/bbl)

Performance Breakdown

6.4 3.4

4.8 1.8

4.9 4.2 4.4

7.9

4.1 5.4

2.0

1.4 1.9

2.1

0.4 0.0 0.4

(0.3)

1.8 0.1

0.5

0.8

1.2

1.0

0.8 0.8 0.7

0.4

0.9 0.7

8.8

5.6

7.9

4.9 6.1

5.1 5.5

8.0

6.8 6.2

TOP TPX TLB GIM

6.6 3.6 5.0

1.9 5.1 4.4 4.6

8.2 4.3 5.7

Q1/13 Q2 Q3 Q4 Q1/14 Q2 Q3 Q4 FY/13 FY/14

20.3 16.5 18.6 21.6

8.2 4.8 8.7 2.9

19.2

6.1

Q1/13 Q2 Q3 Q4 Q1/14 Q2 Q3 Q4 FY/13 FY/14

Q1/13 Q2 Q3 Q4 Q1/14 Q2 Q3 Q4 FY/13 FY/14

-69-

Q4 & FY/2014: Performance Breakdown

Q1/14 1,929 (161) 437 43 39 64 71 72 2,534 (1,433) 3,967

Q2/14 1,729 (397) 337 51 63 (13) 57 204 2,094 1,074 1,020

Q3/14 (2,500) (276) 240 56 (15) (4) 52 219 (2,175) (4,290) 2,115

Q4/14 (6,188) (633) 98 11 3 10 93 89 (6,479) (12,252) 5,773

FY/14 (5,030) (1,467) 1,112 98 153 57 273 591 (4,026) (16,890) 12,864

98%

82% 92% 91% 92%

85% 89% 102% 89%

102%

130%

88% 76%

88%

FY/14 FY/13

*Since Q3/14 onwards, 2014 SAKC capacity = 141 KTA / 2013 SAKC capacity = 76 KTA ** Apply on an equity accounted basis in the consolidated financial statement.(GPSC has been hold by TOP 11.88% and TP 27.71% since 10 Jan 13) ***TP performance are based on TOP’s equity portion (excluding 27.71% shares of profit from the investment in GPSC). TOP hold TP 74% since 4 Dec 12

Refinery Aromatic Lube Solvents Marine Ethanol Power

Performance Breakdown

Consol Stock G/(L) & NRV

Consol Excl Stock G/(L) & NRV

*

Key Points • TOP/ TPX/ TLB: Lower intake

due to CDU-3 & aromatics complex planned MTA (15 Jun-end July 14) & Lube planned S/D during Sep 14

• TS: Completion of capacity expansion but drop in gross profit margins pressured by slow demand & higher regional competition

• TM: Drop in contribution from the dry docking of the VLCC

• TET: Higher ethanol sale as rising domestic gasohol demand but soften margins

• TP: Better contribution from higher run rate & rising Ft rate

** 32.39% holding

Utilization/Production (%) & Net Profit (million THB)

*** 74% holding

1,172

-70-

32.62 30.87 1.75

33.11 32.95 0.16

N/A 10% N/A

THB/US$ - average 32.85 32.24 31.83 0.61

THB/US$ - ending 33.11 32.52 32.95 0.59

Effective Tax Rate (%) * N/A N/A N/A N/A

(16,890) 2,624 (19,514)

12,864 6,692 6,172

Stock G/(L) & NRV (12,252) (4,290) 1,247 (7,962)

Net Profit/ (Loss) excl. Stk G/(L) and NRV

5,773 2,115 (1,237) 3,658

Consolidated Financial Performance Financial

(million THB) Q4/14 Q3/14 Q4/13R QoQ+/(-) FY/14 FY/13R YoY+/(-)

390,090 414,575 (24,485)

2,218 1,292 926

2,651 22,337 (19,686)

19,541 19,713 (172)

(3,966) (3,786) (180)

996 (3,111) 4,107

920 (1,160) 2,080

(4,026) 9,316 (13,342)

(1.97) 4.57 (6.54)

R Restated financial statement . As on 1 January 2014, Thaioil Group adopted Thai Financial Reporting Interpretations Committee 4 (TFRIC4) on determining whether an arrangement contains a lease.

*redeemed BOI privilege for tax exemption on environmental projects in Q4/14 ,= 0 MB, Q3/14 = 0 MB, FY/14 = 0 MB, FY/13 = 640 MB

Sales Revenue 88,545 88,254 107,952 291

Hedging Gain 328 695 388 (367)

EBITDA (5,373) (545) 4,257 (4,828)

EBITDA excl. Stk G/(L) 6,880 3,745 3,010 3,135

Financial Charges (992) (1,004) (968) 12

FX G/(L) & CCS (548) 561 (1,815) (1,109)

(Tax Expense)/reversal 1,451 118 (217) 1,333

Net Profit / (Loss) (6,479) (2,175) 10 (4,304)

EPS (THB/Share) (3.18) (1.07) 0.00 (2.11)

-71-

Free Cash Flow 4,086 (10,111)

FY/2014 Consolidated Cash Flow

Beginning

cash 15,303

S/T investment 28,512

43,815

2014 2013

Operating Cash Flow 24,432 16,131

Net income & non-cash adj. 7,762 24,882

Change in working capital 16,670 (8,751)

+

+ =

+

2014 2013

Investments (20,346) (26,242)

ST investments (1,734) (11,129)

CAPEX (PP&E) & other (18,612) (15,113)

Ending

16,237

30,246

46,483

Effect of FCD

(77)

+ Change

1,011

Financing (3,075) 16,616

Loans proceeding / (repayment)

4,985 25,953

Dividends paid (4,242) (6,269)

Interest (3,818) (3,068)

Operating Cash Flow Investments

Financing

Financial

(Unit: Million THB) (Unit: Million THB)

-72-

• World GRM / Inventory

• Thailand petroleum demand by products

-73-

Asian Margin Vs. US-EU margin

Source: EIA, Norwegian Energy, Thai Oil

Total Capacity: 4.9 MBD

91.0% 63.4% 73.8%

Total Capacity: 17.5 MBD Total Capacity: 17.0 MBD

-74-

Crude Inventory

Source: Norwegian Energy

-75-

Global Distillate Inventory

Source: Norwegian Energy

-76-

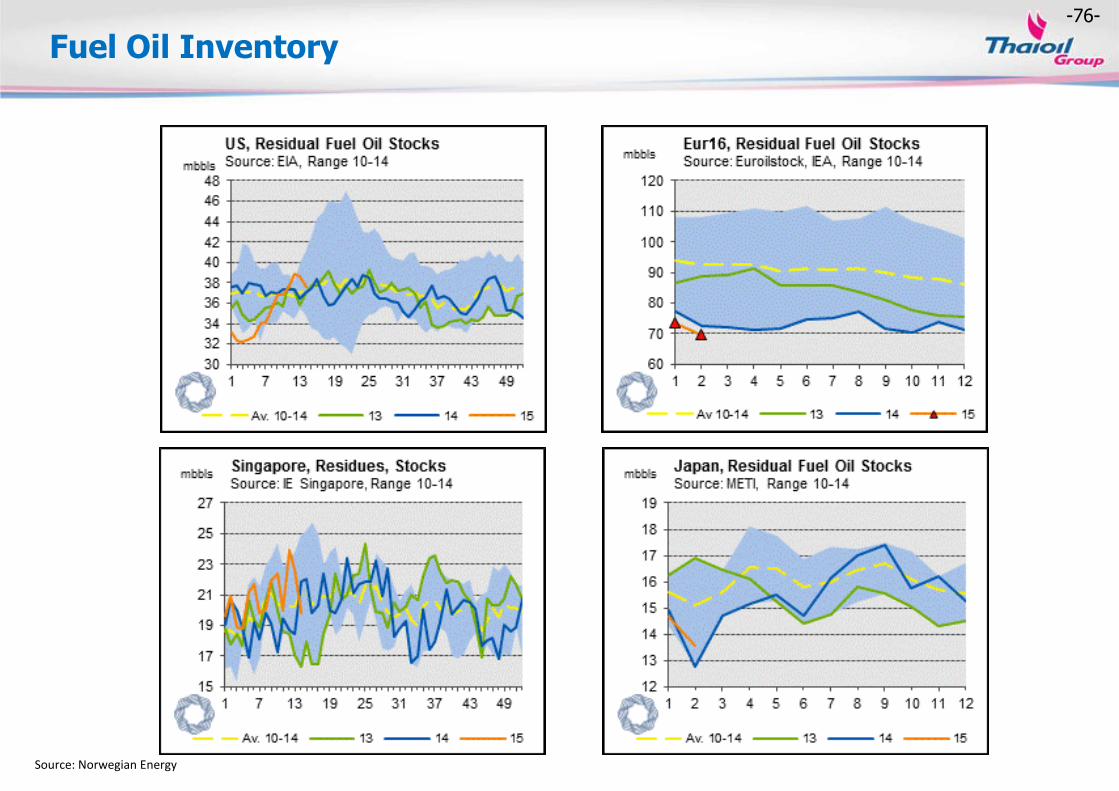

Fuel Oil Inventory

Source: Norwegian Energy

-77-

China’s Product Export

Source: Norwegian Energy

-78-

Domestic LPG Demand

LPG Demand by Sector

LPG Demand Highlight

• In 2014 LPG demand slightly declined by 0.2% YoY as pressured by low usages in cooking, industrial and petrochemical sectors. Consumptions in cooking and industrial sector were limited by increased retail price to reflect real cost and weak Thailand economic activities. However, usages in automobile sector significantly increased as a result of new registered LPG cars.

Outlook for 2015

• LPG demand is expected to grow by 2.9% YoY supported by the expectation of higher demand in auto and cooking sectors following an improving economic.

• However, LPG demand growth was expected to limit by increased of LPG price to reflect market price.

Thailand LPG Demand

Remark : Include Petrochemical and own used consumption

-79-

Domestic Gasoline Demand

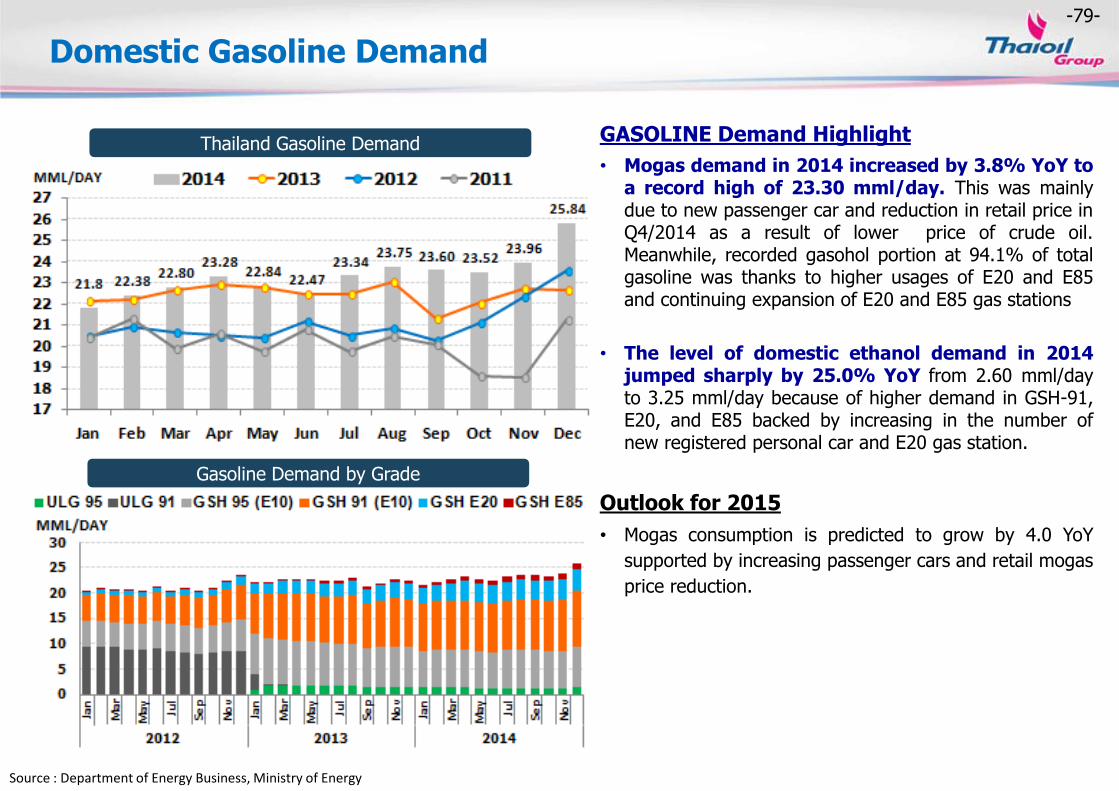

Source : Department of Energy Business, Ministry of Energy

Gasoline Demand by Grade

Thailand Gasoline Demand GASOLINE Demand Highlight

• Mogas demand in 2014 increased by 3.8% YoY to a record high of 23.30 mml/day. This was mainly due to new passenger car and reduction in retail price in Q4/2014 as a result of lower price of crude oil. Meanwhile, recorded gasohol portion at 94.1% of total gasoline was thanks to higher usages of E20 and E85 and continuing expansion of E20 and E85 gas stations

• The level of domestic ethanol demand in 2014 jumped sharply by 25.0% YoY from 2.60 mml/day to 3.25 mml/day because of higher demand in GSH-91, E20, and E85 backed by increasing in the number of new registered personal car and E20 gas station.

Outlook for 2015

• Mogas consumption is predicted to grow by 4.0 YoY

supported by increasing passenger cars and retail mogas

price reduction.

-80-

JET Demand Highlight

• In 2014 Jet consumption marginally decreased by 1.0% YoY mainly due to the concern of politic situation in Thailand during May-Jul 14 and weakening global economic growth especially in Russia which has resulted from declining oil price and economic sanction from US and EU. However, downside was limited by the increased number of flight movement especially from domestic aircraft movement and stability situation in Thailand in Dec-14.

Outlook for 2015

• Jet demand growth is expected to surge by 3.2 YoY owing

to returning tourists from improving global economy and

stable politic situation in Thailand.

Domestic Jet Demand

Source : Department of Energy Business, Ministry of Energy / AOT

Thailand JET-A1 Demand

JET-A1 demand and # of flights

-81-

Diesel Demand Highlight

• In 2014 Diesel demand rose by 0.9% YoY. as

supported by increased transportation demand and retail

fuel price reduction in Q4/14. However, demand growth

was limited by the slow growth of Thailand economy

especially in Manufacturing sector, which has affected by

declined export orders and slowly-than-expected

improvement of domestic orders.

Outlook for 2015

• Diesel demand in 2015 is expected to expand by 1.1%

YoY supported by reducing retail price and increasing

new commercial car sales. However, gasoil demand was

limited gain by concerns on in-recovery of Thailand’s

export sector.

Domestic Gasoil Demand

Source : Department of Energy Business, Ministry of Energy

NGV Demand Highlight

• In 2014 NGV demand increased by 3.2% YoY to 8.8

KT/day thanks to switching on fuel engines, new register

cars and price attractiveness over gasoline and diesel.

Thailand Gasoil Demand

NGV Demand

-82-

Domestic Fuel Oil Demand

FUEL OIL Demand Highlight

• In 2014, Fuel Oil consumption significantly fell by

3.9% YoY. because of lower demand in electrical sector

which has resulted from fuel switching toward Natural gas

and alternative energy. Moreover, demand in transportation

also declined as a result of lower shipping activities.

Outlook for 2015

• Fuel oil demand is expected to dropped by 4.7% YoY

following the government power develop plan (PDP) that

aim to promote alternative fuel. Moreover, power plant also

alternate to use natural gas instead of fuel oil thanks to

lower price.

Source : Department of Energy Business, Ministry of Energy

Thailand Fuel Oil Demand by Sector

Thailand Fuel Oil Demand

-83-

Thank You

Any queries, please contact:

at email: [email protected]

Tel: 662-797-2999 / 662-797-2961

Fax: 662-797-2976

![PTT Multicasting Scheme [호환 모드] · 2 New PTT Group Add by Mouse right button click 3PTTGrouppg Name Setting 4 PTT Group Number Setting 5 PTT Server Setting 6 PTT Group Session](https://static.fdocuments.in/doc/165x107/5f727989ade5745a8a06acb0/ptt-multicasting-scheme-eeoe-2-new-ptt-group-add-by-mouse-right-button.jpg)