Technical Line - EY - United StatesFILE/EY... · Technical Line How to apply S-X Rule 3-14 and the...

20

What you need to know • The SEC staff recently revised its guidance for acquired real estate operations in several ways that will affect how registrants apply Rule 3-14 of Regulation S-X in determining whether audited financial statements of an acquired property are required. • The determination of whether an acquired property qualifies as a real estate operation is essential in the application of Rule 3-14 and often requires judgment by management. • Companies contemplating acquisitions of real estate or forming a real estate investment trust (REIT) should understand Rule 3-14 and the SEC staff’s recent revisions to its guidance. Overview The Securities and Exchange Commission (SEC) staff recently revised its guidance on Rule 3-14 of Regulation S-X (Rule 3-14), which requires registrants to present the audited financial statements of significant consummated or probable acquisitions of real estate operations. These requirements differ significantly from those in Rule 3-05 of Regulation S-X (Rule 3-05), which addresses significant acquisitions of businesses. The recent changes are important because Rule 3-14 itself is rather brief. Application of the rule has been subject to various interpretations by the SEC staff, preparers and their advisers over the years. The latest revisions to the staff guidance came in a recent update of the Division of Corporation Finance’s Financial Reporting Manual (FRM), 1 in Section 2300, Real Estate Acquisitions and Properties Securing Mortgages. These revisions may result in significant changes to a registrant’s assessment of whether audited financial statements of an acquired property must be filed. No. 2013-16 4 September 2013 Technical Line SEC — staff guidance How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions In this issue: Overview ....................................... 1 Key changes to staff guidance ....... 2 Applicability of Rule 3-14 .............. 2 Measuring significance .................. 4 Financial statement requirements ............................ 7 REIT formation transactions ........ 10 Blind pool offerings...................... 12 Acquisitions of properties subject to a triple net lease ..... 13 Properties securing mortgage loans....................................... 15 Appendix A: Example Rule 3-14 financial statements ............... 17 Appendix B: Comparison of Rule 3-14 and Rule 3-05 requirements .......................... 19

Transcript of Technical Line - EY - United StatesFILE/EY... · Technical Line How to apply S-X Rule 3-14 and the...

What you need to know • The SEC staff recently revised its guidance for acquired real estate operations in several

ways that will affect how registrants apply Rule 3-14 of Regulation S-X in determining

whether audited financial statements of an acquired property are required.

• The determination of whether an acquired property qualifies as a real estate operation

is essential in the application of Rule 3-14 and often requires judgment by management.

• Companies contemplating acquisitions of real estate or forming a real estate investment trust

(REIT) should understand Rule 3-14 and the SEC staff’s recent revisions to its guidance.

Overview The Securities and Exchange Commission (SEC) staff recently revised its guidance on

Rule 3-14 of Regulation S-X (Rule 3-14), which requires registrants to present the audited

financial statements of significant consummated or probable acquisitions of real estate

operations. These requirements differ significantly from those in Rule 3-05 of Regulation S-X

(Rule 3-05), which addresses significant acquisitions of businesses.

The recent changes are important because Rule 3-14 itself is rather brief. Application of the

rule has been subject to various interpretations by the SEC staff, preparers and their advisers

over the years. The latest revisions to the staff guidance came in a recent update of the

Division of Corporation Finance’s Financial Reporting Manual (FRM),1 in Section 2300, Real

Estate Acquisitions and Properties Securing Mortgages. These revisions may result in

significant changes to a registrant’s assessment of whether audited financial statements of an

acquired property must be filed.

No. 2013-16 4 September 2013 Technical Line

SEC — staff guidance

How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions

In this issue:

Overview ....................................... 1

Key changes to staff guidance ....... 2

Applicability of Rule 3-14 .............. 2

Measuring significance .................. 4

Financial statement requirements ............................ 7

REIT formation transactions ........ 10

Blind pool offerings ...................... 12

Acquisitions of properties

subject to a triple net lease ..... 13

Properties securing mortgage

loans ....................................... 15

Appendix A: Example Rule 3-14

financial statements ............... 17

Appendix B: Comparison of

Rule 3-14 and Rule 3-05 requirements .......................... 19

EY AccountingLink | www.ey.com/us/accountinglink

2 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

This Technical Line describes the revisions and provides information to help registrants

interpret and apply Rule 3-14. Specifically, we discuss determining whether an acquisition

qualifies as a real estate operation, measuring significance and appropriately presenting

financial information. We also discuss other types of property acquisitions covered by

Rule 3-14 and the related SEC staff guidance, including:

• REIT formation transactions

• “Blind pool” offerings

• Properties subject to a triple net lease

• Properties securing mortgage loans that represent a significant asset concentration

Key changes to staff guidance The SEC staff made the following changes to its guidance related to Rule 3-14:

• The staff clarified that Rule 3-14 requires audited financial statements of an acquired

entity that has operations (e.g., property management) in addition to holding real estate

if the registrant’s investment in the acquisition exceeds 10% but not 20% of its assets and

the acquired property has a rental history.

• For purposes of testing whether individually insignificant acquisitions are significant in the

aggregate, registrants need to consider only acquisitions and probable acquisitions since

the latest audited year-end, not individually insignificant acquisitions made during the last

audited fiscal year.

• The staff will permit the use of the registrant’s pro forma financial information to

calculate significance of a real estate acquisition made after the filing of a Form 8-K that

included historical audited financial statements for a prior significant acquisition, as it

does for business combinations under Rule 3-05.

• The staff revised the significance test for property acquired during the distribution period

of a “blind pool” offering to allow the registrant to use as the denominator total assets as

of the date of the acquisition plus the proceeds (net of commissions) it expects to raise in

the registered offering over the next 12 months.

• Rather than requiring formal pre-clearance, the staff will accept unaudited financial

statements when a registrant acquires an operating property with a rental history of more

than three months but less than nine months, and the staff will not require Rule 3-14

financial statements when the leasing history is less than three months.

• The staff clarified its guidance on the financial statement requirements for concentrations

of properties subject to triple net lease arrangements and added guidance to require

Rule 3-14 financial statements when the acquisition of a property with a rental history

results in a significant concentration greater than 10% but not 20%.

Applicability of Rule 3-14

Defining real estate operations

Rule 3-14 applies to significant consummated and probable acquisitions of real estate

operations that generate revenue through rental income. Acquisitions of commercial real

estate, such as office or industrial buildings, apartment complexes and shopping centers,

generally meet the criteria. Properties such as nursing homes, hotels, golf courses and auto

EY AccountingLink | www.ey.com/us/accountinglink

3 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

dealerships generally do not qualify because leasing doesn’t drive substantially all of their

revenues. A registrant that acquires one of these properties generally applies Rule 3-05, which

has a higher threshold for significance (20%) but requires more robust financial statements.

Registrants must apply Rule 3-14 if they acquire an equity interest in an existing or newly

formed legal entity (e.g., a partnership, corporation, LLC) that will acquire properties under

lease and the related mortgage debt in connection with, or soon after, the entity is formed.

If the acquired entity engages in operations in addition to leasing, the registrant first would

apply Rule 3-05.

The staff added new guidance in the latest FRM stating that if the acquired entity owns

property with a rental history and has operations other than leasing but the acquisition is

not significant under Rule 3-05 (i.e., the acquisition does not exceed 20% under any of the

significance tests), the registrant would have to evaluate and comply with the requirements

of Rule 3-14 if the investment is significant at a level greater than 10%.

Finally, the evaluation of whether Rule 3-14 or Rule 3-05 applies is separate and distinct from

the determination of whether a business has been acquired under US GAAP (i.e., ASC 805,

Business Combinations).

Illustration 1 — Evaluating real estate operations

Scenario A

Company Y acquires a senior residential living community, where residents live

independently and require limited care by the staff. The property leases space to outside

parties that operate a cafeteria and provide on-site medical services. The facility also

operates a small convenience shop where residents can purchase snacks, beverages and

sundry items. In the fiscal year before the acquisition, the community generated $5 million

in rental revenues from residents and the cafeteria and medical operators. The community

also generated $15,000 in revenue from the sale of items at the convenience shop.

Analysis: The senior residential living community likely meets the definition of a real estate

operation. Revenues generated by operations other than the leasing of real property were

nominal in the fiscal year before the acquisition. Company Y could reach a different

conclusion if the residential living community itself provided cafeteria and medical services

and generated significant revenues from them.

Scenario B

Company Z acquires a senior assisted-living facility, where all residents require regular care

and assistance and are unable to prepare their own meals. The facility employs a team of

in-house medical personnel and delivers three meals per day to residents. The facility

generated $3 million in rental revenue from residents, $2 million in medical billings and

$1 million from food service plans in the prior fiscal year.

Analysis: The facility generated a significant portion of its revenues from operations other

than the leasing of real estate. Therefore, the registrant would instead apply Rule 3-05 to

this acquisition and provide full audited financial statements if significance exceeds 20%. If

not, the new guidance would require the registrant to provide audited Rule 3-14 financial

statements if the investment exceeds 10% of the registrant’s assets because the acquired

entity has a rental history.

EY AccountingLink | www.ey.com/us/accountinglink

4 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

How we see it • Many operators of real estate assets seek to maximize the cash flows of a property by

identifying and expanding ancillary sources of revenue. Although the determination of

whether an acquisition qualifies as a real estate operation may initially appear to be

straightforward, registrants must carefully evaluate all revenue sources to evaluate

whether only Rule 3-14 applies.

• While we believe that Rule 3-05 should not be applied to an acquired property or entity

unless revenues from non-leasing operations are significant, companies that acquire

assets with leasing and non-leasing revenue sources should develop and consistently

apply a policy for when these acquisitions should be evaluated under Rule 3-05. In a

close call, a registrant may want to pre-clear its conclusion with the Division of

Corporation Finance’s Office of the Chief Accountant.

Measuring significance Because Rule 3-14 doesn’t say how to calculate significance, the SEC staff provides guidelines

in the FRM for calculating the significance of acquisitions of properties, both individually and

in the aggregate. The staff also provides considerations that must be applied to certain

circumstances arising from the acquisition of a real estate operation.

Calculation of significance

Significance is generally determined by comparing a registrant’s investment in the property

with the registrant’s total assets as of the latest audited fiscal year-end. Properties that are

related must be evaluated as a single acquisition. The SEC staff requires that the investment

(numerator) include any debt secured by the property that is assumed by the purchaser.

Illustration 2 — Calculating significance

Company A, a calendar-year registrant, acquires a fully occupied office building on 30 April

2013. Company A paid cash consideration of $8 million and assumed existing mortgage

debt secured by the property of $22 million. Company A’s total assets at 31 December

2012 were $250 million.

Analysis: Company A’s total investment in the office building of $30 million includes cash

consideration paid and mortgage debt assumed. Because the investment exceeds 10% of

Company A’s total assets at 31 December 2012 of $250 million, management would

conclude that the acquisition was individually significant. Therefore, Company A would be

required to file a Form 8-K within four business days of the acquisition and file audited

Rule 3-14 financial statements and related pro forma information by amendment within

71 days from the due date of the Form 8-K.

Implementation considerations

The SEC staff provides additional implementation guidance related to the timing of acquisitions:

• A registrant that has not completed its first full fiscal year should use total assets from

the most recently audited balance sheet on file with the SEC as the denominator in the

significance calculation.

• A registrant that completes an acquisition after its most recent fiscal year may evaluate

significance based on the total assets of the recently completed fiscal year if it files its

Form 10-K for that year before the due date of the Form 8-K/A to provide Rule 3-14

EY AccountingLink | www.ey.com/us/accountinglink

5 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

financial statements (including the 71-calendar-day extension). For purposes of a

registration statement, the registrant must use the most recent audited financial

statements on file as of the effective date.

• A registrant that makes a real estate acquisition after providing financial statements of

any individually significant acquisition(s) on Form 8-K may evaluate significance using its

pro forma total assets presented in the Form 8-K rather than total assets as of the most

recently completed fiscal year-end. The registrant must, however, exclude the pro forma

effects of transactions that aren’t significant acquisitions. The SEC staff expects

registrants that use this approach to apply it consistently for the rest of the fiscal year.

How we see it • Allowing significance to be calculated based on pro forma total assets resulting from a

previous acquisition is one of the more significant changes the SEC staff made to its

guidance. This change aligns the staff’s guidance on Rule 3-14 with Rule 3-05.

Illustration 3 — Completing an acquisition after fiscal year-end

Company B, a calendar-year registrant, completes an acquisition of a fully leased distribution

facility on 4 January 2013 for a total investment, including assumed debt, of $20 million.

Company B’s total assets for the period ended 31 December 2011 were $190 million.

Company B plans to file Form 10-K for the period ended 31 December 2012 on 28 February

2013 and will report total assets of $210 million as of the balance sheet date.

Analysis: Company B must file a Form 8-K by 10 January 2013 (within four business days)

reporting the significant real estate acquisition. However, assuming Company B files its

Form 10-K within the anticipated time frame, management may use total assets as of

31 December 2012 to determine the significance of the acquired property. As a result, the

acquisition would not meet the 10% threshold for individual significance based on total assets

as of 31 December 2012. Company B would not be required to provide Rule 3-14 financial

statements on Form 8-K/A on or before 22 March 2013 (within the 71-calendar-day extension).

Management of Company B must track subsequent acquisitions to determine whether

those acquisitions, when combined with the acquisition described in this illustration, exceed

the 10% threshold in the aggregate for the purposes of any registration statement

(i.e., whether they exceed 10% of total assets at 31 December 2012).

Illustration 4 — Completing a subsequent acquisition after a significant acquisition

Company C, a calendar-year registrant, completes an acquisition of a fully leased retail

center on 31 July 2013 for a total investment, including assumed debt, of $50 million.

Company C’s total assets for the period ended 31 December 2012 were $475 million. On

15 February 2013, Company C completed an acquisition with a total investment of $75

million. Company C provided Rule 3-14 financial statements for this acquisition on Form

8-K on 10 April 2013. The pro forma financial information as of 31 December 2012

reflected total assets of $550 million.

Analysis: Company C is permitted to evaluate the significance of the $50 million acquisition on

31 July 2013 using the pro forma total assets reported in the 10 April 2013 Form 8-K filing.

As a result, the acquisition would not meet the 10% threshold for individual significance, and

Company C would not be required to file Form 8-K or Rule 3-14 financial statements.

In a key change,

the SEC staff will

permit a registrant

to evaluate

significance under

Rule 3-14 using

pro forma financial

information in a

previously filed

Form 8-K.

EY AccountingLink | www.ey.com/us/accountinglink

6 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

However, management of Company C must track subsequent acquisitions to determine

whether those acquisitions, combined with the $50 million acquisition described in this

illustration, exceed the 10% threshold in the aggregate when compared with pro forma

total assets at 31 December 2012.

Aggregation of individually insignificant properties

A registrant must evaluate in the aggregate acquisitions of real estate operations that do not

individually exceed 10% of total assets. If the combined investment in insignificant acquisitions

exceeds the 10% threshold, a registrant is required to present Rule 3-14 financial statements

for certain of the acquired operations if it files a registration or proxy statement. Audited

financial information of acquired insignificant properties is not required to be filed in Form 8-K

unless the properties are related. (See “Contents of required financial statements” section for

the definition of related properties).

To compute significance, registrants must combine the following:

• Individually insignificant properties acquired after the end of the most recently completed

fiscal year for which the registrant’s audited financial statements are on file

• Individually insignificant probable acquisitions

Properties that, if individually significant, would not require financial statements under

Rule 3-14, such as triple net leased and newly constructed properties, should be excluded

from this computation. (See “Acquisitions of properties subject to a triple net lease” and

“Contents of required financial statements” sections, respectively.)

How we see it In the latest revisions to its guidance, the SEC staff eliminated the previous requirement

to include in the aggregation individually insignificant acquisitions that were completed

during the prior fiscal year. Therefore, a registrant that plans to file a new registration

statement, or update an existing shelf registration, must consider only acquisitions that

have occurred or are probable since the most recent fiscal year for which it has filed

audited financial statements. This change will provide relief to companies that file a

registration statement every few years and those that did not consider obtaining financial

statements for an insignificant property prior to their initial public offering.

If the aggregate of all insignificant real estate properties exceeds the 10% threshold, the

registrant should file audited financial statements for all acquisitions that individually exceed

the 5% threshold.

Further, registrants should determine whether they have filed financial statements for

individually insignificant acquisitions that together exceed 50% of the aggregate purchase

price (including assumed debt). If this threshold is not met, the registrant should file financial

statements of acquisitions that are individually insignificant below the 5% threshold until

financial statements for more than 50% of the aggregate purchase price have been filed.

Registrants that are unable to obtain audited financial information to comply with these

requirements should request relief in writing from the Division of Corporation Finance’s Office

of the Chief Accountant.

Individually

insignificant

properties that

meet the related

property criteria

must be evaluated

for significance in

the aggregate.

Individually

insignificant

properties that

meet the related

property criteria

must be evaluated

for significance in

the aggregate.

EY AccountingLink | www.ey.com/us/accountinglink

7 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

How we see it • Registrants that plan to file new registration statements, or update existing shelf

registrations, should keep in mind the requirements of Rule 3-14 when negotiating the

acquisitions of real estate properties. Companies often fail to consider the aggregation

of individually insignificant properties and are unable to obtain the historical financial

information necessary to comply with Rule 3-14 and meet their desired offering timetable.

• When a registrant believes Rule 3-14 financial statements may be required,

management should try to negotiate into the purchase agreement access to historical

financial records of the acquired property, especially for acquisitions for which the

investment is greater than 5% of the acquirer’s total assets.

Illustration 5 — Evaluating individually insignificant properties

Company D, a calendar-year registrant, plans to file a registration statement on 9 July

2013 and incorporate by reference its 2012 Form 10-K. Throughout 2012 and in 2013 so

far, Company D completed, or determined to be probable, the following acquisitions:

2012 Acquisitions Significance

2013 YTD Acquisitions Significance

Probable Acquisitions Significance

Property G

Property H

Property I

6%

3%

2%

Property A

Property B

Property C

12%

2%

5%

Property D

Property E

Property F

6%

4%

11%

Analysis: Company D is no longer required to evaluate acquisitions that occurred in 2012,

thus Properties G-I are excluded from further evaluation.

Because Property A exceeded 10% significance, audited Rule 3-14 financial statements were

required to be filed in a Form 8-K and must be included or incorporated by reference in the

registration statement. Because Property F exceeds 10% significance, its audited Rule 3-14

financial statements must be included in the registration statement. Properties B, C, D and E

are individually insignificant because none exceeds 10%. In the aggregate, however, the

acquisitions total 17%. As a result, Company D must present the financial statements of

certain of these properties to comply with Rule 3-14.

Company D must provide financial statements of properties C and D because each

individually exceeds the 5% threshold. The inclusion of these financial statements would

provide Company D with greater than 50% coverage (5% + 6% = 11% / 17% = 64.7%) of

individually insignificant acquisitions, thus the SEC staff would not object to the omission of

financial statements of properties B and E from the registration statement.

Financial statement requirements

When to present Rule 3-14 financial statements

Financial statements are required in the following filings for each acquired real estate

property and probable acquisition that is significant, individually or in the aggregate:

• Proxy statements soliciting shareholders’ votes on the acquisition of real estate

• 1933 Act registration statements (e.g., Forms S-1, S-3, S-4, S-11, equivalent foreign forms)

• 1934 Act registration statements (e.g., Forms 10, 20-F)

EY AccountingLink | www.ey.com/us/accountinglink

8 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Financial statements must be provided for each of the following acquisitions or probable

acquisitions:

• Completed purchases of individually significant (greater than 10%) properties made

during each year presented, but not properties acquired from unrelated parties that are

reflected in the audited financial statements of the registrant for a full 12 months

• All completed purchases of individually significant properties made after the end of the

most recent fiscal year

• Any probable acquisition of an individually significant property

• Completed or probable acquisitions of individually insignificant properties that are significant

in the aggregate that occurred, or will occur, after the end of the most recent fiscal year

for which the registrant’s audited financial statements are on file (See “Aggregation

of individually insignificant properties” section below for further discussion of related

significance considerations.)

The SEC staff has indicated that an acquisition is probable if the registrant’s financial

statements alone would not provide investors with adequate financial information with which

to make an investment decision. All relevant facts and circumstances (e.g., imminence of

consummation, materiality of transaction) should be considered in making this judgment.

How we see it • Generally, we believe an acquisition is probable if the parties have agreed in writing to

the major provisions of the transaction. However, an agreement in principle also can lead

to a conclusion that a future acquisition is probable. The SEC staff generally considers

acquisitions probable if they are conditioned only upon obtaining financing or approval by

shareholders or regulators or if they are disclosed in the registration statement.

• Management should consult legal counsel when evaluating whether acquisitions are

probable.

A registration statement or post-effective amendment cannot be declared effective until

financial statements for all acquisitions meeting the requirements of Rule 3-14 have been

provided. While Rule 3-14 financial statements are not required before a company draws

down on an active shelf registration, it must determine whether a significant acquisition, or a

series of individually insignificant acquisitions, constitutes a “fundamental change” that would

require a post-effective amendment to the registration statement. It is the responsibility of

management to determine what constitutes a “fundamental change,” which has not been

defined by the SEC. Additionally, the company should assess whether the absence of Rule 3-14

financial statements is a material omission from the prospectus supplement.

How we see it • Registrants that are nearing the deadline to update an expiring shelf registration should

consider the timing of significant property acquisitions that must be reported on Form 8-K.

• We do not believe that an acquisition that meets the Rule 3-14 threshold automatically

constitutes a “fundamental change.” Nor do we believe that acquisitions of individually

insignificant real estate operations would likely constitute a fundamental change when

aggregated.

EY AccountingLink | www.ey.com/us/accountinglink

9 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Form 8-K requires the reporting of acquisitions of individually significant properties under

Item 2.01. This requirement does not extend to acquisitions of individually insignificant

properties unless the properties are related properties. While a significant acquisition must be

reported four business days after it is consummated, registrants have an additional 71 calendar

days to amend Form 8-K to include Rule 3-14 financial statements.

Updated financial statements would not be required in the Form 8-K if “substantially the same

information” was previously filed (e.g., when the registration statement previously included

the financial statements of a property as a probable acquisition). The previously filed financial

statements and pro forma financial information may be incorporated by reference into the

Form 8-K filed in connection with the acquisition.

Financial statements included in previous filings are generally considered to be “substantially

the same” by the SEC staff unless the previously filed financial statements (1) would not

satisfy the age requirements of Form 8-K because operating results for two or more interim

quarters are omitted or (2) are interim financial statements and the Form 8-K requires

updated audited annual financial statements.

For purposes of Rule 3-14, the SEC staff has determined that properties are related, and

therefore must be aggregated and treated as a single acquisition, if any of the following apply:

• The properties are under common control or management.

• The acquisition of one property is conditioned on the acquisition of each of the other

properties.

• Each acquisition is conditioned on a single common event.

The SEC staff has specifically stated that it does not consider the acquisition of real estate

properties to be in the ordinary course of business for purposes of evaluating the applicability

of Item 2.01 requirements of Form 8-K.

The 74-day exception in Rule 3-05 (b)(4) for registration statements does not apply to the

acquisition of real estate operating properties under Rule 3-14. This exception grants

registrants relief from providing Rule 3-05 financial information of an acquired business if (1) it

is not significant at the 50% level and (2) the effective date of the prospectus, or mailing of the

proxy statement, is no more than 74 days after the consummation of the business combination.

As a result, a registrant that has acquired a significant property must include those financial

statements in the registration statement even if they are not yet due to be reported on

Form 8-K. A registrant2 must either provide the required financial statements within the

applicable registration statement or, if permitted by the form, within a Form 8-K that is

incorporated by reference into the registration statement.

Contents of required financial statements

While the significance thresholds mandated by Rule 3-14 are lower than those in Rule 3-05,

the form and content of the required financial statements are generally less onerous.

Rule 3-14 requires only audited income statements for the most recent fiscal year and the

subsequent unaudited interim period if the property is acquired from an unrelated party. These

statements should also exclude items that are not comparable to the proposed future operations

of the property (e.g., mortgage interest, leasehold rental, depreciation, corporate expenses,

federal and state income taxes). Properties are unrelated if the following conditions are met:

• The property is not acquired from a related party.

EY AccountingLink | www.ey.com/us/accountinglink

10 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

• Material factors considered by the registrant in assessing the property are disclosed in

the filing, including sources of revenue and expense.

• The registrant discloses any other material factors that would cause the reported

financial information not to be indicative of future operating results.

Otherwise, the registrant must provide Rule 3-14 financial statements for the three most

recent fiscal years3 and subsequent unaudited interim period.

The filings must contain financial statements for the properties for a full fiscal year before the

acquisition. The SEC staff will not accept audited financial statements for a rolling 12-month

period prior to acquisition in lieu of audited statements of the latest fiscal year of the

property, nor will it accept audited financial statements for a period of nine to 12 months,

which is permitted under Rule 3-06 for Rule 3-05 financial statements. In addition, pre- and

post-acquisition periods cannot be combined to produce a full year of financial information.

The requirements for updating financial statements are consistent with those of Rule 3-05.

For properties with limited rental history, the following relief is available:

• Registrants may request from the SEC staff relief from the audit requirement for

financial statements of properties with a rental history of nine to 12 months.

• Relief from the audit requirement for financial statements of properties with a rental

history of three to nine months is automatically available to the registrant.

• Financial statements are not required for a property with a rental history of less than

three months.

• The SEC staff also does not object to the omission of financial statements of acquired real

estate operations if the property will be demolished and replaced with a new rental

property since the prior rental history would not be relevant. The registrant should

explain the basis for omission of the financial statements within the relevant filing.

• When the registrant believes the leasing history of the acquired property does not reflect

future utilization, the registrant may request relief in writing from the SEC staff.

See Appendix A for an example of an abbreviated income statement for an acquired real

estate operation as required by Rule 3-14.

REIT formation transactions A newly formed REIT may acquire operating properties immediately before or in connection

with the filing of an initial public offering (IPO) on Form S-11. The SEC staff allows these

registrants to compute significance using a denominator that is the sum of the total investment

in (1) properties acquired immediately before filing an IPO, (2) properties to be acquired

immediately after filing an IPO and (3) probable acquisitions at the date of the IPO filing.

The SEC staff

has provided

registrants with

more flexibility for

acquisitions with

rental histories of

less than a year.

EY AccountingLink | www.ey.com/us/accountinglink

11 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Illustration 6 — Measuring significance in a REIT formation transaction

Company E, a newly formed REIT, filed an IPO registration statement on 9 July 2013. The

table below summarizes properties Company E acquired, or will acquire, from unrelated

third parties throughout 2013. For purposes of the example, properties acquired

immediately before and in connection with the IPO have been combined and are reflected

in “Acquired properties.”

Acquired properties Cost Significance

To-be-acquired properties Cost Significance

Property A

Property B

Property C

$ 1m

$ 6m

$ 15m

4%

22%

54%

Property D

Property E

Property F

$ 2m

$ 2.5m

$ 1m

7%

9%

4%

Total Cost $ 27.5m

Total Significance 100%

Analysis: Because the significance of properties B and C individually exceed 10%, audited

financial statements for each of these properties must be included in the IPO registration

statement. Properties A, D, E and F are individually insignificant acquisitions because none

exceeds 10%. In the aggregate, however, the acquisitions total 24%. As a result, Company E

must present the financial statements of certain of these properties to comply with Rule 3-14.

Company E must provide financial statements of properties D and E because each

individually exceeds the 5% threshold. The inclusion of these financial statements would

provide Company E with greater than 50% coverage (7% + 9% = 16% / 24% = 66.7%) of

individually insignificant acquisitions, thus the SEC staff would not object to the omission of

financial statements of properties A and F from the IPO registration statement.

Illustration 7 — REIT formation transaction including related properties

Assume the same facts as described in Illustration 6 above, except that properties D, E and

F are under common management prior to acquisition. These properties therefore meet

the related property criteria of Rule 3-14 and must be evaluated in the aggregate.

Analysis: Properties D, E and F exceed the 10% threshold in the aggregate. Company E

must include audited financial statements of these properties within the IPO registration

statement. Company E may elect to provide financial statements for these three properties

separately or on a combined basis. Because Property A is individually insignificant and is

not related to properties D, E and F, financial statements of Property A are not required.

Measuring significance after an IPO

In computing significance of any acquisition that was not contemplated at the IPO, a REIT

may continue to use the asset base calculated in connection with its IPO until it files its first

Form 10-K. The asset base should be reduced for any acquisition that has not occurred and is

no longer probable. However, the asset base need not be reduced for probable acquisitions

that were contemplated at the date of the IPO and continue to remain probable.

EY AccountingLink | www.ey.com/us/accountinglink

12 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Blind pool offerings A “blind pool” registration statement allows registrants to sell securities to purchase real

estate operations that are not identified at the effective date of the registration statement.

Item 20.D of SEC Industry Guide 5 requires that such registration statements include the

following undertakings:

• The filing of a sticker supplement to the prospectus during the distribution period (i.e., the

period during which the registrant is conducting a continuous 1933 Act registered offering)

describing each property that has not been identified and disclosed previously whenever a

reasonable probability exists that the property will be acquired

• The consolidation of all sticker supplements into a post-effective amendment filed at least

once every three months during the distribution period. Such a post-effective amendment

must include or incorporate by reference Rule 3-14 financial statements that have been

filed, or should have been filed (considering the 71-calendar-day extension), on Form 8-K

for all significant property acquisitions. Pro forma information is also required for any

significant acquisitions for which Rule 3-14 financial statements are filed. However, unlike

a post-effective amendment filed as a result of a “fundamental change,” financial

statements of significant property acquisitions are not required in such a post-effective

amendment if they have not yet been filed, and were not required to be filed, in a Form 8-K.

Also, unlike other post-effective amendments, a post-effective amendment to consolidate

sticker supplements under the Industry Guide undertakings is not required to include Rule

3-14 financial statements of significant probable acquisitions or individually insignificant

acquisitions even if they are significant in the aggregate.

The prospectus updating regime in the Item 20.D undertakings is intended solely for real estate

companies and not for other types of companies that may be subject to other parts of Industry

Guide 5. Companies subject to the Item 20.D undertakings that acquire a property that

generates significant revenues from operations other than leasing rental property should

follow the Item 20.D updating regime discussed above, except that the significance thresholds

and required financial statements should be those specified in Rule 3-05. If the Rule 3-05

significance tests are not met, an acquisition with a rental history should then be evaluated

under Rule 3-14. Additionally, companies subject to the Item 20.D undertakings that acquire a

triple net leased property also should follow the Item 20.D updating regime discussed above,

except that the significance threshold applied and financial information provided should be

those described in the “Acquisitions of properties subject to a triple net lease” section below.

Measuring significance during the distribution period

In its latest update to the FRM, the SEC staff modified the method entities should use to

compute significance of an acquisition during the distribution period. This method applies to

both acquisitions of “regular” operating properties and properties subject to triple net leases.

Under the latest guidance, a registrant should measure significance during the distribution

period by comparing the total investment in the property, including any debt assumed by the

purchaser, with the sum of the following:

• The registrant’s total assets as of the date of the acquisition

• Proceeds, net of commissions, in good faith expected to be raised in the registered

offering over the next 12 months

An individual property is considered significant if the investment exceeds the 10% threshold.

Properties that are related or that were acquired from a single seller should be evaluated in

the aggregate.

EY AccountingLink | www.ey.com/us/accountinglink

13 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

How we see it • Allowing registrants to combine total assets at the date of an acquisition and future

expected offering proceeds should result in a significant reduction in the number of

Rule 3-14 financial statements required to be presented during the distribution period.

• Common considerations when determining estimates of future proceeds include the

pace of fundraising at the measurement date, the sponsor’s prior public capital raising

experience, and recent offerings by similar registrants. To prepare for possible inquiries

from the SEC staff, management should have evidence to support its assumptions, as

well as documentation of its specific process for determining estimated proceeds.

Distribution period reporting requirement

Financial information of significant properties acquired during the blind pool distribution

period should be provided in a current report on Form 8-K. Financial statements should

comply with Rule 3-14 requirements and include pro forma information.

Updated financial statements would not be required in the Form 8-K if “substantially the same

information” was previous filed. (See “When to present Rule 3-14 financial statements” section.)

Reporting acquisitions after the distribution period

While companies do not file sticker supplements after the distribution period is completed, the

requirement to include Rule 3-14 financial statements of significant acquired properties on

Form 8-K remains in effect. Until a registrant files its first annual report after the distribution

period ends, significance should be computed by comparing the total investment in the

property to the registrant’s total assets as of the acquisition date.

Acquisitions of properties subject to a triple net lease Real estate companies frequently acquire properties subject to a triple net lease arrangement

or enter into such arrangements in conjunction with a property acquisition (e.g., sale-leaseback

transactions). In a triple net lease, the lessee is typically required to pay all costs associated

with the ownership and operation of a property, including property taxes, insurance, utilities

and maintenance. When a property is leased to a single lessee under a triple net lease, the

rental payments by the single lessee likely represent the only cash inflows generated by the

property. In addition, cash outflows from the lessor are typically limited to debt-service

payments. As a result, the SEC staff determined that filing financial statements of properties

under a triple net lease would not provide sufficient information to an investor given the

registrant’s underlying risk exposure to the lessee.

Therefore, when a registrant acquires a property subject to a triple net lease with a single

tenant or enters into such a lease, and such properties represent a significant portion of the

registrant’s assets, the registrant is required to provide financial statements of the lessee(s).

This requirement also extends to co-lessees or guarantors of triple net lease arrangements.

The SEC staff believes that a concentration of assets subject to a triple net lease with a single

lessee (or guarantor) is significant if it exceeds 20% of the registrant’s total assets as of its

most recent balance sheet date.

Measuring concentration significance

The registrant should use the most recent balance sheet on file with the SEC, whether audited

or unaudited, to measure the significance of a concentration of triple net leased assets. If a

triple net lease property is acquired in connection with a blind pool offering, the registrant

Registrants also

should evaluate

whether a new

triple net lease at

an existing property

creates a significant

concentration of

risk from the lessee.

EY AccountingLink | www.ey.com/us/accountinglink

14 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

would add proceeds expected to be raised in the next 12 months to the total asset base as of

the most recent balance sheet date. (Refer to the “Blind pool offerings” section above for

further discussion of tests of significance for a blind pool offering.)

Reporting requirements

Registrants should consider significant asset concentrations when preparing registration

statements under the 1933 and 1934 Acts, as well as when filing annual reports and current

reports on Form 8-K resulting from a property acquisition. The registrant should provide full

audited annual financial statements of the lessee or guarantor and the most recent and

comparable interim financial statements for the periods required by Rules 3-01 and 3-02 or

Rules 8-02 and 8-03 of Regulation S-X, as applicable, of Regulation S-X.4 If the lessee or

guarantor is a public company subject to the periodic reporting requirements of the 1934 Act,

the registrant may include a reference to a publicly available website that contains the

SEC-filed financial information of the lessee or guarantor. A registrant should consult with the

Division of Corporation Finance’s Office of the Chief Accountant if it believes that less-detailed

financial information is appropriate based on the particular facts and circumstances of the

arrangement, or if financial statements of the lessee or guarantor are not available.

How we see it Companies should keep in mind that they can exceed the threshold for concentration of

significance of triple net leased assets by either acquiring a new real estate asset or

signing a new lease at an existing property. Management should monitor all relationships

with tenants (or guarantors) that have the potential to represent a significant

concentration upon the consummation of a new acquisition or signing a new lease.

Privately held tenants or guarantors may resist providing financial information for

inclusion in a registrant’s SEC filings. As a result, when negotiating triple net lease

arrangements, companies should consider obligating tenants or guarantors to help them

fulfill any current or future SEC financial reporting obligations that arise under the lease.

Illustration 8 — Acquisition of property subject to triple net lease

Company F acquired an office building from Company Q, a nonpublic company, on 9 July 2013 for cash consideration of $125 million. Following the transaction, Company F leased

the office building back to Company Q for a term of 10 years. In addition, Company F transferred substantially all of the property’s nonfinancial holding and operating costs to Company Q. Furthermore, Guarantor P, also a nonpublic company, agreed to guarantee

Company Q’s net rental payment to Company F. At 31 December 2012, Company F had total assets of $450 million.

Analysis: Because the significance of the acquired property exceeded 20% ($125 million/ $450 million = 28%), Company F must comply with Form 8-K reporting requirements resulting from the property acquisition and provide the audited financial statements of

Guarantor P for the three years ended 31 December 2012 and for the three-month periods ended 31 March 2013 and 2012. If Guarantor P were a public company, the Form 8-K would be required to include only a reference to a website that contains Guarantor P’s SEC filings.

In addition, audited financial statements of Guarantor P should be included in Company F’s 2013 Form 10-K and any registration statements. Specifically, Company F’s 2013 Form 10-K should include audited financial statements of Guarantor P as of 31 December

2013 and 2012 and for each of the three years in the period ended 31 December 2013. If Guarantor P were a public company, the Form 10-K would be required to include only a reference to a website that contains Guarantor P’s SEC filings.

If Guarantor P had not guaranteed Company Q’s rental payments, audited financial statements of Company Q would be required instead.

EY AccountingLink | www.ey.com/us/accountinglink

15 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Significance between 10% and 20%

In certain circumstances, a registrant may acquire a property subject to a triple net lease that

doesn’t exceed the 20% concentration threshold, but does exceed the 10% Rule 3-14 threshold.

The SEC staff clarified in its recent update of the FRM that in these circumstances, registrants

must provide audited financial statements of the acquired property that comply with the

requirements of Rule 3-14.

How we see it Rule 3-14 financial statements provided when the significance of a triple net leased

property acquisition exceeds 10% but not 20% could be limited to the presentation of only

a single line of rental revenues. Property operating expenses are generally paid by the

lessee in a triple net lease arrangement, and Rule 3-14 excludes from the presentation

historical activities that may not be indicative of future operations (e.g., mortgage

interest, depreciation, corporate expenses).

Properties securing mortgage loans

Acquisition, development and construction (ADC) arrangements

A registrant may originate a mortgage loan that is secured by a real estate operating property

that in substance represents an investment in real estate or a joint venture rather than a loan.

These loans may constitute an ADC arrangement as described in ASC 310, Receivables. ADC

arrangements may have some of the following characteristics:

• The lender participates in expected residual profits.

• The lender provides all of the cash flows to acquire and complete the project, including

agreeing to the addition of interest to the loan balance rather than receiving payment

from the borrower.

• The lender is able to look only to the property itself to recover the loan. The borrower is

not at risk through guarantees or pledging other collateral, nor are there unconditional

contracts with third parties that ensure recovery of the loan.

• The lender’s ability to recover principal and interest depends solely on the sale of the

property or the obtaining of permanent financing from another independent source.

Staff Accounting Bulletin (SAB) Topic 1.I.5 states that financial statements are required under

Rule 3-14 for such properties that secure loan arrangements that meet the definition of an

ADC arrangement under ASC 310.

1933 Act financial statement requirements

Financial statements of operating properties securing ADC loans are required in all 1933 Act

registration statements for any single property for which 10% of the offering proceeds (or

total assets at the latest year-end balance sheet, if greater) has been or will be loaned. The

information required by Items 14 and 15 of Form S-11 also should be included with respect

to these investment type arrangements. However, if no single loan exceeds 10%, but the

aggregate of such loans exceeds 20%, a description of the general character of the properties

and arrangements is required in a note to the financial statements. Such information may

include a description of the terms of the arrangements, participation by the registrant in

expected residual profits and property types and locations.

EY AccountingLink | www.ey.com/us/accountinglink

16 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

1934 Act financial statement requirements

Annual reports on Form 10-K must include the following financial information for operating

properties securing ADC loans:

• If more than 20% of the registrant’s total assets are invested in a single loan, financial

statements of the underlying operating property are required (except in annual reports to

shareholders where only summary data is required).

• If more than 10% but less than 20% of the registrant’s total assets is invested in a single

loan, summarized financial information of the operating property is required.

• When individual loans are not significant but in the aggregate exceed 20% of the

registrant’s total assets, a description of the properties and arrangements is required in a

footnote to the financial statements.

Entering into a significant ADC arrangement also triggers a requirement to file a timely Form

8-K with financial information (based on the significance levels described above) for the

underlying operating property.

Significance of ordinary loan arrangements

SAB Topic 1.I. also states that in certain circumstances, information may be required about

operating properties underlying mortgage loans even when the terms do not constitute ADC

arrangements. Generally, if investment risks exist due to substantial asset concentrations,

financial and other information should be included in the filing with respect to operating properties

underlying a mortgage loan that represents a significant amount of the registrant’s assets.

If more than 20% of the offering proceeds in a registration statement (or total assets at the

latest year-end balance sheet date, if greater) have been or will be invested in a single loan

(or in several loans on related properties to the same or affiliated borrowers), financial

statements of the property securing the loan are required in both 1933 Act and 1934 Act

filings. Properties would be considered related if they are subject to cross-default or

collateralization agreements. The financial statements of the operating property should be

presented for the periods specified in Rule 3-14.

Endnotes: _______________________

1 The Division of Corporation Finance Financial Reporting Manual is available at http://www.sec.gov/divisions/ corpfin/cffinancialreportingmanual.pdf

2 Automatic shelf registration statements and post-effective amendments of well-known seasoned issuers (WKSIs)

become effective immediately upon filing. WKSIs must comply with all Rule 3-14 reporting requirements as of the effective date of those registration statements.

3 Smaller reporting companies may provide only two fiscal years of audited financial information. 4 Rules 3-01 and 3-02 of Regulation S-X generally require the presentation of audited balance sheets at the end of

the two most recent fiscal years and statements of income and cash flows for the three most recent fiscal years.

Rule 8-02 of Regulation S-X allows smaller reporting companies to provide only two years of statements of income and cash flows. Rule 8-03 of Regulation S-X provides interim reporting requirements.

5 SAB Topic 71 has been codified into SAB Topic 1.I.

EY | Assurance | Tax | Transactions | Advisory

© 2013 Ernst & Young LLP.

All Rights Reserved.

SCORE No. CC0373

ey.com/us/accountinglink

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

EY AccountingLink | www.ey.com/us/accountinglink

17 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Appendix A: Example Rule 3-14 financial statements The following is an example of the form and content of Rule 3-14 financial statements. These statements were prepared

assuming that the property was acquired in the fourth quarter of 2012 from an unrelated party. The required pro forma

information reflecting the impact of the acquisition to the registrant has been omitted from this presentation.

Property I

Statements of Revenues and Certain Expenses

Year Ended December 31, 2011, and Nine Months Ended September 30, 2012 (unaudited)

(In thousands)

Nine Months Ended September 30, 2012

(Unaudited) Year Ended

December 31, 2011

Revenues

Rental revenue $ 10,300 $ 14,300

Tenant recoveries 1,100 1,600

Parking and other 1,500 2,100

Total revenues 12,900 18,000

Certain expenses

Operating expenses 3,700 5,000

Taxes and insurance 1,200 1,600

Total certain expenses 4,900 6,600

Revenues in excess of expenses $ 8,000 $ 11,400

See accompanying notes

1. Basis of Presentation

The accompanying statements of revenues and certain expenses include the operations of Property I (“The Property”), an

office building.

The accompanying statements of revenues and certain expenses relate to the Property and have been prepared for the purpose

of complying with Rule 3-14 of Regulation S-X promulgated under the Securities Act of 1933, as amended. Accordingly, the

statements are not representative of the actual operations for the periods presented as revenues and certain operating

expenses, which may not be directly attributable to the revenues and expenses expected to be incurred in the future operations

of the Property, have been excluded. Such items include depreciation, amortization, management fees, interest expense,

interest income and amortization of above- and below-market leases.

2. Summary of Significant Accounting Policies

Revenue Recognition

The Property recognizes rental revenue from tenants on a straight-line basis over the lease term when collectability is

reasonably assured and the tenant has taken possession or controls the physical use of the leased asset.

Tenant recoveries related to reimbursement of real estate taxes, insurance, repairs and maintenance, and other operating

expenses are recognized as revenue in the period the applicable expenses are incurred. The reimbursements are recognized

and presented gross, as the Property is generally the primary obligor with respect to purchasing goods and services from

third-party suppliers, has discretion in selecting the supplier and bears the associated credit risk.

EY AccountingLink | www.ey.com/us/accountinglink

18 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Parking and other revenue is revenue that is derived from the tenants’ use of telecommunications, parking and the fitness

center. Parking and other revenue is recognized when the related services are utilized by the tenants.

Use of Estimates

Management has made a number of estimates and assumptions relating to the reporting and disclosure of revenues and certain

expenses during the reporting periods to present the statements of revenues and certain expenses in conformity with US GAAP.

Actual results could differ from those estimates.

3. Minimum Future Lease Rentals

There are various lease agreements in place with tenants to lease space in the Property. As of September 30, 2012, the minimum future cash rents receivable under noncancelable operating leases in each of the next five years and thereafter are as follows (unaudited):

2012 (three months ending December 31, 2012) $ 3,600

2013 14,800

2014 14,600

2015 13,100

2016 12,200

2017 8,800

Thereafter 17,600

$ 84,700

Leases generally require reimbursement of the tenant’s proportional share of common area, real estate taxes and other

operating expenses, which are excluded from the amounts above.

4. Tenant Concentrations

For the year ended December 31, 2011, and the nine months ended September 30, 2012, three tenants represented 75%, 80%

and 85% (unaudited), respectively, of the Property’s rental revenues.

5. Related Party Transactions

An affiliate of the owner of the property provides engineering services to the property. For the year ended December 31, 2011,

and the nine months ended September 30, 2012, $60 and $50 (unaudited) of engineering related services, respectively, are

included in the Property’s property operating expenses

6. Commitments and Contingencies

The Property is subject to various legal proceedings and claims that arise in the ordinary course of business. These matters are

generally covered by insurance. Management believes that the ultimate settlement of these actions will not have a material

adverse effect on the Property’s results of operations.

7. Subsequent Events

The Property evaluated subsequent events through January 20, 2013, the date the financial statements were available to

be issued.

EY AccountingLink | www.ey.com/us/accountinglink

19 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

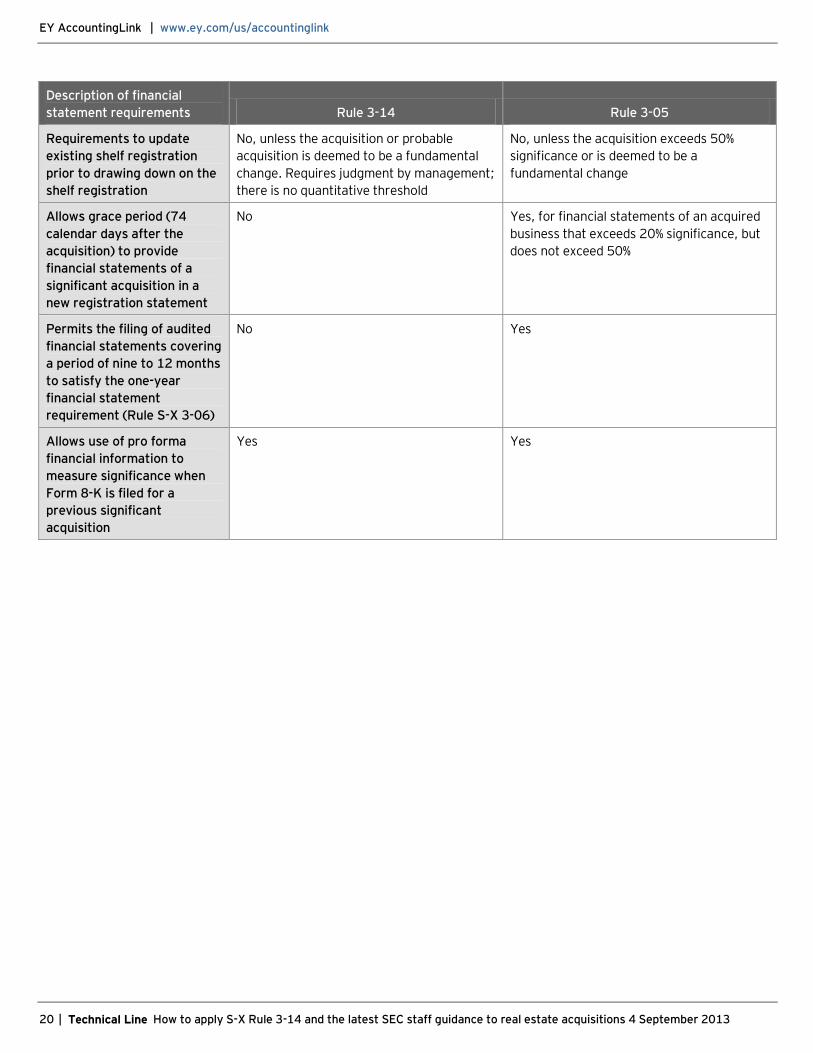

Appendix B: Comparison of Rule 3-14 and Rule 3-05 requirements Rule 3-14 requires companies to include in registration statements and proxy statements abbreviated audited financial

statements for each significant consummated or probable acquisition of operating real estate properties or groups of related

properties. Rule 3-05 requires companies to include audited financial statements of significant acquisitions or probable

acquisitions of businesses in registration statements, including IPOs. Financial statements for significant acquisitions under

both rules are also required to be reported on Form 8-K. This table does not reflect the requirements for blind pool offerings or

net lease arrangements.

Description of financial

statement requirements Rule 3-14 Rule 3-05

Financial statements Abbreviated income statement Full financial statements

Tests performed to

determine significance

Investment test comparing the registrant’s

investment in the acquisition to its total

assets

Investment test, asset test comparing the

acquired business’s assets to the registrant’s

and income test comparing the acquired

business’s pretax income from continuing

operations to the registrant’s

Significance threshold

(minimum)

10% 20% for each test

Number of years of financial

statements required

Depends on the seller:

• Property acquired from unrelated

party — most recent year and latest

interim period

• Property acquired from related party —

three years (two years for smaller

reporting companies) and latest interim

period

Depends on significance:

• Exceeds 20% significance but not 40% —

one year

• Exceeds 40% but not 50% — two years

• Exceeds 50% — three years (but two

years for smaller reporting companies

and emerging growth companies)

Note: The most recent interim financial

statements must be presented with

comparable prior-period statements.

Criteria for individually

insignificant acquisitions and

probable acquisitions

Financial statements are required when the

aggregate investment in all insignificant real

estate properties exceeds 10% of registrant’s

total assets as of the last audited balance

sheet date preceding the acquisition.

Financial statements are required for each

property that has a significance of 5% or more.

Registrant also must assess whether financial

statements for the majority (i.e., more than

50%) of the acquisitions based on purchase

price have been provided. If not, the

registrant must provide financial statements

for other acquired properties below the 5%

level to meet the 50% threshold.

Financial statements are required when the

aggregate significance in the asset test,

investment test or income test of all

insignificant acquisitions exceeds 50% for

those entities. Financial statements are

required for any combination of acquisitions

that represent a mathematical majority of

the applicable significance calculation.

EY AccountingLink | www.ey.com/us/accountinglink

20 | Technical Line How to apply S-X Rule 3-14 and the latest SEC staff guidance to real estate acquisitions 4 September 2013

Description of financial

statement requirements Rule 3-14 Rule 3-05

Requirements to update

existing shelf registration

prior to drawing down on the

shelf registration

No, unless the acquisition or probable

acquisition is deemed to be a fundamental

change. Requires judgment by management;

there is no quantitative threshold

No, unless the acquisition exceeds 50%

significance or is deemed to be a

fundamental change

Allows grace period (74

calendar days after the

acquisition) to provide

financial statements of a

significant acquisition in a

new registration statement

No Yes, for financial statements of an acquired

business that exceeds 20% significance, but

does not exceed 50%

Permits the filing of audited

financial statements covering

a period of nine to 12 months

to satisfy the one-year

financial statement

requirement (Rule S-X 3-06)

No Yes

Allows use of pro forma

financial information to

measure significance when

Form 8-K is filed for a

previous significant

acquisition

Yes Yes