Technology industry analysis and outlook

14

A look at High-tech in the U.S. 2014

-

Upload

jll -

Category

Technology

-

view

1.177 -

download

0

Transcript of Technology industry analysis and outlook

A look at High-tech in the U.S.

2014

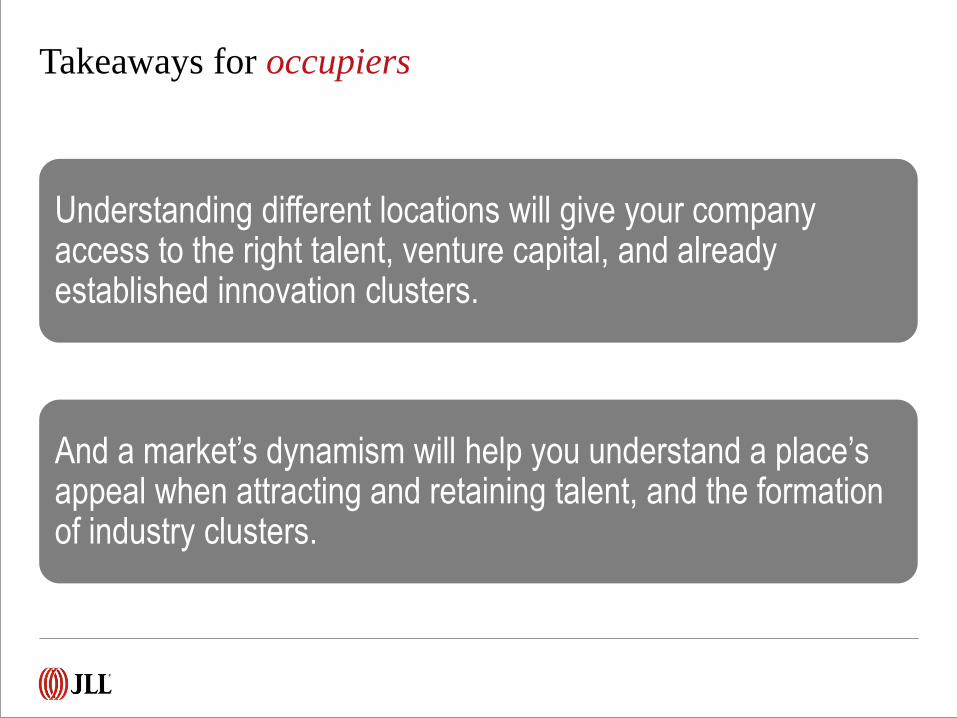

Takeaways for occupiers

Understanding different locations will give your company access to the right talent, venture capital, and already established innovation clusters.

And a market’s dynamism will help you understand a place’s appeal when attracting and retaining talent, and the formation of industry clusters.

Takeaways for investors and owners

Understanding the strength and penetration of high-tech in local markets will help guide investment decisions when targeting markets utilizing new trends in workplace design and development, buoyed by a strong industry.

And understanding workplace preference from both internal and external office perspective will help owners create places where high-tech employers and employees hope to work.

High-tech employment

Since October 2013, the sector has surpassed the dot.com peak by 69,000 jobs, reaching 3.3 million positions as of July 2014.

U.S. high-tech employment

0

500

1000

1500

2000

2500

3000

3500

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

High-tech services employment (000)

High-tech manufacturing employment

Source: Bureau of Labor Statistics

19.1% of office jobs recovered after the recession were within the high-tech services sector, compared with just 14.1% from 2003 to 2007.

Source: Bureau of Labor Statistics

19.1%

80.9%

High-tech services All other office jobs

2009-2014

High-tech employment

U.S. High-tech services share of

office employment growth

Talent and innovation insight

5

Computer-related occupations of

H-1B Visas

2011 2012 vs.

50.8% 59.0%

Total utility patents: Top 5 countries

United States

133,593

Canada 6,547 Germany

15,498

Taiwan 11,071

South Korea 14,548

Japan 51,919

The share of H-1B visa holders working in tech has increased in the last year. But the U.S. remains the innovation leader worldwide.

CA 36,193

TX 9,222

WA 5,878

MN 5,119

IL 4,644 PA

3,961

NJ 4,717

NY 8,489

MA 6,409

Utility patents by state: Top 10 states

Venture capital insight

1.5%

29.4%

44.5%

24.7% Seed Stage

Early Stage

Expansion Stage

Later Stage

VC funding by high-tech sector

65% 11%

8%

6% 3% 7%

Software

Media and Entertainment

IT Services

Consumer Products andServicesComputers and Peripherals

Rest of HT sector

$9.6B total U.S. high-tech

VC funding

U.S. VC funding vs. high-tech funding

Source: PricewaterhouseCoopers

$

$ 5,000,000,000

$ 10,000,000,000

$ 15,000,000,000 US Total HT VC FundingUS Total VC Funding

VC funding by stage of development

$13.3B total Q2 2014

U.S. VC funding

Venture capital investment still far from dot-com high

7

The stock market story

Source: NASDAQ as of July 25, 2014

Cap Range Total number

of firms Total market cap

Total number of

high-tech firms

Total high-tech

market cap

% high-tech

market cap

of total

Mega $200b + 17 $5,075,721,559,704 4 $1,754,702,519,836 34.6%

Large $10-$200b 612 $23,533,824,248,444 68 $2,650,849,622,622 11.3%

Mid $2-$10b 1,098 $4,977,448,070,552 149 $628,925,857,524 12.6%

Small $300m-$2b 1,889 $1,613,827,951,074 235 $205,996,596,473 12.8%

Micro $50-$300m 1,527 $234,878,340,486 152 $23,458,390,266 10.0%

Nano <$50m 1,452 $15,441,043,135 74 $1,882,136,019 12.2%

Total 6,595 $35,451,141,213,395 682 $5,265,815,122,740 14.9%

IPO activity remains muted compared to

dot-com bubble, but drives significant growth

of the stock market.

The stock market story

8

Source: Renaissance Capital, NASDAQ.com

1,181 high-tech companies have gone public from 1995 to 2014

1995

1996 1997 1998 1999 2000

2001

2002 2003 2004 2005 2006 2007 2008

2009

2010 2011 2012 2013

2014

748 IPOs

125

or 16.7% of these

companies remain

public today

222 IPOs

165

or 74.3% of these

companies remain

public today

268 IPOs

71

or 26.5% of these

companies remain

public today

High-tech steadies the office market recovery

9

Source: JLL Research

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Cla

ss A

ask

ing

ren

t

year

-on

-yea

r g

row

th

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

Cla

ss A

dir

ect

aver

age

as

kin

g r

ent

($ p

.s.f

.)

Rents in many of the high-tech submarkets

have jumped more than 10.0% year-over-

year…

…resulting in some of the highest asking

rents across submarkets nationally

Demographics and technology drive productivity and

utilization and the next evolution of office space use.

10

15% Space reduction by

U.S. law firms and

financial services

relocating

72% Of global CREs plan to

aggressively increase

density in next 3 years

200 s.f./employee average

target density, down

from 250-300 s.f. in 2009

50%

of the U.S. workforce

were baby boomers

in 2010. Millennials

will be 50% by 2020

The top anchor tenants across the country also

top the list of most acquisitions

11

5

3

2

2

Number of markets by

anchored company

Top 15 acquiring companies

Cisco 161

Google 154

Microsoft 134

IBM 120

Yahoo! 107

Hewlett-Packard 86

Oracle Corporation 86

AOL 63

EMC 59

Intel 57

Apple 49

eBay 48

Facebook 48

Amazon 45

Adobe Systems 38 Source: Crunch Base

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without

the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no

representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang

LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Contacts

12

For more information, please contact:

Julia Georgules

Vice President, Director of Research

+1 415 354 6908

Amber Schiada

Vice President, Director of Research

+1 415 395 4924

Christan Basconcillo

Senior Research Analyst

+1 650 815 2213

Phil Ryan

Research Analyst

+1 202 719 6295

Lauren Picariello

Senior Vice President, Director of Industry Research

+1 617 531 4208

Chirag Modi

Head of Markets Consulting

+1 248 231 0533

© Copyright 2014 Jones Lang LaSalle

Thank you

>> If you enjoyed this preview,

click here to access the full report.