Telkom SA SOC Limited Group Annual Results

48

Group Annual Results 2018 | 1 Telkom SA SOC Limited Group Annual Results for the year ended 31 March 2018

Transcript of Telkom SA SOC Limited Group Annual Results

Group Annual Results 2018 | 1

Telkom SA SOC Limited

GroupAnnual Resultsfor the year ended 31 March 2018

Group Annual Results 2018 | 2| Business Performance01

Tough trading environment

Low GDP growth

Low business confidence

Consumers under pressure

Macro-economic conditions

Enquiries in market structure

Consolidation in the market

Capital intensity

Competitive environment

Cost to communicate

ICT policy & spectrum

Deferred Investments

Political & Policy Uncertainty

Group Annual Results 2018 | 3Group Annual Results 2018 | 3

01

Business Performance

Group Annual Results 2018 | 4| Business Performance01

Solid performance

Operating revenue

R41.0 bn

EBITDA margin

25.7%

Capex to revenue

19.3%

Annualdividend of

355.0 cents

Headline earnings per share

597.0c

Group Annual Results 2018 | 5| Business Performance01

Investment strategy bearing fruit

Aggressive growth in the mobile

business

Strong growth in fibre and

data ecosystems

Leadership renewed

Strong balance sheet

Growth in future revenue streams

albeit from a lower base

Group Annual Results 2018 | 6|

Sharpening our focus

Business Performance01

GROUP

Key focus areas

> Mobile growth

> High speed broadband growth

> Content and VAS

Group Annual Results 2018 | 8|

Driving growth through mobile

Business Performance01

1 912 2 7723 730794

1 2271 478

FY2016 FY2017 FY2018

‘00

0

Pre-paid Post-paid

2 707

3 999

5 208

Subscriber growth

30.2%

2 663 2 9863 974

FY2016 FY2017 FY2018

Site

s

Mobile sites integrated

33.1%

530 724 874

1 3611 605

2 753

FY2016 FY2017 FY2018

‘00

0

Data only Smartphone users

Mobile broadband subscribers

Mobile broadband traffic

123.6%

55.7%

1 891

2 329

3 627

3786

192

FY2016 FY2017 FY2018Pe

tab

ytes

Group Annual Results 2018 | 9|

High speed broadband customers

1 173

Migration to new technologies

03 Financial overview

860

Speeds

468 532 454

72125

13977

176518

3

27

62

FY2016 FY2017 FY2018

ADSL VDSL LTE Fibre

620

36.4%

0 20 40 60 80 100 120

Fibre

LTE

VDSL

ADSL

Group Annual Results 2018 | 10| Business Performance01

Next Generation Products

• 30% of postpaid customer on FreeMe

• ARPU uplift from migration to FreeMe

• 2.8 million FreeMe bundles sold

• LTE postpaid customers grew 54.9%

• Expansion of our fixed wireless LTE smart offeringsto the pre-paid base

• Attracted 255k LTE prepaid customers in the 2nd half of the year

• 10Mbps base up 25%

• Fixed broadband ARPU up 20.5%

• 54.5% growth in the uncapped product

• 62% growth in data due to increased video usage & uncapped usage

Group Annual Results 2018 | 11| Business Performance01

Content is king

• LIT Video and LIT Music unique users grown substantially since inception in Sep 2017

► >200k LIT Music unique users

► >160k LIT Video unique users

• LIT TV – video capable broadband services

► Approximately 20 000 LIT TV boxes in market

Group Annual Results 2018 | 12

Key focus areas

> Modernise the network

> Commercialise the network

> Transforming service delivery

Group Annual Results 2018 | 13|

LTE/LTE-A/5G

VDSL/FTTH

Fibre/ME

POTNMetro L2/L3

Access SDN DC SDN L2/L3 SDN DC SDN

POTN Core

Satellite Microwave

High speed and reliability | Unlimited bandwidth| Near-real-time latency | World class security

Source: Openserve Technology and Business Strategy

Investing in data & broadband ecosystem

ME

Core Cloud

ME

ME ME

Edge Cloud

01 Business Performance

Group Annual Results 2018 | 14| 01 Business Performance

The Fibre Footprint Passed over 2.5 million premises

Fibre to the home

356 684Fibre to the cabinet

2 237 057

62.3% 12.3%

Fibre network of

> 157 400 kmdeployed to date

Group Annual Results 2018 | 15| 01 Business Performance

Gaining tractionFixed line broadband data consumption1

1. Access links

Fibre to the business

89 818end points terminating

Fibre to the base stations

6 791base stations

461617

828

FY2016 FY2017 FY2018

Peta

byt

es

Homes connected

109 336 connectivity rate of

30.7%

34.3%

70.3% 14.6%

Group Annual Results 2018 | 16| 01 Business Performance

Broadband evolutionData solutions Evolution

145 186 132 340 115 900

FY2016 FY2017 FY2018

Serv

ices

Traditional technology

23 517 27 336 34 938

FY2016 FY2017 FY2018

Serv

ices

Next generation Ethernet Technology

577 279417 519

288 243

FY2016 FY2017 FY2018

Co

nn

ecti

on

s

Traditional Broadband

450 228586 002 690 163

FY2016 FY2017 FY2018

Co

nn

ecti

on

s

Next Generation Broadband

Broadband connection evolution

12.4%

31.0%

27.8%

17.8%

Group Annual Results 2018 | 17| 01 Business Performance

Ramping up service

24%reduction

Re-dispatchrate

16%Increase in Interaction

NPS

Frontline customer interactions every day

~3 000

Group Annual Results 2018 | 18

Key focus areas

> Unified communications

> Cloud computing

> Big data analytics

> Industrial IoT (IIoT)

> Cyber Security

Group Annual Results 2018 | 19| 01 Business Performance

The migration journey

August

– Telkom Group acquires BCX

2015

November– Telkom Enterprise integrated into BCX

2016

April– Telkom Group IT integrated into BCX

2017

•Merged 6 entities to form “One BCX”

•Disposed 4 small BCX subsidiaries

• Identified non-current assets held for sale – action underway

2018

Group Annual Results 2018 | 20|

Less public sector sales

Business Performance01

Large Enterprise

Medium Enterprise

International

Public Sector

Large Enterprise

Medium Enterprise

International

Public Sector

FY2017

FY2018

9.0

7.5

5.5

0.6

7.4

7.9

5.6

0.6

+0.4

-

+0.2

-1.6

-R1bn

Public sector

> 35% of BCX revenue is from public

sector

> R1.6 billion decline mainly from

voice revenue

• general reduction of public

sector expenditure

• decline in traditional voice

revenue

• the inclusion of a number of one-

off hardware deals in the prior

year

> Management of reputational risk in

new customer acquisition

Large & Medium size Enterprise

> Large & Medium size entities

represents 37% and 26% of BCX

revenue respectively

• Large Enterprise revenue grew

by R400 million, as cross

synergies between BCX and

Telkom customers were realised

• Medium size entities grew by

R200 million with good growth

in data volumes

BCX Elims

BCX Elims -0.4

-0.3

Group Annual Results 2018 | 21| 01 Business Performance

Driving Efficiencies

Process optimisation

> Business process

re-engineering to

simplify the business

model

> Simplified corporate

structures

People Procurement

> Talent management –

appropriate capability to

deliver on strategy

> Improved our BBBEE

rating – Level 3

> Centralised procurement

function to take advantage of the

Group scale

> Restructure our cost base to shift

from hard IT-led assets and

towards talent-led ICT integration

capabilities

Group Annual Results 2018 | 22| 01 Business Performance

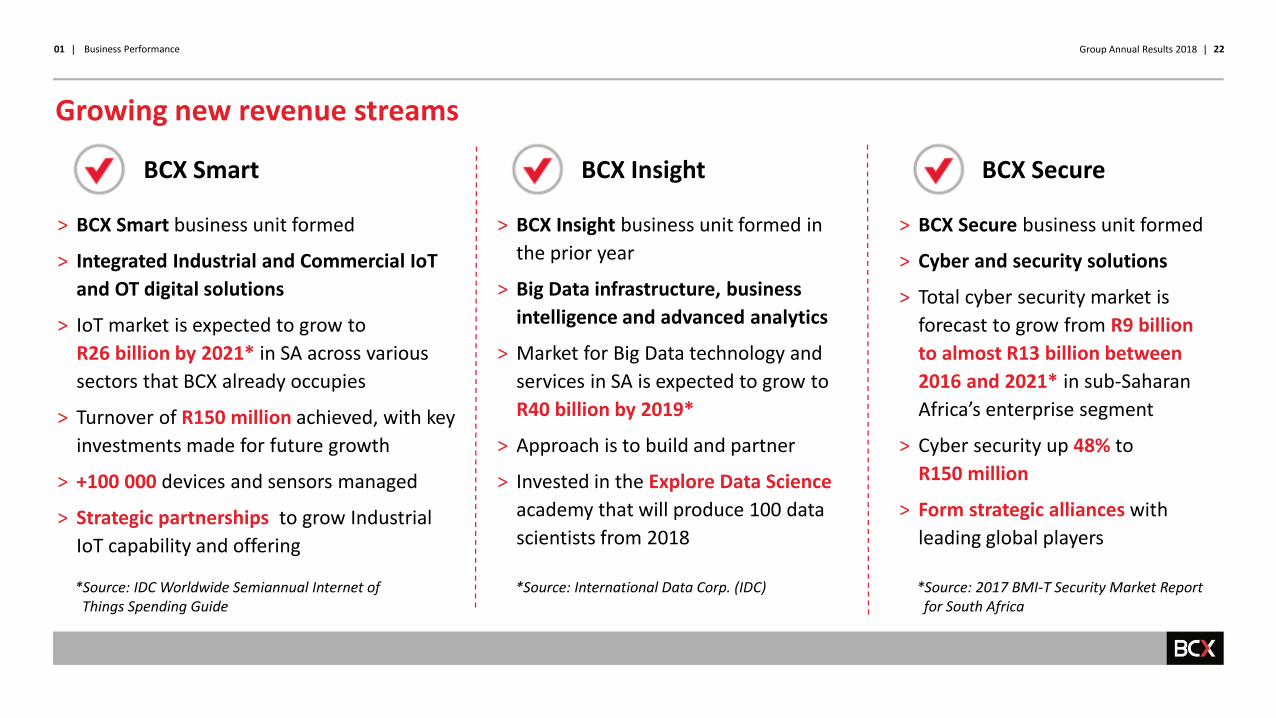

Growing new revenue streamsSocial impact

BCX Smart BCX Insight BCX Secure

> BCX Smart business unit formed

> Integrated Industrial and Commercial IoT

and OT digital solutions

> IoT market is expected to grow to

R26 billion by 2021* in SA across various

sectors that BCX already occupies

> Turnover of R150 million achieved, with key

investments made for future growth

> +100 000 devices and sensors managed

> Strategic partnerships to grow Industrial

IoT capability and offering

> BCX Insight business unit formed in

the prior year

> Big Data infrastructure, business

intelligence and advanced analytics

> Market for Big Data technology and

services in SA is expected to grow to

R40 billion by 2019*

> Approach is to build and partner

> Invested in the Explore Data Science

academy that will produce 100 data

scientists from 2018

> BCX Secure business unit formed

> Cyber and security solutions

> Total cyber security market is

forecast to grow from R9 billion

to almost R13 billion between

2016 and 2021* in sub-Saharan

Africa’s enterprise segment

> Cyber security up 48% to

R150 million

> Form strategic alliances with

leading global players

*Source: International Data Corp. (IDC)*Source: IDC Worldwide Semiannual Internet of Things Spending Guide

*Source: 2017 BMI-T Security Market Report for South Africa

Group Annual Results 2018 | 23

Key focus areas> Commercialise the

property portfolio

> Optimise and grow the Mast & Tower portfolio

> Enhance building operation efficiencies

Group Annual Results 2018 | 24| 01 Business Performance

Unlocking value

Optimising M&T Portfolio

Commercialising Property Portfolio

Optimising Building Operations

• 40 properties selected for Phase

1 development pipeline

• Commenced with town planning

and development planning

• Exploring project development

funding options

• Exploring strategic partnership

opportunities

• Focus on meaningful social

responsibility

• >1 400 properties under

management

• Utilities management, space

utilisation efficiencies as

focus areas

• Energy and water

consumption reduction

focus

• Office consolidation to

optimise occupancy costs

• 6 500 towers across

South Africa

• 1 300 co-located towers

• 1 000 towers prime for additional

co-location

• Intensified and targeted tenant

recruitment

• New build program and acquisition

to grow the portfolio

Group Annual Results 2018 | 25| 01 Business Performance

M&T Commercialisation

External Revenue Growth(R’ million)

496 539

FY2017 FY2018

External Co-Location Tenancy Growth(# of tenants)

2 362 2 581

FY2017 FY2018

9.0%

9.0%

Group Annual Results 2018 | 26

Key focus areas

> Stabilise the Business

> Optimise and rationalise traditional costs

> Rebuild iYP to create an eMarketplace

> Reposition, refresh and evolve the brand

Group Annual Results 2018 | 27| 01 Business performance

Organisational recovery

• Strengthened the Risk, Governance and

Control environment

• Established a Special Task Team to recovery of

funds from the fraudulent entities

• New leadership team – CEO and CFO

• Trudon rebranded to Yellow Pages

> Yellow Pages remains a trusted brand with

heritage of servicing SME’s for the past 58 years

> Significant investment required to achieve the

same brand equity of the Yellow Pages

> Yellow Pages App achieved over 16 000 downloads

since launch in February 2017

Rebranding

Group Annual Results 2018 | 28| 01 Business performance

Market context

• Flat economic growth.• Changing structure of the GDP key contributors

with financial services contributing 20%.• Economic downgrade

• The voice of the client is becoming stronger.• Print business revenue dropping.• Revenue from Digital not growing fast enough• Technology is becoming a key enabler and data a source

of future competitive advantage.• Digital platform business is becoming stronger.

• Regulation lagging Digital and eCommerce.• Digital Skills scarcity / transformation challenge.• eCommerce is growing at 20% yoy• Mobile spent is forecast to grow by 65%.

Source: various public stats and internal research

Broader context

Market

Yellow Pages

Group Annual Results 2018 | 29| 01 Business performance

The Transformation Journey

Source: Idea group strategic presentation

MEDIA eCommerce

pYP iYP aYP WebCard WebSite Location MediatYP

OTT Products

Owned Platforms

Simplified Consolidated Experience Design

• Improve Quality of Service

Leads and Data

Print Desktop Mobile

• Strong play in digital

verticals such as Home

services, Automotive

Medical and Food

• Simplified platform to

reflect an experience

that meets customer

needs

• Increase Sales Channels

Group Annual Results 2018 | 30| 01 Business performance

The future – Yellow Marketplaces

Yellowpages.co.za

Mobile site Mobile App

Directory ServicesSearch

IntelligentSearch

DataCRM

FinancialSystems

eCommerce Platform

B2B

Corporate Partners

Financial & Professional Services

Payment Processing

Engine

Engage, Connect, Experience design

Consumer

SME

Security/Credentials/Integration Layer

Group Annual Results 2018 | 31Group Annual Results 2018 | 31

02

Human and Social Capital

Group Annual Results 2018 | 32|

Investing in our talent

Effective talent management

• Succession plans for 94% of all senior managers

• 58% of permanent placement from internal talent

• Migrating skills for future competitiveness

Training & Development

• Training & development spend grew 47% of R342 million

• Average of 17 hours per employee on training

Significant safety improvements

• 29% improvement in total recordable injuries

• 26% improvement in lost time/ days away from work

• Safety partnership with contractors

02 Human and social capital

Group Annual Results 2018 | 33|

Skills - To address the skills shortage in the ICT sector FutureMakers - Enterprise and Supplier Development Fund

WeThinkCodeAdditional 133 students to gain software engineering related workplace experience

Data Science AcademyFunded 100 learnerships for SETA- accredited one year data science programme

Training of teachersICT integration training provided to 4 269 teachers

R381 millioninvested into FutureMakers

+2500 small businesses benefitted from non-

financial support and 1 600 direct jobs created

Innovation programme &

incubation

Growing skills, enabling ICT entrepreneur

02 Human and social capital

Group Annual Results 2018 | 34Group Annual Results 2018 | 34

Financialoverview

03

Financial Overview

Group Annual Results 2018 | 35| 03 Financial overview

Overview

Impressive growth in our new revenue streams while managing traditional voice revenues

Revenue growth

Working capital and free cash flowContinued focus on our working capital management has positively impacted our free cash flow

Efficient capex deployment We continue to invest in our network for future growth. We were cognisant of the revenue pressures and focused on maximising long term capital returns

Cost management

Continued focus on cost containment. In real terms cost is down by 1.2%

Overview

Group Annual Results 2018 | 36|

Solid performance in a challenging environment

03 Financial overview

FY2018 FY2017 %

Operating Revenue 41 018 40 970 0.1

Net revenue 32 156 31 854 0.9

Operating expenses (excl. depreciation) 22 219 21 647 (2.6)

EBITDA 10 544 10 941 (3.6)

Taxation 1 133 704 (60.9)

Capital investments 7 909 8 654 (8.6)

Adjusted free cash flow 501 (137) 465.7

Headline earnings per share (cents) 597.0 731.4 (18.4)

Group Annual Results 2018 | 37|

2 5283 498

5 150

FY2016 FY2017 FY2018

Rm

3786

192

FY2016

Peta

byt

es

EBITDA (excluding internal costs)

Mobile data broadband trafficMobile service revenue

89 89 98

FY2016 FY2017 FY2018

Blended mobile ARPU

10.2%

123.6%47.2%

163.9%

Impressive performance from mobile

-43660

1 742

FY2016 FY2017 FY2018

03 Financial overview

FY2018

Ran

d

Rm

FY2017

Group Annual Results 2018 | 38|

25 515 24 337 23 191

FY2016 FY2017 FY2018

Rm

472

632848

FY2016

Peta

byt

es

Fixed voice ARPU

Fixed broadband

traffic volumes

Fixed service revenue

34.3%4.7%

1.9%

Managing decline in fixed revenue streams

367 368 361

FY2016 FY2017 FY2018

03 Financial overview

FY2018

Ran

d

FY2017

Group Annual Results 2018 | 39|

116 762 107 612 94 236

FY2016 FY2017 FY2018

Serv

ices

12 745 16 338 24 088

FY2016 FY2017 FY2018

Cir

cuit

s

8 129 39 640

109 336

FY2016 FY2017 FY2018

Cu

sto

mer

lin

es

Sub-rate services

FibreMetro-Ethernet

35 02432 460

30 036

FY2016 FY2017 FY2018Se

rvic

es

7.5%

175.8%

47.4%

12.4%

Managing decline in fixed revenue streams (continued)

03 Financial overview

Diginet

Group Annual Results 2018 | 40|

3 498

14 546

5 620

1 052 3 119

5 150

13 245

5 326

1 574 3 046

Mobile service revenue Fixed voice Traditional data products New data products Other data products

2017 2018

Fixed data

Fixed service revenue

4.7%

47.2%

8.9%

5.2%

49.6%2.3%

1.6%

Managing decline in fixed revenue streams (continued)

Rm

03 Financial overview

Group Annual Results 2018 | 41|

31 854 32 156

1 746(1 176)

155 242(528)

(137)

FY2017 Netrevenue

Mobile Voice Fixed data Cost of sales Informationtechnology

Other FY2018 Netrevenue

New revenue streams offset pressures in voice

Net revenue movement

0.9%

R302m

03 Financial overview

Group Annual Results 2018 | 42|

10 941 10 544

302 105 (71) (127)(185) (421)

FY2017EBITDA

Netrevenue

S,G&A Operatingleases

Otherincome

Servicefees

Employeeexpenses

FY2018EBITDA

EBITDA

EBITDA movement

3.6%

R397m

03 Financial overview

Group Annual Results 2018 | 43|

FY2018 FY2017 %

Mobile 2 319 1 936 19.8

Fibre 2 112 2 392 11.7

OSS/BSS programme 294 741 60.3

Network rehabilitation/sustainment 303 567 46.6

Service on demand 1 292 1 251 3.3

Core network 902 962 6.2

Investing for growth

03 Financial overview

Group Annual Results 2018 | 44|

FY2018 FY2017 %

Cash sources

Opening cash balance 1 519 2 542 (40.2)

Cash flow from operating activities 8 274 7 713 7.3

Net loans raised 2 995 892 235.6

Significant cash applications

Cash paid on capital expenditure (7 773) (8 479) 8.3

Dividend paid (2 190) (2 171) (0.9)

Cash at the end of the period 2 698 1 519 77.6

Adjusted free cash flow 501 (137) 465.7

Discretionary investments 1 672 2 514 (33.5)

Cash position to support growth

03 Financial overview

Group Annual Results 2018 | 45|

FY2018 guidance

FY2018 Actual

FY2019 – FY2021 guidance

Operating revenue Flat 0.1 Mid-single digits

EBITDA margin 23% - 25% 25.7% 24% - 27%

Capex to revenue 17% - 20% 19.3% 16% - 20%

Net debt to EBITDA ≤ 1 0.6 ≤ 1

Guidance

Annual dividend of 355 cents per share

03 Financial overview

* Excluding corporate action

Group Annual Results 2018 | 46Group Annual Results 2018 | 46

04

Outlook

Group Annual Results 2018 | 47|

Strategic focus areas for each business unit

04 Outlook

• Modernise the

network

• Commercialise the

network

• Transforming

service delivery

• Unified

communications

• Cloud computing

• Big data analytics

• Industrial IOT

• Cyber Security

• Mobile growth

through data-led

propositions

• High speed

broadband

• Content and VAS

• Stabilise the Business

• Optimise and

rationalise traditional

costs

• Rebuild iYP to create

an eMarketplace

• Reposition, refresh

and evolve the brand

• Commercialise the

property portfolio

• Optimise and grow

the Mast & Tower

portfolio

• Enhance building

operation

efficiencies