Terry Hungle CFO - s1.q4cdn.coms1.q4cdn.com/350838982/files/doc_presentations/MVNR_Feb2015.pdf ·...

45

Private & Confidential February 2015 Transforming Mobile Networks to 4G LTE Terry Hungle CFO

Transcript of Terry Hungle CFO - s1.q4cdn.coms1.q4cdn.com/350838982/files/doc_presentations/MVNR_Feb2015.pdf ·...

Private & Confidential February 2015

Transforming Mobile Networks to 4G LTE

Terry Hungle

CFO

2Private & Confidential February 2015

Forward-Looking Statements

This presentation has been prepared by Mavenir Systems, Inc. (“Mavenir”) solely for informational purposes.

Mavenir has filed a registration statement (including a prospectus) with the U.S. Securities and Exchange

Commission (the “SEC”) for the offering to which this presentation relates. Before you invest, you should read

the prospectus for more complete information about Mavenir and this offering.

Statements in this presentation that are not historical fact are forward-looking statements. Some of the forward-

looking statements contained in this presentation can be identified by the use of forward-looking words such as

“anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate” and “potential,” among others.

Forward-looking statements include, but are not limited to, statements regarding our intent, belief or current

expectations with respect to matters such as future industry trends, capital expenditures by mobile service

providers, the adoption of 4G LTE technology by mobile service providers and users, and our expected

financial performance subsequent to our most recently released financial results. Forward-looking statements

are based on our management’s beliefs and assumptions and on information currently available to our

management. Such statements are subject to risks and uncertainties, and actual results may differ materially

from those expressed or implied in the forward-looking statements due to various factors. Investors should

review factors described in our filings with the SEC, including under the heading “Risk Factors” in such

filings. Forward-looking statements speak only as of the date they are made, and we do not undertake any

obligation to update them in light of new information or future developments or to release publicly any revisions

to these statements in order to reflect later events or circumstances or to reflect the occurrence of

unanticipated events.

3Private & Confidential February 2015

Customers include 12 of top 20

operators globally; Top 4 US

operators & 4 of top 5 in Europe

First mover advantage with several

world’s first commercial

deployments of 4G LTE solutions

Capitalizing on two key network

trends: 4G All-IP and software-

based cloud deployments

1172 employees

959 across

eng/ops

Founded in 2005 with a

vision to lead the

transformation to 4G LTE

A leading provider of converged voice,

video, messaging and mobile core

network solutions

Disruptive, virtualized

software platform with

>30 products

Company Highlights

$101M 2013 Rev

37% YoY Growth

30% YoY Growth

$96.1M 9mo Rev

4Private & Confidential February 2015

Investment Highlights

Strong competitive position in a large and rapidly growing market

Disruptive software-based mobile networking solutions provider

Capitalizing on two major trends: 4G all-IP & cloud networks

Solid foundation of deployments into Tier-1 carriers

Attractive financial model with proven track record of execution

5Private & Confidential February 2015

Investment Highlights

Mavenir is

• Wireless Pure Play networking solutions provider

• Disruptive software-based mobile approach

• Capitalizing on two major trends: 4G all-IP & cloud networks

• Strong competitive position in a large and rapidly growing market

• Solid foundation of deployments into Tier-1 carriers

• Attractive financial model with proven track record of execution

6Private & Confidential February 2015

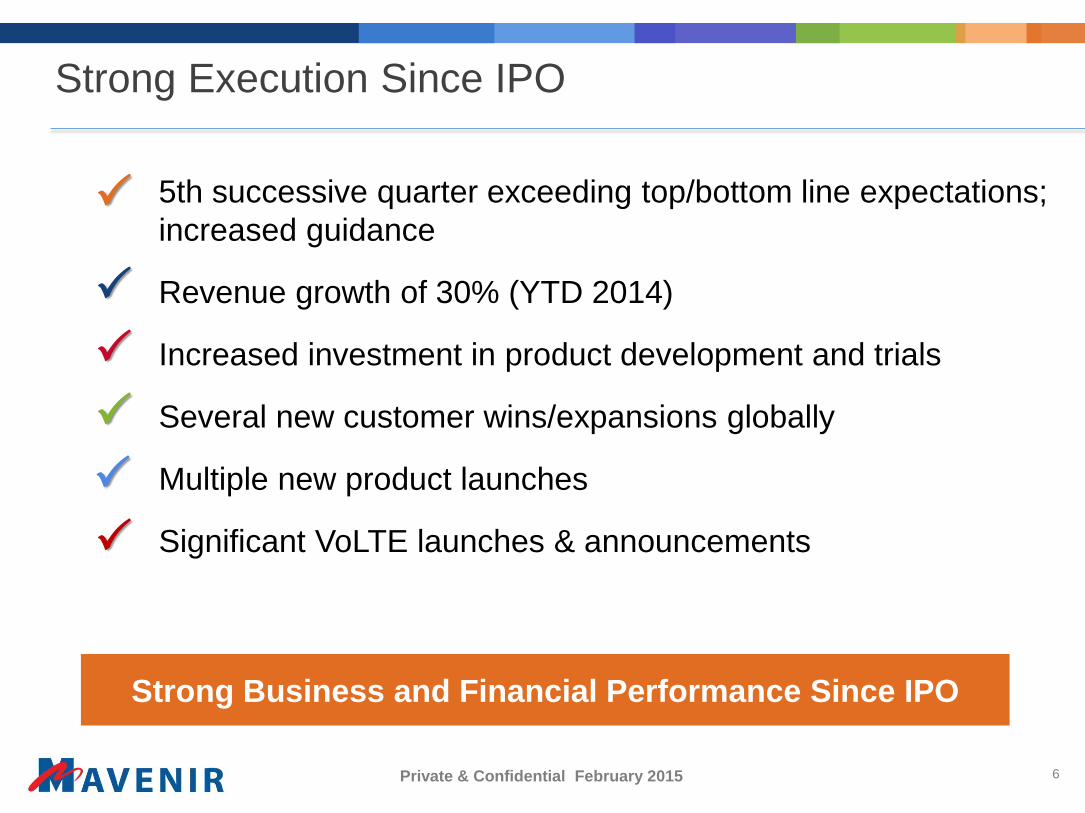

Strong Execution Since IPO

5th successive quarter exceeding top/bottom line expectations;

increased guidance

Revenue growth of 30% (YTD 2014)

Increased investment in product development and trials

Several new customer wins/expansions globally

Multiple new product launches

Significant VoLTE launches & announcements

Strong Business and Financial Performance Since IPO

7Private & Confidential February 2015

Mavenir Global Presence

Richardson

Head Office

Architecture Devt

Americas Ops

Sales/BD Sales

EMEA Ops

Shanghai

Platform &

Protocal

Development

Bangalore

Application Dev

Asia Pack Ops

Support

Global Call Center

Reading

8Private & Confidential February 2015

Speed

up to 15x

faster

Services

more

revenue

Savings

less

cost

Spectrum

up to 10x

better

Why 4G LTE is a Necessity

9Private & Confidential February 2015

Phase 1 Phase 2

4G LTE

HighSpeed

Data

2G/3G

CircuitSwitched

Voice

4G LTE

Better VoiceHigh Speed DataRich, New Services

First Phase of LTE is “Data Only”…

Two Networks for Voice & Data

Next Phase of LTE is “Unified”…

One Network for Voice and Data

Reallocate Spectrum from 2G/3G

to spectrally efficient 4G LTE

4G LTE Network Evolution Phases

10Private & Confidential February 2015

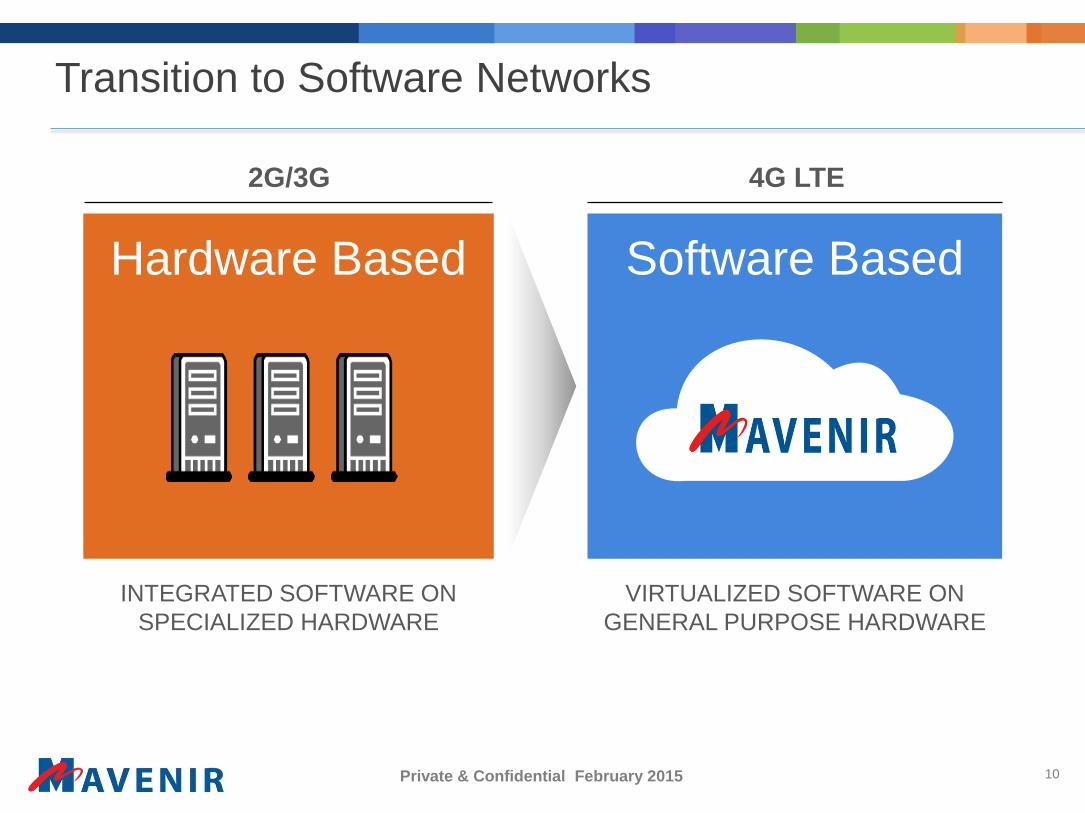

Software Based

Transition to Software Networks

2G/3G 4G LTE

Hardware Based

INTEGRATED SOFTWARE ON

SPECIALIZED HARDWARE

VIRTUALIZED SOFTWARE ON

GENERAL PURPOSE HARDWARE

11Private & Confidential February 2015

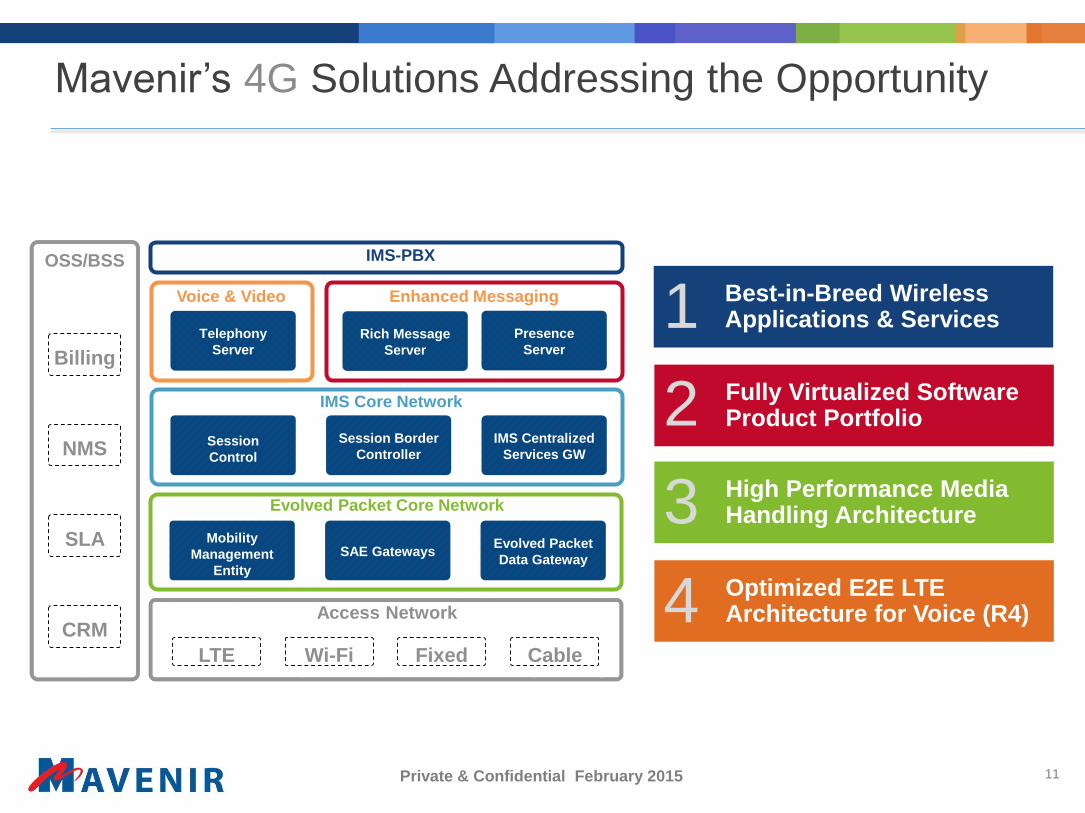

Mavenir’s 4G Solutions Addressing the Opportunity

Best-in-Breed Wireless Applications & Services

Fully Virtualized Software Product Portfolio

High Performance Media Handling Architecture

1

2

3

Session

Control

Session Border

Controller

Voice & Video

IMS-PBX

IMS Core Network

IMS Centralized

Services GW

Rich Message

Server

Presence

Server

Telephony

Server

Mobility

Management

Entity

SAE Gateways

Evolved Packet Core Network

Evolved Packet

Data Gateway

Optimized E2E LTE Architecture for Voice (R4)4

Enhanced Messaging

Access Network

CableLTE Wi-Fi FixedOSS

OSS/BSS

Billing

NMS

SLA

CRM

12Private & Confidential February 2015

Key Differentiators

VoLTE RCSIMSEPC

SERVICE PARITY

CONVERGEDMESSAGING

SCALE & FLEXIBILITY

VIRTUALIZED & EFFICIENT

• Integrated IN

• MCS Equivalency

• Deployment Flexibility

• Convergence (FMC, VoWi-Fi)

• First Mover Advantage (Metro)

• Investment Protection (RMS)

• Solution Breadth (full RCS 5)

• Next Gen IP Leadership (CPM)

• First Mover Advantage (Metro)

• Designed for Wireless

• Optimized for large scale deployments

• Unique Next Gen SW-based SBC

• ICS GW for CS Replacement

mONE® SOFTWARE PLATFORM

• Unique Distributed Architecture

• Lower TCO Thru SW Performance

• R4 Architectural Optimization of LTE

• Enhanced with M2M Features

13Private & Confidential February 2015

4G Network Connectivity & Topology

Public

Internet

SGWSEG

PGW

ePDG

MME

A-SBC

P-CSCF

DRAATGW

ATCF I-SBC

LTE Backhaul Wi-Fi Access

Data Services

Carrier

Networks

IMS Service

Interoperability

2G/3G CS Core

I-CSCF

CSCF

DSCMGW

MGCF HSS

IMS

Co

ntr

ol

IMS

Bo

rder

EP

C

PSTN

Networks

Legacy Voice

Interworking

mStore™

RMS

XDMSMRF

TAS PRS

IMS

Ap

ps &

Serv

ices

Voice

Handover

Bearer Plane

Control Plane

3rd Party Component

PCRF

IMS-PBX

IMS/LTE Policy

Control

14Private & Confidential February 2015

4G LTE Progress

Operators globally

1000+

801 invested in LTE

<5%

445 launched

Connections on LTE

Source: GSMA, February 2015

15Private & Confidential February 2015

4G LTE Investment Cycle and Opportunity

Launch

Voice

over LTE

Launch

4G LTE

Data

Coverage Capacity

Launch

New

Services

Global 4G LTE CAPEX

Source: Gartner - January 2015.

2018

$13.9B

$34.8B

2014

26%

CAGR

16Private & Confidential February 2015

2014/2015 VoLTE – Industry Profile

Launches Planned

OperatorsLaunched

OperatorsTrialing

DevicesAvailable

2014 2015

13 50 20 146

Source: GSMA, GSA – January 2015.

17Private & Confidential February 2015

VoLTE Total Market Forecast

50m

VoLTE subscriptions in

2014

1200m

VoLTE subscriptions in

2019

Source: Mavenir, ABI Research June 2014

82%CAGR

18Private & Confidential February 2015

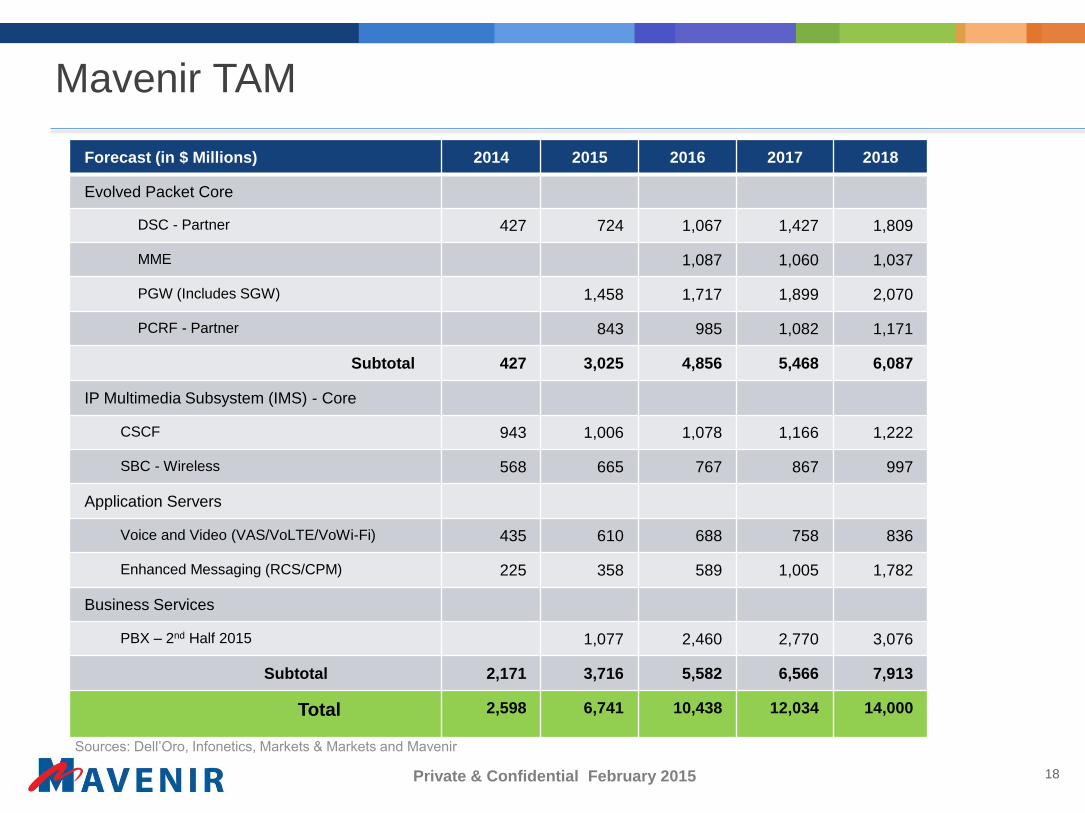

Mavenir TAM

Forecast (in $ Millions) 2014 2015 2016 2017 2018

Evolved Packet Core

DSC - Partner 427 724 1,067 1,427 1,809

MME 1,087 1,060 1,037

PGW (Includes SGW) 1,458 1,717 1,899 2,070

PCRF - Partner 843 985 1,082 1,171

Subtotal 427 3,025 4,856 5,468 6,087

IP Multimedia Subsystem (IMS) - Core

CSCF 943 1,006 1,078 1,166 1,222

SBC - Wireless 568 665 767 867 997

Application Servers

Voice and Video (VAS/VoLTE/VoWi-Fi) 435 610 688 758 836

Enhanced Messaging (RCS/CPM) 225 358 589 1,005 1,782

Business Services

PBX – 2nd Half 2015 1,077 2,460 2,770 3,076

Subtotal 2,171 3,716 5,582 6,566 7,913

Total 2,598 6,741 10,438 12,034 14,000

Sources: Dell’Oro, Infonetics, Markets & Markets and Mavenir

19Private & Confidential February 2015

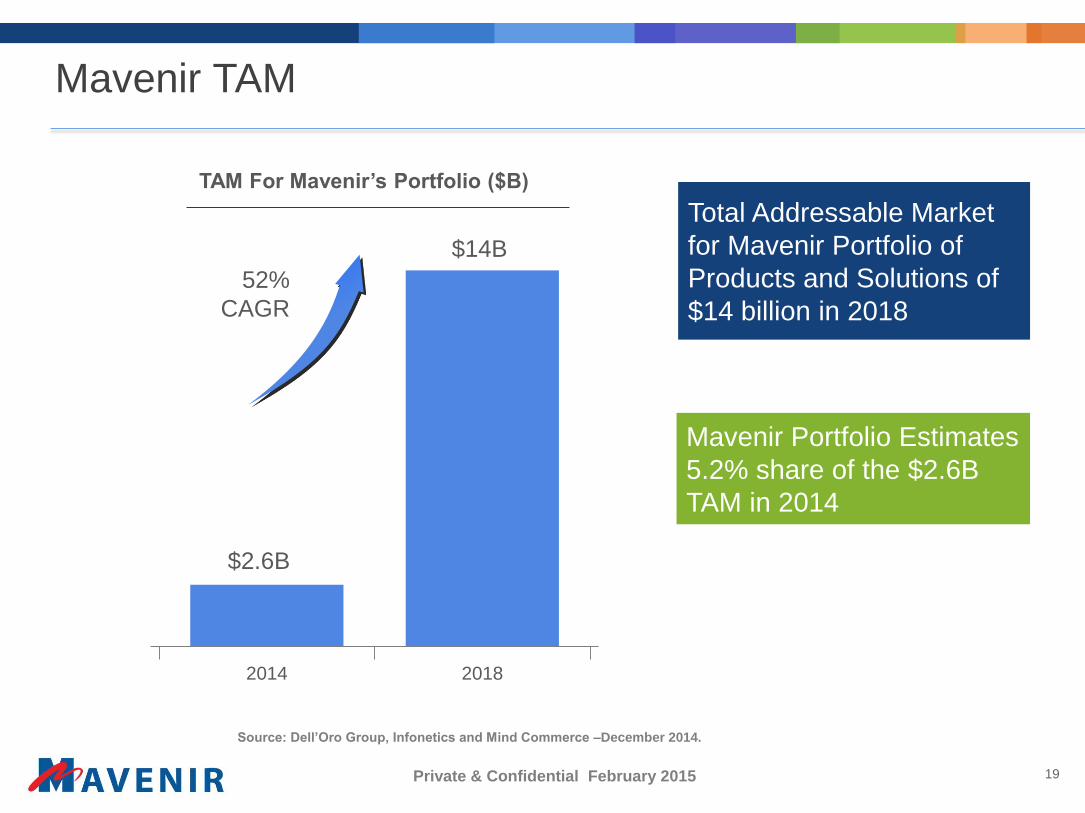

Mavenir TAM

TAM For Mavenir’s Portfolio ($B)

Total Addressable Market

for Mavenir Portfolio of

Products and Solutions of

$14 billion in 2018

Mavenir Portfolio Estimates

5.2% share of the $2.6B

TAM in 2014

2018

$2.6B

$14B

2014

52%

CAGR

Source: Dell’Oro Group, Infonetics and Mind Commerce –December 2014.

20Private & Confidential February 2015

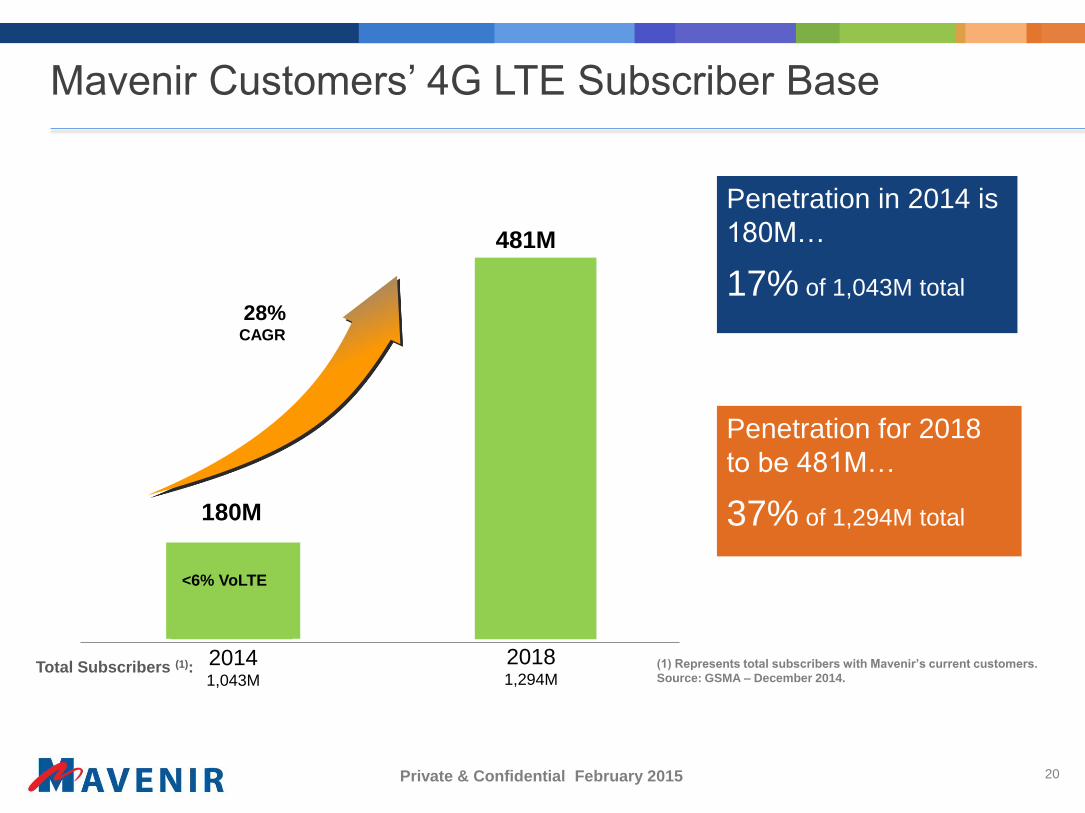

Mavenir Customers’ 4G LTE Subscriber Base

28%CAGR

<6% VoLTE

481M

Penetration in 2014 is

180M…

17% of 1,043M total

20181,294M

180M

20141,043M

Penetration for 2018

to be 481M…

37% of 1,294M total

(1) Represents total subscribers with Mavenir’s current customers.

Source: GSMA – December 2014.Total Subscribers (1):

21Private & Confidential February 2015

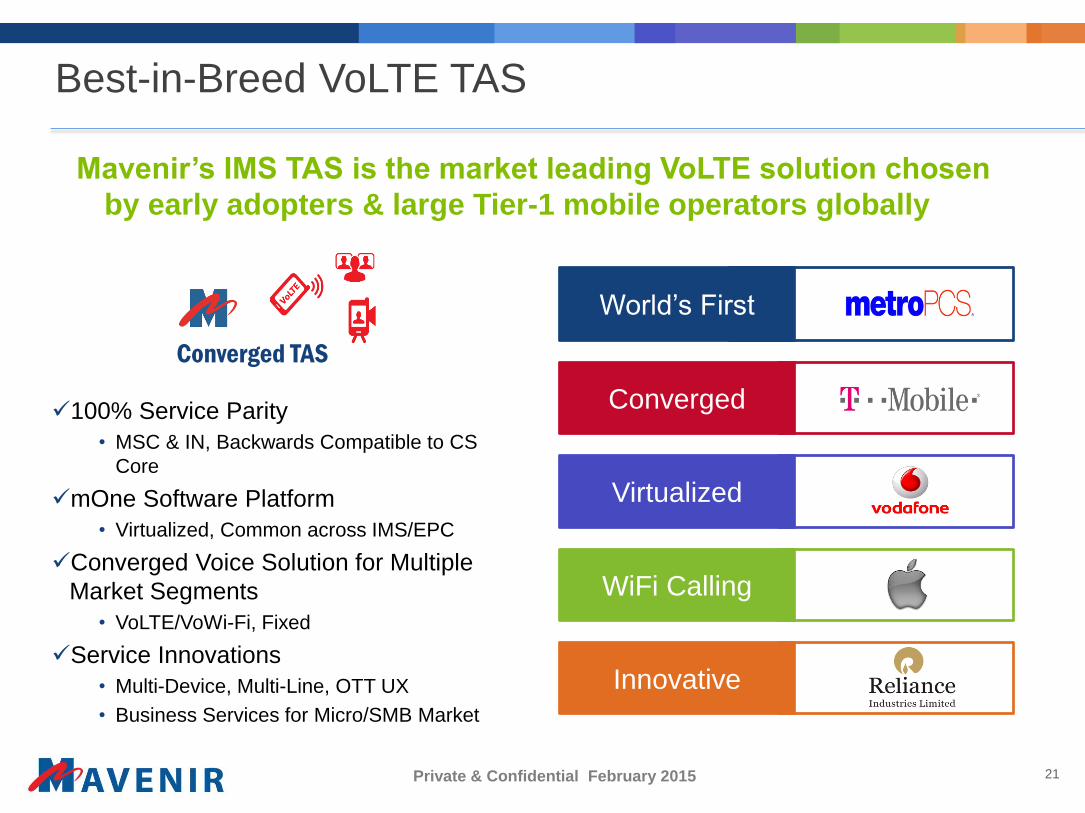

Best-in-Breed VoLTE TAS

Mavenir’s IMS TAS is the market leading VoLTE solution chosen

by early adopters & large Tier-1 mobile operators globally

100% Service Parity

• MSC & IN, Backwards Compatible to CS

Core

mOne Software Platform

• Virtualized, Common across IMS/EPC

Converged Voice Solution for Multiple

Market Segments

• VoLTE/VoWi-Fi, Fixed

Service Innovations

• Multi-Device, Multi-Line, OTT UX

• Business Services for Micro/SMB Market

Converged TAS

World’s First

Converged

Virtualized

WiFi Calling

Innovative

22Private & Confidential February 2015

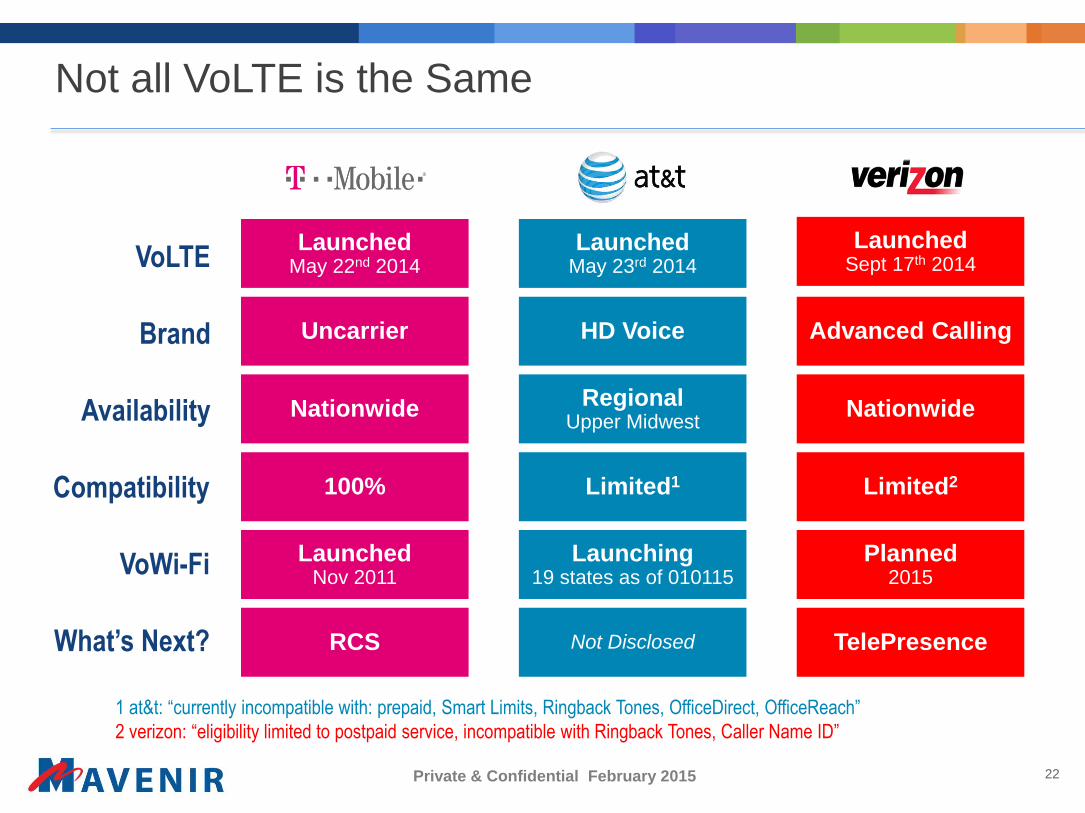

Not all VoLTE is the Same

LaunchedMay 22nd 2014

LaunchedNov 2011

Nationwide

100%

LaunchedSept 17th 2014

Planned2015

Nationwide

Limited2

LaunchedMay 23rd 2014

Launching19 states as of 010115

RegionalUpper Midwest

VoLTE

Availability

Compatibility Limited1

VoWi-Fi

RCS TelePresenceNot DisclosedWhat’s Next?

1 at&t: “currently incompatible with: prepaid, Smart Limits, Ringback Tones, OfficeDirect, OfficeReach”

2 verizon: “eligibility limited to postpaid service, incompatible with Ringback Tones, Caller Name ID”

Uncarrier Advanced CallingHD VoiceBrand

23Private & Confidential February 2015

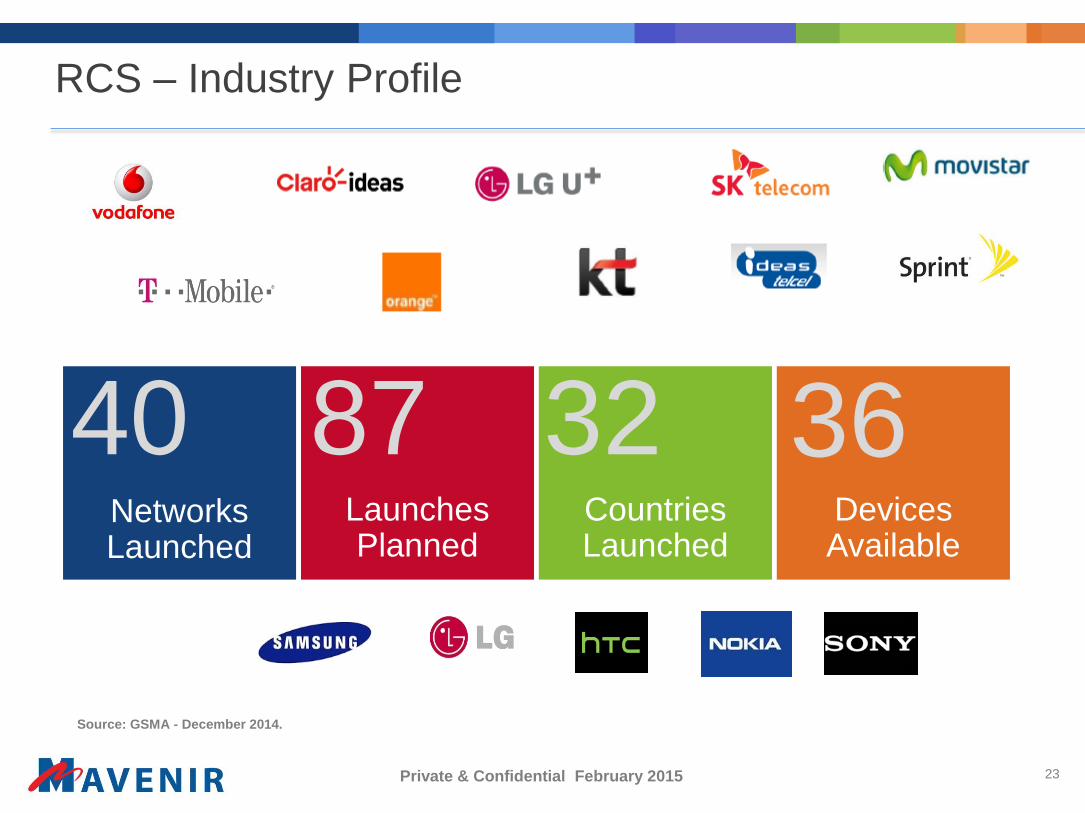

RCS – Industry Profile

Launches Planned

NetworksLaunched

Countries Launched

DevicesAvailable

40 87 32 36

Source: GSMA - December 2014.

24Private & Confidential February 2015

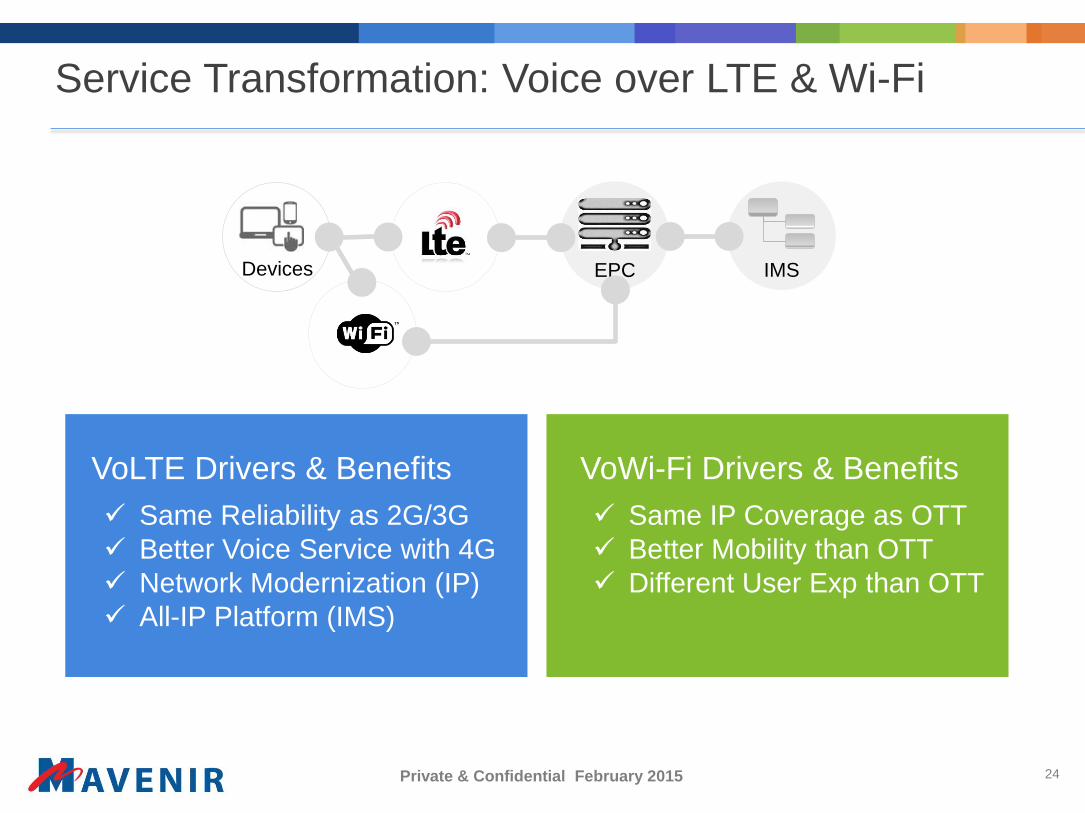

Service Transformation: Voice over LTE & Wi-Fi

EPC IMSDevices

Same Reliability as 2G/3G

Better Voice Service with 4G

Network Modernization (IP)

All-IP Platform (IMS)

VoLTE Drivers & Benefits VoWi-Fi Drivers & Benefits

Same IP Coverage as OTT

Better Mobility than OTT

Different User Exp than OTT

25Private & Confidential February 2015

EPC IMSDevicesCloud Store

Identity

Mgmt.

Internet

RCS

Service Transformation: RCS & Multi-Device

RCS & Multi-Device Drivers & Benefits

LTE Device Ecosystem

User Experience & Demand

OTT/Apple UX

Service Extensions - RCS

Single Mobile Identity

Interoperable Ecosystem

26Private & Confidential February 2015

Business Transformation: Adjacent Markets

Mobile

Consumer

Devices

Markets

Fixed / CableEnterprise

FMC IMS-PBX

VoLTERCS

Residential

Voice

Hosted

PBX / UC

27Private & Confidential February 2015

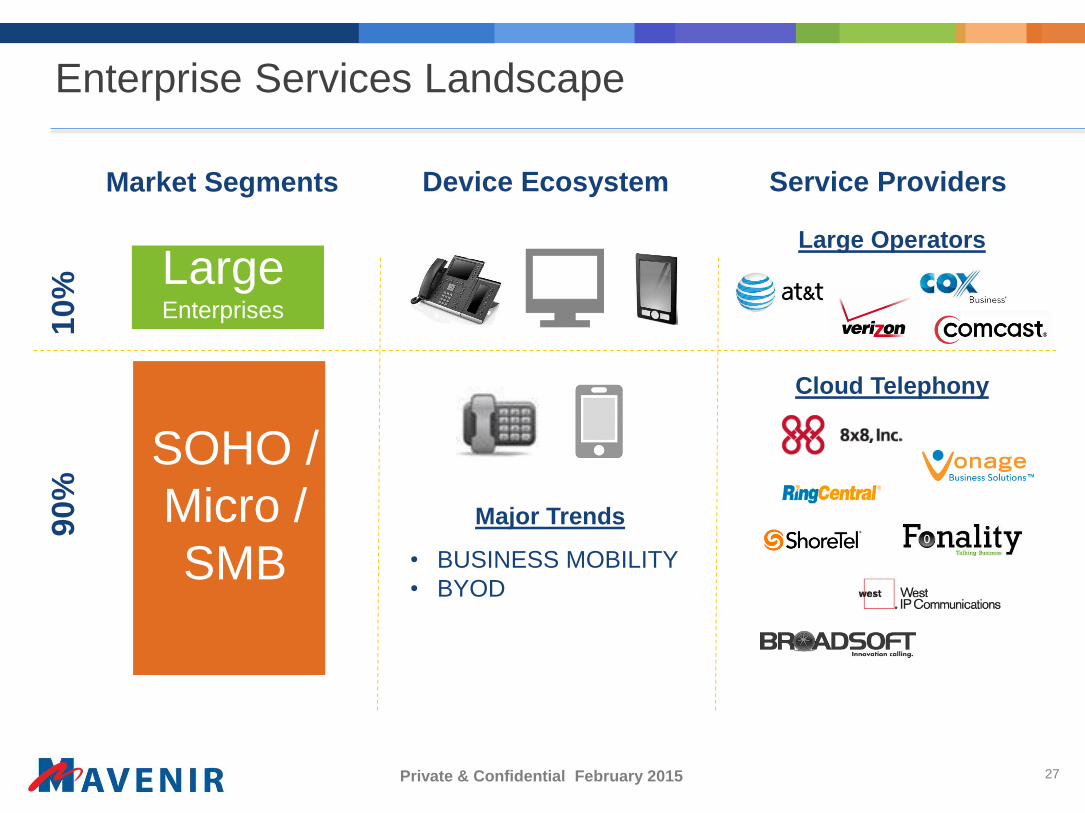

Enterprise Services Landscape

SOHO /

Micro /

SMB

LargeEnterprises

10

%

• BUSINESS MOBILITY

• BYOD

Market Segments

90

%

Device Ecosystem

Major Trends

Service Providers

Large Operators

Cloud Telephony

28Private & Confidential February 2015

IMS-PBX Solution Targeting Micro SMB Segments

Personal#

Personal

Work

Family

2.5G 3G 4G

Work#Family#

Multi-Lines Handling Personas

Multi-Device Extending Reach

Integrated UC for Collaboration

Custom Service Personalization

29Private & Confidential February 2015

Complete Portfolio of 4G LTE Services

Multiple Services

Delivered across

multiple networks

Services

VoiceVoIP • VoLTE • VoWi-Fi

VideoMobile Video

Video Calling/Conferencing

MessagingCPM • IP-SM-GW

RCS • Web

Platforms

Next Gen NetworksLTE • Wi-Fi • HSPA • FIXED

Multi-Device

DevicesLandline Smartphone Computer Tablet TV

Better Voice & Video New Services More Efficient Networks

30Private & Confidential February 2015

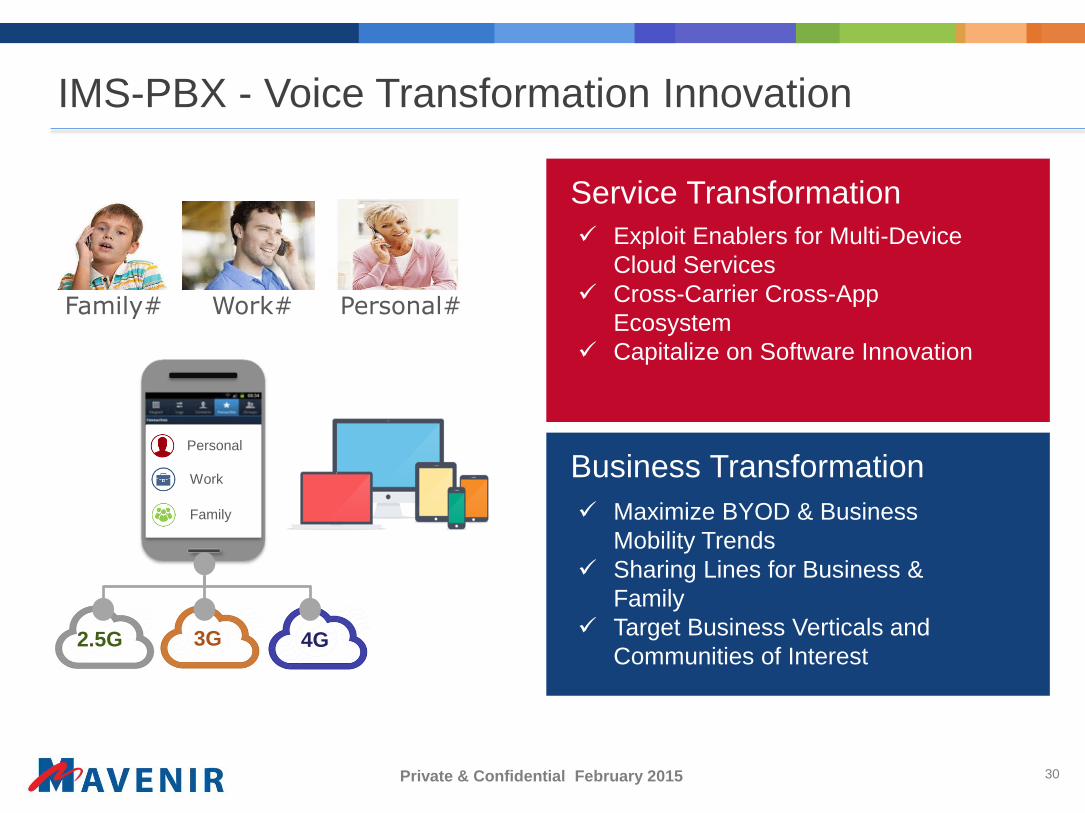

IMS-PBX - Voice Transformation Innovation

Personal#

Personal

Work

Family

2.5G 3G 4G

Work#Family#

Service Transformation

Business Transformation

Maximize BYOD & Business

Mobility Trends

Sharing Lines for Business &

Family

Target Business Verticals and

Communities of Interest

Exploit Enablers for Multi-Device

Cloud Services

Cross-Carrier Cross-App

Ecosystem

Capitalize on Software Innovation

31Private & Confidential February 2015

Competitive Landscape

End to End

(proprietary H/W)

Point S/W-based

Solutions

Complete S/W Portfolio

32Private & Confidential February 2015

Customer Highlights

VoLTE/WiFi

17RCS

17CORE

23 Growing Roster of Blue Chip 4G Customers

• Top 4 operators in the US; 3 of top 4 operators in Europe

Diversified 4G Customer Base• Geographically diverse, as well across product lines

Strong 2G/3G Customer Base • 12 of top 20 operators globally

2G/3G/4G120+

Based on Mavenir 2Q2014 data

33Private & Confidential February 2015

Reasons Why We Win

Flexibility

Innovation

Technology

Experience

• Customer First attitude

• Adapting products to existing networks

• Lower Total Cost of Ownership

• Accelerate Time To Market

• Disruptive SW platform

• Best-in-breed wireless applications

• First Mover Advantage

• Passionate and knowledgeable workforce

Vision• Mobile network transformation

• Evolution to the cloud

34Private & Confidential February 2015

Business Drivers for Mavenir’s Growth

Pure-play vendor focused on 4G LTE infrastructure with

industry spending forecast to grow 30% through 2018

Leverage

Technology to

Enable

Software

Based

Networks

Innovate to

Extend

Technology

Advantage

Selectively

Pursue

Strategic

Relationships

Expand into

Emerging

Markets

Source: Gartner – October 2014.

Private & Confidential February 2015

Transforming Mobile Networks to 4G LTE

36Private & Confidential February 2015

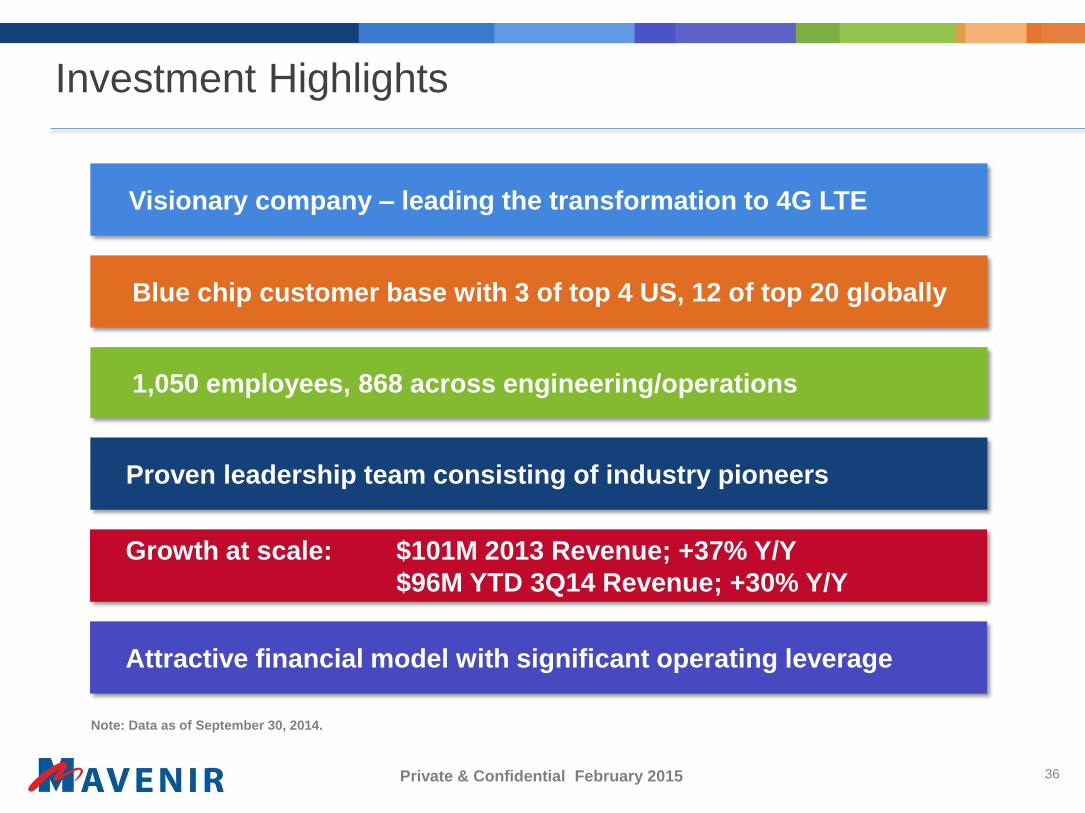

Investment Highlights

1,050 employees, 868 across engineering/operations

Visionary company – leading the transformation to 4G LTE

Blue chip customer base with 3 of top 4 US, 12 of top 20 globally

Proven leadership team consisting of industry pioneers

Growth at scale: $101M 2013 Revenue; +37% Y/Y

$96M YTD 3Q14 Revenue; +30% Y/Y

Attractive financial model with significant operating leverage

Note: Data as of September 30, 2014.

37Private & Confidential February 2015

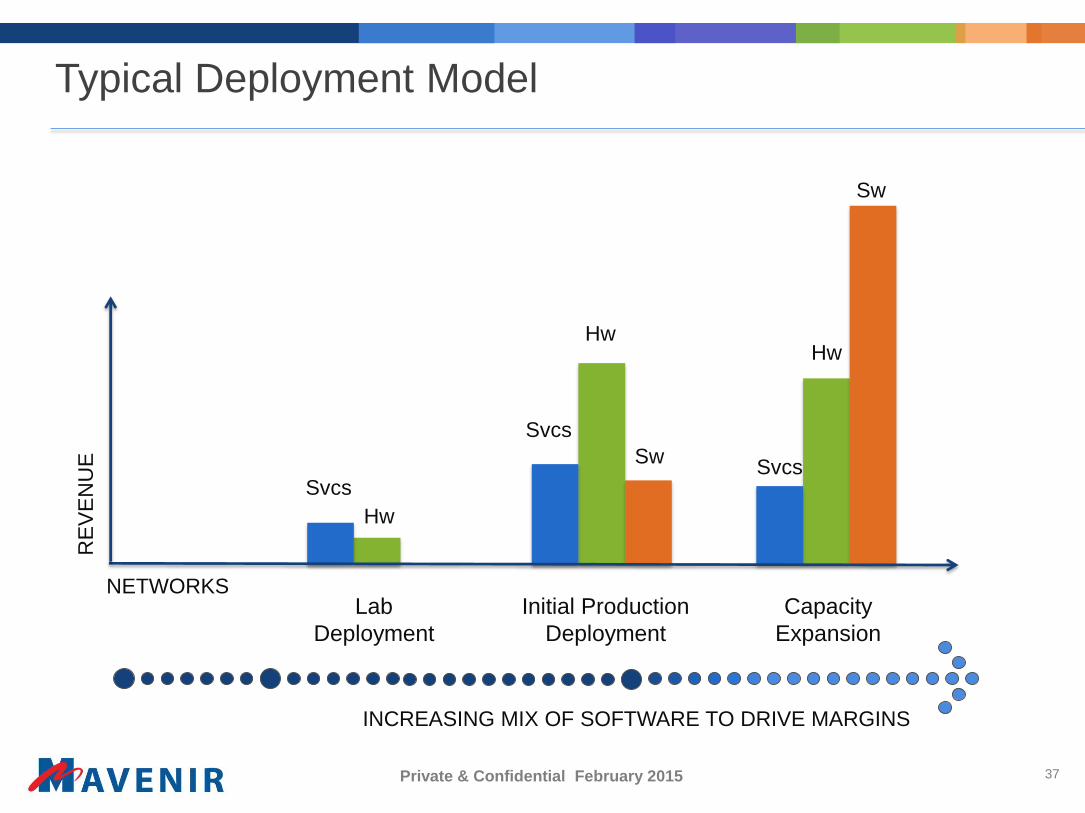

Typical Deployment Model

Svcs

Hw

Svcs

Hw

Sw

Lab

Deployment

Initial Production

Deployment

Capacity

Expansion

NETWORKS

RE

VE

NU

E

Svcs

Hw

Sw

INCREASING MIX OF SOFTWARE TO DRIVE MARGINS

38Private & Confidential February 2015

Pricing Structure

Messaging

• PRS/XDMS

• mStore

• RCS, IPSM GW

• SMSC, MMSC

• Video/Voice Mail

IP Core

• I/S/P-CSCF

• EIR, HSS, AG

• SBC/ICS GW

• WebRTC GW

• EPC, SEG, DRA

$2.95/sub $9.00/sub

Voice & Video

• TAS/MRF

• SCC/VCC

• IWF/CSFB

• CCPS/Client

• IMS-PBX

• Per Project

• Per Customer

• $/Unit

Hardware

Professional

• Day Rates

Maintenance

• Annual

• 10-15%

Optional$2.65/sub Variable

ServicesSoftware (Standard SW Discount)

Funnels into Average Sales Price per Subscriber

$1.75 $0.50$2.25 $4.50 =

39Private & Confidential February 2015

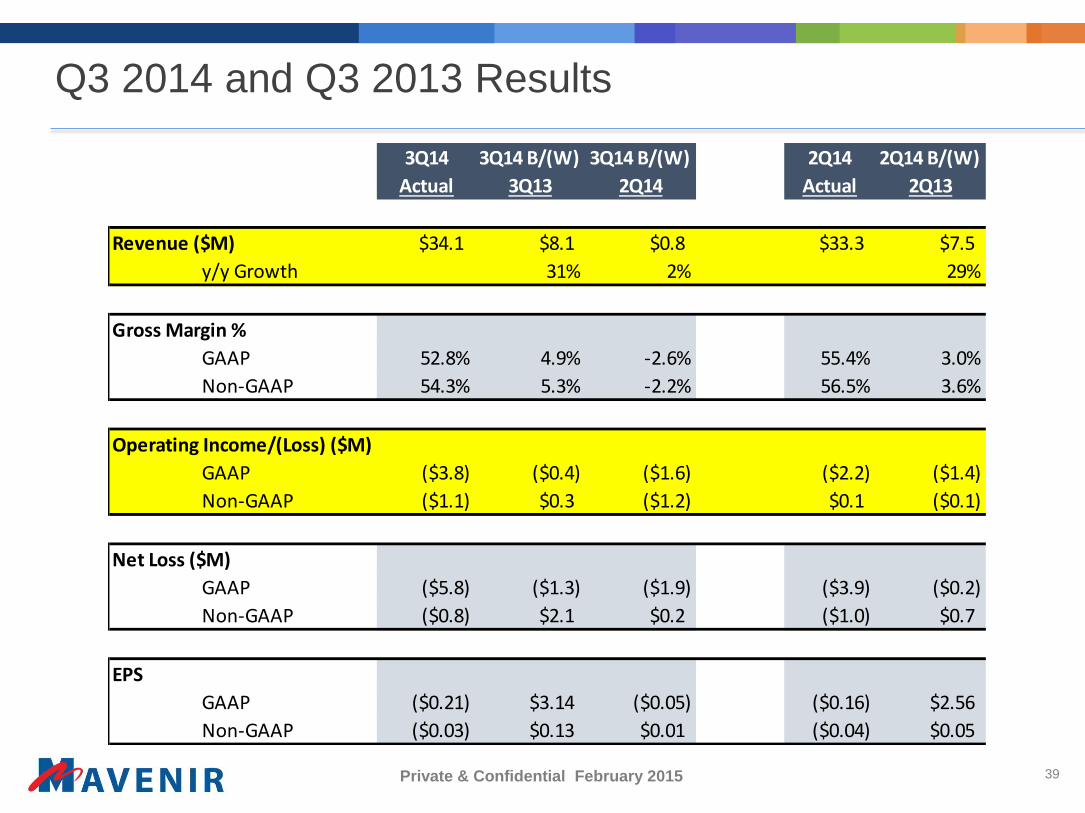

Q3 2014 and Q3 2013 Results

3Q14 3Q14 B/(W) 3Q14 B/(W) 2Q14 2Q14 B/(W)

Actual 3Q13 2Q14 Actual 2Q13

Revenue ($M) $34.1 $8.1 $0.8 $33.3 $7.5

y/y Growth 31% 2% 29%

Gross Margin %

GAAP 52.8% 4.9% -2.6% 55.4% 3.0%

Non-GAAP 54.3% 5.3% -2.2% 56.5% 3.6%

Operating Income/(Loss) ($M)

GAAP ($3.8) ($0.4) ($1.6) ($2.2) ($1.4)

Non-GAAP ($1.1) $0.3 ($1.2) $0.1 ($0.1)

Net Loss ($M)

GAAP ($5.8) ($1.3) ($1.9) ($3.9) ($0.2)

Non-GAAP ($0.8) $2.1 $0.2 ($1.0) $0.7

EPS

GAAP ($0.21) $3.14 ($0.05) ($0.16) $2.56

Non-GAAP ($0.03) $0.13 $0.01 ($0.04) $0.05

40Private & Confidential February 2015

Highly Diversified Revenue Profile

Americas47%EMEA

38%

Asia15%

REVENUE PROFILEBY REGION 2013

SW Products78%

Maint. Services

22%

REVENUE PROFILEBY COMPONENT 2013

Direct 48%

Channel Partners

52%

REVENUE PROFILEBY SOURCE 2013

Voice& Video

34%Enhanced Messaging

66%

REVENUE PROFILEBY PRODUCT 2013

Americas52%

EMEA35%

Asia13%

YTD 3Q14

SW Products

81%

Maint.Services

19%

YTD 3Q14

Voice& Video

69%

EnhancedMessaging

31%

YTD 3Q14

Direct68%

ChannelPartners

32%

YTD 3Q14

41Private & Confidential February 2015

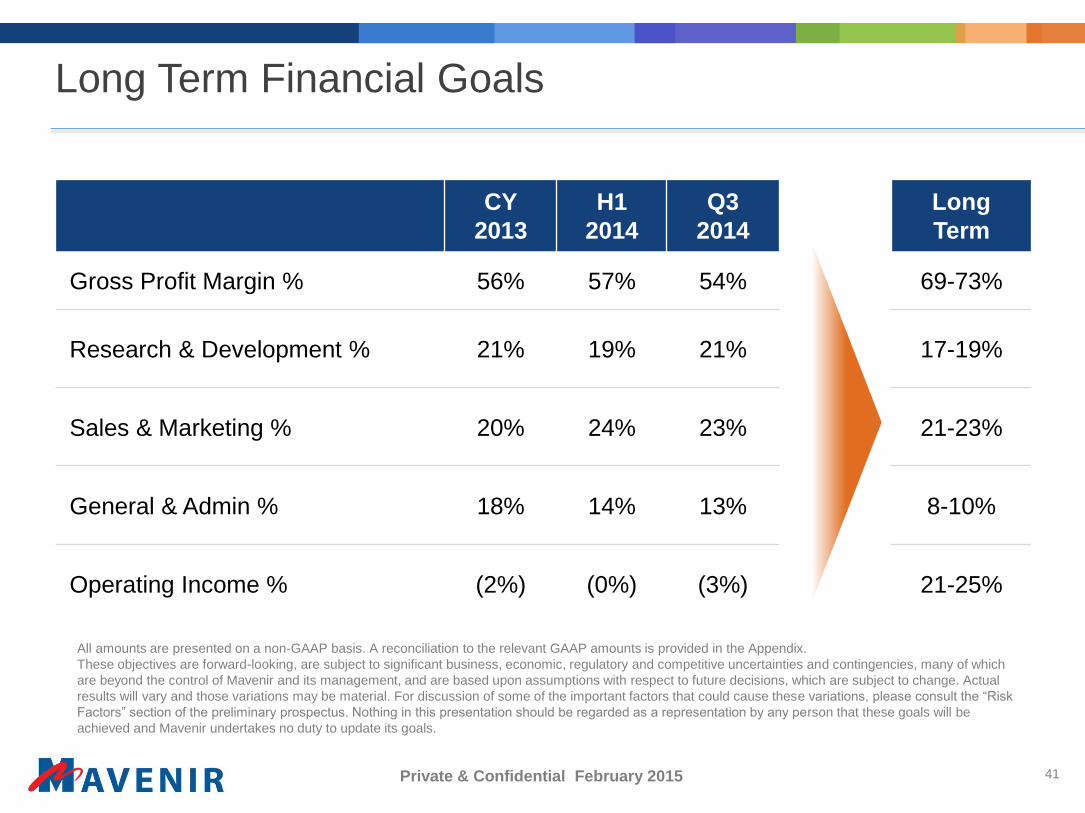

Long Term Financial Goals

CY

2013

H1

2014

Q3

2014

Long

Term

Gross Profit Margin % 56% 57% 54% 69-73%

Research & Development % 21% 19% 21% 17-19%

Sales & Marketing % 20% 24% 23% 21-23%

General & Admin % 18% 14% 13% 8-10%

Operating Income % (2%) (0%) (3%) 21-25%

All amounts are presented on a non-GAAP basis. A reconciliation to the relevant GAAP amounts is provided in the Appendix.

These objectives are forward-looking, are subject to significant business, economic, regulatory and competitive uncertainties and contingencies, many of which

are beyond the control of Mavenir and its management, and are based upon assumptions with respect to future decisions, which are subject to change. Actual

results will vary and those variations may be material. For discussion of some of the important factors that could cause these variations, please consult the “Risk

Factors” section of the preliminary prospectus. Nothing in this presentation should be regarded as a representation by any person that these goals will be

achieved and Mavenir undertakes no duty to update its goals.

Private & Confidential February 2015

Transforming Mobile Networks from 2G/3G to 4G LTE

Appendix

43Private & Confidential February 2015

Broad 4G Product Portfolio

Subscriber Data

HSS HLR UDR

Accounting

Online Offline

Service Platforms

SCPs OSA/Parlay Web 2.0

Policy

Anti-Spam Anti-Virus

Legacy Networks

SMS MMS Email

RMSTAS PRS

Session ControlMGCF

IBCF

XDMS

Oauth

Mavenir Product

DRA

Session Border

EATF E-CSCF ATCF

P-CSCF ATGW

CCF

Voice

HSS/ENUM FE

LRF

IBCF

PCRF

3rd Party Partner

Existing Equipment

I-CSCF S-CSCF BGCFE-CSCF

LI MF

Evolved Packet Core

SGW PGW ePDG

EIR

VoLTE IWF

SR-VCC CSFB IM-SSF VVM

PS RLS SMSC HNR

MMSCRCS

IPSM-GW

MRF

UDR

HLR

AAA

ENUM

NP

MME

mStore™

IMAPVVM

AG

A-SBC

WebRTC

EATF LRF

VCCMMTELSCC

IPX Proxy

HSS

44Private & Confidential February 2015

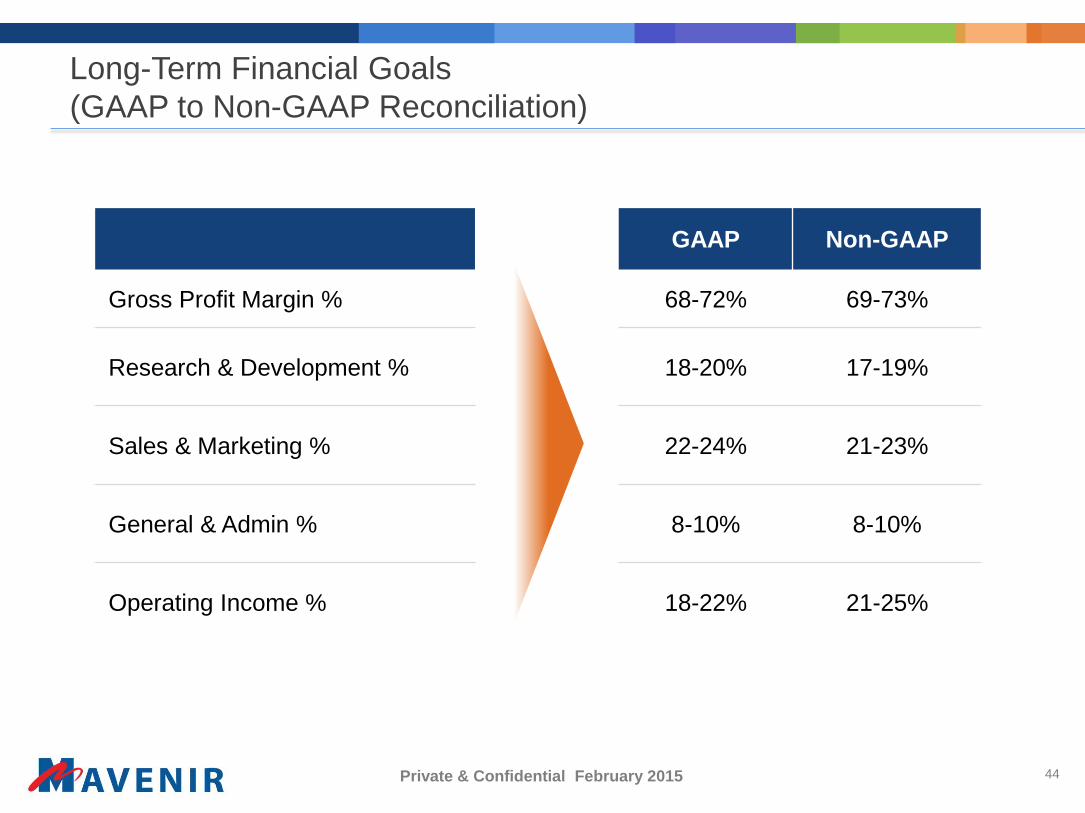

Long-Term Financial Goals

(GAAP to Non-GAAP Reconciliation)

GAAP Non-GAAP

Gross Profit Margin % 68-72% 69-73%

Research & Development % 18-20% 17-19%

Sales & Marketing % 22-24% 21-23%

General & Admin % 8-10% 8-10%

Operating Income % 18-22% 21-25%

45Private & Confidential February 2015

Q3 2014 Results

(Non-GAAP Net Loss Reconciliation)

*(Note: 000’s USD except share and per share data)

Three Months Ended

30-Sep-14

Total Revenue $34,052

Gross Profit (GAAP) $17,982

Amortization and Depreciation 279

Stock Based Compensation 221

Gross Profit (Non-GAAP) $18,482

Operating Income (GAAP) ($3,837)

Amortization and Depreciation 1,336

Stock Based Compensation 1,357

Operating Income (Non-GAAP) ($1,144)

Net Interest $404

Pre-Tax Income ($1,548)

Income Taxes (GAAP) ($657)

Adjustment for Uncertain Tax Provisions (102)

Net Loss (Non-GAAP) ($789)

Adjusted weighted average common shares outstanding 27,392,000

Non-GAAP Net Loss Per Share ($0.03)