Telematics: Wheels in motion - finity.com.au · Market Update Recent Launches and market action...

34

© 2015 Finity Consulting Pty Limited Telematics: Wheels in motion Finity Personal Lines Pricing and Portfolio Management Seminar 30 April 2015 Jon Tindall

Transcript of Telematics: Wheels in motion - finity.com.au · Market Update Recent Launches and market action...

© 2015 Finity Consulting Pty Limited

Telematics:

Wheels in motion

Finity Personal Lines Pricing

and Portfolio Management Seminar

30 April 2015

Jon Tindall

Overview

1. Quick Market Update

2. Alternative Customer Propositions

3. Technology, Data & Scoring

4. Using the Data for Pricing & Portfolio

Management

5. Into the Crystal Ball

6. Wrap-up

2

Market Update

Market Update

Recent Launches and market action

AAMI – SafeDriver App

QBE – Launched 2013 – moving to an app strategy

What's been happening overseas?

UK - 2% penetration – mainly in the younger market

EU – Italy estimate to see 5% penetration by end of 2015

- Octo launches Rider 1 – 1st motorcycle telematics

product

India - Liberty Videocon undertaking trial in Mumbai

Japan - MS&AD spent £105m on buying InsureTheBox 4

Market Update

5

More than 50 Insurance brands have entered the

telematics market globally

+ NZ

South Africa

Source: Wunelli 2014

AAMI SafeDriver

Early-mover advantage – owning the

safe-driver ‘angle’

First app-based telematics launch in

Australia

Auto-start functionality

No significant premium discounting at

the moment

using competitions and ‘safety’

as the incentives.

$100k Competition prize –

“Australia’s Best Driver” 6

Feedback

7

“Inaccurate speed limits”

“rigged competition”

“As if I’d trust an insurance

company ….”

“Keeps getting me for speeding when im not!, unreliable”

“They say that now but this is just the start

….”

“Not a good competition

when there are so many bugs”

“….. your app is no good, it's got no idea of the posted speed”

8

Alternative Customer

Propositions

Marketing drive/focus

How do you differentiate your Telematics product /

program?

Safe-driving is a common theme – but what other

options are there?

Requires some ‘thinking outside the box’

Product Design – thinking outside the box

10

Technology options Benefit mechanisms

Product Design – Case Studies

AXA

Individualised driver score and Premiums

Upfront discount + review of premium after

3,6 and 9 months

Premiums can go up or down:

62% receive a decrease (ave. = - £37)

22% have no change

16% get an increase (ave. = + £47)

11

‘Driveology’

Product Design – Case Studies

Discovery

50% of your BP fuel spend every month - max R750 –

approx. AUD$80

Contribute points towards the Excess Funder Account

Paying off excess in the case of an accident

Withdrawn for cash under particular circumstances

12

‘Vitalitydrive’

Points-style Program

Earn points for driving well or other things

that improve the risk

Spend these points on:

Premium discounts

Improved policy terms and conditions

3rd party goods and services e.g. fuel, service and repairs, retail outlets etc

Tie-ins with 3rd parties – Cheaper than the face

value of benefits + enriched data

13

‘Frequent-Flyer’ style reward program

1

Technology, Data and

Scoring

Key Rating Factors*

15

Time of Day

Speeding

Braking

Type of Road

Familiarity

Day of the Week

Location

doesn’t need to be recorded

* Assumes distance as a factor has already been accounted for

Smartphone vs ‘Box’

Which Technology?

16

Key difference is in the data

‘Snippets’ of driving behaviour

Importance of Auto-start and hence Driver

DNA

Smartphone – is this the only viable business

model for Aus & NZ in the short-term?

Which Technology?

17

Hardwire OBD II Tethered Smartphone

Data transmission cost

High High

Low Low

Identify vehicle? Yes Yes Yes No

Identify driver?

No

No

Yes

Yes

Vehicle Score? Yes Yes No No

Driver Score No No Yes Yes

Future proof No No No Yes

Mileage Yes Yes Yes No

Logistics required High

Med Med

Low

Smartphone vs OBDII

18

LexisNexis smartphone GPS test, 2012

OBDII recorded speed

40

30

20

10

0

mph

Overlay of OBDII and smartphone

40

30

20

10

0

mph

Smartphone recorded speed

40

30

20

10

0

mph

Driver DNA

19

Mapping and Ancillary Services

20

Large investment to get

the ‘enrichment’ required – i.e.

accurate speed zones and

road types

Potentially other geospatial

‘enrichment’ of the data – e.g. for

weather or traffic conditions

Using Data in Pricing &

Portfolio Management

Usage based is not enough

Just using distance as an

exposure or risk factor is

not enough

Other things influence

risk:

Road type

Speed limit

22

Road Speed

Limit

Miles

Travelled

% total

miles

Fault claim

rate per

mile

<= 40 mph 75,645,841 42% 11.6

50 - 60 mph 53,317,470 29% 4.8

70 mph 52,624,061 29% 1.0

and likely others as well:

Behaviour – speeding, braking

Time of day, familiarity, weather conditions

Predicting Claims

23

Strong correlation between driving score

and loss ratios ……

…. but little correlation between driving score and

‘risk premium’ based on traditional variables

Source: Wunelli – ‘Think Outside the Box’ 2014

Stabilisation of the Score

24

So the driving score is

predictive, but …

How quickly can the driving score be established?

80% of the variation

reduced after

approximately 600km

Source: Wunelli – ‘Think Outside the Box’ 2014

• Progressive – 6 weeks (42 days)

• TOWER NZ – now 150km (3 trips)

• AAMI – 300km (10 trips)

Translated from average UK driving

distances

0%

5%

10%

15%

20%

25%

30%

35%

0%

5%

10%

15%

20%

25%

30%

35%

1 2 3 4 5 6 7 8 9 10

At

Fau

lt C

laim

Fre

qu

en

cy

Telematics Score Quantile

Actual Traditional Model Prediction

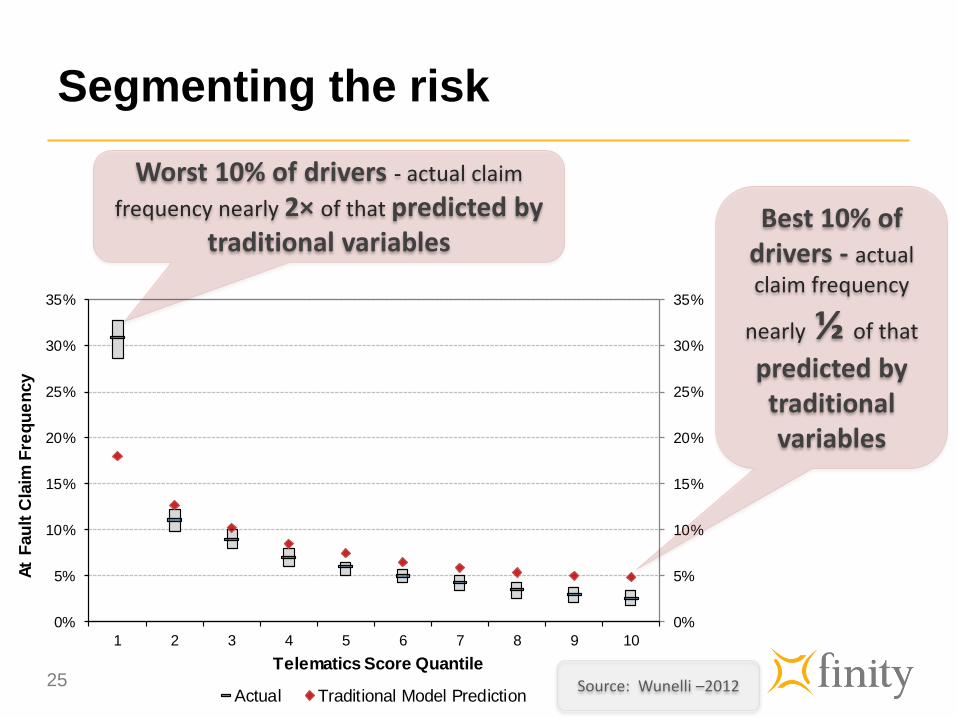

Segmenting the risk

25 Source: Wunelli –2012

Worst 10% of drivers - actual claim

frequency nearly 2× of that predicted by traditional variables

Best 10% of drivers - actual

claim frequency

nearly ½ of that

predicted by traditional variables

Into the Crystal Ball

– 20 years from now

Into the crystal Ball – 10 years from now

27

Will we be creating a class of uninsurable

risks?

How will telematics interplay with the

automation of the motor vehicle and the

connected car?

How and where will the data be

utilised?

What might the Telematics Industry

look lie in 2025?

2025 - The Connected Car

In a decade more than

2/3 of all vehicles on

the road should have inbuilt

telematics capability

28

How will this affect the insurers place in the world?

e.g. Manufactures

How will telematics

devices interact with

other car technologies?

Who is to blame? The

driver or the car?

2025 - The Connected Car

29

Apps loaded onto on-

board computer + tethered with

the smartphone. No more auto-

start or driver DNA

Follow the driver – multiple

cars, car-sharing programs, rental

vehicles

2-way ‘comms’ (upload &

downloadable content)

Integrated information

Marketing opportunities

Wrap-up

Questions for lunch ….

31

Where are things heading in Australia and NZ over the

next 12 months?

What are the predictions for 2015/16

Further launches

Product innovation / evolution

What are the challenges going to be?

The customer proposition

Privacy and security

Handling the ‘big-data’

Questions?

32

Contact

Your Name

Title

Tel: +61 2 8252 3300

Mobile:

www.finity.com.au

Jon Tindall

Senior Consultant

Tel: +61 2 8252 3300

www.finity.com.au

Distribution & Use

This presentation has been prepared for the

Finity Consulting Personal Lines Pricing &

Portfolio Management Seminar, held on 30

April 2015. It is not intended, nor

necessarily suitable, for any other purpose.

Third parties should recognise that the

furnishing of this presentation is not a

substitute for their own due diligence and

should place no reliance on this

presentation or the data contained herein

which would result in the creation of any

duty or liability by Finity to the third party.

Reliances & Limitations

Finity wishes it to be understood that the

information presented at the Seminar is of a

general nature and does not constitute

actuarial advice or investment advice.

While Finity has taken reasonable care in

compiling the information presented, Finity

does not warrant that the information

provided is relevant to a particular reader’s

situation, specific objectives or needs.

Finity does not have any responsibility to

any attendee at the conference or to any

other party arising from the content of this

presentation. Before acting on any

information provided by Finity in this

presentation, readers should consider their

own circumstances and their need for

advice on the subject – Finity would be

pleased to assist.