Technology in Trial - Dallas Bar Association · Page 32 – Technology in Trial Using Technology to...

48

This document contains two papers prepared by Christopher Egan. Page 2 – E-Litigation Leveraging Technology Throughout Your Case Page 32 – Technology in Trial Using Technology to Persuade Four Generations

Transcript of Technology in Trial - Dallas Bar Association · Page 32 – Technology in Trial Using Technology to...

This document contains two papers prepared by Christopher Egan.

Page 2 – E-Litigation Leveraging Technology Throughout Your Case

Page 32 – Technology in Trial Using Technology to Persuade Four Generations

E-Litigation Leveraging Technology Throughout Your Case

Presentation Outline

Presented by: Christopher Egana1

August 2012 Dallas Bar Association Tax Section Meeting

E-Litigation Leveraging Technology Throughout Your Case

I. INTRODUCTION

A. Description

1. E-Discovery is a hot topic these days. Attorneys often think of e-discovery as a new burden that threatens to send litigation costs out of control. But there is a flip side to technology’s effect on litigation. If used properly, technology can help control your costs while increasing the quality of your analysis. This presentation is titled E-Litigation instead of E-Discovery because it takes a broader view of how technology can be used throughout your case to improve the quality and efficiency of your analysis. Instead of lecturing about how technology can be used, we will walk through an example case and show you how technology can be used during each stage of your case.

B. Why Use Technology?

1. Efficiency – Technology can increase your efficiency in litigation. Leveraging technology requires more work during the beginning of your case. This up-front work often discourages attorneys from using technology because they don’t see the immediate benefits. But that early work is an investment that pays off later in your case. This presentation demonstrates the pay off.

2. Focus – Technology helps you focus on your most important evidence. It provides methods for eliminating irrelevant evidence and highlighting important evidence.

3. Quality – Technology can increase the quality of your case analysis and presentation. Technology helps you organize your documents in a way that places facts within their proper context and reveals relationships: documents to documents; people to people; actions to actions; documents to people…etc…

II. OVERALL PROCESS

A. Process Your Evidence

B. Review Your Evidence

C. Build Your Case

D. Present Your Case

III. PROCESS YOUR EVIDENCE

A. Purpose

1. Convert your paper documents and digital evidence into a format that you can efficiently review.

- 2 -

2. Establish a bates-numbering system that helps you reference documents and identify their source.

B. Process

1. Paper documents are scanned into images and searchable text. The images and text are then loaded into a viewer program that allows you to review and search the documents. The text may also be loaded into a more sophisticated database.

2. Digital evidence (ex. native Outlook files or Microsoft Word files) is broken down into images, text, user-created data, and meta-data. The images are loaded into a viewer program and the data is loaded into a database.

a. User-Created Data - Native files can include user-created data that cannot be seen in a hard-copy print out. A word processing file, for example, can contain reviewer comments. Spreadsheets include cell formulas.

b. Metadata - Metadata is data that the computer automatically creates and saves in the background. It can include information like document creator, date created, changes made.

C. Example Products

1. E-Scan IT

2. LAW PreDiscovery (Lexis)

3. AD eDiscovery

4. DocuLex

5. EnCase eDiscovery

D. Practice Tips

1. When asking for help from tech support, give clear instructions. Don’t assume that your tech support person knows what you need. (See Exhibit 001)

2. Single-page tiff format is generally the easiest format to review. Tiff is a raw image format that can easily be converted into many different formats for production and presentation.

3. Use a Bates-numbering scheme that identities the document’s source.

- 3 -

IV. REVIEW YOUR EVIDENCE

A. Narrow Your Pool

1. Purpose

a. Eliminate copies.

b. Eliminate irrelevant types.

c. Eliminate irrelevant groups.

2. Process

a. Document management software can tag duplicates and near-duplicates.

b. Sophisticated search methods can identify relevant documents and eliminate irrelevant documents.

3. Example Products

a. Synthetix

b. Other

B. Eyes-On Review

1. Purpose

a. Tag important documents.

b. Set document beaks.

c. Mark privileged material.

d. Process

Briefly review each page of your narrowed-down pool of documents. As you review, tag important documents, clean up document breaks, and redact privileged material. (See Exhibit 002)

e. Example Products

(1) IPRO

(2) Other

2. Practice Tips

a. Multiple attorneys can work on the document database at the same time. Consider delegating parts of this process to other attorneys.

- 4 -

b. Buy a second monitor. A second monitor allows you to review two documents at the same time or use multiple programs at the same time.

c. Back up your work. All hard drives fail. It is not a matter of if; it is matter of when.

C. Drilling Below Your Evidence’s Surface

1. Purpose

a. Find important documents that may escape an eyes-only review.

b. Find important information buried within your documents’ metadata.

c. Search large databases of documents for which an eyes only review is impractical.

2. Process

a. To support and back up your eyes-on review, your document database can be searched for key people, organizations, locations, facts, and other concepts.

3. Example Products

a. Concordance

b. Summation

4. Efficiency of Electronic Searching

a. If done properly, electronic review is more efficient and effective than an eyes-on review

b. Stats from recent study cited in the ABA Journal on use of advanced search algorithms versus manual review (ABA Journal, “Efficient E-Discovery,” April 2012 citing Maura R. Grossman & Gordon v. Cormack, Technology-Assissted Review in E-Discovery Can Be More Effective and More Efficient Than Exhaustive Manual Review, Richmond Journal of Law and Technology (Spring 2011)

(1) Documents Needing Eyes-On Review – Reduced by 98%

(2) Relevant Documents Found – E-Search found an average of 76.7%; Manual Search found average of 59.3%

5. Practice Tips

a. Review your search results and repeat as needed. Good searches usually require multiple rounds. (See Exhibit 003)

- 5 -

b. The searching process should be repeated as you learn more about your case and receive new evidence.

c. Review your document database’s work index for different spellings.

d. Consider conceptual search methods instead of just key word searches. A leading study found that a key word search produced only 20% of the responsive documents. Information Inflation: Can the Legal System Adapt? 13 Rich. J.L. & Tech. 10, 40 (2007).

V. BUILD YOUR CASE

A. Indentify your Building Blocks

1. Purpose

a. Identify important documents.

b. Identify important people.

c. Identify important organizations.

d. Identify open questions; i.e. what factual questions do you need to answer?

2. Process

a. Carefully review and label each document that you tagged as important.

b. While naming your documents, look for important people and organizations. Input those people and organizations into your fact database. (See Exhibit 004)

3. Example Products

a. Case Map – Case Map provides a fact database. It includes a chart of document information, but it is not document management software. It is fact management software. Document management software helps you obtain the raw evidence you need to build your case. Case Map helps you take that raw evidence and build.

b. Excel

\

- 6 -

4. Practice Tips

a. Take your notes in a database. Think of Case Map as an efficient way to take notes. Instead of filling up note pads with important facts and thoughts, input those facts and thoughts into a database that can be leveraged for other uses. Efficiently leveraging technology prevents double input. As we will see in the next sections, fact management software allows you to export those same labels into production lists, exhibit lists, privilege logs, ect… You do not need to recreate document lists every time you need to identify documents.

b. Labeling your important documents takes time, but if you have strong keyboard skills, you should consider doing it yourself instead of delegating it to an associate or paralegal. Creating document labels helps you understand your case evidence while you create a document list that can be used over and over.

c. While narrowing down your list of important documents, tag pages with important facts. After your document list is finished, return to those pages and input the facts into Case Map.

d. Case Map is team friendly. Team members can simultaneously work on the same Case Map database. Each team member’s work is instantly integrated into a database.

B. Build

1. Purpose

a. Identify your facts and create a timeline.

b. Identify your issues.

c. Organize your facts by issue.

d. Identify relationships between people, organizations, and facts.

2. Process

a. Create facts that reference your building blocks.

b. After creating your facts, Case Map’s automated tools help you organize those facts by date, witness, organization, or issue. (See Exhibit 005)

3. Example Products

a. Case Map

b. Excel

c. Smart Draw

d. Power Point

- 7 -

4. Practice Tips

a. Building your case does not fit into a neat linear process. This building occurs throughout your case as you discover new information and relationships.

b. Building a case requires more than a document database. You need a fact database.

c. Documents can also be facts. Consider exporting all of your dated documents into your fact page.

d. Timelines enlighten by telling your case’s story. They help you see your case facts from a new perspective. They place facts within their proper context and reveal relationships; relationships between different events, people, and organizations. Timelines also help you and your fact finder remember important facts. Context and relationships fuel memory and understanding.

e. Determine your issues early. Your issue list is like a case blueprint. You can’t build a case without knowing where to place each block.

f. Prepare organization and flow charts during the beginning of your case. Don’t wait to until your dispositive motion or trial to create charts that display relevant organizations and transactions. Building these charts increases the quality of your analysis by helping you understand the relevant transactions. Everyone thinks they understand a transaction until they have to build a demonstrative that accurately presents the transaction.

C. Use Discovery to Disclose Your Evidence and Fill In Missing Pieces

1. Purpose

a. Prepare focused requests for production and interrogatories.

b. Prepare focused deposition questions.

c. Efficiently respond to discovery requests.

d. Identify and organize important facts obtained from depositions.

2. Production Process

a. Electronically redact and track privileged information.

b. Use the data that has already been input into Case Map to create initial disclosures, privilege logs, and other production lists.

c. Use agreed search techniques to respond to production requests.

3. Request Process

- 8 -

a. Run fact reports to identify key witness for deposition. In other words, determine how many facts each witness is a part of.

b. List all documents related to a witness for use in a deposition.

c. Assign exhibit numbers to documents and use case database to automatically create deposition exhibits and lists.

d. Refer to case timeline to identify meetings and other events. Ask about those meetings and events during depositions.

e. Refer to case timeline to identity missing documents. Include those documents in your request for production.

f. Mark key deposition testimony and tag it by issue. (See Exhibit 006)

4. Example Products

a. Text Map – Text Map is transcript management software.

b. All of the Above

c.

5. Practice Tips

a. Consider asking opposing counsel whether he or she is willing to accept electronic copies of your deposition exhibits instead of a paper notebook. If you are willing to provide your exhibits in advance, opposing counsel may appreciate this approach.

b. Consider redacting instead of withholding. Technology makes redaction easy. You need only draw a box around the privileged material, and your redaction page is automatically logged. You can even mark your redaction by type and label each redaction on the redacted page. Redacting this way instead of withholding often prevents privilege disputes. Opposing counsel need not question your description of the document because the actual document is produced with all of its identifying information.

VI. PRESENT YOUR CASE

A. Motion Practice

1. Purpose

a. Further narrow your evidence to the most important facts that establish your case.

b. Prepare organized briefs that present your facts clearly and persuasively.

- 9 -

2. Process

a. Use fact reports from your case database to organize your facts by date or issue.

b. Use your database to create timelines, fact charts, or exhibit lists that can be inserted into your brief. (See Exhibit 007)

c. Use graphing software to diagram complicated transactions.

3. Example Products

a. Time Map

b. Smart Draw

c. Power Point

d. Excel

e. or one part of a key transaction.

4. Practice Tips

a. For date-intensive cases (ex. fraudulent transfer) consider presenting your facts in a chart organized by date. You can make the chart especially useful by referencing and hyper-linking the source of each fact.

b. Avoid needlessly complicated charts. Focus on the important parts of your transaction.

c. When pasting charts into your brief, pasting your chart as an image will solve most formatting problems.

B. Trial

1. Purpose

a. Prepare pre-trial filings.

b. Prepare focused witness questions/outlines.

c. Prepare opening and closing statements.

d. Admit evidence.

e. Efficiently present your evidence.

f. Highlight your important evidence without boring your fact finder. Repetition is a common jury complaint.

g. Demonstrate important relationships with comparisons, visuals, and timelines.

- 10 -

2. Process

a. Create an exhibit list, and assign each document to a witness that can authenticate them and provide a foundation for their admission. Create sub-lists of documents organized by foundation witness.

b. Create a list of important facts that you intend to establish, and assign each fact to the witnesses that can establish them. Create sub-lists of facts by witness. (See Exhibit 10)

c. Assign exhibit numbers to documents and use your fact database to automatically create deposition exhibits and lists.

d. Present and highlight important portions of your documents using trial software.

3. Example Products

a. CaseMap

b. Sanction

c. Trial Director

d. Smart Draw

e. Power Point

f. Excel

g. All of the Above

4. Practice Tips

a. The sub-lists described above (e.g. documents, facts) can be used to delegate parts of the trial. For example, you can give co-counsel a list of facts that you need their assigned witnesses to establish.

b. Keep it simple. Trial presentations do not have to be complicated. Simple practices like highlighting and magnification increase the quality of your presentation without distracting you.

c. Effective trial presentations don’t always require a dedicated employee running the trial software. If you are comfortable with a computer, consider running a simple presentation by yourself. Once you become comfortable with the software, using it can be no more distracting than opening an exhibit note book and highlighting words with a marker.

d. Early practice avoids technology problems. Show up early and practice using your venue’s equipment.

- 11 -

VII. CLOSING COMMENTS

Invest in Your Practice – Technology requires an early investment, but that investment pays off. Using technology requires an investment of money and time. You have to spend money to buy these products and you have to spend time learning how to use them. I’ve seen that investment discourage attorneys. In the paper world, they expect immediate results. When technology does not give them that immediate result, they quit before reaping the benefits of their investment. This presentation has demonstrated some of those benefits. If used properly, technology saves you time and money while it increases the quality of your analysis.

Contact me if you have any questions. I love to discuss litigation technology. Chris Egan 214-880-9732 [email protected] a1 J.D., 2002, Southern Methodist University School of Law; B.B.A., M.P.A., 1997, The University of Texas at Austin; Certified Public Accountant, Texas. Mr. Egan worked two years as a tax accountant for Arthur Andersen, L.L.P., and he currently works as a trial attorney for the U.S. Department of Justice, Tax Division, Dallas, TX. The views expressed in this outline are the personal views of the author and are not necessarily the views of the Department of Justice or the Internal Revenue Service. Mr. Egan, the Department of Justice, and the Internal Revenue Service do not endorse any of the products discussed during this presentation. Those products are presented as examples only.

Evidence Processing Request Scanning

1. File Format: single-page tiff

2. Bates Stamping: begin with prefix marked on each box, followed by 6 digit number; restart number with each box

3. Document Breaks: insert document break at each staple, paperclip, and folder

4. OCR Text: Yes

5. Data Load File: IPRO compatible

Digital Processing of Native Files

1. Current File Location: G:\ALS_Cases\Smith_John\Digital Source Files

2. Database Software: Concordance

3. Auto Populate Description Fields: Yes – Document Date, Date Created (meta), Author, Recipient, Subject, Type

4. Bates Stamping: Yes – please process all files into tiff and stamp each page with prefix “DOJ-” followed by 6 digit number

cegan

Generic Yellow

cegan

Generic Yellow

22222144

22222145

22222157

22222182

32523223

32523224

Delton

Del‐Ton

Eight Star

EightStar

H&M Farm

H&M Well

H.A.S. Rentals

Halty Mine

HAS Rentals

Haverty

HM Farm

HM Well

Hook

HSHD

L222514

Lenderson

Lindham

M322522

Marker

Midd

Middel

PLPG

Pride

Q222521

QTOM

Ridgeharmer

Roberts

Sasson

Saulter

Smith

Space

Stasey

Tastleford

Ustig

Vrauman

X222513

Yield Fund

Z152522

Z152523

Search Terms for Database A

cegan

Generic Yellow

1/30/2012 9:23 PMCast of Characters

Full Name Role In Case Type + Addresses Key

Linda Collins Anstar Biotech Industries SalesManager - Philip Hawkins madederogatory comments about her toKaren Thomas at company 4th ofJuly picnic.

Fact Witness Org A-B123 Park WayDallas, TX [email protected]

ü

Randy Fosheim Anstar Biotech Industries plantmanager - Was at the 4th of JulyPicnic where Philip Hawkinsapparently made derogatory remarksto Linda Collins. Survived theReduction in Force.

Fact Witness Org Destruction123 Main StDallas, TX [email protected]

Anne Freeman Plaintiff damage expert Expert Witness Expert Co.123 New York Ave.New York, NY [email protected]

Philip Hawkins Plaintiff - Former Vice President ofSales at Anstar Biotech Industries.

Fact Witness 123 Park WayDallas, TX [email protected]

ü

Robert Kalinski Defense age discrimination expert Expert Witness Expert Co.123 New York Ave.New York, NY [email protected]

William Lang CEO of Anstar Biotech Industries.Decided that poor financial forecastsrequired Reduction in Force.

Fact Witness Anstar123 Park WayDallas, TX [email protected]

ü

George Ny Anstar Biotech Industries accountsreceivable collections specialist let goin RIF

Fact Witness Org A-B123 Park WayDallas, TX [email protected]

Gregory Poole Attorney from Poole and Rainfordwho is counsel for Philip Hawkins.

Opposing Counsel Poole & Poole123 Lawyer WayDallas, TX [email protected]

Confidential Attorney Work Product. Do Not Reproduce. AttorneyCPage 2 of 3

cegan

Generic Yellow

1/21/2012 1:11 PMFact Chronology

Date & Time Fact Text Source(s) Linked Issues

Mon 11/25/2002 William Lang meets Philip Hawkins while touring ConverseChemical Labs plant in Bakersfield.

Deposition of William Lang,25:14; InterviewNotes, Emailfrom Phil Hawkins at20050923 1514 to WilliamLang

12/??/2002 William Lang invites Philip Hawkins to visit Anstar BiotechIndustries facilities in Irvine.

InterviewNotes Wrongful Termination

01/??/2003 William Lang offers Philip Hawkins Sales Manager positionat Anstar Biotech Industries.

InterviewNotes, Email fromPhil Hawkins at 200509231514 to William Lang

Retaliation

Mon 01/13/2003 Philip Hawkins joins Anstar Biotech Industries as aSales Manager.

Anstar Biotech IndustriesEmployment Records

Mon 12/01/2003 Philip Hawkins promoted to Anstar Biotech Industries VP ofSales.

InterviewNotes Retaliation

Fri 01/09/2004 to Wed01/21/2004

Philip Hawkins negotiates draft Hawkins EmploymentAgreement with William Lang.

Hawkins EmploymentAgreement

Wrongful Termination

02/??/2004 William Lang tells Philip Hawkins that he has changed hismind regarding the Hawkins Employment Agreement. It isnot in force as it was never signed and changes were notfinalized.

Philip Hawkins, Deposition ofWilliam Lang, 11:3.

Wrongful Termination

03/??/2004 Susan Sheridan has dinner with Linda Collins and complainsabout Anstar Biotech Industries management.

Deposition of Linda Collins,33:15.

Wed 05/11/2005 Philip Hawkins receives Hawkins Performance Review fromWilliam Lang. Is rated a 1 "Outstanding Performer."

Hawkins PerformanceReview

Wrongful Termination,Deserved Termination

06/??/2005 William Lang makes decision to reduce size of staff. Deposition of Karen Thomas43:19

Hawkins Specific

07/??/2005 Susan Sheridan is terminated. Deposition of Philip Hawkins Pattern & Practice

Mon 07/04/2005 Philip Hawkins allegedly makes derogatory remarks aboutLinda Collins to Karen Thomas during Anstar BiotechIndustries Fourth of July picnic. Randy Fosheim inattendance.

InterviewNotes Deserved Termination

Confidential Attorney Work Product. Do Not Reproduce. AttorneyCPage 2 of 4

cegan

Generic Yellow

Issue:�� 10Employer

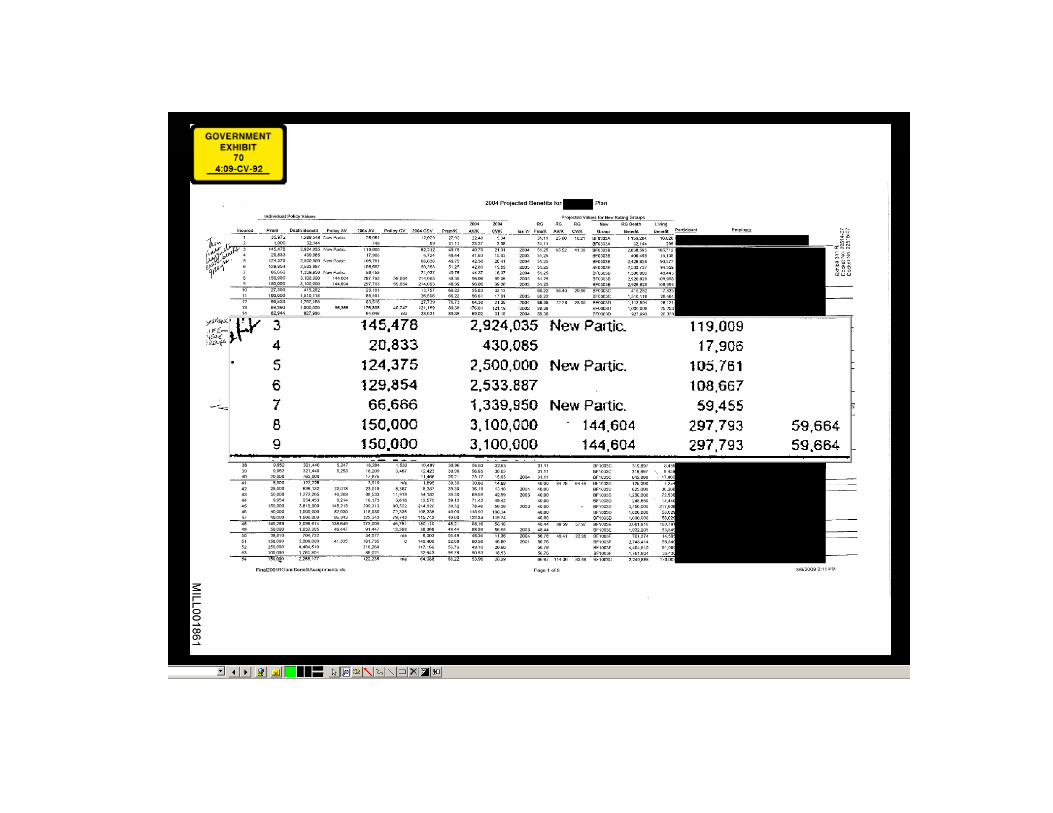

Page 8 17 Q. What were the results of that analysis? 18 A. You're aware that we changed the rating groups 19 in 2005? 20 Q. Okay. 21 A. Okay. Before that, there were a lot of 22 employers that contributed more than 10 percent within a 23 rating group because the rating groups were really 24 small -- 25 Q. Okay.Page 9 1 A. -- at that time. And then after the -- after 2 the change, I'd say about 99 percent were less than 10 3 percent. 4 Q. Okay. So the change in 2005 was a result of 5 that analysis? 6 A. I'm not sure exactly. 7 (Mr. exited the deposition room.)

Issue:�� 10Employer

Page 15 6 Q. Okay. You see the spreadsheet has -- has 7 lines, and those lines represent -- those breaks 8 represent different rating groups; is that right? 9 A. Yes. 10 Q. And you see there -- I guess it would be the 11 second group. Mr. is in that group? 12 A. Yes. 13 Q. Geoffrey ? 14 A. Uh-huh. 15 Q. And there are six employers in that group; is 16 that right? 17 A. Yes, that -- yes.

Issue:�� 10Employer

Page 21 16 Q. What are death benefit identifiers? 17 A. All the participants are placed in death 18 benefit identifiers, and within each of those, the 19 contribution per thousand of plan death benefit is 20 equal. 21 Q. So the death benefit identifiers are used to 22 allocate death benefits to the plan participants? 23 A. Yes.

Testimony by Issue

Page 103/30/2010 9:12 amPrinted for cegan

cegan

Generic Yellow

2

2. Whether Hildalgo Interest holds the real property at 8608 County Road 453 West in

Eastville, Texas, as Mr. Smith’ nominee?

STATEMENT OF UNDISPUTED MATERIAL FACTS

The undisputed facts of this case reveal that Stephen Smith’ attitude toward the Internal

Revenue Service dramatically changed in 1991. Prior to that year, he filed federal tax returns

and reported income from a veterinary practice that he owned and operated in the Houston area.

Starting with tax year 1991, however, Mr. Smith stopped filing tax returns and started forming

entities that he thought would shield his income and hide his assets. As the IRS started asking

questions about his non-compliance, Mr. Smith responded by sending the IRS letters asserting

that he had no obligation to pay federal income taxes. When it became clear that Mr. Smith’s

letters were not going to satisfy the IRS, Mr. Smith sold his veterinary practice and moved to

Eastville, Texas. In Eastville, he moved onto the real estate at issue in this lawsuit (the “Eastville

Property”). Since the day he moved to Eastville, it is undisputed that Defendants Stephen and

Kattya Smith are the only persons that have enjoyed the benefits and assumed the burdens of

owning the Eastville property.

A. In 1991, Mr. Smith stopped filing tax returns and started forming entities to hold his assets and hide his income.

Before he began accruing the delinquent taxes at issuing this case, Defendant Stephen

Smith recognized and paid taxes on income that he received from owning and operating a

veterinarian practice. Mr. Smith started this practice in 1980, when his 100-percent-owned entity

Stephen Smith P.C. purchased a veterinary practice named Spring Animal Hospital.1 About

seven years after that, in 1987, Mr. Smith built a second animal hospital named Animal Hospital

1 Gov. Ex. 57 (Dep Tran) at 7:1 - 8:10.

cegan

Generic Yellow

3

of Humble.2 Prior to 1991, Mr. Smith had been recognizing the income from his practice as

flow-through income from Stephen Smith P.C.3 As the following fact chart shows, however, Mr.

Smith stopped filing tax returns in 1991.4 At the same time, he formed two entities: Service

Facility Company and Professional Veterinarian Resources.5 He used those entities as shells that

allegedly owned his veterinarian practice and his personal residence.6 When the IRS starting

asking questions about Mr. Smith’ non-filing, Mr. Smith began sending the IRS letters asserting

that he was exempt from federal taxation.7 When it became apparent that Mr. Smith’ letters were

not going to satisfy the IRS, the following fact chart shows that Mr. Smith sold his veterinary

practice for over $1.8 million and moved to Eastville, Texas:8

1980 Spring Animal Hospital Purchased - Mr. Smith testified that he used an entity named Stephen Smith, P.C. to purchase 100 percent of Spring Animal Hospital (Gov. Ex. 57 at 7:13-17)

Gov. Ex. 57 (Dep Tran) at 7:1 - 8:10

1980 - 1990

Hospital Income Flows Through – Stephen Smith recognizes taxable income from veterinary practice as flow-through income from Stephen Smith P.C.

Gov. Ex. 57 (Dep Tran) at 13:17 - 14:17

1987 Humble Hospital Built – Stephen Smith builds Animal Hospital of Humble

Gov. Ex. 57 (Dep Tran) at 11:3-21.

01/12/1992 Service Facility Company Formed - Mr. Smith testified that he came up with the idea to form Service Facility Company by doing "research." - Upon formation, Stephen Smith testified that he was Service Facility Company's only officer, and it had no employees. (Gov. Ex. 57 at 17:16 - 17:24) - Mr. Smith testified that Service Facility Company's only business was to hold and operate Animal Hospital of

Gov. Ex. 57 (Dep Tran) at 14:18 - 21:15

Gov. Ex. 54 (Exam Rpt)

2 Gov. Ex. 57 (Dep Tran) at 11:3-21. 3 Gov. Ex. 57 (Dep Tran) at 13:17 - 14:17. 4 DOJ-000397. 5 Gov. Ex. 57 (Dep Tran) at 14:18 - 21:15; Gov. Ex. 54 (Exam Rpt) at DOJ-001004] (formation of Service Facility Company). Gov. Ex. 57 (Dep Tran) at 8:16 - 10:7; Gov. Ex. 54 (Exam Rpt) at DOJ-001005 (formation of Professional Veterinarian Resources). 6 Id. 7 See, e.g., Gov. Ex. 36, 38, 39, 40, 42. 8 Gov. Ex. 57 (Dep Tran) at 10:20-22; Gov. Ex. 54 (Exam Rpt) at DOJ-001023 - DOJ-001024 (Sale of Spring Animal Hospital). Gov. Ex. 57 (Dep Tran) at 11:19 - 12:3; Gov. Ex. 54 (Exam Rpt) at DOJ-001023 - DOJ-001024 (Sale Humble Animal Hospital).

4

Humble. (Gov. Ex. 57 at 19:1 -8) - Mr. Smith testified he transferred his home to Service Facility Company in exchange for "certificates of interest." (Gov. Ex. 57 at 15:20 - 16:10)

04/15/1992 Smith Fails to File 1991 Form 1040 Gov. Ex. 24 (Acct Tran) at DOJ-000398 - DOJ-000402

06/1992 Professional Veterinarian Resources Formed - Mr. Smith testified that he transferred Spring Animal Hospital to Professional Veterinarian Resources in return for 100 percent ownership. (Gov. Ex. 57 at 8:16 - 10:7)

Gov. Ex. 57 (Dep Tran) at 8:16 - 10:7

Gov. Ex. 54 (Exam Rpt) at DOJ-001005

12/20/1992 Affidavit by Stephen Smith Asserting Natural-Born Status

Gov. Ex. 42

04/15/1993 Smith Fails to File 1992 Form 1040 Tax Return Gov. Ex. 24 (Acct Tran) at DOJ-000404 - DOJ-000409.

08/13/1993 Humble Hospital Sold – Smith sells Animal Hospital of Humble to Robert Leonpacher for $222,000

Gov. Ex. 57 (Dep Tran) at 11:19 - 12:3

Gov. Ex. 54 (Exam Rpt) at DOJ-001023 - DOJ-001024

04/15/1994 Smith Fails to File 1993 Form 1040 Gov. Ex. 24 (Acct Tran) at DOJ-000411 - DOJ-000416.

06/22/1994 IRS Issues Notice of Non-Filing for 1991 Form 1040 Gov. Ex. 41 07/13/1994 Letter from Smith Asserting Non-Liability for Federal

Tax Gov. Ex. 39

08/02/1994 Letter from Smith Asserting Non-Liability for Federal Tax

Gov. Ex. 34

09/20/1994 Affidavit by Smith Asserting Non-Liability for Federal Tax

Gov. Ex. 38

10/03/1994 Smith Files 1991 Form 1040 Asserting No Taxable Income - An attachment to the return asserts that "THE INCOME TAX IS VOLUNTARY," and "THE 16TH AMENDMENT AND THE INCOME TAX IS LIMITED TO INDIRECT EXCISE TAXES." (DOJ-001219)

Gov. Ex. 37

01/27/1995 IRS Issues Notice Refusing Smith 1991 Return as Frivilous

Gov. Ex. 35

5

02/03/1995 Letter from Stephen Smith Asserting Non-Liability for Federal Tax

Gov. Ex. 36

04/15/1995 Smith Fails to File 1994 Form 1040 Gov. Ex. 24 (Acct Tran) at DOJ-000418 - DOJ-000423

04/15/1996 Smith Fails to File 1995 Form 1040 Gov. Ex. 24 (Acct Tran) at DOJ-000425

11/05/1996 Spring Hospital Sold – Stephen Smith sells Spring Animal Hospital to Veterinary Centers of America for $1,600,000

Gov. Ex. 57 (Dep Tran) at 10:20-22

Gov. Ex. 54 (Exam Rpt) at DOJ-001023 - DOJ-001024

04/01/1997 IRS Issues Examination Letter to Smith for 1991 Tax Year

Gov. Ex. 60 (Exam Ltr)

Gov. Ex. 61 (Ack Ltr)

07/1997 - 08/1997

Smith Files 1992-1996 Forms 1040 Gov. Ex. 24 (Acct Tran) at DOJ-000404, DOJ-000411, DOJ-000418, DOJ-000425, DOJ-000432

09/04/1997 IRS Issues Deficiency Notice to Smith for 1991 Tax Year

Gov. Ex. 32

11/24/1997 Smith Files Tax Court Petition for 1991 Tax Year Gov. Ex. 31

B. After selling his veterinary practice for over $1.8 million, Mr. Smith moved to

Eastville and began enjoying the benefits of the property at issue in this lawsuit.

When Mr. Smith moved to Eastville, two events occurred simultaneously: (1) a deed

transferring the Eastville property to an alleged entity named State Standard LLC was executed;9

and (2) Stephen Smith moved onto the Eastville property.10 Since then, the Eastville property

9 Gov. Ex. 1 (Deed). 10 Gov. Ex. 57 at 30:4-12 (moved on to property after leaving Houston); 90:4-15 (first discovered property in 1998).

6

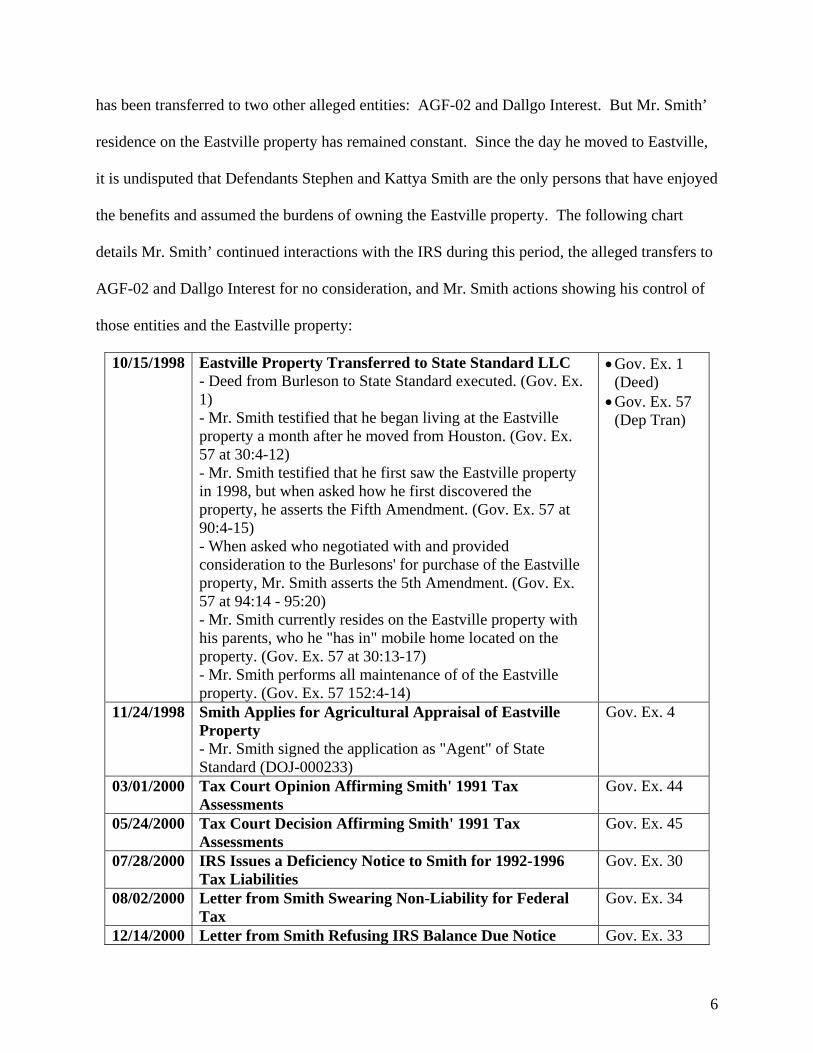

has been transferred to two other alleged entities: AGF-02 and Dallgo Interest. But Mr. Smith’

residence on the Eastville property has remained constant. Since the day he moved to Eastville,

it is undisputed that Defendants Stephen and Kattya Smith are the only persons that have enjoyed

the benefits and assumed the burdens of owning the Eastville property. The following chart

details Mr. Smith’ continued interactions with the IRS during this period, the alleged transfers to

AGF-02 and Dallgo Interest for no consideration, and Mr. Smith actions showing his control of

those entities and the Eastville property:

10/15/1998 Eastville Property Transferred to State Standard LLC - Deed from Burleson to State Standard executed. (Gov. Ex. 1) - Mr. Smith testified that he began living at the Eastville property a month after he moved from Houston. (Gov. Ex. 57 at 30:4-12) - Mr. Smith testified that he first saw the Eastville property in 1998, but when asked how he first discovered the property, he asserts the Fifth Amendment. (Gov. Ex. 57 at 90:4-15) - When asked who negotiated with and provided consideration to the Burlesons' for purchase of the Eastville property, Mr. Smith asserts the 5th Amendment. (Gov. Ex. 57 at 94:14 - 95:20) - Mr. Smith currently resides on the Eastville property with his parents, who he "has in" mobile home located on the property. (Gov. Ex. 57 at 30:13-17) - Mr. Smith performs all maintenance of of the Eastville property. (Gov. Ex. 57 152:4-14)

Gov. Ex. 1 (Deed)

Gov. Ex. 57 (Dep Tran)

11/24/1998 Smith Applies for Agricultural Appraisal of Eastville Property - Mr. Smith signed the application as "Agent" of State Standard (DOJ-000233)

Gov. Ex. 4

03/01/2000 Tax Court Opinion Affirming Smith' 1991 Tax Assessments

Gov. Ex. 44

05/24/2000 Tax Court Decision Affirming Smith' 1991 Tax Assessments

Gov. Ex. 45

07/28/2000 IRS Issues a Deficiency Notice to Smith for 1992-1996 Tax Liabilities

Gov. Ex. 30

08/02/2000 Letter from Smith Swearing Non-Liability for Federal Tax

Gov. Ex. 34

12/14/2000 Letter from Smith Refusing IRS Balance Due Notice Gov. Ex. 33

7

01/22/2003 Eastville Property Transferred to AGF-02 - Deed from State Standard to AGF-02 appears to state "Wayne A. Paul" in signature line (DOJ-000216), but when shown a copy of the deed, Mr. Paul did not recognize the deed or remember signing it. (Gov. Ex. 59 at 25:15 - 26:1) - Mr. Paul does not remember making any decisions for State Standard or acting in any specific capacity for State Standard. (Gov. Ex. 59 at 30:17-2) - When asked whether AGF-02 provided any consideration to State Standard, Mr. Smith asserts the Fifth Amendment. (Gov. Ex. 57 at 99:14-23)

Gov. Ex. 2 (Deed)

Gov. Ex. 57 (Dep Tran)

Gov. Ex. 59 (Dep Tran)

07/16/2003 Levy Notice Issued to Smith for Tax Years 1991-1998 Gov. Ex. 62 08/11/2003 Smith Issues Notice of Severence and Independence from

United States Gov. Ex. 22

08/14/2003 Letter from Smith to IRS re Admin Requirement Gov. Ex. 20 11/12/2003 Letter from Smith to IRS re Failure to Respond to

Admin Requirement Gov. Ex. 19

02/24/2004 Smith Applies for Agricultural Appraisal of Eastville Property - Mr. Smith signed the application as "Administrator" of AGF-02 (DOJ-000246).

Gov. Ex. 5

03/15/2004 Smith Gives Notice of his Powers as Trustee of Dallgo Interest

Gov. Ex. 17

07/23/2004 Eastville Property Transferred to Dallgo Interest - Mr. Smith lived at the Eastville property before the transfer to Dallgo and he lived at the Eastville property after the transfer to Dallgo. (Gov. Ex. 57 at 111:17 - 112:4) - When asked whether Dallgo provided any consideration to AGF-02 for the transfer, Mr. Smith asserts the Fifth Amendment. (Gov. Ex. 57 109:25 - 110:3) - Mr. Smith testified that he is trustee of Dallgo with the authority to act on behalf of Dallgo and write checks drawn on Dallgo's bank account. (Gov. Ex. 57 at 85:4-7 (trustee), 152:21:25 (wrote check)) - Mr. Smith testified that Dallgo's only asset is the Eastville property. (Gov. Ex. 57 87:16-18) - When asked whether Dallgo has an office, conducts any business, or retains any business records, Mr. Smith asserts the Fifth Amendment. (Gov. Ex. 57 at 87:19 - 88:1)

Gov. Ex. 3 (Deed)

Gov. Ex. 57 (Dep Tran)

08/05/2004 IRS Issues Notice of State Standard Nominee Lien for Years 1991-1997

Gov. Ex. 63

09/17/2004 Smith Applies for Homestead Exemption on Eastville Property - Mr. Smith signed application as "Trustee" of AGF-02. (DOJ-000250)

Gov. Ex. 6

8

10/01/2004 Smith Allegedly Executes Lease Agreement with Dallgo Interest - When asked whether he has ever made a payment toward this lease, Mr. Willliams said yes, but he initially refused to disclose where he sent his lease checks. Later in the deposition, he admitted that he sent the rent checks to himself. (Gov. Ex. 57 at 114:19 - 119:15)

Gov. Ex. 51 (Lease)

Gov. Ex. 57 (Dep Tran) at 113:25 - 119:15

01/03/2005 Smith Applies for Homestead Exemption on Eastville Property - Mr. Smith signed the application as "Trustee" of Dallgo Interest. (DOJ-000250)

Gov. Ex. 6

03/21/2005 Smith Applies for Agricultural Appraisal of Eastville Property - Mr. Smith signed the application as "Trustee" of Dallgo. (DOJ-000257)

Gov. Ex. 9

03/21/2005 Smith Applies for Open Space Timber Appraisal of Eastville Property - Mr. Smith signed the application as "Trustee" of Dallgo Interest. (DOJ-000254)

Gov. Ex. 8

05/18/2005 Rusk County Issues Letter Denying Dallgo Interest's Agriculture and Homestead Application

Gov. Ex. 13

06/17/2005 Rusk County Issues Notice of Protest Hearing to Dallgo Interest

Gov. Ex. 12

07/06/2005 Rusk County Appraisal District Hearing – Smith attends Rusk County Appraisal District protest hearing as representative of Dallgo Interest

Gov. Ex. 11 (Hearing Aff)

Gov. Ex. 57 (Dep Tran) at 134:18-20.

07/06/2005 Smith Returns Rusk County Denial Letter - Mr. Smith signed the return as "Trustee" of Dallgo Interest.

Gov. Ex. 13

07/06/2005 Smith Issues Notice to Rusk County re Dallgo Interest - Mr. Smith signed the notice as "Trustee" of Dallgo Interest.

Gov. Ex. 14

07/06/2005 Rusk County Issues Order Denying Appraisal Protest Gov. Ex. 15 01/19/2006 IRS Issues Levy Notice to Smith for 2000-2004 Tax Years Gov. Ex. 64

U.S. M.S.J. Page 12 of 30

honored the summons request related to Mr. Smith.39 Jenkens did not honor the summons

requests related to Mr. Brown until July 21, 2004.40

Mr. Brown’s and Mr. Smith’s assessment limitations periods were again suspended when

the IRS issued an FPAA to Choice Concrete. Under section 6229(d), the issuance of an FPAA

suspends the section 6501 assessment limitations period for tax attributable to partnership

items.41 In this case, section 6229(d) suspended Mr. Brown’s and Mr. Smith’s 1999 assessment

limitations periods when the IRS issued a 1999 FPAA to Choice Concrete’s partners on

September 7, 2006.42

When both the summons suspension and the FPAA suspension are accounted for, the

following chart demonstrates that the limitations period ran for only 5 years and 300 days before

the 1999 FPAA suspended it:

2000 2001 2002 2003 2004 2005 2006

Apr 17, 2000 1999 Returns

Filed

Jul 15, 2004

Summons Docs Provided

Sep 7, 2006

1999 FPAA Issued

Running 3 yrs, 246 days

Dec 19, 2003

6 Months After Summons Issued

Suspended209 days

Running2 yrs, 54 days

Nov 12, 2006 Last Day to

Suspend

B. Mr. Brown and Mr. Smith Omitted Income from their Tax Returns

Section 6501(e) applies only if the taxpayer has omitted “gross income” from a tax

return. As a threshold matter, therefore, the Court must decide whether Mr. Brown and Mr.

Smith omitted any “gross income.” Mr. Brown and Mr. Smith, relying upon the Supreme

39Dorsey Declaration. 40 Id. 41 E.g., Epsolon Ltd. v. United States, 78 Fed. Cl. 738, 760-762 (2007); Rhone-Poulenc Surfactants & Specialties,

L.P. v. Comm’r, 114 T.C. 533, 551-557 (2000). 42 Gov. Ex. 55 (FPAA).

cegan

Generic Yellow

U.S. M.S.J. Page 5 of 30

securities to DB Alex Brown) to Choice Concrete.13

Step Three – Short Sale Closed

One day later, on May 18th, Choice Concrete satisfied the short-sale obligation by

purchasing treasury securities for $7,474,181 and repaying those notes to the short-sale

lender, DB Alex Brown.14

As the following chart shows, this series of circular transactions lasted fewer than five days:

DB Alex Brown

Choice Concrete& Supply, LLC

May 13th (Start)

$7,472,405 of Treas. Securities

Transferred

May 17th

$7,472,405 of Proceeds and Close Obligation

Transferred

May 18th (Finish)

$7,474,181 of Treas. Securities

Transferred

May 18th

CC&S Purchases Treas. Securities for

$7,474,181

May 13th

Brown & SmithSellTreas. Sec. for

$7,472,405

Robert Brown &Stephen Smith

(through Grantor Trusts andSingle-Member LLCs)

Jenkens & Gilchrist charged Mr. Brown and Mr. Smith $300,000 for “TAX ADVICE”

regarding the above transaction.15 Why would Mr. Brown and Mr. Smith engage in such a

circular transaction and pay Jenkens $300,000 for tax advice related to the transaction? Basis.

Before the transaction, Mr. Brown and Mr. Smith had agreed to sell their business, Choice Oil; a

letter of intent to sell the business had been executed before the short-sale transactions

13 Pl. Comp. at ¶ 19(i)-(l); Gov. Ex. 16 (Salisbury Transfer Request); Gov. Ex. 17 (JMP Trust Transfer Request);

Gov. Ex. 18 (RCP Trust Transfer Request); Gov. Ex. 19 (Goodnight Transfer Request). 14 Gov. Ex. 29 (Close Confirmation). The $7,359,043 listed in the plaintiffs’ complaint at ¶ 19(m) fails to account

for interest and the transaction fee. 15 Gov. Ex. 54 (Jenkens Invoice)

cegan

Generic Yellow

Date & Time Fact Text Source(s)

11/25/2002

William Lang meets Philip Hawkins while touring Converse Chemical Labs

plant in Bakersfield.

Deposition of William Lang, 25:14;

InterviewNotes, Email from Phil Hawkins at

20050923 1514 to William Lang

12/??/02

William Lang invites Philip Hawkins to visit Anstar Biotech Industries facilities

in Irvine. InterviewNotes

01/??/03

William Lang offers Philip Hawkins Sales Manager position at Anstar Biotech

Industries.

InterviewNotes, Email from Phil Hawkins at

20050923 1514 to William Lang

1/13/2003 Philip Hawkins joins Anstar Biotech Industries as a Sales Manager. Anstar Biotech Industries Employment Records

12/1/2003 Philip Hawkins promoted to Anstar Biotech Industries VP of Sales. InterviewNotes

01/09/04 to 01/21/04

Philip Hawkins negotiates draft Hawkins Employment Agreement with

William Lang. Hawkins Employment Agreement

02/??/04

William Lang tells Philip Hawkins that he has changed his mind regarding the

Hawkins Employment Agreement. It is not in force as it was never signed and

changes were not finalized. Philip Hawkins, Deposition of William Lang, 11:3.

5/11/2005

Philip Hawkins receives Hawkins Performance Review from William Lang. Is

rated a 1 "Outstanding Performer." Hawkins Performance Review

7/4/2005

Philip Hawkins allegedly makes derogatory remarks about Linda Collins to

Karen Thomas during Anstar Biotech Industries Fourth of July picnic. Randy

Fosheim in attendance. InterviewNotes

7/30/2005 Philip Hawkins demoted to sales manager. Deposition of Philip Hawkins, 24:18

08/02/05 #1 Philip Hawkins and William Lang meet. ????

08/02/05 #2

Philip Hawkins alleges that William Lang tells him "The old wood must be

trimmed back hard."

Complaint, p. 8; Deposition of Philip Hawkins,

21:13; Hawkins Letter of 9/19/2005, Hawkins

Letter of 8/2/2005

8/11/2005 Philip Hawkins transferred to Anstar Biotech Industries office in Fresno. Deposition of Philip Hawkins, p.43, l18.

8/12/2005 Frank Varvaro has lunch with Philip Hawkins. Deposition of Philip Hawkins, 52:3‐14

Important FactsCross Examination of Philip Hawkins

cegan

Generic Yellow

cegan

Generic Yellow

cegan

Generic Yellow

Technology in Trial

Using Technology to Persuade Four Generations

Prepared by: Christopher Egana1

August 2012 Dallas Bar Association Tax Section Meeting

Technology in Trial Using Technology to Persuade Four Generations

I. USING TECHNOLOGY TO PERSUADE FOUR GENERATIONS

A. Communicating to Four Generations

The jury box and bench now includes four generations:

Matures – Born 1928-1945 Baby Boomers – Born 1946-1964 Generation X – Born 1965-1980 Millennials – Born 1981-1993

Technology can help trial attorneys communicate with all four of these generations. Technology improves the efficiency and effectiveness of courtroom presentations. The digital format alone allows attorneys to move quickly between exhibits. More importantly, trial software allows attorneys to present evidence in new ways. Exhibits can be highlighted, drawn on, magnified, and compared during trial. Absent witnesses can be presented via deposition video synced with transcript text. Complicated transactions and concepts can be illustrated with graphs and charts. While these techniques can help attorneys communicate more effectively with all generations, these techniques are critical for Generation X and Millennials. These generations have incorporated technology into every aspect of their lives. Technology affects the way these groups learn and communicate.

B. Data on Generation X and Millennials

More than half of the United States’ adult population is included in Generation X or the Millennial generation. Douglas L. Keene & Rita R. Handrich, Talkin’ ‘bout our Generations: Are we who we wanted to be?, THE JURY EXPERT, Vol. 24, Issue 1, at 3 (Jan. 2011) (available at www.thejuryexpert.com). Research shows that frequent use of technology has shaped these generations into visual learners that prefer efficient communication styles. 1. Generation X

a. Members of Generation X are visual learners that embrace technology. See, e.g., Douglas L. Keene & Rita R. Handrich, Generation X members are “active balanced and happy” Seriously?, THE JURY EXPERT, Vol. 23, Issue 6, at 10, (Nov. 2011) (available at www.thejuryexpert.com). For example, only 15 percent of Generation X obtains news from print newspapers. Instead, most of Generation X obtains news from the internet (30%) or television (46%). Keen & Handrich, Talkin’ ‘bout our Generations, supra, at 12.

- 2 -

b. Members of Generation X prefer a more direct, efficient communication style. They want people to get to the point. See, e.g., Mary Noffsinger, Generation X and Y: Communication in Today’s Litigation Environment, CSI LITIGATION PSYCHOLOGY, at 7 (2011) (available at www.courtroomsciences.com) (Members of Generation X “desire to communicate directly, and expect the message to be succinct and supported with evidence, not conjecture.”); Keene & Handrich, Generation X, supra, at 9 (“They want the facts, they want them succinctly, and they don’t want a great deal of extraneous detail.”).

c. Members of Generation X are skeptical of authority and slick sales pitches. See, e.g., Keene & Handrich, Generation X, supra, at 9 (“Gen Xers are not as impressed with snappy argument or authoritative presence.”); Noffsinger, Generation X and Y, supra, at 7 (“Generation X does not simply accept something as truth simply because it was derived from a person or source of authority.”).

2. Millennials

a. Millennials are visual learners that process information rapidly. Elaborate explanations bore them. Noffsinger, Generation X and Y, supra, at 7. For example, only 10 percent of Millennials obtain news from print newspapers. Instead, most Millenials obtain news from the internet (38%) or TV (37%). Keen & Handrich, Talkin’ ‘bout our Generations, supra, at 12.

b. Millennials are “digital natives” that incorporate technology into almost all of their everyday activities. Douglas L. Keene & Rita R. Handrich, Tattoos, Tolerance, Technology, and TMI: Welcome to the Land of Millennials, The Jury Expert, Vol. 22, Issue 4, at 38-39 (July 2010) (available at www.thejuryexpert.com); Noffsinger, Generation X and Y, supra, at 6 (referring to Millennials as “digital natives”). For example, in a survey asking about their prior 24 hours, 32 percent of Millennials stated that they had watched an online video. Millennials, A Portrait of Generation Next, PEW RESEARCH CENTER, at 36 (February 24, 2010) (available at http://pewresearch.org/). Only 9 percent of Baby Boomers had watched an online video. Id.

c. Seventy-four percent of Millennials believe that “technology makes life easier.” Id. at 26.

d. Millennials expect and desire presentations that incorporate technology. A small study of Texas Tech law students, for example, indicates that Millennials favor graphical presentations. John G. Browning & Wendy A. Humphrey, The Millennial Juror, TEXAS BAR JOURNAL, Vol. 75, No. 4 (April 2012). Consider the Millennials’ responses to the following research questions:

(1) “If a witness was unable to testify live, attorneys should present videotaped testimony rather than simply reading the testimony.” 97.5% agreed or strongly agreed.

- 3 -

(2) “Attorneys should use graphic presentation software (such as PowerPoint) to summarize the main points during the trial, e.g., during opening statement and closing statement.” 72.5% agreed or strongly agreed.

(3) “Attorneys should use timeline software to help organize and explain events in the case.” 77.5% agreed or strongly agreed.

C. Presentation Strategies

Members of Generation X and the Millennials are visual learners that prefer succinct fact presentations. To persuade these groups, consider the following strategies:

Communicate Visually – Use charts and graphs to illustrate complicated transactions or concepts. Use timelines to efficiently show the relationship between events.

Divide Your Presentation into Digestible Bites of Information – Use magnification and sequencing to isolate parts of complicated transactions and build up to a complete picture. Use video deposition technology to present only the important parts of a deposition.

Get to the Point – A well-designed graphic is worth a thousand words. Instead of relying only on lengthy testimony, use graphics, charts, and timelines that describe complicated transactions in an instant.

II. PRESENTATION TECHNIQUES

A. Highlight

Highlighting is a simple and effective way to draw an audience to important information. See Ex. 1. Consider highlighting during trial instead of before. The act alone draws a viewer’s attention.

B. Magnify

Magnification helps divide complicated documents into digestible parts. See Ex. 2. For example, parts of a large data chart can be magnified as a witness testifies about the data.

C. Compare Evidence to Show Relationships

A fact often depends on the relationship between two documents. Trial software can be used to show those documents on the same screen. Highlighting and magnification can be used to focus a fact finder’s attention on the relevant parts of each document. See Ex. 3. For example, two checks can be presented side-by-side to establish a money flow.

- 4 -

D. Draw Arrows to Focus Attention

Arrows can be used to draw attention to part of a picture or diagram. See Ex. 4. As with highlighting, consider drawing the arrow during trial instead of before. The act alone grabs a fact finder’s attention.

E. Roadmap Testimony with a Demonstrative

Experts and summary witnesses often use demonstrative graphics to illustrate their testimony. See Ex. 5. Use these demonstratives during direct testimony. Demonstratives can often help fact finders visualize complicated concepts and transactions. Use Magnification to break up complicated charts into digestible bites.

F. Use Timelines

Proving a fact often requires establishing a timeline of events. Establishing that timeline through verbal testimony alone can burden a fact finder’s short-term memory. Timelines, on the other hand, show all of the relevant facts at once. See Ex. 6. They instantly place facts within their proper context and reveal relationships; relationships between different events, people, and organizations. They can be used during open, close, or testimony. For example, an attorney can build a timeline as a forensic accountant testifies about a transaction’s events. Events appear on screen as the accountant testifies. Testimony ends with a complete timeline.

G. Present Deposition Video Synced with Transcript Text

Trial attorneys must sometimes present deposition testimony at trial because an important witnesses is outside of the trial court’s subpoena range or otherwise unavailable. Traditionally, attorneys have read the testimony into the record. This reading usually bores the fact finder and provides little basis for judging credibility. Video testimony, on the other hand, allows the fact finder to see the witness with all of his non-verbal signals. Trial presentation technology can be used to create video clips of important testimony. Those clips can be played with synced transcript text. See Ex. 7. In addition, referenced exhibits can be presented next to the deponent video.

H. Integrate Evidence into Closing

Closing presentations can include screen shots of your important evidence, with highlighting and other annotations. See Ex. 8. Let the evidence speak for itself. Sometimes evidence persuades more than speech.

- 5 -

III. TOOLS

A. What You Need

1. Computer

2. Trial Software

3. Projector

4. Screen

B. Example Trial Presentation Softwarea2

1. Sanction

a. Basic Features: Features: annotations, magnification, side-by-side comparison, video and audio clip editing, video with synced transcript text.

b. Price: Contact Company

c. Website: www.verdictsystems.com/Software/

2. Trial Director

a. Basic Features: annotations, magnification, side-by-side comparison, video and audio clip editing, video with synced transcript text.

b. Price: Single-User licenses start at $695

c. Website: www.indatacorp.com/TrialDirector.html

3. Visionary

a. Basic Features: annotations, magnification, side-by-side comparison, video and audio clip editing, video with synced transcript text.

b. Price: $495 (Pro Version)

c. Website: www.visionarylegal.com/

4. Exhibit View

a. Basic Features: annotations, magnification, video and audio clip editing, video with synced transcript text.

b. Price: $499

c. Website: http://exhibitview.net/

- 6 -

5. Trial Pad (iPad Application)

a. Basic Features: annotations, magnification, basic video editing.

b. Projection: To project onto a screen, plug your iPad into a projector via Apple’s VGA Adaptor.

c. Price: $89.99

d. Website: www.trialpad.com/

6. Exhibit A (iPad Application)

a. Basic Features: annotations, magnification.

b. Projection: To project onto a screen, plug your iPad into a projector via Apple’s VGA Adaptor.

c. Price: $9.99

d. Website: www.lecturaapps.com/

7. RLTC: Evidence (iPad Application)

a. Basic Features: annotations, magnification.

b. Price: $4.99

c. Website: www.rosenltc.com/app.html

C. Support Staff

Effective trial presentations do not always require a dedicated employee running the trial software. If you are comfortable with a computer, consider running a simple presentation by yourself. Once you become comfortable with the software, using it can be no more distracting than opening an exhibit notebook and highlighting with a marker. Note that some software is easier to use than others. If you plan to present cases without support staff, consider purchasing an easy-to-use product that may not have as many features. For example, an iPad app like Trial Pad has a user-friendly interface that most attorneys will find easy to learn.

- 7 -

IV. BEST PRACTICES

A. Know Your Venue

Courtroom technology varies from courtroom to courtroom. Call ahead to determine equipment available, screen placement, and judicial preferences. Visit the courtroom at least a day ahead of time to test your equipment and placement. Even if the courtroom has no technology, a mobile projector and screen can be brought into the courtroom.

B. Know Your Fact Finder

Call ahead to obtain any special technology instructions prior to trial. Some judges, for example, have strict rules about screen and projector placement. Other judges may want a hard copy of your exhibits. But do not assume that a judge requesting hard copies will not appreciate your digital presentations. Digital presentations often draw the judge’s attention to the important parts of your evidence.

C. Keep Demonstratives Simple

Avoid needlessly complicated charts. Focus on the important parts of your transaction. Technology allows us to create charts that show every detail of every transaction. Those complicated charts usually confuse the fact finder instead of helping. The important parts of those charts are lost in the complication. Instead of trying to convey every detail, consider focusing on one key transaction or one part of a key transaction.

D. Practice at Your Venue

Show up early and practice using your venue’s equipment. Practice increases your confidence and helps you resolve any unexpected quirks with your venue’s equipment.

E. Bring a Back Up

If possible, bring a second laptop loaded with your trial exhibits and presentation software. This allows you quickly switch computers if one fails. As a simple, less-voluminous back up, consider bringing an iPad loaded with your exhibits and a trial presentation application.

Contact me if you have any questions. I love to discuss litigation technology. Chris Egan 214-880-9732 [email protected]

- 8 -

a1 J.D., 2002, Southern Methodist University School of Law; B.B.A., M.P.A., 1997, The University of Texas at Austin; Certified Public Accountant, Texas. Mr. Egan worked two years as a tax accountant for Arthur Andersen, L.L.P., and he currently works as a trial attorney for the U.S. Department of Justice, Tax Division, Dallas, TX. The views expressed in this outline are the personal views of the author and are not necessarily the views of the Department of Justice or the Internal Revenue Service. Mr. Egan, the Department of Justice, and the Internal Revenue Service do not endorse any of the products discussed during this presentation. Those products are presented as examples only. a2 The author does not endorse any particular software product.

cegan

Generic Yellow

cegan

Generic Yellow

cegan

Generic Yellow

cegan

Generic Yellow

ABInvestments

May 13th (Start)

$7.4 Million of Treas Securities

May 18th (Finish)

$7 4 Million ofTreas. Securities Transferred

$7.4 Million of Treas. Securities

Transferred

May 18thMay 13thl h ff ll

Robert Paul &North CarolinaConcrete, LLC

y 8

HC&S Purchases Treas. Securities for

$7.4 Million

Paul & Chaff Sell Treas. Sec. for

$7.4 Million

Robert Paul &Stephen Chaff

(through Grantor Trusts andSingle-Member LLCs)

May 17th

$7.4 Million of Proceeds and Close Obligation

Transferred

cegan

Generic Yellow

Apr 17, 2000 Jul 15, 2004 Sep 7, 2006

Running3 yrs, 246 days

Dec 19, 2003

Suspended209 days

Running2 yrs, 54 days

Nov 12, 2006

2000 2001 2002 2003 2004 2005 2006

p ,

1999 Returns Filed

Jul 15, 2004

Summons Docs Provided

Sep 7, 2006

1999 FPAA Issued

Dec 19, 2003

6 Months After Summons Issued

Nov 12, 2006

Last Day to Suspend

2000 2001 2002 2003 2004 2005 2006

cegan

Generic Yellow

cegan

Generic Yellow

Payment Flow

cegan

Generic Yellow